Falling off the Subsidy Cliff: How ACA Premiums Would Change for People Losing Rescue Plan Subsidies

The Affordable Care Act (ACA) offers subsidies to offset the cost of health insurance, capping how much people signing up on the ACA Marketplaces pay at a certain percent of their income. These subsidies work on a sliding scale, with people whose incomes are just above poverty receiving the most generous subsidies while those with incomes of three to four times poverty paying more. For years, people with incomes just over four times the federal poverty level were not eligible for subsidies under the ACA, meaning even a small increase in income could mean they would have to pay full price – what came to be known as the “subsidy cliff.”That was the case until the American Rescue Plan Act (ARPA) expanded subsidy eligibility, now capping what people with higher incomes pay for a silver plan premium at 8.5% of their income. By doing so, the ARPA temporarily did away with the ACA’s subsidy cliff, in addition to enhancing subsidies for lower-income people who were already eligible for some help with premiums. Congress is considering extending these enhanced subsidies or making them permanent at an estimated cost of about $22 billion per year. If the ARPA subsidies expire, as they are set to at the end of this year, people with incomes over four times the poverty level would no longer qualify for subsidies and would have to pay full price for insurance coverage.

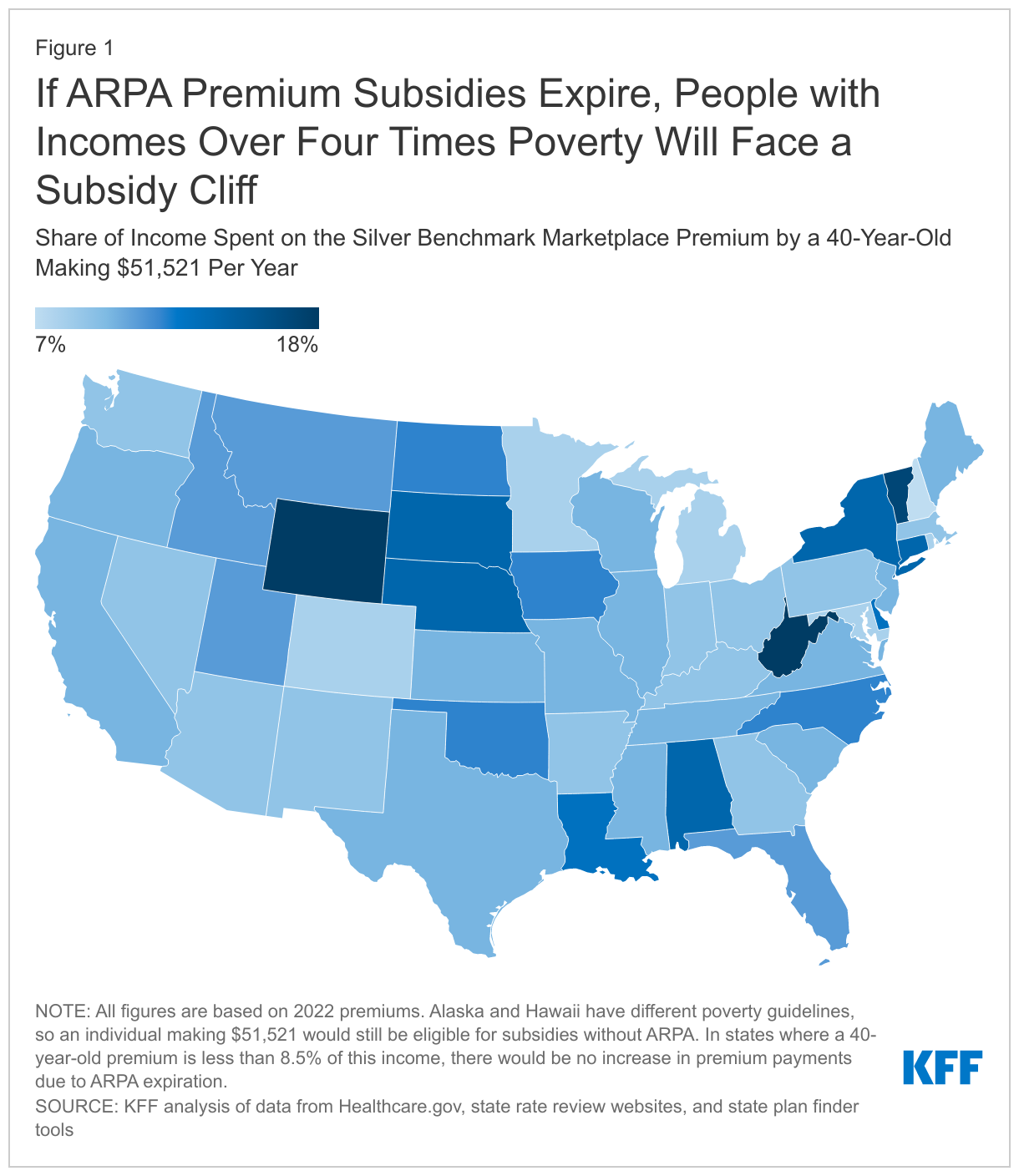

On average across the U.S., a 40-year-old with an income just over four times the poverty level ($51,520 per year for individuals buying coverage in 2022), will see their premium payments increase from 8.5% of their income to about 10% of their income if ARPA subsidies expire. The typical 40-year-old would go from having subsidized monthly payments of $365 to an unsubsidized $438, or an increase in their premium payment of about 20% simply due to the loss of subsidies. That’s before accounting for any increase in the unsubsidized premium from 2022 to 2023.

Because unsubsidized premiums vary so much across the country, Marketplace enrollees living in some states would pay more than those living in other states. For example, a 40-year-old with an income of just over four times the poverty level living in West Virginia or Wyoming would have to pay an average of 18% of his or her income for a silver plan without the ARPA’s subsidies. That’s an increase of over 100% in their premium payments. Meanwhile, the same person living in one of six low-premium states (Colorado, Maryland, Michigan, Minnesota, New Hampshire, and Rhode Island) already pays less than 8.5% of their income for an unsubsidized silver premium.

Older residents of high-premium states would see even steeper increases in premium payments from the loss of ARPA subsidies. Instead of paying 8.5% of their income for a silver plan, as they do under the ARPA, a 64-year-old Marketplace enrollee making just over four times the poverty level in West Virginia or Wyoming would have to pay more than 40% of their income for a silver plan if they lost access to the ARPA subsidies. That would amount to an increase of over 380% in their premium payment. Again, this is all based on 2022 premiums, so it’s not accounting for any additional increase in unsubsidized premiums heading into 2023. Insurers are just now starting to file their 2023 premiums with state regulators, but it’s likely unsubsidized premiums in many states will rise.

If the ARPA subsidies expire, premium payments will increase across the board for all 13 million subsidized Marketplace enrollees. But the approximately one million people with incomes above four times the poverty level will face a double whammy: Not only will many of them lose subsidies, but they will also have to start paying for any increase in the unsubsidized premium beyond that. The reality is that for many people, such an increase in premium payments would be unaffordable, leading them to drop their health coverage.