The KFF COVID-19 Vaccine Monitor is an ongoing research project tracking the public’s attitudes and experiences with COVID-19 vaccinations. Using a combination of surveys and qualitative research, this project tracks the dynamic nature of public opinion as vaccine development and distribution unfold, including vaccine confidence and acceptance, information needs, trusted messengers and messages, as well as the public’s experiences with vaccination.

Key Findings

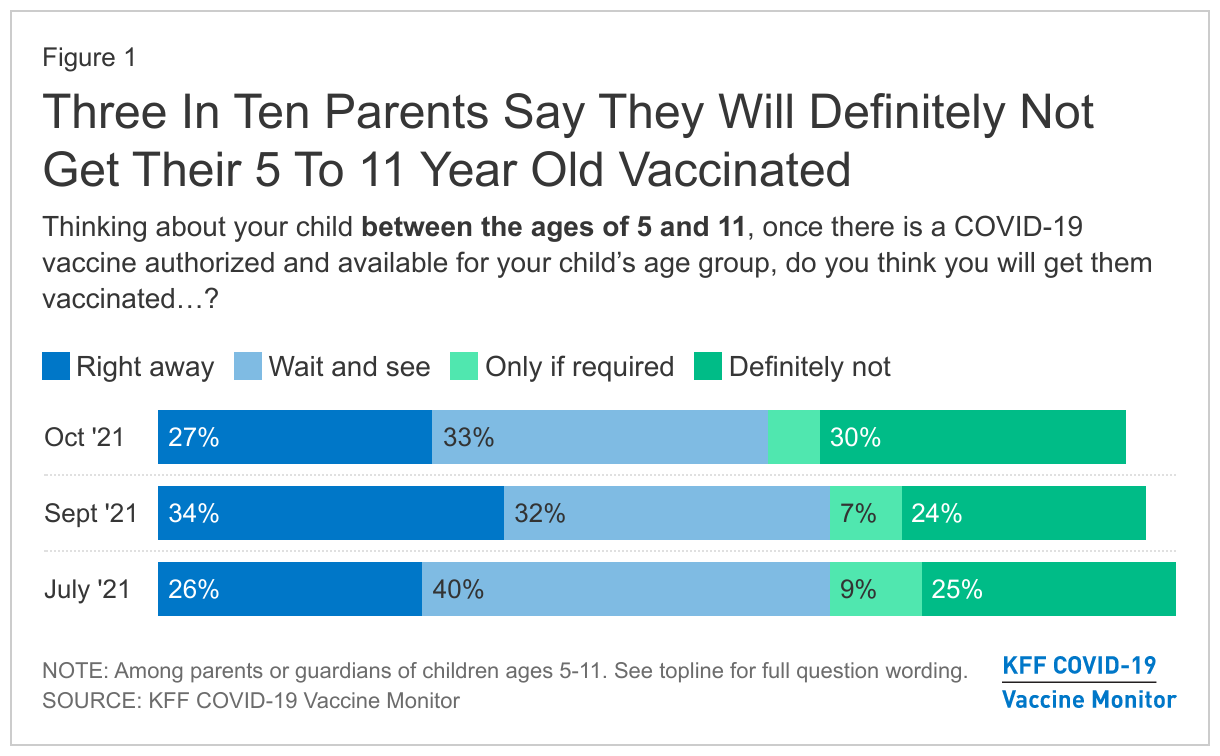

- With the expected expansion of vaccine authorization to younger age groups in the coming weeks, the latest KFF COVID-19 Vaccine Monitor indicates that vaccine uptake has slowed among 12-17 year-olds, with half of parents saying their teen has gotten vaccinated or will do so right away. About three in ten parents of 5-11 year-olds (27%) are eager to get a vaccine for their younger child as soon as one is authorized, while a third say they will wait a while to see how the vaccine is working. Three in ten parents say they will definitely not get the vaccine for their 12-17 year-old (31%) or their 5-11 year-old (30%).

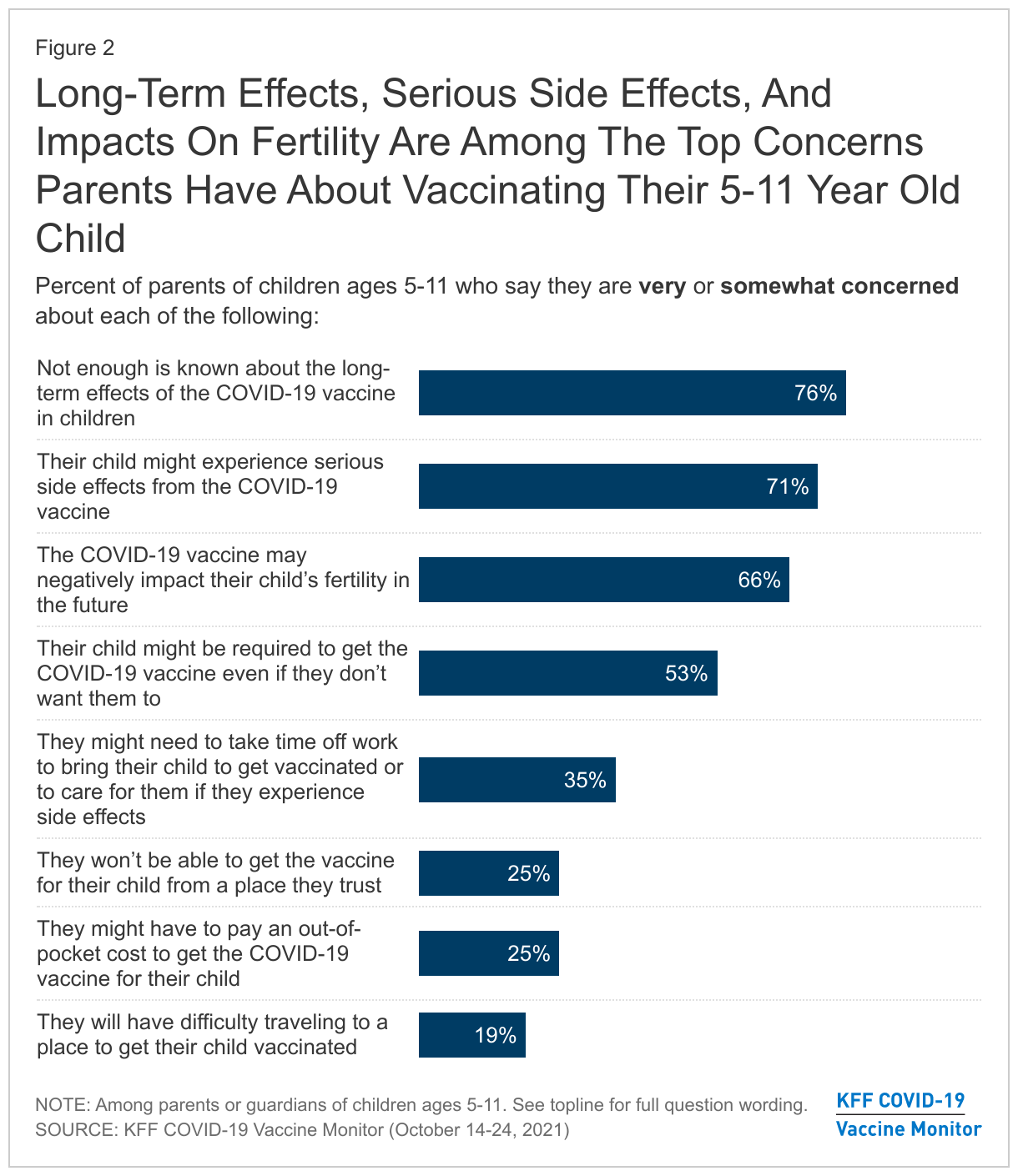

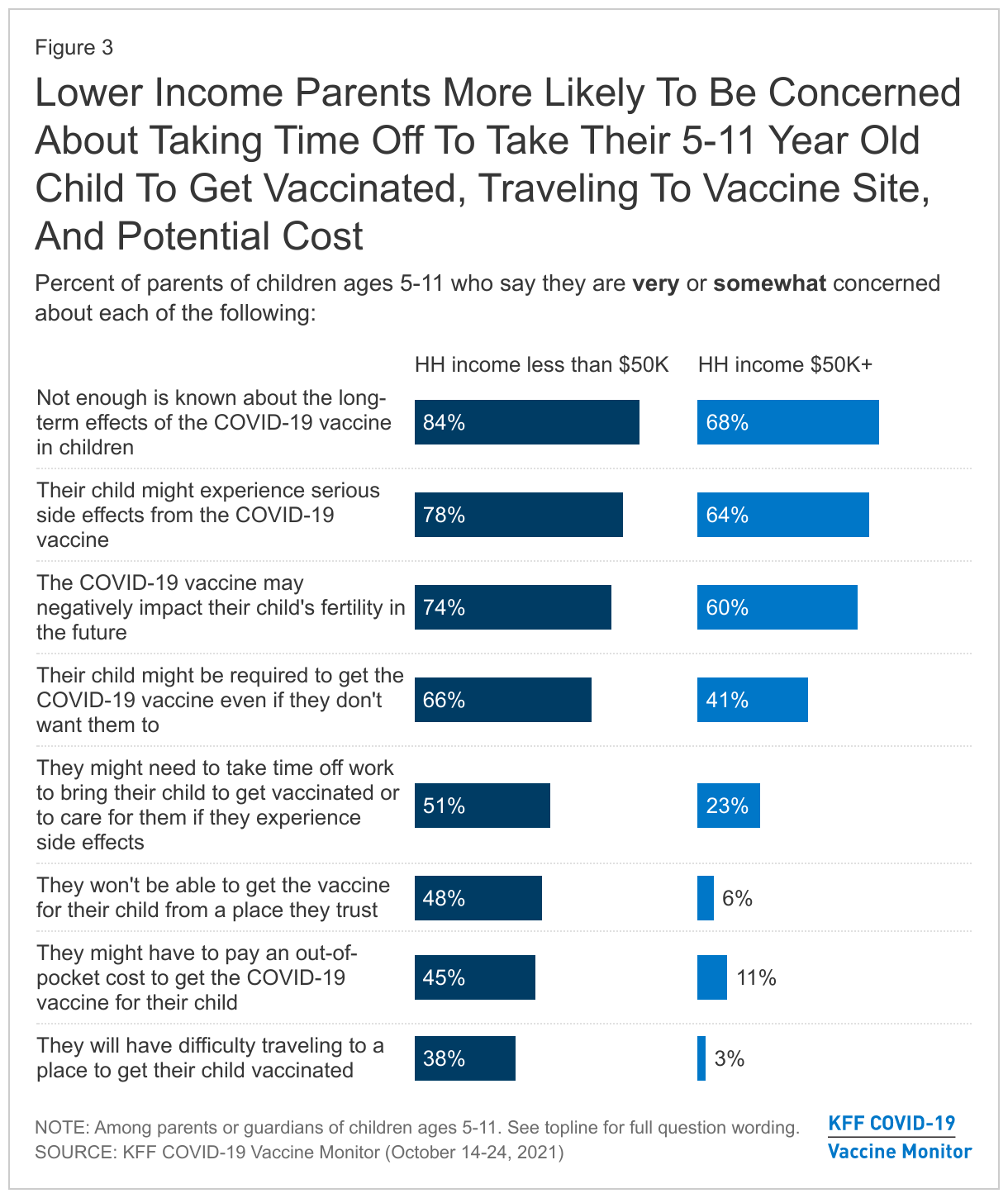

- Parents’ main concerns when it comes to vaccinating their younger children ages 5-11 have to do with potential unknown long-term effects and serious side effects of the vaccine, including two-thirds who are concerned the vaccine may affect their child’s future fertility. With talk of possible school vaccine mandates, over half (53%) of parents are worried their child may be required to get vaccinated for COVID-19 even if they don’t want them to. Some parents also express concerns related to access or information-related barriers to vaccination, including larger shares of lower-income parents who are concerned about missing work to deal with children’s vaccinations (51%), having to pay out-of-pocket to get their child vaccinated (45%), not being able to get the vaccine from a trusted place (48%), or having difficulty traveling to a vaccination location (38%).

