Community Health Centers: A 2013 Profile and Prospects as ACA Implementation Proceeds

Executive Summary

In 2013, more than 1,200 federally funded community health centers provided access to care for low-income populations living in medically underserved communities throughout the country. The Affordable Care Act made expansion of health centers a key part of its strategy for ensuring that these communities would realize the benefits of increased health insurance coverage for their residents. As health insurance coverage expands under the Affordable Care Act (ACA) and the demand for primary care increases, the role of health centers is likely to increase. A key question going forward is whether health centers’ expanded capacity, developed over the past five years, will be sustained going forward.

2013 profile

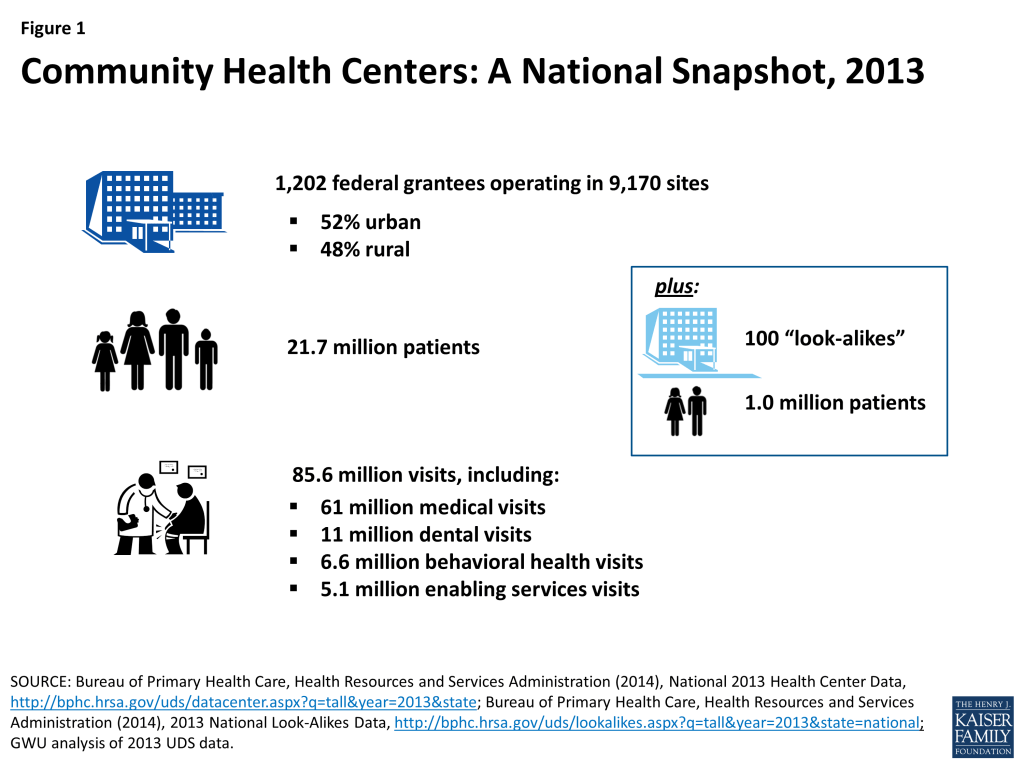

- Health centers’ safety-net role. In 2013, 1,202 federally funded health centers operating in 9,170 sites provided 61 million medical care visits, 11 million dental visits, 6.6 million visits for behavioral health needs, and 5.1 million visits for enabling services such as case management. In all, health centers provided more than 85 million visits. Another 100 “look-alike” health centers funded by states and localities served an additional 1 million patients. More than 70% of health center patients have income below 100% of the federal poverty level (FPL), which is $11,770 for an individual and $20,090 for a family of three in 2015. Nearly 60% are women; almost all (93%) are children and working-age adults. A majority of health center patients are people of color.

- Health center patients. Over one-third (35%) of health center patients were uninsured in 2013, and 41% were covered by Medicaid. As the ACA is implemented, early evidence suggests that the proportion of insured patients in the health care system will grow substantially. At the same time, however, the uninsured rate among health center patients is expected to remain high, because millions of people who will remain uninsured lack other sources of care. In 11 states and the District of Columbia, health centers serve over 30% of the low-income population.

- Scope of services. Health centers provide primary care spanning physical, dental, and behavioral health care. They also provide enabling services, such as translation and transportation, which help patients to access care. Between 2000 and 2013, the number of health centers offering dental and mental health services grew, by 22% and 81%, respectively, reflecting both increased federal resources and widespread need for such care. Although the percentage of health centers offering substance abuse services has declined slightly, dramatic growth in the number of health centers between 2000 and 2013 means also that the total number of health centers offering these services has increased.

Health centers and Medicaid

- Medicaid support. In 2013, Medicaid provided 40% of health center operating revenues, making the program the single largest source of health center financing. Medicaid’s large financing role reflects the large share of health center patients covered by Medicaid, as well as Medicaid’s prospectively set, cost-based payment system, which is also used by Medicare, CHIP, and Qualified Health Plans sold in the ACA Marketplaces. Operating grants that health centers receive through the federal annual appropriations process provide crucial support for care for uninsured patients and for services not covered by insurance. The ACA augmented regular appropriations for health centers with a dedicated five-year, $11 billion Health Center Trust Fund that has supported the establishment of new health centers and sites and initiatives to build service capacity in key areas.

- Health centers in Medicaid expansion versus non-expansion states before the ACA. Even before the ACA, health center patients in states that later expanded Medicaid were significantly more likely to be covered by Medicaid and less likely to be uninsured, compared to those in states that have not expanded Medicaid, reflecting broader Medicaid eligibility for adults in the pre-ACA period. By extension, health centers in expansion states also had higher revenues per patient and derived a larger share of their total revenues from Medicaid. Overall, leading up to 2014, they were in a stronger revenue position to expand patient capacity and the scope of their services, and their states’ decisions to expand Medicaid enhanced their position. About half of the 22 states that have not expanded Medicaid are southern states that have among the highest poverty rates in the nation as well as high uninsured rates. These states’ decisions not to expand Medicaid have a disproportionate effect on African-Americans, who reside in high numbers in the southern states and are more likely to be low-income and uninsured than the general population. One in four health center patients in the non-expansion states is African-American.

- Health center opportunities and challenges under the ACA. The share of health center patients who are uninsured is expected to decline significantly because of expanded coverage under the ACA. However, especially in non-expansion states, health centers will continue to treat high numbers and shares of uninsured people. In addition, health centers can expect to face significant uncompensated care costs even for patients who are insured, attributable to cost-sharing for covered services that low-income patients may be unable to pay, treatments and services not covered by insurance, such as vision and dental care for adults, and care provided to insured patients in plans whose provider networks do not include their health center.

Looking ahead

The ACA made significant investments in health coverage and care for disadvantaged communities. As implementation of the health reform law continues, the experience of health centers serves as one bellwether of its impact on these communities. Measures of health centers’ scope and activity, and of rates of coverage and access among their patients, are important gauges of how the ACA goals are translating into improvements for the populations and communities most at risk of disparities in health and health care. Moving forward, analyses that investigate the implications of state Medicaid expansion decisions for health centers and their patients can illuminate the relationship among Medicaid expansion, health center capacity, and access to care.

