Medicare Advantage in 2026: Enrollment Update and Key Trends

Editorial Note

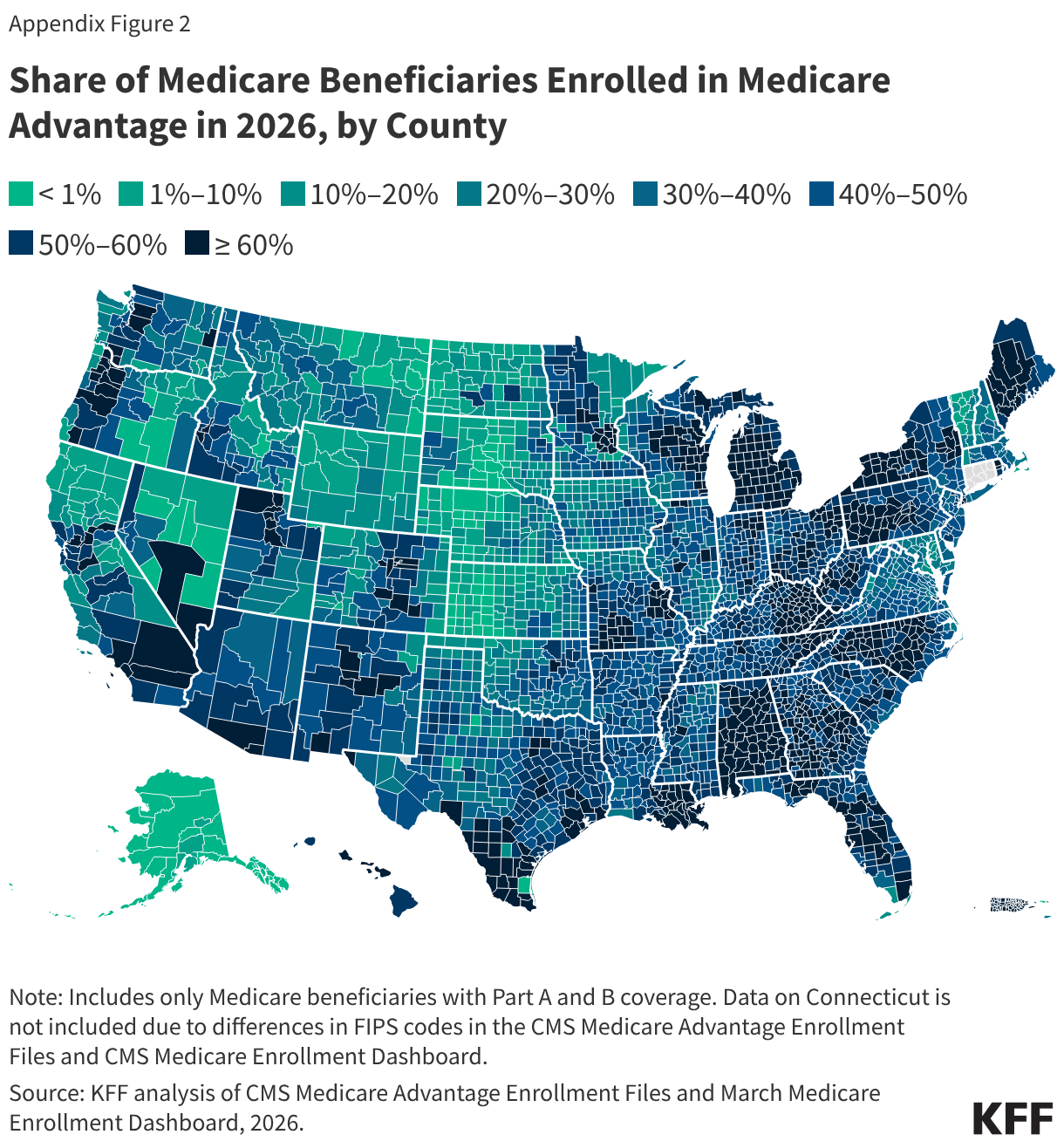

This analysis has been updated July 1, 2026 to reflect March 2026 data for overall Medicare Advantage penetration, though the Medicare Advantage penetration rate remains at 55%. It also now includes Medicare Advantage penetration by state and county (see Appendix figures).

Enrollment in Medicare Advantage, the private plan alternative to traditional Medicare, has increased steadily over the past two decades, with more than half of eligible beneficiaries enrolled in Medicare Advantage since 2023. The growth in enrollment has implications for federal spending, because according to the Medicare Payment Advisory Commission (MedPAC), Medicare payments to private plans are higher than spending for similar beneficiaries in traditional Medicare. In 2026, payments are 14% more per person, which translates into an additional $76 billion in federal spending this year. While payments per person relative to traditional Medicare are similar to a decade ago (15% higher), the impact on federal spending was substantially lower at $24 billion because enrollment was substantially lower with about one-third of eligible beneficiaries enrolled in a Medicare Advantage plan at that time.

Given the enrollment and spending trends, policymakers have become increasingly focused on how Medicare pays private plans, though without broad agreement on how or when to move forward with any changes to how Medicare Advantage plans are paid. In part, the difficulty stems from concerns about the effects of payment changes on beneficiaries’ choice among plans and access to supplemental benefits, such as coverage of dental, vision and hearing.

To better understand trends in the growth of the Medicare Advantage program, this brief provides current information about enrollment, including by plan type and firm. A second, companion analysis describes Medicare Advantage premiums, out-of-pocket limits, supplemental benefits offered, and prior authorization requirements in 2026.

