Key Facts About Medicare Beneficiaries in Rural Areas

Over the years, policymakers have expressed ongoing concern about barriers to medical care in rural areas, due to workforce shortages, long travel times to medical facilities, and rural hospital closures. For the more than 10 million people with Medicare who live in rural areas, both older adults and younger beneficiaries with permanent disabilities, these issues may pose particular challenges to the extent they are more likely than other people to have medical conditions that require frequent visits to health care providers. Compounding existing challenges to the delivery of health care in rural areas, current proposals by the GOP-led Congress to cut billions in Medicaid spending and discontinue enhanced subsidies for Marketplace coverage could impact the financial stability of rural hospitals and other health care providers, which could heighten concerns about access to care for rural residents, including millions of people with Medicare.

Over the years, federal and state lawmakers have taken steps to improve rural health care for Medicare beneficiaries, including support for Rural Health Clinics (RHCs), preservation of rural hospitals at risk of closure under the Rural Emergency Hospital (REH) and Critical Access Hospital (CAH) programs, and increased training opportunities for medical residents at sites that serve rural communities. Additionally, the House-passed 2025 reconciliation bill proposes to expand the definition of a rural emergency hospital under the Medicare program. However, the Trump administration is proposing $1 billion in cuts to HRSA’s Health Workforce Programs, which support training for providers in rural and underserved areas, as part of the President’s FY 2026 budget. While budget decisions ultimately rest with Congress, these proposed changes could also affect the health care of people living in rural communities.

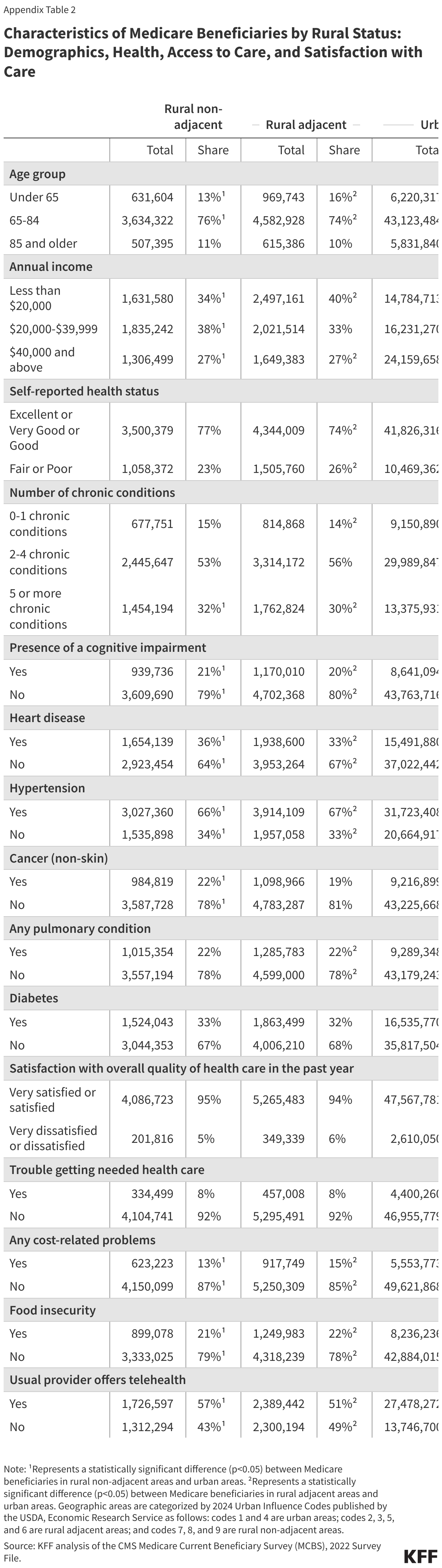

To help inform current policy discussions, this brief analyzes various data sources to highlight key facts about Medicare beneficiaries living in rural areas, including their demographic and health characteristics, access to care, and satisfaction with care. The analysis compares Medicare beneficiaries living in rural areas, including those that are not adjacent to any urban areas (referred to as the “most rural areas”) and those that are adjacent to an urban area (“rural adjacent areas”), and urban areas (see Methods for further details). More than 10 million Medicare beneficiaries lived in rural areas in 2024, 3.4 million of whom were in the most rural areas.

