Marketplace Enrollees with Unpredictable Incomes Could Face Bigger Penalties Under House Reconciliation Bill Provision

New legislative proposals released this week could potentially expose Marketplace enrollees to higher costs if their income at the end of the year differs from what they originally estimated. Most Marketplace enrollees (92% in 2025) receive a tax credit to help pay their premiums, and the vast majority of those receive the credit in advance to lower their monthly payments, rather than when they file their taxes.

To receive the Advance Premium Tax Credit (APTC), Marketplace enrollees must estimate their income for the upcoming year. If, by the time they file their taxes over a year later, their income is different, they must reconcile the tax credit they received with what they were eligible for. This could result in receiving additional assistance or having to repay some or all of the credit back to the federal government. The ACA currently caps how much low and middle-income enrollees must repay. Currently, individuals with incomes between 100% and 400% of the federal poverty level (FPL) have a capped repayment amount, regardless of how much their income changes. Repayment limits range from $375 to $1,625 for an individual, on a sliding scale based on income. Premium tax credits are only available for people whose income is above the poverty level.

At least three current policy issues could affect Marketplace enrollees with volatile incomes:

- A recent Trump Administration proposed rule suggests there could be a widescale practice of people with incomes below poverty inflating their expected incomes to exceed the poverty level to gain eligibility for premium tax credits. In response, the proposed rule would require some applicants to submit additional documentation to support their expectation that their income will exceed poverty in the coming year. Additionally, individuals who do not file their taxes and reconcile their premium tax credits would become ineligible for these tax credits in future years. These potential changes could reduce federal spending on tax credits and address concerns about fraud, but could also pose challenges and reduce coverage for enrollees with less predictable income.

- Additionally, the House Reconciliation bill would codify the proposed rule described above. It would similarly require certain Marketplace applicants to present documentation verifying expected changes in their income before they can enroll in subsidized coverage. In addition it would eliminate repayment caps on the premium tax credit, meaning enrollees would have to repay the full amount of their excess premium tax credit.

- Later this year, enhanced premium tax credits are set to expire unless Congress extends them, meaning that tax credits will be lower for all subsidized enrollees and people with incomes over four times poverty will no longer be eligible for premium tax credits. Because the original ACA did not include any repayment caps for people with incomes over four times poverty, even a small increase in a household’s income putting them over that threshold would mean they have to pay back the entire premium tax credit.

To explore the challenges families may face in predicting their annual income, this analysis uses data from the 2023 Survey of Income and Program Participation (SIPP). It compares each family’s estimated annual income — based on the first three months of reported monthly income — to their actual income at the end of the year.

