Renewals in Medicaid and CHIP: Implementation of Streamlined ACA Policies and the Potential Role of Managed Care Plans

Introduction

In addition to expanding the Medicaid program to cover low-income adults, the Affordable Care Act (ACA) established new modernized, streamlined enrollment and renewal rules for Medicaid and CHIP that are designed to create a coordinated, “no wrong door” system and keep individuals enrolled for as long as they are eligible. States must implement these new policies regardless of whether they adopt the Medicaid expansion to low-income adults.

While much attention has been focused on enrollment efforts, this brief reviews the new renewal requirements for Medicaid and CHIP that are designed to maintain continuity of coverage for eligible individuals. It provides an overview of state implementation of the new renewal policies and considers the potential role managed care plans can play in supporting renewals. Key findings include:

- While states have made significant progress implementing new enrollment processes, some aspects of the simplified renewal policies have not yet been fully implemented due to a range of challenges.

- While many states have been delayed in implementing the streamlined renewal policies, some states, including Washington and Rhode Island, have successfully implemented the new policies and achieved high retention rates with more than nine in ten enrollees successfully renewed.

- Managed care plans can support renewals by reminding members to renew and providing direct assistance with the renewal process. However, plans identified challenges to supporting renewal, including lack of accurate data on member renewal dates; concerns about how marketing guidelines apply to renewal outreach; and lack of clear guidance, expectations, and financial support from states for plans’ role in supporting renewals.

Issue Brief

Medicaid and CHIP Renewals under the ACA

Effective renewal processes are important for maintaining the coverage gains that have been achieved under the ACA to date, supporting access to care, and promoting administrative efficiency. There is substantial evidence demonstrating the negative effects of “churning” on and off of health coverage, including health consequences and increased medical costs resulting from disruptions in care as well as administrative delays and inefficiencies for families, providers, health plans and states. Research over the years has confirmed that a significant number of enrollees who lose coverage at renewal remain eligible and return to Medicaid within the same year.1

The ACA established new simplified renewal rules for Medicaid and CHIP designed to keep individuals enrolled for as long as they are eligible. In March 2012, the Centers for Medicare & Medicaid Services published federal regulations that outlined new renewal processes for states to promote continuity of coverage as envisioned by the ACA.2 The regulations were informed by prior state successes reducing administrative burdens on families in renewing Medicaid and CHIP coverage and built on longstanding policy and regulations that limit information states can collect to renew Medicaid eligibility.3 The regulations take into account the availability of new technology, the enhanced ability to conduct electronic matches with state databases, and the creation of a federal data services hub that allows states to conduct real-time electronic data matches against federal data sets.4

The new renewal processes are designed to minimize the information requested from families and support transitions to other coverage. Following are the new renewal processes for individuals determined eligible for Medicaid or CHIP based on modified adjusted gross income (MAGI) (see Appendix A for details):

- States must first seek to renew eligibility on an ex parte basis, which does not require any action from the enrollee. To complete an ex parte renewal, states check all available data sources to confirm if eligibility can be renewed without contacting the family. The state then sends a notice informing the enrollee of his or her continued eligibility. If nothing has changed, the enrollee does not need to sign or return the notice.

- If an ex parte renewal cannot be achieved, states must provide enrollees with a pre-populated form that includes information available to the agency and requests any additional information needed to renew eligibility. Individuals must sign and return the form with any additional information required to complete renewal.

- If an individual does not complete his or her renewal, states must provide at least a 90-day reconsideration period after coverage ends. During this period, individuals can provide the necessary information to continue coverage without submitting a new application.

- When an individual is found no longer eligible for Medicaid or CHIP, states must assess or determine eligibility for Marketplace coverage, and electronically transfer the account to the Marketplace if an individual is assessed as potentially eligible.

Eligibility may only be re-determined once every 12 months unless the state has information provided by the beneficiary or through data sources indicating changes in circumstances that may affect eligibility.5 Individuals are required to report changes that might affect their eligibility,6 and states must enable families to report changes in a timely manner and promptly address any changes. 7 The rules also no longer permit states to require an in-person interview at either enrollment or renewal.8