Issue Brief

Introduction

Community health centers are an integral component of the health care safety-net in the U.S., providing access to care for over 21 million mostly low-income patients in medically underserved areas across the country. The Affordable Care Act (ACA) made a major investment in the health center program to help ensure access to care as coverage expands, establishing a five-year, $11 billion trust fund to support health center growth and new construction over five years, and providing $1.5 billion to expand the National Health Service Corps (NHSC), from which health centers recruit many of their clinical staff.

This brief is the latest in an annual series of updates on community health centers produced by the Kaiser Commission on Medicaid and the Uninsured in partnership with the George Washington University’s Geiger Gibson Program in Community Health Policy. It provides a current overview of community health centers, the patients they serve, the services they furnish, and the sources of their revenues. Finally, this report considers the prospects for sustaining and building on the gains in primary care access that have been achieved for medically underserved communities as a result of the Medicaid expansion and the Health Center Fund established under the ACA.

An Overview of Health Centers

Health Centers’ Safety-net Role

The community health centers program was established in 1965 by the Office of Economic Opportunity as a small demonstration program. Under Section 330 of the Public Health Service Act, which authorized the health centers program and is now a permanent authority under the ACA, health centers must satisfy five key requirements to receive federal grant funding. They must be located in or serve medically underserved communities and populations. Their doors must be open all patients, regardless of their ability to pay. They must furnish comprehensive primary health care, defined in both federal statute and regulations. They must prospectively adjust their charges in accordance with patients’ ability to pay (i.e., sliding scale fees). And they must be governed by community boards, at least 51% of whose members are health center patients.

Over the nearly five decades since the program was established, both the number of health centers and health center patient volume have grown substantially. In 2013, 1,202 federally funded health centers located in all 50 states, the District of Columbia (DC), and six U.S. Territories, and distributed about evenly between urban and rural areas, served 21.7 million patients in 9,170 different service delivery sites (Figure 1). In addition, 100 “look-alike” health centers, which meet all federal requirements but are supported with state and local funds rather than federal grants, served 1 million patients.

Two main factors have fueled health center growth. The first is the investment of federal grant funding to build and support health centers. The second is increased revenues from the Medicaid program due to both expansions of Medicaid coverage for low-income pregnant women, children, and parents over time, and Medicaid’s prospective, cost-based “Federally Qualified Health Center” (FQHC) payment methodology, which also applies to payments made by Medicare, CHIP, and qualified health plans (QHPs) operating in the new health insurance Marketplaces. The FQHC rate enhances health centers’ capacity by covering much of the cost of care furnished to insured patients, which means that health centers do not have to use their grant funds to subsidize those patients, and can instead use their grants, as intended, to finance care for their uninsured patients and to expand both the scope of services they provide and the number of community locations in which they operate. Indeed, while health centers are serving increasing numbers of patients with Medicaid coverage, they are also serving more uninsured patients – 7.6 million in 2013, up from 4.9 million in 2003.1

Health Center Patients

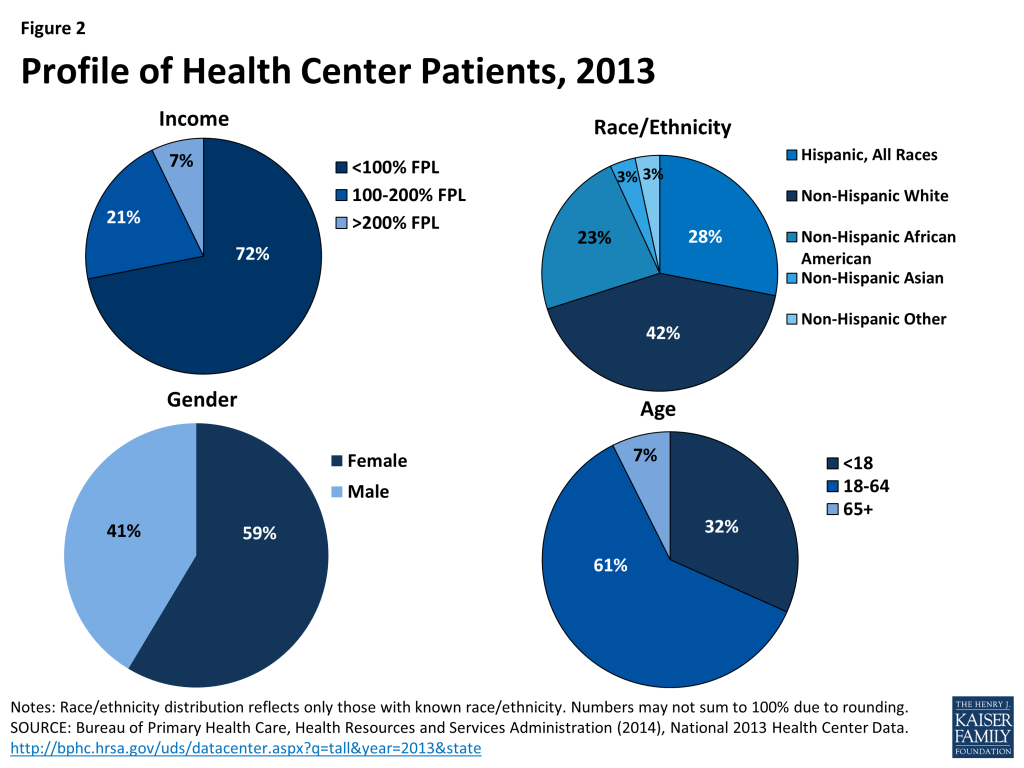

Reflecting the statutory mission of the health center program, almost three-quarters of health center patients have family incomes at or below 100% FPL (Figure 2). About six in ten patients are female. Working-age adults make up the largest share of health center patients – about 60% – while children account for roughly one-third, and about 7% are seniors. More than half (57%) of health center patients who report their race and ethnicity are people of color.

