President Trump’s FY 2027 budget request, the second of his second term, was released on April 3, 2026, and proposes significantly reduced funding for some domestic HIV programs. A budget request lays out presidential administration priorities both in terms of policy issues and the level of funding requested (or proposed for elimination). Congress then considers the request but ultimately has “the power of the purse” and is responsible for appropriating funding for discretionary programs. Those appropriations can, and often do, differ from levels proposed by the administration. Indeed, while President Trump also called for reduced HIV funding in his budget request for FY 2026, Congress appropriated funding similar to prior year levels.

Beyond the traditional budget process, the Trump administration has taken several executive actions to terminate or limit already appropriated funding by delaying or cancelling funding, including for accounts and grants related to HIV. In some cases these actions have led to litigation, sometimes resulting in grants being reinstated. In addition, the administration has used the recission process, whereby the president asks Congress to rescind appropriated funds, which reduces funding if approved by Congress, though to date, recissions have not impacted domestic HIV accounts. These administrative actions have led to uncertainty regarding availability of federal dollars, including for HIV programs, grantees, and sub-grantees, even after funds are appropriated.

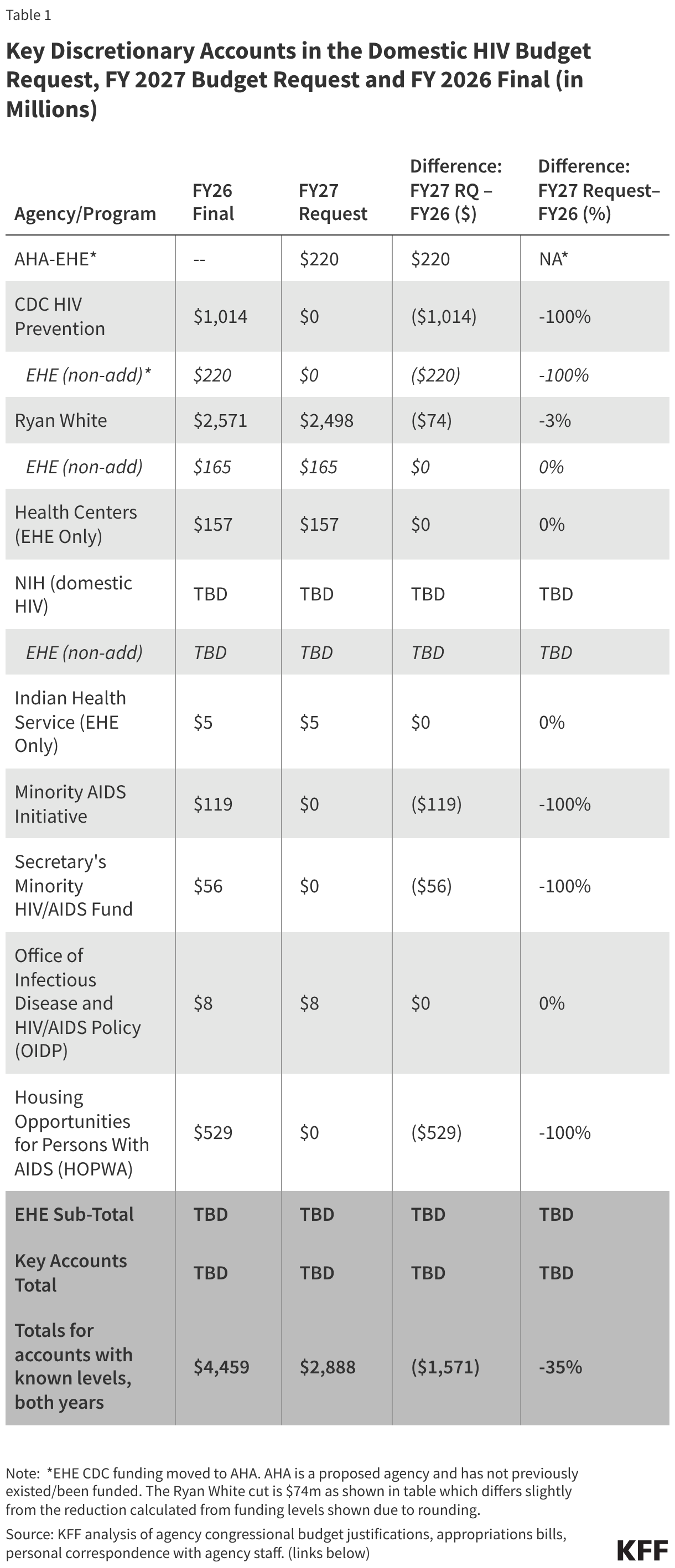

The FY 2027 request for domestic HIV, like the FY 2026 request, calls for the elimination or transformation of several core programs, while maintaining others. As with the FY 2026 request, proposals to bolster PrEP uptake that had become a feature of Biden Administration HIV requests, were not included. Funding for the Ending the HIV Epidemic Initiative, an effort born during the first Trump Administration, has been maintained. While detailed funding information is not available for all accounts, where levels are known, the FY 2027 budget request for domestic HIV programs represents a $1.6 billion (35%) decline compared to final FY 2026 funding levels.

