Navigator Funding Restored in Federal Marketplace States for 2022

On August 27, 2021, the Centers for Medicare and Medicaid Services (CMS) announced $80 million in funding for 60 Navigator programs serving consumers in 30 Federally-Facilitated Marketplace (FFM) states for the 2022 plan year. Navigator programs help consumers understand their plan choices and complete their application for financial help for Marketplace coverage or for Medicaid or CHIP. The multi-year award provides $80 million annually for 3-years; awardees must comply with grant terms and conditions to receive funding each year. Shortly after the funding announcement, CMS also finalized certain changes to regulatory standards for navigators in the federal marketplace.

The 2021 funding is significantly higher than the $10 million in annual funding awarded in 2018-2020 during the Trump Administration and more than the $63 million awarded in the final year of the Obama Administration. Total funding announced this year is 27% higher than the total announced in 2016, though funding changes vary considerably by state (Table 1). Four FFM states (Georgia, Hawaii, Iowa and South Carolina) received less navigator funding than in 2016, while in five other states (Kansas, Montana, New Hampshire, South Dakota, and Tennessee) funding more than doubled. In Delaware, federal navigator funding is more than three times the 2016 total.

Increased funding will support growth in the number of navigator programs – which had fallen to 30 by the end of the Trump Administration. Compared to the first year the FFM was open, when more than 100 Navigator programs received grants, a smaller number of grantees will begin work this fall; however, nearly half of the FFM navigators (29) will operate statewide programs, and most of those (20) will coordinate and share funding with a network of local partners. By contrast, in 2016, coordination among marketplace assister programs was more limited, although those that did so regularly said coordination was important to their effectiveness.