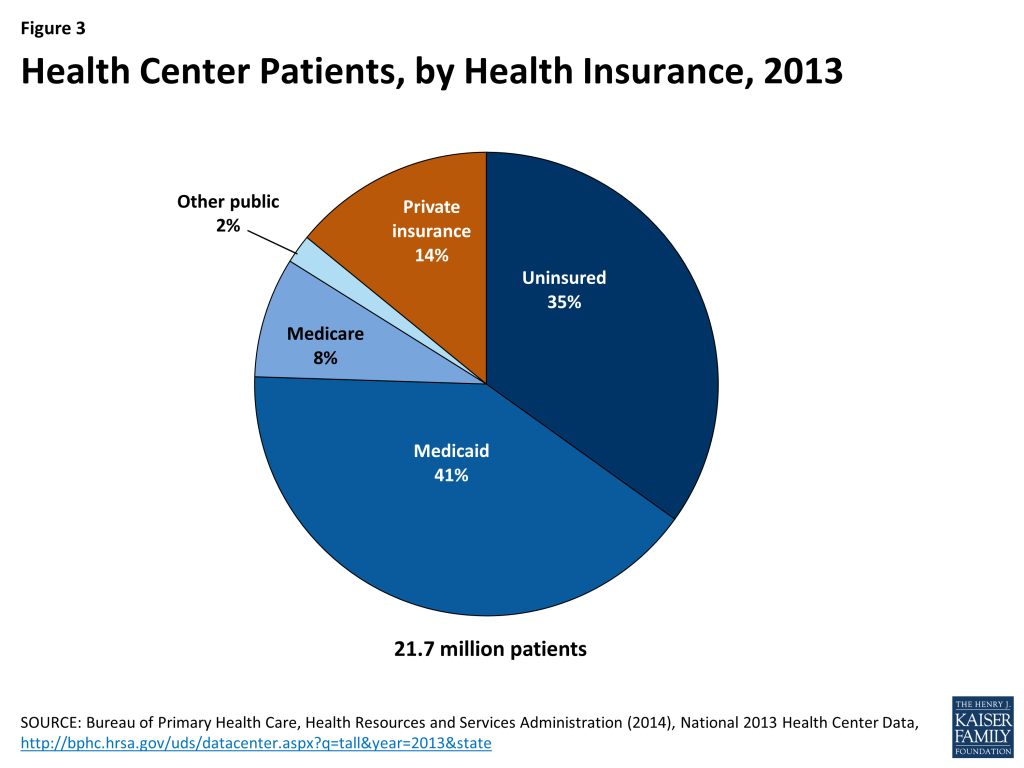

Consistent with their low income, a large share of health center patients are uninsured, and a large share have Medicaid coverage. In 2013, 35% of health center patients were uninsured (Figure 3), more than double the uninsured rate of 13% for the population overall.2 Similarly, 41% of health center patients were covered by Medicaid, compared to 16% of all Americans.

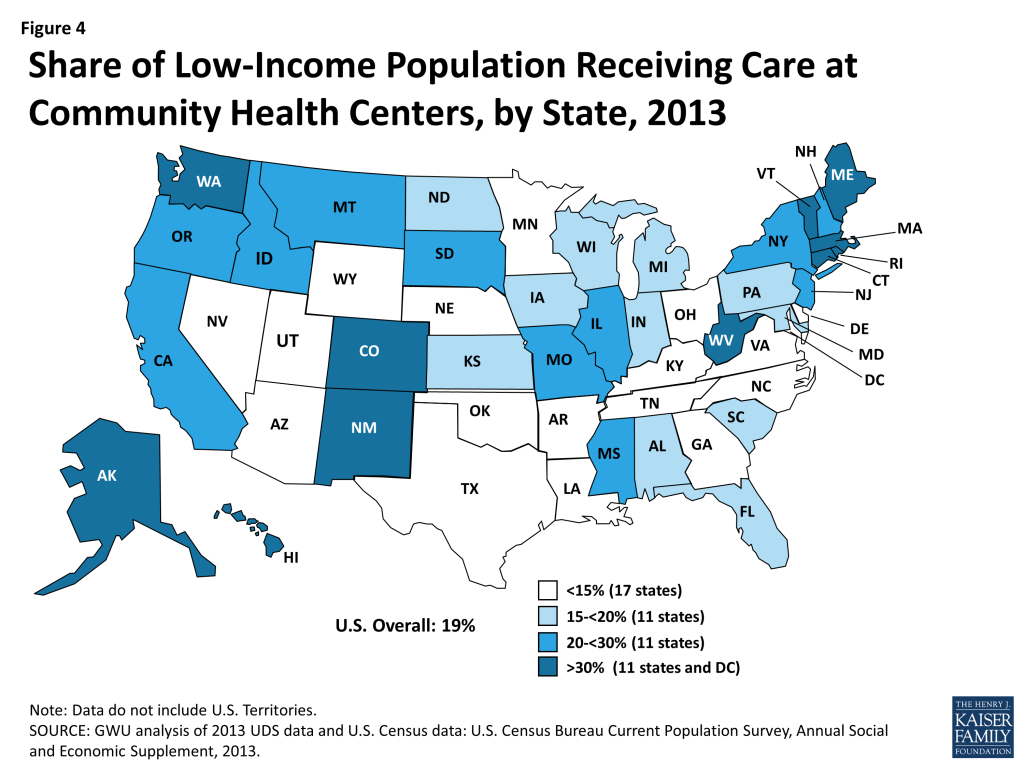

Health centers play a major role nationally in providing care for low-income populations and an even larger role in many states. In 22 states and DC, health centers serve at least one in five people with income below 200% FPL; in 11 of these states and DC, health centers provide care to more than 30% of the population with income at this level (Figure 4).

Health Center Volume, Services, and Staffing

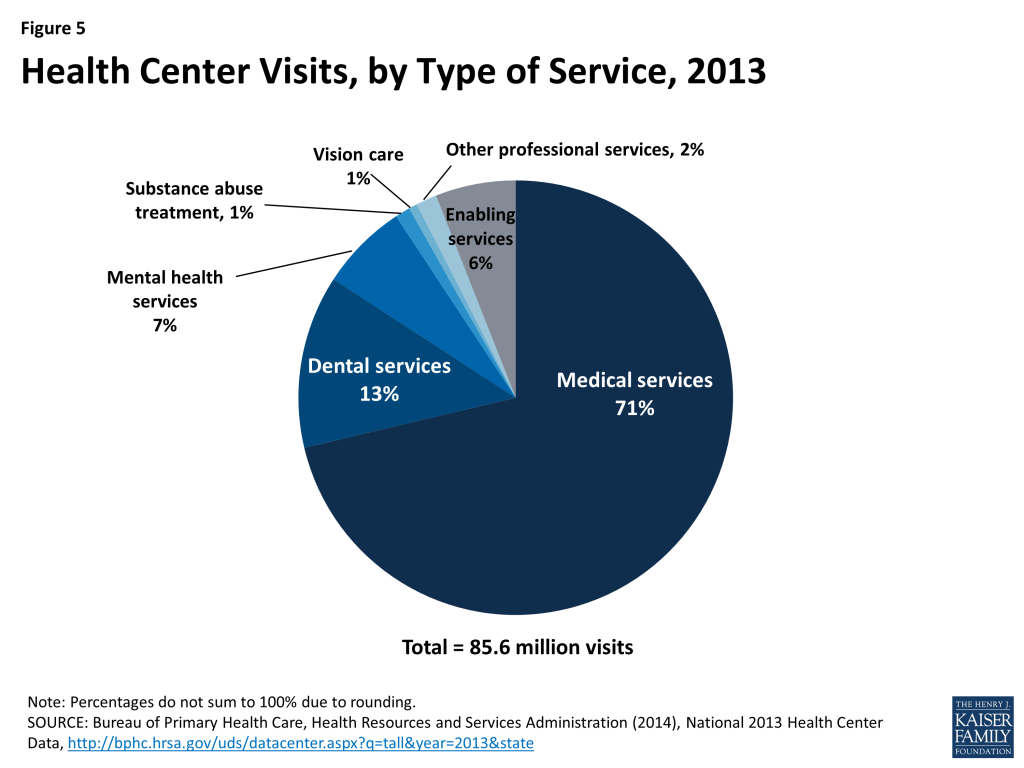

In 2013, patients made 85.6 million visits to health centers (Figure 5). The vast majority of visits (71%) were for primary medical care. Visits for dental care (13%) accounted for the next largest share of the total, highlighting health centers’ important role of as a source of oral health care in underserved communities. Another 8% of all visits were for mental health or substance abuse treatment services. In addition to clinical services, health centers offer enabling services, such as case management, transportation, and interpretation services, which help address language, cultural, and other barriers facing low-income individuals and communities. Enabling services, such as case management, transportation, and interpretation services, accounted for 6% of all health center visits in 2013.

