Data Note: 2020 Medical Loss Ratio Rebates – Data Note – 9346-02

The Medical Loss Ratio (or MLR) requirement of the Affordable Care Act (ACA) limits the portion of premium dollars health insurers may use for administration, marketing, and profits. Under the ACA, health insurers must publicly report the portion of premium dollars spent on health care and quality improvement and other activities in each state in which they operate.

The Medical Loss Ratio provision requires insurance companies that cover individuals and small businesses to spend at least 80% of their premium income on health care claims and quality improvement, leaving the remaining 20% for administration, marketing, and profit. The MLR threshold is higher for large group insured plans, which must spend at least 85% of premium dollars on health care and quality improvement. Insurers failing to meet the applicable MLR standard have been required to pay rebates to consumers since 2012 (based on their 2011 experience). Currently, MLR rebates are based on a 3-year average, meaning that 2020 rebates are calculated using insurers’ financial data in 2017, 2018, and 2019. Insurers may either issue rebates in the form of a premium credit or a check payment and, in the case of people with employer coverage, the rebate may be shared between the employer and the employee. Insurers will begin issuing rebates later this fall. Rebates issued in 2020 will go to subscribers who were enrolled in rebate-eligible plans in 2019.

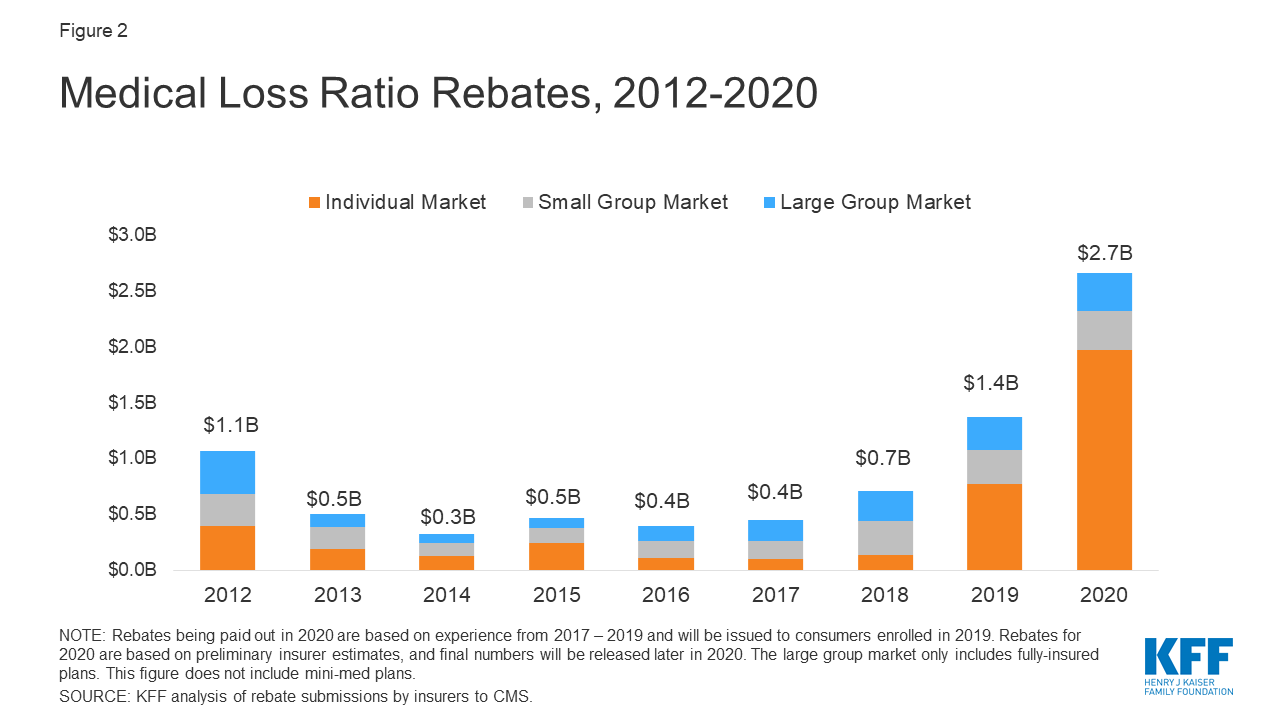

Using preliminary data reported by insurers to state regulators and compiled by Market Farrah Associates, we estimate insurers will be issuing a total of about $2.7 billion across all markets – nearly doubling the previous record high of $1.4 billion last year. The amount varies by market, with insurers reporting about $2 billion in the individual market, $348 million in the small group market, and $341 million in the large group market. These amounts are preliminary estimates, and final rebate data will be available later this year.

| Table 1: Preliminary Estimates of Insurer Rebate Payments in 2020 | ||||

| Individual Market | Small Group Market | Large Group Market | Total – All Markets | |

| Total Rebates | $1.97 billion | $348 million | $341 million | $2.66 billion |

| Number of members owed a rebate* | 4,735,000 | 189,000 | 2,988,000 | 7,912,000 |

| Average rebate per member | $420 per member | $1,850 per member | $110 per member | $340 per member |

| NOTES: *The number of members is rounded to the nearest thousand, and shows the average 2019 monthly membership in plans that owe rebates in 2020. These figures do not include health plans managed by the California Department of Managed Health Care. SOURCE: KFF analysis of data from Mark Farrah Associates Health Coverage Portal TM. |