Highlights for 2026:

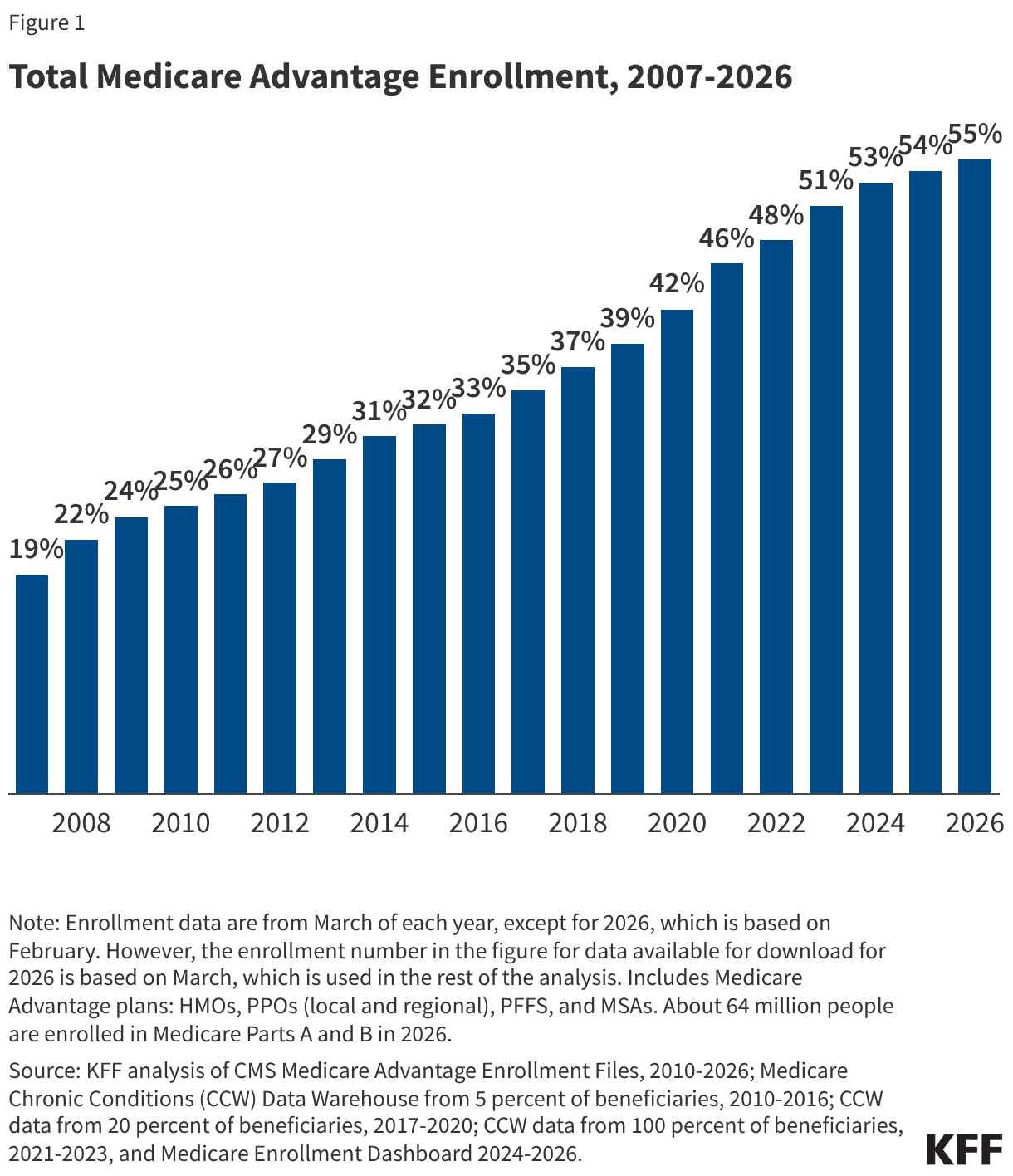

- More than half (55%) of eligible Medicare beneficiaries are enrolled in Medicare Advantage in 2026. While a growing share of Medicare beneficiaries are enrolled in a Medicare Advantage plan, the pace of the increase in enrollment continued to slow in 2026.