Between 2000 and 2013, the number of health centers rose by two-thirds, from 730 to 1,202. Over this time period, both the number of patients served by health centers and the number of visits provided more than doubled (Table 1).

| Table 1: Total health centers, patients, and visits,2000-2013 | |||

| Year | Health centers | Patients(millions) | Visits(millions) |

| 2000 | 730 | 9.6 | 38.3 |

| 2002 | 843 | 11.3 | 44.8 |

| 2004 | 914 | 13.1 | 52.3 |

| 2006 | 1,002 | 15.0 | 59.2 |

| 2008 | 1,080 | 17.1 | 66.9 |

| 2010 | 1,124 | 19.5 | 77.1 |

| 2012 | 1,198 | 21.1 | 83.8 |

| 2013 | 1,202 | 21.7 | 85.6 |

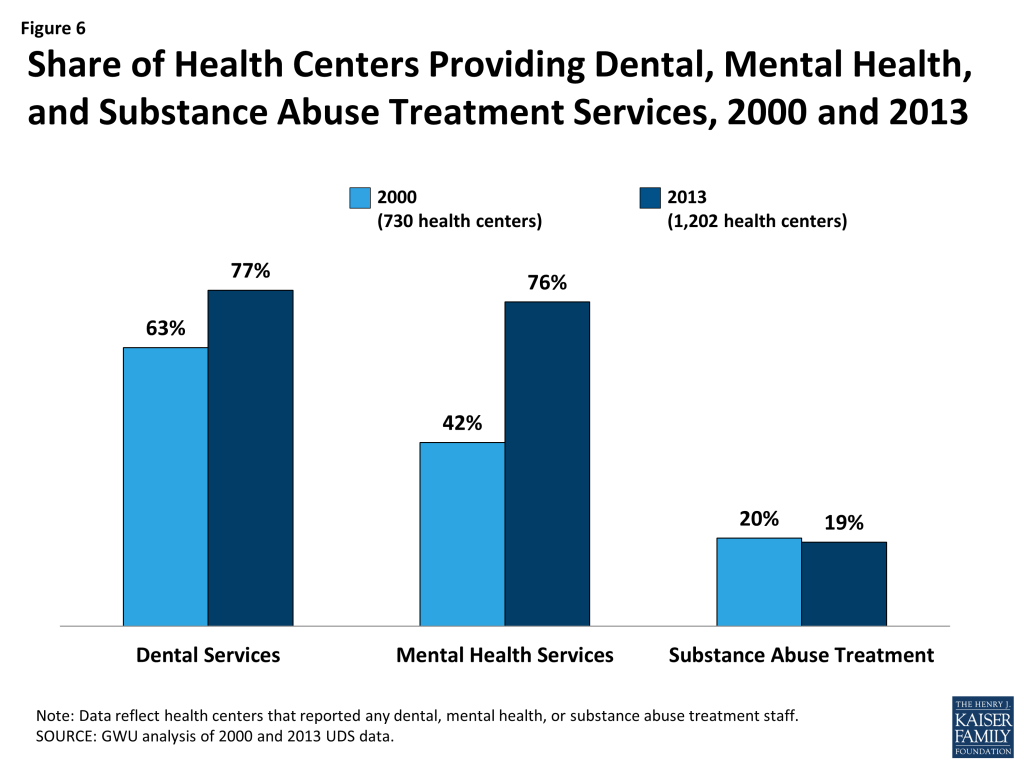

In addition, the scope of services available at many health centers expanded over this 13-year time period (as measured by the share of health centers reporting specified types of clinical staff). In particular, more than three-quarters of health centers offered dental services in 2013, compared to less than two-thirds in 2000 (Figure 6). The share offering mental health services grew even more dramatically, from 42% of health centers in 2000 to 76% in 2013. The fraction of health centers providing substance abuse treatment remained flat at about one-fifth over the period. Still, because of major growth in the number and patient capacity of health centers during this time, many more people using health centers now have access to these services.

Health centers are major employers in their communities, bringing economic benefits as well as health care to the urban and rural areas they serve. In 2013, nearly 157,000 full-time equivalent (FTE) staff, including over 10,700 physicians and more than 5,100 nurse practitioners, worked in health centers; health centers employed an average of 130 FTEs.3

Health Center Revenues

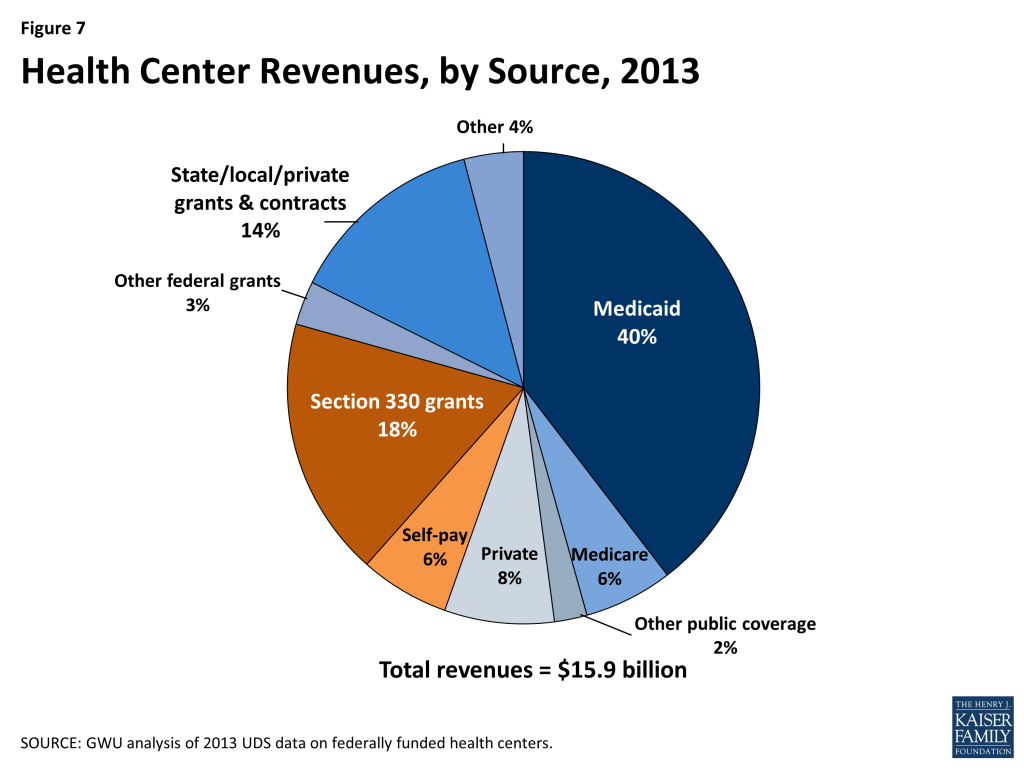

Health center revenues in 2013 totaled $15.9 billion. The single largest source of revenue was Medicaid, which accounted for 40%. Health center grants from the Bureau of Primary Health Care (BPHC), made up the second-largest share, accounting for 18%, and other federal grants provided 3%, while state, local, and private grants and contracts provided 14%. Private insurance, Medicare, and amounts paid directly by patients provided 8%, 6%, and 6% of health center revenues, respectively (Figure 7).

