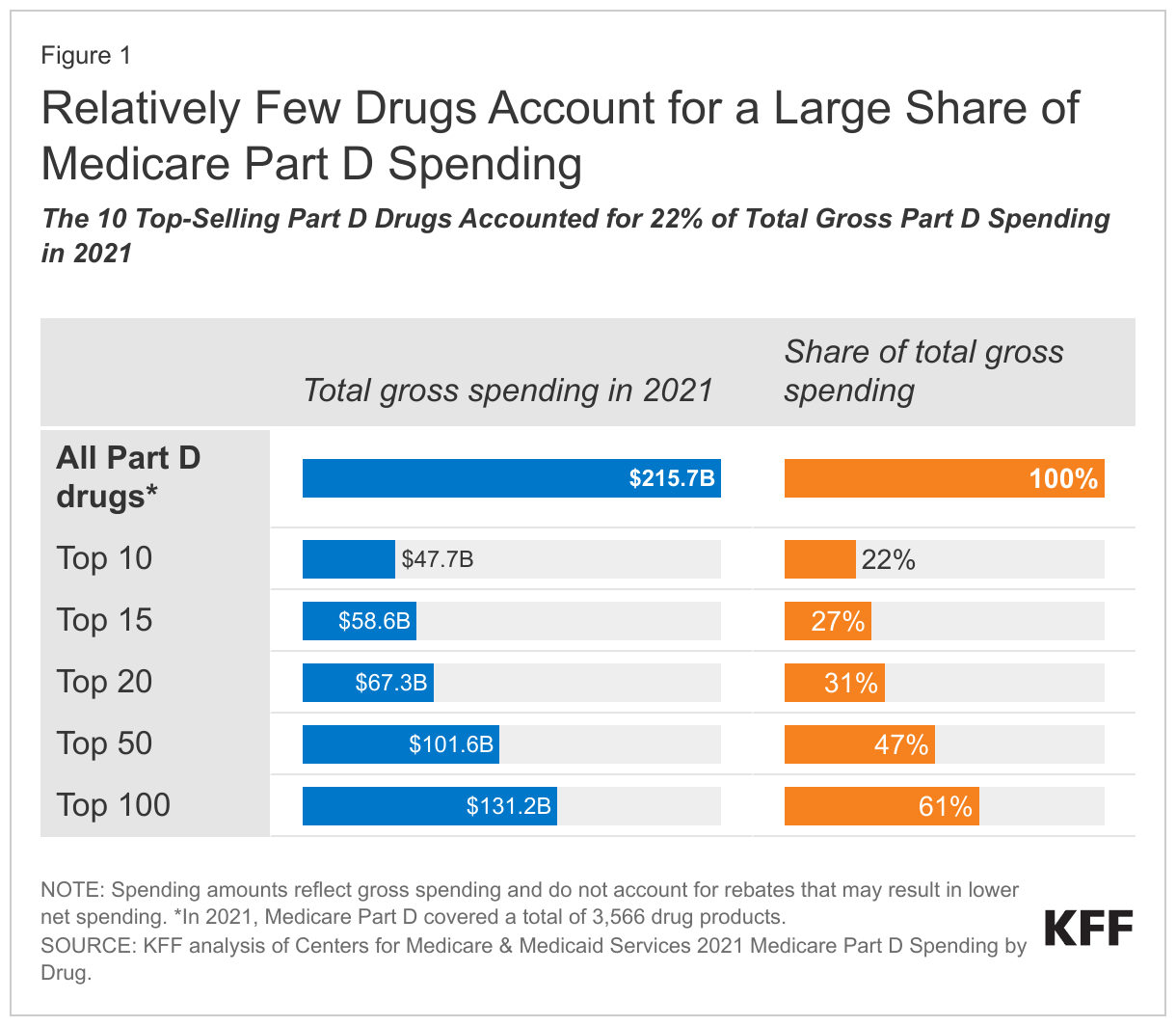

A Small Number of Drugs Account for a Large Share of Medicare Part D Spending

The Inflation Reduction Act requires the federal government to negotiate the price of certain high-spending drugs covered by Medicare Part D, Medicare’s outpatient prescription drug benefit program, and Medicare Part B, which covers physician and outpatient services, including drugs administered by physicians and other providers. Under the new Medicare Drug Price Negotiation Program, the number of drugs subject to price negotiation will be limited to 10 Part D drugs for 2026, another 15 Part D drugs for 2027, another 15 Part D and Part B drugs for 2028, and another 20 Part D and Part B drugs for 2029 and later years. The number of drugs with negotiated prices available will accumulate over time.

The 10 Part D drugs that will be selected for price negotiation for 2026 will be published by September 1, 2023. These 10 drugs will be chosen from the top 50 negotiation-eligible Part D drugs with the highest total Medicare Part D expenditures (defined as total gross covered prescription drug costs). Subject to specific exclusions and exceptions, drugs qualify for price negotiation if they are single-source brand-name drugs or biological products without therapeutically-equivalent generic or biosimilar alternatives, and are at least 7 years (for small-molecule drugs) or 11 years (for biologics) past their FDA approval or licensure date, as of the date that the list of drugs selected for negotiation is published.

