For ACA Enrollees, How Much Premiums Rise Next Year is Mostly up to Congress

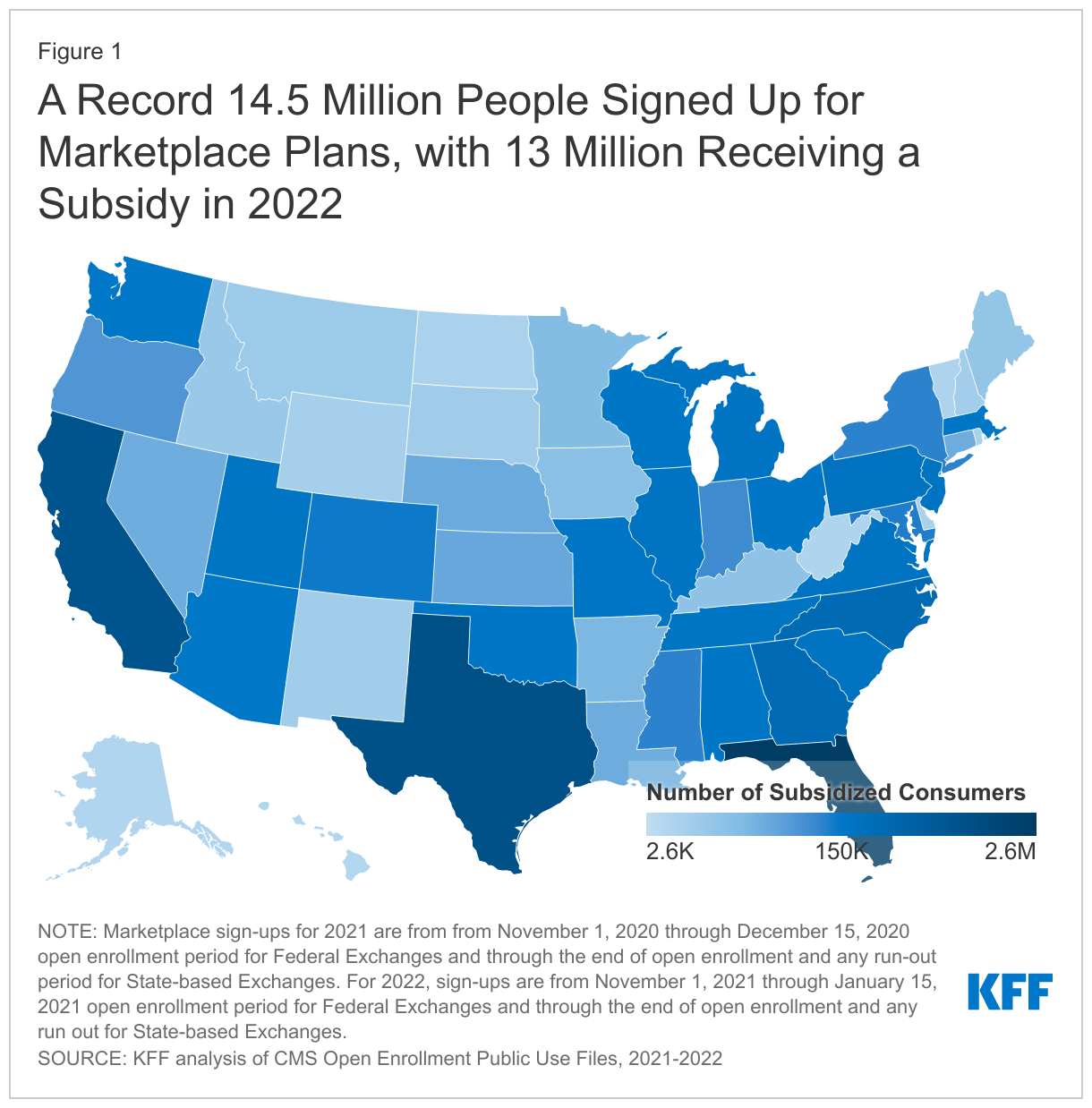

Health insurers are now submitting to state regulators proposed 2023 premiums for plans offered on the Affordable Care Act (ACA) Marketplaces. Changes in these unsubsidized premiums attract a lot of attention, but what really matters most to the people buying coverage is how much they pay out of their own pockets. And the amount ACA Marketplace enrollees pay is largely determined by the size of their premium tax credit. Generally speaking, when unsubsidized premiums rise, so do the premium tax credits, meaning out-of-pocket premium payments hold mostly steady for people getting financial assistance.For just over a year, ACA Marketplace enrollees have benefited from enhanced tax credits under the American Rescue Plan Act (ARPA), which Congress passed as temporary pandemic relief. The enhanced assistance lowers out-of-pocket premiums substantially, and millions of enrollees saw their premium payments cut in half by these extra subsidies. ACA Marketplace signups reached a record high of 14.5 million people in 2022, including nearly 13 million people who received tax credits to lower their premiums.

Soon, the vast majority of these nearly 13 million people will see their premium payments rise if the ARPA subsidies expire, as they are set to at the end of this year.