Key Findings

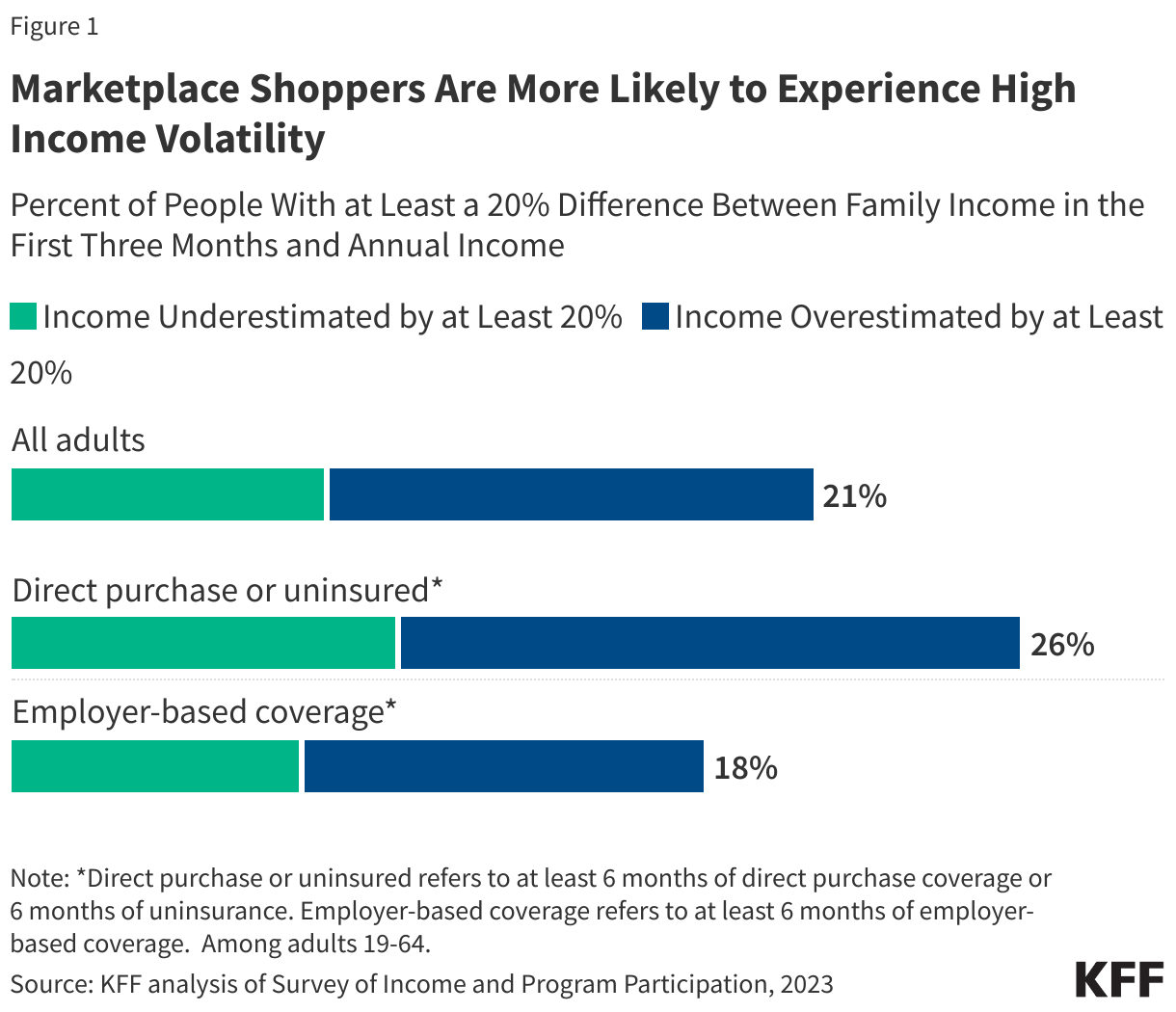

- Many Americans experience high income volatility, in particular potential ACA Marketplace shoppers. One in five people aged 19-64 were in families that saw more than a 20% difference in their income, split approximately equally between people who ended up with higher income and those who ended up with lower income.