State Implementation of Streamlined Renewal Policies

States prioritized implementing streamlined enrollment processes, which led to delays in implementing new renewal procedures in most states. In order to implement the new ACA enrollment and renewal policies, many states needed to make significant upgrades to their eligibility and enrollment systems. CMS facilitated these efforts by providing an enhanced federal Medicaid matching rate for systems work.9 However, many states faced challenges completing their system builds and upgrades prior to implementation of the ACA and had to prioritize their policy changes in conjunction with system functionality decisions. Initially, states and the federal government focused heavily on implementing streamlined enrollment processes and establishing coordination between Medicaid and Marketplace coverage. As a result, most states were delayed in their ability to focus on implementation of the new renewal procedures. Recognizing this challenge, and the large scope of work facing states with enrollment under the coverage expansions and changes in the eligibility rules, CMS offered states the opportunity to temporarily delay renewals for existing Medicaid or CHIP enrollees, a strategy that 36 states adopted during 2014. While a number of these states had completed all delayed renewals by 2015, others extended these delays into 2015.10

Many states are still transitioning to the streamlined renewal processes due to a range of challenges. For example, states needed to migrate data for existing Medicaid and CHIP enrollees from old legacy systems to their new MAGI-based eligibility systems. Moreover, states were not able to conduct ex parte renewals for existing Medicaid enrollees since they needed to collect additional information – including MAGI-based income and tax filing household information – which they did not have on file for these individuals to conduct determinations based on the new MAGI-based rules. Finally, states were still developing systems capacity to process ex parte renewals and produce pre-populated forms and notices for individuals.

Given these challenges, CMS worked with states to develop interim mitigation strategies and utilize flexibility to facilitate renewals. Specifically, states can use simpler “non-filer” tax rules to calculate ongoing eligibility for existing Medicaid enrollees. They also can receive approval to conduct renewals using data from the Supplemental Nutritional Assistance Program (SNAP or food stamps) and to accept self-attestation that a family’s income and other circumstances have not changed.11 A number of states took up these strategies as part of their mitigation plans and, to date, there have not been any substantial downward trends in enrollment data that would suggest coverage losses due to problems with renewals.12 CMS reports that most states have now implemented or are in the process of implementing pre-populated renewal forms, and most states expect to have the full ability to conduct ex parte renewals during 2015.13 However, renewals remain a concern in some states.

In May 2013 guidance, CMS reiterated that states may adopt 12-month continuous eligibility for parents and other adults through Section 1115 waiver authority, but states have not taken up this option. One effective strategy for promoting continuity of Medicaid and CHIP coverage and minimizing administrative burdens and costs is to provide 12 months of continuous eligibility, regardless of changes in family circumstances. This policy has been available as a state option for children enrolled in Medicaid and/or CHIP since 1997 and can be implemented under Medicaid section 1115 waiver authority for parents and other adults. When CMS reiterated the waiver opportunity, it clarified that, because some newly eligible adults who qualify for an enhanced federal matching rate might have become ineligible at some point in the year, a financial adjustment would be applied to these “newly eligible” adults. Under the adjustment, 97.4% of the 12 months of coverage for each enrollee would be matched at the enhanced rate, and 2.6% of the enrollee months would be matched at the regular match rate.14 To date, New York is the only state that has taken up this option. Limited state interest may reflect less perceived need for 12-months continuous eligibility because of the shift toward real-time eligibility and streamlined renewal policies. States may also have reservations about the financial adjustment.

Examples of State Successes with New Renewal Policies

While many states have been delayed in implementing the new streamlined renewal policies, some states, including Washington and Rhode Island, which have been long-time leaders in adopting renewal simplification strategies for children, have already achieved significant success implementing the new policies based on information reported by state officials, as described below.15

Washington

Prior to the ACA, Washington had a largely manual renewal process. Most renewals were completed by an enrollee returning a paper renewal form and attaching documentation to verify current wages. Renewal forms were sent out 45 days prior to the renewal date and were manually reviewed and completed by eligibility staff.

Today, Washington primarily relies on a process it calls “auto-renewal.” The state first conducts an electronic data match with available data sources (from the Internal Revenue Service and the state’s more timely quarterly wage database) to confirm continued eligibility. If the data match is successful, 60 days before the renewal date, the state sends a pre-populated form informing the individual of continued eligibility and providing an opportunity to update information. If nothing has changed, the individual does not need to return the form to continue coverage. If the data match is not successful, the state requests the additional information needed to complete the renewal. If an individual does not complete the renewal and is within the 90-day reconsideration period, he or she can renew in real-time by going on-line or calling the state’s customer service center.

