KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Starting on his first day of his second term in office, President Trump and his administration have taken several executive actions that directly impact U.S. global health efforts. This timeline, which is a companion resource to components of KFF’s Overview of President Trump’s Executive Actions on Global Health, provides a detailed overview of actions, including counter-actions, related to the administration’s efforts to freeze all U.S. foreign aid, dissolve the U.S. Agency for International Development (USAID), which implements most U.S. global health programs, and reorganize the Department of State. It will be updated as needed to reflect additional developments.

Editorial Note: The Policy Actions tracker will no longer be updated as the data source has ceased tracking government responses to COVID-19. For more information, please visit the Oxford Covid-19 Government Response Tracker.

Section:

0/0

Cases and Deaths

This tracker provides the cumulative number of confirmed COVID-19 cases and deaths, as well as the rate of daily COVID-19 cases and deaths by country, income, region, and globally. It will be updated weekly, as new data are released. As of March 7, 2023, all data on COVID-19 cases and deaths are drawn from the World Health Organization’s (WHO) Coronavirus (COVID-19) Dashboard. Prior to March 7, 2023, this tracker relied on data provided by the Johns Hopkins University (JHU) Coronavirus Resource Center’s COVID-19 Map, which ended on March 10, 2023. Please see the Methods tab for more detailed information on data sources and notes. To prevent slow load times, the tracker only contains data from the last 200 days. However, the full data set can be downloaded from our GitHub page. While the tracker provides the most recent data available, there is a two-week lag in the data reporting.

Note: The data in this tool were corrected on March 18, 2024, to clarify that they represent new cases and deaths over a full week rather than the average per day over a seven-day period.

Policy Actions

This tracker contains information on policy measures currently in place to address the COVID-19 pandemic. Policy categories currently being tracked include social distancing & closure measures, economic measures, and health systems measures. Policies are tracked at the country-, income-, and region-level. Please see the Methods tab for more detailed information on data sources and notes.

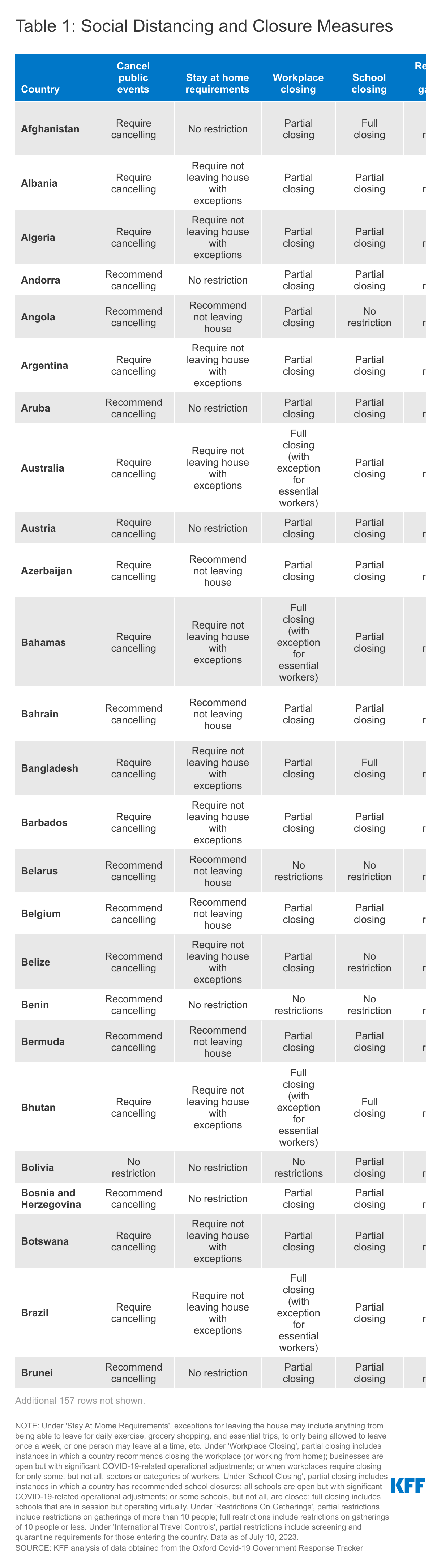

Social Distancing and Closure Measures

As countries continue to implement policies to prevent the transmission of SARS-CoV-2, the virus that causes COVID-19, these tables and charts show which social distancing and closure measures are currently in place by country.

Economic Measures

The COVID-19 pandemic has placed an unprecedented strain on country economies. These tables and charts show which economic-related measures, namely income support and debt relief, are currently in place by country.

Health Systems Measures

The COVID-19 pandemic continues to strain and disrupt global health systems. These tables and charts show which health systems measures are currently in place by country.

Policy actions data include the measure that was in place for each indicator at the country-level as of the end of 2022. Policy actions data will no longer be updated as the data source has ceased tracking government responses to COVID-19. For more information, please visit the Oxford Covid-19 Government Response Tracker.

Social Distancing and Closure Measures

Under 'Stay At Home Requirements', exceptions for leaving the house may include anything from being able to leave for daily exercise, grocery shopping, and essential trips, to only being allowed to leave once a week, or one person may leave at a time, etc. Under 'Workplace Closing', partial closing includes instances in which a country recommends closing the workplace (or working from home); businesses are open but with significant COVID-19-related operational adjustments; or when workplaces require closing for only some, but not all, sectors or categories of workers. Under 'School Closing', partial closing includes instances in which a country has recommended school closures; all schools are open but with significant COVID-19-related operational adjustments; or some schools, but not all, are closed; full closing includes schools that are in session but operating virtually. Under 'Restrictions On Gatherings', partial restrictions include restrictions on gatherings of more than 10 people; full restrictions include restrictions on gatherings of 10 people or less. Under 'International Travel Controls', partial restrictions include screening and quarantine requirements for those entering the country. Values for ‘Cancel Public Events’ were not recodified.

Economic Measures

Under 'Income Support', narrow support includes instances in which a country's government is replacing less than 50% of lost salary (or if a flat sum, it is less than 50% median salary); broad support includes instances in which a country's government is replacing 50% or more of lost salary (or if a flat sum, it is greater than 50% median salary). Under 'Debt/Contract Relief', narrow support includes instances in which a country's government is providing narrow relief, such as relief specific to one kind of contract.

Health Systems Measures

Under 'Vaccine Eligibility', partial availability includes availability for some or all of the following groups: key workers, non-elderly clinically vulnerable groups, and elderly groups, or for select broad groups/ages. Under 'Facial Coverings', recommend/partial requirement includes instances in which a country's government recommends wearing facial coverings, requires facial coverings in some situations, and requires facial coverings when social distancing is not possible.

Note: The data presented below are updated monthly as new Medicaid/CHIP enrollment data become available.

This tracker presents the most recent data on monthly Medicaid and Children’s Health Insurance Program (CHIP) enrollment reported by the Centers for Medicare & Medicaid Services (CMS) as part of the Performance Indicator Project. It includes data for Medicaid and CHIP and reports enrollment data for children and adults. The data are generally the most recent data available and are useful for reporting trends in Medicaid enrollment. However, the data only capture full-benefit enrollees, excluding those who receive limited benefits, such as those who receive family planning services only, and consequently, do not provide a full count of the total population enrolled in Medicaid. Additionally, these data cannot be used to monitor changes in enrollment by eligibility pathway, including for adults in the Medicaid expansion group. Enrollment data for the full Medicaid population is available here, and for more information on how implementation of Medicaid work requirements is affecting Medicaid expansion enrollment, please see Tracking Implementation of the 2025 Reconciliation Law Medicaid Work Requirements.

Medicaid/CHIP Enrollment Trends

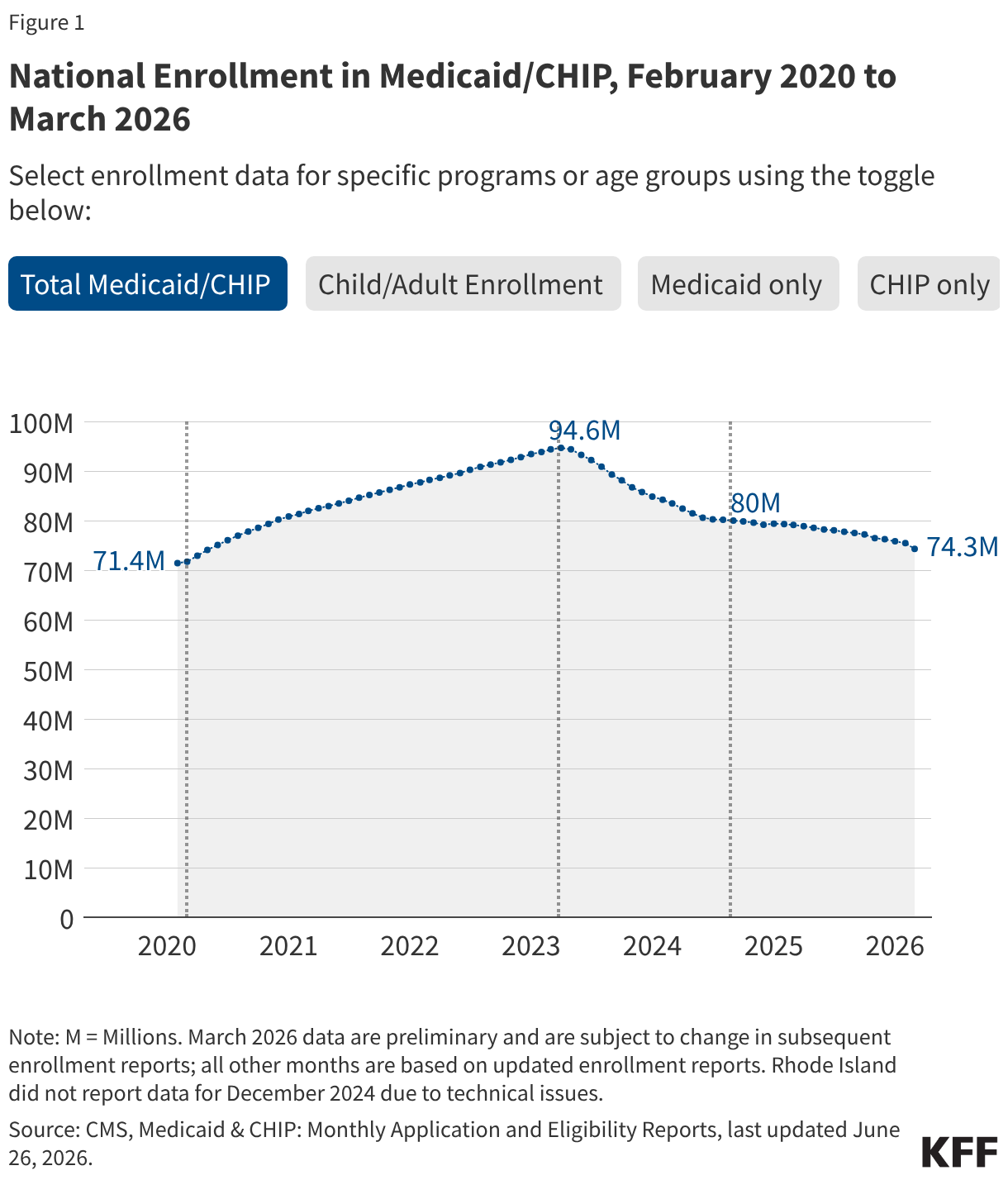

Following implementation of the Affordable Care Act’s (ACA) Medicaid expansion in January 2014, Medicaid enrollment increased as adults with income up to 138% of the federal poverty level (FPL) gained coverage. As more states adopted the expansion, Medicaid enrollment peaked at just over 75 million in March 2017 before declining steadily until the start of the COVID-19 pandemic in March 2020. By February 2020, enrollment had dropped to 71 million.

At the start of the pandemic, Congress enacted legislation that included a provision that Medicaid programs keep people continuously enrolled in exchange for enhanced federal funding. As a result, national Medicaid/CHIP enrollment increased to a record high of 94 million enrollees in March 2023 when the continuous enrollment provision ended. The unwinding of this provision started on April 1, 2023, and millions were disenrolled from Medicaid over the subsequent 16 months. By September 2024, national Medicaid/CHIP enrollment had dropped to 80 million. Medicaid enrollment stabilized briefly at the end of 2024 but began declining again in March 2025.

Passage of the 2025 reconciliation bill in July 2025 included significant changes to Medicaid that are expected to reduce Medicaid enrollment over the next 10 years relative to what would have been expected under current law. For the first time, the law conditions Medicaid eligibility for Medicaid expansion enrollees on meeting work and reporting requirements. These work requirements, which will go into effect in January 2027, or sooner at state option, represent the largest source of enrollment declines in the law. The bill also restricts eligibility for certain immigrant populations starting in October 2026, which is also expected to affect Medicaid enrollment.

The figures below show Medicaid and CHIP enrollment from February 2020 through the most current month of available data. Figures include enrollment for adults and children in Medicaid/CHIP and for Medicaid only and CHIP only. Key enrollment data and trends asof April 2026 include:

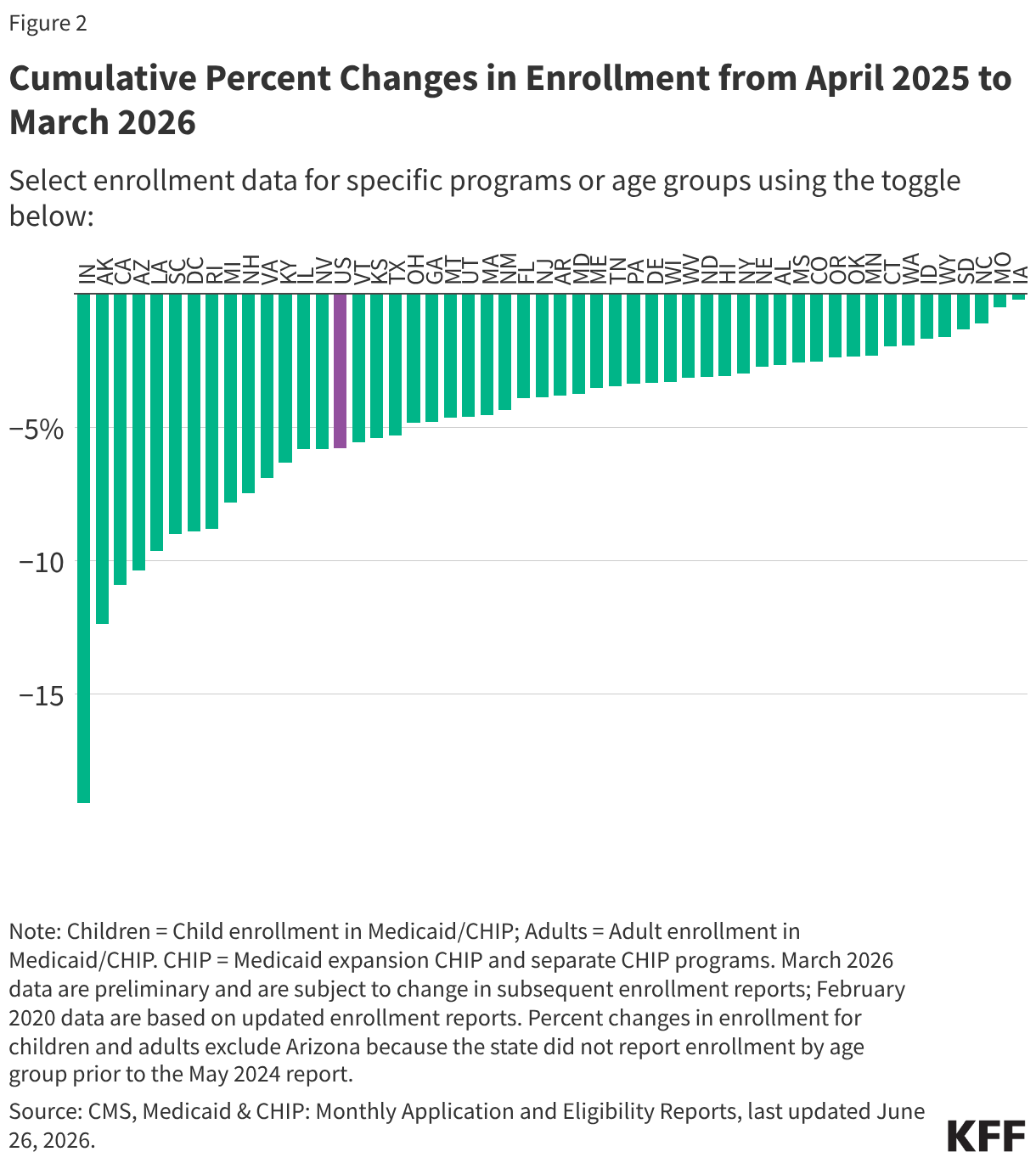

There were 73.9 million people enrolled in Medicaid/CHIP nationally (Figure 1). Medicaid enrollment declined by 5 million or 6% from April 2025 through April 2026 (Table 1).

Total Medicaid/CHIP enrollment has decreased in all states since April 2025. Enrollment changes since April 2025 vary from a less than 1% decrease in Iowa to a 20% decrease in Indiana (Figure 2).

Child enrollment in Medicaid/CHIP decreased in all states and DC but Hawaii from April 2025 through April 2026. Adult enrollment has decreased in all but five states (IA, MO, NC, OK, SD) (Figure 2).

There were 66.7 million people enrolled in Medicaid and 7.1 million people enrolled in CHIP (Figure 1). Since April 2025, Medicaid enrollment has decreased in all states and DC but Iowa while CHIP enrollment has increased in eighteen states (AL, CA, CT, DE, FL, HI, IL, MO, NJ, NM, NC, ND, RI, SC, TN, VT, WA, WI).

Total Medicaid/CHIP enrollment was 3% higher in April 2026 compared to enrollment in February 2020, prior to the pandemic. However, in the 49 states and DC with complete enrollment data by age, the number of children enrolled in Medicaid/CHIP declined by 631,000 or 2% from February 2020 to April 2026 (Figure 2 and Table 1).

Unwinding Data - Archived

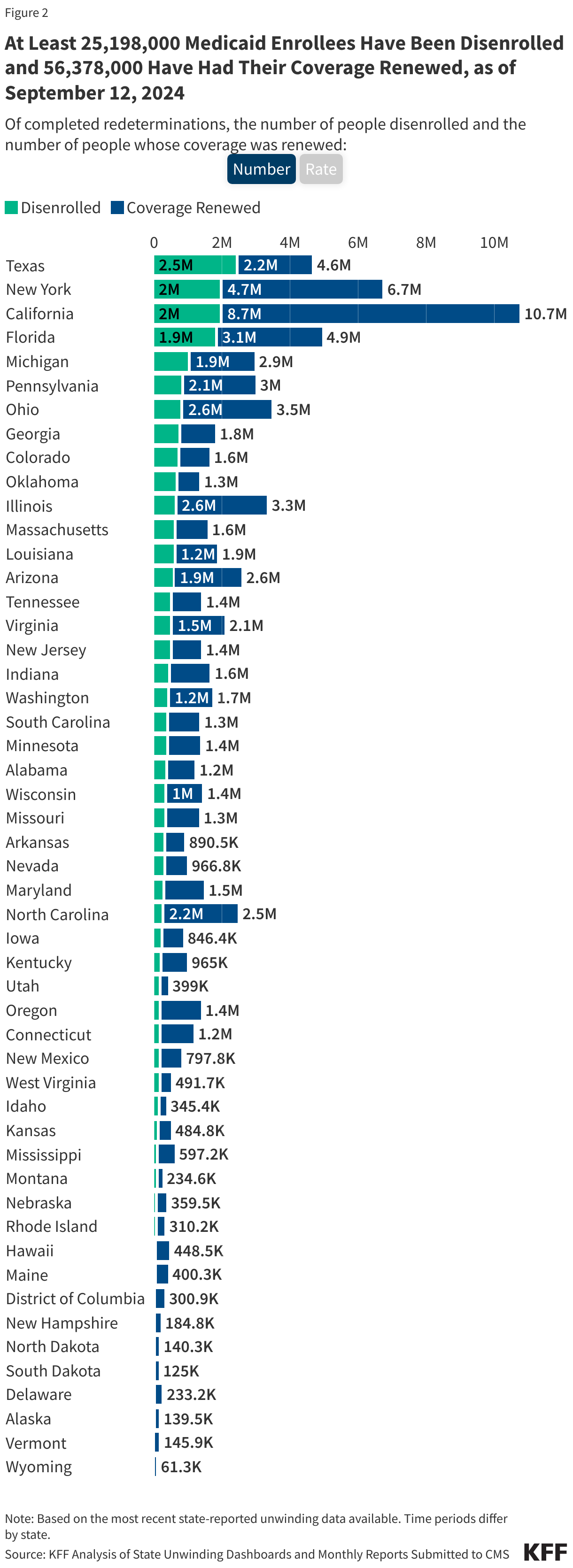

Note: The data on unwinding renewal outcomes presented below were last updated on September 12, 2024; since most states have now completed the Medicaid unwinding, the information will not be updated again.