- The pace of vaccine uptake also appears to be slowing among adults, with 72% saying they have gotten at least one dose, the same share who said so last month. Partisanship continues to be a sharp dividing line in vaccine attitudes, including among fully vaccinated adults, with nearly four in ten fully vaccinated Republicans saying they are unlikely to get a booster dose when it’s recommended for them.

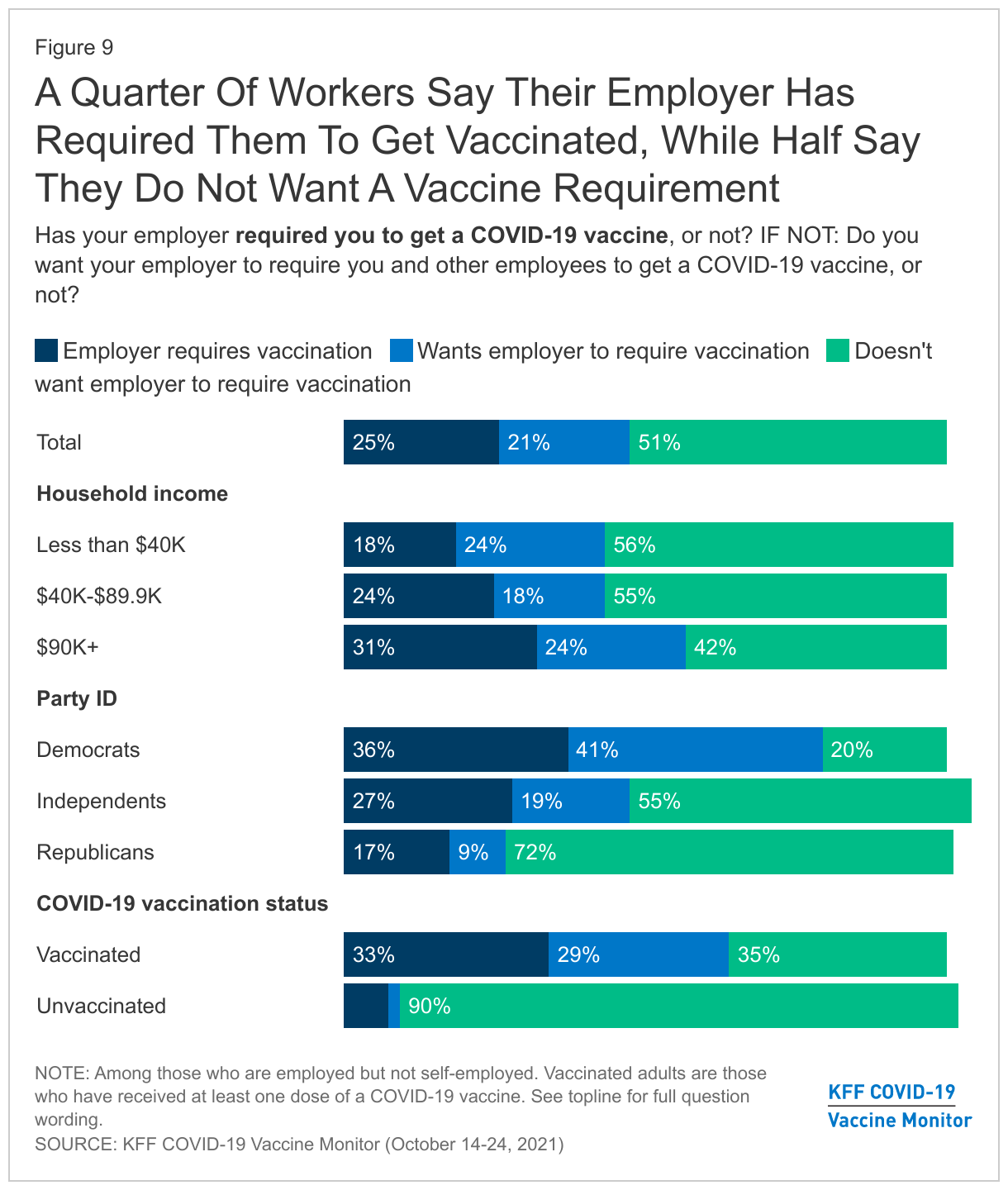

- With a rise in vaccine mandates, one in four workers (25%) now say their employer has required them to get the COVID-19 vaccine, up 16 percentage points since June. Half of workers continue to say they do not want their employer to put in place a vaccine requirement. More than a third (37%) of unvaccinated workers (5% of adults overall) say they would leave their job if their employer required them to get a vaccine or get tested weekly, a share that rises to seven in ten unvaccinated workers (9% of all adults) if weekly testing is not an option. Six in ten workers (8% of all adults) also say they would ask for an exemption if presented with such a mandate. Still, while about a quarter of all adults say they know someone who has left a job because of a vaccine requirement, just 5% of unvaccinated workers (1% of all adults) say they have personally done so.

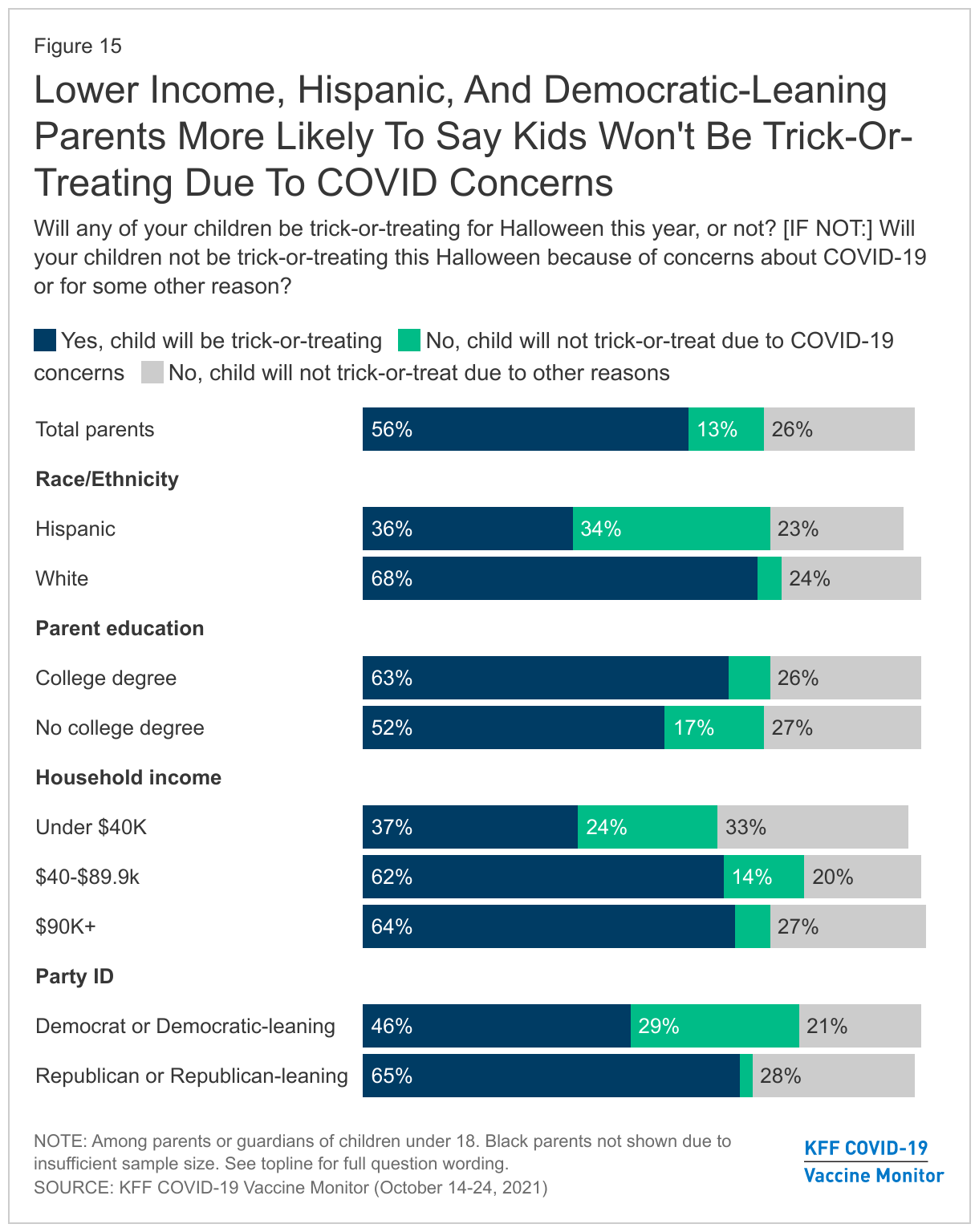

- With the Delta surge abating in most of the country, the Monitor finds that about half the public has returned to their normal pre-pandemic activities and many expect to engage in regular holiday traditions, including a majority of parents who say their kids will be trick-or-treating this Halloween. Some groups remain more cautious, including Democrats, vaccinated adults, and Hispanic parents, one-third of whom say their children will not be trick-or-treating this year specifically because of concerns about COVID-19.