Health Center Quality

The quality of care provided by health centers has been extensively researched, and studies dating back to the 1970s have documented positive outcomes associated with health centers. For example, one early study found evidence that health centers contributed to the decline in infant mortality between 1970 and 1978, particularly among African-American babies.4 More recent studies show that racial and ethnic disparities in rates of low birth weight babies are small in magnitude in health centers, and narrower compared to disparities in the total population.5 6 Other research also shows that health centers are associated with reduced disparities in health care based on race and ethnicity and insured status, and with reduced disparities in health.7 8 9

Two studies point to improvements in selected outcomes associated with access to health center services in combination with health insurance coverage. One study, looking at the first 10 years in which the Medicare program was in effect, examined the impact of the earliest health centers, also established in that period, on mortality rates. The study findings suggest that health centers were associated with reductions in older adult mortality rates, and that increased use of primary care and access to lower-cost medication provided by health centers were likely important mechanisms.10 The other study, using more recent data, examined the association between health center use (a proxy for primary care access) by low-income Medicare beneficiaries and Medicare spending and clinical quality. The researchers found that, in regions where a relatively higher proportion of low-income residents were served by health centers, Medicare spending per beneficiary was significantly lower with no apparent compromise of clinical quality of care.11

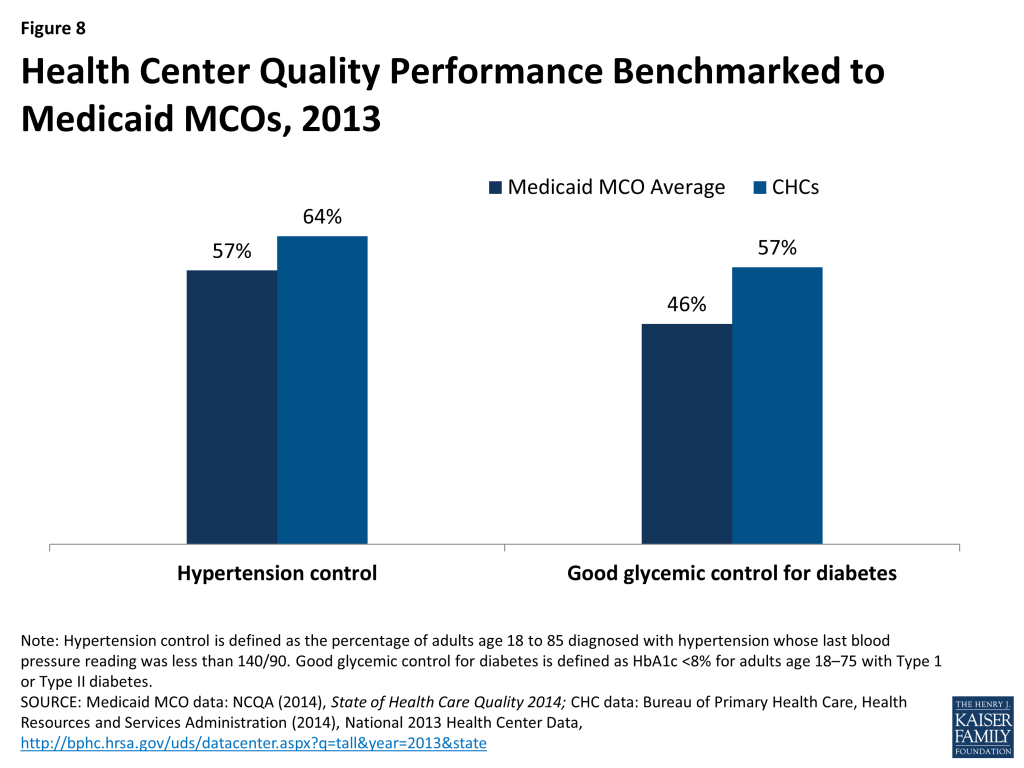

Despite serving some of the nation’s highest-risk, medically vulnerable populations, health centers provide effective care. Responding to needs in underserved communities, health centers focus on primary and preventive services, team-based care, and enabling services such as translation and transportation services and case management, which help populations who face significant barriers to access to obtain needed care. There is evidence that health centers provide better access to timely preventive services for vulnerable populations compared to typical primary care settings.12 For example, one study showed that uninsured patients who received care from health centers were 22% more likely to receive Pap tests than uninsured patients receiving care in other primary care settings.13 Health centers also perform at least as well as Medicaid MCOs on important measures of chronic care management (Figure 8).

At the same time, health centers struggle to furnish adequate health care, especially for uninsured patients, for whom referrals to specialty care outside the health center are extremely difficult to arrange. Securing referrals for Medicaid patients can be difficult as well, but as health centers increasingly develop formal affiliations with integrated health care delivery systems that provide a full range of primary and specialty care, these problems may diminish. Virtually all health centers are included in Medicaid managed care plan networks, and many are part of provider networks offered by qualified health plans (QHPs) sold in the Marketplaces.

Health Centers and State Decisions about the ACA Medicaid Expansion

Under the ACA, federal grant funds continue to flow to health centers through the regular annual Congressional appropriations process. In addition, federal allocations from the ACA Health Center Trust Fund will continue through 2015. These two sources of federal grant funding have enabled health centers to grow in recent years to more fully meet the health care needs of their communities, including the uninsured. Increased awareness of health coverage options due to ACA-related outreach efforts, and modernized and streamlined Medicaid eligibility and enrollment systems required of all states under the ACA, have also contributed to higher participation in Medicaid among uninsured people who were previously eligible but not enrolled, potentially generating increased patient revenues for health centers.