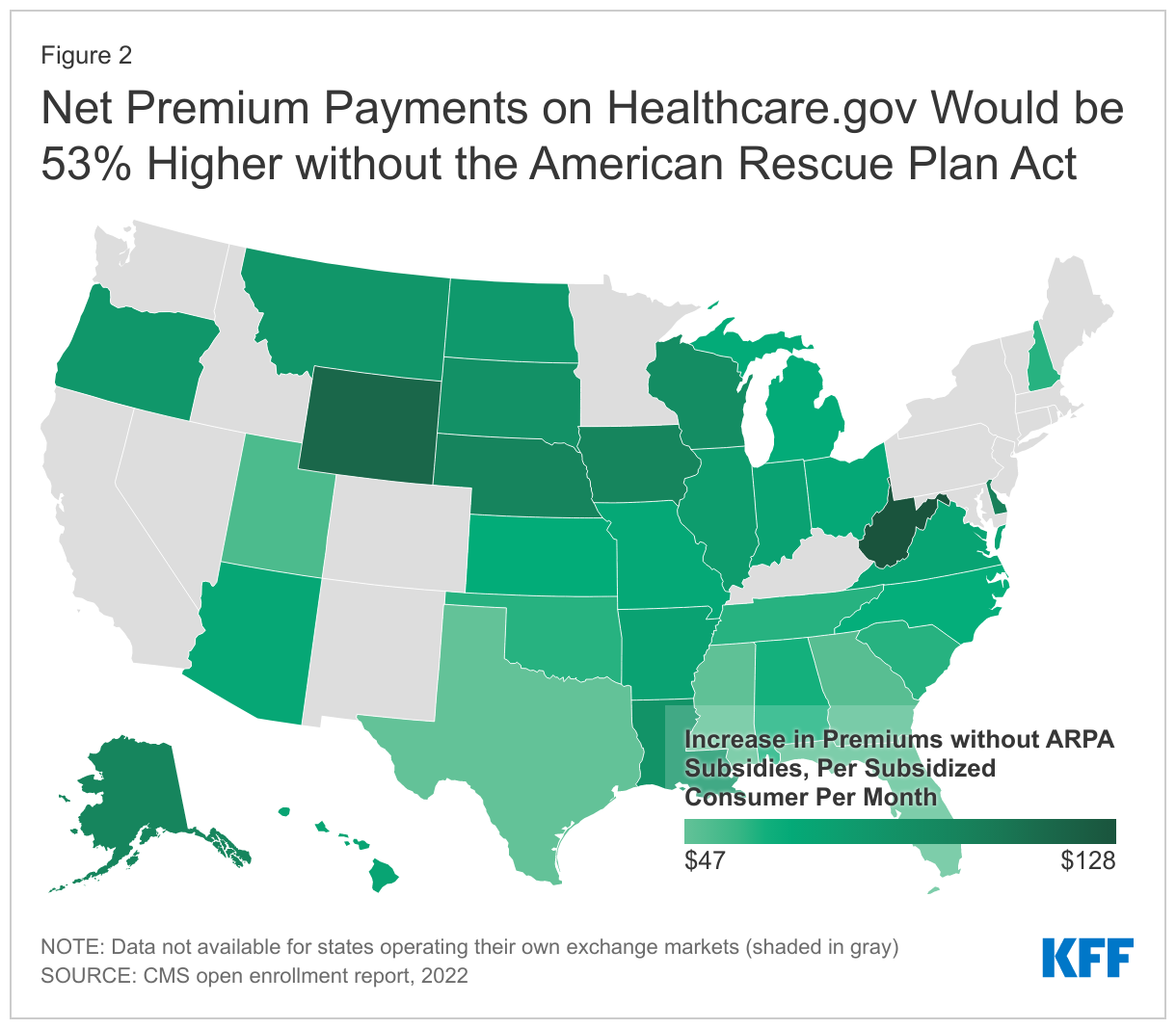

The ARPA subsidies were enacted temporarily for 2021 and 2022 as pandemic relief, but congressional Democrats are considering extending or making the expanded subsidies permanent as a way of building on the ACA, as President Biden had proposed during his 2020 campaign. If Congress does not extend the subsidies, out-of-pocket premium payments will return to their pre-ARPA levels, which would be seen as a significant premium increase to millions of subsidized enrollees. In the 33 states using HealthCare.gov, premium payments in 2022 would have been 53% higher on average if not for the ARPA extra subsidies. The same is true in the states operating their own exchanges. In New York, for example, premiums for tax credit-eligible consumers would be 58% higher if not for the ARPA. Such an increase in out-of-pocket premium payments would be the largest ever seen by the millions receiving a subsidy. Exactly how much of a premium increase enrollees would see depends on their income, age, the premiums where they live, and how the premiums charged by insurers change for next year.

For states, the timing of Congressional action on ARPA subsidies matters both for rate review and state enrollment systems. State-based exchanges – as well as the federal government, which operates HealthCare.gov – will need to reprogram their enrollment websites and train consumer support staff on policy changes ahead of open enrollment in November. States will start making these changes as soon as this month. Additionally, as insurers submit premiums for review, state insurance commissioners and other regulators must assess the reasonableness of 2023 rates, and some of that determination will depend on the future of ARPA subsidies. The non-partisan National Association of Insurance Commissioners (NAIC) wrote to Congress asking for clarity on the future of ARPA subsidies by July.

For insurers, the timing matters because 2023 premiums get locked in later this summer. Last summer, when insurers were setting their 2022 premiums, some said the ARPA had a slight downward effect on their premiums, based on the risk profile of enrollees. Insurers are now in the process of setting 2023 premiums and some might factor in an upward effect on premiums if