Parents Attitudes Towards COVID-19 Vaccinations For Children

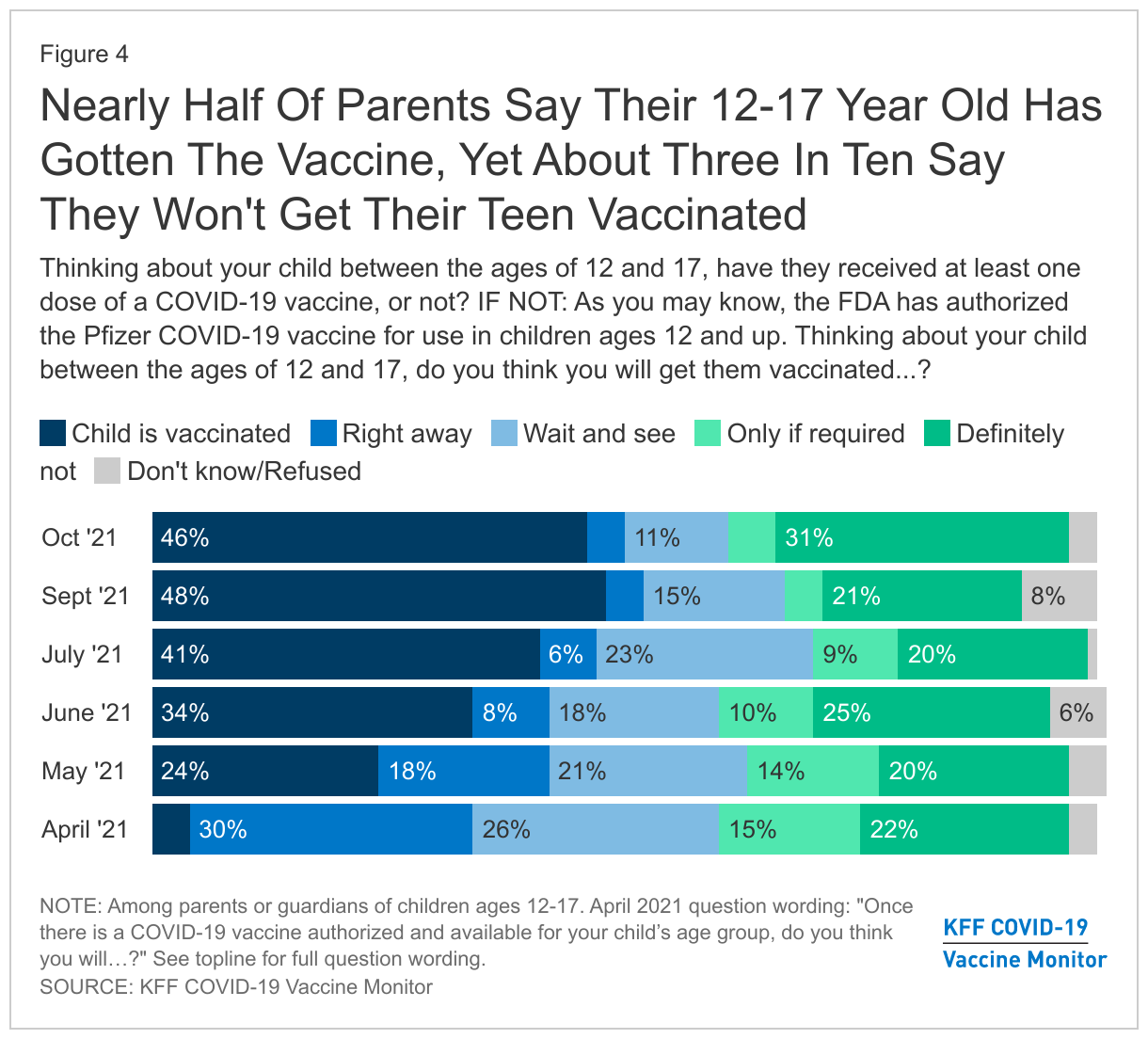

Pfizer’s announcement in September that their COVID-19 vaccine was shown to be safe and effective for children ages five to eleven in clinical trials seems to have had little impact on parents’ intentions to vaccinate their children in that age group. The KFF COVID-19 Vaccine Monitor finds that about three in ten parents (27%) say they will vaccinate their 5-11 year old child “right away” once a vaccine is authorized for their age group – statistically similar to shares who said the same in September and in July. A third of parents say they will “wait and see” how the vaccine is working before having their 5-11 year old vaccinated while three in ten say they definitely won’t get their 5-11 year old vaccinated (30%) and 5% say they will only do so if their school requires it.

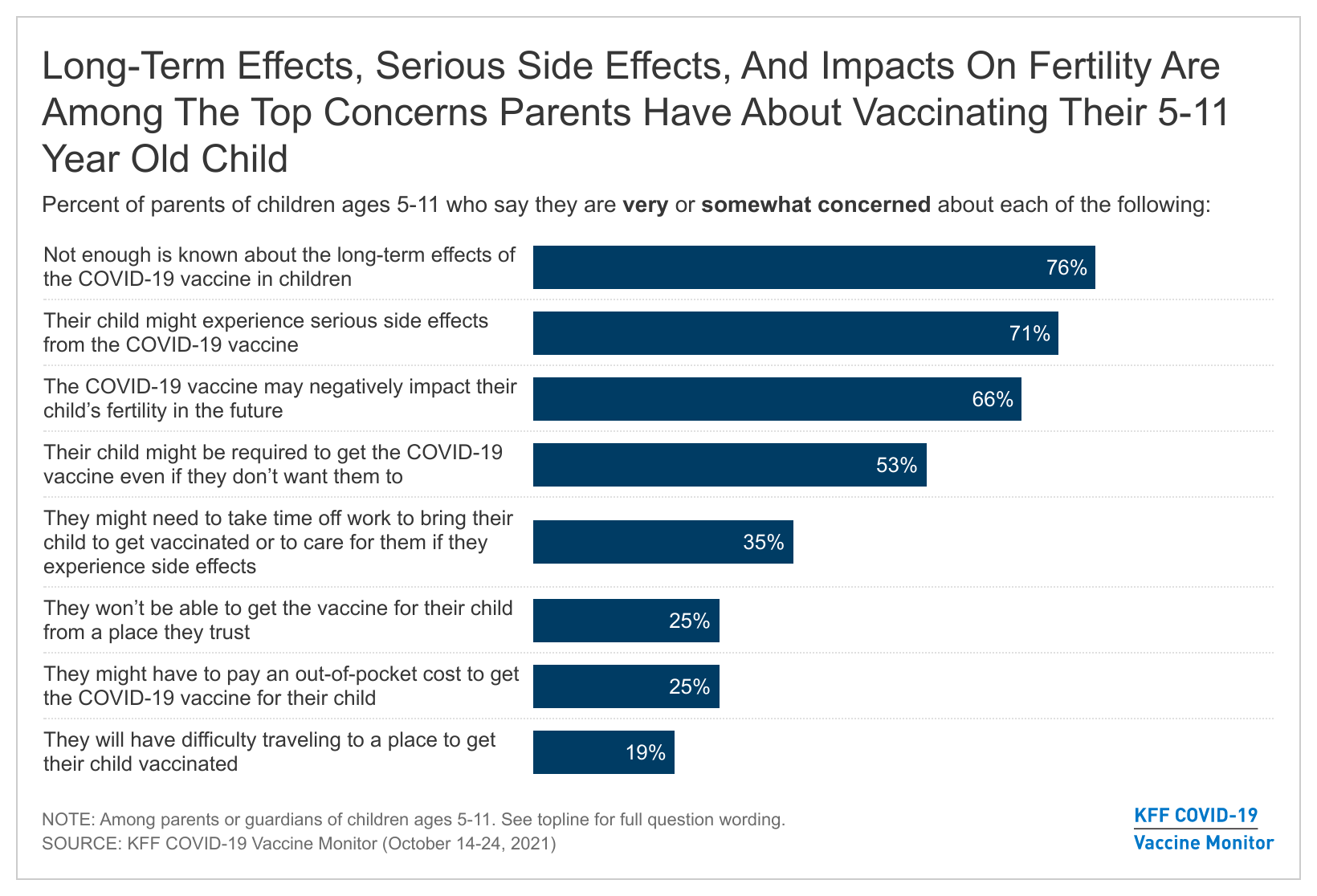

Parents of 5-11 year-olds cite a range of concerns when it comes to vaccinating their children for COVID-19, with safety issues topping of the list. More than seven in ten parents of 5-11 year-olds say they are “very” or “somewhat” concerned that not enough is known about the long-term effects of the COVID-19 vaccine in children (76%) or their child might experience serious side effects from the COVID-19 vaccine (71%). Additionally, two-thirds say they are concerned the vaccine may negatively impact their child’s fertility in the future, despite the CDC stating there is no evidence that the COVID-19 vaccines cause fertility problems.1 With talk of possible school vaccine mandates, over half (53%) of parents are worried their child may be required to get vaccinated for COVID-19 even if they don’t want them to.

Smaller shares of parents express concerns related to access or information-related barriers to vaccination, including about one-third (35%) who are concerned they might need to take time off work to get their child vaccinated or care for them if they experience side effects, one-quarter who are concerned they won’t be able to get their child vaccinated at a trusted place or they might have to pay an out-of-pocket cost, and one in five (19%) who are concerned they may have difficulty traveling to a vaccination location.

Notably, parents with household incomes under $50,000 are more likely than those with higher incomes to say they are very or somewhat concerned about issues related to vaccine access, with about half saying they are concerned about taking time off work to take their 5-11 year old to get the vaccine and recover from symptoms (51%), not being able to get the vaccine from a place they trust (48%), or having to pay an out-of-pocket cost to get their child vaccinated (45%). Nearly four in ten lower-income parents they are concerned about difficulty traveling to a place to get their child vaccinated (38%). Few higher-income parents express these same concerns.

The latest KFF COVID-19 Vaccine Monitor suggests a slowdown in vaccination uptake among 12 to 17 year-olds with about half of parents of teens (46%) saying their child has received at least one dose of a vaccine, similar to the share who said the same in September (48%). Just 4% of parents say they want to get their 12 to 17 year old vaccinated right away while about one in ten parents (11%) say they want to “wait and see” before getting their teen vaccinated. Notably, three in ten parents (31%) say they definitely will not get their 12 to 17 year old vaccinated.