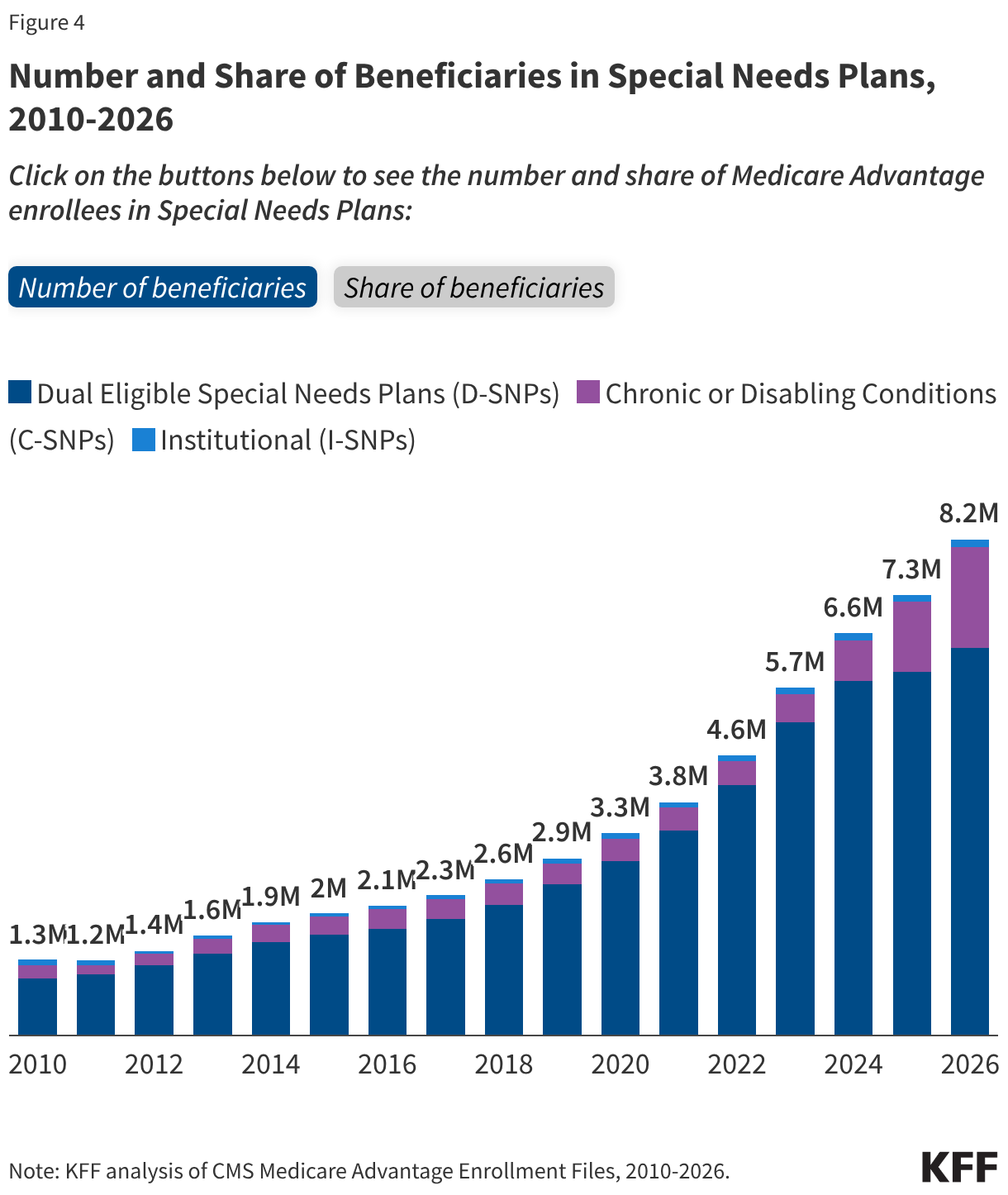

- In 2026, nearly one quarter (23%) of Medicare Advantage enrollees are in a special needs plan (SNP), reflecting a steady increase in recent years. Most (85%) of the net increase in Medicare Advantage enrollment between 2025 and 2026 across all plan types was among SNPs, up from 48% in the prior year.

- More than three-quarters of SNP enrollment (78%) is in plans designed for people who are dually eligible for Medicare and Medicaid (D-SNPs), with plans for people with certain chronic conditions (C-SNPs) continuing to see a surge in enrollees in 2026 as in 2025. Enrollment in C-SNPS increased by 45% between 2025 and 2026, rising to 20% of SNP enrollment.

- Medicare Advantage enrollment is highly concentrated among plans owned by a small number of parent organizations, with UnitedHealth Group leading the market, and, together with Humana, accounting for nearly half (46%) of all Medicare Advantage enrollees nationwide, the same as in 2025, and consistent with the pattern in prior years. However, market shares for the leading parent organizations changed with UnitedHealth Group dropping to 26% (down from 29%), and Humana increasing to 20% (up from 17%). In absolute numbers, Humana had the largest growth in enrollment, with 1.3 million more enrollees in 2026 than in 2025. In contrast, enrollment in UnitedHealth Group plans decreased by nearly 647,000 from 2025 to 2026.

More than half of eligible Medicare beneficiaries are enrolled in Medicare Advantage in 2026.

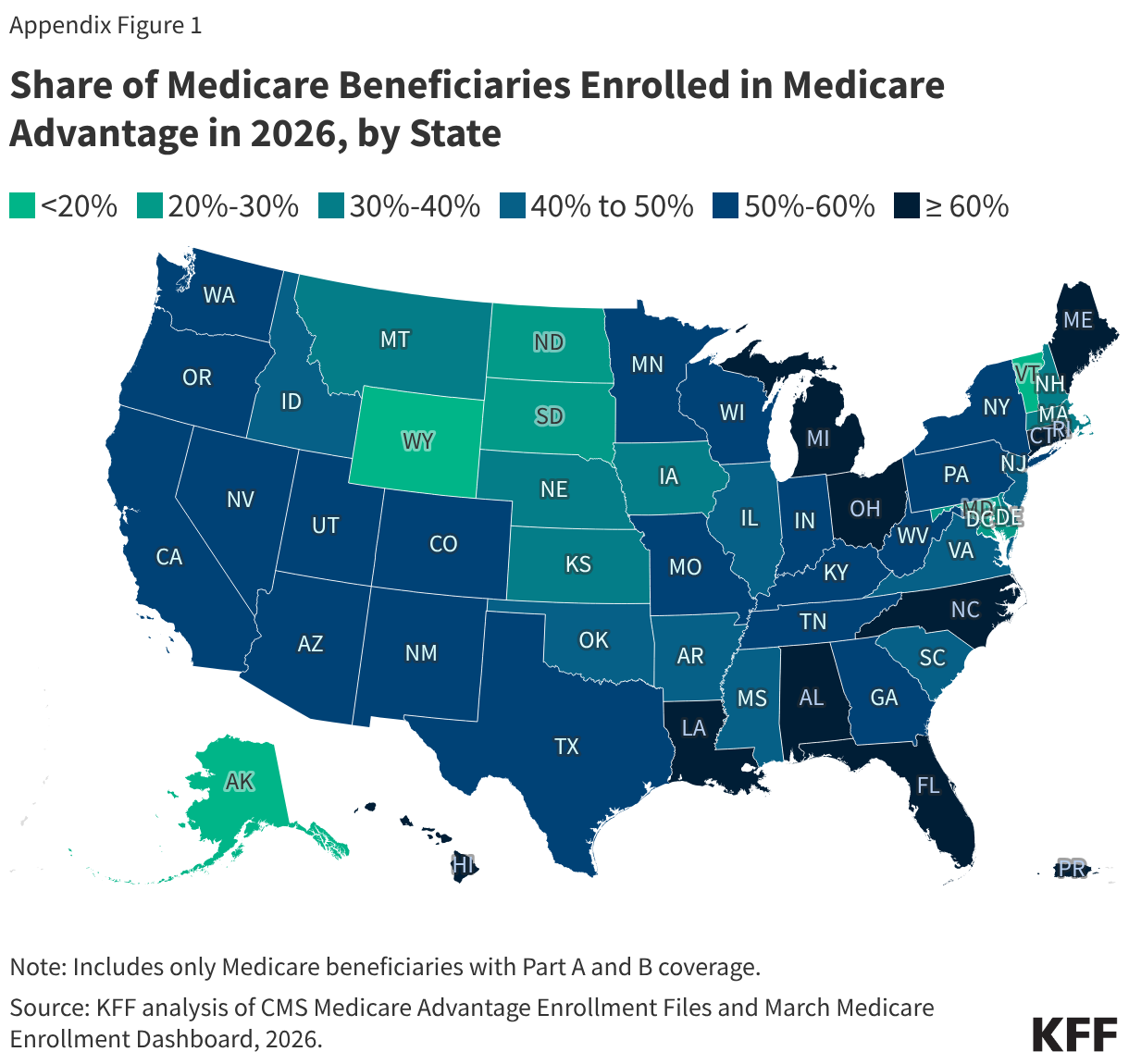

In 2026, more than half (55%) of eligible Medicare beneficiaries – 35.2 million out of 64.2 million Medicare beneficiaries with both Medicare Parts A and B – are enrolled in Medicare Advantage plans (Figure 1). The share of Medicare beneficiaries in Medicare Advantage plans varies by state and by county (Appendix Figures 1 and 2). Medicare Advantage enrollment as a share of the eligible Medicare population has jumped from 19% in 2007 to 55% in 2026.

