Coverage for Abortion Services and the ACA

Issue Brief

The Patient Protection and Affordable Care Act (ACA) makes significant changes to health coverage for women by expanding access to coverage and broadening the health benefits that many will receive. In January 2014 the coverage expansions to assist uninsured individuals gain access to coverage took effect. The issue of abortion coverage was at the heart of many debates in the run up to the passage of the law and continues to the present day. This brief reviews current federal and state policies on Medicaid and insurance coverage of abortion services, and presents national and state estimates on the availability of abortion coverage for women who are newly eligible for Medicaid or private coverage as a result of the ACA.

Impact of the Affordable Care Act on Health Coverage for Women

Signed into law on March 23, 2010, the ACA is a federal law that aims to ensure that U.S. citizens and legal residents have health insurance by requiring most individuals to obtain a minimum level of insurance coverage. This is to be achieved through a combination of public and private insurance expansions. The ACA was designed to expand health care coverage to the poorest uninsured by extending Medicaid eligibility to all qualifying individuals with incomes up to 138% of the Federal Poverty Level (FPL).1 The 2012 Supreme Court ruling, however, had the effect of giving states the option to expand their Medicaid programs rather than requiring this expansion, as was the design of the ACA. As of September 2014, 27 states and the District of Columbia have expanded Medicaid eligibility, but 23 states have not,2 leaving millions of poor individuals without a pathway to affordable coverage.3

The ACA also includes reforms that aim to make insurance more affordable and accessible. Individuals with incomes above the federal poverty level will be able to obtain insurance through healthcare Marketplaces, also known as exchanges, which will offer a variety of plans from which they can purchase insurance. To help those with low and moderate incomes with the costs of insurance, the federal government will provide subsidies (in the form of premium tax credits) to eligible individuals and families with incomes between 100% and 400% FPL.4 All plans offered on the Marketplace must provide coverage for 10 Essential Health Benefits (EHB). Abortion services, however, are explicitly excluded from the list of EHBs that all plans are required to offer. Under federal law, no plan is required to cover abortion.

Federal and State Laws Regarding Coverage of Abortion Services

Since 1977, federal law has banned the use of any federal funds for abortion, unless the pregnancy is a result of rape, incest, or if it is determined to endanger the woman’s life. This rule, also known as the Hyde Amendment, is not a permanent law; rather it has been attached annually to Congressional appropriations bills, and has been approved every year by the Congress. The Hyde Amendment initially affected only funding for abortions under Medicaid, but over the years, its reach broadened to limit federal funds for abortion for federal employees and women in the Indian Health Service. Until recently, insurance coverage of abortion for women in the military had been even more restricted so that pregnancies resulting from rape or incest were not covered. In early 2013, an amendment to the National Defense Authorization Act expanded insurance coverage for servicewomen and military dependents to include abortions of pregnancies resulting from rape or incest, as permitted in other federal insurance policies.5 Federal funds cannot be used to pay for abortions in other circumstances, and abortions can only be performed at military medical facilities in cases of life endangerment, rape or incest.

State level policies also have a large impact on how insurance and Medicaid cover abortions, particularly since states are responsible for the operation of Medicaid programs and insurance regulation. The Medicaid program serves millions of low-income women and is a major funder of reproductive health services nationally. Approximately two-thirds of adult women on Medicaid are in their reproductive years.6 As discussed earlier, the federal Hyde Amendment restricts state Medicaid programs from using federal funds to cover abortions beyond the cases of life endangerment, rape, or incest. However, if a state chooses to, it can use its own funds to cover abortions in other circumstances. Currently, 17 states use state-only funds to pay for abortions for women on Medicaid in circumstances different than those federal limitations set in the Hyde Amendment.7 In 32 states and the District of Columbia, Medicaid programs do not pay for any abortions beyond the Hyde exceptions (Appendix 1). South Dakota limits coverage to cases of life endangerment for the woman, in apparent violation of federal law.