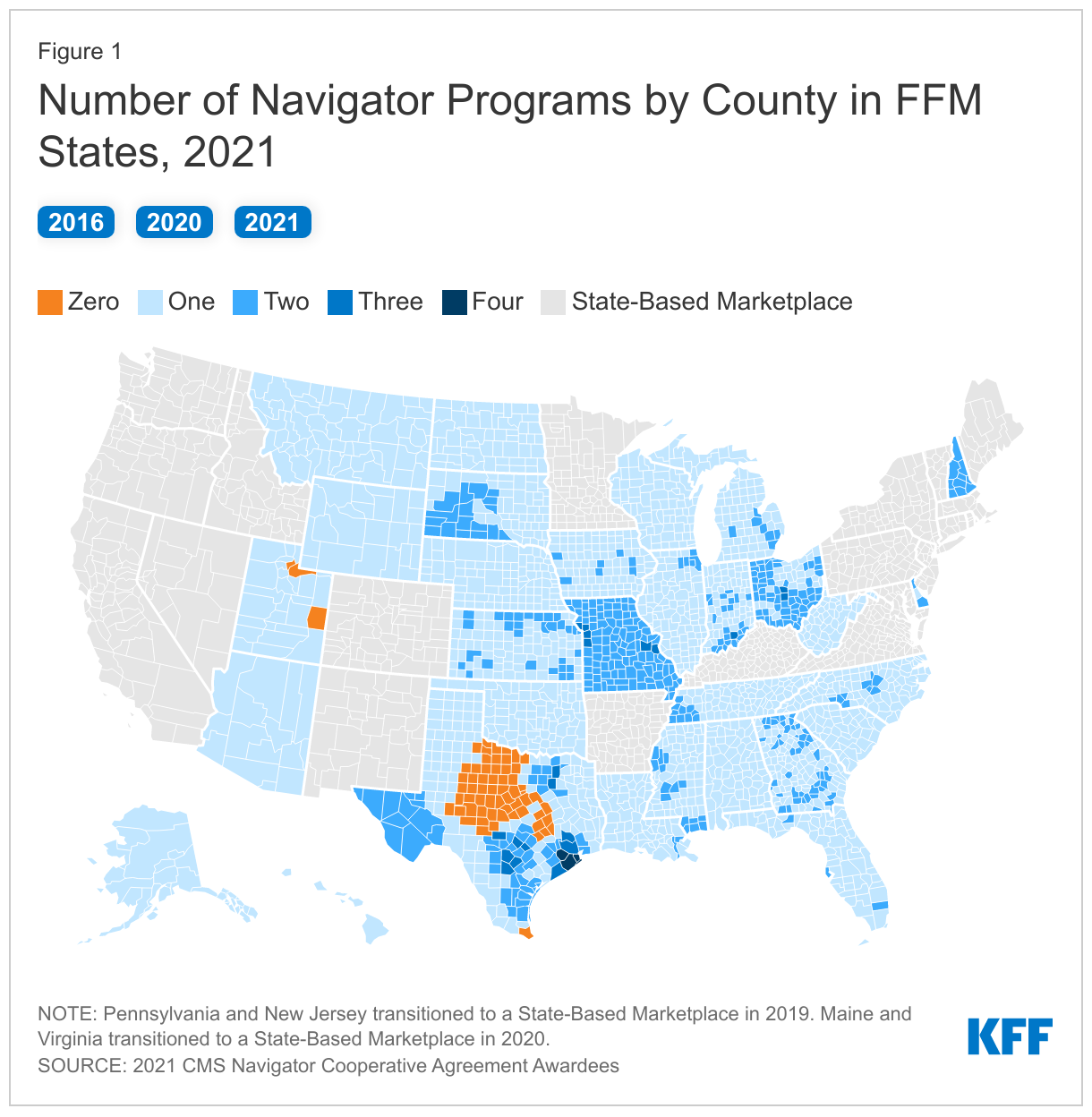

Federal regulatory standards for navigators previously required that there be a minimum of two navigators per state, at least one of which should be a community-based nonprofit. These requirements were eliminated during the Trump Administration and have not been restored. In all but two of the FFM states (Utah and Texas), every county will be included in the service area of at least one navigator program and nearly one in five (19%) counties in FFM states will be included in the service area of at least two programs (Figure 1). Although the funding awards posted by CMS do not indicate the type of grantee organization, it appears that nearly two-thirds (38 of 60) of navigator grantees are community-based nonprofits, another 15 are providers or provider groups--federally qualified health centers, primary care associations, or hospitals—and 4 are public universities, government agencies, or tribal organizations. Until 2017, federal navigators were required to maintain a physical presence in their state. This requirement also was eliminated during the Trump Administration and has not been restored, though CMS did encourage grant applicants to meet this standard. One of the non-physically-present grantees funded during the Trump years has been funded to provide statewide services in three states during the 2022 plan year and apparently will offer only call-center assistance in the state of Iowa.

Discussion

A 2020 KFF national survey on consumer assistance documented significant unmet need for enrollment help by consumers seeking coverage through the marketplace. Since then, the COVID-19 epidemic has increased reliance on marketplace coverage and Medicaid. Following enactment of subsidy increases and expanded enrollment periods during the pandemic, enrollment in marketplace plans increased by 2.8 million this year, including 2.1 million in HealthCare.gov states. Recently published regulations will extend the federal marketplace open enrollment period for the 2022 plan year from 6 weeks to 8 weeks (November 1 - January 15), and will allow people with income up to 150% of the federal poverty level (or $19,320 for an individual in 2021) to enroll throughout the year. Assuming the public health emergency ends in 2022, the moratorium on Medicaid disenrollment will be lifted and many more low-income people may need to transition to marketplace plans if their Medicaid eligibility is terminated. The restoration of federal navigator funding comes at a time when the need for consumer assistance may reach new, higher levels.

In addition to increasing funding for navigators, ensuring consumers are aware that navigator assistance is available and where to find it can help improve access to enrollment assistance. In recent years CMS has taken various steps to facilitate consumer access to agents and brokers – including a “Help On Demand” feature of HealthCare.gov that connects individual consumers directly with brokers. CMS has also promoted the use of web broker sites, called enhanced direct enrollment entities (EDE), that offer online dashboards and other technological tools to make broker-assisted enrollments faster and more efficient. Comparable initiatives have not been undertaken to promote and facilitate enrollment assistance by marketplace navigators. Because CMS accumulated more than $1 billion in unspent marketplace user fee revenue during the Trump Administration, additional resources are available to increase support for enrollment assistance if needed.