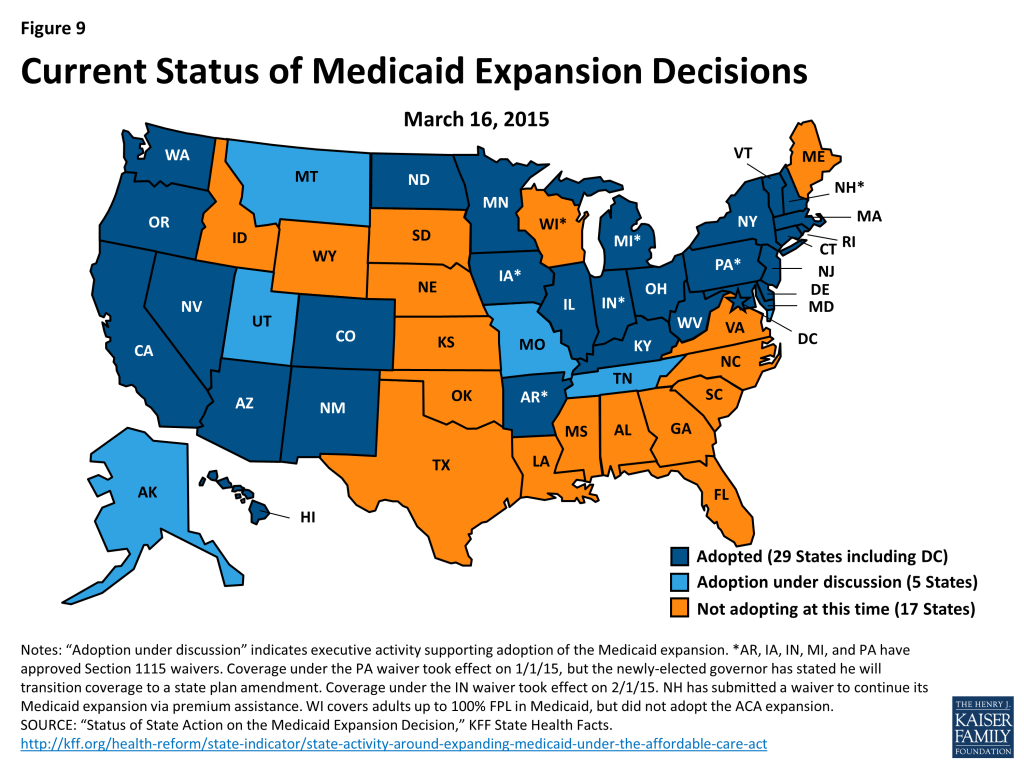

State Medicaid expansion decisions have a separate, additional impact on health centers. States that expand Medicaid provide comprehensive benefits for low-income nonelderly adults, ensuring payment for health centers that serve these patients and enhancing their ability to furnish or arrange for a broader range of services. As outlined earlier, in 2013, a majority of health center patients were working-age adults (61%). Over 70% had income at or below 100% FPL and 35% were uninsured. This profile closely matches the target population for the ACA expansion of Medicaid. Thus, state decisions to expand Medicaid could have a large positive impact on access to coverage for adult health center patients. In the 29 states (including DC) that have expanded Medicaid to date, many poor, previously uninsured health center patients have now gained access to Medicaid coverage (Figure 9). Soon, federal data on health centers will provide official figures on growth in the number and share of health center patients with Medicaid or other coverage during 2014, the first year of full ACA implementation.

In the 22 states that have so far not adopted the Medicaid expansion, close to 4 million nonelderly adults with income below 100% FPL fall into a coverage gap.14 This is so because they cannot qualify for tax subsidies to purchase QHPs sold in the Marketplace, which begin at 100%FPL. In 2013, 2.5 million uninsured adults in the 22 non-expansion states received health center services. Assuming that uninsured adult health center patients are equally as likely (72%) as uninsured adults overall to have income below 100% FPL, most of these health center patients could qualify for Medicaid if their state adopted the expansion. About half the 22 states that have not expanded Medicaid are southern states that have among the highest poverty rates in the nation as well as high uninsured rates. These states’ decisions not to expand Medicaid have a disproportionate effect on African-Americans, who reside in high numbers in the southern states and are more likely to be low-income and uninsured than the general population.15 African-Americans account for approximately one in four health center patients in the non-expansion states.16

Data reported by the Centers for Medicare and Medicaid Services (CMS)17 indicate that Medicaid enrollment in the Medicaid expansion states grew by 27% between the summer of 2013 leading up to the first ACA open enrollment period, and December 2014. Even in the non-expansion states, Medicaid enrollment grew by 7%, meaning that health centers in these states, too, can be expected to receive additional Medicaid patient revenues that may help support expanded clinical care capacity, although on a far more modest scale.

A comparison between health centers in the 29 Medicaid expansion states and the 22 non-expansion states back in 2013 reveals important differences between health centers in the two groups of states prior to full implementation of the ACA (Table 3).

| Table 3: A comparison of health centers in Medicaid expansion and non-expansion states: patients, staffing, and revenues, 2013 | |||

| Health centers in expansion states (n=690) | Health centers in non-expansion states (n=483) | ||

| Total patients*** | 21,091 | 14,035 | |

| Location*** | |||

| Rural | 39% | 60% | |

| Urban | 61% | 40% | |

| Health insurance profile of patients | |||

| Uninsured*** | 33% | 44% | |

| Medicaid*** | 40% | 27% | |

| Medicare** | 9% | 10% | |

| Private insurance | 16% | 17% | |

| Revenues | |||

| Total revenue per patient*** | $795 | $723 | |

| Medicaid share of revenues*** | 36% | 23% | |

| Medicaid revenue per Medicaid patient*** | $716 | $585 | |

| Medicare share of revenues** | 6% | 7% | |

| Other public insurance share of revenues*** | 2% | 1% | |

| Private insurance share of revenues | 8% | 8% | |

| Self-pay share of revenues*** | 6% | 9% | |

| Section 330 grants as share of revenues*** | 23% | 35% | |

| Total grants as share of revenues*** | 43% | 52% | |

| Staffing (per 10,000 patients) | |||

| Physicians*** | 5.2 | 4.1 | |

| Mid-level professionals*** | 4.5 | 5.3 | |

| Dental FTEs | 6.2 | 6.1 | |

| Mental health FTEs | 3.5 | 3.1 | |

| Substance abuse treatment FTEs** | 1.2 | 0.5 | |

| Enabling services*** | 8.6 | 7.1 | |

| SOURCE: GWU analysis of 2013 UDS data on federally funded health centers. ***p<.01; ** p<.05Notes: Data do not include health centers in U.S. Territories. | |||

- Coverage. In 2013, before the ACA Medicaid expansion took effect, health center patients in the states now moving ahead with the expansion were already significantly more likely to be covered by Medicaid (40% vs. 27%), and significantly less likely to be uninsured (33% vs. 44%). Privately insured patients accounted for similar proportions of health center patients in both group of states. The differences in Medicaid and uninsured rates between health center patients in the two groups of states largely reflect much broader Medicaid eligibility for adults in the expansion states even before 2014 – as of January 2013, the median income eligibility threshold for working parents in the expansion states was 106%, compared to 48% FPL in the non-expansion states.18

- Revenues. Mirroring differences in the pre-ACA coverage status of their patients, health centers in expansion and non-expansion states also had distinctly different revenue profiles prior to the ACA. In 2013, average Medicaid revenue per Medicaid patient was significantly higher in health centers in the states that later expanded Medicaid, and Medicaid accounted for 36% of their operating revenues, compared to 23% in health centers in states that have not adopted the expansion. Heading into 2014, health centers in the non-expansion states were already significantly more dependent than those in Medicaid expansion states on federal section 330 grants (35% vs. 23% of operating revenues) and grant funding overall (52% vs. 43%), as well as on self-pay patient revenues (9% vs. 6% of total operating revenues).

