Medicaid Spending and Enrollment: Updated for FY 2022 and Looking Ahead to FY 2023

Over the past two years, the COVID-19 pandemic and recession have had significant implications for Medicaid spending and enrollment. Early in the pandemic, Congress passed the Families First Coronavirus Response Act (FFCRA), which authorized a 6.2 percentage point increase in the federal Medicaid match rate (“FMAP”) for states that meet certain “maintenance of eligibility” (MOE) requirements, including a continuous enrollment requirement. The additional funds were retroactively available to states beginning January 1, 2020 and continue through the quarter in which the public health emergency (PHE) period ends. States must meet MOE requirements through the end of the month in which the PHE ends.

The current PHE declaration is set to expire in mid-April 2022. However, it is now expected that the PHE will be extended through at least mid-July 2022 (the beginning of state fiscal year (FY) 2023 for most states) since the Biden administration indicated it would give states 60 days-notice before the PHE is terminated or is allowed to expire. While uncertainty remains around the duration of the PHE, the unwinding of the PHE will have significant implications for state Medicaid enrollment and spending trends, which states have begun to plan for.

In February 2022, the Kaiser Family Foundation (KFF) and Health Management Associates (HMA) fielded a rapid, mini-survey of Medicaid directors in all 50 states and the District of Columbia as a follow-up to the annual Medicaid Budget Survey conducted in summer 2021. At the time of the latest survey, most states were mid-way through FY 2022 and governors were releasing proposed budgets for FY 2023.1 A total of 44 states responded to the survey,2 although not all states answered every survey question. At the time of this survey, a majority of responding states’ spending and enrollment projections assumed the PHE would not be extended past April 2022, meaning projections assumed the MOE continuous enrollment requirement would end April 30, 2022 and the enhanced FMAP would end June 30, 2022. This brief explores Medicaid enrollment and spending growth estimates, as reported by state Medicaid directors, for FY 2022 and projections for FY 2023. Median calculations were used throughout the analysis.3 Extensions of the PHE would likely mean that increases in state spending and decreases in enrollment will occur later than what states have projected in our survey, but still within FY 2023 if the PHE is not extended beyond July.