Key Takeaways

- A larger share of Medicare beneficiaries living in the most rural areas than beneficiaries living in urban areas had annual incomes of less than $20,000 per person in 2022 (34% vs. 27%).

- Rural Medicare beneficiaries are more likely to also be enrolled in Medicaid than those in urban areas (23% and 18% respectively).

- About one-third (32%) of Medicare beneficiaries living in the most rural areas had 5 or more chronic health conditions, as compared to 25% of beneficiaries living in urban areas.

- The majority (58%) of Medicare beneficiaries living in the most rural areas are covered by traditional Medicare instead of Medicare Advantage, while in rural adjacent and urban counties, traditional Medicare is less common (48% and 44%, respectively).

- While more than 9 in 10 Medicare beneficiaries living in the most rural areas were satisfied with the quality of their medical care and fewer than 1 in 10 reported trouble getting needed care, larger shares reported food insecurity (21%) and health care cost-related problems (13%) than beneficiaries in urban areas (16% and 10%, respectively).

- A smaller share of Medicare beneficiaries living in the most rural areas reported that their usual provider offers telehealth services than beneficiaries in urban areas (57% vs.67%).

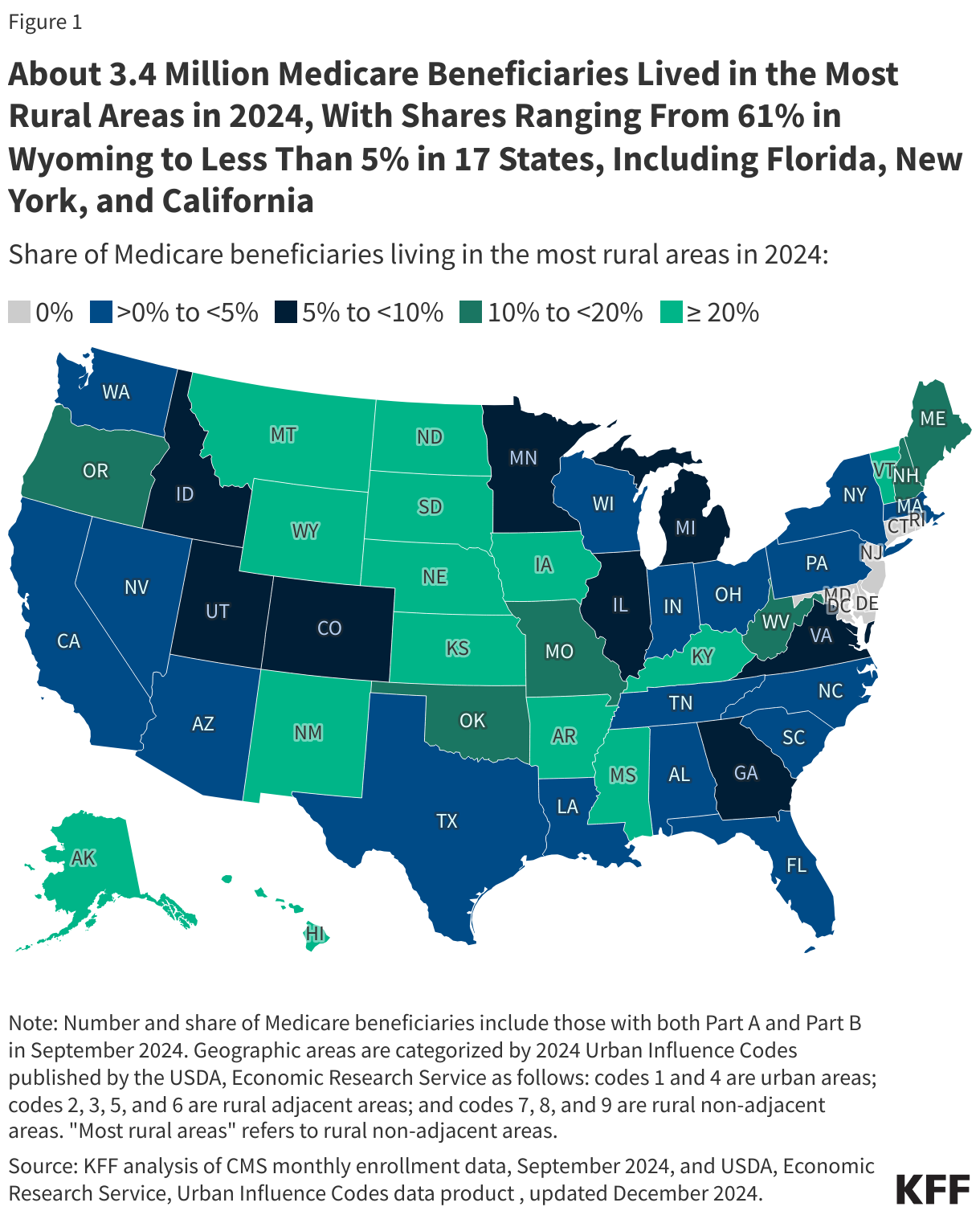

More than 10 million Medicare beneficiaries live in rural areas, including 3.4 million who live in the most rural areas

Among the 61 million Medicare beneficiaries with both Parts A and B in 2024, 3.4 million, or 6%, lived in the most rural areas of the country (Figure 1). Another 7.3 million lived in rural adjacent areas and 50.4 million lived in urban areas. The share of Medicare beneficiaries living in the most rural areas varied across states, ranging from 61% in Wyoming to less than 5% in 17 states, including Florida, New York, and California (Figure 1, Appendix Table 1).

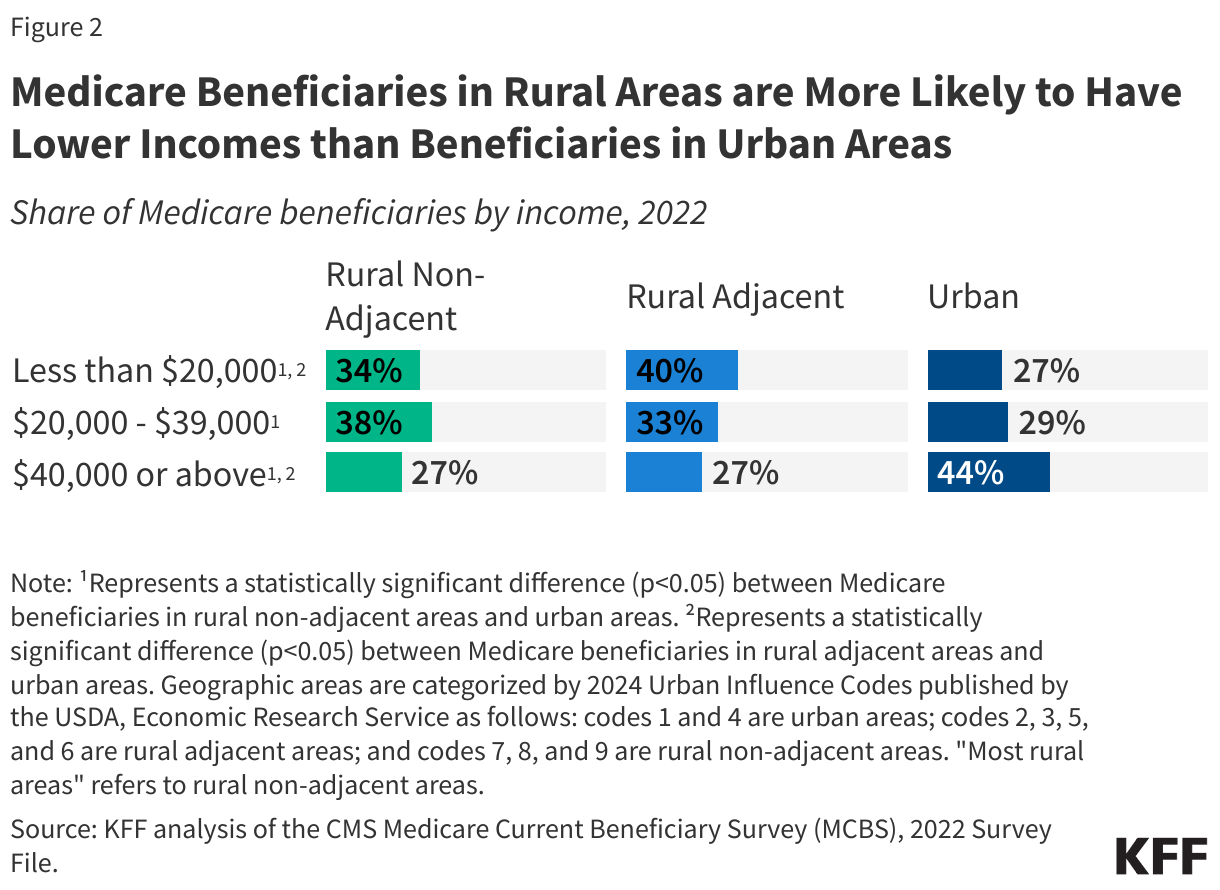

Medicare beneficiaries in the most rural areas are more likely to have lower incomes than beneficiaries in urban areas