Trends In COVID-19 Vaccination Intentions And Uptake

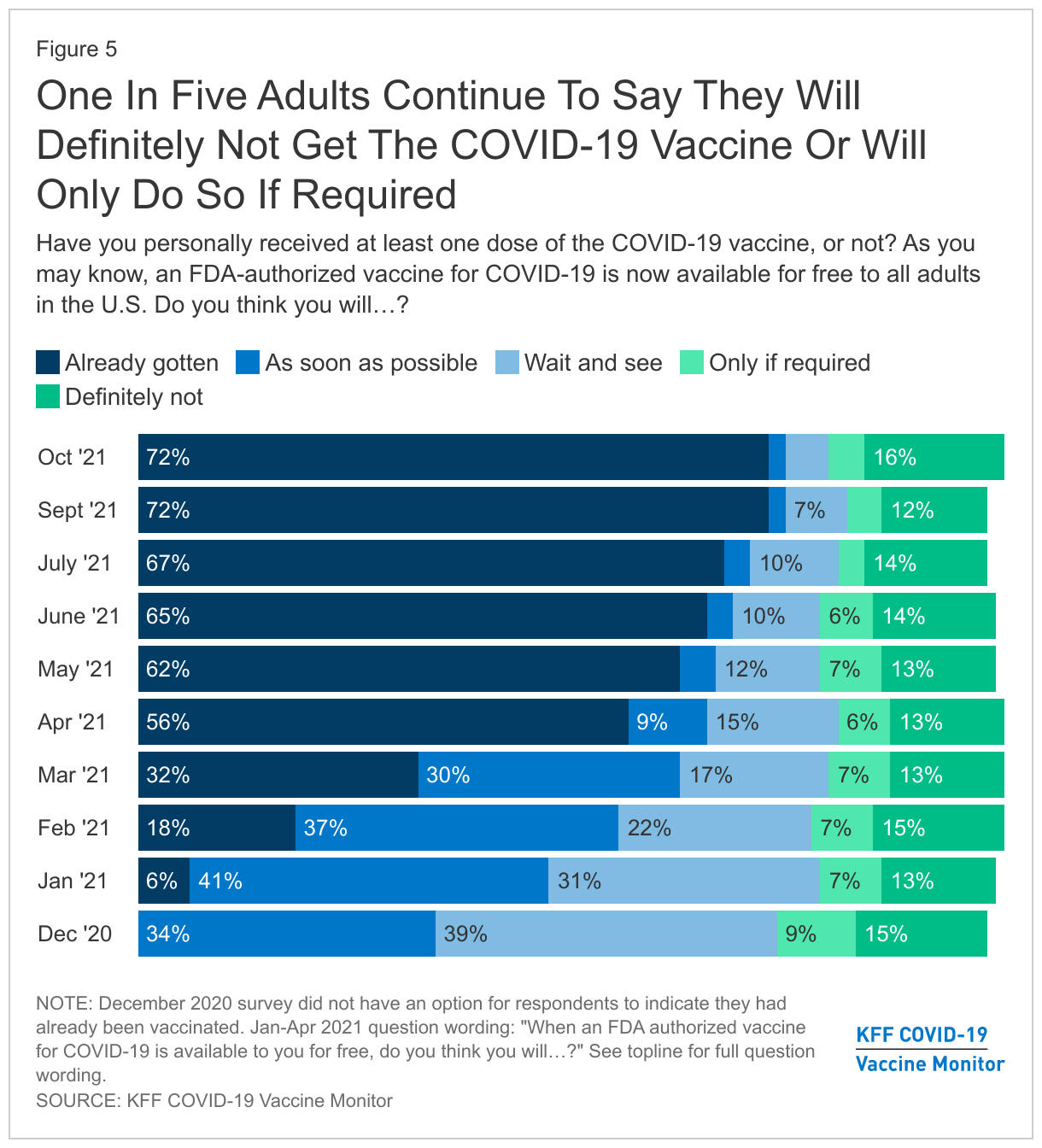

With the Delta surge of COVID-19 cases waning, vaccine uptake among adults has slowed considerably. Just over seven in ten (72%) of adults now say they have received at least one dose of the COVID-19 vaccine and another 2% say they will get vaccinated “as soon as possible,” similar to the shares who reported the same in September. Just 5% say they want to “wait and see” before getting vaccinated, a share that has steadily declined since the spring. Sixteen percent of the public say they will definitely not get vaccinated (a share that has held relatively steady since December 2020) and a further 4% say they will only do so if they are required for work, school, or other activities.

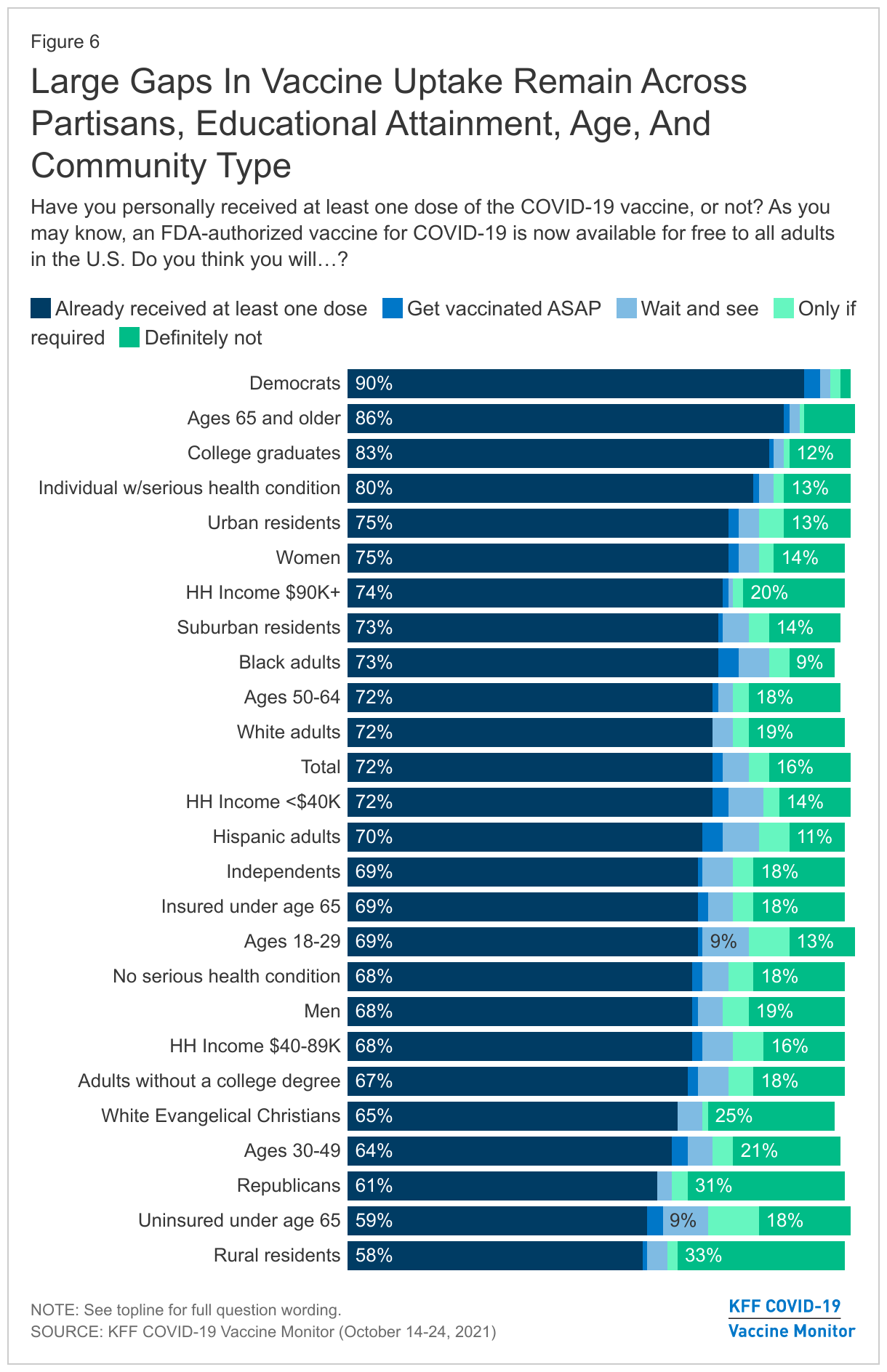

As the Vaccine Monitor has been finding for months, large gaps in self-reported vaccination rates remain across partisanship, age, education, and community type. Across partisans, 90% of Democrats say they have gotten at least one dose compared to 69% of independents and 61% of Republicans. There are also large differences in vaccination rates between college graduates and those without a college degree (83% vs. 67%) and notably, vaccine uptake among rural adults (58%) continues to lag behind those of urban (75%) and suburban (73%) residents. Mirroring the September Vaccine Monitor findings, the gap in vaccination rates across race and ethnic groups has narrowed with similar shares of Black adults (73%), White adults (72%) and Hispanic adults (70%) now reporting having received at least one dose of a COVID-19 vaccine.