The ACA reinforces the current Hyde Amendment restrictions, continuing to limit federal funds to pay for pregnancy terminations that endanger the life of the woman or that are a result of rape or incest (Table 1). State Medicaid programs continue to have the option to cover abortions in other circumstances using only state funds and no federal funds. President Obama issued an executive order as part of health reform that restated the federal limits specifically for Medicaid coverage of abortion.8 The law also explicitly does not preempt other current state policies regarding abortion, such as parental consent or notification, waiting period laws or any of the abortion limits or coverage requirements that states have enacted.

| Table 1: Summary of Abortion Provisions in the Patient Protection andAffordable Care Act (P.L. 111-148) | |

| Benefit Design |

|

| Financing |

|

| State Role |

|

| Discrimination/ Protection |

|

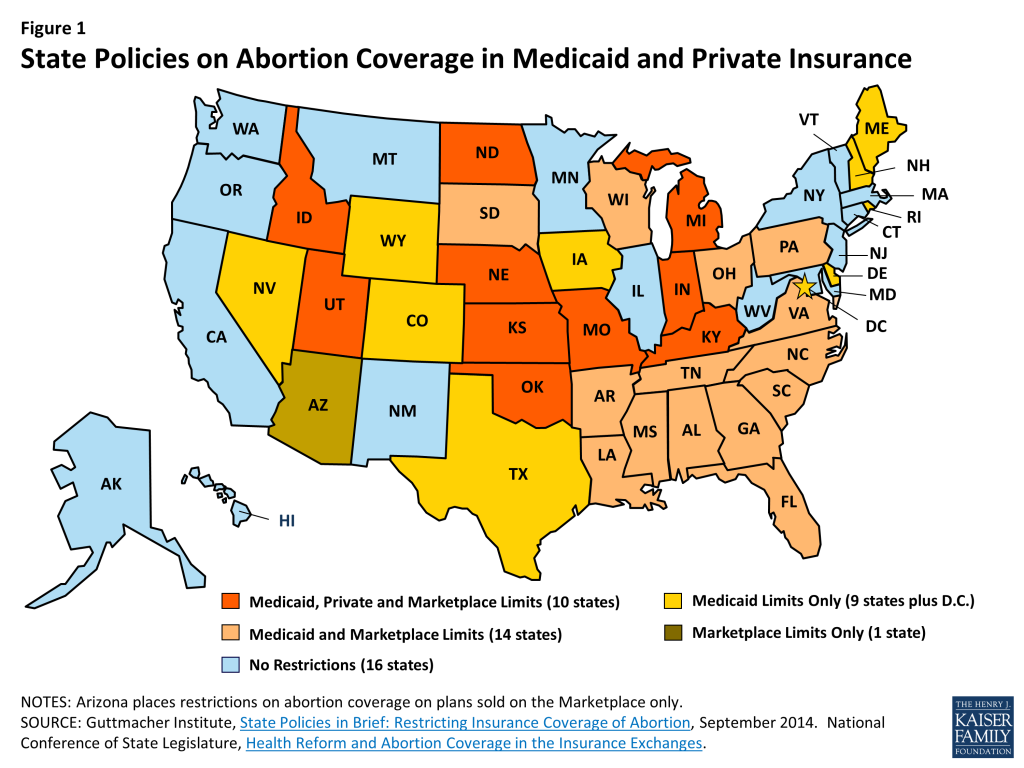

In the private insurance sector, where states have the authority to regulate plans that are issued in the state, 10 states impose restrictions on the circumstances under which insurance will cover abortions in Medicaid, Marketplace plans, and private insurance (Figure 1 and Appendix 1). Some states follow the same restrictions as the federal Hyde Amendment for their private plans, while some are more restrictive. Idaho has exceptions for cases of rape, incest, or to save the woman’s life for plans sold on the Marketplace, but limits abortion coverage to cases of life endangerment to the woman for all other private plans issued in the state. Utah has exceptions to save the life of the mother or avert serious risk of loss of a major bodily function, if the fetus has a defect as documented by a physician that is uniformly diagnosable and lethal, and in cases of rape or incest. However, six states (Kansas, Kentucky, Missouri, Nebraska, North Dakota, and Oklahoma) have an exception only to save the woman’s life for all private plans. Michigan allows abortion coverage in cases of life endangerment to a woman and when the abortion increases the probability of a live birth or preserves the life or health of the child after live birth, such as in cases involving a reduction, or multi-fetal pregnancy.9 Five states had these laws on the books prior to the ACA, and five more states have passed new laws banning private plan coverage post-ACA. While nine of these states allow insurers to sell riders for abortion coverage on the private market, there is little evidence about their availability and no documentation of their cost or impact on access. Utah does not allow riders to be sold for abortion coverage.