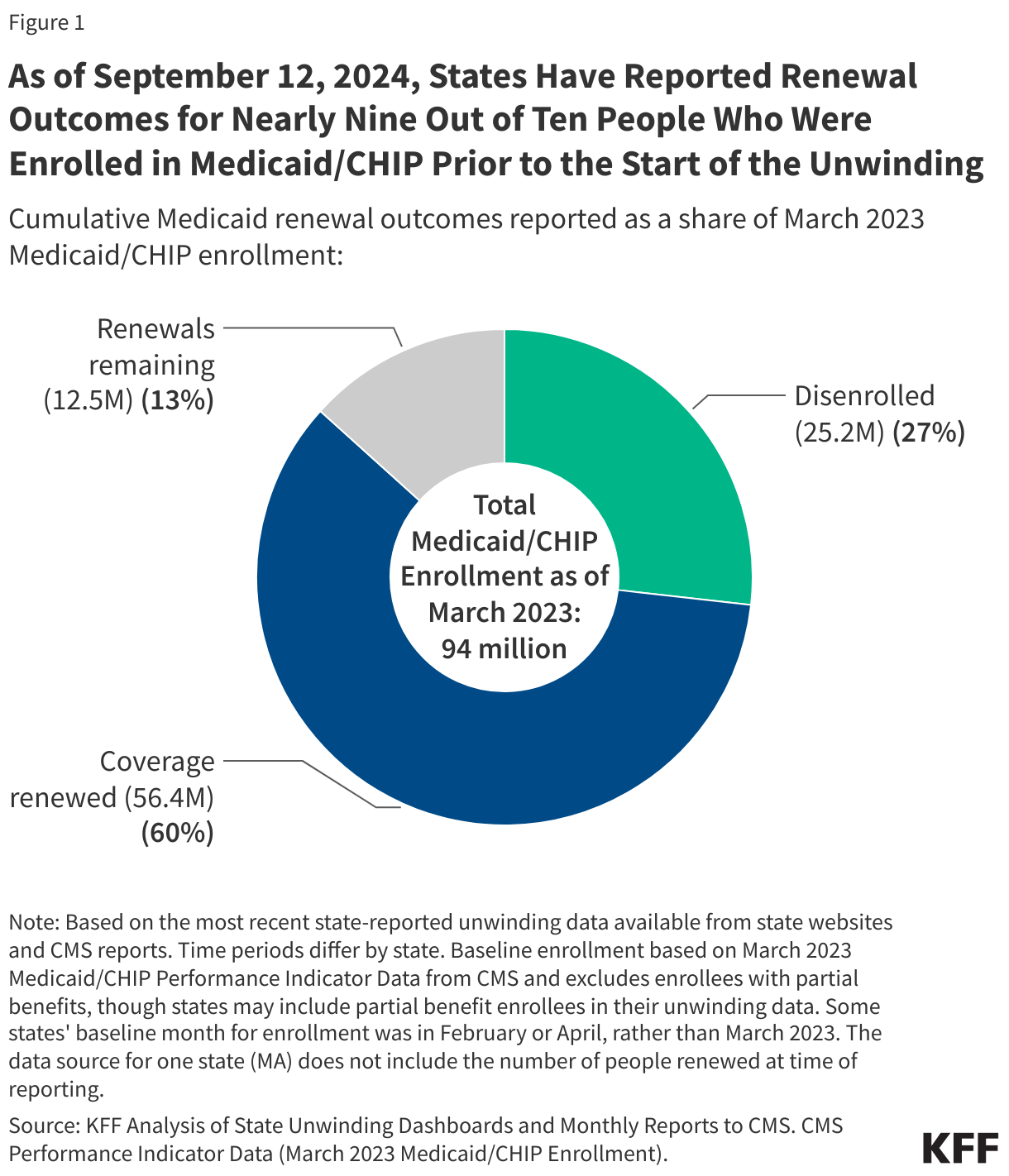

As of September 12, 2024 and with nearly complete unwinding data for most states:

Over 25 million people were disenrolled (31% of completed renewals) and over 56 million people had their coverage renewed (69% of completed renewals).

Disenrollment rates varied across states from 57% in Montana to 12% in North Carolina, driven by a variety of factors including differences in renewal policies and procedures as well as eligibility expansions in some states.

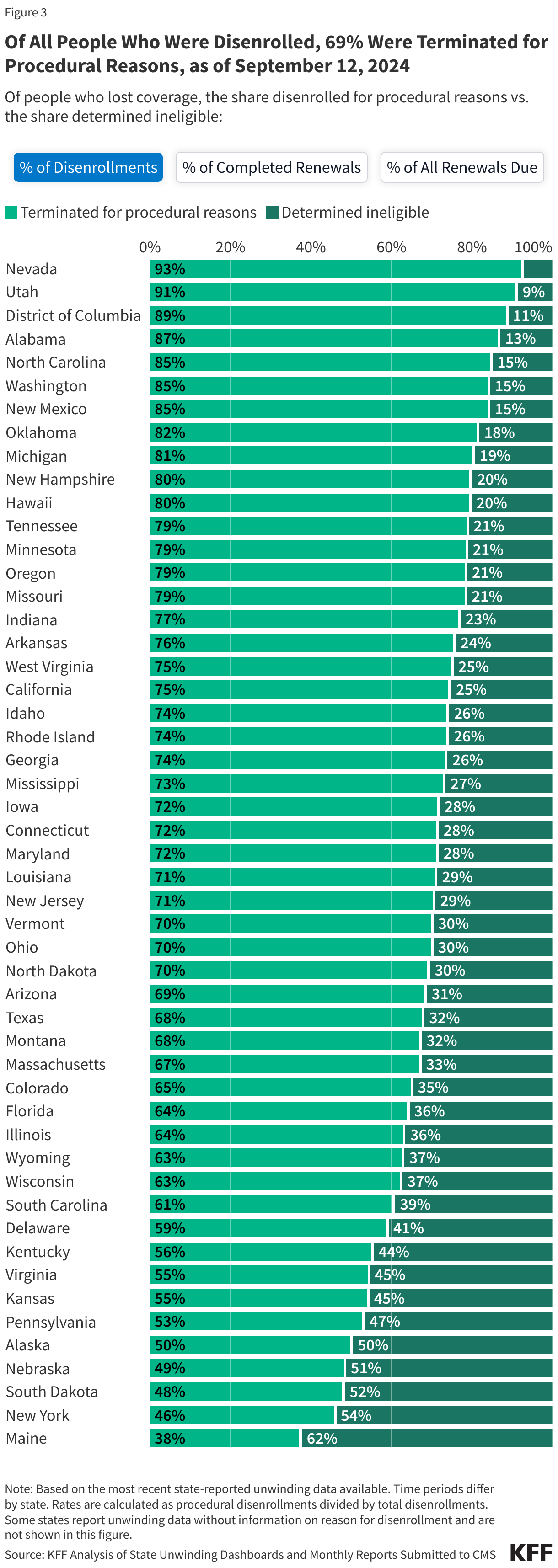

Among those who were disenrolled, nearly seven in ten (69%) were disenrolled for paperwork or procedural reasons while three in ten (31%) were determined ineligible.

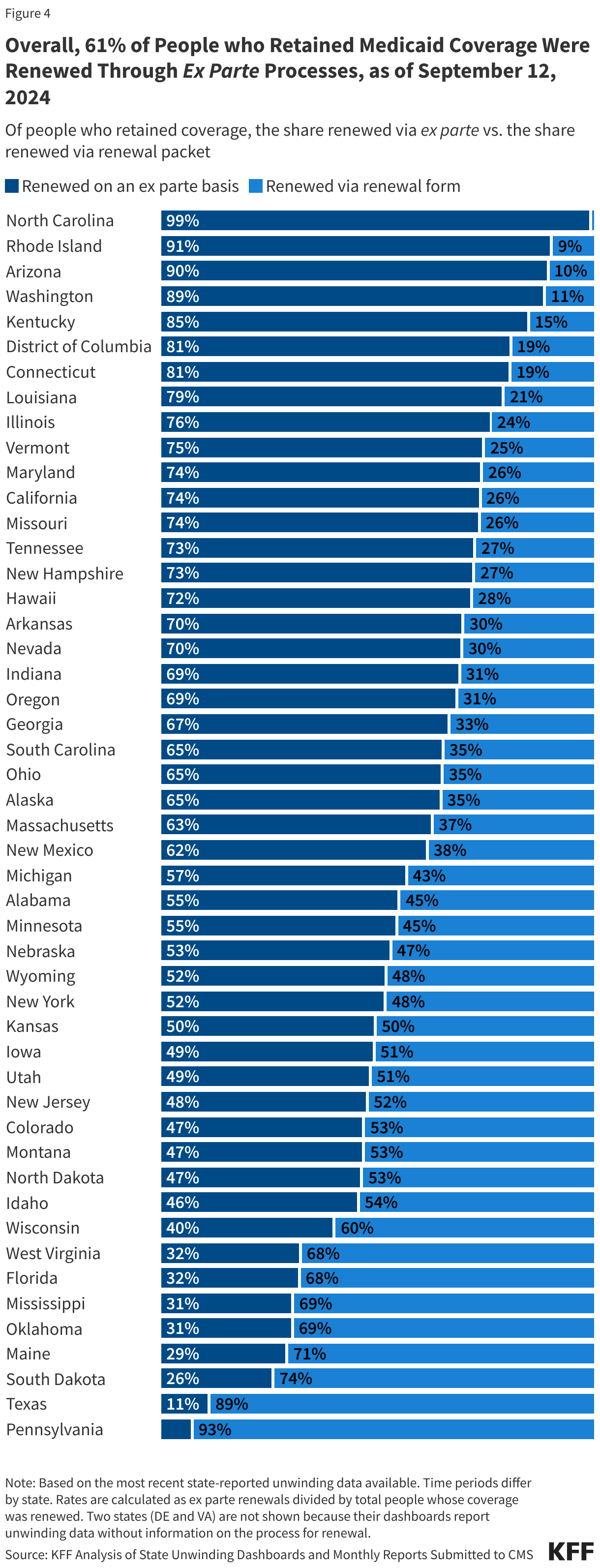

Among those whose coverage was renewed during the unwinding, 61% were renewed on an ex parte, or automated, basis, meaning the individual did not have to take any action to maintain coverage.

State Data on Renewal Outcomes

The data on unwinding-related renewal outcomes presented in this section rely primarily on monthly reports that states were required to submit to the Centers for Medicare & Medicaid Services (CMS) during the unwinding period. The data also reflect updates to the monthly reports that states submit three months after the original report submission to account for the resolution of pending cases and any other changes in renewal metrics. For 13 states, data were pulled from dashboards or reports published on state websites that provide more complete information, and for a few additional states, updated monthly reports were pulled from state websites because they were more timely than what is reported on the CMS website.

As of September 12, 2024, at least 25,198,000 Medicaid enrollees had been disenrolled during the unwinding of the continuous enrollment provision. Overall, 31% of people with a completed renewal were disenrolled in reporting states while 69%, or 56.4 million enrollees, had their coverage renewed.

There is wide variation in disenrollment rates across reporting states, ranging from 57% in Montana to 12% in North Carolina.A variety of factors contribute to these differences, including differences in renewal policies and system capacity. Some states adopted policies that promote continued coverage among those who remain eligible and/or have automated eligibility systems that can more easily and accurately process renewals while other states have adopted fewer of these policies and have more manually-driven systems. In addition, North Carolina and South Dakota adopted Medicaid expansion and other states increased eligibility levels for certain populations (e.g., children, parents, etc.) during the unwinding, which may have lowered disenrollment rates in these states.

Across all states with available data, 69% of all people disenrolled had their coverage terminated for procedural reasons. However, these rates vary based on how they are calculated (see note below). Procedural disenrollments are cases where people are disenrolled because they did not complete the renewal process and can occur when the state has outdated contact information or because the enrollee does not understand or otherwise does not complete renewal packets within a specific timeframe. High procedural disenrollment rates are concerning because many people who are disenrolled for these paperwork reasons may still be eligible for Medicaid coverage.

(Note: The first tab in the figure below calculates procedural disenrollment rates using total disenrollments as the denominator. The second tab shows these rates using total completed renewals, which include people whose coverage was terminated as well as those whose coverage was renewed, as the denominator. And finally, the third tab calculates the rates as a share of all renewals due, which include completed renewals and pending cases.)

Medicaid Renewals

Of the people whose coverage has been renewed as of September 12, 2024, 61% were renewed on an ex parte basis while 39% were renewed through a renewal form, though rates vary across states. Under federal rules, states are required to first try to complete administrative (or “ex parte”) renewals by verifying ongoing eligibility through available data sources, such as state wage databases, before sending a renewal form or requesting documentation from an enrollee. Ex parte renewal rates varied across states from 90% or more in Arizona, North Carolina, and Rhode Island to less than 20% in Pennsylvania and Texas.

Federal Data on Renewal Outcomes

The data presented here are cumulative unwinding metrics published by CMS. These counts and percentages may differ from the above data, which present renewal metrics reported on state websites when state-reported data are more complete.

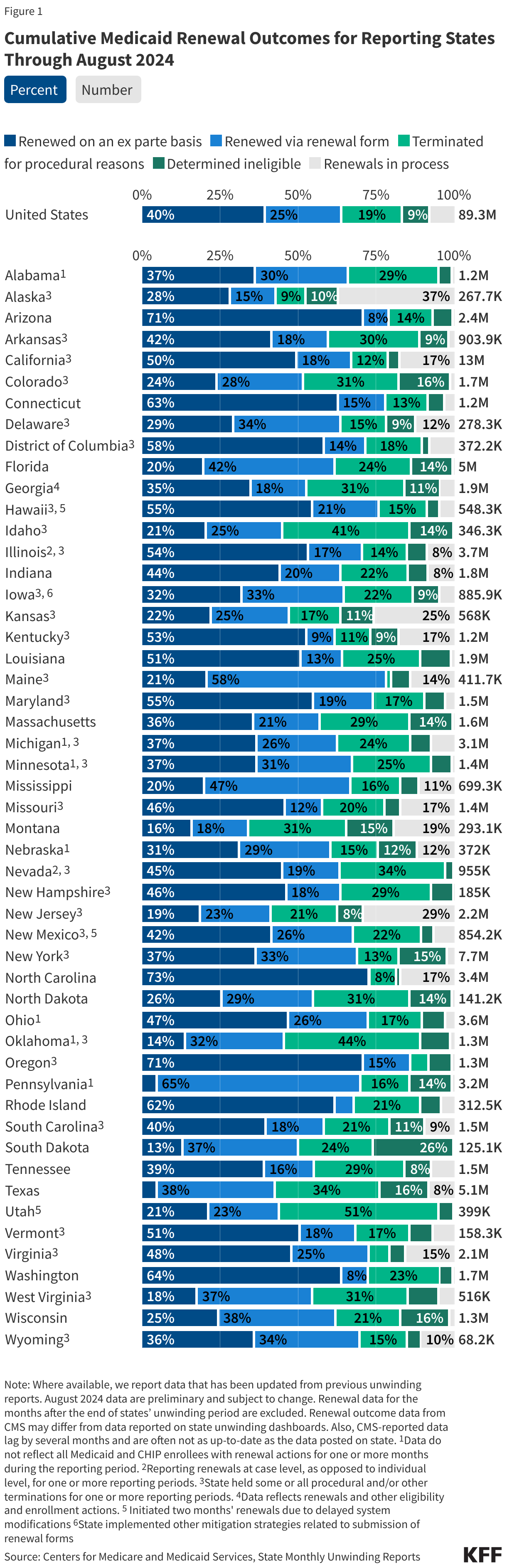

Figure 1 below shows cumulative renewal data reported by CMS during states’ unwinding periods. Renewal data for the months after the end of states’ unwinding period are excluded. The data reflect updated unwinding data reported by states three months after the original monthly reports as they become available.

Note: The state data presented below were last updated on September 12, 2024; since most states have now completed the Medicaid unwinding, the information will not be updated again.

The data presented here provide state-level data on enrollment trends and renewal outcomes during the unwinding period. Figure 1 shows total Medicaid enrollment by month starting in January 2023 and, once disenrollments resumed in a state, the cumulative percent change in Medicaid enrollment relative to the month before Medicaid disenrollments started (this baseline month will differ across states). Figure 2 shows renewal metrics for each month of a state’s unwinding period (or cumulative data for the unwinding period for some states).

This brief, originally published on September 9, 2025, was updated with the most recently available data on July 31, 2026.

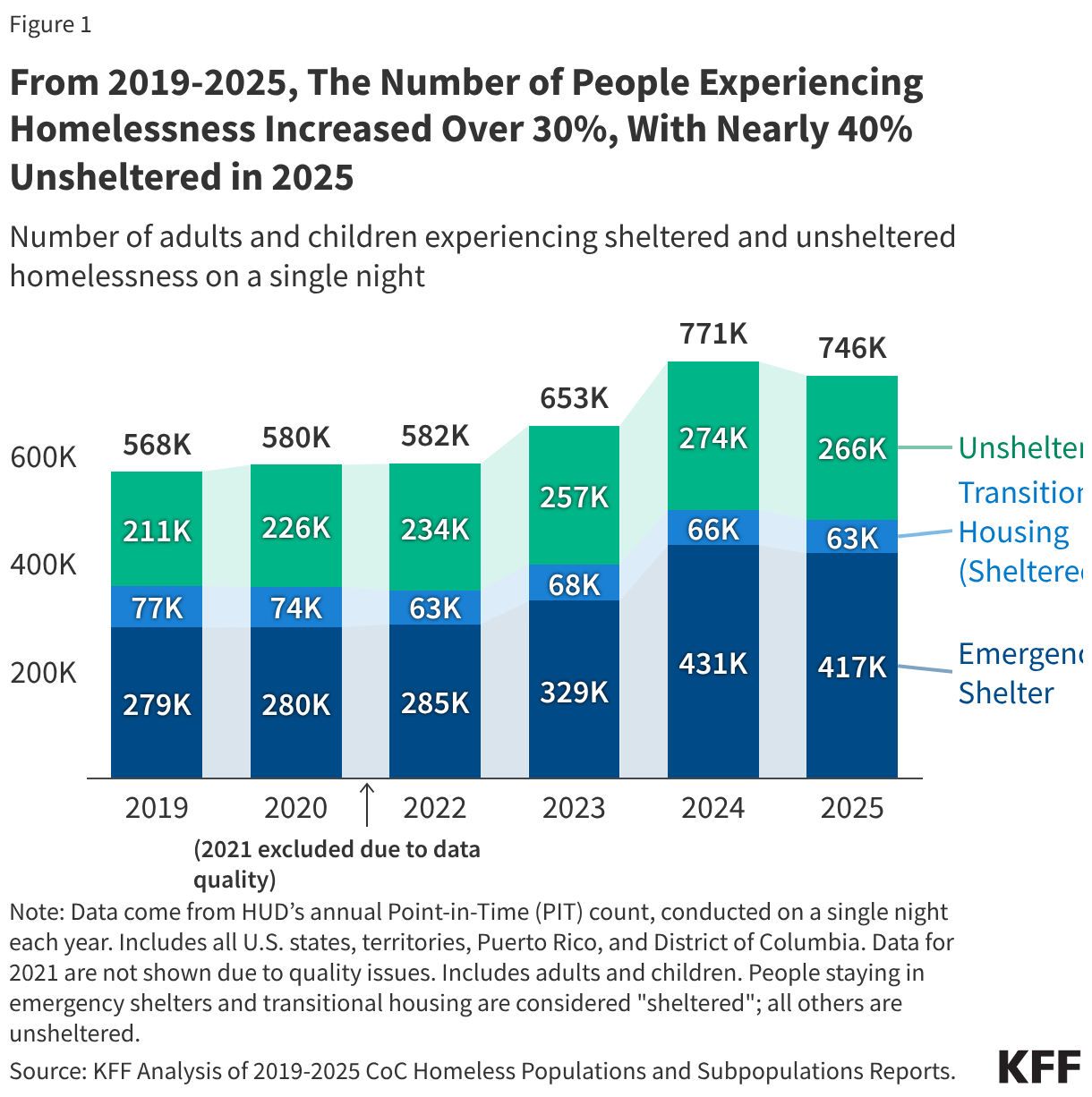

According to the most recent data available from the U.S. Department of Housing and Urban Development (HUD), nearly 746,000 people were experiencing homelessness on a single night in January 2025, an over 30% increase from 2019, but also a 3% decrease from the highest levels ever recorded in 2024. The links between homelessness and health are complex, and past KFF research found that people with prior experiences of homelessness have disproportionate physical and mental health needs and face greater socioeconomic challenges compared to those who have never experienced homelessness. People experiencing homelessness who are unsheltered also experience higher rates of chronic homelessness, chronic disease, mental illness, and substance abuse than those who are sheltered.

This data note reviews trends in homelessness and characteristics of people who are homeless using data from HUD’s Point-in-Time (PIT) count of sheltered and unsheltered people experiencing homelessness. The PIT count is generally conducted on a single night during the last ten days of January. While the PIT count is the primary nationally standardized measure to track trends in homelessness over time, these estimates likely undercount the total number of people experiencing homelessness, particularly among the unsheltered, due to challenges locating individuals who are unsheltered, local staffing capacity, and weather. The PIT count also does not include people who are staying with family or friends, referred to as “doubling up”, in other unstable housing situations, or living in permanent supportive housing.

These data capture a look at homelessness amid a number of federal policy changes aimed at clearing homeless encampments, limiting provisions for housing alternatives, and potentially resulting in institutionalization among people experiencing homelessness. President Trump signed an executive order in July 2025 on homelessness, mental health, and substance use that encouraged states to remove unhoused people from public spaces, following nationwide passage of Supreme Court-backed local laws making it easier for law enforcement to ticket, fine, or arrest people sleeping on public property. HUD proposed to shift homelessness services spending away from “Housing First” programs–which provide immediate housing without preconditions such as sobriety or mandatory mental health treatment—towards “transitional housing” programs, and require local homelessness services entities to cooperate with law enforcement to prohibit homeless encampments, but was blocked by court ruling in June 2026. Most recently, the Department of Justice (DOJ) issued an opinion in June 2026 and a notice in July 2026 challenging the longstanding interpretation of the Olmstead Supreme Court decision, signaling narrower federal enforcement of the integration mandate, which has helped spur state investment in rental assistance, supportive housing, and community services for people with disabilities. These changes could potentially result in fewer community services and increased institutionalization among people experiencing homelessness.

