Quantifying Tax Credits for People Now Buying Insurance on Their Own

A number of states have recently released information on what premiums will be in the individual insurance market in 2014, when significant changes in that market take effect due to the Affordable Care Act (ACA). In some cases, states have provided estimates of how those premiums compare to what people buying their own insurance are paying today.

However, these premiums are in effect “sticker prices” that many people will not pay because they will be eligible for federal tax credits under the ACA to offset the cost of insurance. In this data note, we explain how the tax credits will work and estimate how much premium assistance people now buying their own insurance will be eligible for in 2014.

Why Premiums in the Individual Market Will Change

There are a number of reasons why individual market premiums will change, both overall and for any given individual now buying coverage:

- Prohibiting discrimination against people with pre-existing health conditions will tend to raise premiums as higher cost individuals who have previously been excluded from the market buy coverage. This may be offset by an influx of younger and healthier people, due to the ACA’s individual mandate and premium subsidies for low- and middle-income people buying insurance in new health insurance marketplaces (also known as exchanges).

- Eliminating premium surcharges based on health status and limiting premium variation due to age will tend to lower premiums for people who are older and sicker and raise premiums for people who are younger and healthier. Also, eliminating gender-based rating will generally result in higher premiums for younger men and lower premiums for younger women.

- Establishing a minimum level of coverage will generally raise premiums for people who are buying skimpier coverage today, though it will also lower their out-of-pocket costs on average when they use services.

- Creating a $10 billion reinsurance pool to reimburse insurers for high-cost enrollees in the individual market in 2014 will tend to lower premiums.

Premiums will be higher in 2014 for some current individual market purchasers and lower for others, and on average will likely be higher in most states.

How Premium Tax Credits Work

Premium subsidies (in the form of federal tax credits) will be available for people buying their own insurance in new marketplaces or exchanges who have incomes from 100% up to 400% of the poverty level (about $24,000 to $94,000 per year for a family of four in 2014). Those with access to affordable employer-provided insurance or Medicaid are ineligible for tax credits.

The amount of the tax credit is based on a benchmark premium, which is the cost of the second-lowest-cost silver plan in the area where a person lives. The tax credit equals that benchmark premium minus what the individual is expected to pay based on their family income (which is calculated on a sliding scale from 2% to 9.5% of income).

Here is how the calculation might work for a 40-year-old individual making $30,000 a year:

- Estimated benchmark premium for a 40-year old = $3,857 per year (which will vary from area to area)

- Person is responsible for paying 8.37% of their income = $2,512

- Tax credit = $1,345

The tax credit can be used in any plan offered in the health insurance marketplace, so the person would end up paying less than $2,512 to enroll in the lowest cost silver plan or a lower cost bronze plan, and more to enroll in a higher cost plan. A calculator from the Kaiser Family Foundation provides subsidy estimates for families of varying characteristics.

Estimating Tax Credits for People Currently Buying in the Individual Market

While premium tax credits will provide substantial subsidies to people now buying individual insurance, it can be difficult to characterize the level of subsidies because they vary so much based on personal characteristics (e.g., age, income, family size, and place of residence). To provide a sense of how much assistance these subsidies will provide, we quantified how much of a tax credit on average current individual market enrollees will be eligible for. We look at people who are currently purchasing their own insurance and are anticipated to continue to do so in 2014 because they do not have access to employer coverage and are not eligible for Medicaid (including expanded Medicaid eligibility in states that have adopted the ACA expansion) or the Child Health Insurance Program.

Our analysis – which is described more fully in the methodology appendix – is based on premium estimates from the Congressional Budget Office (CBO) and the characteristics of current individual market enrollees in the federal government’s Survey of Income and Program Participation. While our premium estimate is based on CBO’s projection and actual premiums will vary from area to area, the premium values we are using are consistent with those that have been released to date in several states.

Using CBO’s estimate of an average premium for the second-lowest-cost silver in 2016, we estimate that the national average benchmark premium for a 40-year-old in 2014 would be $3,857 per year (or $321 per month). Benchmark premiums at other ages are based on uniform age factors that have been established in regulations issued by the Department of Health and Human Services.

