The Small Share of Employers Offering Retiree Health Benefits Are Increasingly Turning to Medicare Advantage

Few employers offer retiree health benefits, and those that do increasingly are turning to Medicare Advantage plans to provide that coverage – a shift that has implications both for retirees and for federal spending, finds a new KFF analysis.

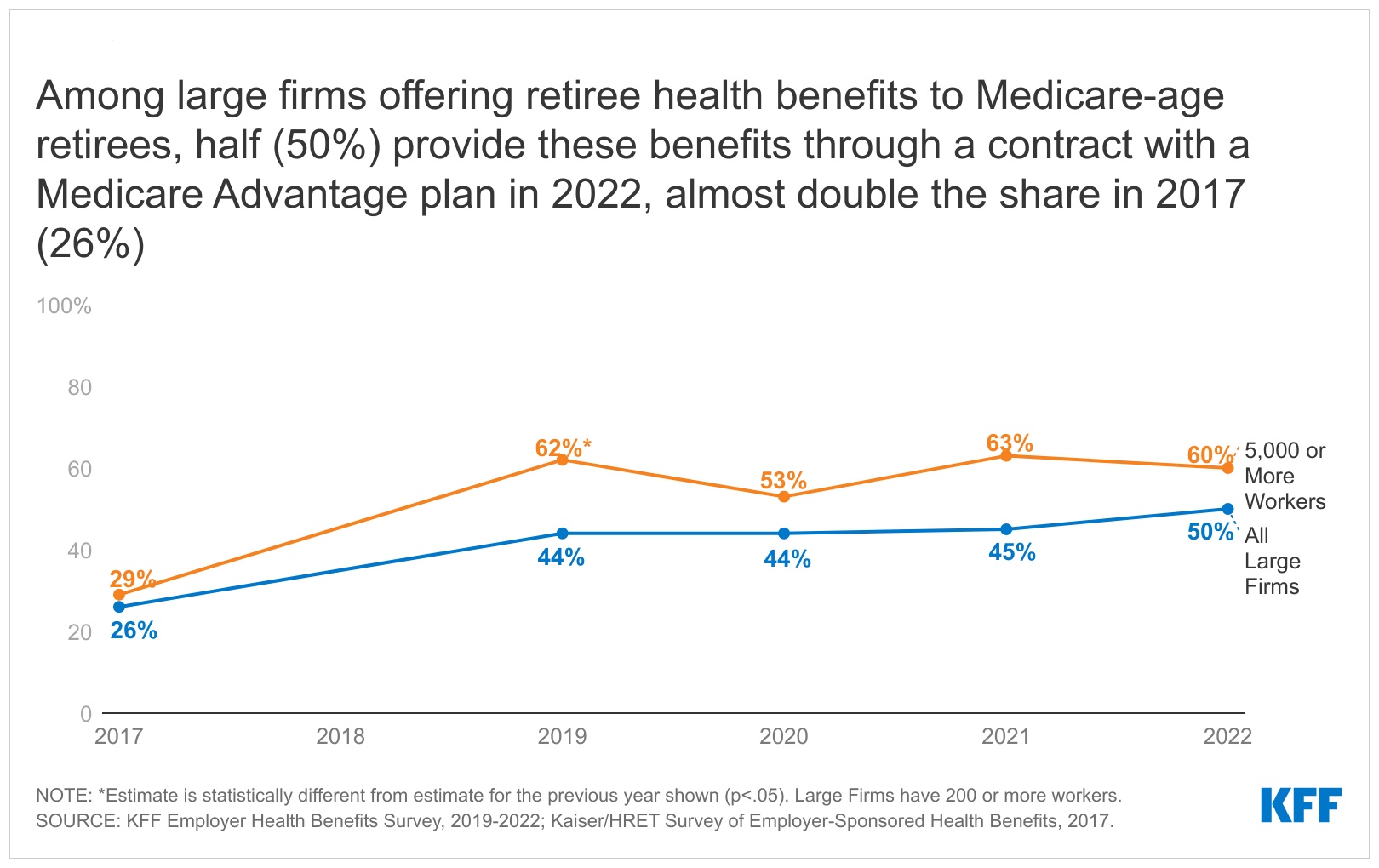

Among the relatively small share of large firms (200 or more workers) that offer retiree health benefits to Medicare-age retirees, half (50%) provide these benefits through a Medicare Advantage plan in 2022, according to the analysis of data from the 2022 KFF Employer Health Benefits Survey. That’s up from 26 percent in 2017.

Under this approach, employers contract with a Medicare Advantage private insurer that provides all Medicare-covered benefits in addition to supplemental benefits, rather than other approaches, such as providing supplemental coverage that wraps around traditional Medicare.

Just 13 percent of large employers offer retiree health benefits to Medicare-age retirees in 2022, the analysis finds. It also finds that:

- Among larger employers with 1,000 or more workers that offer retiree health benefits through a Medicare Advantage plan, the most common reason the employer elected this option was the lower cost.

- About 44 percent of large employers offering Medicare Advantage coverage to their retirees give them no choice but to receive their benefits through a Medicare Advantage plan, rather than give them a choice between Medicare Advantage and non-Medicare Advantage options.

The shift to Medicare Advantage has implications for retirees. On the one hand, this approach may help retirees if it enables employers to maintain or even broaden retiree health benefits rather than scale back or even terminate coverage. On the other hand, it has the potential to restrict retirees’ access to doctors and hospitals for Medicare-covered services, depending on the plan’s provider network, and subject retirees to utilization management tools, such as prior authorization, that may limit access to Medicare-covered services.

The rising number of large employers choosing Medicare Advantage for their Medicare-eligible retirees also has implications for federal spending because Medicare spends more per person for enrollees in Medicare Advantage plans (including in group plans) than for beneficiaries covered by traditional Medicare.

For the full analysis and other data and analyses about Medicare Advantage, visit kff.org.