1. From 2019 to 2025, the number of people experiencing homelessness on a single night increased by over 30% to nearly 746,000 people, with nearly four in ten (36%) staying in unsheltered locations.

The HUD PIT survey counts people experiencing homelessness in both sheltered and unsheltered settings on a single night. People are counted as unsheltered if they sleep in locations not ordinarily used as a regular sleeping accommodation, such as cars, parks, abandoned buildings, or campgrounds. The remainder of people experiencing homelessness were in sheltered locations, with nearly six in ten (56%) staying in emergency shelters and nearly one in ten (8%) in transitional housing, which is temporary housing with supportive services (Figure 1).

Between 2019 and 2025, the number of people experiencing homelessness rose by 31%. This increase was primarily driven by the growth in the number of people staying in emergency shelters and experiencing unsheltered homelessness, while the number of people in transitional housing declined over the same period. According to HUD, rising housing costs and the end of the COVID-19 public health emergency in May 2023, which ended the eviction moratorium and other income and safety net programs, drove recent increases. Counts of people experiencing homelessness peaked in 2024 and then decreased 3% from 2024 to 2025, with nearly 60% of the decrease driven by a reduction in the number of people in emergency shelters.

Beyond shifts in sheltered and unsheltered homelessness, the share of people experiencing homelessness identified as “chronic homelessness”—defined by HUD as having a disability, including physical, mental, developmental, substance use-related, or HIV/AIDS-related disabilities, and experiencing long-term or repeated episodes of homelessness of at least 12 months—increased from 19% in 2019 to 23% in 2025 (from about 106,000 to 170,000). However, the share of adults experiencing homelessness who were veterans fell from 8% in 2019 to 5% in 2025 (from about 37,000 to 33,000), similar to their share of the general adult population (6%). An increase in housing assistance programs from the Department of Veterans Affairs (VA) in recent years likely drove this decrease.

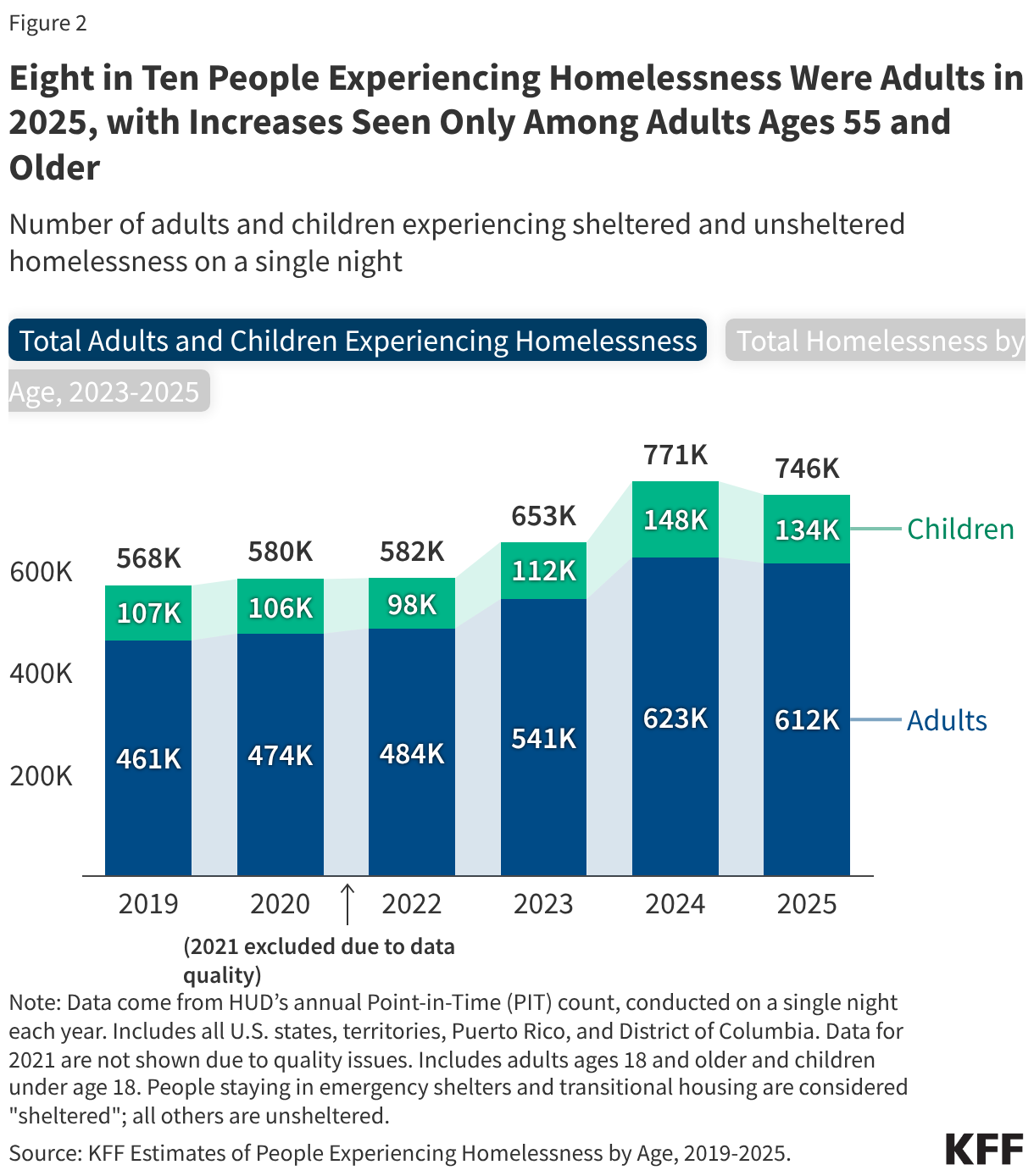

2. In 2025, over eight in ten (82%) people experiencing homelessness were adults, with decreases in the number of people experiencing homelessness seen across age groups since 2024 except among adults ages 55 and older.

On a single night in January 2025, there were about 612,000 adults and 134,000 children experiencing homelessness, with adults consistently representing about eight in ten of all people experiencing homelessness since 2019 (Figure 2). The number of children experiencing homelessness increased 25% from 2019 to 2025. However, after several years as the fastest-growing age group among people experiencing homelessness, the number of children experiencing homelessness fell 10% (from about 148,000 to 134,000) from 2024 to 2025. Most households with children experiencing homelessness are sheltered, as children made up less than one in ten (4%) unsheltered people in 2025. Housing insecurity during childhood is associated with negative health outcomes later in life, including anxiety and depression. The number of adults experiencing homelessness fell 11% among adults ages 18-24 and 2% among adults ages 25-54 from 2024 to 2025 but increased among those ages 55 and older by 2%. While long-term data for these specific age ranges are not available prior to the 2023 PIT count, research found that adults born between 1955 and 1965 have comprised a disproportionate share of single adults experiencing sheltered homelessness across several decades, suggesting that the aging of this cohort has contributed to the recent rise in adults ages 65 and older experiencing homelessness.

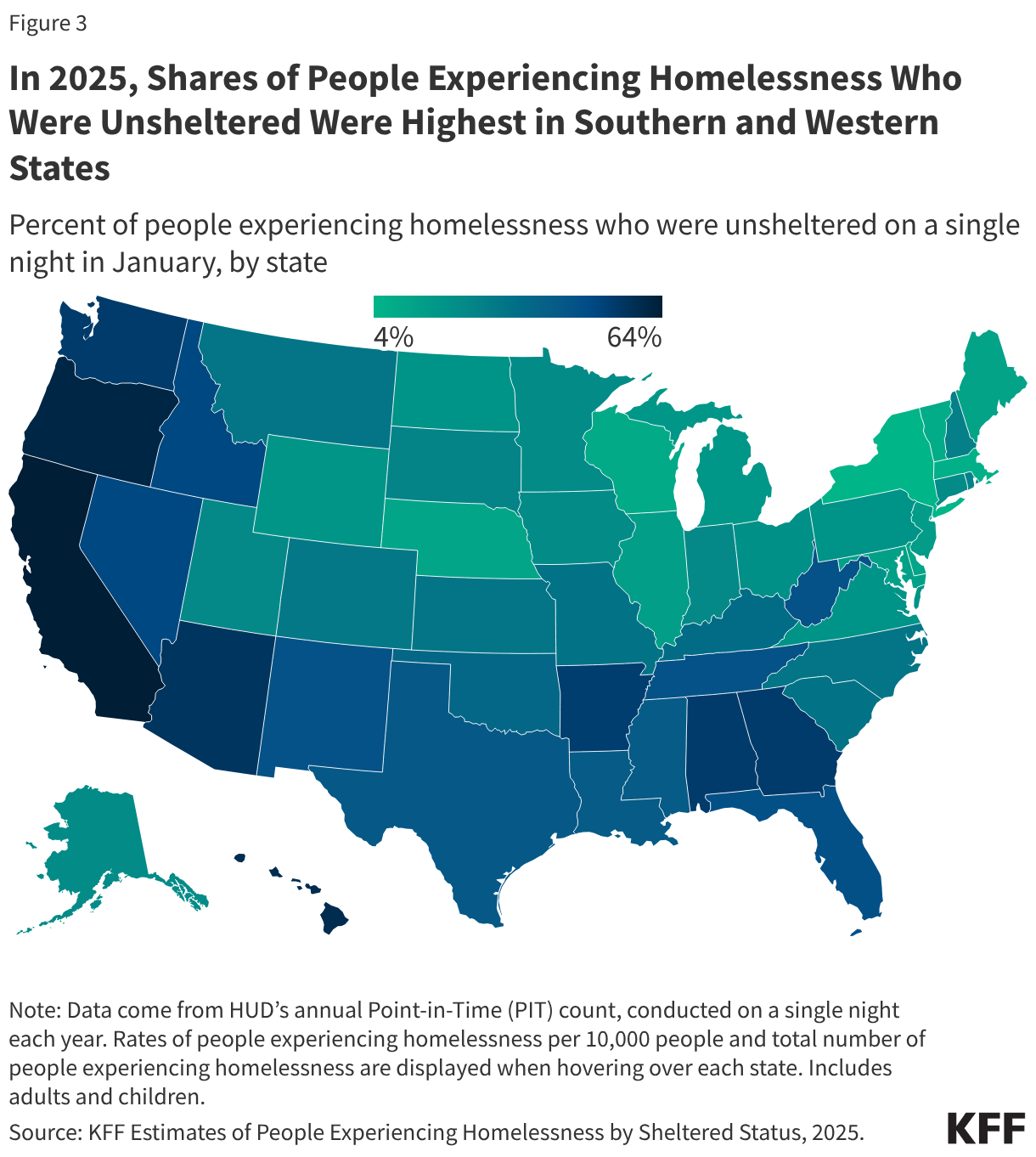

3. In 2025, Southern and Western states had higher shares of people who were experiencing homelessness who were unsheltered compared to other parts of the country.

States in the Northeast and West had higher rates of people experiencing homelessness per 10,000 people than elsewhere in the country on a single night in January 2025 (Figure 3). The share of people experiencing homelessness who were unsheltered by state were highest in Southern and Western states, including in California (64%), Oregon (61%), Arizona (56%), and Georgia (54%). In contrast, the shares of people experiencing homelessness who were unsheltered were lowest in New York (4%) and Massachusetts (6%), despite these states having relatively high rates of people experiencing homelessness per 10,000 people. These patterns may reflect a combination of local factors, including climate, housing costs, shelter capacity, right to shelter laws, and law enforcement policies that bring more people into emergency shelters or other sheltered housing.

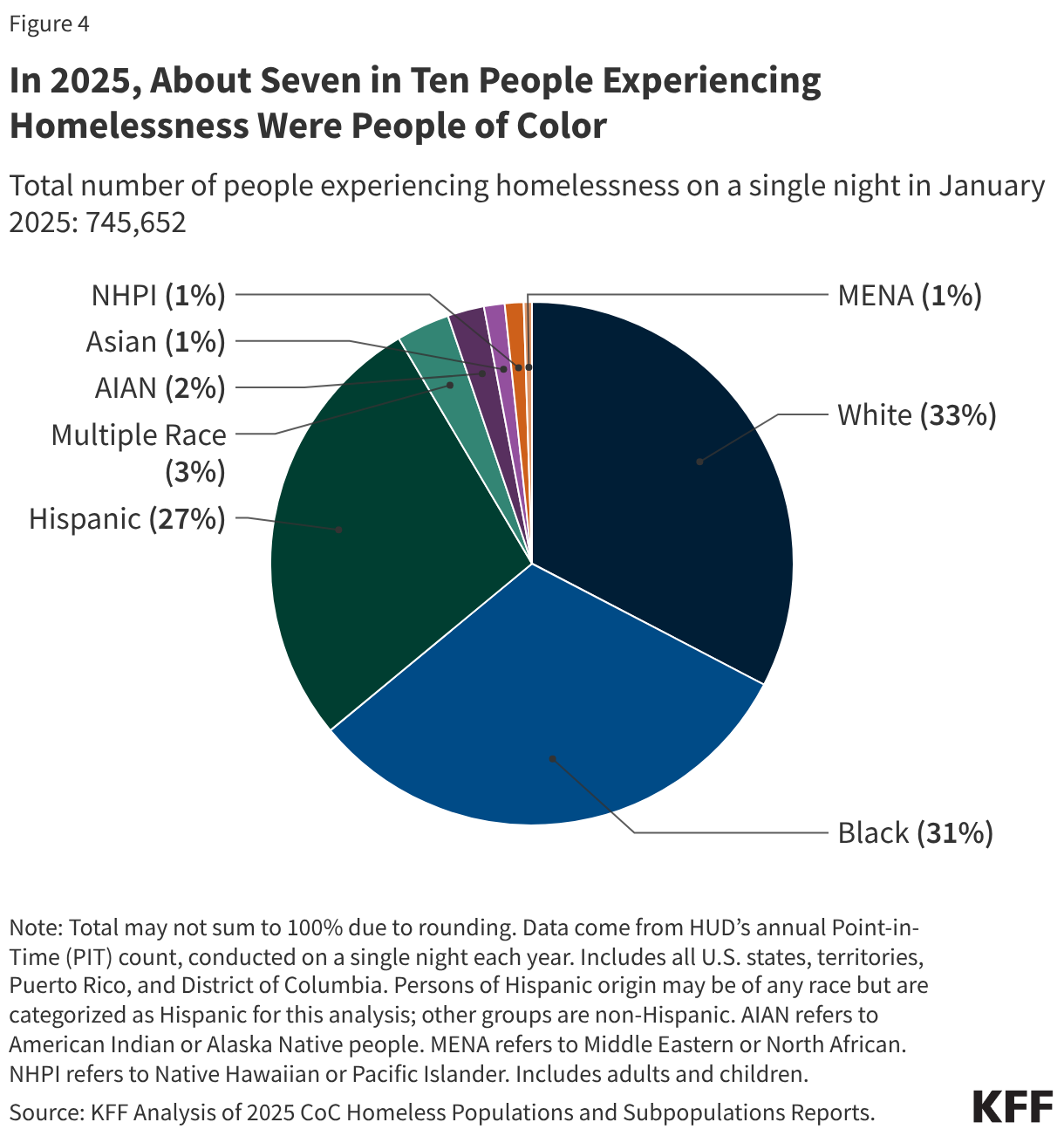

4. In 2025, about seven in ten (67%) people experiencing homelessness were people of color.

White (33%), Black (31%), and Hispanic (27%) people each accounted for about three in ten of people experiencing homelessness on a single night in January 2025, with other racial and ethnic groups making up smaller shares (less than 5%) (Figure 4). Black, Hispanic, AIAN, and NHPI people made up a disproportionate share of the people experiencing homelessness compared to their share of the total population.

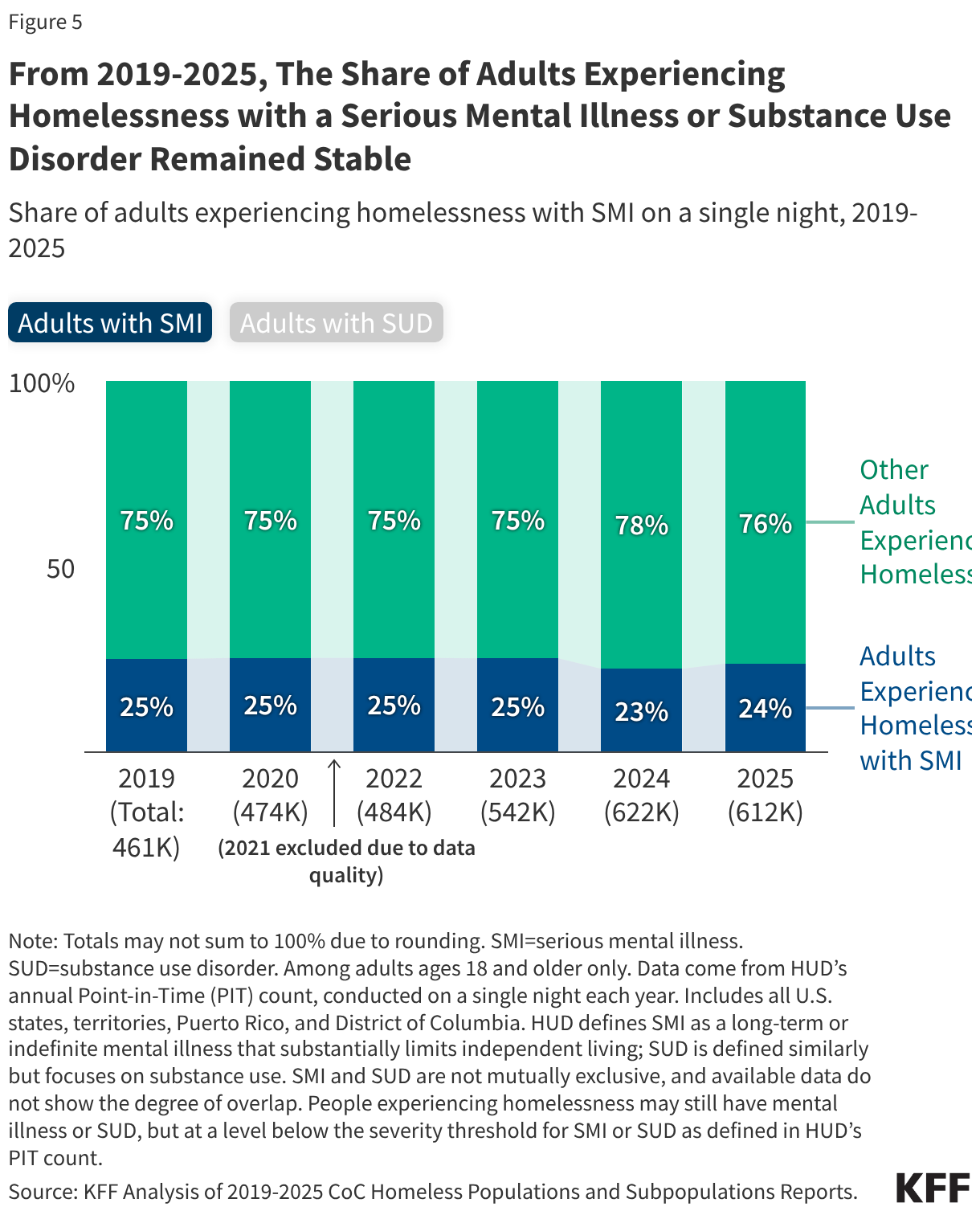

5. From 2019 to 2025, the share of adults experiencing homelessness with serious mental illness (SMI) or substance use disorder (SUD) remained stable, suggesting that rising homelessness reflects broader factors affecting both people with and without these conditions.

In 2025, about a quarter (24%, or 146,000) of adults experiencing homelessness on a single night in January met HUD’s SMI definition and nearly one in five (18%, or 112,000) had SUD according to HUD’s definition in the point-in-time count, about a 1% decrease from 2019 (Figure 5). SMI and SUD often co-occur—about one-quarter of people with SMI also have an SUD—but HUD’s publicly available data do not report the overlap of these conditions. The prevalence of SMI and SUD represents an outsized share of the population of adults experiencing homelessness as about 5-6% of adults overall have SMI according to the National Survey of Drug Use and Health (NSDUH) and 3% of adults in the general population meet NSDUH criteria for severe SUD. While homelessness among adults increased sharply from 2019 to 2025, the share of adults with SMI or SUD changed little, suggesting the increase was not concentrated among people with behavioral health conditions, and likely reflects broader pressures, such as rising housing and living costs. A Government Accountability Office (GAO) report found that a $100 increase in median rental price was linked to a 9% increase in estimated homelessness rate. Other research found increases in the number of people experiencing homelessness from 2019 to 2024 were more strongly associated with reductions in eviction moratoriums and climate-related events.

As of 2024, there were about 50 million immigrants residing in the U.S. Within this group, there were 24 million noncitizen immigrants, including lawfully present and undocumented immigrants, and 26 million naturalized citizens, who accounted for about 7% and 8% of the total population, respectively. Actions taken by the Trump administration and Congress will likely have major impacts on health and health care for immigrant families, including increasing the number of uninsured immigrants.

While undocumented immigrants have been ineligible for federally-funded health coverage programs under longstanding policy, the 2025 reconciliation law includes new eligibility restrictions for many lawfully present immigrants, including refugees and asylees, to access Medicaid and the Children’s Health Insurance Program (CHIP), subsidized Affordable Care Act (ACA) Marketplace, and Medicare coverage. The CBO estimates that 1.4 million lawfully present immigrants could lose health coverage by 2034 due to the law’s eligibility changes. Research shows that having insurance makes a difference in whether and when people access needed care. Those who are uninsured often delay or go without needed care, which can lead to worse health outcomes over the long-term that may ultimately be more complex and expensive to treat.