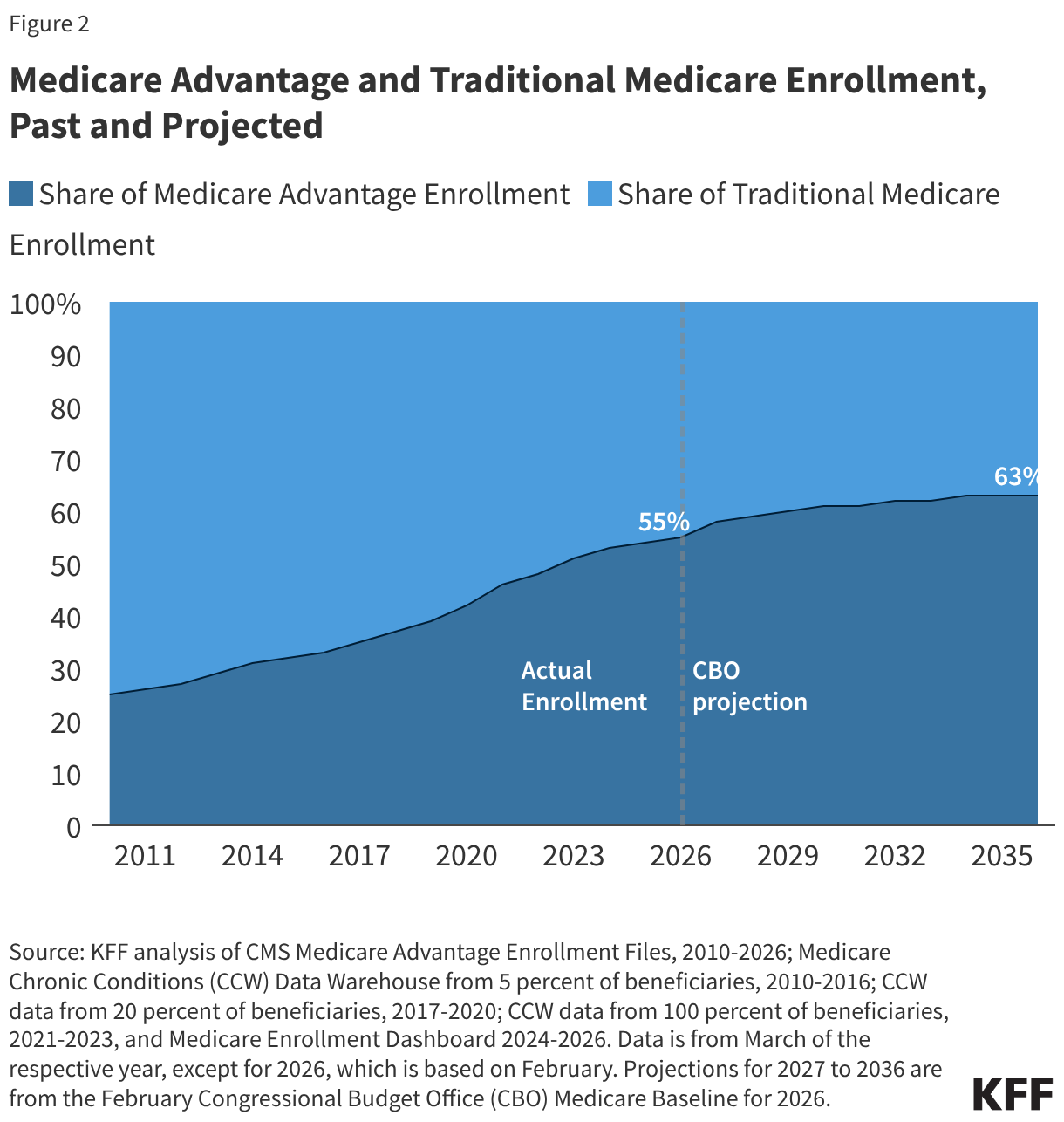

Between 2025 and 2026, total Medicare Advantage enrollment grew by about 1.1 million beneficiaries, or 3% – a similar growth rate to the prior year (4%). The Congressional Budget Office (CBO) projects that the share of all Medicare beneficiaries enrolled in Medicare Advantage plans will rise to 63% by 2034 and remain at 63% for 2035 and 2036 (Figure 2).