More than one-third of Medicare beneficiaries living in the most rural areas had annual incomes of less than $20,000 per person in 2022 (34% vs. 27% in urban areas) (Figure 2). Likewise, nearly three-quarters of beneficiaries living in the most rural areas had annual incomes of less than $40,000 per person (72% vs. 56% in urban areas). Having a relatively low income can pose a barrier to access to care for Medicare beneficiaries who may need to pay for costly or unanticipated medical care, as well as services not covered by Medicare, including dental services and long-term services and supports.

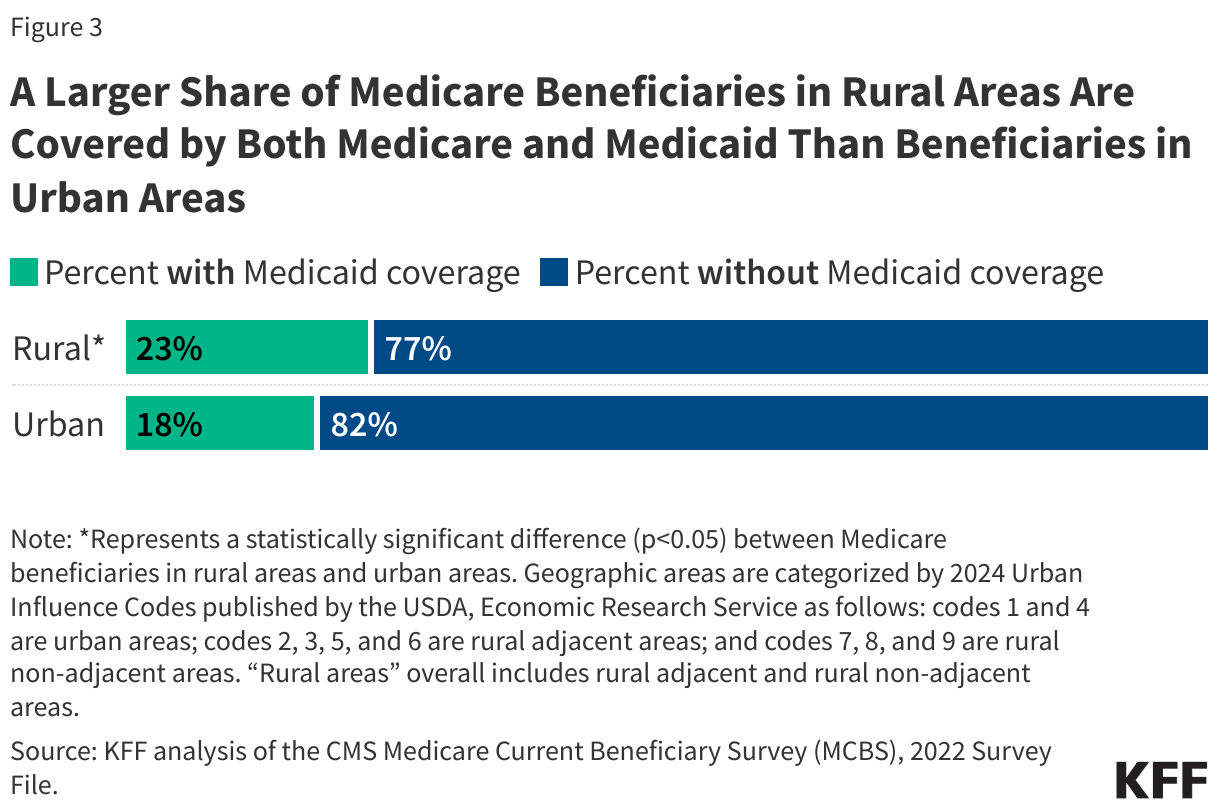

Medicare beneficiaries living in rural areas are more likely to rely on Medicaid than beneficiaries in urban areas

In 2022, a larger share (23%) of Medicare beneficiaries living in rural areas (including the most rural counties and rural adjacent counties) also had Medicaid coverage (i.e., “dual-eligible individuals”) than beneficiaries in urban areas (18%) (Figure 3). For these individuals, Medicare is their primary source of health insurance coverage, and Medicaid wraps around their Medicare coverage by paying Medicare premiums, and in most cases, cost sharing. Many dual-eligible individuals also have Medicaid coverage of benefits not covered by Medicare, including long-term services and supports. Dual-eligible individuals generally have low incomes, modest assets, and are more likely to be in poorer health and have greater health needs than Medicare beneficiaries without Medicaid.