This analysis provides context for understanding the potential impact of negotiating prices for a limited number of Medicare-covered drugs by identifying the 10 top-selling drugs in 2021, measuring the share of total Medicare Part D drug spending accounted for by top-selling drugs that year, and examining changes in spending and use of these drugs since 2018 (the first year that all 10 of the drugs were covered under Part D). We focus on drugs covered under Part D, rather than Part B, since negotiation will be limited to Part D drugs for the first two years of the negotiation program. We ranked drugs by total gross spending in 2021 since that is the measure that will be used to rank drug products in the negotiation program. Our analysis is based on Centers for Medicare & Medicaid Services’ data on Medicare Part D spending by drug.

It is important to note that this analysis is not designed to identify which drugs are likely to be subject to price negotiation for 2026, since we do not take into account all of the factors that determine whether a drug is negotiation-eligible and we do not have access to the more current spending data that CMS will use in selecting drugs for price negotiation.

A small number of drugs account for a disproportionate share of Medicare Part D prescription drug spending, with the 10 top-selling drugs accounting for nearly one-fourth of gross Part D spending in 2021

In 2021, Medicare Part D covered more than 3,500 prescription drug products, with total gross spending of $216 billion, not accounting for rebates paid by drug manufacturers to pharmacy benefit managers (PBMs). The 10 top-selling Part D drugs accounted for 0.3% of covered drugs and 22% of total gross Medicare drug spending in 2021 (Figure 1). The top 100 drugs, representing just 3% of covered drugs, accounted for 61% of total gross spending that year.