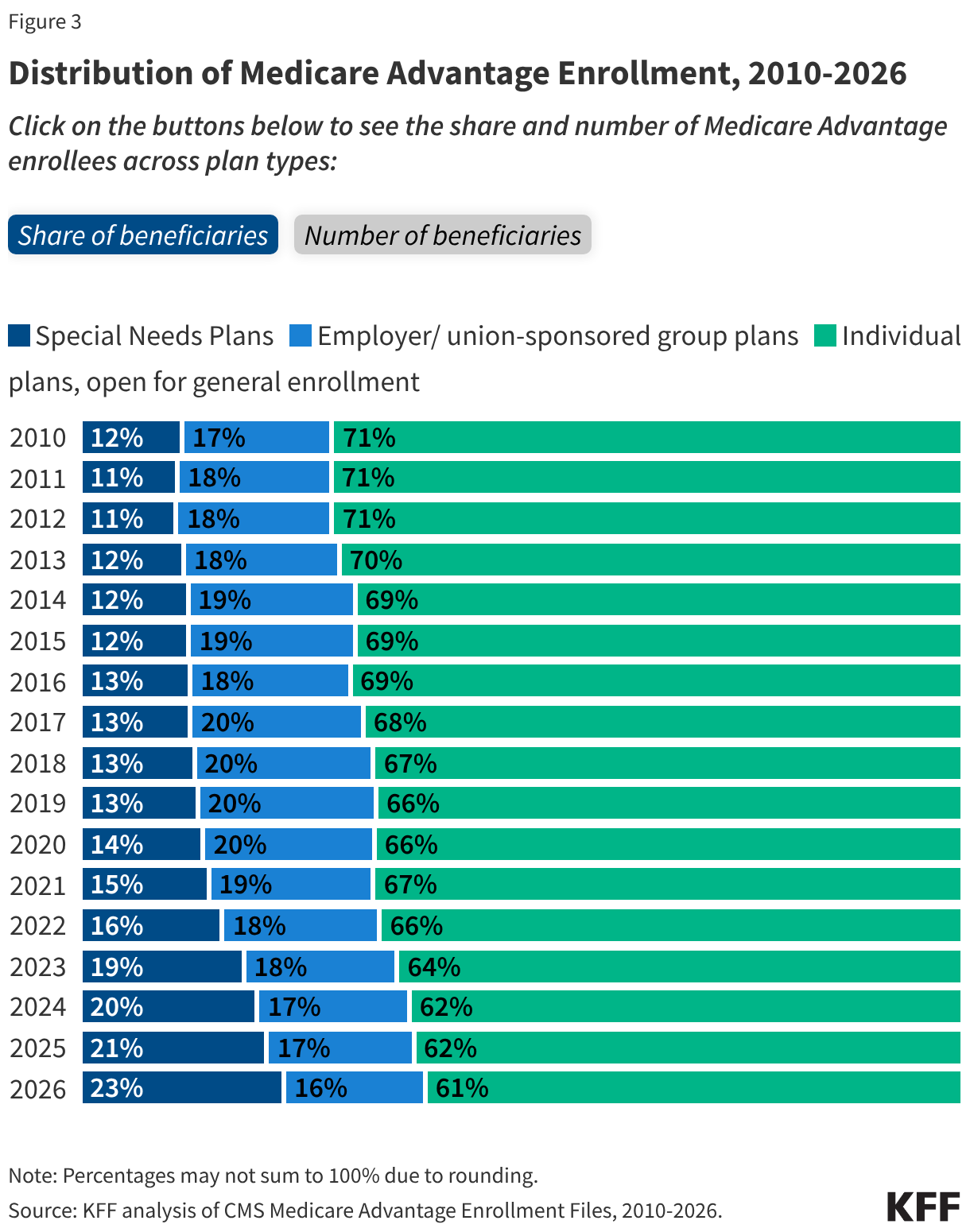

In 2026, about six in ten Medicare Advantage enrollees are in individual plans that are open for general enrollment.

About 6 in 10 Medicare Advantage enrollees (61%), or 21.4 million people, are in plans generally available to all Medicare beneficiaries for individual enrollment (Figure 3). That is an increase of 0.2 million enrollees compared to 2025, though individual plans comprised a slightly smaller share of total Medicare Advantage enrollment in 2026 (61%) compared to 2025 (62%), and their share of enrollment has declined since 2010 when they comprised 71% of all enrollees. The decline in the share of enrollment in individual plans is due to faster enrollment growth in special needs plans (SNPs), especially since 2018.

Special needs plans (SNPs) comprise a growing share of Medicare Advantage enrollment.

Nearly 8.2 million Medicare beneficiaries are enrolled in special needs plans (SNPs), an increase of more than 900,000 enrollees since 2025, and accounted for 85% of the net increase in Medicare Advantage enrollment over the last year. SNPs restrict enrollment to beneficiaries with significant or relatively specialized care needs, or who qualify because they are eligible for both Medicare and Medicaid. SNPs comprise a growing share of Medicare Advantage enrollment, accounting for 23% of enrollees in 2026 compared with 21% of enrollees in 2025 (Figure 4).

The increase in SNP enrollment is consistent with the increasing number of SNP plans available on average and more dual-eligible individuals having access to these plans since the Bipartisan Budget Act of 2018 made SNPs a permanent part of the Medicare Advantage program. Growth in SNP enrollment may also stem from the sharp increase in rebate payments, which have more than doubled since 2017 and are higher than for individual plans, which enables SNPs to offer extra benefits that are attractive to dual-eligible individuals.

Further, the Medicare Advantage Value-Based Insurance Design Model (VBID), which launched in 2017, gave plans the ability to provide additional interventions to enrollees such as reduced cost sharing and extra benefits based on their socioeconomic status (e.g., LIS eligibility), along with other targeting criteria. This meant many enrollees in SNPs, including those dually eligible for Medicare and Medicaid, may have been eligible for additional benefits. For example, plans enrolled in the model were able to offer benefits such as food and produce, assistance with utilities, and transportation for non-medical needs, among others, to a broader group of enrollees, when many of those benefits were typically reserved for enrollees who met the stricter definition of eligibility for Special Supplemental Benefits for the Chronically Ill (SSBCI). However, CMS discontinued this model in 2025 due to the “unprecedented cost” of this model, including increased rebates and increased Part D expenditures.

D-SNPs. Most SNP enrollees (78%) are in plans for beneficiaries dually enrolled in both Medicare and Medicaid (D-SNPs), a decline from 83% in 2025. While D-SNPs are designed specifically for dually-eligible individuals, among the 3.9 million dually-eligible enrollees with full benefits enrolled in Medicare Advantage plans, 28% were enrolled in Medicare Advantage plans that are generally available to all beneficiaries (not designed specifically for the dually-eligible population).

C-SNPs. Another 20% of SNP enrollees are in plans for people with severe chronic or disabling conditions (C-SNPs) – an increase from 16% in 2025. C-SNP enrollment in 2026 (about 1.7 million people) is 45% higher than it was in 2025 – an increase of about 518,000 enrollees. Nearly all (97%) C-SNP enrollees are in plans for people with diabetes or cardiovascular conditions in 2026, the same as in 2025.

I-SNPs. And 2% of SNP enrollees in 2026 are in plans for beneficiaries requiring a nursing home or institutional level of care (I-SNPs), the same as 2025. Enrollment in I-SNPs increased slightly in 2026 124,000 enrollees, an increase of about 9,000 enrollees since 2025.

SNP enrollment varies across states. In the District of Columbia and Puerto Rico, SNP enrollees comprise about half of all Medicare Advantage enrollees (51% in DC and 49% in PR). In eleven states, SNP enrollment accounts for at least a quarter of Medicare Advantage enrollment: 46% in MS, 40% in AR, 37% in NY, 36% in LA, 33% in FL, 32% in SC, 30% in GA, 27% in OK and AL, 26% in CT, and 26% in RI. In the remaining 39 states, fewer than a quarter of Medicare Advantage enrollees are in SNPs, including Alaska and Vermont, which have no SNP enrollment.