This brief provides data on health and health care experiences of uninsured immigrant adults based on a KFF survey of immigrant adults ages 18 and older conducted in partnership with The New York Times in Fall 2025. The data provide insight into how the projected coverage losses under the 2025 reconciliation law may impact health and health care for immigrant families as more lawfully present immigrants become uninsured. Key takeaways include the following:

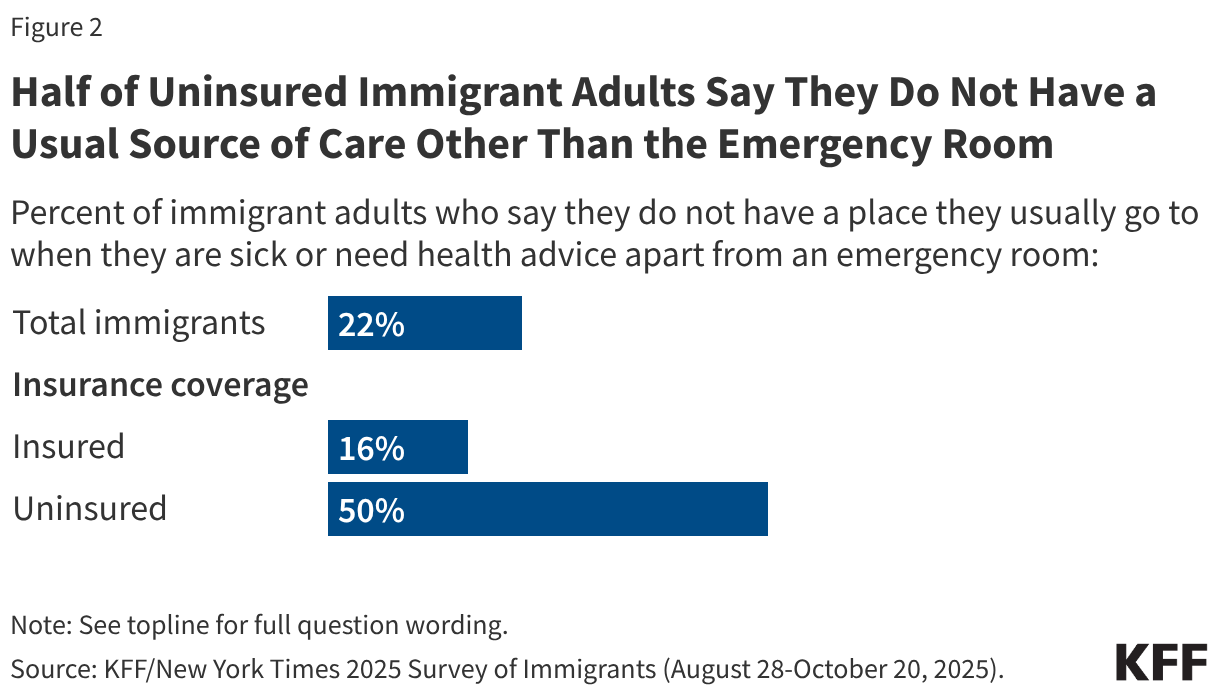

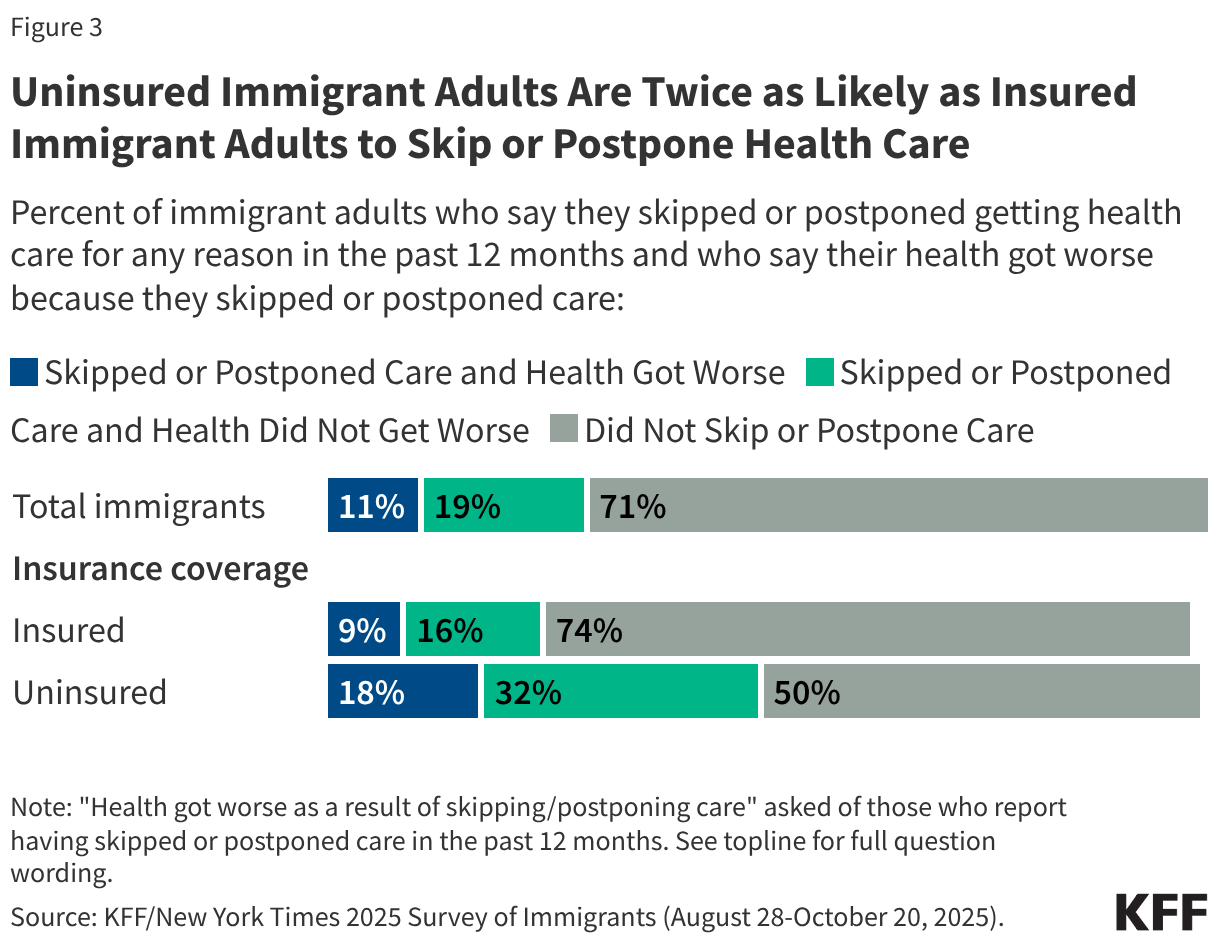

Compared to those with insurance coverage, uninsured immigrant adults are more likely to not have a usual source of care and to delay or go without health care. Half of uninsured immigrant adults say that they do not have a usual source of health care other than the emergency room compared to about one in six (16%) of their insured counterparts. Further, half of uninsured immigrant adults report skipping or postponing care, twice the share of those with coverage (50% vs. 26%). Nearly one in five (18%) of all uninsured immigrant adults said their health got worse as a result of skipping or postponing health care.

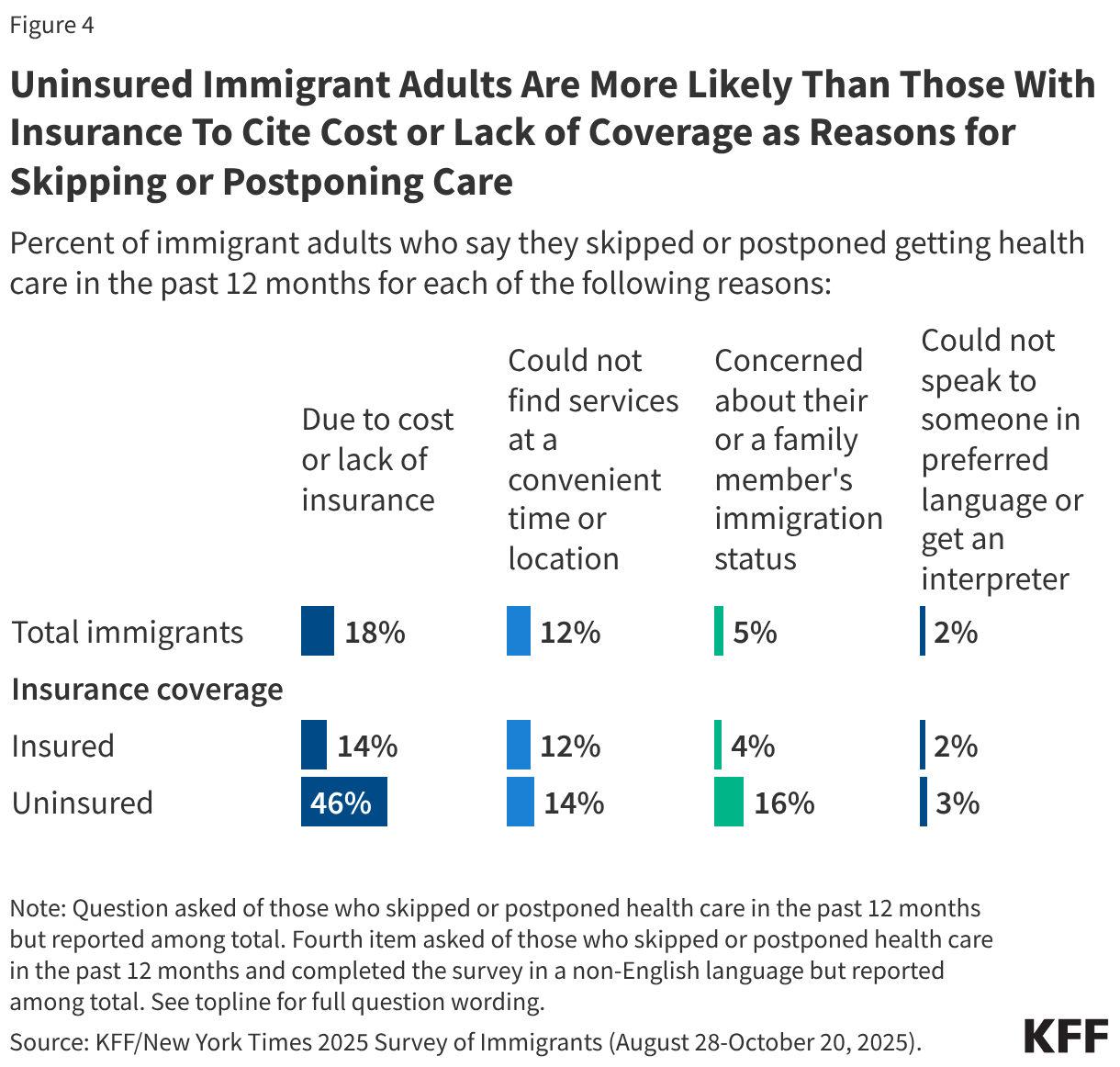

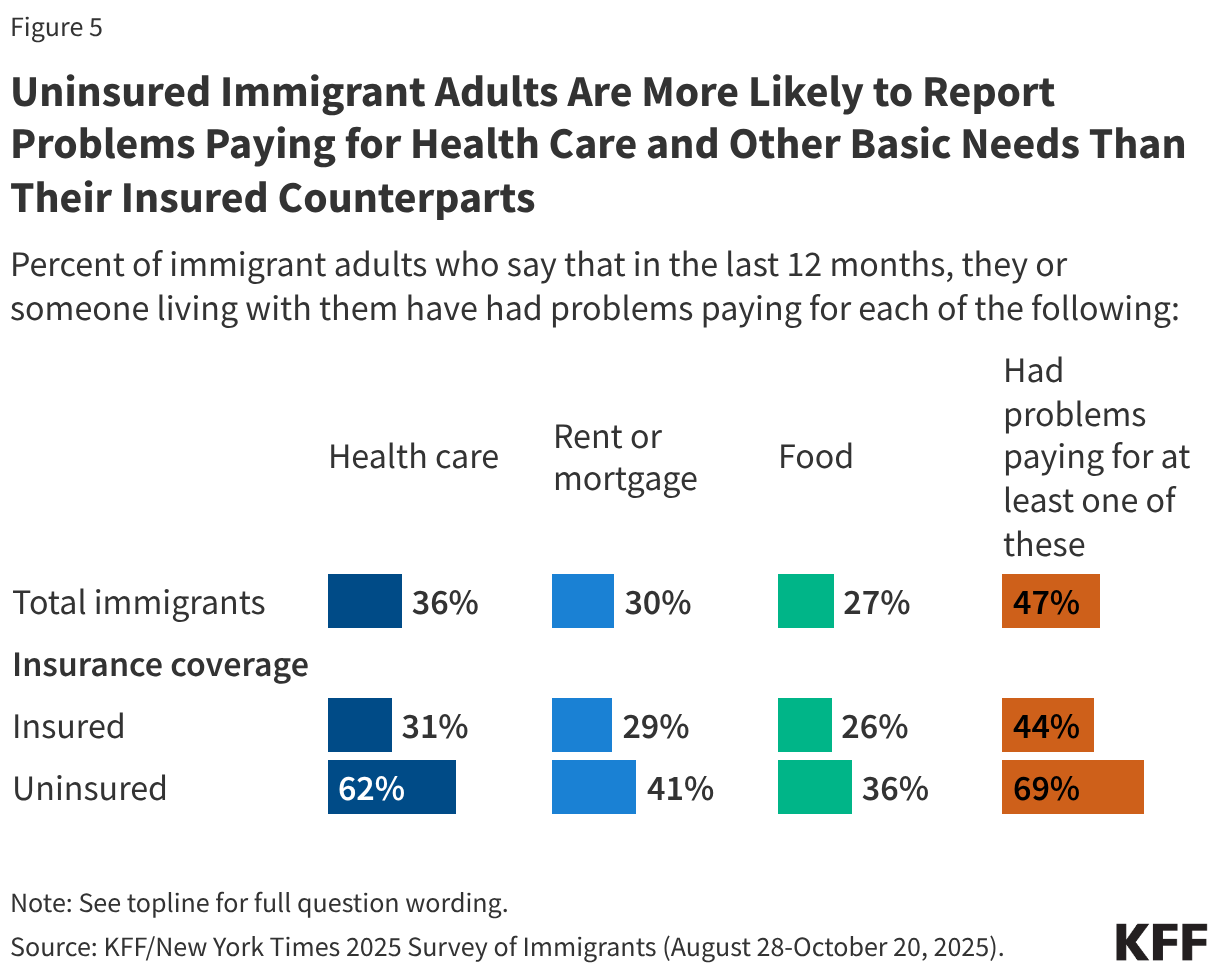

Cost or lack of coverage is the primary reason uninsured immigrant adults cite for skipping or postponing care, reflecting the role insurance plays in facilitating access to care. Almost half (46%) of uninsured immigrant adults say they delayed or went without care because of cost or lack of insurance compared to 14% of insured immigrant adults. Overall, about seven in ten (69%) uninsured immigrant adults say they have had problems paying for health care (62%), housing (41%), or food (36%) in the past 12 months. In comparison, over four in ten (44%) insured immigrant adults report problems paying for health care (31%), housing (29%), or food (26%) in the past 12 months.

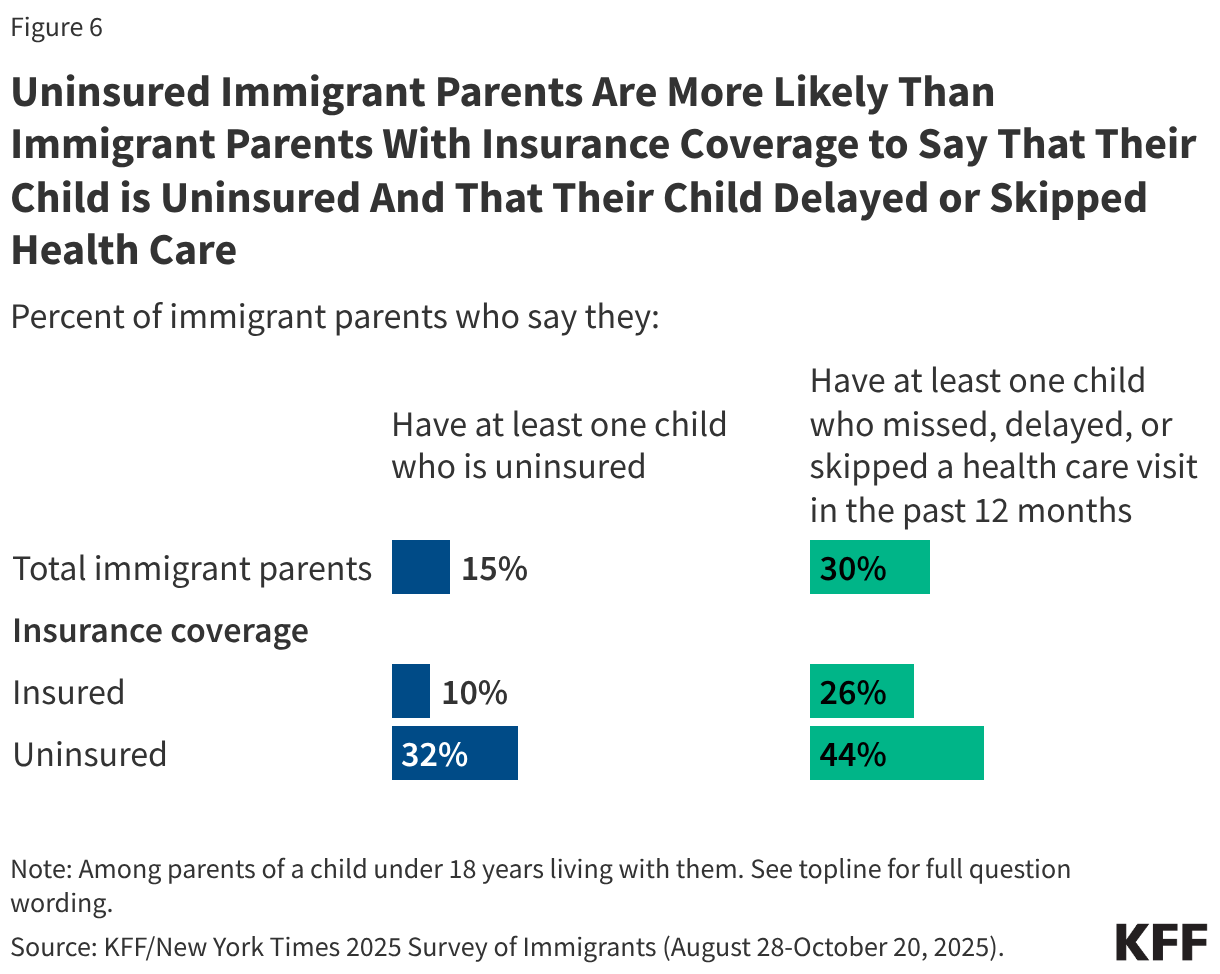

Consistent with other researchdemonstrating that parental coverage affects children’s health coverage and access to care, uninsured immigrant parents are three times as likely as those with insurance coverage (32% vs. 10%) to say they have at least one child who is uninsured. Further, over four in ten (44%) uninsured immigrant parents say any of their children delayed or skipped health care in the past 12 months compared to about a quarter (26%) of those with insurance coverage.

Findings

Characteristics of Uninsured Immigrants

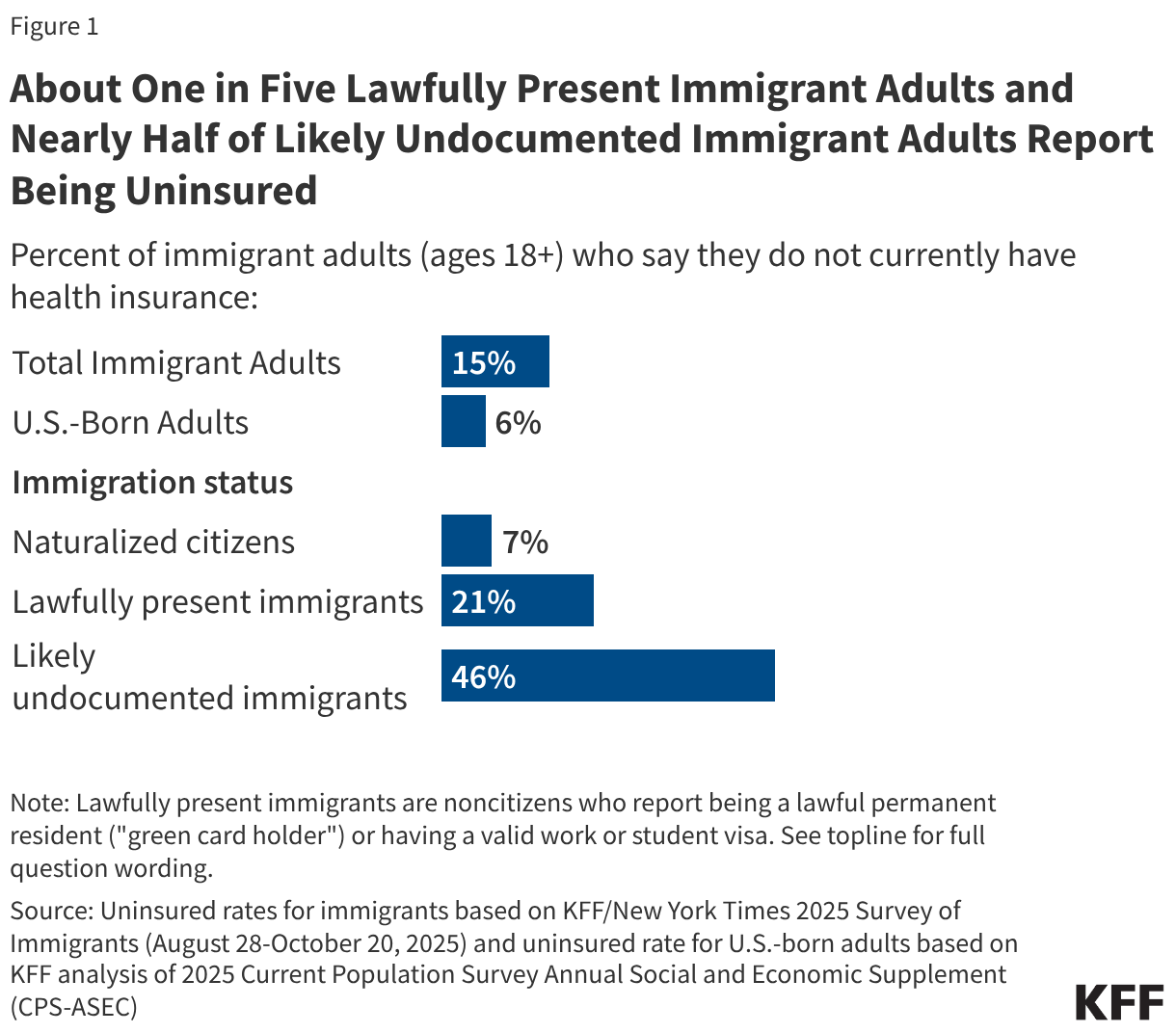

About one in seven (15%) immigrant adults age 18 and older report being uninsured as of 2025, with higher uninsured rates among those who are noncitizens, Hispanic, lower income, have limited English proficiency (LEP), or live in states with less expansive coverage. Nearly half of likely undocumented immigrant adults (46%) and one in five lawfully present immigrant adults (21%) report being uninsured compared to fewer than one in ten of their U.S.-born (6%) and naturalized citizen (7%) counterparts (Figure 1). Uninsured rates also are higher among immigrant adults who are Hispanic (27%), have lower incomes (household income of less than $40,000 per year) (23%), or have LEP (23%) compared to their White (5%), higher income (household income of $90,000 or more per year) (4%), and English proficient (10%) counterparts, likely reflecting that these groups also are more likely to be noncitizens. Further, immigrant adults who live in states that provide less expansive coverage, including not adopting the ACA Medicaid expansion to all low-income adults or any coverage expansions for immigrants, are about twice as to be uninsured compared with those living in states with more expansive policies (23% vs. 11%).