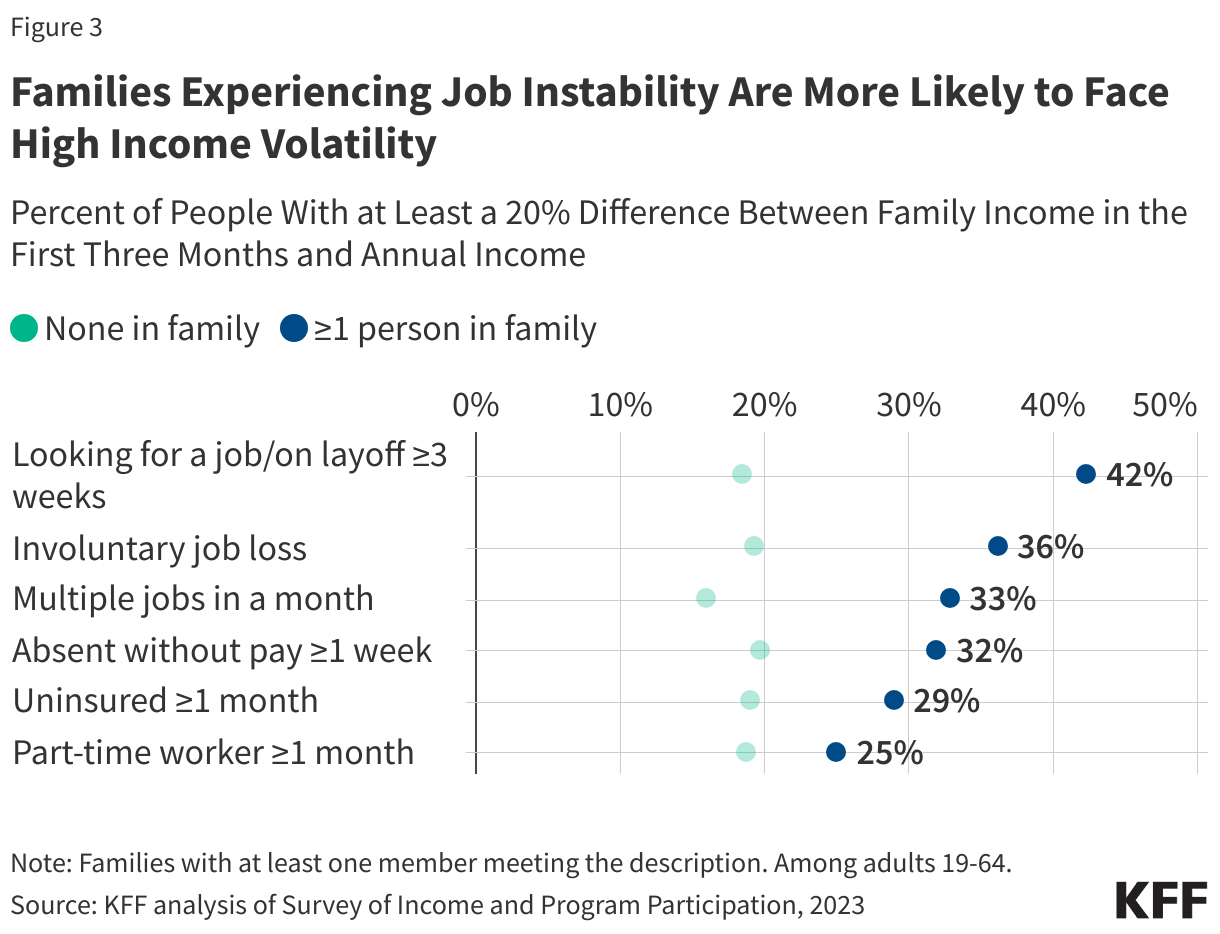

- People with less stable work are more likely to have high income volatility. For example, among people aged 19-64, families in which someone lost a job were more likely to have a 20% swing in their family income.