||||

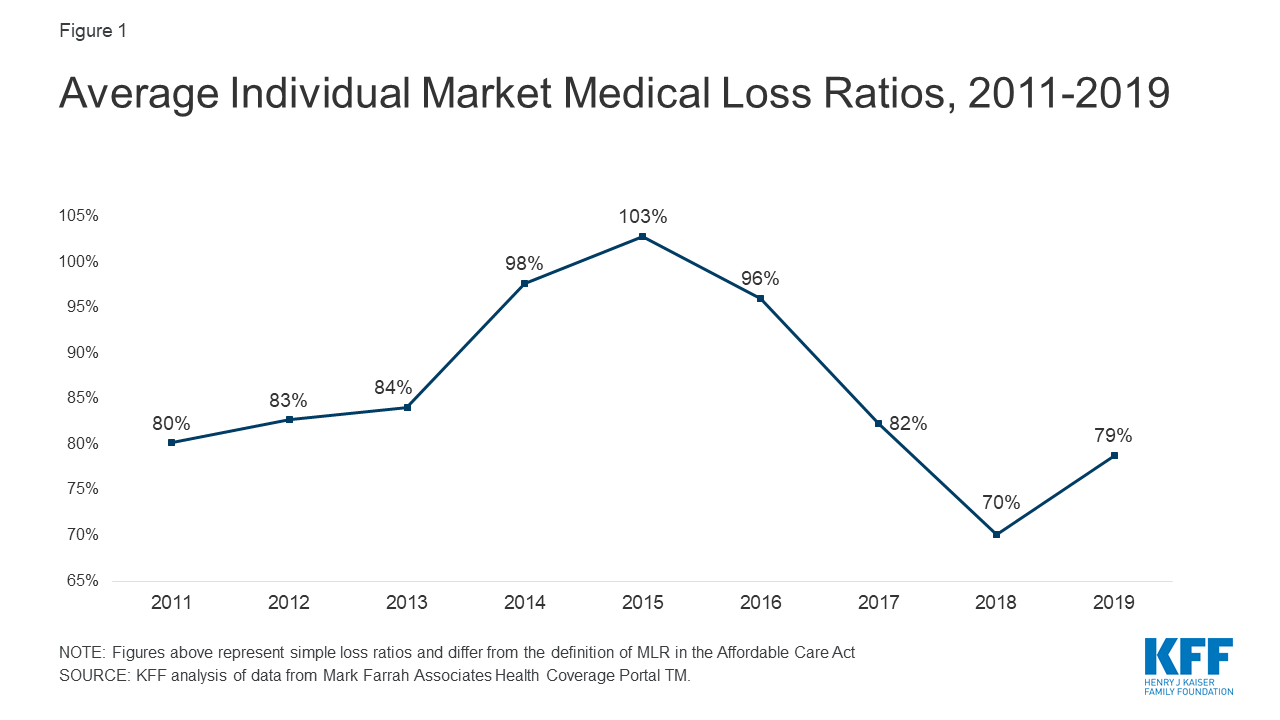

Insurers in the individual market in 2018 and 2019 are driving this record-high year of MLR rebates in 2020. Rebates issued in 2020 are based on 2017, 2018, and 2019 financial performance. As our previous analysis of insurer financial performance found, in 2017 financial performance in the market had begun to stabilize as premiums rose. Insurers in 2018 were highly profitable and arguably overpriced. In 2019, despite the absence of the individual mandate penalty and premiums dropping a bit on average, insurers continued to perform strongly. On average, insurer loss ratios (the share of premium income paid out as claims) in the individual market in 2019 were 79%. (This is a simple loss ratio; the ACA allows insurers to make some adjustments to this ratio when calculating rebates).

Figure 1: Average Individual Market Medical Loss Ratios, 2011-2019

Rebates may either be paid out in the form of a premium credit (for those who are currently enrolled with the same insurer as in 2019), or as a lump-sum payment. Last year, most insurers reported issuing rebates in the form of a lump sum.

Figure 2: Medical Loss Ratio Rebates, 2012-2020

Rebates in the small and large group markets are more similar to past years. In the case of employer-sponsored insurance plans, the cost of coverage is often split between the employer and employees. Therefore, for many employer-sponsored plans, the handling of refunds to employers and employees may depend on the plan’s contract and the manner in which the policyholder and participants share premium costs. If the amount of the rebate is exceptionally small (“de minimis”, $5 for individual rebates and $20 for group rebates), insurers are not required to process the rebate, as it may not warrant the administrative burden required to do so.

As more people are expected to move into the individual market this year after losing job-based coverage, it is worth considering the possibility of future rebates based on the 2020 calendar year. The cost to insurers for covering coronavirus treatment are still unknown, but could be tens if not hundreds of billions of dollars. That said, hospitals and outpatient offices are canceling elective procedures and individuals are delaying or forgoing other care due to lessened access from social distancing measures and concerns over contracting the virus. Even if individual market insurers experience losses in 2020, it is entirely possible they will owe rebates in 2021 because those rebates will be based on 2018 and 2019 experience as well.

These high rebate estimates come at a time when insurers are working on submissions to regulators for proposed premiums for 2021, in the midst of significant uncertainty about how the coronavirus pandemic will affect health care costs. For 2021 premiums, key factors will include how many people are expected to become infected and severely ill next year, as well as how much pent up demand there may be for care delayed this year. Enrollment in individual market plans is expected to increase as millions of people lose their jobs and health insurance and qualify for a special enrollment period, but these new enrollees will not qualify for rebates when they are paid out in 2020 unless they were also enrolled at some point in 2019.