How Marketplace Costs and Premiums will Change if Rescue Plan Subsidies Expire

The American Rescue Plan Act (ARPA) passed earlier this year temporarily expanded subsidies available in the Affordable Care Act (ACA) health insurance Marketplaces, building on the ACA’s existing subsidies. Through the end of 2022, low-income families who were already eligible for financial assistance under the ACA are eligible for even more financial help to buy their own health insurance and pay for their copays and deductibles for coverage bought on healthcare.gov or their state’s exchange. Additionally, middle income families who were often priced out of ACA coverage before the ARPA, are now eligible for financial help with their monthly insurance premiums for the first time.

These new and additional subsidies were created under the ARPA as part of a larger pandemic relief strategy, but Democrats have long favored similar strategies to reduce the cost of ACA marketplace plans to enrollees. And the state of California, along with a handful of other states, had already implemented its own state-funded subsidies to address premium affordability. One of the key criticisms of the ACA has been the high and rising premiums, particularly for working families with incomes over four times the poverty level (a little more than $50,000 for a single person or just over $103,000 for a family of four), who previously were not eligible for financial assistance. While the relief package did not directly address high cost-sharing for these enrollees, larger premium subsidies can help them afford plans with lower deductibles.

Now, there is a debate in Congress over whether to make these additional premium subsidies permanent, or at least extend them for a longer time period. On the one hand, if Congress extends the ARPA subsidies or makes them permanent, federal costs would increase. On the other hand, if Congress does not extend these subsidies, premium payments will rise sharply for nearly all marketplace enrollees.

If the ARPA subsidies are extended, federal costs will rise

The Congressional Budget Office (CBO) and Joint Committee on Taxation (JCT) originally estimated that the additional temporary subsidies provided under the ARPA would increase federal deficits by $34.2 billion. Most of that cost is concentrated in the first couple of years since the additional subsidies expire at the end of 2022, though CBO expected some lingering costs as some subsidized people would remain enrolled for a time, even after the ARPA subsidy enhancements end.

The Department of Health and Human Services (HHS) reports that ARPA subsidies for existing consumers cost $537 million per month. It is likely these costs could rise next year as more people take up coverage during open enrollment.