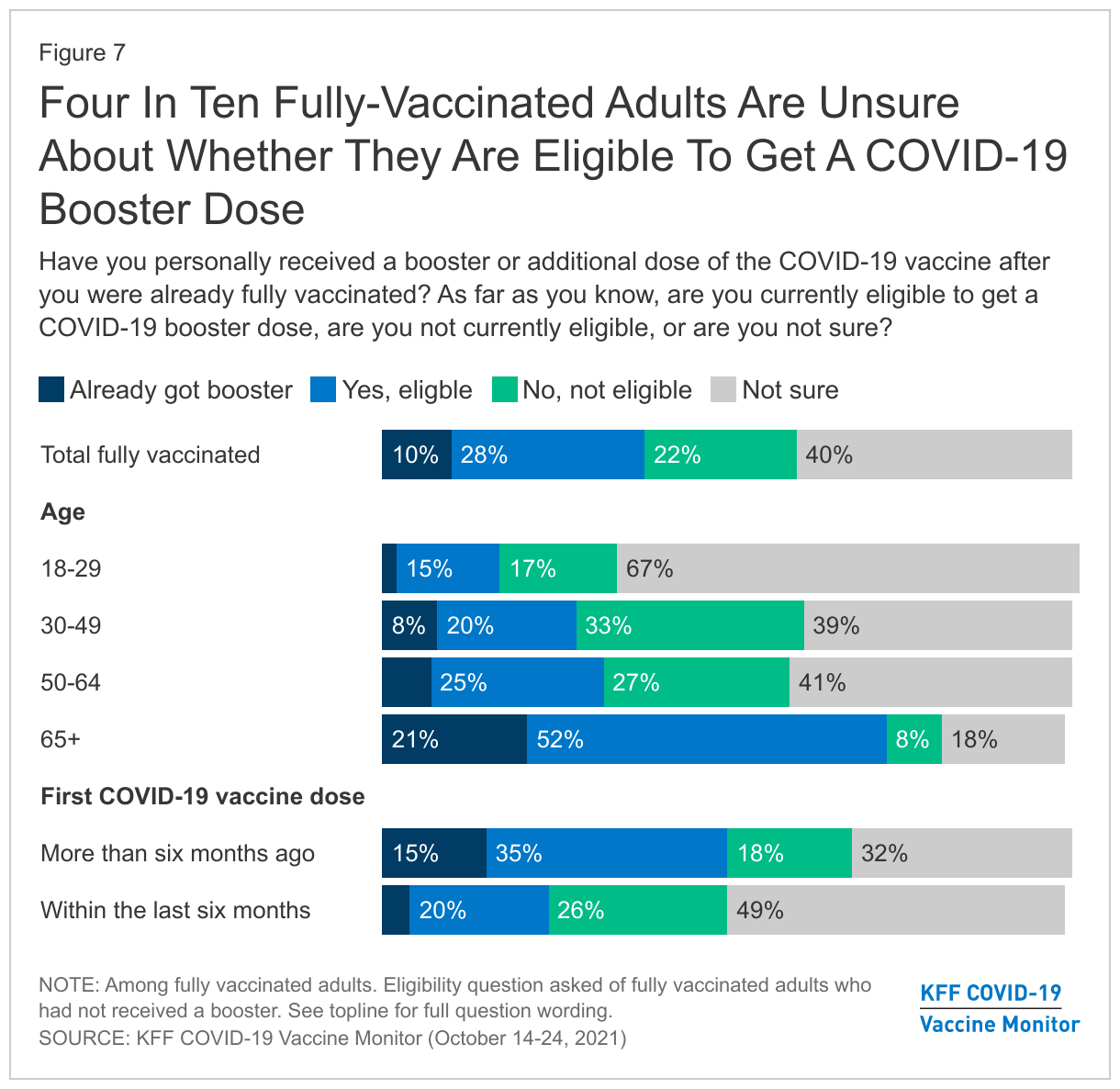

Vaccine Boosters Eligibility And Uptake

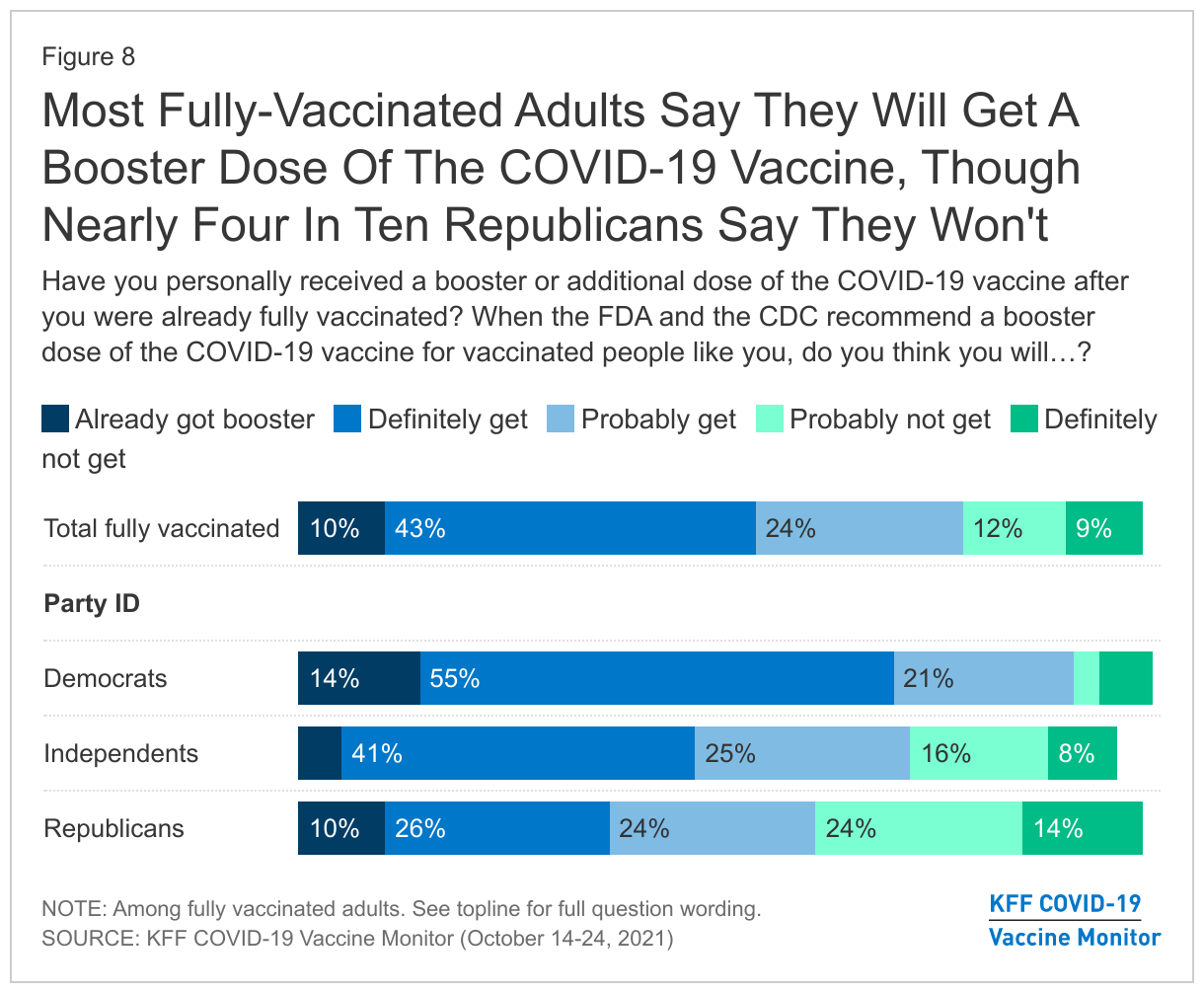

In September, the U.S. Food and Drug Administration (FDA) amended the emergency use authorization for the Pfizer COVID-19 vaccine to allow for a booster dose for those who had received their second dose at least six months prior and are either 65 or older, at high risk for severe COVID-19, or in high exposure occupations. The COVID-19 Vaccine Monitor finds that 10% of fully vaccinated adults (7% of all adults) say they have received a booster dose of the COVID-19 vaccine.

More recently, the FDA announced their support for emergency use authorization for booster doses of the Moderna COVID-19 vaccine for those who received their last dose of the vaccine at least six months prior and who are either 65 or older, at high risk for severe COVID-19, or in high exposure occupations. The FDA also authorized a booster dose of the Johnson & Johnson vaccine for adults who received their initial Johnson & Johnson vaccine at least two months prior and also authorized “mix and match” booster doses for approved or authorized vaccines. These more recent developments occurred while the survey was in the field.

There appears to be some uncertainty among fully vaccinated adults around eligibility for a booster dose. Four in ten fully vaccinated adults (40%) say they are unsure whether or not they are eligible for a booster dose. While 21% of fully vaccinated adults ages 65 and older say they have already gotten a booster dose and another 52% believe they are eligible, young adults are more uncertain with two-thirds of fully vaccinated adults ages 18-29 (67%) saying they are unsure if they are eligible for a vaccine.

As the FDA booster authorizations and CDC recommendations for eligibility evolve, most fully vaccinated adults say they will definitely (43%) or probably (24%) get a booster once it is recommended for people like them. As we found in September, partisans differ in their intentions to get a booster dose of the vaccine even among fully vaccinated adults, with Democrats more than twice as likely as Republicans to say they’ll “definitely” get one if recommended (55% vs. 26%). Indeed, nearly four in ten (38%) fully vaccinated Republicans say they will probably or definitely not get a booster if the FDA and CDC recommend it for people like them.

COVID-19 Vaccine Requirements

Across the country, more and more business, universities, and state and local governments are instituting COVID-19 vaccination requirements. In September, President Biden announced a requirement for all federal government employees and contractors to be vaccinated and for employers with 100 or more employees to either require their workers to provide proof of vaccination or regular COVID testing. And recently in California, Governor Gavin Newsom announced that COVID-19 vaccinations will be required for students attending public school once the vaccines are fully approved by the FDA for their age group.

Workers’ Experiences and Preferences

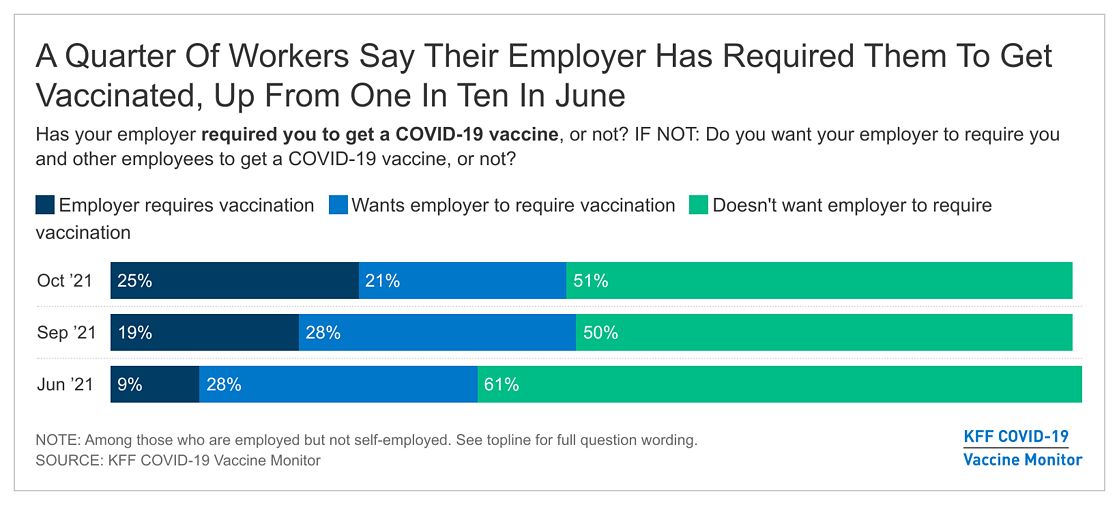

One in four workers (25%) say their employer has required them to get the COVID-19 vaccine, up 16 percentage points since June when just 9% said their employer had required vaccination. Notably, adults with a household income of $90,000 or more are more likely than those with incomes below $40,000 to say their employer has required them to get a COVID-19 vaccine (31% vs. 18%).

While the share saying they are currently subject to an employer vaccine mandate has increased since July, half of all workers say their employer has not required them to get a COVID-19 vaccine and that they do not want their employer to require vaccination, the same share who said this in September. Divisions remain by partisanship and vaccination status, with large majorities of Republicans (72%) and unvaccinated workers (90%) saying they do not want their employer to require employees to get vaccinated whereas most Democrats and vaccinated workers say their employer has either required them to get the vaccine or say they want their employer to impose such a requirement.

The Biden Administration’s COVID-19 action plan announced in September included a requirement for larger employers with more than 100 employees to make sure their workers get vaccinated for COVID-19 or require unvaccinated workers to get tested at least weekly and to give workers paid time off to get a COVID-19 vaccine and recover from side effects. While majorities across partisans, race/ethnicity, and income support the requirement for paid time off, there are differences in support for the “vaccination or testing” requirement. More than seven in ten Black (78%) and Hispanic adults (71%) support the federal government requiring larger employers to ensure their employees are vaccinated or providing weekly COVID tests, compared to about half of White adults (49%) who say the same. Similarly, those with household incomes under $40,000 (68%) are more likely than higher income adults to support the federal requirements for larger businesses to mandate vaccination or testing for employees.