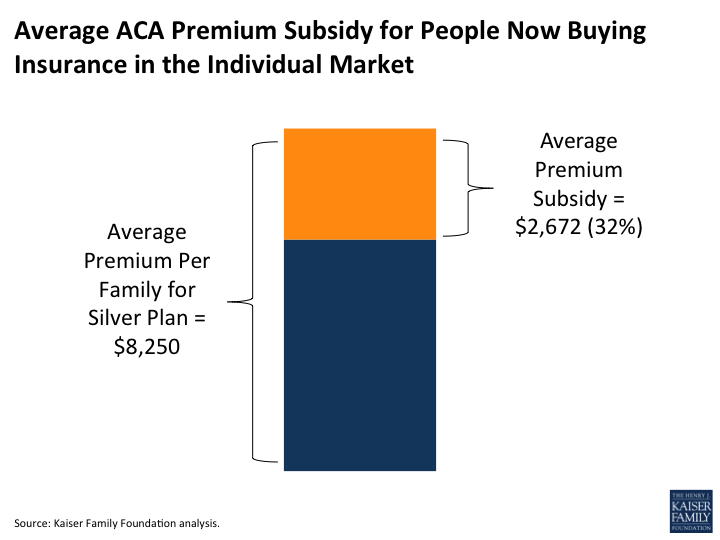

We estimate that current individual market purchasers will face an average premium per family for the second-lowest-cost silver plan of $8,250 in 2014. This is an average premium across families of all sizes. Most current individual market enrollees are in families of one person (55%) or two people (29%). (Note that for the purposes of tax credit eligibility under the ACA, families are defined as including people who are claimed as dependents on an income tax return. Our estimates reflect that definition to the extent possible with data available.)

About half (48%) of people now buying their own insurance would be eligible for a tax credit that would offset their premium. This does not include over one million adults buying individual insurance today who will be eligible for Medicaid starting in 2014 (i.e., they have family income up to 138% of the poverty level and are living in states that have decided to expand Medicaid under the ACA).

Tax credits have the potential to cover a substantial portion of the premiums paid by current individual market enrollees:

- Across all current individual market purchasers anticipated to continue buying coverage, the average tax credit their families would be eligible for would be $2,672. Assuming all eligible current enrollees applied for a tax credit, the subsidy would reduce the premium for the second-lowest-cost silver plan by an average of 32% across all people now buying insurance in the individual market.

- Among the approximately half of current enrollees who will be eligible for tax credits, the average subsidy would be $5,548 per family, which would reduce their premium for the second-lowest-cost silver premium by an average of 66%.

- Tax credits would subsidize a higher share of the premium for individuals choosing to enroll in lower cost plans. For example, enrolling in a bronze plan from the same insurer offering the benchmark silver plan would mean an average subsidy across all current individual market enrollees of about 38% of the premium and an average subsidy among only those eligible for tax credits of 77%.

Methodology

We estimated the availability and size of health insurance premium subsidies for people enrolled in non-group coverage using data from the 2008 Survey of Income and Program Participation (SIPP), Wave 6 (interview period April to July, 2010).

Individuals were grouped into families based on a series of decision rules designed to approximate what is referred to as “health insurance unit (HIU)” or “tax filing unit,” which is the basis for determining eligibility for premium tax credits under the ACA.

The analysis is based on the universe of people currently purchasing non-group insurance (also referred to as individual insurance) and anticipated to continue to do so. Based on ACA rules regarding eligibility for premium tax credits in health insurance marketplaces (also known as exchanges), certain groups of current non-group purchasers were assumed to obtain alternative coverage:

- All individuals belonging to a health insurance unit where any member received health insurance through work or an offer of employer-sponsored insurance. All members of a family were assumed to have access to employer-sponsored insurance if one member of the family was offered coverage. People with access to affordable employer coverage are ineligible for exchange-based premium tax credits.

- Adults with incomes up to 138% of the poverty level and living in a state that has decided to expand Medicaid under the ACA (as of July 1, 2013). People eligible for Medicaid are ineligible for tax credits in exchanges. In states that choose not to expand, adults with incomes below 100% of the poverty level are included in the analysis but are ineligible for premium tax credits.

- Children (up to age 18 and full-time students up to age 20) with family income that would qualify them for Medicaid of the Child Health Insurance Program (CHIP) based on current eligibility levels.

- All individuals currently receiving Medicare or Medicaid as well as purchasing non-group coverage, who would be ineligible for premium tax credits and presumed not to purchase exchange-based coverage starting in 2014.

There are a small number of uninsured people (under 200,000 nationwide) living in families where another person is currently buying non-group coverage, and they are assumed to remain uninsured for the purposes of this analysis. If they purchased coverage, average tax credits would be higher than are reported here.

Health insurance units were assigned a premium based on age and family composition, assuming all current non-group purchasers (excluding those described above) continue to buy coverage. Premiums are based on our estimates for 2014 using the latest projection from the Congressional Budget Office (CBO) of the national average premium for the second-lowest-cost silver plan in 2016. Some states have begun to report approved premiums for 2014, and these early reports suggest CBO’s estimates are reliable.

Since tax credits are determined at the family level, all premium and subsidy figures are reported for adult purchasers based on the aggregate amounts for their entire health insurance units.