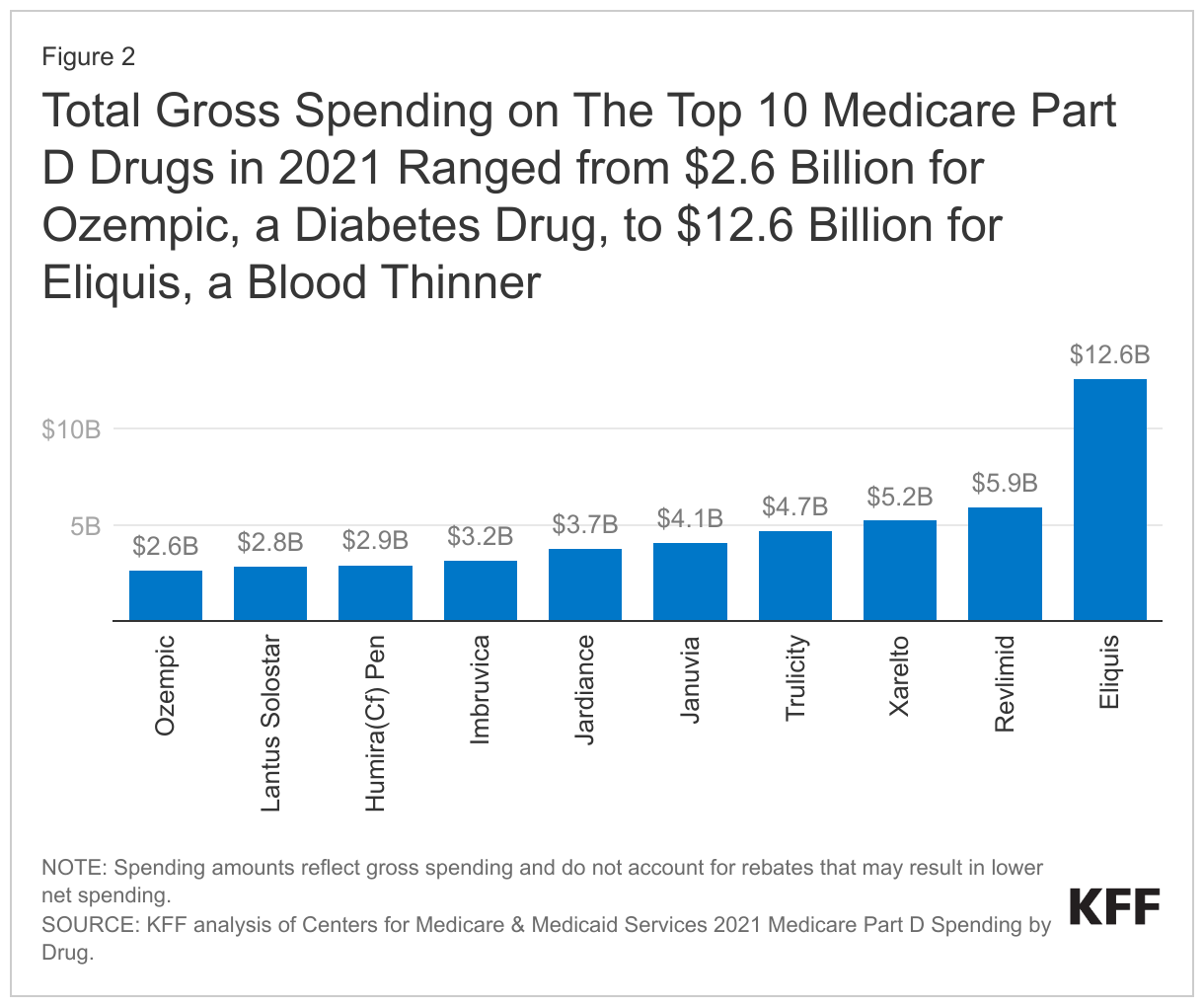

Total gross spending on the top 10 Medicare Part D drugs in 2021 ranged from $2.6 billion for Ozempic, a diabetes drug, to $12.6 billion for Eliquis, a blood thinner

In the aggregate, gross Medicare drug spending on the top 10 Part D drugs in 2021 was $48 billion. Eliquis, a blood thinner manufactured by Bristol Myers Squibb, was the top-selling drug, accounting for a quarter of this total, or $12.6 billion (Figure 2). Gross Medicare Part D spending exceeded $5 billion for both Revlimid, a treatment for multiple myeloma also manufactured by Bristol Myers Squibb, and Xarelto, a blood thinner manufactured by Janssen.

Five of the 10 top-selling Part D drugs in 2021 are diabetes drugs: Trulicity, Januvia, Jardiance, Lantus Solostar, and Ozempic. Notably, Ozempic belongs to a class of medications that have gained attention in recent months because they are highly effective weight loss agents. Manufactured by Novo Nordisk, Ozempic was approved by the FDA in 2017 as a treatment for type 2 diabetes. While Medicare does not cover Ozempic when prescribed off-label for weight loss due to the current law prohibition on Medicare coverage of drugs when used for weight loss, it is covered as a diabetes drug. Gross Part D spending on Ozempic, used by 0.5 million Part D enrollees in 2021, totaled $2.6 billion.