Medicare beneficiaries living in the most rural areas have higher rates of chronic conditions and are more likely to be under 65 with permanent disabilities than beneficiaries in urban areas

Roughly one-third of Medicare beneficiaries living in the most rural areas had 5 or more chronic health conditions (32% vs. 25% in urban areas) (Figure 4). The share of beneficiaries in the most rural areas with specific chronic conditions included 66% with hypertension (vs. 61% in urban areas), 36% with heart disease (vs. 30% in urban areas), and 22% with a pulmonary condition (vs. 18% in urban areas) (Appendix Table 2).

More than one in five Medicare beneficiaries living in the most rural areas had a cognitive impairment (21% vs. 16% in urban areas), which may present additional challenges when navigating the health care system, particularly for those who must travel long distances to reach their health care appointments and may need to rely on family members or caregivers for transportation.

A larger share of Medicare beneficiaries in living in the most rural areas and in rural adjacent areas were under age 65 with permanent disabilities, relative to those living in urban areas (13%, 16% and 11%, respectively). People under age 65 typically qualify for Medicare once they have received Social Security Disability Insurance benefits for at least 24 months. Medicare beneficiaries under age 65 are more likely than older beneficiaries to experience problems with their health insurance, including cost-related problems and difficulty accessing needed health services.

A majority of Medicare beneficiaries in the most rural areas get their coverage from traditional Medicare than Medicare Advantage

In 2024, nearly 6 in 10 (58%) Medicare beneficiaries living in the most rural areas were in traditional Medicare and 42% were enrolled in a Medicare Advantage plan (Figure 5). This pattern is in contrast to beneficiaries living in other areas, where more than half of eligible beneficiaries (52% in rural adjacent areas and 56% in urban areas) were in Medicare Advantage, and the remaining 48% and 44%, respectively, were in traditional Medicare. This pattern is driven in part by the fact that fewer Medicare Advantage plans are available to people living in the most rural areas. More limited participation of local providers in Medicare Advantage plan provider networks in rural areas is also likely to factor into lower Medicare Advantage enrollment in the most rural areas.