- Staffing. In 2013, health centers in the Medicaid expansion states had significantly higher ratios of physicians to patients but significantly lower ratios of mid-level professionals (such as nurse practitioners and physician assistants) to patients, relative to health centers in the non-expansion states. In part, this difference may reflect the fact that health centers in the non-expansion states are more likely to be located in rural areas, where physician supply is more limited. Health centers in expansion states also had significantly more staff capacity to provide enabling services and substance abuse treatment. Notably, however, dental and mental health staff capacity did not differ between health centers in the two groups of states.

Financial Challenges Facing Health Centers

The ACA investments in health centers and the NHSC are supporting substantial expansion of preventive and primary care capacity in underserved communities as coverage and the demand for care increase, and helping to ensure and improve access for those who remain uninsured. However, both the Health Center Trust Fund and the increase in NHSC funding are set to expire in 2015. Thus, health centers face increased financial challenges going forward.

The uninsured rate among health center patients is expected to decline significantly due to expanded coverage under the ACA – from 36% in 2012, to an estimated 20% by 2020 if the Medicaid expansion is fully implemented and 29% if it is not.19 Even so, health centers, even in Medicaid expansion states, are likely to continue to treat high numbers and shares of low-income patients without insurance. The health center experience in Massachusetts following the state’s 2006 expansion of coverage to adults with income up to 300% FPL may presage the situation of health centers under the ACA.20 Although the share of Massachusetts health center patients without insurance declined sharply due to the coverage expansion, health centers continue to a serve a population with a disproportionately high uninsured rate – about 19% compared to 4% statewide.21 In states not expanding Medicaid, nonelderly adults with income between 100% and 138% FPL are generally eligible for subsidies to purchase Marketplace health plans. However, many health center patients with income at this level may be unable to afford remaining cost-sharing obligations under these plans, as discussed below.

In addition to the costs of providing caring for those who remain uninsured, health centers may also face uncompensated care costs for patients who are insured, due to under-insurance and QHP provider network limitations:

- Under-insurance. Under the ACA, people with income up to 250% FPL who purchase Silver plans can qualify for cost-sharing reductions. The reductions are substantial but do not eliminate cost-sharing, which can be considerable for individuals and families with low income. To illustrate, enrollees with income between 100% and 150% FPL have out-of-pocket obligations equivalent to 6% of covered costs in a Silver plan. Out-of-pocket exposure rises to 13% of covered costs for those with income between 150% and 200% FPL, and 27% of covered costs for families with income between 200% and 250% FPL.22 Cost-sharing reductions do not apply in the more affordable Bronze and catastrophic plans. When patients cannot afford their cost-sharing amounts, their providers must absorb the uncompensated costs.

Although the cost-sharing reduction assistance has the potential to greatly increase the affordability of health care, even nominal cost-sharing can burden low-income health center patients. In communities where a sizeable proportion of health center patients have subsidized QHP coverage rather than Medicaid, health centers could still face uncompensated costs, depending on how health plans structure cost-sharing reductions – for example, if a plan requires relatively high cost-sharing for chronic care management, or for prenatal care that extends beyond routine screenings and encompasses treatment for conditions that could complicate pregnancy.23 Health centers may also incur uncompensated costs for services that are not covered by their patients’ QHPs, such as vision and dental services for adults. Grant funding for health centers continues to play a critical role in subsidizing these costs for insured patients as well as the costs of care for uninsured patients.

- Medicaid and QHP provider network limitations. Federal standards do not require that either Medicaid plans or QHPs sold in the Marketplace include all health centers (or other “essential community providers,” the term used in the ACA to identify providers that specialize in the treatment of higher-risk and medically underserved populations) in their provider networks. Although health centers are expected to be available to all community residents, health plans in both markets maintain significant discretion in establishing their networks. To the extent that patients covered by Medicaid plans or health plans seek services at health centers that are out-of-network, health centers may be exposed financially as payment for the services may be denied or reduced. Research on the Massachusetts experience cited earlier highlighted the importance of network counseling as part of assistance with selecting a health plan, to protect established health center patients from inadvertently selecting a QHP that does not include their regular source of health care.24

Looking Ahead

The ACA makes significant investments in health coverage and care for communities that are disadvantaged from an economic and health perspective. The law’s principal investment, of course, was the creation of pathways to affordable health coverage for low- and middle-income people, through Medicaid and tax subsidies. However, the Supreme Court’s decision on the Medicaid expansion has resulted in a coverage gap in the non-expansion states for millions of the poorest people in the nation, who are among those most likely to rely on community health centers for primary care. Should the Supreme Court decide in King v. Burwell that subsidies for Marketplace coverage are available only through state-based Marketplaces, health centers in the Medicaid non-expansion states, all but one of which defaulted to the federal Marketplace, will be exposed not only to the impact of the coverage gap on their poorest patients, but also to the impact of reduced access to private coverage for their patients with income at or above the federal poverty level. The other major ACA investment from the standpoint of health centers, the $11 billion dedicated trust fund, sunsets at the end of 2015. Whether the fund will be continued has become an increasingly important question, as the number of patients health centers serve is projected to fall by one-third – 7 million people – if it is not extended.25

As ACA implementation continues, health centers serve as a bellwether of the impact of health reform on the nation’s most vulnerable communities. Several important questions offer a framework for ongoing analysis and evaluation:

- What is the relationship between state Medicaid expansion decisions and health centers’ staffing and capacity?

- How do health centers’ outreach and enrollment practices affect the rate at which their patients are able to gain and maintain coverage? What are health centers’ experiences in maintaining coverage for patients who move between Medicaid, CHIP, and Marketplace plans due to changes in eligibility?

- What patterns emerge in Medicaid expansion states where uninsured populations and services are concerned? How do health centers with relatively larger proportions of uninsured patients compare with other health centers that may rely less on federal grants, in terms of growth in patient volume, patient-staffing ratios, range of services, and quality? To what extent do health centers leverage the increase in Medicaid revenue to expand access to care for the remaining uninsured?

- Are health centers incurring uncompensated costs for patients enrolled in qualified health plans? To what extent are they able to negotiate inclusion in health plan networks?

- How are health centers participating in or leading efforts to improve quality? How are they participating in health system transformation efforts? Can health centers, like other providers, move toward a payment system that is less encounter-based and more tied to performance measures?

Measures of health centers’ scope and activity, and of rates of coverage and access among their patients, are important gauges of how the ACA’s goals are translating into improvements for the populations and communities most at risk of disparities in health and health care. Moving forward, analyses that investigate the implications of state Medicaid expansion decisions for health centers and their patients can illuminate the relationship among Medicaid expansion, health center capacity, and access to care in underserved communities.

Funding support for this paper was provided to The George Washington University by the RCHN Community Health Foundation.