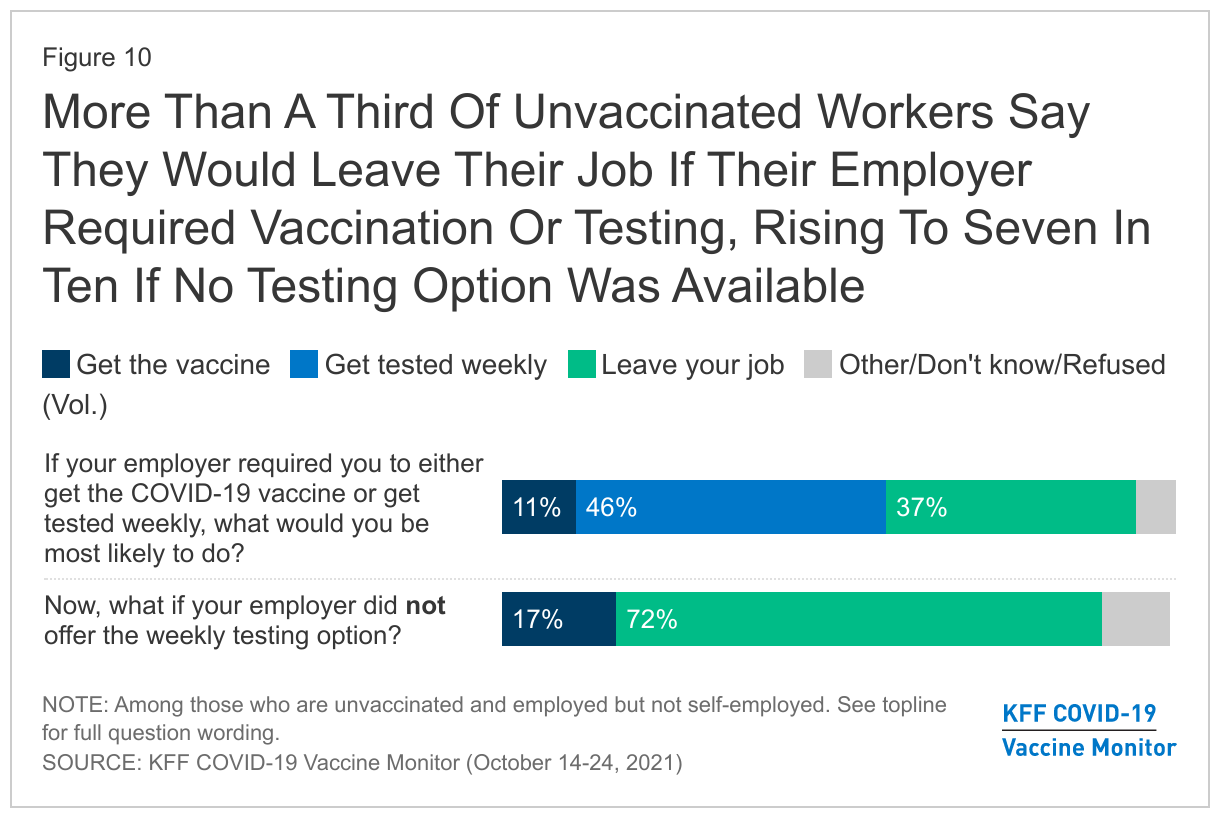

When unvaccinated workers are asked what they would do if their employer required them to either get the COVID-19 vaccine or undergo weekly COVID-19 testing, 11% say they would be most likely to get the vaccine, a plurality (46%) say they would opt for weekly testing, and over a third (37%) say they would be likely to leave their job. Among all adults, this translates to 1% who would get the vaccine if faced with an employer mandate and 5% who say they would leave their job. However, if their employer did not offer an option for weekly tested, the share of unvaccinated workers who say they would get the vaccine increases to 17% (2% of all adults) and the share saying they would leave their job increases to 72% (9% of all adults).

About six in ten unvaccinated workers (59%) say they would be likely to apply for an exemption if their employer required them to get the COVID-19 vaccine, including 44% who say they would be “very likely” to do so. Nearly four in ten (38%) say they would be either “very” or “somewhat” unlikely to apply for an exemption. When asked what type of exemption they would apply for, about one in four unvaccinated workers (27%) say they would apply for a religious exemption, one in six (16%) say they would apply for a medical exemption, while the remainder say they would apply for some other kind of exemption, multiple types, or they are unsure.

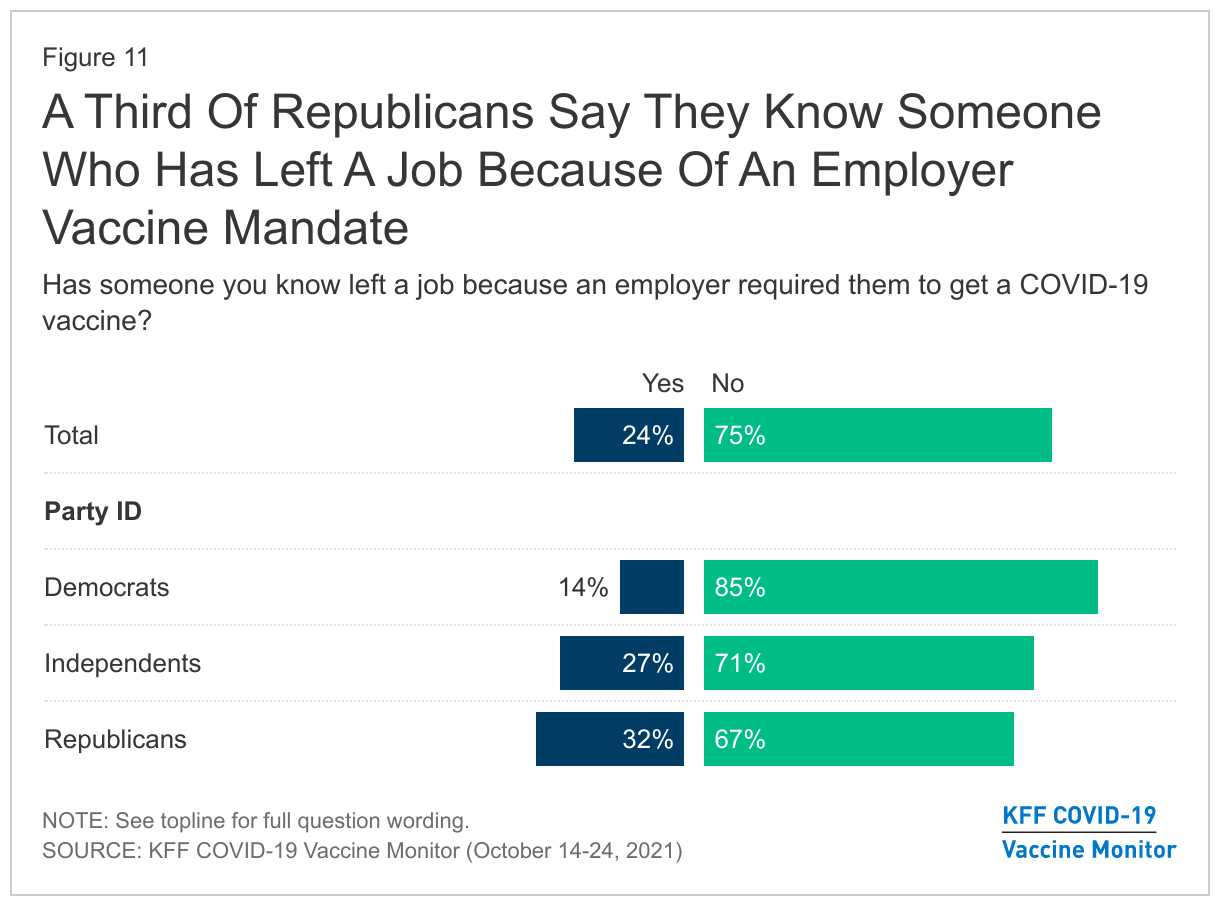

Despite numerous reports of employees leaving their jobs due to employer-imposed vaccination requirements, only 5% of unvaccinated adults say they have left a job because an employer required them to get vaccinated, accounting for 1% of adults nationwide. A larger share (24%) of all adults say they know someone who has a left a job due to an employer vaccination requirement, with Republicans more than twice as likely as Democrats to say they know someone who has done so (32% vs. 14%).

A Return To Normal?

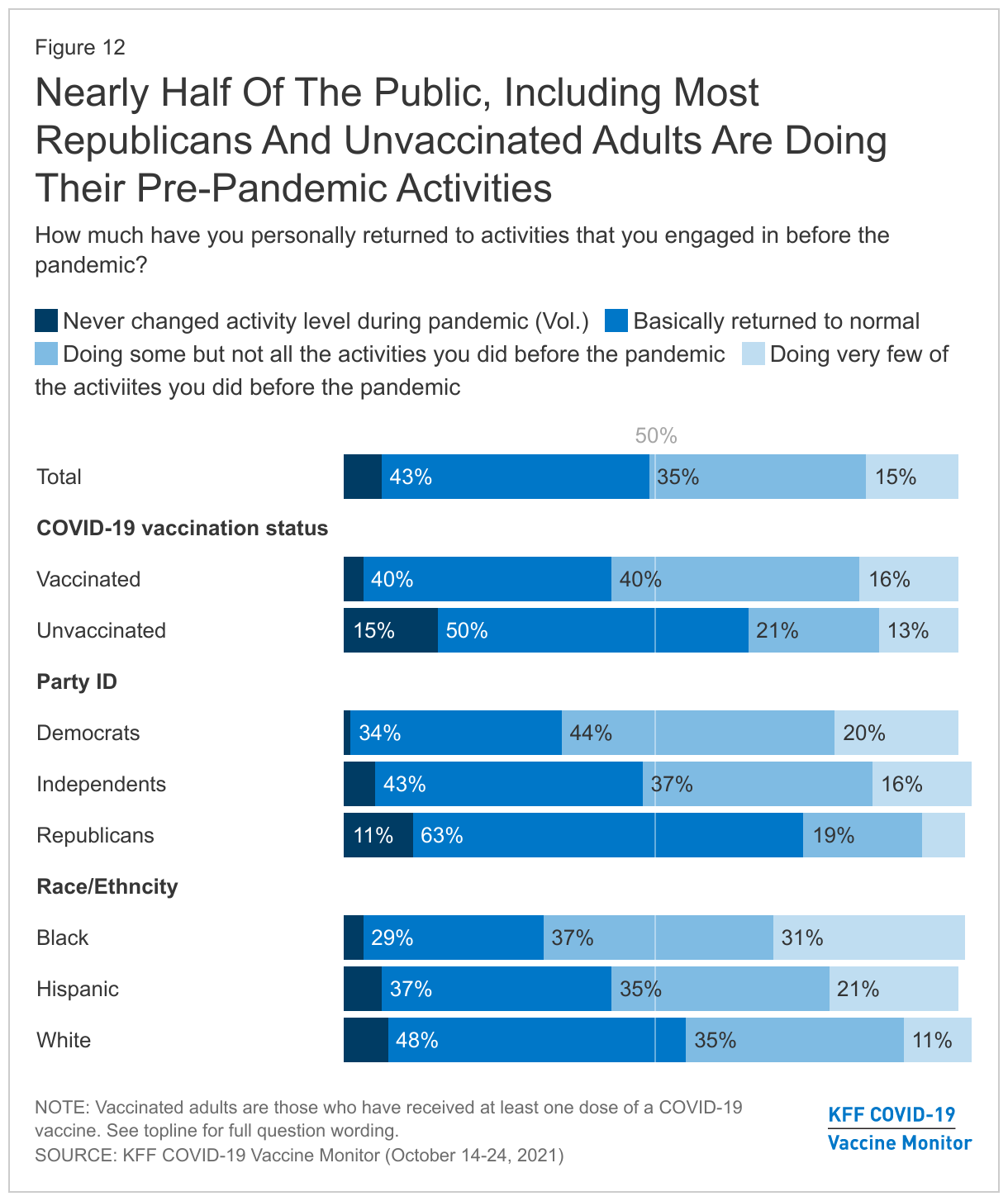

As the holiday season approaches with the COVID-19 Delta variant still present but waning, nearly half of the public say they have either basically returned to normal when it comes to the activities they were doing before the pandemic (43%) or offered that they never really changed their activity level to begin with (6%). A further 35% say they have returned to “doing some, but not all,” of their pre-pandemic activities, and about one in six (15%) say they are still “doing very few of the activities” they did before the pandemic.