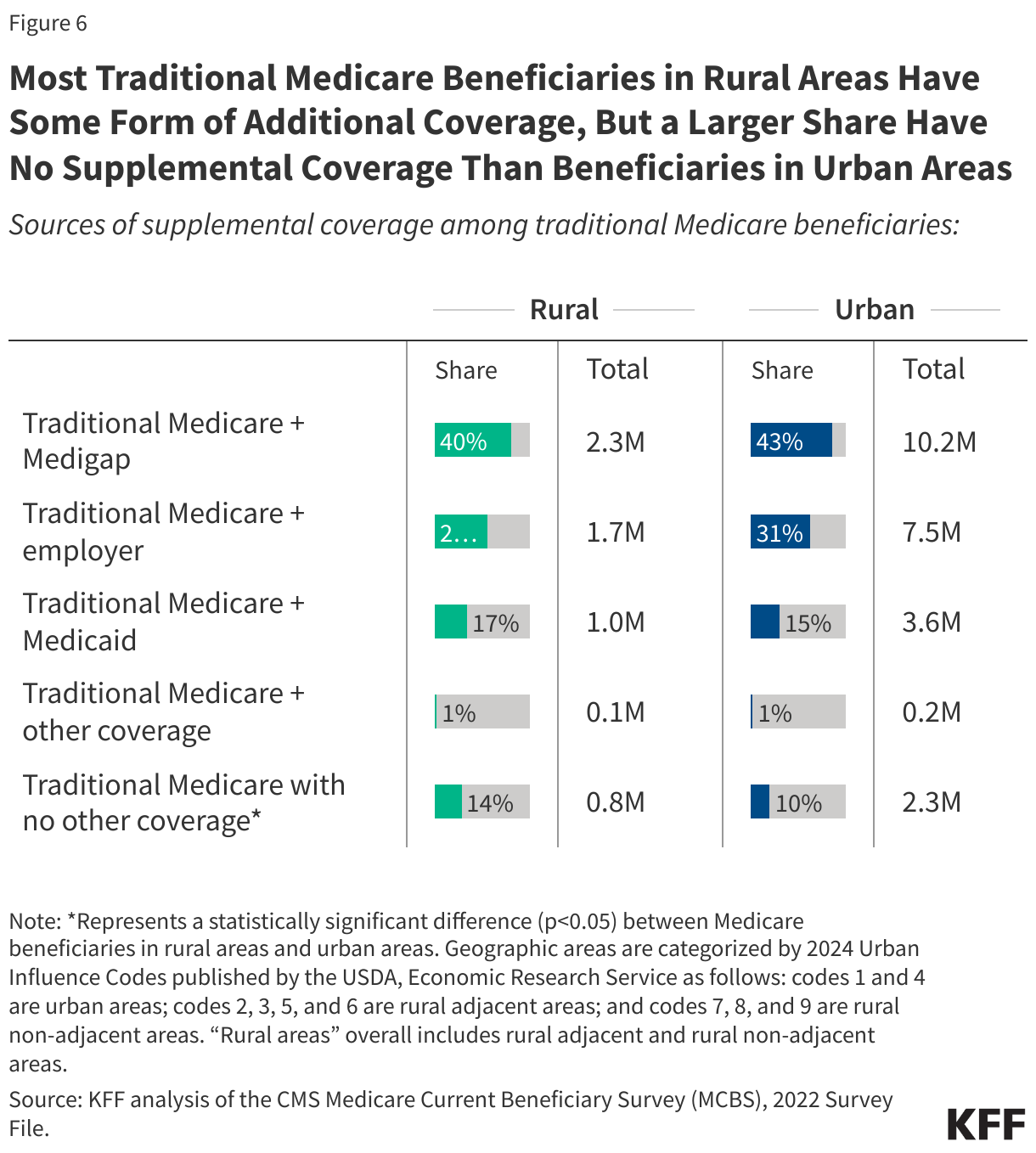

Among traditional Medicare beneficiaries in rural areas, most had some form of additional coverage—including 4 in 10 with a Medigap policy—but a larger share had no form of supplemental coverage compared to beneficiaries in urban areas. In 2022, similar shares of traditional Medicare beneficiaries in rural and urban areas (40% vs 43%) had a Medicare supplement insurance policy, also known as Medigap, to supplement their traditional Medicare coverage (Figure 6). Medigap policies, sold by private insurance companies, limit the financial exposure of Medicare beneficiaries by partially or fully covering Medicare’s cost-sharing requirements, but premiums for these policies can be costly and vary by state and policy type. Additionally, similar shares had some employer-sponsored insurance in addition to their traditional Medicare coverage.

However, a larger share of traditional Medicare beneficiaries in rural areas, including both the most rural counties and rural adjacent counties (14%), had no supplemental coverage than beneficiaries in urban areas (10%). These beneficiaries are fully exposed to Medicare’s cost-sharing requirements, and for those under age 65 in rural areas, getting a Medigap policy may be particularly challenging due to the lack of guaranteed issue rights for this group.

A small share of rural Medicare beneficiaries report difficulty accessing medical care, but they are more likely than beneficiaries in urban areas to report economic struggles, including health care cost-related problems and food insecurity