Because the ACA explicitly prohibits states from including abortion in any essential benefits package, states or insurers offering plans in a state Marketplace will not be required to offer abortion coverage. The ACA also stipulates that at least one multi-state plan that must limit abortion coverage to those permitted by current federal law. States can also pass laws that bar all plans participating in the state Marketplace from covering abortions, which 25 states have done since the ACA was signed into law in 2010. Most states include narrow exceptions for women whose pregnancies endanger their life or are the result of rape or incest, but two states (Louisiana and Tennessee) do not provide for any exceptions.10 The ACA prohibits plans in the state Marketplaces from discriminating against any provider because of “unwillingness” to provide abortions.

In states that do not bar coverage of abortions on plans available through the Marketplace, insurers may offer a plan that covers abortions beyond the federal limitations, but this coverage must be paid for using private, not federal, dollars. Plans must notify consumers of the abortion coverage as part of the summary of benefits and coverage explanation at the time of enrollment. The ACA outlines a methodology for states to follow to ensure that no federal funds are used towards coverage for abortions beyond the Hyde limitations. Any plan that covers abortions beyond Hyde limitations must estimate the actuarial value of such coverage by taking into account the cost of the abortion benefit (valued at least $1 per enrollee per month). This estimate cannot take into account any savings that might be achieved as a result of the abortions (such as prenatal care or delivery).11

Furthermore, the federal rules stipulate that plans that offer abortion coverage and receive federal subsidies (it is believed that all plans in the state Marketplace will receive at least some federal subsidies) need to collect two premium payments, so that the funds go into separate accounts. One payment would be for the value of the abortion benefit and the other payment would be for the value of all other services. The funds are to be deposited in separate allocation accounts, overseen for compliance by state health insurance commissioners. If a state has multi state plans on the marketplace, then at least one of those plans must limit abortion coverage to the Hyde Amendment restrictions.12 In 2014, of the 150 multi-state plans, two offered coverage of abortion beyond the Hyde restrictions. Both of these plans were offered only in Alaska.13