Some groups report being more cautious than others in their return to pre-pandemic activities. Most Democrats say they are “doing some, but not all” of the activities they did before the pandemic (44%) or say they are doing few of their pre-pandemic activities (20%), whereas most Republicans say they have “basically returned to normal” (63%) or never changed their activity level during the pandemic (11%). Similarly, vaccinated adults are less likely than their unvaccinated counterparts to say they have “basically returned to normal.” Notably, Black and Hispanic adults (groups that have been particularly hard hit by COVID-19) are more likely than White adults to say they are doing very few of their pre-pandemic activities.

Holiday Plans In The Midst Of A Pandemic

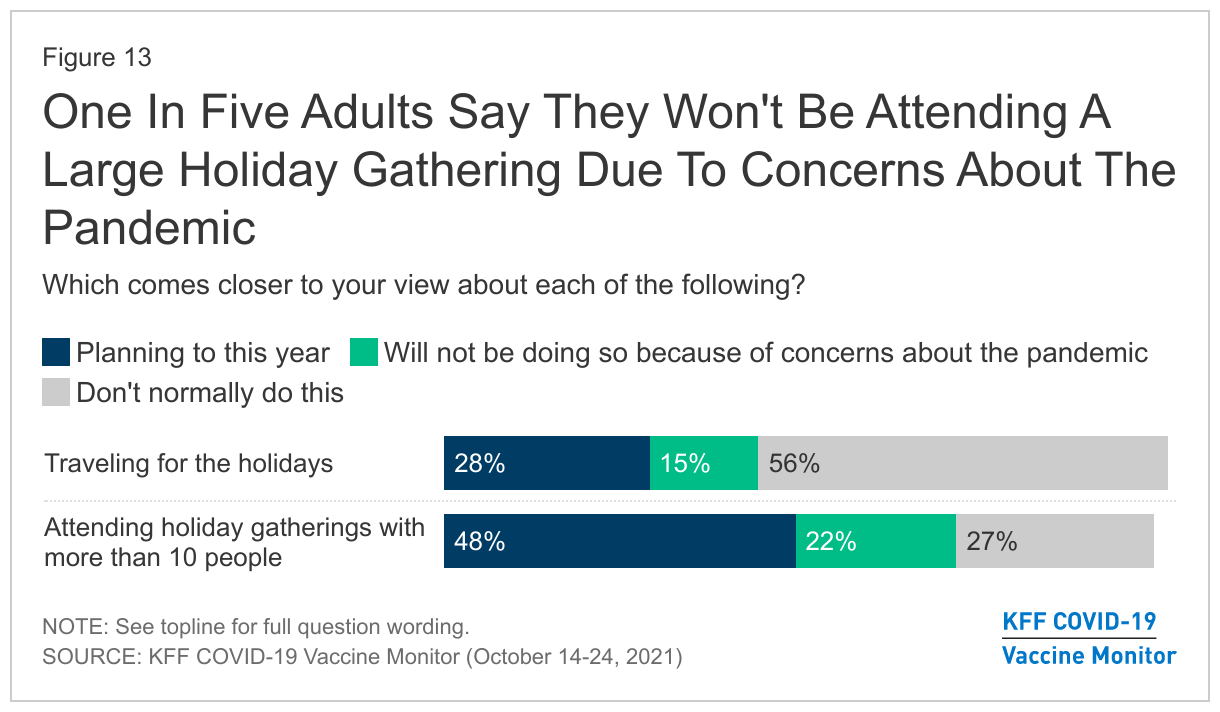

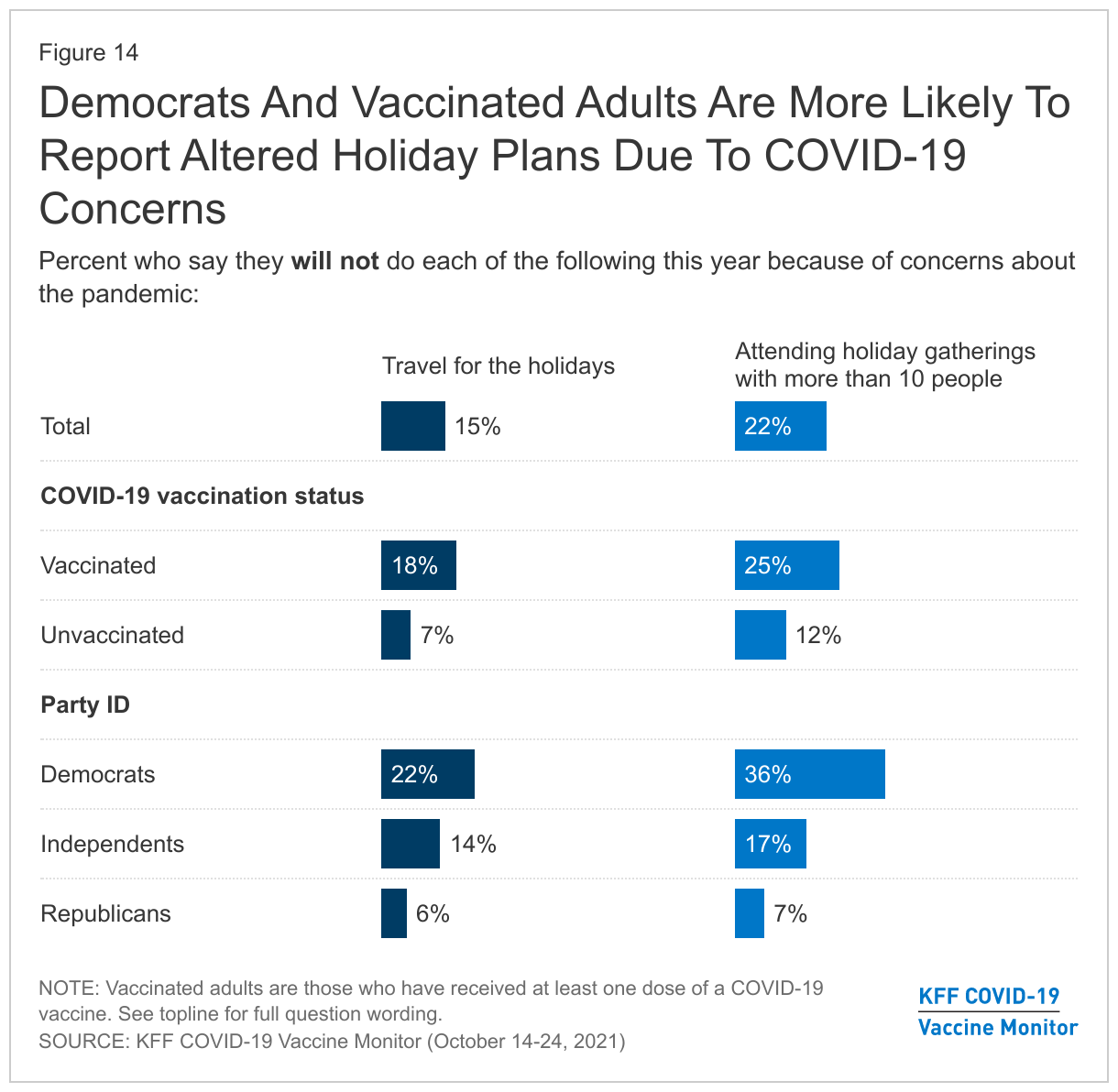

With the holiday season approaching, some adults are still not ready to return to their “normal” holiday activities. About one in six adults (15%) say they will not be traveling for the holidays specifically due to concerns about the pandemic and about one in five (22%) say they will not be attending holiday gatherings with more than ten people this year due to pandemic concerns.

Mirroring their more cautious approach to returning to their normal pre-pandemic activities, Democrats (36%) are more than twice as likely as independents (17%) and five times as likely as Republicans (7%) to say they will avoid attending large holiday gatherings due to concerns about the pandemic. Likewise, vaccinated adults are about twice as likely as those who are unvaccinated to say they will not be traveling for the holidays (18% vs. 7%) or attending a holiday gathering with more than ten people (25% vs. 12%) due to concerns about the pandemic.

While some people remain hesitant to partake in their usual holiday activities, most parents (56%) say their children will be trick-or-treating for Halloween this year. About one in eight parents say their children will not be doing so due to COVID-19 concerns (about one-quarter say their child will not be trick-or-treating for other reasons). Hispanic parents are about eight times more likely than their White counterparts to say their children will not be trick-or-treating this year because of concerns about COVID-19 (34% vs. 4%). Similarly, nearly three in ten parents who are Democrats or lean towards the Democratic Party say their children will not be going trick-or-treating on Halloween due to concerns about the virus, compared to just 2% of Republican and Republican-leaning parents who say the same. Notably, parents without a college degree (17%) and those with a household income under $40,000 (24%) are more likely than their counterparts with higher educational attainment and income to say their children will not be trick-or-treating this year due to COVID-19 concerns.