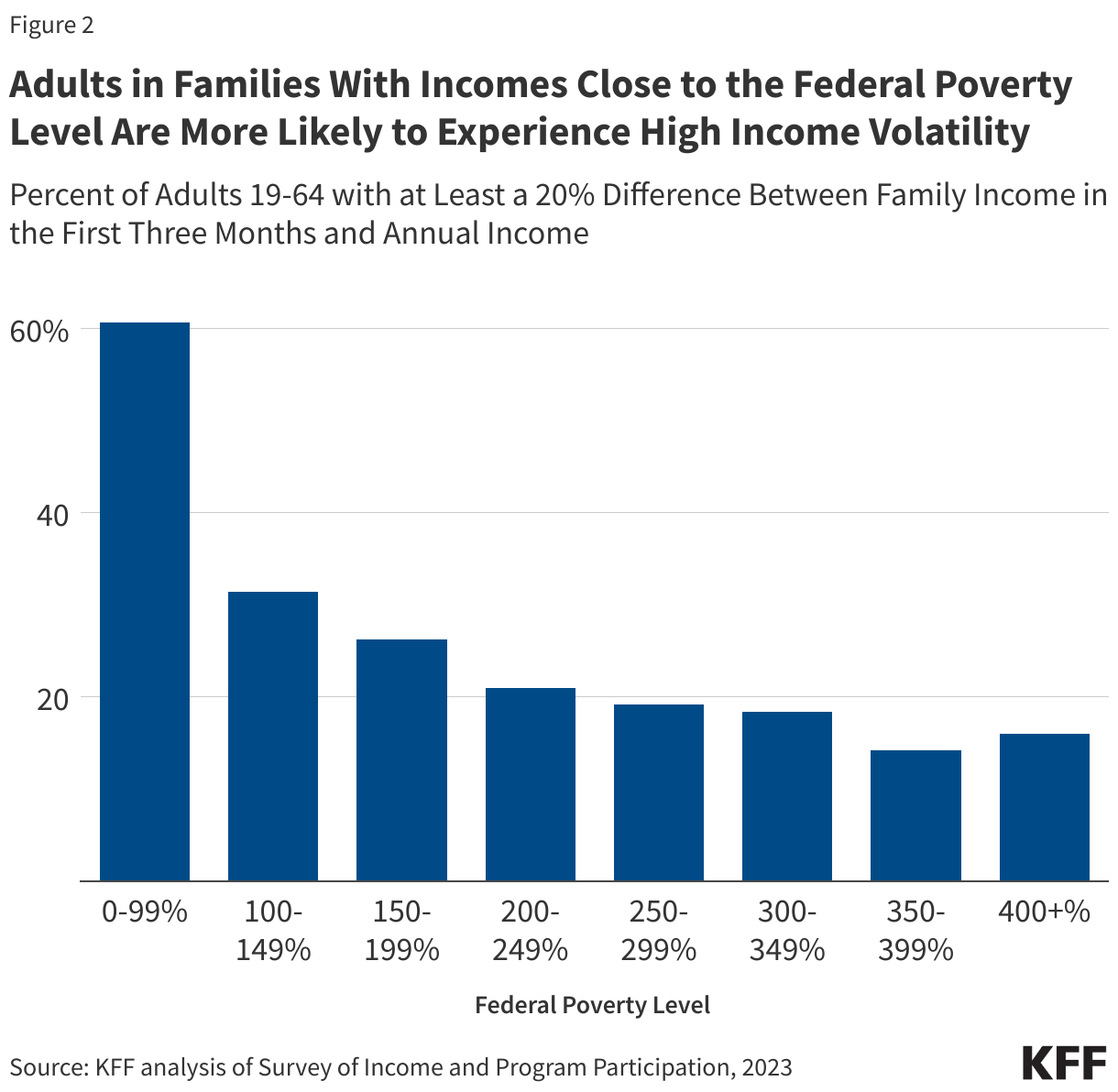

- For those near poverty, predicting annual income may be especially difficult. Many people with incomes just above poverty at the beginning of the year end up below poverty by the end of the year, and conversely many who start out with incomes below poverty end up with incomes above poverty. More than half (61%) of people with starting incomes below poverty end the year with an income more than 20% different than their income during the first three months of the year.

Income Volatility Among ACA Marketplace Shoppers:

Overall, one in five people (21%) aged 19-64 were in families that had high levels of income volatility, defined here as a difference of at least 20% between the estimated annual income based on the first three months of the year and the families’ actual income. People potentially shopping on the Marketplaces—those that had at least 6 months of non-group coverage or uninsurance—experience higher levels of income volatility than others. In 2023, more than one in four (26%) adults aged 19–64 with non-group coverage or who were uninsured for at least six months had high income volatility—higher than 18% among those with employer-based coverage.

Having an uninsured adult family member is associated with high income volatility: 29% people aged 19 to 64 in a family with at least one person who was uninsured for at least one month had high income volatility, compared to 19% for people in a family without an uninsured member during the year. In 2023, 9.5% of the population under age 65 were uninsured, the majority (73.7%) in families with at least one full-time worker in the family. Unaffordable coverage is the most cited reason for being uninsured.

Repayment caps currently in effect protect Marketplace enrollees with high levels of income volatility from large tax bills for excess premium tax credits. For example, consider a 56-year-old individual in Boulder County, CO, who estimated their annual income would be $40,000 (266% of the federal poverty level for 2025), but ultimately earned $55,000 (365% FPL). They would have received $7,123 in advance premium tax credits but were only ultimately eligible for $4,774—an excess of $2,349. Under current rules, their repayment would be capped at $1,625, limiting the amount they owe to about 3% of their income. If the repayment caps were eliminated, however, they would be responsible for repaying $2,349.

Income Volatility Among Families near Poverty:

People with family incomes close to the threshold for qualifying for a premium tax credit (100%) have particularly volatile incomes. Among adults aged 19–64 in families with incomes between 100% and 150% of FPL during the first three months of the year, nearly one-in-ten ended the year with incomes below the poverty line. Conversely, many people with incomes below poverty during the first three months of the year finish the year with an income above the poverty line (30%). These people may lose out on potential subsidized coverage if they had assumed that their income would be below poverty.