If these cuts are enacted, it could make addressing HIV more challenging at a time when other changes to the health policy landscape could negatively impact access to HIV care and prevention services.

A summary of the request for domestic HIV programs is below.

Overview

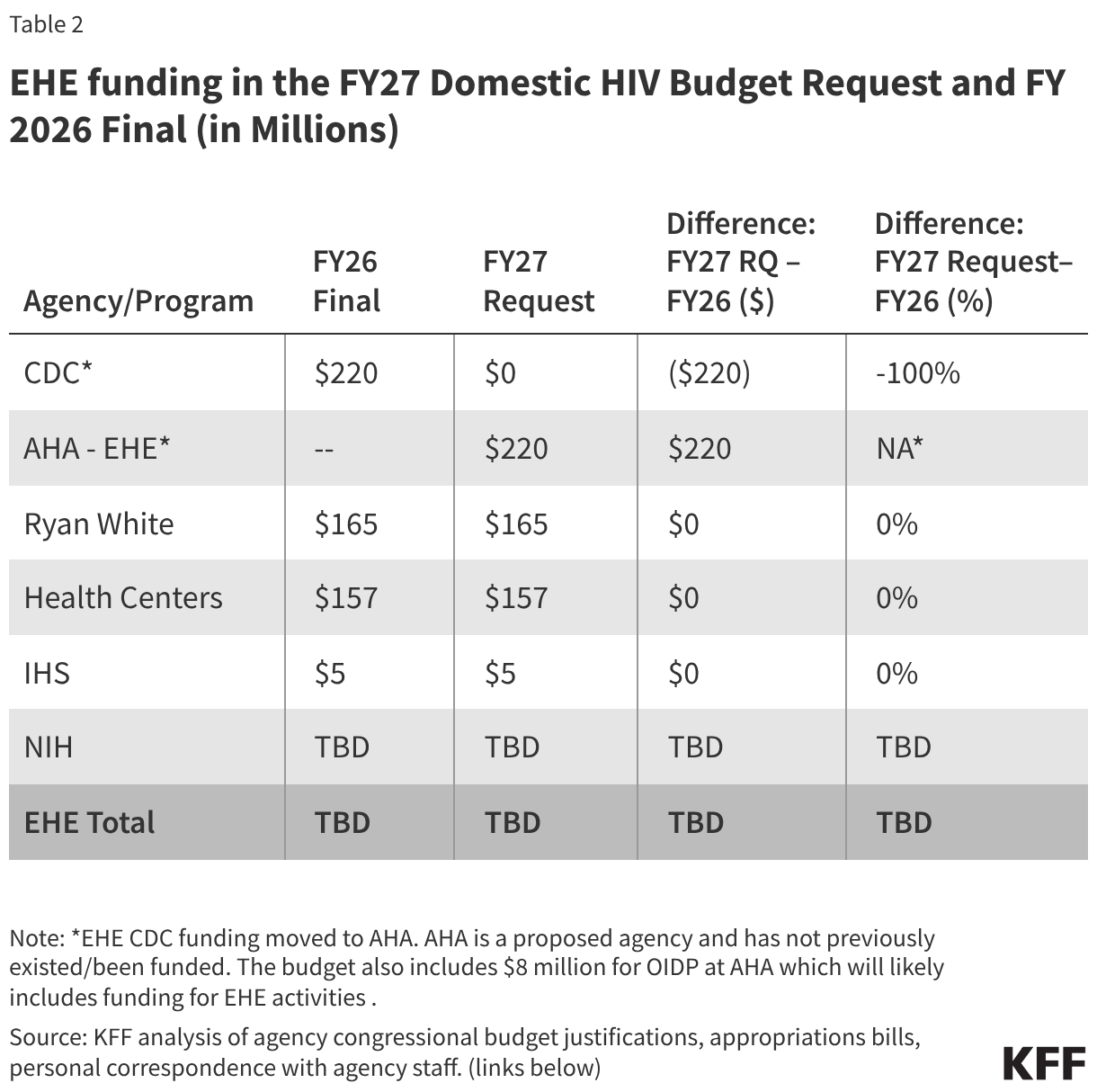

The request includes discretionary funding for key programs aimed at addressing the domestic HIV epidemic, including for the Ryan White HIV/AIDS and Health Center Programs, programs that the budget moves from the Health Resources and Services Administration (HRSA) to the proposed new agency, the Administration for Healthy America (AHA). Congress rejected the FY26 request’s proposal to create and fund AHA during the appropriations process. The FY27 request states that AHA will prioritize HIV/AIDS programs (among other areas), “aligning with the Administration’s priorities”. Other funding that has been provided to other departments/agencies for HIV activities is also moved to AHA. This includes funding for the Office of Infectious Disease and HIV/AIDS Policy (OIDP) for HIV and other infectious disease related activities, as well as all EHE funding previously allocated to Centers for Diseases Control and Prevention (CDC).