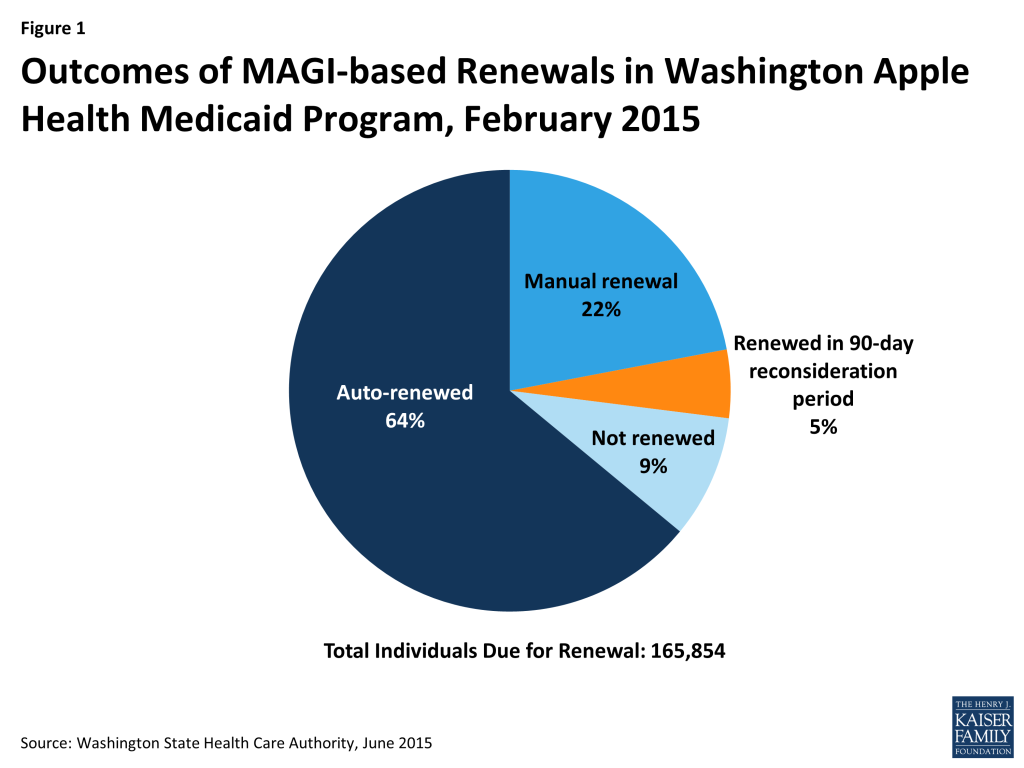

Two-thirds of MAGI-based enrollees are now renewed through ex parte processes and overall retention rates have increased to above 90% in Washington. About two-thirds of the Washington’s MAGI-based enrollees (children, pregnant women, parents, and expansion adults) qualify for auto-renewal. Overall, more than eight in ten individuals are successfully renewed during their 12-month eligibility period through both auto-renewals and manual renewals, for which families must submit additional information. An additional 5% of renewals are completed during the 90-day reconsideration period. The state reported an overall retention rate of 91% as of February 2015, after taking into account those renewing during the reconsideration period (Figure 1).

Rhode Island

Building on previous success with adopting innovative practices and efficient processes, Rhode Island has also achieved a high Medicaid retention rate of 94%. The Rhode Island Executive Office of Health and Human Services sends out a pre-populated renewal form to every MAGI Medicaid beneficiary who is coming up for renewal 60 days in advance of the renewal date. The pre-populated form includes all of the information known to the state, including the results of electronic data matching conducted immediately before sending the forms. Rhode Island reports that two-thirds of the renewal forms do not request any additional information and, in those cases, families are renewed without having to take any action if nothing has changed. For the remaining one-third of cases that request information or documentation, the state asks for the information to be returned within 15 days.16 Thirty days before the renewal date, the state sends notices to all households notifying them of their renewal and any change in eligibility category.

Leveraging Managed Care Plans to Support Renewals

Managed care plans can play a key role in supporting renewals given their ongoing relationship with enrollees. Information collected from 14 plans in 9 states (CA, CO, MA, NY, OH, RI, TX, VA, and WA) by the Association for Community Affiliated Plans and follow-up telephone interviews conducted with four health plan representatives identified both promising examples of how managed care plans can facilitate renewals, as well as challenges to maximizing the potential of this role.