Enrollment in a D-SNP comprises the largest share of enrollment in SNPs in all states except New Hampshire where C-SNP enrollment is higher, though overall SNP enrollment only represents 2% of Medicare Advantage enrollment in New Hampshire. C-SNP enrollment represents a relatively large share of Medicare Advantage SNP enrollment in Illinois, Utah, South Carolina, Delaware, Nevada, and Oregon, where 40% or more of SNP enrollment is in C-SNPs.

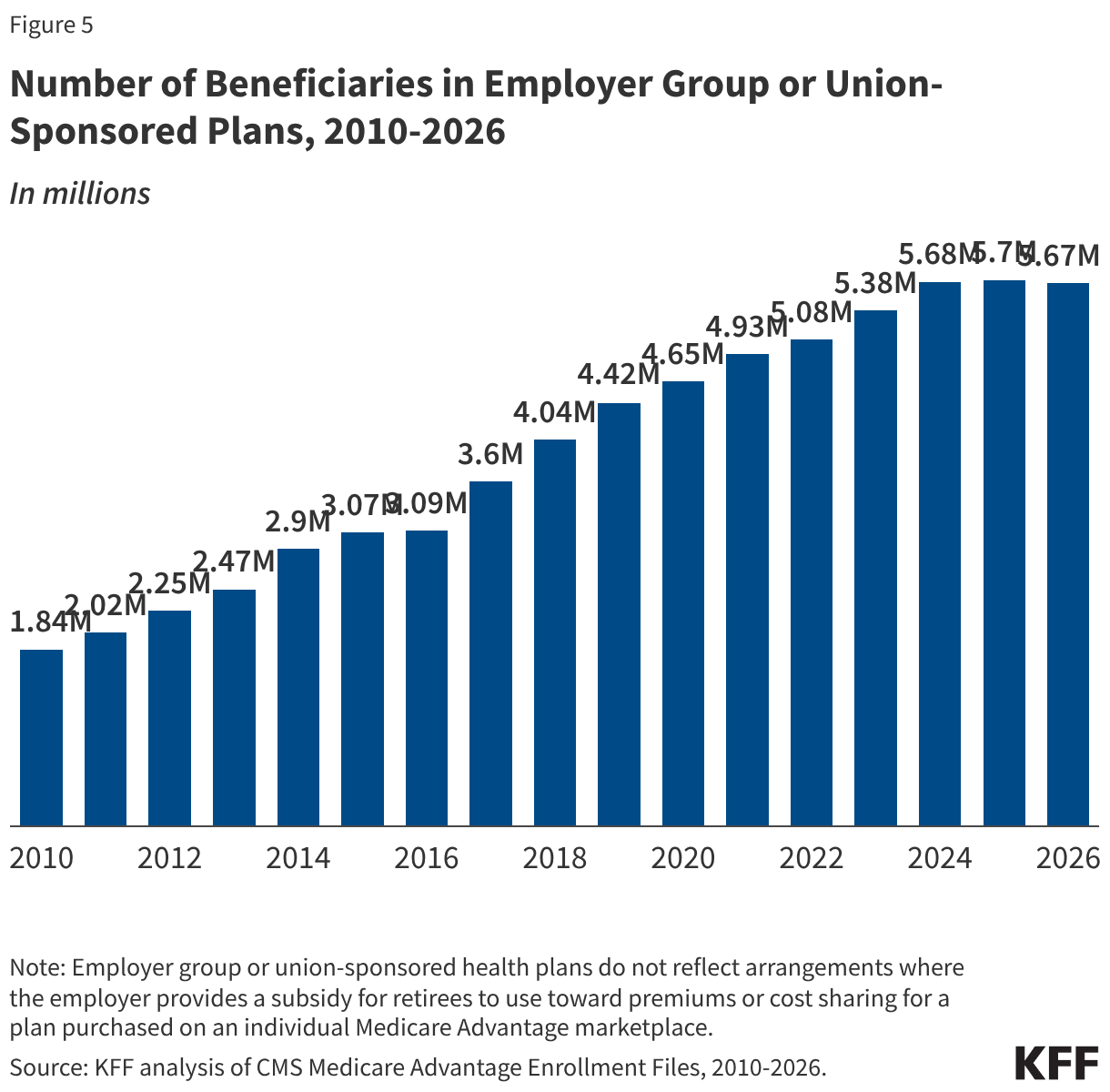

Slightly less than one in five (16% or about 5.7 million) Medicare Advantage enrollees are in a group plan offered to retirees by an employer or union.

Group enrollment as a share of total Medicare Advantage enrollment is 16%, the lowest share since 2010, though it has generally fluctuated between 17% and 20% of enrollment. At the same time, the number of enrollees has increased from 1.8 million in 2010 to 5.7 million in 2026. The 2026 enrollment in group plans is a slight decrease from 2025 (a decrease of about 31,000 enrollees), the first time since 2010 that enrollment in this type of plan has declined year-to-year (Figure 5). With a group plan, an employer or union contracts with an insurer and Medicare pays the insurer a fixed amount per enrollee to provide benefits covered by Medicare. For example, 13 states provided health insurance benefits to their Medicare-eligible retirees exclusively through Medicare Advantage plans in 2024.

As with other Medicare Advantage plans, employer and union group plans may provide additional benefits and/or lower cost sharing than traditional Medicare and are eligible for bonus payments if they obtain required quality scores. The employer or union (and sometimes the retiree) may also pay an additional premium for these supplemental benefits. Group enrollees comprise a quarter or more of Medicare Advantage enrollees in seven states: 100% in AK, 60% in VT, 34% in MI, 31% in NJ, 28% in MD and WV, and 25% in IL.

Medicare Advantage enrollment is highly concentrated among a small number of parent organizations.

The average Medicare beneficiary is able to choose from Medicare Advantage plans offered by 8 parent organizations in 2026, the same as in 2025 and 2024, and nearly three in ten (29%) can choose among Medicare Advantage plans offered by 10 or more parent organizations.