The Availability of Abortion Coverage to Women Newly Eligible Under the ACA

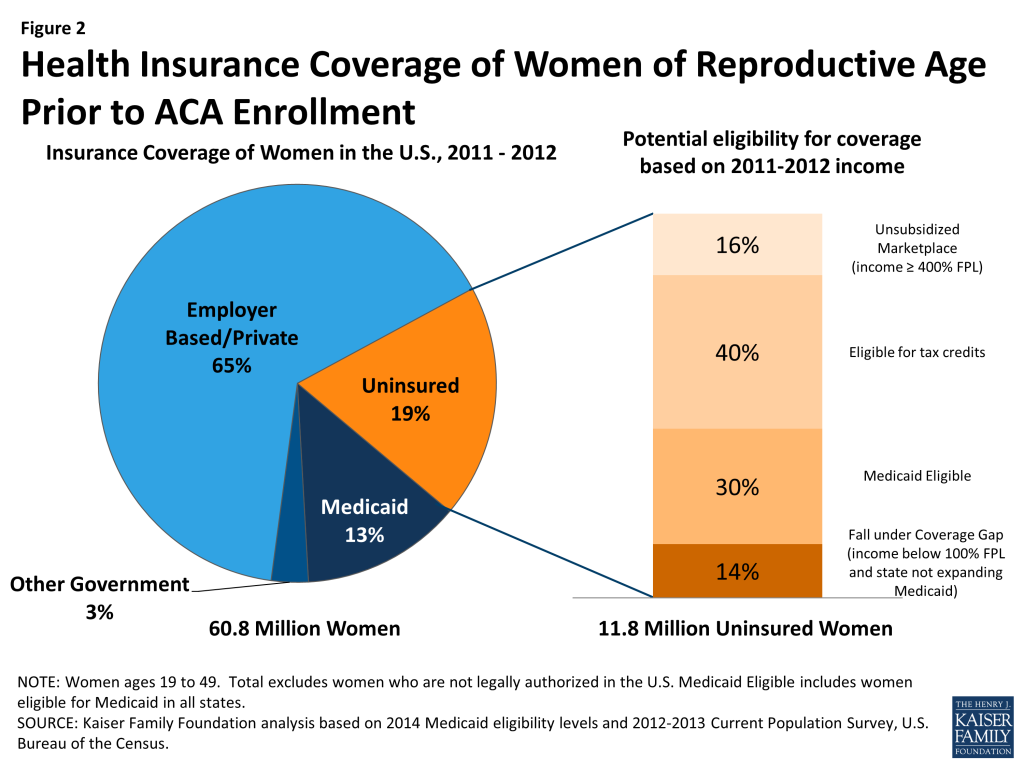

The ACA intended to increase affordability of health insurance and extend coverage to uninsured individuals through a number of changes to the insurance market, including expansion of Medicaid to include individuals with incomes up to 138% FPL, the creation of the state Marketplaces, and the availability of premium subsidies for low to moderate income individuals and families. However, due to a 2012 Supreme Court decision, Medicaid expansion is now optional for states; currently 23 states have not implemented Medicaid expansion. Women in these states who do not meet traditional Medicaid eligibility requirements and whose incomes are below 100% FPL are not eligible for Medicaid, and do not qualify for subsidies on the Marketplace, effectively creating a coverage gap.14 Using survey data prior to ACA enrollment (from 2011/2012) and applying current state Medicaid and Private insurance policies, one is able to get an estimate of the number of uninsured women who would be eligible for coverage in today’s health insurance market . In 2011/2012, there was an average of 11.8 million uninsured women of reproductive age (ages 19 to 49) legally residing in the United States (Figure 2). Of these uninsured women, an estimated 3.4 million (29%) qualify for Medicaid or have been eligible, but had not previously enrolled in the program (Figure 2). About 4.8 million women (40%) have incomes between 100 – 400% of the Federal Poverty Level (FPL) and qualify for subsidies in the form of tax credits if they obtain coverage through their state Marketplace. About 1.8 million uninsured women with incomes at or above 400% of FPL are eligible to obtain coverage on the state Marketplace or through the individual market, but do not qualify for subsidies because their income is too high. Finally, an estimated 1.7 million uninsured women fall into the so-called “coverage gap” because they live in one of the 23 states that is not expanding Medicaid and their income is below 100% FPL, leaving them ineligible for subsidies to purchase coverage on the health care Marketplace under the law.15 , 16