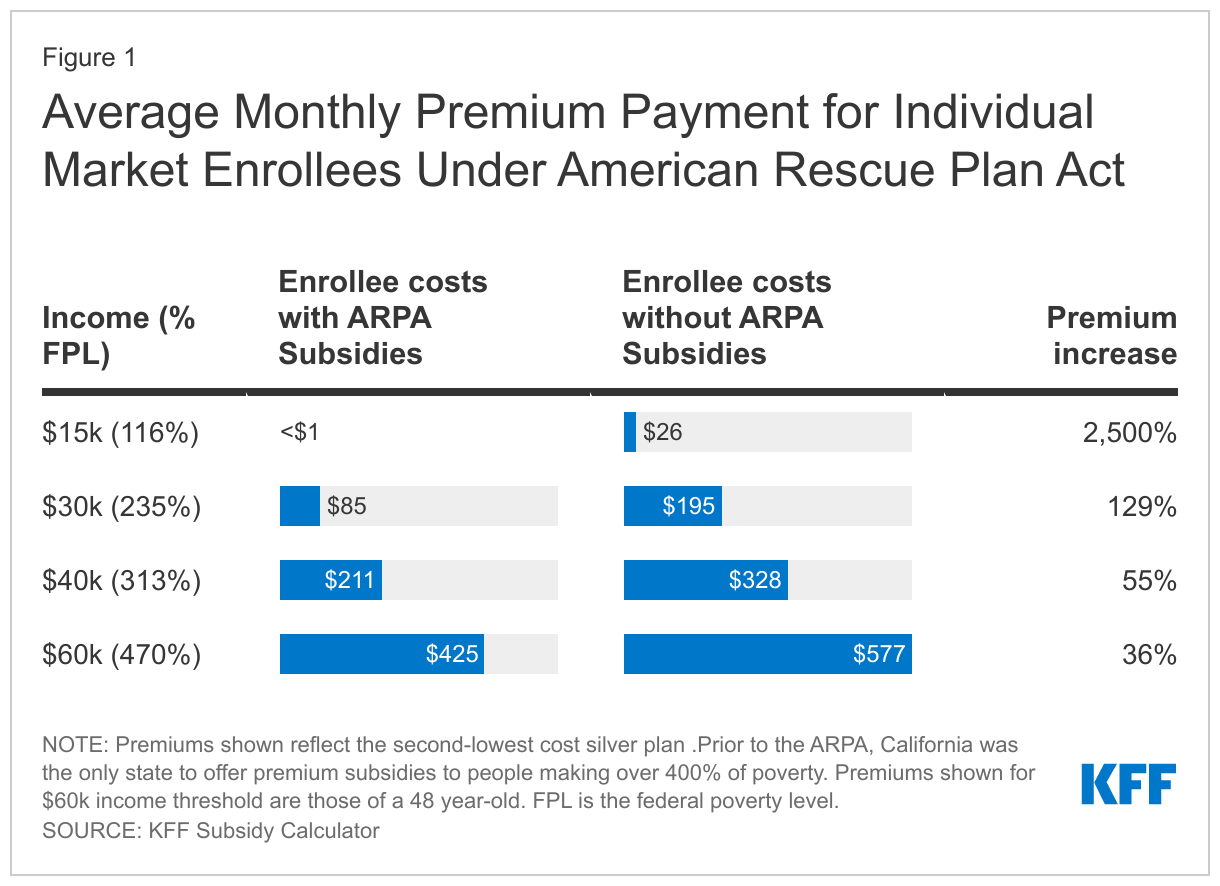

If subsidies expire, premium payments could double for millions of Marketplace enrollees

According to HHS, the 8 million marketplace enrollees who signed up before the ARPA subsidies were enacted are now paying $68 per month, after accounting for an average monthly premium savings due to the ARPA of $67. Without the ARPA subsidies, premiums would double on average for these enrollees and they would pay an average of $800 per year more if enrolled for the full year.

Premiums or deductibles would increase most steeply for the lowest-income Marketplace enrollees

People with incomes between 1 and 1.5 times the poverty level currently represent 42% of enrollees, and, with the ARPA subsidies, now pay nothing or next to nothing for their monthly premium. Before the ARPA, these individuals had to contribute more than 2% of their income toward the benchmark silver plan premium. These lowest-income enrollees would therefore see the steepest percent increases if ARPA subsidies expire.

Because of these premium increases, some low-income people may move from very generous silver plans with deductibles under $200, to bronze plans with deductibles of about $7,000 – more than 30 times higher. HHS reports that the median deductible in the federal marketplace decreased by more than 90%, from $750 in 2020 to $50 in 2021, because some low-income enrollees moved from bronze to silver plans.

Millions of middle-income people would lose subsidy eligibility

Middle income individuals and families also buy coverage in the marketplace when they don’t have access to job-based group plan coverage. These include people who work for small businesses that don’t offer group health benefits, gig and other self-employed workers, and people who retire early, before the age of Medicare eligibility. We estimate that 3.7 million people (most with incomes between 4 and 6 times poverty) gained subsidy eligibility with the ARPA.

Under the ARPA, the vast majority of people buying their own health insurance coverage can be sheltered from premium increases by taking advantage of the subsidies offered in the ACA marketplace. If these subsidies expire, though, middle and upper-middle income people who lose subsidy eligibility will not only have to make up the difference in the subsidy; they will also be on the hook for any increase in the “sticker price” of the premium between now and January 1, 2023.

Although these individuals earn a living wage, it is often not enough to afford full-priced insurance. A 48-year-old making $60,000 per year would see their monthly premium payments increase by 36% if they lost subsidy eligibility, and that doesn’t account for any additional increase in the sticker price of premiums. Families and older enrollees would see even larger premium increases.

Without a subsidy, a 60-year-old’s health insurance premium currently averages more than $11,000 per year. If that 60-year-old has an income just above $51,000 – over four times the poverty level – their ARPA subsidy covers more than half of their monthly costs. Without the ARPA, their premium would increase 165%.

The timing of potential premium increases could have political implications

In the event ARPA subsidies are allowed to expire, the timing of the resulting impact on insurance affordability could become an election issue. The ARPA premium subsidy enhancements are set to expire at the end of 2022. Open enrollment begins on November 1, just one week before the midterm election is held on November 8, 2022.