Access to Health Care

Half of uninsured immigrant adults say they do not have a usual source of care other than an emergency room (Figure 2). In comparison, about one in six (16%) insured immigrant adults say they do not have a usual source of care other than an emergency room. Research shows that having a usual source of care is associated with better access to health care even after controlling for demographic and socioeconomic characteristics.

Uninsured immigrant adults are about twice as likely as those who are insured to report delaying or going without needed care (50% vs. 26%) (Figure 3). Delaying or going without needed care can contribute to health problems becoming worse and taking more time and resources to treat. Nearly one in five (18%) of uninsured immigrant adults say they skipped or postponed health care and their health got worse compared to 9% of insured immigrant adults.

Uninsured immigrant adults are more likely than those with insurance to cite cost or lack of coverage and immigration-related concerns as reasons for delaying or going without care. Almost half (46%) of uninsured immigrant adults say they delayed or went without care because of cost or lack of insurance compared to 14% of insured immigrant adults (Figure 4). Additionally, 16% of uninsured immigrant adults identified concerns about their or a family member’s immigration status as a reason compared to 4% of insured immigrant adults, likely reflecting that uninsured immigrants include a higher share of likely undocumented immigrants. Similar shares of uninsured (14%) and insured immigrant adults (12%) cited not being able to find services at a time or location that worked for them as a reason for delaying or going without care. Language barriers were also cited by some of those with LEP.

Likely reflecting their lower incomes, uninsured immigrant adults report more difficulty paying for basic needs, including health care, compared to those with insurance. Six in ten uninsured immigrant adults say that it has been harder to earn a living since January 2025 (60%) and about seven in ten (69%) say they have had problems paying for basic necessities such as health care (62%), housing (41%), or food (36%) in the past 12 months (Figure 5). These shares are higher compared to those with insurance coverage, with the largest gap in difficulty paying for health care (62% vs. 31%).

Impacts of Parental Coverage on Children’s Coverage and Access to Care

Uninsured immigrant parents are about three times as likely as insured immigrant parents (32% vs. 10%) to report at least one uninsured child as of 2025 (Figure 6). Further, over four in ten (44%) uninsured immigrant parents say any of their children delayed or skipped health care in the past 12 months compared to about a quarter (26%) of those with insurance coverage. These findings are consistent with other research showing that parental coverage impacts children’s access to health coverage and care.

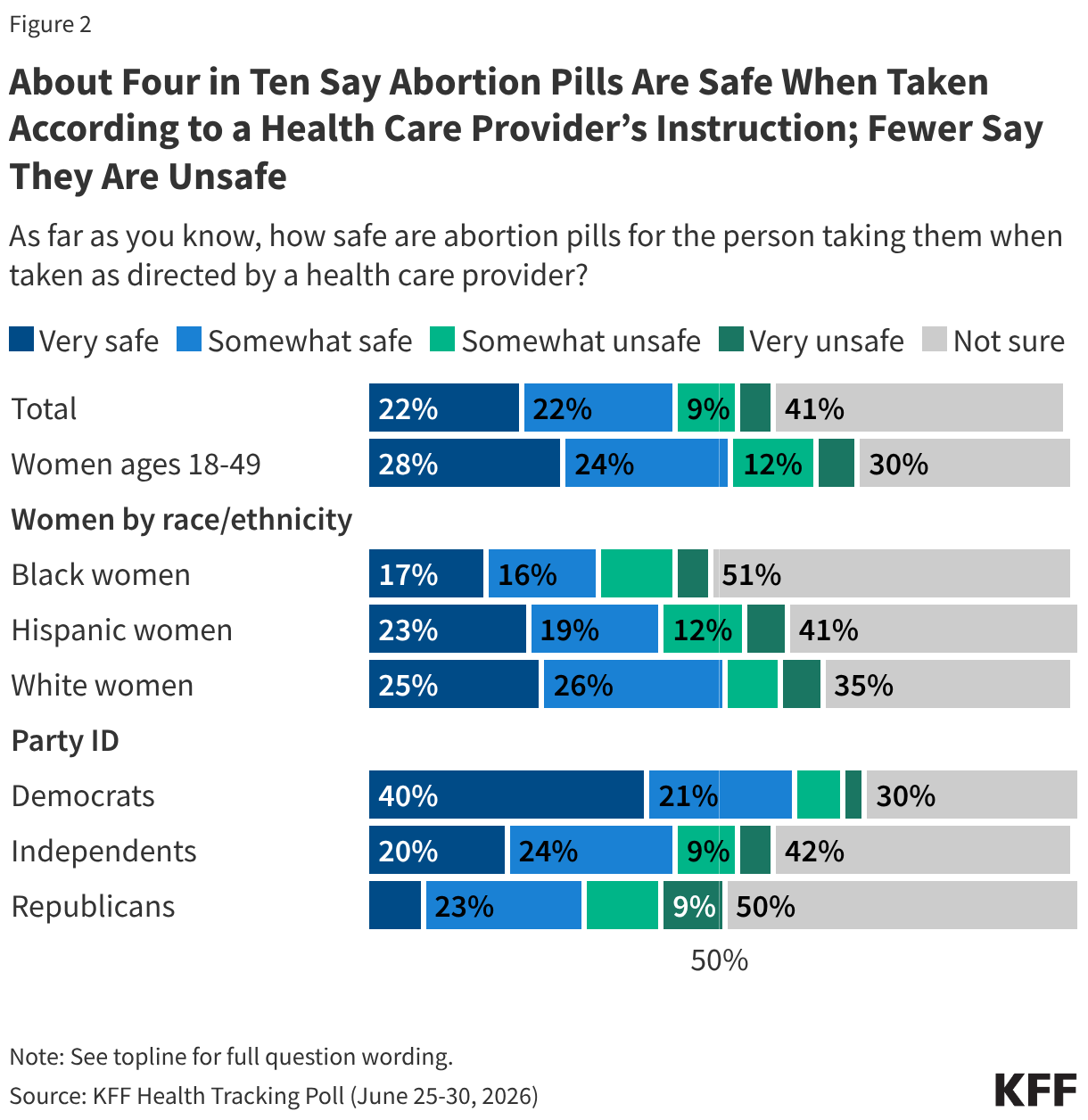

The latest KFF Health Tracking Poll finds that though a majority of the public has heard of the abortion medication mifepristone, public awareness of its prevalence and longstanding safety record is limited. Six in ten adults say they have heard of mifepristone, but just one in four (26%) correctly identify abortion pills as the most common way abortions are administered in the U.S. Additionally, while about four in ten (44%) adults say abortion pills are safe when taken according to a health care provider’s instruction, one in seven (15%) say they are unsafe and four in ten (41%) are unsure of their safety.

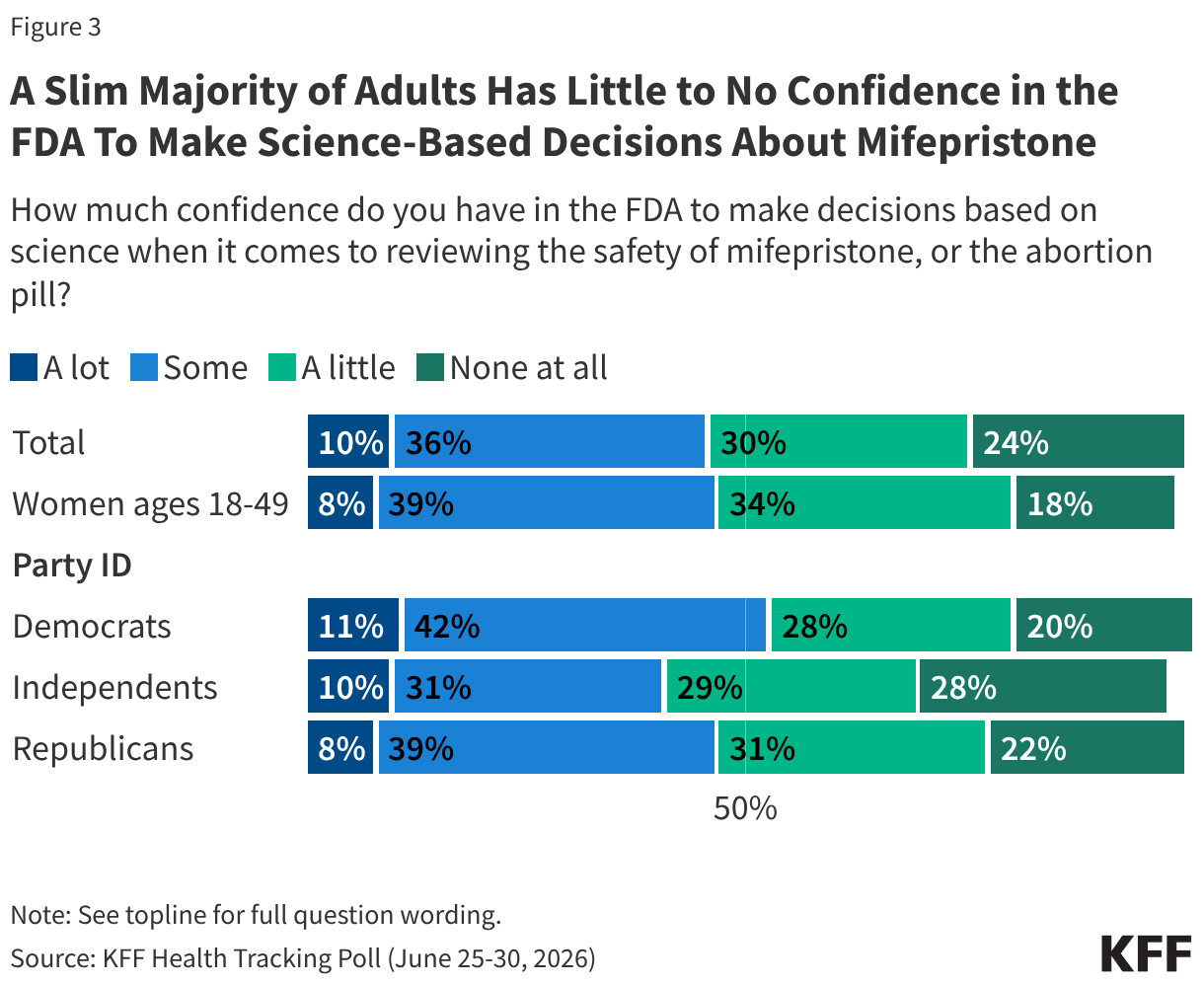

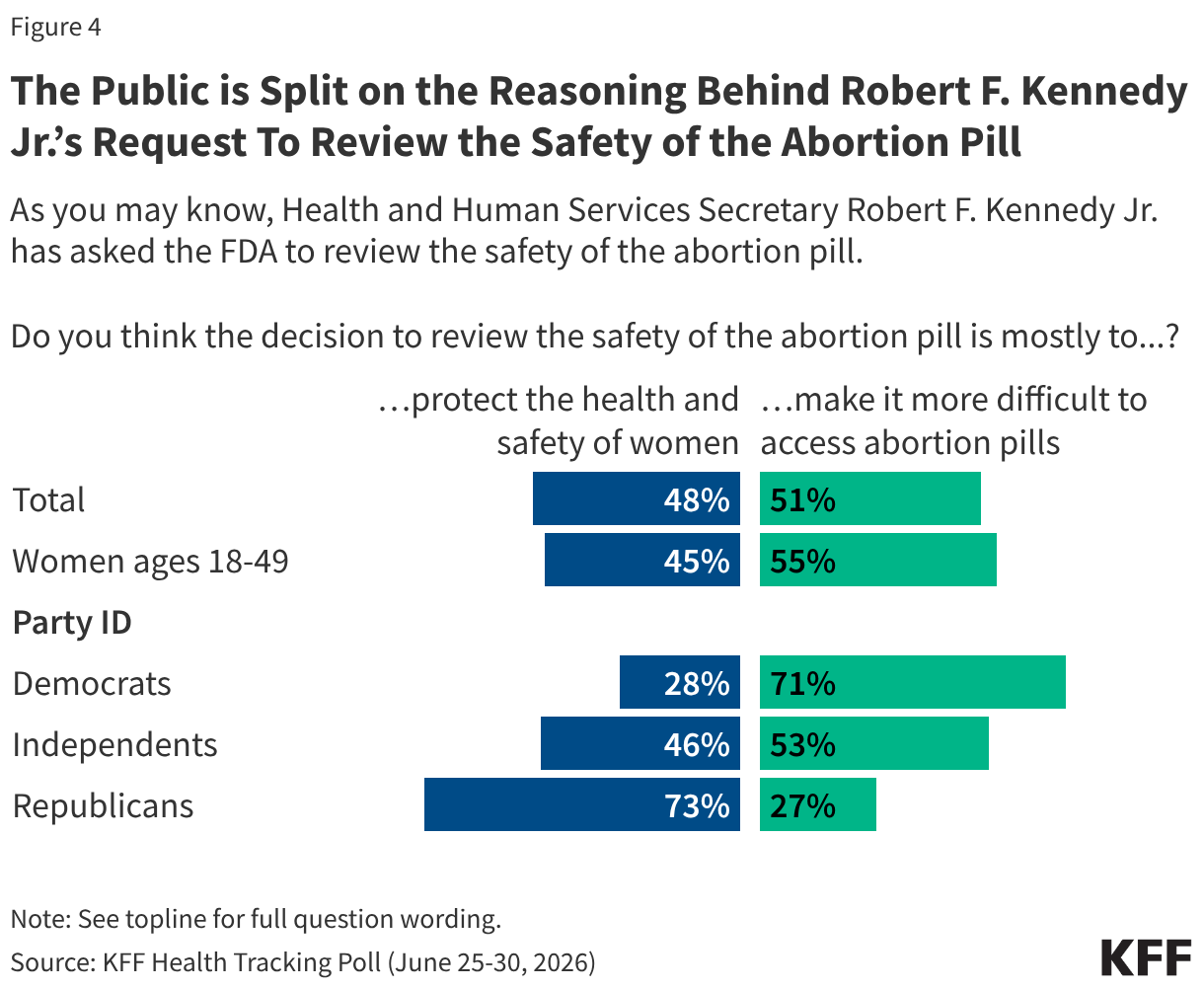

The FDA’s re-evaluation of the safety of mifepristone is now underway, following Health and Human Services Secretary Robert F. Kennedy Jr.’s call to the federal health agency late last year. Public confidence in the FDA to make decisions based on science when reviewing the safety of mifepristone is somewhat limited as slightly more than half (54%) say they have little to no confidence at all in this regard. Partisans differ over the motivation behind the review, with a majority of Republicans saying it was mostly to protect the health and safety of women and a similar majority of Democrats saying it was to make abortion pills more difficult to access.

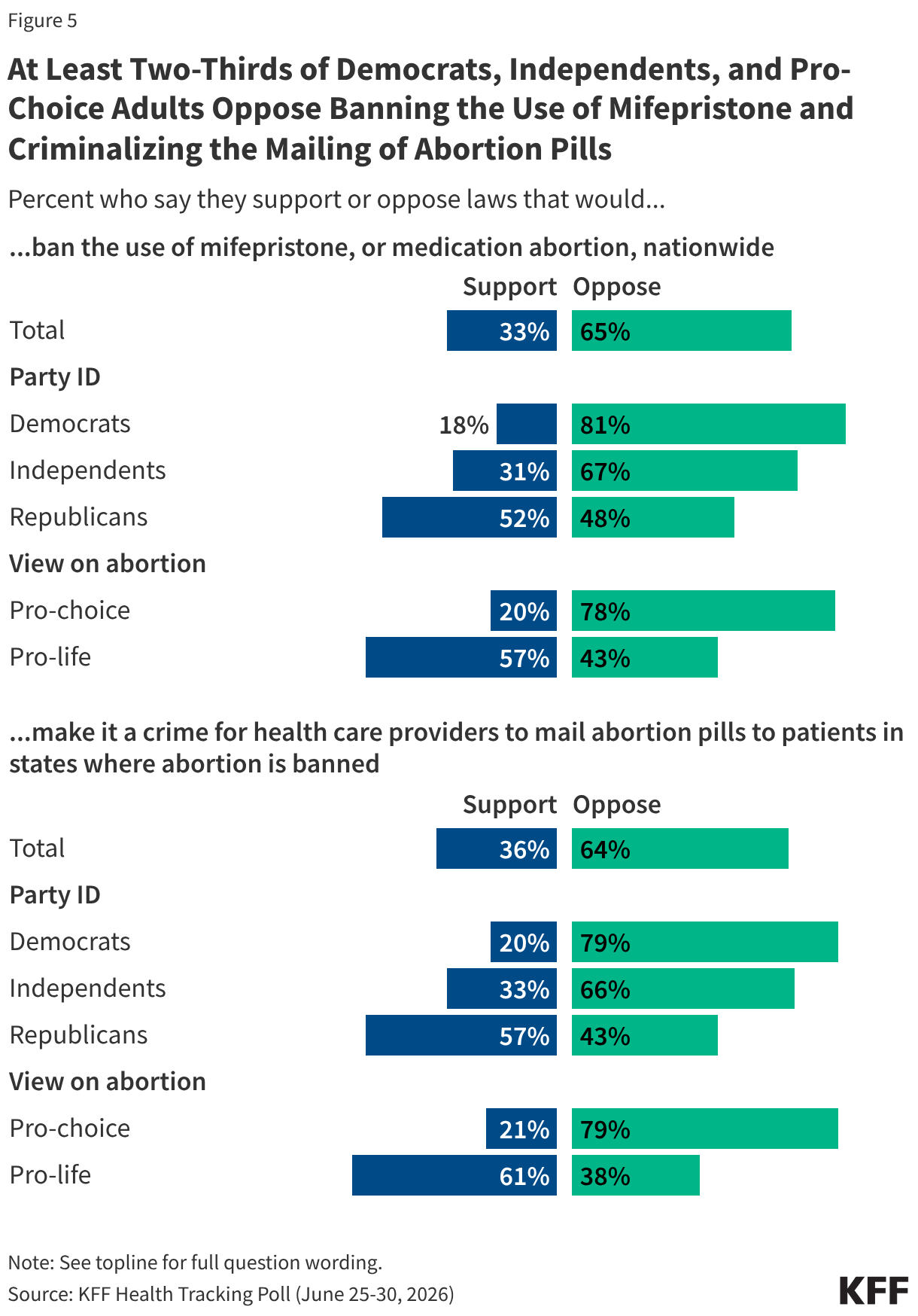

Majorities of the public oppose laws restricting medication abortion, though Republicans lean more in support. Two-thirds of the public – including large majorities of Democrats and independents – oppose laws that would ban mifepristone nationwide (65%) and laws that would make it a crime for health care providers to mail abortion pills to patients in states with abortion bans (64%). Republicans are notably split on the issue of banning mifepristone nationwide (52% support, 48% oppose), while a majority (57%) of Republicans support laws criminalizing health care providers mailing abortion pills to patients in states with abortion bans.