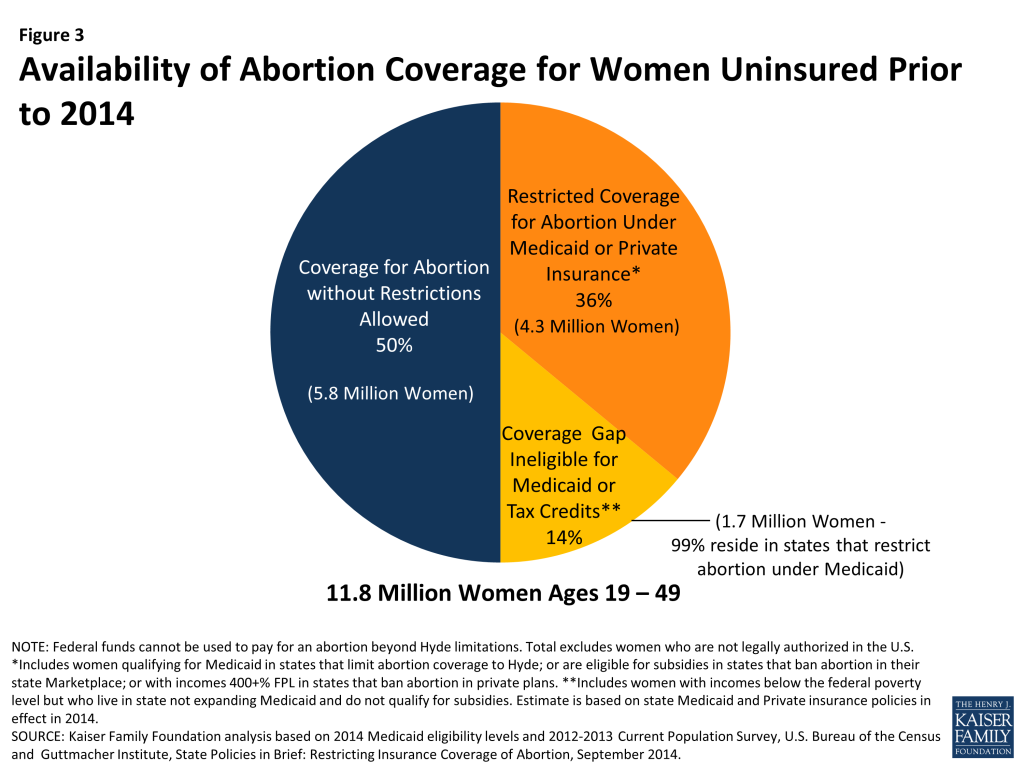

Because of the Hyde Amendment rules and the state laws that govern coverage of abortion services in private plans, the availability of abortion coverage varies across the states among the women who are newly eligible for Medicaid and private coverage. Of the estimated 11.8 million women who are uninsured and legally present in the United States, half (50%) have been eligible to enroll in a Medicaid plan or private insurance plan that does not limit the scope of coverage for abortion services if they wish (Figure 3). Over one third, 4.3 million women, live in a state where state policy limits the availability of coverage for abortion services in private or Medicaid plans to pregnancies that result from rape or incest or are a medical threat to a woman’s life as in the Hyde Amendment or, in the case of some states, even more limited circumstances, such as only in the case of life endangerment. About 1.7 million women (14%) are in the Medicaid coverage gap and do not have access to affordable coverage, either to Medicaid or subsidies, because their state did not expand Medicaid and their incomes are too low to qualify for tax credits under the law. Out of the 23 states not expanding Medicaid, 21 are states that follow the Hyde Amendment. Two states, Montana and Alaska, use state-only funds to cover abortions beyond the Hyde limits but are not expanding Medicaid eligibility. As a result, nearly all of the women in the coverage gap states (99%) would have restricted availability of abortion coverage under Medicaid even if their state were to broaden eligibility.

Women who seek an abortion but do not have coverage for the service need to shoulder the out-of-pocket costs of the services. The cost of an abortion varies depending on factors such as location, facility, timing, and type of procedure. A clinic-based abortion at 10 weeks’ gestation is estimated to cost between $400 and $550, whereas an abortion at 20-21 weeks’ gestation is estimated to cost $1,100-$1,650 or more.17 Though the vast majority (~90%) of abortions are performed early in pregnancy, the costs could be economically challenging for many low-income women.18 Approximately 5% of abortions are performed at 16 weeks or later in the pregnancy.19 For women with medically-complicated health situations or who need a second-trimester abortion, the costs could be prohibitive. In some cases, women may have to delay their abortion while they have time to raise funds20 , or women may first learn of a fetal anomaly in the second trimester when the costs are considerably higher.21

Conclusion

While millions of women have gained health insurance coverage as a result of the ACA insurance expansions, many are enrolled in insurance plans that restrict the circumstances in which abortion services will be covered. As a result of state actions to limit coverage of abortion in the Marketplace plans and federal law limiting abortion coverage under Medicaid, over one third of women who were newly eligible for coverage are limited to enrollment in a plan that restricts abortion coverage to Hyde restrictions or, in some states, more restrictive circumstances. Half of women of reproductive age who are legally residing in the U.S. qualify for coverage in plans that do not have limitations, and 14% are in the coverage gap and have not been able to qualify for Medicaid or affordable coverage.

These coverage limitations are occurring at a time when many states are taking other actions to curtail access to abortion through multiple fronts. These efforts include state level legislation that focuses on the doctors and clinics that provide abortion services to women. Some state legislatures are enacting laws that expand the regulatory requirements on abortion clinics, place gestational limits on when women can have abortions, include new rules for women to have ultrasounds and multiple visits, and impose new regulations on clinicians such as requiring them to have hospital admitting privileges.22 In addition, legislative activity has focused on prohibiting certain providers and clinics that perform abortions from qualifying for any public financing, including Title X allotments and Medicaid funds, even when those funds are specifically required to be used for other services such as family planning and other preventive services and not abortions.

The impact of the abortion coverage restrictions is disproportionately felt by poor and low-income women who have limited ability to pay for abortion services with out-of pocket funds. The effect of the absence of abortion coverage could be magnified by laws that have been enacted in some states requiring that additional services, such as sonograms, be performed before all abortions or by the multiple visits and waiting periods that are required in some states which will result in increased costs of abortion procedures and higher travel costs. These requirements, along with policies that increase the regulations on clinics and providers, can have the expected result of limiting access to and the availability of abortion services in some states, especially for low-income women.

In the coming years as the ACA is implemented, the laws that are enacted at the federal and state level as well as the choices that are made by insurers, employers, and policy holders will ultimately determine the extent of abortion coverage that will be available to women across the nation.

