Those Long Lines To Enroll In The ACA

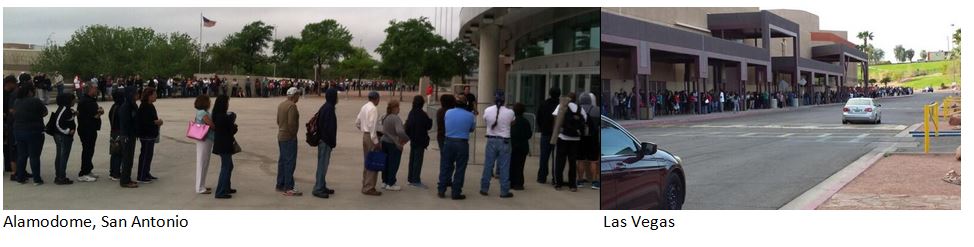

On the last day of open enrollment for private insurance plans under Obamacare Twitter was full of powerful photographs of people waiting in long lines to sign up for coverage.

The photos were a signal that the Administration was going to reach its goal of seven million exchange enrollees in year one; a remarkable comeback from the rollout woes of October and November.

They also showed that people procrastinate, especially when it comes to insurance, just as they do when they file their taxes; about a quarter of all tax filings are made in the last two weeks before the deadline.

And the lines show that the mandate and the deadline have an effect, even if it took until the last minute for many people to act on it.

But the pictures showed something else as well. Those people weren’t online, they were lining up at community centers and local government agencies. When they finally decided to enroll they wanted to go somewhere and talk to a real person. And they felt they needed help navigating the enrollment process.

A survey of the uninsured we did in California recently showed that almost seven in ten have been uninsured for two years or more and about three in ten have never had insurance. More than three in ten do not have internet access at home and roughly one in five say they don’t have any access to the internet. Studies show that health insurance literacy – the percentage of uninsured people who know what a premium is or what a deductible is – is low. For the long term, harder to reach uninsured, enrolling will never be as simple as shopping on Travelocity or Amazon.com. Reaching them will take hands on community based outreach.

Experience so far shows that outreach can be reinforced by targeted media campaigns emphasizing how the tax credits offered under the law can make insurance more affordable. It is also important to emphasize the deadline and the penalty if the uninsured don’t buy insurance. The tax credits – and Medicaid, especially in the half of states that have decided to expand eligibility under the ACA – are important to outreach messages because the uninsured have always found insurance unaffordable in the past and need a reason to believe it might now be something they can finally afford.

Through a quirk in the law, states operating their own health insurance exchanges had access to substantial federal grant dollars to conduct outreach and consumer assistance. Resources in states using the federally-operated health insurance marketplace were much more limited since an appropriation to support Obamacare was never going to get through the current Congress.

California, which operates its own exchange, had more money for outreach from public and private sources than all of the federal exchange states have combined.

It’s hard to see where more money for outreach will come from in the short term. Foundations can help at the margin at the state and local level. State governments that have embraced the idea of expanding coverage might be able to do more. It starts with the recognition that while a working website is critical to the ACA, and to enrolling people with health insurance experience who are likely to be healthier to ensure a sound risk pool, enrolling the long term uninsured will take hands on outreach at the community level. That’s one thing the pictures of the long lines showed clearly. If the ACA is to reach the uninsured who need its coverage expansions most, it is – and ultimately needs to be – much “more than a website”.