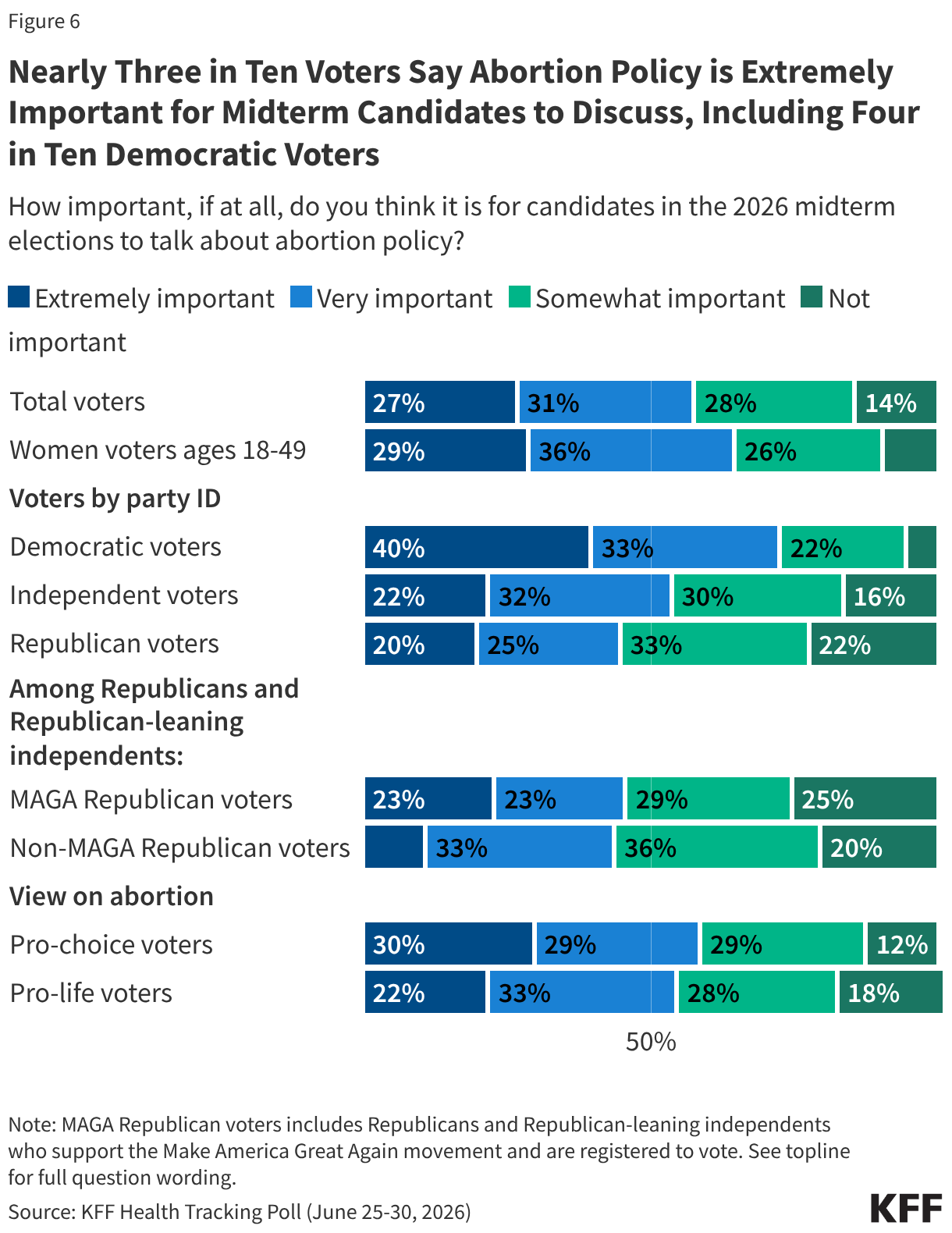

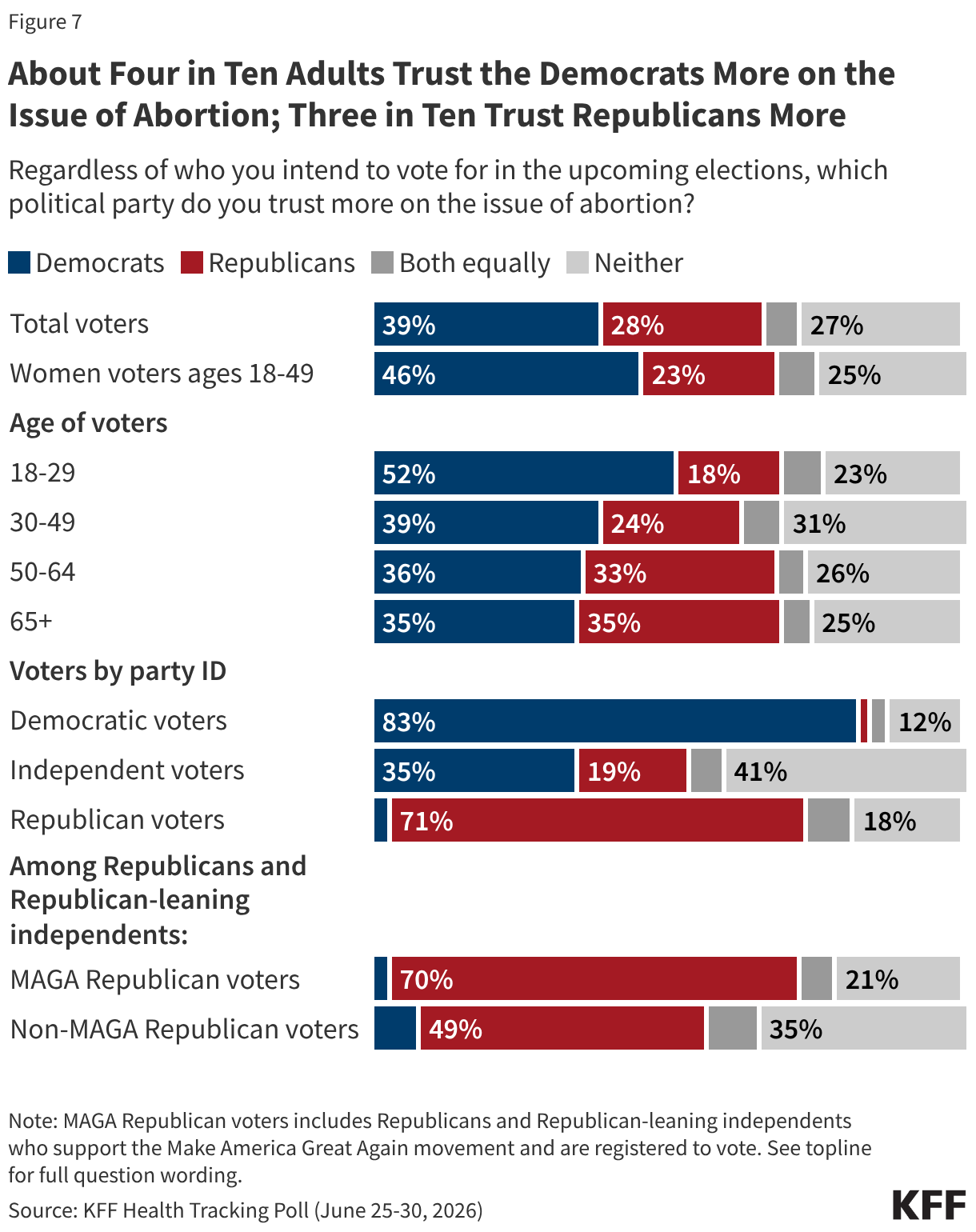

While health costs and the future of government health programs are key health issues for voters in the upcoming midterm elections, a majority of voters (57%) say it is “extremely” or “very important” for candidates to discuss abortion policy. Since the Dobbs decision, abortion policy remains a core issue for Democratic voters. Four in ten Democratic voters say abortion policy is “extremely important” for 2026 midterm candidates to talk about, compared to fewer independent (22%) and Republican (20%) voters. The Democratic Party has the advantage over the Republican Party when it comes to which political party voters trust more on the issue of abortion (39% vs. 28%, respectively), though nearly three in ten (27%) voters say they trust neither party on this issue. Among independent voters, the Democratic Party has the edge over the Republican Party (35% vs. 19%), though four in ten say they trust neither party on the issue.

Sizeable Shares of the Public Are Unaware of Mifepristone’s Prevalence and Safety

Mifepristone, commonly known as the abortion pill, is one of two drugs that are used in medication abortion, the most common abortion method in the United States. While mifepristone has been approved by the FDA for over 25 years and has a longstanding safety record, Congressional Republicans and anti-abortion groups continue to call into question the safety of the abortion pill. The latest KFF Health Tracking Poll finds six in ten (60%) adults have heard of the abortion medication mifepristone, including two-thirds (66%) of women of reproductive age (ages 18 to 49). Public awareness of mifepristone has risen sharply since the overturning of Roe v. Wade and the lawsuits and public scrutiny of the abortion pill that followed, increasing from 31% in January 2023 to about six in ten since then.

Despite increased awareness of mifepristone, the public is still largely unaware that most abortions in the U.S. are done by taking abortion pills. About one-quarter of adults (26%) correctly identify abortion pills as the most common way abortions are administered in the United States, while another quarter (26%) incorrectly say medical procedures are the most common, and nearly half (48%) say they are not sure. Democrats, independents, women of reproductive age, and adults who identify as “pro-choice” are most likely to correctly say most abortions in the U.S. are done using abortion pills. Yet, even among these groups, about half say they are not sure how most abortions in the U.S. are provided.

A large share of the public is unaware of the abortion medication’s longstanding safety record. Less than half (44%) of adults say abortion pills are safe when taken according to a health care provider’s instruction, about three times larger than the share who say they are unsafe (15%). Still, four in ten (41%) adults are “not sure” about the safety of abortion pills when administered according to a health care provider’s instruction.

Similar shares of adults overall say abortion pills are safe compared to last year (42% in November 2025). Among women ages 18 to 49, the group who would be most directly impacted by changes to the availability of mifepristone, about half (52%) say abortion pills are safe when taken as directed by a health care provider, a share that has increased from four in ten (41%) last November. Currently, one in five (19%) women ages 18-49 say they are not safe and three in ten are not sure of their safety.

Looking at women across racial and ethnic groups, Black women are less likely than White women to say abortion pills are safe (33% vs. 51%) and more likely than White women to say they are unsure how safe they are (51% vs. 35%). Among Hispanic women, about four in ten (42%) say abortion pills are safe, while a similar share (41%) say they are unsure.

Partisans differ in their assessment of the safety of mifepristone, with about six in ten Democrats (61%) saying medication abortion pills are “very” or “somewhat safe,” compared to about four in ten (44%) independents and three in ten Republicans. Larger shares of independents (42%) and Republicans (50%) than Democrats (30%) say they are not sure whether abortion pills are safe.

Public Divides Over Motives Behind FDA Review of Mifepristone and Ability to Conduct a Scientific Review

Last September, Health and Human Services Secretary Robert F. Kennedy Jr. and the FDA Commissioner at the time—Dr. Marty Makary—wrote to Republican state attorneys general in response to states’ concerns about mifepristone, announcing the FDA would conduct another review of the abortion pill’s safety. This new review has now begun and FDA officials are investigating whether the abortion pill’s current Risk Evaluation and Mitigation Strategy (REMS) is “sufficient to protect women from unstated risks” following the 2023 update that removed the in-person dispensing requirement and therefore made the drug accessible through telehealth. Depending on the safety review’s conclusions, the FDA could restrict mifepristone access, potentially limiting its availability through telehealth and mail, limiting the ability of advance practice clinicians from prescribing the medication, or removing pharmacies as authorized dispensers.

The latest KFF Health Tracking Poll finds a slim majority (54%) of the public has little to no confidence in the FDA to make decisions based on science when it comes to reviewing the abortion pill’s safety—including one in four (24%) who say they have no confidence “at all.” Fewer than half (46%) have “a lot” (10%) or “some” (36%) confidence. Among women of reproductive age, about half (52%) say they have little to no confidence, while 47% say they have at least some confidence. This limited trust is consistent with KFF’s Health Information and Trust research, which has found less than half of adults have confidence in the FDA’s ability to fulfill core responsibilities, such as making recommendations about childhood vaccine schedules and ensuring the safety and effectiveness of vaccines.

Across partisans, about half of Democrats and Republicans say they have little or no confidence (47% of Democrats; 53% of Republicans) in the FDA to make decisions based on science when evaluating the safety of mifepristone and similar shares say they have least some confidence (53% of Democrats; 47% of Republicans). Among independents, most (57%) say they have little to no confidence at all in the FDA in this regard.

When asked about the motivation behind Secretary Kennedy’s request to the FDA to review the safety of the abortion pill, the public is split, with half (51%) saying this decision was mostly to “make it more difficult to access abortion pills,” and another half (48%) saying it was mostly to “protect the health and safety of women.”

Notably, Democrats are more likely to say the reasoning behind Kennedy’s request was to “make it more difficult to access abortion pills” (71%), while Republicans are more likely to say it was to “protect the health and safety of women” (73%). Independents are split with about half saying the decision was to make abortion access more difficult (53%) and half saying it was to protect women’s safety (47%).

Women ages 18 to 49 are also divided on the motivation behind Secretary Kennedy’s request, with about half saying his call to review mifepristone was to “make it more difficult to access abortion pills” (55%) and another half saying it was to “protect the health and safety of women” (45%).

The latest KFF Health Tracking Poll finds majorities oppose laws that would place further restrictions on medication abortion. Around two-thirds of adults say they oppose banning the use of mifepristone, or medication abortion, nationwide (65%) and a similar share oppose making it a crime for health care providers to mail abortion pills to patients in states where abortion is banned (64%).

Eight in ten Democrats (81%) and two-thirds of independents (67%) say they oppose banning mifepristone entirely. However, Republicans are split in their views, with half (52%) saying they support laws that would ban the abortion pill nationwide while a similar share (48%) say they are opposed. And, while large majorities of Democrats (79%) and independents (66%) oppose laws making it a crime to mail abortion pills to patients in states with abortion bans, a majority (57%) of Republicans support such laws while 43% are opposed.

Unsurprisingly, about eight in ten adults who identify as pro-choice oppose the restrictive abortion laws asked about in this KFF Health Tracking Poll (78% banning mifepristone; 79% criminalizing the mailing of abortion pills to patients in states with abortion bans). Among those who identify as pro-life, majorities say they support these laws (57% and 61%, respectively), though sizeable shares—about four in ten—say they would oppose laws banning mifepristone nationwide (43%) and criminalizing the mailing of abortion pills to abortion-banned states (38%).

Voters’ Attitudes Toward Abortion in the Upcoming Midterm Elections

While health costs and the future of government health programs such as Medicare and Medicaid are the health issues taking center stage in this election, a majority of voters (57%) say it is “extremely” (27%) or “very important” (31%) for candidates to talk about abortion policy. Looking at voters by views on abortion, slightly larger shares of pro-choice voters say abortion is extremely important for 2026 midterm candidates to discuss compared to their pro-life counterparts (30% vs. 22%).

Previous election-related polling at KFF has found that, since the Dobbs decision, voters who view abortion policy as an important issue are disproportionately Democrats, and this election is no exception. Three-quarters (73%) of Democratic voters say abortion policy is important for 2026 midterm candidates to talk about, including four in ten who say it is “extremely important.” Notably, the share who say abortion policy is “extremely important” is consistent among Democratic voters, regardless of whether those voters live in states where abortion is either banned or limited (40%) or where abortion is available (39%). In contrast, fewer independent (22%) and Republican (20%) voters say abortion policy is extremely important for midterm candidates to discuss.

Among Republican and Republican-leaning independent voters who support the Make America Great Again movement, nearly one in four (23%) say abortion policy is extremely important for candidates to discuss, compared to one in ten (11%) non-MAGA-supporting Republicans and Republican-leaning independents who say the same. About two-thirds of MAGA Republicans identify as pro-life (63%), while about four in ten (44%) non-MAGA supporting Republicans identify as pro-choice.

The Democratic Party has the advantage over Republicans when it comes to which political party voters trust more on the issue of abortion (39% vs. 28%, respectively), though nearly three in ten (27%) voters say they trust neither party on this issue. Women voters ages 18 to 49 and younger voters (ages 18 to 29) are notably among the most likely to trust the Democratic Party more (46% and 52%, respectively).

Unsurprisingly, voters are largely split across partisan identification when it comes to which political party they trust more on the issue of abortion. Among independent voters, the Democratic Party has the edge over the Republican Party (35% vs. 19%), though four in ten (41%) say they trust neither party on the issue.

Methodology

This KFF Health Tracking Poll/KFF Tracking Poll on Health Information and Trust was designed and analyzed by public opinion researchers at KFF. The survey was conducted June 25 – June 30, 2026, online and by telephone among a nationally representative sample of 1,321 U.S. adults in English (n=1,238) and in Spanish (n=83). The sample includes 1,015 adults (n=69 in Spanish) reached through the SSRS Opinion Panel either online (n=990) or over the phone (n=25). The SSRS Opinion Panel is a nationally representative probability-based panel where panel members are recruited randomly in one of two ways: (a) Through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS) provided by Marketing Systems Groups (MSG) through the U.S. Postal Service’s Computerized Delivery Sequence (CDS); (b) from a dual-frame random digit dial (RDD) sample provided by MSG. For the online panel component, invitations were sent to panel members by email followed by up to three reminder emails.

Another 306 (n=14 in Spanish) adults were reached through random digit dial telephone sample of prepaid cell phone numbers obtained through MSG. Phone numbers used for the prepaid cell phone component were randomly generated from a cell phone sampling frame with disproportionate stratification aimed at reaching Hispanic and non-Hispanic Black respondents. Stratification was based on incidence of the race/ethnicity groups within each frame. Among this prepaid cell phone component, 142 were interviewed by phone and 164 were invited to the web survey via short message service (SMS).

Respondents in the prepaid cell phone sample who were interviewed by phone received a $15 incentive via a check received by mail or an electronic gift card incentive. Respondents in the prepaid cell phone sample reached via SMS received a $10 electronic gift card incentive. SSRS Opinion Panel respondents received a $5 electronic gift card incentive (some harder-to-reach groups received a $10 electronic gift card). In order to ensure data quality, cases were removed if they failed two or more quality checks: (1) attention check questions in the online version of the questionnaire, (2) had over 30% item non-response, or (3) had a length less than one quarter of the mean length by mode. Based on this criterion, 1 case was removed.

The combined cell phone and panel samples were weighted to match the sample’s demographics to the national U.S. adult population using data from the Census Bureau’s 2025 Current Population Survey (CPS), September 2023 Volunteering and Civic Life Supplement data from the CPS, and the 2026 KFF Benchmarking Survey with ABS and prepaid cell phone samples. The demographic variables included in weighting for the general population sample are gender, age, education, race/ethnicity, region, civic engagement, frequency of internet use and political party identification. The weights account for differences in the probability of selection for each sample type (prepaid cell phone and panel). This includes adjustment for the sample design and geographic stratification of the cell phone sample, within household probability of selection, and the design of the panel-recruitment procedure.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available on request. Sampling error is only one of many potential sources of error and there may be other unmeasured error in this or any other public opinion poll. KFF public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

The recently proposed 2027 Medicare Hospital Outpatient Perspective Payment System (OPPS) rule from the Centers for Medicare & Medicaid Services (CMS) includes a proposal to reduce Medicare’s reimbursement for 340B drugs. The proposal would reduce reimbursement for 340B drugs from average sales price (ASP) plus 6% (what Medicare generally pays for Part B outpatient drugs administered by providers) to ASP minus 33.4%, a 37% reduction. CMS indicated that this change would better align Medicare reimbursement with hospitals’ costs of acquiring 340B drugs.

The 340B Drug Pricing Program requires drug manufacturers participating in Medicaid to sell outpatient drugs to eligible nonprofit and government providers at a substantial discount, allowing providers to earn larger profits when being reimbursed for 340B drugs. The intent of the program is to support providers, such as certain disproportionate share hospitals and federally qualified health clinics, that care for low-income and other underserved populations. Critics have raised concerns that the 340B program, which has grown substantially over time, is not well-targeted; that savings from the program are not shared with patients; and that the program incentivizes hospitals to acquire clinics and physician practices in order to extend 340B discounts to those settings, enabling them to generate more revenue. Supporters of the program say that revenues generated by the difference between Medicare (and other payer) reimbursement for 340B drugs and the discounted price help 340B providers care for underserved populations and invest in operations.

CMS based the amount of the proposed payment reduction on a cost acquisition survey of 340B drugs completed by hospitals in early 2026. This proposed change revives an earlier effort by CMS to reduce Medicare payments for 340B drugs that was implemented in 2018 under the first Trump administration, but the Supreme Court overturned that rule in 2022 because the agency had not first conducted a cost acquisition survey. If finalized, CMS’s proposed Medicare 340B payment reduction would take effect on January 1, 2027, and would have disparate effects on different types of hospitals, as described more below.

CMS’s proposed cut to 340B drug reimbursement would reduce Medicare spending on 340B drugs by an estimated $4.85 billion in 2027, while increasing spending on non-drug outpatient services by the same amount because of budget neutrality requirements. Under federal law, CMS is generally required to maintain the same amount of aggregate spending through OPPS regardless of reimbursement changes (i.e., maintain budget neutrality). Based on this requirement, CMS proposed an 8.44% across-the-board increase in payments for non-drug outpatient services covered under the OPPS, which the agency estimates will offset the impact of cuts to spending on 340B drugs in 2027.

The budget neutrality requirement means that savings from reductions in 340B payments to 340B hospitals would be redistributed to both 340B and non-340B hospitals through higher payments for non-drug outpatient services. Similarly, Medicare beneficiaries would face lower cost sharing on 340B drugs (e.g., based on 20% coinsurance applied to a lower amount) but higher cost sharing for non-drug outpatient hospital services. CMS estimates that Medicare beneficiaries who use 340B drugs would save $1.15 billion in total in 2027, but cost sharing would increase for beneficiaries who use non-drug outpatient hospital services based on Medicare’s proposed 8.44% payment increase.