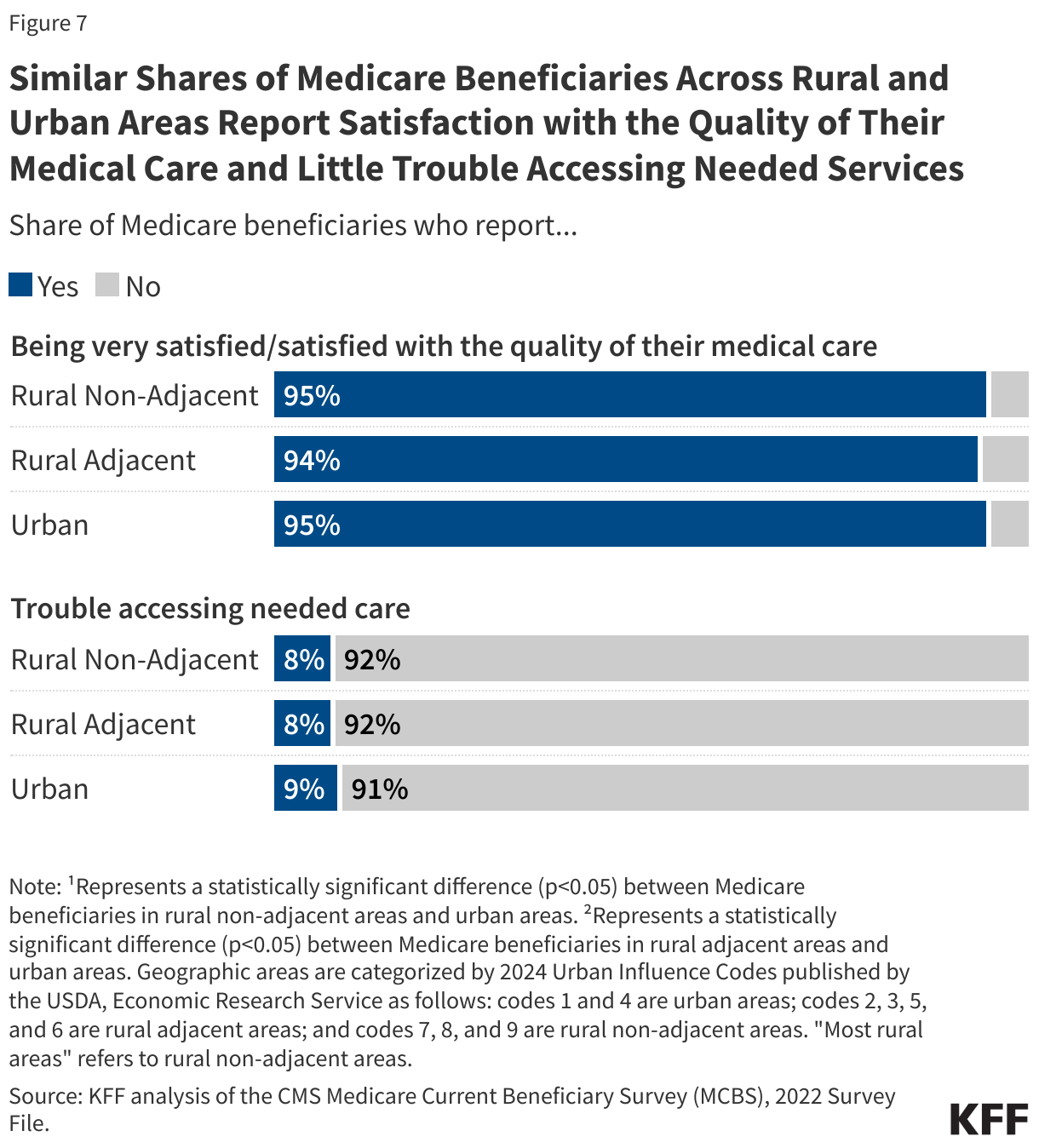

Most Medicare beneficiaries, including those in rural areas, report being satisfied with the quality of their medical care and few report difficulty accessing care. More than 9 in 10 Medicare beneficiaries living in the most rural areas, rural adjacent areas, and urban areas reported being satisfied or very satisfied with the quality of their medical care. Likewise, fewer than 1 in 10 beneficiaries in the most rural areas, rural adjacent areas, or urban areas reported difficulty accessing needed health care (Figure 7).

Medicare beneficiaries living in rural areas were more likely to report economic struggles, however, including food insecurity and health care cost-related problems (Figure 8). In 2022, more than one in five beneficiaries living in the most rural areas (21%) and rural adjacent areas (22%) reported some type of food insecurity in the past year compared to 16% of beneficiaries in urban areas. This includes running out of food and not having money to buy more, cutting the size of meals or skipping meals because there wasn’t enough money for food, eating less because there wasn’t enough money for food, or feeling hungry and not eating because there wasn’t enough money for food.

Additionally, larger shares of Medicare beneficiaries in the most rural areas (13%) and rural areas adjacent to urban areas (15%) reported having at least one of the following health care cost-related problems than beneficiaries in urban areas (10%): trouble getting needed health care due to cost, delays in health care due to cost, or problems paying medical bills.