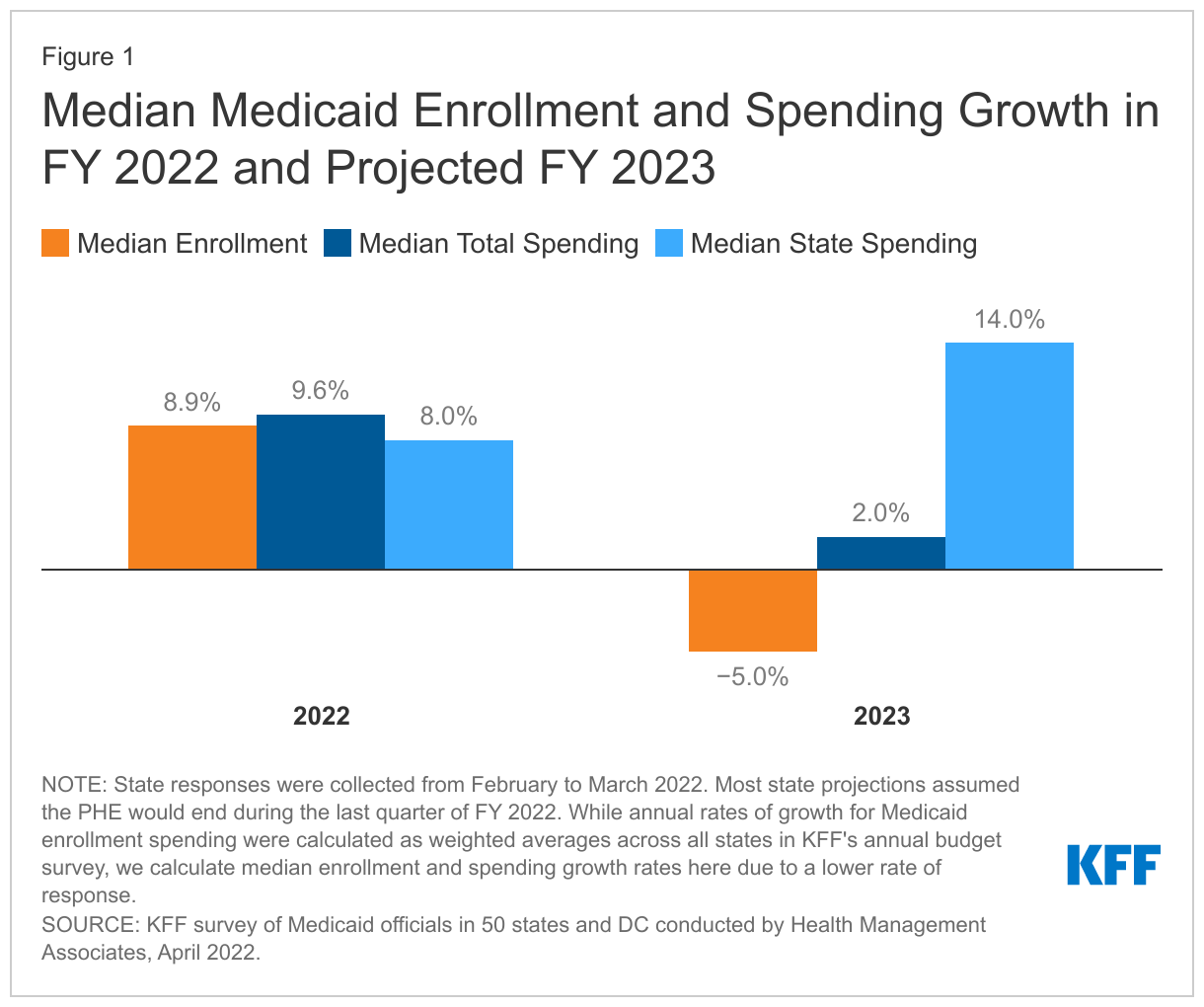

State Medicaid agency reported growth rates for FY 2022 show increasing Medicaid enrollment and spending, reflecting state assumptions about the end of the PHE (Figure 1). Most states assumed that the PHE would be in place through the last quarter of FY 2022 reflecting the continuation of the MOE and fiscal relief provisions. Among responding states, the median enrollment growth rate was 8.9% for FY 2022. Many states identified ACA expansion adults as the eligibility group with the most enrollment growth so far in FY 2022, but with notable enrollment growth in other eligibility groups including children, parents, pregnant women, and other adults. Among states that responded to the mini-survey, median total spending was 9.6% in FY 2022. Among responding states, the median state spending growth rate was 8.0% in FY 2202. Enrollment and total spending growth rates reported here are higher and the state spending growth rate is lower than projections provided by states in the summer 2021 annual Medicaid Budget Survey due to updated assumptions about the duration of the PHE (earlier projections largely assumed the PHE would end at the end of December 2021).

State Medicaid agencies project enrollment and total spending growth will decline or slow in FY 2023 as a majority of states assumed the PHE would end in the last quarter of FY 2022 (Figure 1). At the time of the mini-survey, over three-quarters of state projections assumed the FFCRA enhanced FMAP would expire at the end of FY 2022, or June 30, 2022. Among responding states, enrollment is projected to decline by 5.0% in FY 2023, with most states pointing to the unwinding of the PHE and the MOE requirements as the most significant downward enrollment change driver. States expect to see larger enrollment declines across eligibility groups that experienced notable growth during the PHE (e.g., expansion adults, parents, children, and other adults). The median total Medicaid expenditure growth rate for responding states slows to 2.0% in FY 2023 with almost two-thirds of responding states indicated lower enrollment as the most significant downward driver for total Medicaid spending. Despite slowing total spending growth, states identified some upward drivers for FY 2023 including increases in utilization (6 out of 44) and provider reimbursement rates (15 out of 44). Some states (9 out of 44) noted higher enrollment could remain an upward pressure as it takes states time to process redeterminations and renewals following the end of the MOE.

For FY 2023, state Medicaid agencies project the state share of Medicaid spending will increase sharply by 14.0% (Figure 1). The state share of Medicaid spending typically grows at a similar rate as total Medicaid spending growth unless there is a change in the FMAP rate, like during the PHE, causing state spending on Medicaid to decline as federal support increases. States expected state spending growth to accelerate in FY 2023 following the projected end of the PHE and enhanced FMAP, as states will need to replace the expiring federal funds with state funds unless they make other changes to reduce spending.

Looking Ahead

While state economic conditions have improved and COVID-19 vaccines are now available for most U.S. residents, uncertainty remains around the trajectory of the pandemic and the duration of the PHE, especially with the rise of a new Omicron subvariant, BA.2. As states approach the end of FY 2022 and adopt budgets for FY 2023 (which begins in July for most states), this uncertainty has big fiscal implications. Medicaid plays a significant role in state budgets and has played a key role in the COVID-19 response and recovery across states. Unlike the federal government, states must meet balanced budget requirements, so dealing with these uncertainties makes it difficult to budget appropriately.

When the PHE and continuous enrollment requirement ends, states will begin processing redeterminations and renewals, likely leading to enrollment declines and decreased total Medicaid spending growth. The end of the PHE, however, will also end the enhanced FMAP, requiring states to increase state spending to replace the expiring federal funds.

Changes in Medicaid enrollment and spending are an inevitable consequence of the end of the PHE, but when they occur will depend on when the PHE does in fact end. And, the magnitude of the changes will depend on how states react. States will largely be responsible for managing the unwinding of the PHE and continuous enrollment requirement, which will likely lead to significant variation in Medicaid spending and enrollment growth trends across states.

- A few states will enact biennial budgets for FY 2023 and FY 2024 and some states with previously enacted biennial budgets may introduce/consider revised or supplemental budgets. ↩︎

- The 7 states that did not respond were: Connecticut, Georgia, Mississippi, New Mexico, Ohio, Pennsylvania, and Utah. The 44 responding states accounted for over three-quarters of total Medicaid enrollment. ↩︎

- Medians are calculated among all states that responded to each growth rate question. Number of respondents to each question varied. For FY 2022, 44 states reported Medicaid enrollment and expenditure growth rates. For FY 2023, 33 states reported enrollment growth rates, 37 states reported total expenditure growth rates, and 36 states reported state expenditure growth rates ↩︎