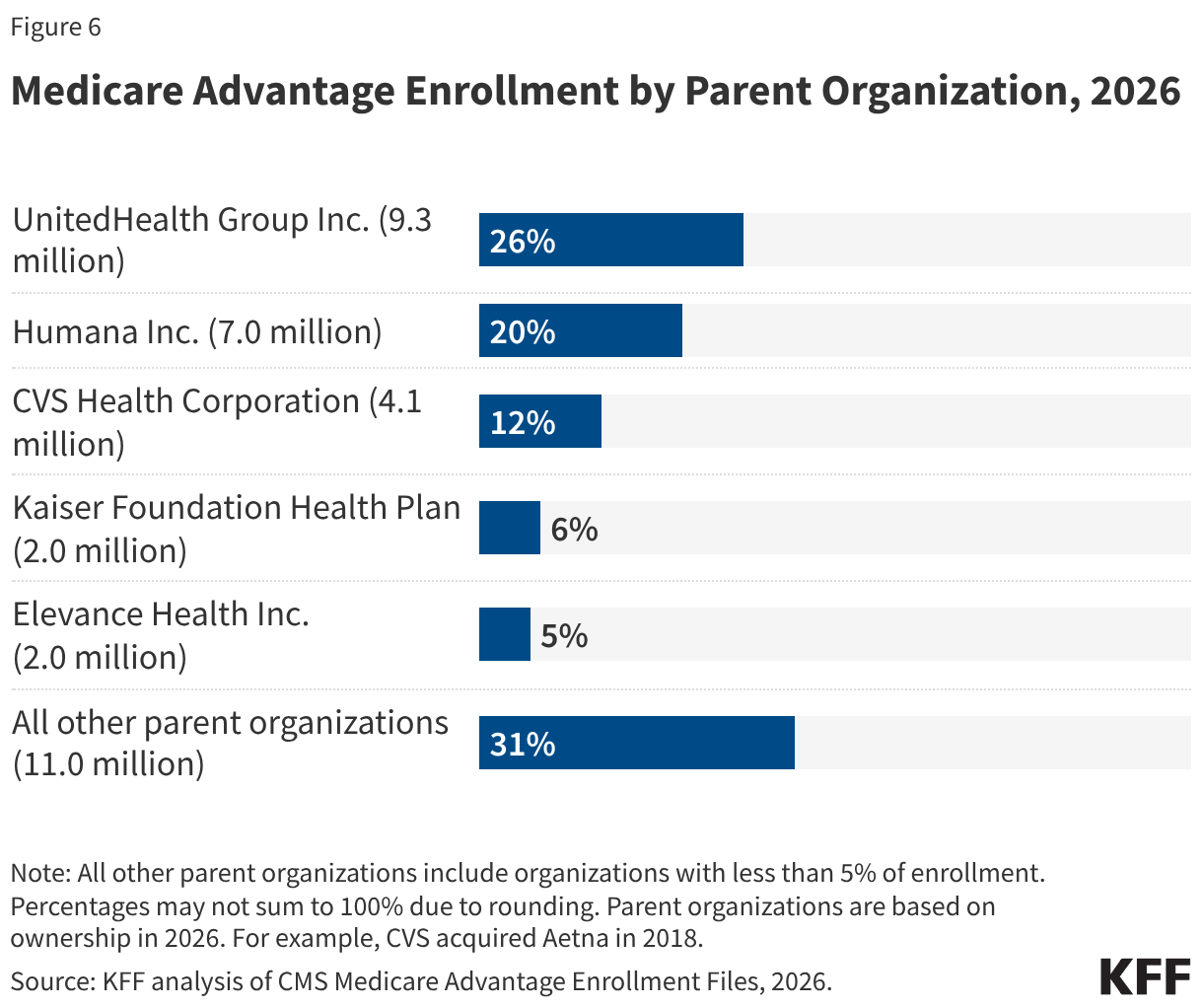

UnitedHealth Group and Humana account for nearly half of all Medicare Advantage enrollees nationwide in 2026.

Despite most beneficiaries having access to plans operated by several parent organizations, Medicare Advantage enrollment is highly concentrated among a small number of parent organizations (Figure 6). UnitedHealth Group Inc. accounts for 26% of all Medicare Advantage enrollment in 2026 (a decline from 29% in 2025), or 9.3 million enrollees. Humana Inc. accounts for 20% of all Medicare Advantage enrollment in 2026 (an increase from 17% in 2025), or 7 million enrollees. Together, UnitedHealth Group Inc. and Humana Inc. account for nearly half (46%) of all Medicare Advantage enrollees nationwide, the same share as in 2025. In more than a quarter of counties (28% or 889 counties), these two organizations account for at least 75% of Medicare Advantage enrollment. These counties include East Baton Rouge (Baton Rouge), LA (81%), Travis County (Austin), TX (78%), Jackson County (Kansas City), MO (76%), and Palm Beach, Florida (75%).

Three other parent organizations comprise more than 5% of Medicare Advantage enrollment: CVS Health Corporation (12%), Kaiser Foundation Health Plan Inc. (6%), and Elevance Health Inc, (5%). (In contrast, as of 2025, CVS Health and Centene Corporation dominate the market for stand-alone prescription drug plans (PDP) that supplement traditional Medicare, with both organizations accounting for just over half of enrollment in PDPs).