Medicare beneficiaries in rural areas are less likely to be offered telehealth services by their usual providers than beneficiaries in urban areas

Among Medicare beneficiaries with a usual source of care, a lower share of beneficiaries in the most rural areas (57%) and areas adjacent to urban areas (51%) reported that their usual provider offers telehealth services compared with beneficiaries in urban areas (69%) (Figure 9). Lower rates of telehealth offerings by rural providers may reflect differences in provider capacity and health system infrastructure challenges in rural areas relative to urban areas.

Additionally, among traditional Medicare beneficiaries, 10% of those in rural areas used Medicare-eligible telehealth services compared to 14% of those in urban areas as of the third quarter of 2024, based on fee-for-service claims data. While telehealth use has the potential to improve access to care in areas with a shortage of health care providers or where people must travel farther to access medical care, lower use of telehealth services in rural areas could be partly due to more limited broadband access. According to the Federal Communications Commission, in 2022, 28% of Americans in rural areas lacked broadband internet coverage compared to just 2% of people in urban areas.

During the COVID-19 public health emergency, Congress enacted several Medicare telehealth flexibilities that were initially set to expire at the end of the public health emergency. However, these flexibilities have been extended multiple times, with the latest extension set to expire on September 30, 2025, unless Congress takes further action.

Methods |

| This analysis is based on several data sources, including the Centers for Medicare & Medicaid Services (CMS) Medicare Monthly Enrollment data, September 2024, and the Medicare Current Beneficiary Survey (MCBS), 2022 Survey file data (the most recent year available). The MCBS is a nationally representative survey of Medicare beneficiaries (66.1 million people in 2022, weighted), including beneficiaries living in the community and in facilities. The MCBS analysis accounted for the complex sampling design of the survey, including topical survey weights where applicable and relevant replicate weights.

For Medicare Advantage enrollment by rural status, the analysis used CMS’ 2024 Medicare Advantage Landscape files and the September 2024 Medicare Monthly Enrollment data (See KFF, “Most People in the Most Rural Counties Get Medicare Coverage from Traditional Medicare”, April 2025). This analysis combines these datasets with the 2024 Urban Influence Codes published by the U.S. Department of Agriculture Economic Research Service for estimates of beneficiaries in counties that are part of rural or urban areas. To examine the role of urban influence, which affects access to infrastructure, including for the delivery of health care services, rural counties are further classified as adjacent to or not adjacent to an urban (metropolitan) area. The 2024 Urban Influence Codes classifies 3,235 counties and county-equivalents into 9 categories, which we categorize as follows: Urban 1. Large metro (in a metro area with at least 1 million residents) 4. Small metro (in a metro area with fewer than 1 million residents) Rural adjacent 2. Micropolitan, adjacent to a large metro area 3. Noncore, adjacent to a large metro area 5. Micropolitan, adjacent to a small metro area 6. Noncore, adjacent to a small metro area Rural non-adjacent 7. Micropolitan, not adjacent to a metro area 8. Noncore, not adjacent to a metro area and contains a town of at least 5,000 residents 9. Noncore, not adjacent to a metro area and does not contain a town of at least 5,000 residents In this analysis, large and small metropolitan areas (Urban Influence Codes 1 and 4) are referred to as “urban” areas; rural counties not adjacent to an urban (metropolitan) area (Urban Influence Codes 7, 8, and 9) are referred to as the “most rural” areas, and rural counties adjacent to an urban (metropolitan) area (Urban Influence Codes 2, 3, 5, and 6) are referred to as “adjacent to urban areas”. The analysis on sources of coverage in traditional Medicare used the MCBS and was based on the source of coverage held for the most months of Medicare enrollment in 2022. The analysis includes 59.6 million people with Medicare in 2022 (weighted), excluding beneficiaries who were enrolled in Part A only or Part B only for most of their Medicare enrollment in 2022 (weighted n=5.0 million) and beneficiaries who had Medicare as a secondary payer (weighted n=1.6 million). The analysis on use of Medicare-eligible telehealth services is based on CMS’ Medicare Telehealth Trends dataset, which is restricted to fee-for-service claims data and does not capture telehealth services used by Medicare Advantage enrollees. For this dataset, CMS defines rural and urban status using the beneficiary’s mailing ZIP code and the Rural Urban Commuting Area Crosswalk (RUCA). |

Appendix