The high share of people near poverty moving across the poverty threshold reflects the significant income volatility many low-income families experience. 3 in 5 adults living in poverty (61%) and nearly one in three (31%) of those with incomes between 100% and 150% of the federal poverty level (FPL), saw their annual income differ by more than 20% from what they earned in the first three months of the year. Under current IRS rules, households that fall below the poverty line are not required to repay the full premium tax credit they received, as long as their income estimate was made in good faith.

Common Causes of Income Volatility:

A family’s poverty level can change for many reasons, including shifts in household income or changes in family structure, such as birth, marriage, or divorce. In some cases, such as among seasonal workers, families may anticipate uneven income over the year. In others, these changes are unexpected. Families with an adult that was laid off during the year were more likely to have high income variability. Among adults aged 19 to 64, 42% of those in families where someone was looking for work or had been laid off for at least three weeks during the year experienced high-income volatility, compared to 18% of those in families without such disruptions. Other factors associated with high income volatility among non-elderly adults included:

- Involuntary job loss for someone in the family during the year (36% vs 19%)

- Someone in the family having multiple jobs during the year (33% vs 16%)

- Having someone in the family who was absent without pay from a job (32% vs 20%) for at least one week during the year.

Unpredictable annual income is often tied to the type of work someone does and how they are paid. For example, workers who are paid hourly but have irregular shifts may find it difficult to estimate their total earnings over the course of a year. Similarly, those in contract or gig economy jobs often don’t know in advance how many hours they will be able to work. Certain occupations are particularly associated with high income volatility: 38% of families with a packager, 32% with a landscaper or childcare worker, and 30% with a truck driver, food preparation worker, or security guard experienced high levels of income volatility. Additionally, 25% of households with a part-time worker had high income volatility.

Families Whose Incomes Exceeds the APTC Eligibility Thresholds

In 2022, the Inflation Reduction Act increased premium tax credits for all subsidized enrollees and expanded eligibility for premium tax credits to individuals in families with annual incomes above 400% of the FPL for the first time, but this provision is set to expire after 2025. Unless extended, individuals who see income increases beyond 400% of poverty, may become ineligible for the tax credits that subsidized their coverage. Fifteen percent of adults aged 19 to 64 with incomes between 350% and 450% of FPL experienced high income volatility. Among families with incomes between 100% and 400% of FPL after the first three months of the year, 9% of adults ended the year above 400% of FPL, while 2% ended the year below the poverty line.

Without premium tax credits, many potential Marketplace shoppers may not have the financial resources to enroll in coverage. For others, the risk of misestimating their income—and facing large repayment obligations—may discourage them from applying. Current rules cap the amount that households with incomes between 100% and 400% of the federal poverty level (FPL) must repay if they receive excess premium tax credits. However, proposals included in the Ways and Means reconciliation bill would eliminate these repayment caps, potentially exposing households with volatile incomes to significant tax burdens.