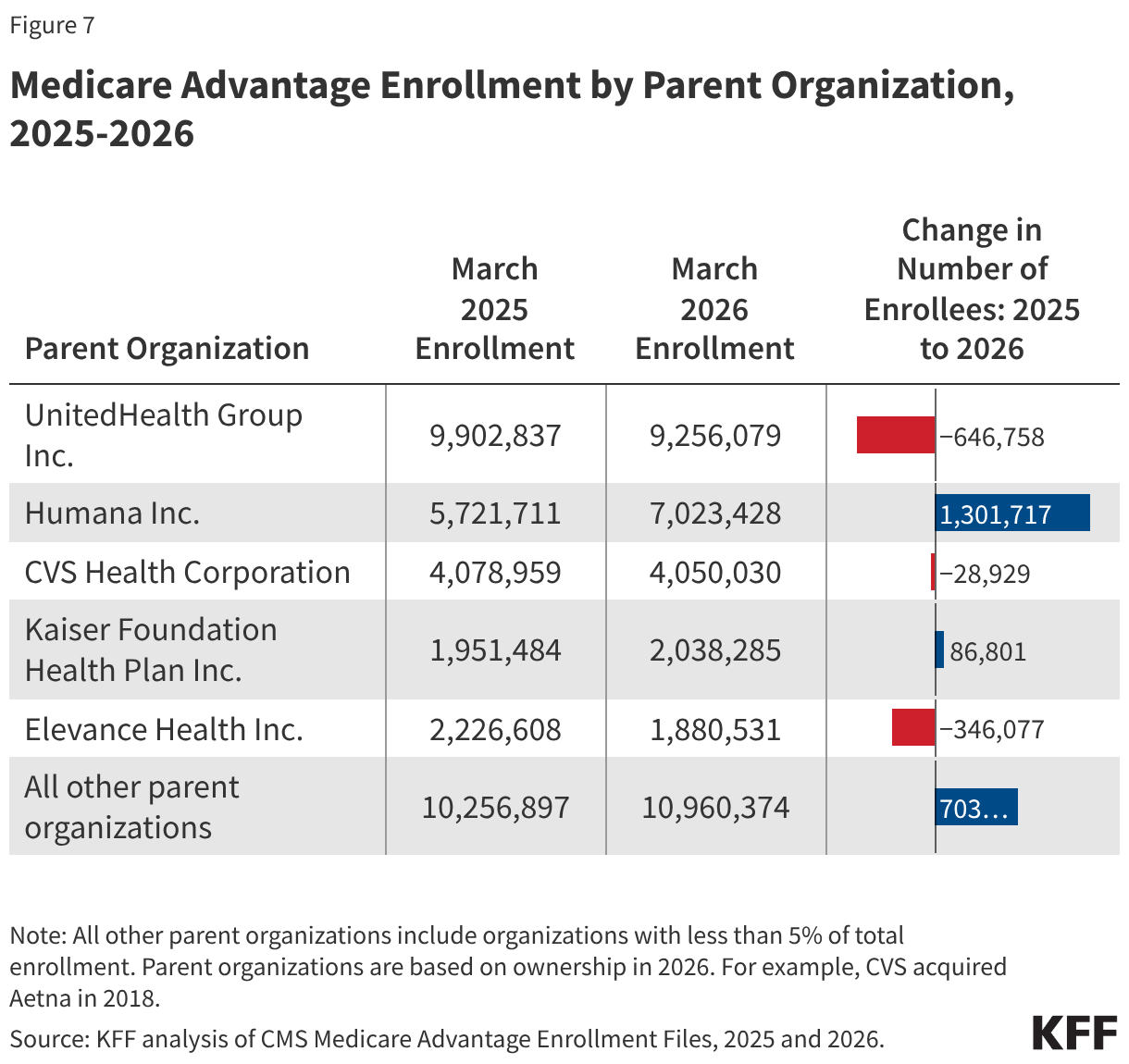

Humana and Kaiser Permanente were the only large insurers to increase enrollment from 2025 to 2026.

In absolute numbers, Humana had the largest growth in enrollment, with 1.3 million more beneficiaries enrolled in a plan sponsored by Humana in March 2026 than in March 2025 (Figure 7). Of the largest insurers (5% of enrollment or more), Kaiser Permanente had the second largest growth in enrollment, with an increase of nearly 87,000 beneficiaries between March 2025 and March 2026. However, some smaller insurers had even larger growth – Devoted Health had an increase of nearly 258,000, SCAN Group had an increase of 136,000, and Aware Integrated had an increase of 89,000 beneficiaries between March 2025 and March 2026 (data not shown).

In contrast, enrollment in UnitedHealth plans declined, decreasing by nearly 647,000 beneficiaries between March 2025 and March 2026, and Elevance had the second largest enrollment drop, losing 346,000 beneficiaries, while enrollment in CVS plans declined by nearly 29,000.

Methods

This analysis uses data from the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage Enrollment, Benefit and Landscape files for the respective year. KFF uses the Medicare Enrollment Dashboard for enrollment data for March 2024-2026, and the CMS Chronic Conditions Data Warehouse Master Beneficiary Summary File (MBSF) for March for earlier years. For other analyses of enrollment in this brief, KFF uses March data; enrollment data is only provided for plan-county combinations that have at least 11 beneficiaries; thus, this analysis excludes approximately 400,000 individuals who reside in a county where county-wide plan enrollment does not meet this threshold. Trend analysis begins in 2007 because that was the earliest year of data that was based on March enrollment. Data from the Medicare enrollment dashboard (used to calculate penetration rates) may change retroactively as CMS updates and reconciles administrative enrollment records. As a result, historical enrollment counts and penetration rates may differ from earlier downloads of the same data.

KFF calculates the share of eligible Medicare beneficiaries enrolled in Medicare Advantage, meaning they must have both Part A and B coverage. In previous years, KFF calculated the share of Medicare beneficiaries enrolled in Medicare Advantage by including Medicare beneficiaries with either Part A and/or B coverage. We modified our approach in 2022 to estimate the share enrolled among beneficiaries eligible for Medicare Advantage who have both Medicare Part A and Medicare B.

Additionally, in previous years, KFF had used the term Medicare Advantage to refer to Medicare Advantage plans as well as other types of private plans, including cost plans, PACE plans, and HCPPs. However, cost plans, PACE plans, and HCPPs are excluded from this analysis in addition to MMPs. In this analysis, KFF excludes these other plans as some may have different enrollment requirements than Medicare Advantage plans (e.g., may be available to beneficiaries with only Part B coverage) and in some cases, may be paid differently than Medicare Advantage plans. These exclusions are reflected in all data displayed trending back to 2007.

Beginning with the analysis of 2025 Medicare Advantage enrollment, KFF has relied on the parent organization field reported to CMS to identify plans sponsored by the same insurer. Previously, KFF had supplemented these data with publicly available information about acquisitions, mergers, and business relationships. The previous approach led to fewer total plan sponsors.

Medicare projections for 2027-2036 are from the February Congressional Budget Office (CBO) Medicare Baseline for 2026. Using the CBO baseline, Medicare enrollment is based on individuals who are enrolled in Part B, which is designed to include only individuals who are eligible for Medicare Advantage and exclude those who only have Part A only (~5.7 million people in 2026) and cannot enroll in Medicare Advantage. However, it may include some individuals who have Part B only and also are not eligible for Medicare Advantage.

Enrollment counts in publications by firms operating in the Medicare Advantage market, such as company financial statements, might differ from KFF estimates due to inclusion or exclusion of certain plan types, such as SNPs or employer group health plans.

Appendix

Meredith Freed, Jeannie Fuglesten Biniek, Nancy Ochieng, and Tricia Neuman are with KFF. Anthony Damico is an independent consultant.