Endnotes

- Uniform Data System (UDS) Report, 2003. Bureau of Primary Health Care, Health Resources and Services Administration, U.S. Department of Health and Human Services. ↩︎

- Health Insurance Coverage of the Total Population, 2013, State Health Facts, Kaiser Family Foundation, https://modern.kff.org/other/state-indicator/total-population/ ↩︎

- Bureau of Primary Health Care, Health Resources and Services Administration (2014), National 2013 Health Center Data. http://bphc.hrsa.gov/uds/datacenter.aspx?q=tall&year=2013&state= ↩︎

- Goldman F and Grossman M, The Impact of Public Health Policy: The Case of Community Health Centers, November 1982, National Bureau of Economic Research (NBER) Working Paper Series, http://www.nber.org/papers/w1020.pdf ↩︎

- Lebrun L et al., “Racial/Ethnic Differences in Clinical Quality Performance Among Health Centers,” Journal of Ambulatory Care Management, 2013, 36(1), http://bphc.hrsa.gov/publications/racialdifferences.pdf ↩︎

- Shi L et al., “America’s Health Centers: Reducing Racial and Ethnic Disparities in Perinatal Care and Birth Outcomes,” Health Services Research, 2004, 39(6, Part 1), http://eds.b.ebscohost.com.proxygw.wrlc.org/eds/pdfviewer/pdfviewer?vid=1&sid=9557d0d8-e63e-4cc5-8d44-b10e851312de%40sessionmgr111&hid=111 ↩︎

- O’Malley A et al., “Health Center Trends, 1994-2001: What Do They Portend For the Federal Growth Initiative,” Health Affairs, March-April 2005: 24(2), http://content.healthaffairs.org/content/24/2/465.full.pdf+html ↩︎

- Shi L et al., “Community Health Centers and Racial/Ethnic Disparities in Healthy Life,” International Journal of Health Services, 2001, 31(3), http://www.jhsph.edu/research/centers-and-institutes/johns-hopkins-primary-care-policy-center/Publications_PDFs/2001%20IJHS.pdf ↩︎

- Shi L et al., “Reducing Disparities in Access to Primary Care and Patient Satisfaction with Care: The Role of Health Centers,” 2013, Journal of Health Care for the Poor and Underserved, 21(1), http://www.ncfh.org/pdfs/2k12/9628.pdf ↩︎

- Bailey M and Goodman-Bacon A, The War on Poverty’s Experiment in Public Medicine: Community Health Centers and the Mortality of Older Americans (October 2014), NBER Working Paper Series, http://www.nber.org/papers/w20653.pdf ↩︎

- Sharma R et al., “Costs and Clinical Quality Among Medicare Beneficiaries: Associations with Health Center Penetration of Low-income Residents,” Medicare and Medicaid Research Review, 2014, 4(3), https://www.cms.gov/mmrr/Downloads/MMRR2014_004_03_a05.pdf ↩︎

- Roby D et al., Exploring Healthcare Quality and Effectiveness at Federally-Funded Community Health Centers: Results from the Patient Experience Evaluation Report System (1993-2001), National Association of Community Health Centers, March 2003, http://www.nachc.com/client/PEERSreportfinal0226.pdf ↩︎

- Dor A et al., Uninsured and Medicaid Patients’ Access to Preventive Care: Comparison of Health Centers and Other Primary Care Providers, 2008, Policy Brief #4, Geiger Gibson Program/RCHN Community Health Foundation Research Collaborative, George Washington University, https://publichealth.gwu.edu/departments/healthpolicy/DHP_Publications/pub_uploads/dhpPublication_A5EFC6C5-5056-9D20-3DBB2F5E5B966398.pdf ↩︎

- Garfield R et al., The Coverage Gap: Uninsured Poor Adults in States that Do Not Expand Medicaid: An Update, Kaiser Family Foundation, 2014, https://modern.kff.org/health-reform/issue-brief/the-coverage-gap-uninsured-poor-adults-in-states-that-do-not-expand-medicaid-an-update/ ↩︎

- Artiga S et al., The Impact of the Coverage Gap in the States not Expanding Medicaid by Race and Ethnicity, 2013, Kaiser Family Foundation, https://modern.kff.org/disparities-policy/issue-brief/the-impact-of-the-coverage-gap-in-states-not-expanding-medicaid-by-race-and-ethnicity/ ↩︎

- GWU analysis of 2013 HRSA UDS reports, http://bphc.hrsa.gov/healthcenterdatastatistics/statedata/index.html ↩︎

- Centers for Medicare and Medicaid Services, Medicaid and CHIP: December 2014 Monthly Applications, Eligibility Determinations and Enrollment Report, February 23, 2015, http://medicaid.gov/medicaid-chip-program-information/program-information/downloads/december-2014-enrollment-report.pdf ↩︎

- Heberlein M et al., Getting into Gear for 2014: Shifting New Medicaid Eligibility and Enrollment Policies into Drive, Appendix Table 2, 2013, Kaiser Commission on Medicaid and the Uninsured, Kaiser Family Foundation, https://modern.kff.org/report-section/getting-into-gear-for-2014-shifting-new-medicaid-eligibility-and-enrollment-policies-into-drive-section-2-medicaid-and-chip-eligibility-as-of-january-1-2014/ ↩︎

- Ku L et al., How Medicaid Expansions and Future Community Health Center Funding Will Shape Capacity to Meet the Nation’s Primary Care Needs: A 2014 Update, 2014, Policy Research Brief #37, Geiger Gibson/RCHN Community Health Foundation Research Collaborative, George Washington University, http://www.rchnfoundation.org/wp-content/uploads/2014/06/GG-caseload-impact-brief-6-19-14.pdf ↩︎

- Massachusetts Health Care Reform: Six Years Later, 2012, Kaiser Family Foundation, https://modern.kff.org/health-costs/issue-brief/massachusetts-health-care-reform-six-years-later/ ↩︎

- GWU analysis based on 2013 Health Center Data: Massachusetts Program Grantee Data, http://bphc.hrsa.gov/uds/datacenter.aspx?q=tall&year=2013&state=MA, and Current Population Survey, Annual Social and Economic Supplement, 2013, US Census Bureau (2014), http://www.census.gov/cps/data/cpstablecreator.html ↩︎

- Health Insurance Marketplace Calculator, Kaiser Family Foundation, https://modern.kff.org/interactive/subsidy-calculator/ ↩︎

- The list of preventive services for women that must be furnished free of charge, which can be found at https://www.healthcare.gov/preventive-care-benefits/women/, includes a variety of screening services including routine screenings and screening for conditions such as domestic violence. However, conditions requiring treatment during pregnancy because of the risk of complications (e.g., gestational diabetes, high blood pressure) would not be considered part of the preventive services benefit for women and could be subject to cost sharing. See HRSA preventives guidelines at http://www.hrsa.gov/womensguidelines/ ↩︎

- Paradise J et al., Providing Outreach and Enrollment Assistance: Lessons Learned from Community Health Centers in Massachusetts, 2013, Kaiser Commission on Medicaid and the Uninsured, Kaiser Family Foundation, https://modern.kff.org/report-section/providing-outreach-and-enrollment-assistance-chcs-in-ma-introduction/ ↩︎

- Ku et al., op. cit. ↩︎