Also included in the top 10 is Imbruvica, a cancer treatment manufactured by Pharmacyclics, with gross Medicare spending of $3.2 billion in 2021, and Humira Citrate-free (Cf) pen, a treatment for rheumatoid arthritis (among other conditions), manufactured by Abbvie, with gross Medicare spending of $2.9 billion in 2021. (While the original version of Humira was approved in 2002, Abbvie launched the citrate-free version in 2018). Gross Medicare spending across all formulations of Humira totaled $4.7 billion in 2021, including the citrate-free and original versions and various formulations and dosages of each version approved for different indications and populations.

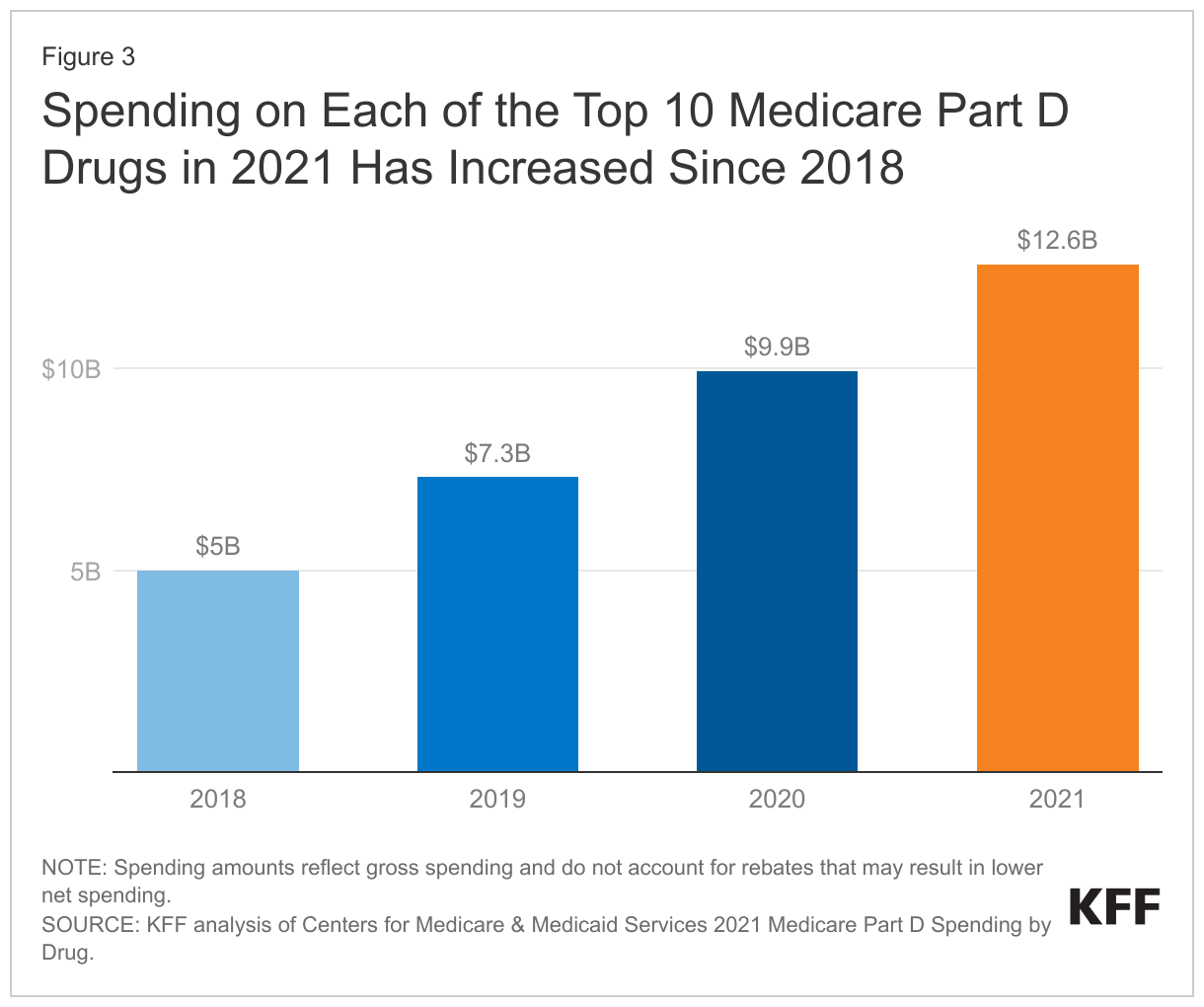

In the aggregate, gross Medicare spending for the 10 top selling Part D drugs more than doubled between 2018 and 2021

Between 2018 and 2021, aggregate gross spending on the 10 top-selling drugs in 2021 increased from $22 billion to nearly $48 billion. The increase in gross spending on these 10 drugs alone accounted for more than half of the increase in gross Medicare spending across all covered Part D drugs over these years. In the aggregate, gross Part D spending rose from $166 billion in 2018 to $216 billion in 2021.

Over these years, total gross Part D spending on Eliquis, the top selling drug in Medicare Part D in 2021, increased by 2.5 times from $5 billion in 2018 to $12.6 billion in 2021; gross spending for the diabetes drug Trulicity more than tripled from $1.4 billion to $4.7 billion; and gross spending on the diabetes drug Jardiance increased more than five times from $0.7 billion to $3.7 billion (Figure 3). For all of these drugs, the percentage increase in gross spending between 2018 and 2021 outpaced the percentage increase in the number of users over these years (data not shown, see Figure 2 for number of users per drug in 2018 and 2021).

Conclusion

The Medicare drug price negotiation program established by the Inflation Reduction Act is designed to target high-spending drugs that have been on the market for several years and lack generic or biosimilar competition. CBO estimates nearly $100 billion in Medicare savings between 2026 and 2031 from the drug negotiation program. Our analysis shows that Medicare Part D spending is highly concentrated among a small share of covered brand-name drugs, and that increases in gross spending on the 10 top-selling drugs have contributed to a substantial increase in overall Medicare drug spending in recent years.