Proposed cuts would reduce revenues among safety-net hospitals while increasing revenues among for-profit hospitals, among other differences. For 340B hospitals, total Medicare revenues would decrease or increase depending on how reliant they are on revenues from 340B drugs versus non-drug outpatient services, but non-340B hospitals would experience revenue increases only based on the higher payment rate for non-drug outpatient services. CMS’s proposal to reduce reimbursement for 340B drugs would exempt rural sole community hospitals (SCHs) (rural hospitals that are the only source of short-term, acute inpatient care in a region), children’s hospitals, and PPS-exempt cancer hospitals. Changes would not affect hospitals that are not reimbursed under the OPPS, including critical access hospitals (CAHs), which make up the majority of rural hospitals.

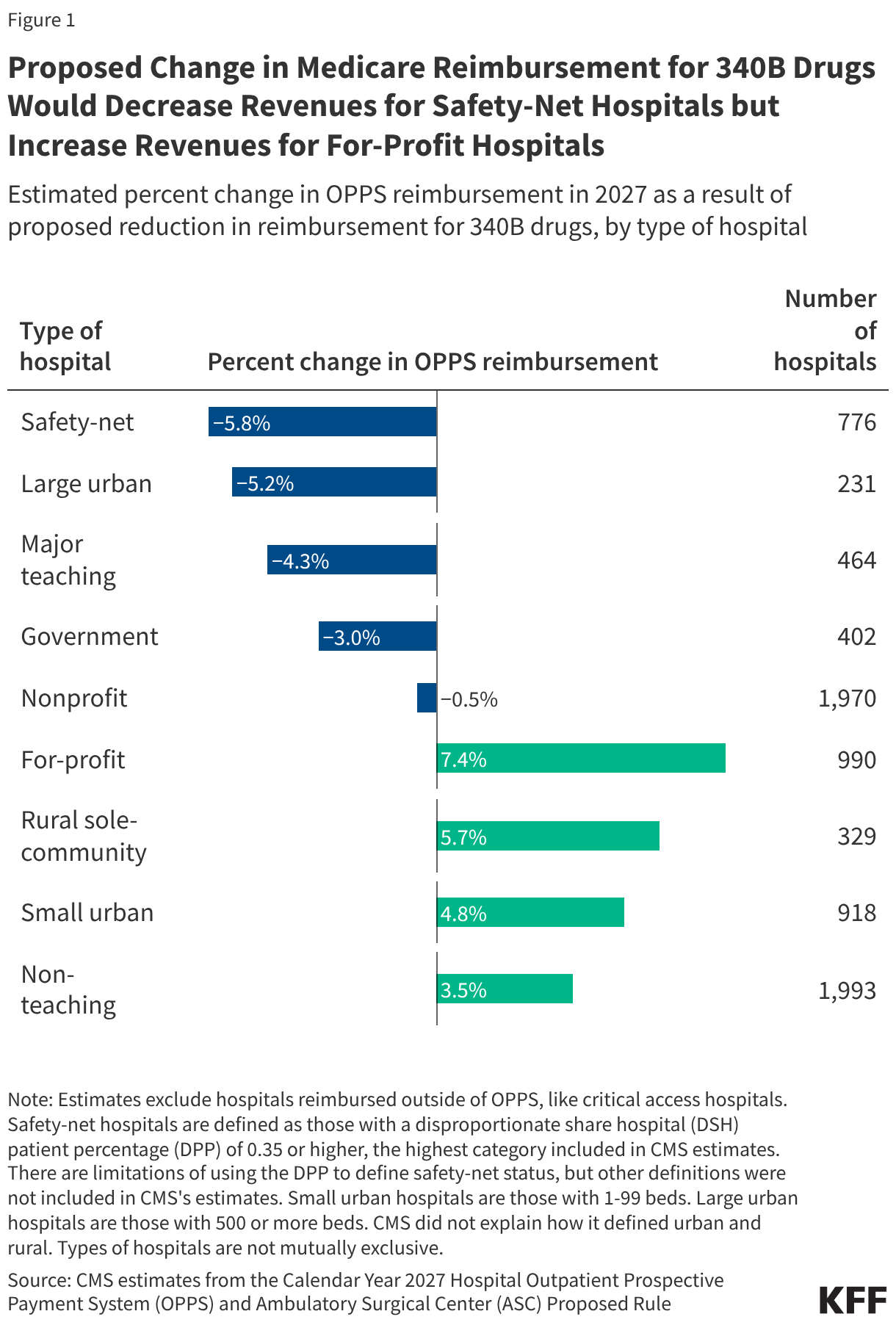

In the aggregate, some types of hospitals would lose or benefit more from these changes than others, based on estimates from CMS (Figure 1):

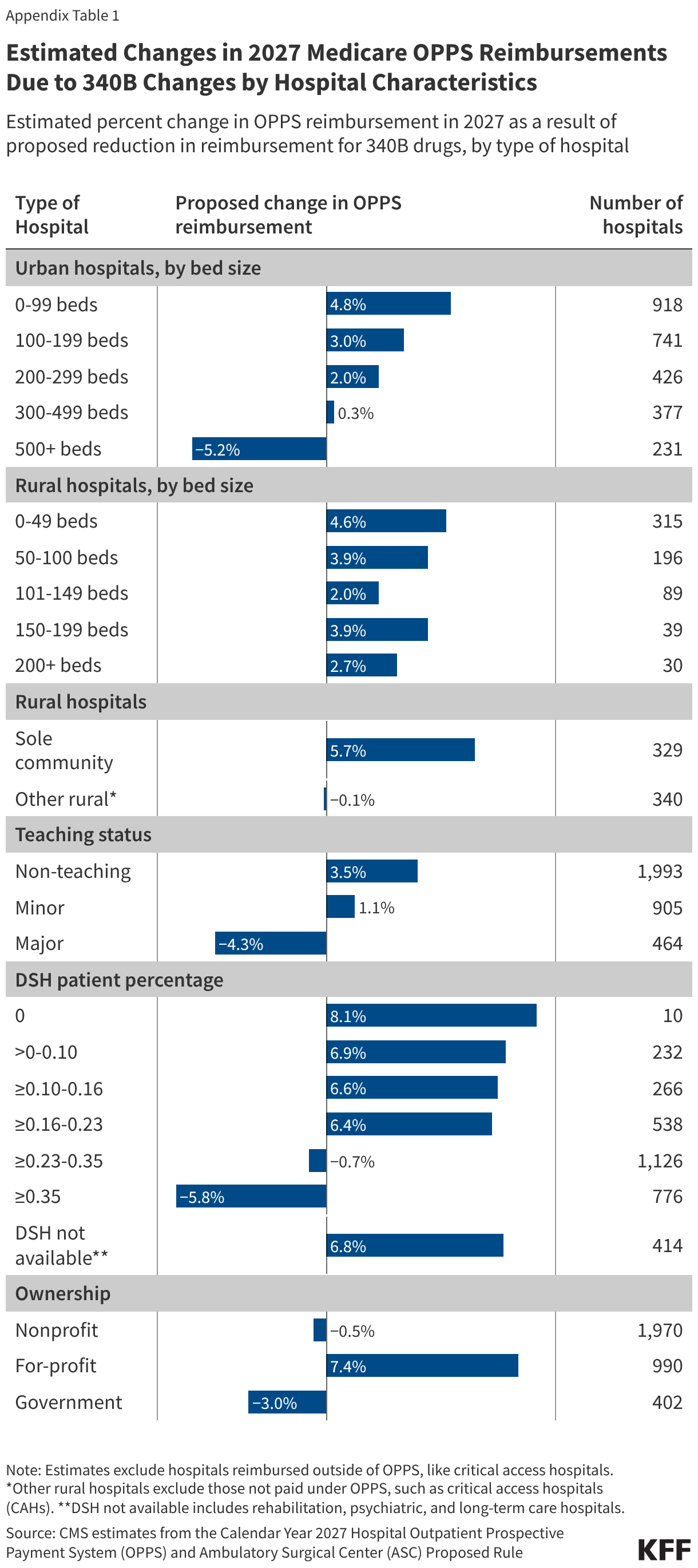

Safety-net hospitals would face a 5.8% net reduction of OPPS revenue under this proposal (see figure notes for definition of “safety-net hospitals”). Other types of hospitals would also see net reductions in OPPS revenue in the aggregate, including large urban hospitals (with 500 beds or more) (-5.2%), major teaching hospitals (-4.3%), government hospitals (-3.0%), and nonprofit hospitals (-0.5%). Some hospitals that would see the largest decrease in revenue likely fall into more than one of these categories (e.g., major teaching hospitals tend to be large urban hospitals).

For-profit hospitals would see a 7.4% net increase in OPPS revenues. For-profit hospitals are not eligible for the 340B program and so would only see increases in reimbursement for non-drug outpatient services. Other types of hospitals would also face net increases in Medicare OPPS reimbursement in aggregate, including rural SCHs (5.7%), small urban hospitals (with 0 to 99 beds) (4.8%), and non-teaching hospitals (3.5%).

Reductions in 340B payments could add to the financial challenges facing safety-net hospitals while increasing margins of for-profit hospitals. Safety-net hospitals havelower operating margins than average and so could have an especially difficult time absorbing any revenue losses from the 340B payment cut, while for-profit hospitals have muchhigher operating margins than the average hospital. Additionally, safety-net hospitals, which are particularly dependent on Medicaid revenues, are likely to be disproportionately affected by the 2025 reconciliation law, as it achieves most of its health care savings through federal Medicaid spending reductions.

The substantial growth of the 340B program in recent years has led hospitals, pharmaceutical companies, and policymakers to focus on whether and how to change the program. At the federal level, lawmakers haveproposedoptions that would preserve or narrow the scope of the program and have proposed increasing transparency around the program, such as by requiring hospitals to report 340B savings. At the state level, some states have passed laws that would preserve the ability of hospitals to use multiple contract pharmacies to dispense 340B drugs, among other things. Other states have implemented requirements for hospitals to disclose the amount of savings generated from the 340B program (as required by Minnesota) or how those savings are spent.

Some pharmaceutical companies have attempted to start providing 340B drug discounts through a rebate model, an approach that would require hospitals to purchase 340B drugs at a non-discounted price and receive post-sale rebates after submitting claims information. These efforts have been halted by the courts due to lack of authorization from HHS, the agency that administers the 340B program. In 2025, the Trump administration attempted to implement the 340B Rebate Model Pilot Program, but a court halted the pilot after a lawsuit was filed by the hospital industry. HHS has recently requested information from stakeholders on a revised rebate model pilot.

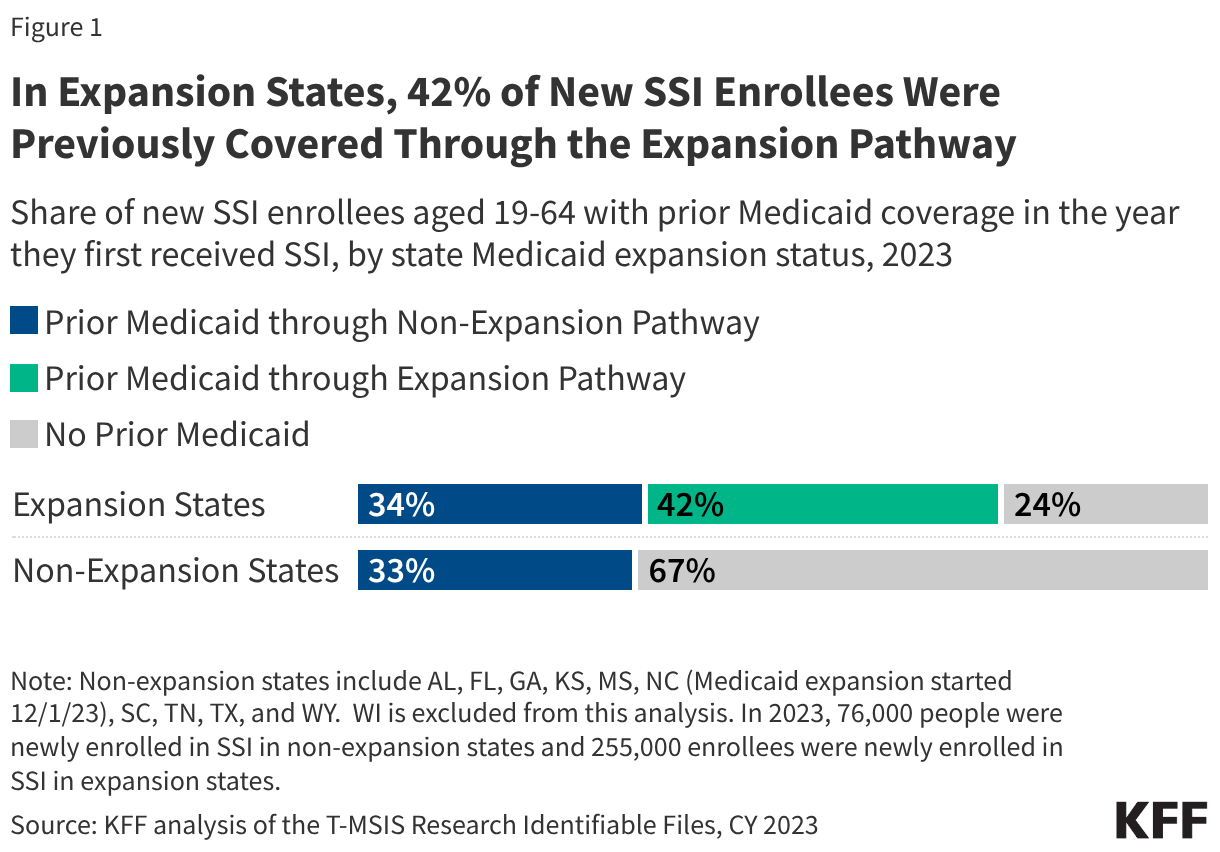

The 2025 reconciliation law requires 44 states to condition Medicaid eligibility for adults in the Affordable Care Act (ACA) Medicaid expansion group and enrollees in certain waiver programs, on meeting work requirements starting January 1, 2027, or sooner at state option. While the law specifies mandatory exclusions, including for individuals who are “medically frail,” the approach to determining medical frailty specified in the June 2026 interim final rule could make it difficult for some people to qualify for this exclusion. Medicaid expansion provides coverage to many adults with significant health care needs, including some with disabilities who are applying for the Supplemental Security Income Program (SSI). This coverage could be at risk for some because of the planned approach to defining medical frailty.

SSI is a means-tested federal program administered by the Social Security Administration (SSA) that pays monthly cash assistance to people with limited resources who are unable to work because of a disability and generally qualifies people to receive health coverage through Medicaid. Once approved for SSI, Medicaid enrollees would not be subject to work requirements, but the application for SSI can be a lengthy and complicated process, spanning months, if not years, during which time applicants may be at risk of uninsurance because they are unable to work. Medicaid can fill coverage gaps during the SSI application period, particularly in states that have adopted the Medicaid expansion.

This issue brief finds that the percent of new SSI enrollees ages 19 through 64 with Medicaid prior to SSI entitlement is twice as high in ACA expansion states as it is in non-expansion states, and in 2023, over 100,000 new SSI enrollees had ACA Medicaid coverage prior to their SSI entitlement. It also describes the lengthy SSA process for determining SSI eligibility, particularly assessing ability to work, and how the current approach to determining medical frailty could cause some SSI applicants to undergo concurrent assessments of their ability to work using different processes and criteria. The new documentation requirements and processes could cause some people with disabilities to lose Medicaid coverage or be denied Medicaid enrollment while they are waiting on their SSI determination.

How does Medicaid provide coverage for people during the SSI application process?

Medicaid provides coverage for many people with disabilities, including those who are applying for SSI.One in five Medicaid enrollees have a disability, including 43% of adults ages 50-64, but only one-third of these individuals receive SSI income, generally qualifying for Medicaid for that reason. The remaining people with disabilities are covered through different Medicaid eligibility pathways, including the ACA Medicaid expansion. Because of the lengthy process for obtaining an SSI determination and the fact that people who are applying for SSI are unable to work, many people applying for SSI rely on Medicaid to avoid going uninsured.

In 2023, 223,000 SSI applicants ages 19 through 64 had Medicaid while they were waiting for an SSI determination, including over 106,000 with coverage through the ACA expansion. KFF analyzed detailed Medicaid administrative data to identify people who were ages 19 through 64 and became eligible for Medicaid because of SSI during the calendar year 2023 and whether those enrollees had Medicaid coverage in the months prior to their SSI-based eligibility (see Methods). Among the 337,000 people who started SSI during the calendar year, over 200,000 had prior Medicaid coverage through a different eligibility pathway, with roughly half receiving that coverage through the ACA expansion.

In ACA expansion states, 76% of new SSI enrollees ages 19 through 64 had Medicaid coverage through a different eligibility pathway prior to their disability determination (including 42% who were covered through the Medicaid expansion) compared with only 33% in non-expansion states (Figure 1). In both expansion and non-expansion states, roughly 1 in 3 new SSI enrollees ages 19 through 64 were enrolled in non-ACA Medicaid coverage (such as coverage for parents and caretakers) prior to becoming eligible for SSI. However, in expansion states, an additional 42% of new SSI enrollees were enrolled in Medicaid through the expansion, covering over 100,000 people in 2023. New SSI enrollees who were not covered by Medicaid prior to their SSI approval were likely uninsured because of their low income and inability to work.

How do people demonstrate eligibility for SSI?

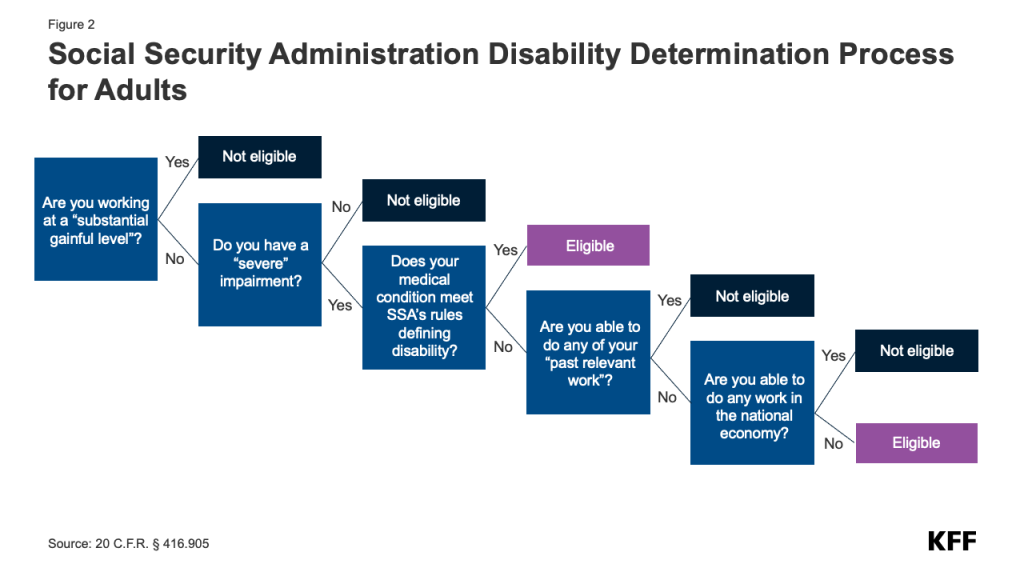

To be eligible for SSI, people must have limited income (defined as no more than $2,073 per month in 2026), limited resources (defined as no more than $2,000 for an individual or $3,000 for a couple), and a disability that affects their ability to work for at least a year or result in death or be age 65 and older.

For applicants under age 65, demonstrating a disability is often the most complicated part of the SSI application process, involving a lengthy five-step process that starts by proving one is not gainfully employed (Figure 2). The federal government establishes verification processes that all states must use to determine applicants’ disability status, and funds state Disability Determination Services (DDS) offices to carry out these processes. The same processes are used for SSI and for Social Security Disability Insurance. Illustrating the high costs of this lengthy process, the Social Security Administration provided states with $2.6 billion in Fiscal Year (FY) 2025 to run the DDS offices. The first step requires people to demonstrate that their current earnings are below the threshold of “substantial gainful activity” (SGA, $1,690 per month in 2026).

The second step assesses whether applicants have a severe impairment, where impairment is defined based on which body system is affected. For adults, impairments are classified into the following categories with associated medical criteria: musculoskeletal disorders, special senses and speech, respiratory disorders, cardiovascular system, digestive disorders, genitourinary disorders, hematological disorders, skin disorders, endocrine disorders, congenital disorders that affect multiple body systems, neurological disorders, mental disorders, cancer, and immune system disorders.

The third step assesses whether the impairment qualifies as a disability that wouldn’t require further demonstration of an inability to work using established criteria for disabilities. Some impairments allow applicants to qualify for SSI without further demonstrating an inability to work, including blindness and several hundred specific disorders or conditions included in the “compassionate allowance program,” which quickly identifies diseases and other conditions that meet SSA’s standards for disability benefits. Examples of such conditions include Amyotrophic Lateral Sclerosis (ALS), certain cancers, and Duchenne Muscular Dystrophy. SSA reports that between 2008 and 2025, the agency approved more than 1 million people (for SSI and Social Security Disability Insurance combined) through the compassionate allowance program.

The final two steps respectively assess peoples’ ability to engage in “past relevant work” or any job in the national economy that is feasible considering the applicant’s residual functional capacity, age, education, and work experience. The SSA makes this assessment based on information provided in Form 3368 which requires people to provide personal information including their English language proficiency, current work activity, job history over the last 15 years, the claimed disability onset date, list of medical conditions, prescription list, and medical treatment history. Medical records from providers can be submitted with the application. Along with this form, the SSA will request any missing medical records and may request that the person have a consultative medical examination by an SSA medical consult. SSA also compares information about people’s jobs from the past 5 years (such as job title and pay; tasks performed; tools, machinery, and equipment used; knowledge, skills, and ability required; physical demands; and environmental conditions) with tables of rules about the requirements for jobs in the national economy.