they expect ARPA subsidies to expire. Premiums for 2023 are locked in by this August, so if Congress does not act before its August recess, whatever assumptions insurers make about the future of ARPA subsidies will be locked in to their 2023 premiums. Additionally, although this is not necessarily at the same scale of the uncertainty seen in 2017 surrounding the ACA repeal and replace debates (when many insurers explicitly said that uncertainty was driving their premiums up), it is possible that some insurers will price 2023 plans a bit higher than they otherwise would, simply because of uncertainty around the future of the ARPA’s enhanced subsidies. The NAIC letter to Congress warned that “uncertainty may lead to higher than necessary premiums.”

For enrollees, the timing matters both for knowing how much they will pay and for maintaining continuous coverage. Nearly all of the 13 million subsidized enrollees will see their out-of-pocket premium payments rise if the ARPA subsidies expire. But if the subsidies are renewed by Congress, but not until the end of the year right before subsidies are set to expire, there could still be a disruption if states and the federal government do not have enough lead time to update their enrollment websites to reflect the enhanced subsidies. In this scenario, the millions of enrollees who currently have access to $0 premium Marketplace plans might have to pay a premium in January – putting them at risk of losing coverage due to non-payment. Similarly, middle-income enrollees might temporarily lose access to advanced payments of the tax credit in the month of January, making it unaffordable for them to maintain coverage.

Congress’s action or inaction on ARPA subsidies will have a much greater influence over how much subsidized ACA Marketplace enrollees pay for their premiums than will market-driven factors that affect the unsubsidized premium. Even if unsubsidized premiums hold steady going into 2023, the expiration of ARPA subsidies would result in the steepest increase in out-of-pocket premium payments that most enrollees in this market have seen. This would essentially be a return to pre-pandemic normal, but the millions of new enrollees and others who have received temporary premium relief may not see it that way.