The authors would like to thank Anthony Damico for assistance with data analysis.

Appendix

| Appendix 1: Scope of Abortion Coverage in Medicaid and in Private Plans, By State | ||||||

| State | States with No MedicaidExpansion | States with Medicaid Expansion and Restricting Abortion Coverage to Hyde Rules | State Law Restricting Abortion Coverage to Limited Circumstances in Marketplace Plans | State Law Limiting Abortion on Private InsuranceIssued in the State | Total Number of Uninsured Women ages 19 to 49 (2012-2013) | Percent of Uninsured Women in the Coverage Gap or Eligible for Medicaid or Private Plans that Restrict Abortion Coverage, by State (2012-2013) |

| Grand Total | 23* | 13 | 25 | 10 | 11.8 million | 50% |

| Alabama | X | X | 190,661 | 87% | ||

| Alaska | X | 30,960 | 15% | |||

| Arizona | X | 233,855 | 29% | |||

| Arkansas | X | X | 160,494 | 89% | ||

| California | 1,479,007 | 0% | ||||

| Colorado | X | 180,735 | 47% | |||

| Connecticut | 70,518 | 0% | ||||

| Delaware | X | 20,207 | 54% | |||

| DC | X | 12,631 | 69% | |||

| Florida | X | X | 947,741 | 82% | ||

| Georgia | X | X | 517,898 | 86% | ||

| Hawaii | 21,261 | 0% | ||||

| Idaho | X | X | X | 75,854 | 100% | |

| Illinois | 393,032 | 0% | ||||

| Indiana | X | X | X | 242,016 | 100% | |

| Iowa | X | 79,787 | 54% | |||

| Kansas | X | X | X | 94,608 | 100% | |

| Kentucky | X | X | X | 191,284 | 100% | |

| Louisiana | X | X | 258,491 | 93% | ||

| Maine | X | 31,808 | 26% | |||

| Maryland | 179,405 | 0% | ||||

| Massachusetts | 56,534 | 0% | ||||

| Michigan23 | X | X | X | 304,977 | 100% | |

| Minnesota | 110,194 | 0% | ||||

| Mississippi | X | X | 128,006 | 95% | ||

| Missouri | X | X | X | 239,709 | 100% | |

| Montana | X | 50,331 | 29% | |||

| Nebraska | X | X | X | 53,191 | 100% | |

| Nevada | X | 148,567 | 52% | |||

| New Hampshire | X | 39,288 | 24% | |||

| New Jersey | 276,254 | 0% | ||||

| New Mexico | 113,877 | 0% | ||||

| New York | 587,307 | 0% | ||||

| North Carolina | X | X | 411,742 | 84% | ||

| North Dakota | X | X | X | 17,046 | 100% | |

| Ohio | X | X | 375,764 | 93% | ||

| Oklahoma | X | X | X | 180,106 | 100% | |

| Oregon | 160,392 | 0% | ||||

| Pennsylvania | X | X | 378,798 | 81% | ||

| Rhode Island | X | 32,024 | 51% | |||

| South Carolina | X | X | 199,734 | 89% | ||

| South Dakota** | X | X | 30,435 | 90% | ||

| Tennessee | X | X | 207,923 | 80% | ||

| Texas | X | 1,434,290 | 37% | |||

| Utah | X | X | X | 100,442 | 100% | |

| Vermont | 11,872 | 0% | ||||

| Virginia | X | X | 258,342 | 82% | ||

| Washington | 247,674 | 0% | ||||

| West Virginia | 86,105 | 0% | ||||

| Wisconsin | X | X | 125,212 | 82% | ||

| Wyoming | X | 22,132 | 31% | |||

| NOTES: Women ages 19 to 49; Pennsylvania is implementing Medicaid expansion starting January 2015. Indiana and Utah indicated that they are planning on moving forward with Medicaid expansion post-2014. *All 23 states except Montana and Alaska limit Medicaid coverage of abortion to the Hyde Amendment.**South Dakota violates federal law by only providing abortions in cases of life endangerment for Medicaid beneficiaries.SOURCES: Kaiser Family Foundation State Health Facts; Guttmacher Institute State Policies in Brief, Overview of Abortion Laws ; Analysis of the coverage gap and abortion coverage based on data from Kaiser Family Foundation/Urban Institute estimates of ASEC supplement to March 2012 and March 2013 Current Population Surveys, U.S. Bureau of the Census. Methods available | ||||||