Plans identified a range of strategies they have employed to educate and remind members about renewal. Several plans reported that they conduct live or automated calls to let members know that their renewal date is approaching, send reminder postcards, and are starting to use newer communication strategies like text messages. In addition, some plans reported including reminders in member newsletters about the importance of watching for and responding to mail from the state, making sure mailboxes are accessible, and providing a number to call if assistance is needed. Some plans indicated that they work with individual providers to remind their patients to renew. For example, plans share renewal dates with primary care providers or community health centers and ask the provider or health center to remind patients about upcoming renewals during visits or through direct outreach by phone or in-person. One plan noted that it has established a partnership with the state human service agency to provide grant funding to community-based organizations to focus on renewal outreach.

A number of plans described more hands-on approaches to assist members with completing their renewals. These included working closely with county eligibility offices to validate eligibility information and renewal dates; the plan acting as a “authorized representative” for the member, enabling the plan to complete the renewal process on the member’s behalf; and assisting members with providing additional information to reinstate coverage if they have not completed a renewal and are in the 90 day reconsideration period.

However, the plans indicated that conducting renewal outreach is sometimes challenging due to lack of accurate data on member renewal dates. The plans indicated that, while state Medicaid agencies generally are willing to provide the plans with eligibility information and renewal dates for their members, the renewal dates are sometimes inaccurate or out-of-date. This can result in confusion for individuals if a plan reminds a member about renewal after the individual has already completed the renewal process. Some plans noted that the information they have on file for their members is often more up-to-date than the state’s data, but that the state will not or cannot update its information based on the plan’s data. Some plans also noted that counties sometimes have more timely information than the state due to their administration of other social services programs. Plans also mentioned that enrollment and renewal dates provided by the state may cover several programs, and sometimes it is not clear which date applies to Medicaid. Further, with the change to new eligibility systems, some states have been temporarily unable to provide information to plans. This issue may be resolved as systems reach full functionality, but, in the short-term, it has created a challenge for plans in conducting renewal outreach.

A number of plans also indicated concerns about how marketing guidelines apply to renewal outreach, particularly since materials must be approved by the state. These perceptions could be due at least, in part, to misunderstanding of how federal rules regarding marketing practices for Medicaid managed care plans may apply to activities designed to facilitate renewal. To clarify these rules, in January 2015, CMS released a set of Frequently Asked Questions (FAQs) that confirm that Medicaid managed care plans may conduct outreach to their enrollees regarding the Medicaid renewal process. As long as outreach to enrollees is directed at “beneficiaries who are currently enrolled with that Medicaid managed care plan, and is not intended to influence the beneficiary to re-enroll in that particular Medicaid managed care plan,” the activity is appropriate. The FAQs further clarify that educational materials emphasizing the importance of completing the state’s Medicaid renewal process in a timely fashion are not considered marketing materials.17 Moreover, the most recent proposed rules for managed care plans issued by CMS in May 2015 include similar assurances confirming the policy outlined in the FAQs.18

In addition, plans reported feeling limited in the ability to provide direct assistance with renewals. Some plans noted that they are encouraged by their state to educate their members about renewal, but that the plan must refer the member back to the county or state to complete the renewal process. One plan reported that their managed care contract specifically prevents the plan from assisting with renewal. Other plans noted that the lack of clear guidance, expectations, and financial support for the plans’ role in facilitating renewals limits their activities.

Conclusion

States have achieved significant progress implementing streamlined enrollment and renewal procedures under the ACA, but there is still more work to be done, particularly in fully implementing new renewal processes to facilitate continuity of coverage. While many states have faced challenges in implementing the new renewal policies, several states, including Washington and Rhode Island, have already experienced success and high retention rates under the new policies. As more states complete the implementation process, it will be important to continue to monitor impacts on retention rates to assess the extent to which they are supporting the ACA’s vision of keeping individuals enrolled for as long as they are eligible. Looking ahead, managed care plans could play a key role in supporting renewals given their ongoing relationship with enrollees, but plans also have identified a range of challenges they face in supporting renewals. Addressing these challenges may bolster plans’ ability to collaborate with states to promote continuity of coverage.

This brief was prepared by Jennifer Ryan of Harbage Consulting and Samantha Artiga of the Kaiser Family Foundation. The authors express their appreciation to Mary Wood, Washington State Health Care Authority; Amy Lapierre, Rhode Island Executive Office of Health and Human Services; Brenda Whittle and Lisa Carcieri, Neighborhood Health Plan of Rhode Island; Carolyn Thon, Health Plan of San Mateo; Michael Nguyen and Gerri Casillas, Health Plan of San Joaquin; and Anne Marie Costello and Sarah deLone, Center for Medicaid and CHIP Services, CMS for their assistance and insights in developing this paper.