While this analysis is not designed to identify which drugs will be selected for negotiation for 2026, two of the 10 top-selling Part D drugs in 2021 would not be eligible for selection based on when they were approved (Trulicity, a biologic approved in 2014, and Ozempic, a small-molecule drug approved in 2017) and three would not be eligible for selection based on generic or biosimilar availability in 2023 (Revlimid, Humira, and Lantus). The final list will be determined based on more current spending data than is publicly available and consideration of several factors not included here. While all of the 10 top-selling Part D drugs in 2021 will not be included on the list of 10 drugs selected for price negotiation this year, this analysis suggests that targeting negotiation on a small number of high-spending drugs could affect a disproportionate share of Medicare drug spending in the future.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

This analysis is based on 2021 Medicare Part D Spending by Drug data from the Centers for Medicare & Medicaid Services (CMS). The data includes spending for beneficiaries in both traditional Medicare and Medicare Advantage who are enrolled in Medicare Part D plans.

Drug spending metrics for Part D drugs presented in the CMS data are based on the gross drug cost, which represents total spending for the prescription claim, including Medicare, plan, and beneficiary payments. The Part D spending metrics do not reflect manufacturer rebates or other price concessions, because CMS is prohibited from publicly disclosing such information.

We sorted the list of drugs in the Part D dashboard in 2021 (n=3,566) by total spending and calculated the percent of total spending accounted for by each drug, summing across the top 10, 15, 20, 50, and 100 drugs ranked by total spending.

We used the FDA’s Drugs@FDA database to identify FDA approval dates for the top 10 drugs by Part D gross spending in 2021.