Economic Impact Of The Pandemic

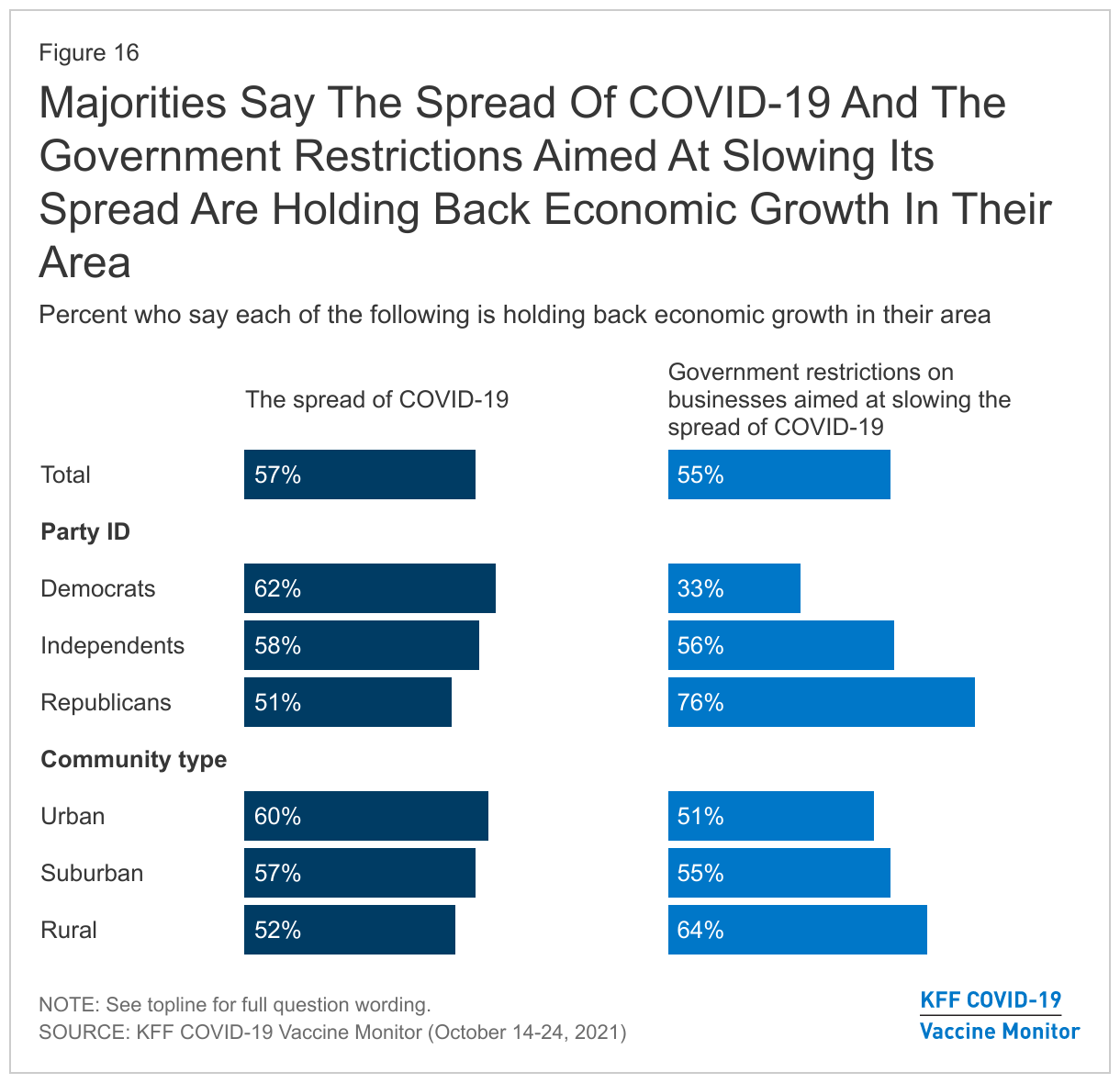

The pandemic continues to impact the public’s economic outlook as majorities see both the spread of COVID-19 (57%) and government restrictions aimed at slowing its spread (55%) as hindering economic growth in their area. While about six in ten Democrats and independents and about half of Republicans say the spread of COVID-19 is holding back economic growth in their area, there are larger partisan differences when it comes to government restrictions aimed at limiting the spread of the virus. About three in four Republicans (76%) say government restrictions are holding back economic growth in their area compared to a third of Democrats and a slight majority of independents (56%) who say the same. Notably, nearly two-thirds of rural residents (64%) say government restrictions aimed at limiting the spread of COVID-19 is holding back economic growth in their area, compared to about half of suburban (55%) and urban (51%) residents.

COVID-19 Treatments

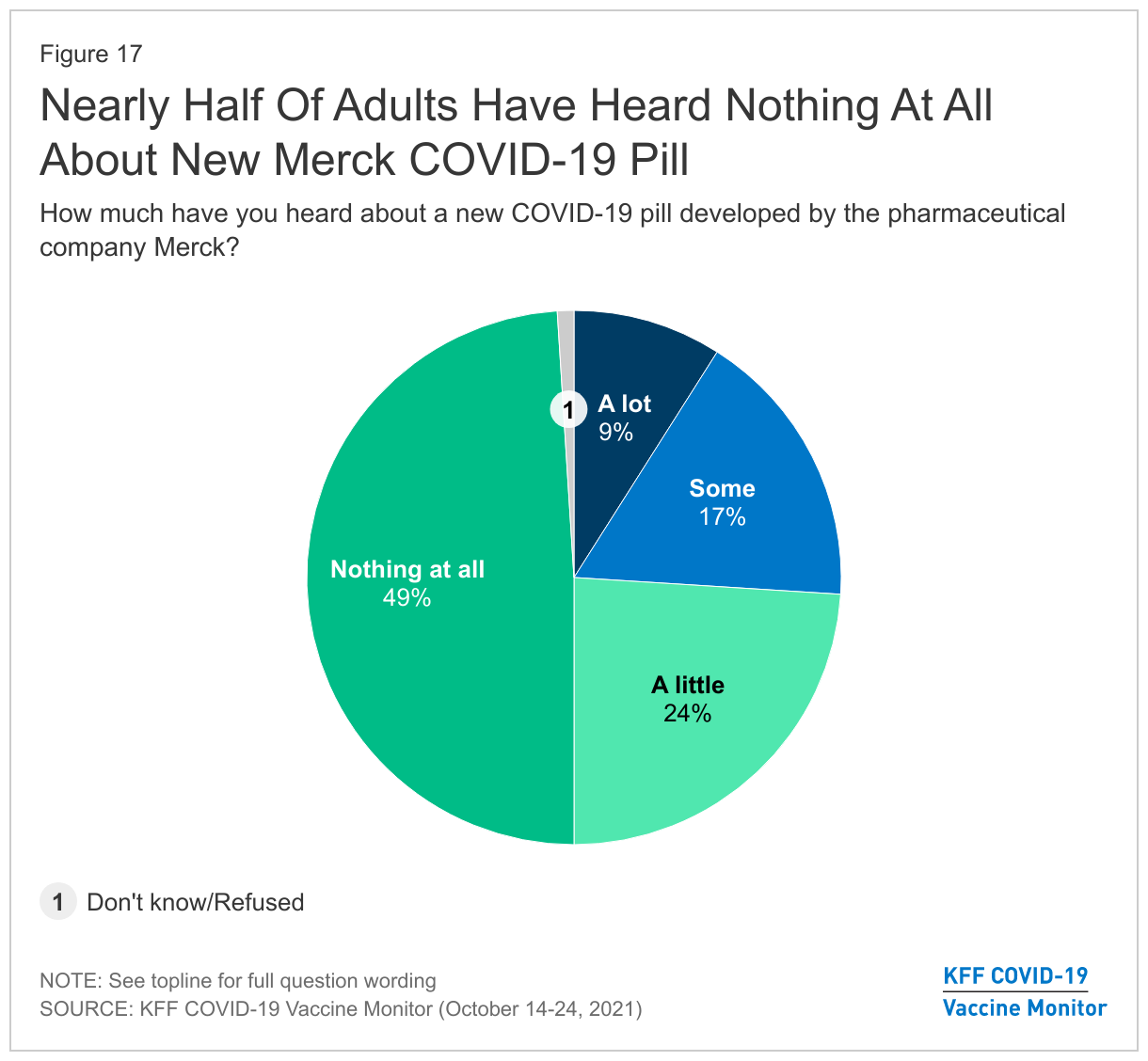

A new pill, created by the pharmaceutical company Merck, provides antiviral support against mild to moderate COVID-19 cases, helping to prevent them from developing into more severe cases. While not yet available to the public, many are hopeful this will help control the impact of the virus among unvaccinated populations. The latest Vaccine Monitor finds that 9% of adults have heard “a lot” about the new COVID-19 pill, 17% “some,” about a quarter (24%) have heard “a little.” Half (49%) say they have not heard anything at all.

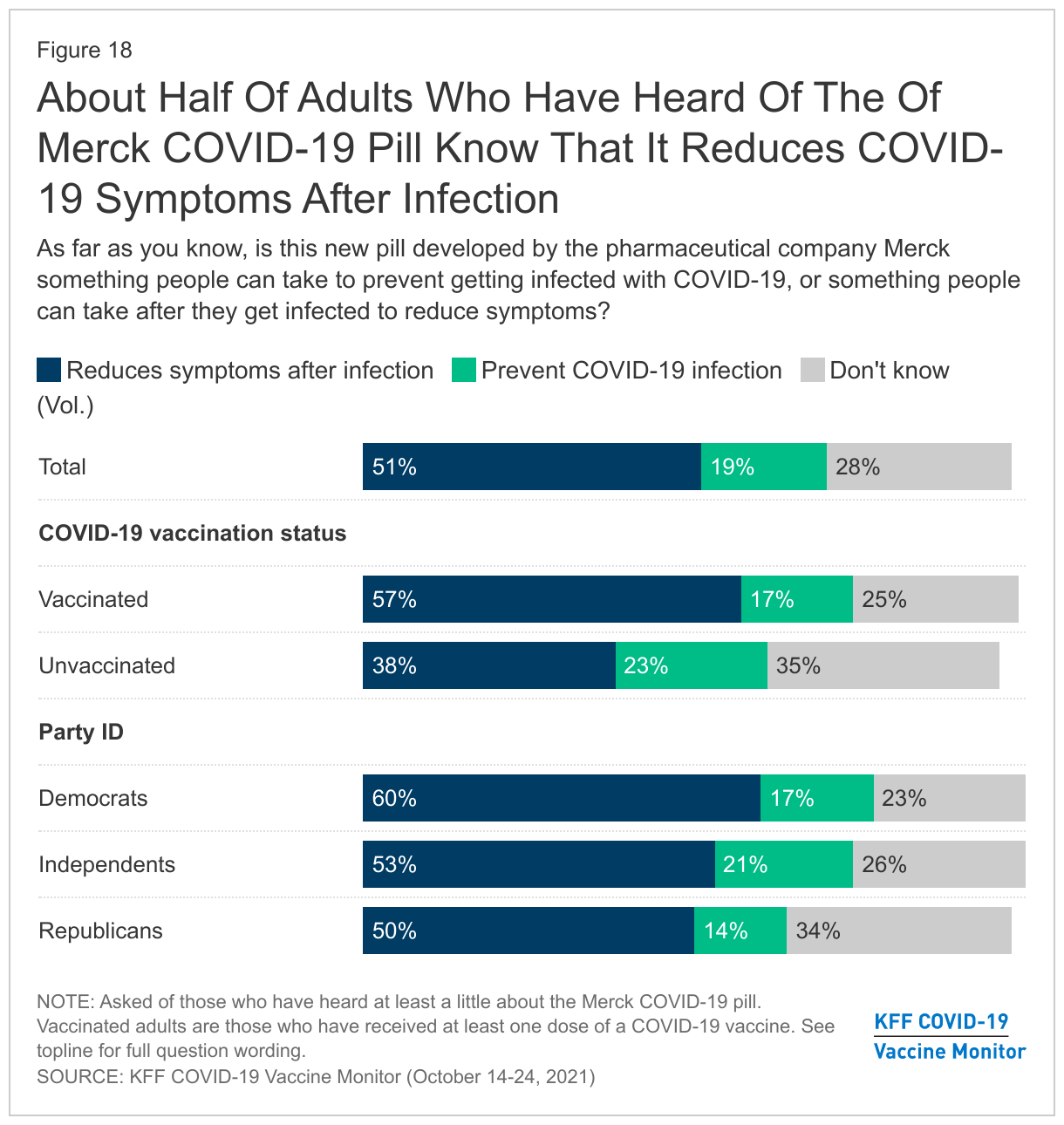

Among those who have heard at least a little about the Merck pill, about half correctly believe it reduces symptoms after infection, compared to 19% who think it prevents COVID-19 infections, and 28% who are unsure what it does. Among those who have heard about the Merck COVID-19 pill, vaccinated adults are more likely to have the correct information about the Merck pill, with 57% believing it reduces symptoms compared to 38% of unvaccinated adults.

But the existence of the pill is unlikely to change much in terms of vaccination rates, with nine in ten (89%) of unvaccinated adults who have heard about the Merck pill saying it won’t make a difference in how likely they are to get vaccinated for COVID-19. Few say the pill will make them either “more likely” (5%) or “less likely” (6%) to get the vaccine.