Assessing ability to engage in any job requires information about all jobs in the economy, which can be difficult to implement in practice, and SSA is currently relying on outdated job information. SSA’s current jobs listing comes from the Department of Labor’s Dictionary of Occupational Titles which was last updated in 1991 and is not currently used by the Department of Labor. Since FY 2021, SSA has partnered with the Department of Labor to develop a survey that will be the main source of updated occupational information, but that new system has not yet been implemented. Congressional Research Services reports that between FYs 2012 and 2024, SSA spent $300 million on this project.

The application for disability benefits can be a lengthy and complicated process, spanning months, if not years, meaning hundreds of thousands of people are currently waiting for determinations. As of May 2026, the initial processing time for all disability applications was 184 days—over 6 months—and roughly 862,000 people were waiting for their initial determinations. (This number includes applications for SSI and applications for Social Security Disability Insurance, a related program that uses the same disability determination process.) Many people receive initially unfavorable decisions and choose to appeal, which can considerably lengthen the process. Having a lawyer increases the likelihood of being approved at the initial stage and, on average, can reduce the time it takes to reach a final decision by nearly one year.

How might work requirements affect Medicaid coverage for people during the SSI application process?

Starting in January 2027, individuals applying for or enrolled in coverage through the ACA expansion and in certain waiver programs will be required to work or engage in qualifying activities, such as volunteer community service, for 80 or more hours per month, attend school half-time, unless they qualify for an exemption or exclusion from the requirements. SSI applicants enrolled in the ACA expansion will be subject to these new requirements. Applicants who meet the SSI criteria do not have to meet the community engagement requirements, but there may be challenges for them in proving their eligibility for the medical frailty exclusion while they are applying for SSI.

People applying for SSI are generally unable to work, but current rules could make it challenging for them to qualify for a medical frailty exclusion. Because individuals must have earnings below the SGA level to be eligible for SSI, they are unlikely to be able to work 80 or more hours in a month. Additionally, most people with new impairments significant enough to qualify for SSI will likely also face challenges meeting the Medicaid community engagement requirements through education or volunteering. Instead, to obtain or retain Medicaid, individuals applying for SSI who are subject to the work requirements will need to qualify for an exclusion from the requirements, most likely through the medical frailty exclusion. The interim final rule implementing Medicaid work requirements issued on June 1, 2026, adopts a restrictive definition of medical frailty that requires individuals to have a physical or mental health condition that impairs their ability to meet community engagement requirements. This two-part test for medical frailty will require navigating a verification process that may lead to people losing coverage because they cannot provide the required documentation, even though they qualify for the exclusion.

Different requirements for Medicaid eligibility determinations mean SSI applicants covered through the Medicaid expansion could face two concurrent assessments of their ability to work: one for SSI and one for Medicaid. Medicaid eligibility determinations of whether an individual meets the medical frailty exclusion will need to be done on a faster timeline than SSI determinations. States are required to process Medicaid applications for individuals who qualify based on income within 45 days, and starting January 1, 2027, they must conduct renewals for individuals enrolled through the Medicaid expansion every six months instead of annually. That makes it likely that many SSI applicants will not have a disability determination before they have an assessment of their ability to work to meet the medical frailty exclusion from Medicaid work requirements. These new requirements could place additional administrative burdens on individuals who are experiencing significant physical or mental health challenges and could cause people to lose health insurance while they wait for an SSA disability determination.

In contrast to the SSI determination process, the Medicaid interim final rule is not clear on how states should determine ability to work in the context of Medicaid work requirements, which will lead states to adopt different approaches that could put coverage at risk for some SSI applicants. The rule requires states to automate, to the extent possible, verification of the Medicaid medical frailty exclusion using claims and encounter data before requesting information from the individual. However, claims data alone will often be insufficient to assess whether a condition impairs the ability to work or engage in community service, and claims data do not include information about people’s ability to engage in the activities of daily living (one measure of disability) or their overall functional status and frailty. Given the broader Medicaid definition of community engagement activities, states will need to assess people’s ability to participate in education or volunteer activities in addition to doing any work in the national economy. The lack of information about minimum acceptable practices raises questions about what standards states will use to assess ability to work, and what types of documentation will be sufficient to prove the inability to comply with the requirements. As they develop processes for verifying medical frailty, states will rely more heavily on provider determinations or other documentation and self-attestation, to the extent permitted by the rule, for individuals who cannot be automatically verified. Self-attestation will be permitted in 2027 and once for each individual in 2028. Absent clearer guidance, the approaches states develop will differ. This variability coupled with enhanced documentation requirements could cause some people with disabilities to lose Medicaid coverage or be denied Medicaid while they are waiting on their SSI determination.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

Data: Data are from the 2023 Transformed Medicaid Statistical Information System (T-MSIS) Analytic Files (TAF) Research Identifiable Files (RIF) files.

State inclusion criteria: National estimates include enrollees living in 49 states and DC and exclude residents in the U.S. territories. Non-expansion states include AL, FL, GA, KS, MS, NC (Medicaid expansion started 12/1/23), SC, TN, TX, and WY. WI is excluded from this analysis because it has an 1115 waiver that offers coverage similar to the ACA expansion. The pre-SSI Medicaid coverage rates look much more similar to those of an ACA expansion state, but the T-MSIS data do not clearly identify people enrolled in the 1115 coverage.

Identifying new SSI enrollees using Medicaid administrative data: Enrollees are classified as new SSI enrollees if their latest eligibility group in the year is SSI (having ELGBLTY_GRP_CD_LTST with value of 11-22, 37, 38, 40, or 41) but in January, they are either not enrolled in Medicaid or they are enrolled through some other pathway (ELGBLTY_GRP_CD_01 not having value of 11-22, 37, 38, 40, or 41). The analysis is limited to enrollees ages 19 through 64 who are in Medicaid only (and not CHIP) during the year.

Assessing prior Medicaid coverage in the year for new SSI enrollees: Monthly eligibility group codes (ELGBLTY_GRP_CD_01-ELGBLTY_GRP_CD_12) are used to determine the first month of SSI enrollment (first monthly eligibility group code with value of 11-22, 37, 38, 40, or 41). Then, all monthly eligibility group codes prior to the first month of SSI enrollment are used to assess prior Medicaid enrollment during the year as follows:

Prior Medicaid coverage through the expansion pathway: having at least one monthly eligibility group code indicating enrollment through the ACA expansion group (value of 72, 73, 74, or 75) before the first month of SSI enrollment.

Prior Medicaid coverage through non-expansion pathway: having at least one non-missing monthly eligibility group code and no monthly eligibility group codes indicating enrollment through the ACA expansion group (value of 72, 73, 74, or 75) before the first month of SSI enrollment.

No prior Medicaid coverage: eligibility group codes for all months before the first month of SSI enrollment are missing.

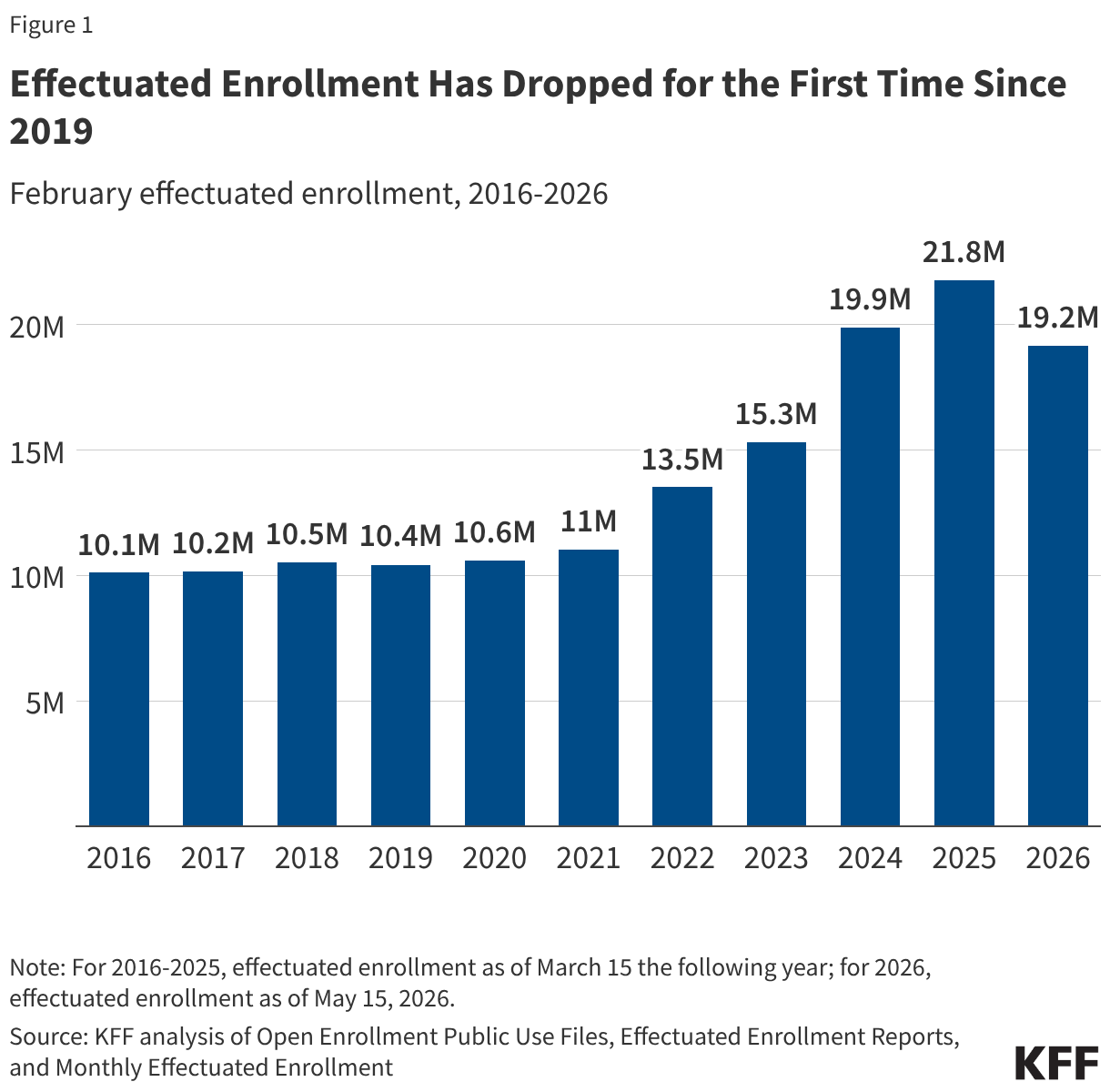

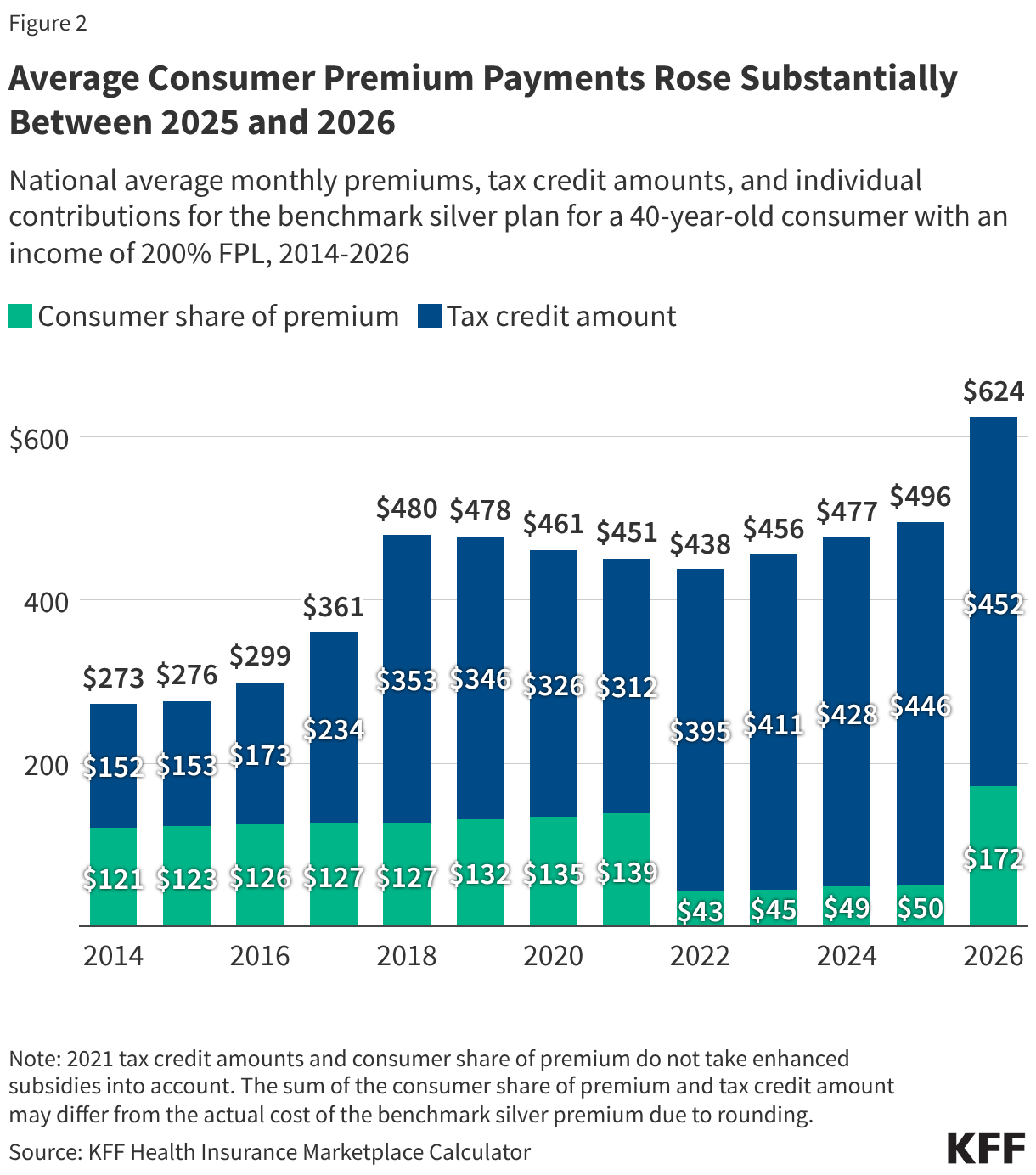

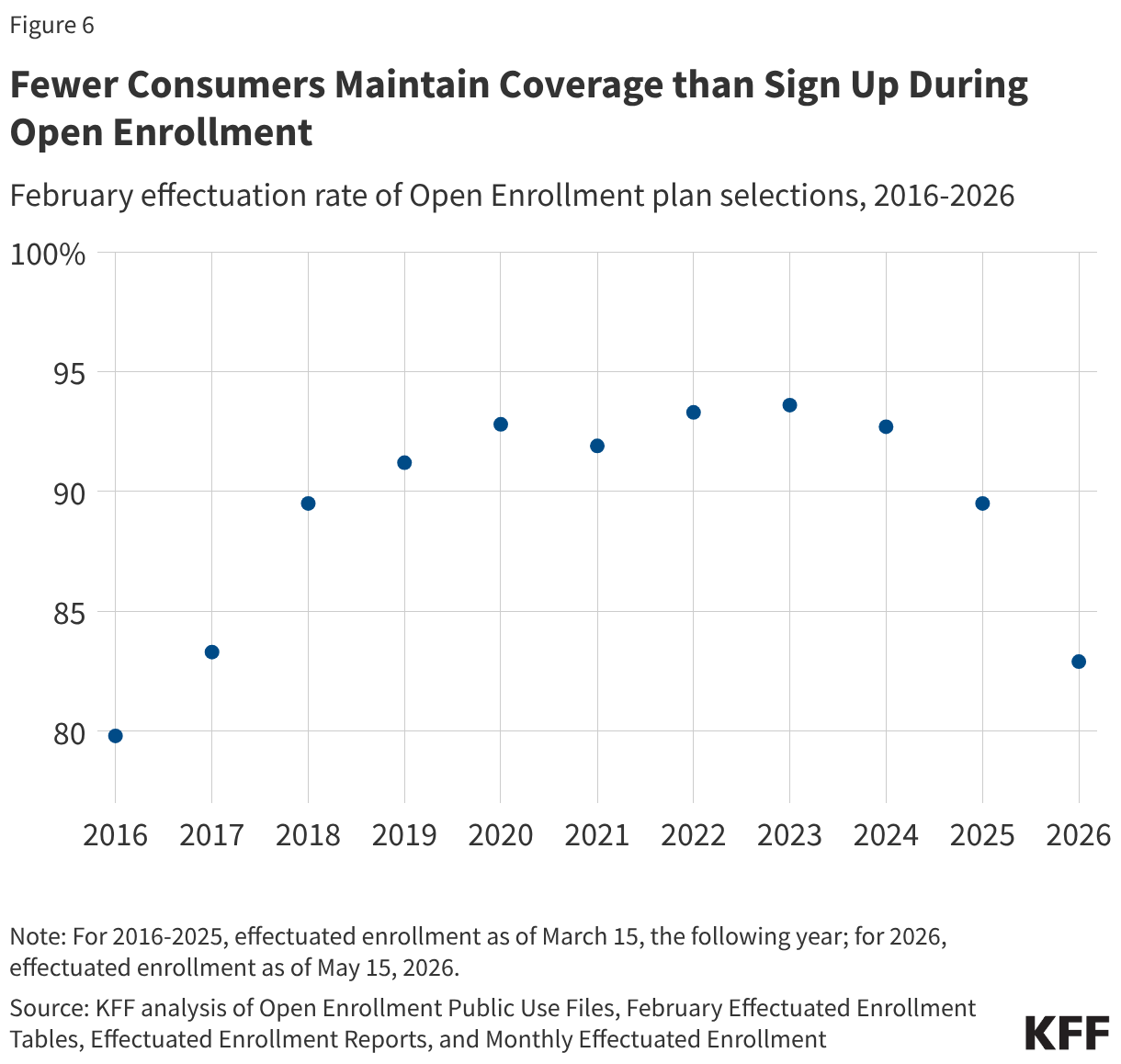

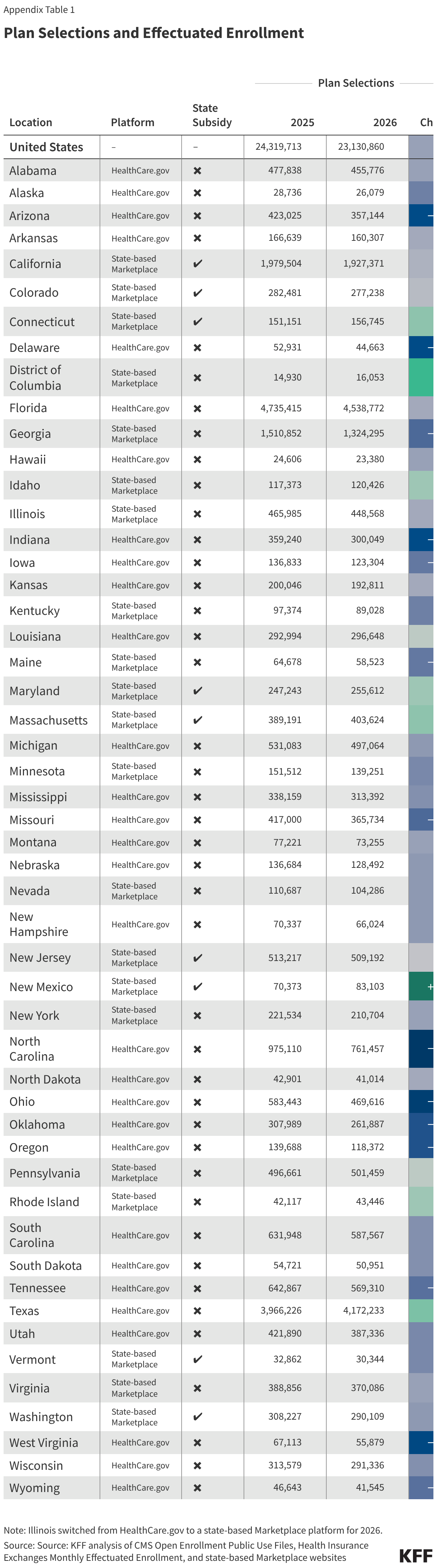

Following several years of rapid enrollment growth in the Affordable Care Act (ACA) Marketplaces that corresponded with temporary enhanced premium tax credits, enrollment fell for the first time in seven years in 2026, when those tax credits expired. The Assistant Secretary for Planning and Evaluation (ASPE) of the Department of Health and Human Services reported that enrollment declined by nearly three million people between 2025 and 2026.

Earlier federal data and analysis had focused on plan selections, or sign-ups, which decreased by about one million (5%) from last year, but plan selections do not account for enrollees who ultimately do not make their premium payments and are not covered. Effectuated enrollment is different from selection or sign-up data in that it accounts for who paid their premiums. Consumers who canceled their coverage or did not make their premium payments, resulting in termination of coverage, do not contribute to effectuated enrollment totals.

This analysis uses data from the Centers for Medicare and Medicaid Services (CMS) on effectuated enrollment in addition to Open Enrollment plan selections to examine how enrollment in the ACA Marketplaces has changed in 2026.

Key Findings

Every state except for New Mexico saw a drop in ACA Marketplace enrollment from 2025 to 2026. New Mexico is the only state to fully replace the expired federal enhanced premiums tax credits with state-funded subsidies.

State-based Marketplaces that run their own enrollment platforms, including those that partially offset the expiring federal enhanced tax credits, generally saw lower drops in enrollment (a 6% decline versus a 15% decline for states that use the federal marketplace).

The effectuation rate (the rate at which people who initially signed up for a plan kept their coverage by making their premium payments) was lower in 2026 than in recent years.

States that run their own Marketplaces, and particularly those that offered state-funded subsidies, generally saw higher-than-average effectuation rates.