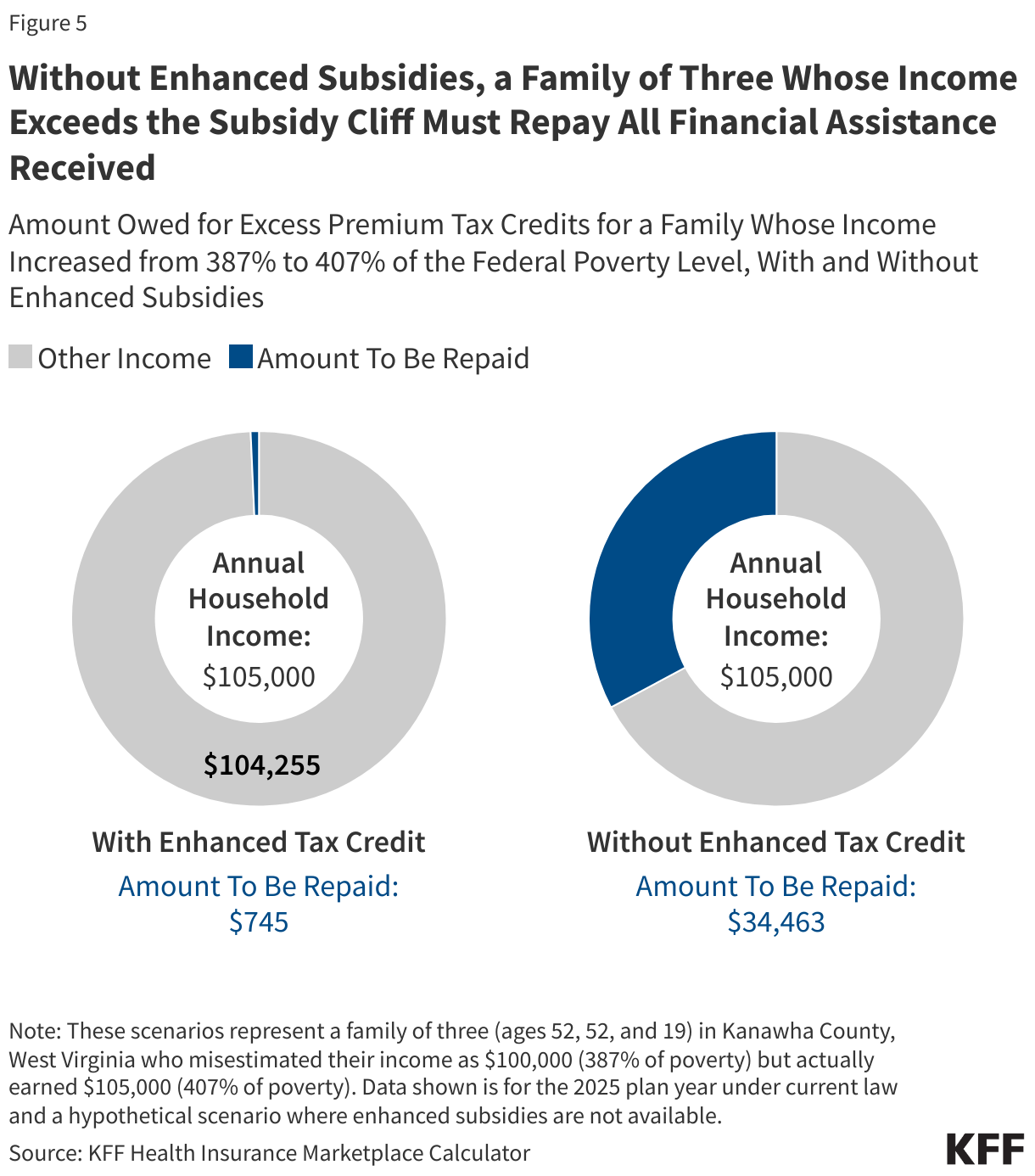

Although repayment caps do not apply to households with incomes above 400% of FPL ($60,240 for an individual in 2025), the enhanced premium tax credits currently limit the amount such enrollees may need to pay for ACA Marketplace coverage. That is, even if their income exceeds expectations, they may remain eligible for some level of premium subsidy. For example, consider a family of three (aged 52, 52, and 19) in Kanawha County, WV, who estimated their income at $100,000 (387% FPL) but ultimately earned $105,000 (407% FPL). With the enhanced subsidies, they would receive a $34,463 premium tax credit but would have been eligible for $33,718—a difference of $745. They would be required to repay only the $745 when filing taxes—less than 1% of their annual income. If the enhanced subsidies expire, however, this family’s income above 400% of poverty would disqualify them for any tax credits . By falling off the subsidy cliff, they would be required to repay the entire premium tax credit of $34,463, or about 33% of their annual income.

Methods |

The Survey of Income and Program Participation (SIPP) reports the incomes and other characteristics for households and household members for each month during the year. The annual income used in this analysis approximates the modified adjusted gross income used to determine eligibility for premium tax credits. Total personal income during the reference year was summed up for each member of the family, except from the following sources:

The estimated annual income of each family, based on its reported household income during the first three months of the year, was compared to the actual annual income of the family at the end of the year to see how well the early year income predicted the annual amount. Families where the annual income predicted by the first three months was either 20 percent below or above the actual annual amount were considered to have “high income volatility.” Families were defined by SIPP and included in the analysis if they had data for 12 months, had at least one adult whose annual earned income exceeded $1000, and whose reference person was at least 15 years old; adults within a family were also required to have 12 months of data. The income to poverty ratio (%FPL) was calculated using the 2022 federal poverty guidelines and the estimated annual income from the first three months of the year. |