Appendix

Appendix A:

Renewal Processes for Medicaid and CHIP under the ACA

Ex parte renewals.19 The state should check all data sources to determine if eligibility can be renewed based on available data without contacting the family. Because the decision is based on reliable data sources, a signed renewal form is not needed. The state must send a notice to the beneficiary informing him or her of continued eligibility and providing the opportunity to correct any inaccurate information, but, if nothing has changed, the individual is not required to sign or return the notice.20 The concept of ex parte renewal is a longstanding federal Medicaid policy, but it had previously been inconsistently applied by states, since many states had limited systems capability to check against data sources and renew eligibility without the enrollee providing information. The broader systems upgrades facilitated by the ACA, coupled with access to electronic verification data, enhanced states’ ability to implement an effective ex parte process.

Pre-populated forms. If an ex parte renewal cannot be achieved, states must provide the enrollee a pre-populated renewal form that includes information available to the agency and requests additional information needed to renew eligibility.21 These pre-populated forms must be provided at least 30 days in advance of the renewal date and must be accepted through multiple modes, including online, by phone, mail and in person.22 Individuals must sign and return the pre-populated renewal form to complete the renewal, and states must provide several signature options, including telephonic signatures, electronic signatures and handwritten signatures that can be transmitted electronically.23 States also are required to provide notices to individuals following completion of the renewal.24

90-day reconsideration period. If an individual does not complete the renewal, states must provide at least a 90-day reconsideration period after the date coverage ends.25 During this period, families have the opportunity to provide the necessary information to continue coverage without being required to complete a new application. Under regulations, retroactive Medicaid coverage is available back to the date coverage ended, although some states have received waivers of retroactive coverage.

Coverage transitions. Prior to terminating Medicaid coverage, the state must consider eligibility through all eligibility pathways (both MAGI and non-MAGI) and assess or determine eligibility for other coverage options including CHIP and Marketplace coverage.26 If the state assesses the individual as potentially eligible for Marketplace coverage, it must electronically transfer that individual’s account to the Marketplace for a complete determination of eligibility.27

Renewals for Non-MAGI groups. There are some differences in renewal rules for elderly and disabled populations whose Medicaid eligibility is determined based on non-MAGI rules.28 Eligibility is renewed at least every 12 months, and ex parte renewal is required if sufficient information is available. States may, but are not required, to use a pre-populated renewal form for these groups. In general, states have delayed systems upgrades for non-MAGI groups, with most planning toward incorporating them into new or upgraded systems in 2016.29

Endnotes

- C. Mann and L. Summer, “Instability of Public Health Insurance Coverage for Children and Their Families: Causes, Consequences, and Remedies,” The Commonwealth Fund, June 2006, available at http://www.commonwealthfund.org/~/media/files/publications/fund-report/2006/jun/instability-of-public-health-insurance-coverage-for-children-and-their-families–causes–consequence/summer_instabilitypubhltinschildren_935-pdf.pdf ↩︎

- Medicaid Program; Eligibility Changes Under the Affordable Care Act of 2010; Final Rule, March 23, 2012, available at http://www.gpo.gov/fdsys/pkg/FR-2012-03-23/pdf/2012-6560.pdf ↩︎

- States may only collect “information that is necessary to determine ongoing eligibility and that relates to circumstances that are subject to change, such as income and residency. States cannot require individuals to provide information that is not relevant to their ongoing eligibility, or that has already been provided with respect to an eligibility factor that is not subject to change, such as date of birth or United States citizenship.” Health Care Financing Administration, Letter to State Medicaid Directors from Tim Westmoreland, April 7, 2000, available at http://downloads.cms.gov/cmsgov/archived-downloads/SMDL/downloads/smd040700.pdf ↩︎

- The hub is designed to provide states and the federal government with coordinated and real-time access to information about applicants, including their quarterly wages, citizenship and immigration status, and other eligibility criteria. ↩︎

- 42 CFR 435.916(a)(1) ↩︎

- With the exception of states that have adopted 12 months continuous eligibility for children in CHIP/Medicaid. ↩︎