Endnotes

- Legislation extends Medicaid coverage to all individuals with incomes up to 133% of the poverty level (FPL) and includes a provision to disregard first 5% of income, effectively extending Medicaid to all individuals with incomes up to 138% FPL. ↩︎

- Kaiser Family Foundation, Status of State Action on the Medicaid Expansion Decision, Updated August 28, 2014. Currently, 23 states have not expanded Medicaid, though many states are looking to expand Medicaid in the future. Indiana has an expansion plan pending, while Utah is in negotiation with CMS on its plan. Tennessee, Wyoming, and Maine are also considering expansion. ↩︎

- Kaiser Family Foundation, The Coverage Gap: Uninsured Poor Adults in States that Do Not Expand Medicaid, March 2014. ↩︎

- Kaiser Family Foundation, State-by-State Estimates of the Number of People Eligible for Premium Tax Credits Under the Affordable Care Act, November 2013 ↩︎

- Senator Shaheen, “Shaheen Amendment Signed into Law” January 3, 2013 ↩︎

- Kaiser Family Foundation, Medicaid’s Role for Women Across the Lifespan, December 2012 ↩︎

- Guttmacher Institute, State Policies in Brief: State Funding of Abortion Under Medicaid, September 2014 ↩︎

- The White House Office of the Press Secretary, Executive Order – Patient Protection and Affordable Care Act’s Consistency with Longstanding Restrictions of the Use of Federal Funds for Abortion, March 24, 2010 ↩︎

- Michigan, Act 182: Abortion Insurance Opt Out Act ↩︎

- Guttmacher Institute, State Policies in Brief: Restricting Insurance Coverage of Abortion, September, 2014 ↩︎

- The Patient Protection and Affordable Care Act, Section 1303 Special Rules ↩︎

- 45 CFR § 800.602: Consumer choice with respect to certain services ↩︎

- Office of Personnel Management, Letter to Representative Chris Smith, November 8, 2013 ↩︎

- Wisconsin has not formally expanded Medicaid under the ACA, but extends coverage to adults up to 100% of FPL. Wisconsin does not have a coverage gap. ↩︎

- Ibid. ↩︎

- For a discussion of the methods used to derive the estimates of women in the coverage gap and eligible for tax credits see: KFF, The Coverage Gap: Uninsured Poor Adults in States that Do Not Expand Medicaid and KFF, State-by-State Estimates of the Number of People Eligible for Premium Tax Credits Under the Affordable Care Act. The estimates of the availability of abortion coverage were derived using a two-step process. 1) Using state level estimates we classified the number of uninsured women of reproductive age (19 to 49) legally residing in the United States in 2011/2012 into four groups: those who were eligible for Medicaid, tax credits, had incomes below poverty and resided in a state that was not expanding Medicaid (coverage gap), or had incomes that were at or above 400% of the federal poverty level. 2) These calculations were then used to estimate the number of women with differing levels of abortion coverage based on whether or not their state permitted the use of state only funds to pay for abortions beyond the Federal Hyde limitations; enacted laws that banned coverage on the plans available through the state Marketplace beyond limited circumstances; and those enacting similar legislation affecting private plans available in the state. The number of women with limitations in the scope of abortion coverage or who were in the insurance coverage gap was summed and divided by the number of uninsured women who were legally residing the state. The policies used to determine the availability of abortion coverage were based on those collected by the Guttmacher Institute and available in: State Policies in Brief: Overview of Abortion Laws, September 2014. ↩︎

- Jones, R and K Kooistra. (2011). Abortion Incidence and Access to Services in the United States, 2008. Perspectives on Sexual and Reproductive Health 43(1), 41-50. ↩︎

- Guttmacher Institute. State Policies in Brief, Overview of Abortion Laws, September 2014 ↩︎

- Guttmacher Institute, Facts on Induced Abortion in the United States, July 2014 ↩︎

- Ibid. ↩︎

- National Journal, “Should Mothers Be Forced to Bear Disabled Children Against Their Will?”, October 2013 ↩︎

- Jones, R. and K. Kooistra. (2011). Abortion Incidence and Access to Services in the United States, 2008. Perspectives on Sexual and Reproductive Health 43(1): 41-50. ↩︎

- Michigan, Act 182: Abortion Insurance Opt Out Act ↩︎