- 42 CFR 435.916(c) and (d) ↩︎

- 42 CFR 435.916(a)(3)(iv) ↩︎

- CMS offered states an enhanced 90 percent federal Medicaid matching rate to build new eligibility and enrollment systems and a 75 percent matching rate for upgrading existing systems and supporting ongoing maintenance and operating costs Medicaid Program; Federal Funding for Medicaid Eligibility Determination and Enrollment Activities; Final Rule, April 19, 2011; available http://www.gpo.gov/fdsys/pkg/FR-2011-04-19/pdf/2011-9340.pdf. CMS recently proposed to extend this enhanced match rate on a permanent basis. Letter from Cindy Mann to National Association of Medicaid Directors and the American Public Human Services Association indicating CMS’ intent to publish a proposed regulation that will permanently extend the availability of the 90% and 75% matching funds for E & E systems modernization activities. The letter also discusses an extension of the OMB Circular A-87 waiver that enables states to pursue integrated eligibility systems with other human services programs. October 28, 2014, available at http://www.medicaid.gov/medicaid-chip-program-information/by-topics/data-and-systems/downloads/medicaid-90/10-funding-extension.pdf. The proposed rule is available at http://www.gpo.gov/fdsys/pkg/FR-2015-04-16/pdf/2015-08754.pdf ↩︎

- T. Brooks, J. Touschner, S. Artiga, J. Stephens, A. Gates, “Modern Era Medicaid: Findings from a 50-State Survey of Eligibility, Enrollment, Renewal, and Cost-Sharing Policies in Medicaid and CHIP as of January 2015,” January 20, 2015, available at https://modern.kff.org/health-reform/report/modern-era-medicaid-findings-from-a-50-state-survey-of-eligibility-enrollment-renewal-and-cost-sharing-policies-in-medicaid-and-chip-as-of-january-2015/. ↩︎

- For detailed information about the new renewal options, see Medicaid.gov at http://www.medicaid.gov/state-resource-center/mac-learning-collaboratives/learning-collaborative-state-toolbox/downloads/all-state-call-renewal-refresher-7-31-14.pdf ↩︎

- Medicaid and CHIP enrollment has continued to increase, both in states that have expanded Medicaid and those that have not. For more information see CMS monthly Medicaid/CHIP Application, Eligibility Determination and Enrollment Reports, available at http://www.medicaid.gov/medicaid-chip-program-information/program-information/medicaid-and-chip-enrollment-data/medicaid-and-chip-application-eligibility-determination-and-enrollment-data.html ↩︎

- Author interviews with CMS officials, March and April 2015. ↩︎

- Martha Heberlein, Georgetown Center for Children and Families blog post, “FMAP Guidance on 12-Month Continuous Eligibility for Adults,” February 16, 2014, available at http://ccf.georgetown.edu/all/fmap-guidance-on-12-month-continuous-eligibility-for-adults/ ↩︎

- Author interview with Mary Wood, Director of Eligibility Policy and Service Delivery, Washington State Health Care Authority, April 13, 2015 and follow-up email conversations on May 20 and June 16, 2015 and author interview with Amy Lapierre, Administrator, Rhode Island Executive Office of Health and Human Services, April 16, 2015. ↩︎

- Although individuals have 30 days to respond before termination can take place. ↩︎

- Center for Medicaid & CHIP Services Frequently Asked Questions, January 16, 2015, available at http://www.medicaid.gov/Federal-Policy-Guidance/Downloads/FAQ-01-16-2015.pdf ↩︎

- See 42 CFR Section 438.104 of the May 26, 2015 proposed rule, “Medicaid and Children’s Health Insurance Program (CHIP) Programs; Medicaid Managed Care, CHIP Delivered in Managed Care, Medicaid and CHIP Comprehensive Quality Strategies, and Revisions Related to Third Party Liability; Proposed Rules,” p.31273. Available at http://www.gpo.gov/fdsys/pkg/FR-2015-06-01/pdf/2015-12965.pdf. ↩︎

- 42 CFR 435.916(a)(2) ↩︎

- 42 CFR 435.916(a)(2) ↩︎

- 42 CFR 435.916(a)(3)(i) ↩︎

- The regulation requires that the state give the individual at least 30 days from the date of receipt of the renewal form. States generally send the form well in advance of the end date of coverage so that they can give the person the 30 days to respond and for the state to receive the form and have time to process it prior to the coverage end date. ↩︎

- 42 CFR 435.907(f) and 435.916(a)(3)(i)(B) ↩︎

- 42 CFR 435.916(a)(2) ↩︎

- 42 CFR 435.916(a)(3)(iii) ↩︎

- 42 CFR 435.916(f) ↩︎

- For more information see 42 CFR 435.1200 ↩︎

- 42 CFR 435.916(b) ↩︎

- Author conversations with CMS/CMCS. ↩︎