At the same time, the request eliminates a range of historical HIV programs including funding for domestic HIV prevention at the CDC, Part F of the Ryan White HIV/AIDS Program, and at least some parts of the Minority AIDS Initiative (MAI). Additionally, large cuts are proposed for the National Institute of Allergy and Infectious Diseases (NIAID) at the National Institutes of Health, which has been the largest source of HIV research funding in the world. The request also proposed cutting the Housing Opportunities for People with AIDS (HOPWA) program which is a program of Department of Housing and Urban Development.

Specific, known funding levels are as follows:

Centers for Disease Control and Prevention (CDC)- Domestic HIV Prevention

Funding for core HIV prevention programs at the CDC is eliminated in the budget request and only funding previously provided to the CDC for EHE activities ($220 million) is preserved but moved to AHA. Historically, CDC has accounted for almost all (91%) federal funding for domestic HIV prevention. This cut would represent a $794 million decrease (78%) over the FY26 level ($1 billion, including the EHE) for HIV funding, but a total elimination of funding for the division.

While CDC’s HIV prevention funds are eliminated in the proposal, some funding for infectious diseases has been retained and combined into one account. Previously, CDC funding for viral hepatitis, sexually transmitted infections, and tuberculosis prevention had separate funding lines. The request proposes to group those accounts into a single $300 million line. The $300 million funding level is $70 million below the sum of these individual accounts in FY 2026.

These changes at CDC were also proposed in the FY26 budget request but rejected by Congress.

Ryan White HIV/AIDS Program

The Ryan White HIV/AIDS Program, the nation’s safety-net for HIV care and treatment (now housed at HRSA, and would be moved to AHA), receives $2.5 billion in the FY 2026 request, a $74 million (3%) decrease over the FY 2026 enacted level. The request includes $165 million for EHE activities within Ryan White, the same as in FY 2026. The overall program decrease of $74 million is attributed to the elimination of funding for Part F of the program which has included the following components:

- AIDS Education and Training Centers (AETCs) whichprovide education and training for health care providers who treat people with HIV.

- Dental Programs: The “Dental Reimbursement Program” reimburses dental schools and providers for oral health services. The “Community-Based Dental Partnership Program” supports dental provider education and expands access to oral care for people with HIV.

- Minority AIDS Initiative (MAI): Created in 1998 to address the impact of HIV on racial and ethnic minorities, MAI provides funding to strengthen organizational capacity and expand HIV services in minority communities. (See additional discussion of MAI below.)

The FY 2027 budget request includes $157 million in HIV funding for the Health Center Program (now housed at HRSA and would be moved to AHA), all of which is for the EHE initiative; the same amount as the FY 2026 level. EHE funding in health centers “support efforts to reduce new HIV infections through outreach, routine and risk-based testing, and increased access to Pre-Exposure Prophylaxis for patient.”

Office of Infectious Disease and HIV/AIDS Policy (OIDP)

The FY27 budget provides $7.6 million in funding to the Office of Infectious Disease and HIV/AIDS Policy (OIDP) (now housed at the Office of the Assistant Secretary of Health, it would be moved to AHA). OIDP plays a coordinating role, including historically for EHE effort and national HIV, STI, and hepatitis strategies. Funding for OIDP is provided in the request to “drive progress [in] MAHA priorities by implementing innovative, evidence-based interventions to prevent, diagnose, and treat HIV/AIDS, STIs, viral hepatitis, nosocomial infections/hospital – acquired infections (HAIs), and antibiotic-resistant organisms.” It also supports OIDP to “coordinate national strategies, support data-driven program development, and engage communities most affected by these conditions.”

National Institutes of Health – Domestic HIV Research

Historically, the National Institutes of Health (NIH) has carried out almost all federally funded HIV research activities. The budget proposes significant cuts to NIH overall, including to the National Institute of Allergy and Infectious Disease (NIAID) which would be cut by $1.8 billion (27%), from approximately $6.5. billion to $4.8 billion. While the amount of funding for domestic HIV research at NIH is not yet known, in FY 2025, it was $3.3 billion (amount provided to KFF via data request). The Office of AIDS Research, which sits in the Office of the NIH Director and plays a coordinating role withing NIH is mentioned in the budget’s technical appendix, although a specific funding amount is not provided.

Indian Health Service (IHS)

In the FY27 budget, $5 million for IHS EHE activities to support ending HIV and hepatitis C in Indian Country is continued, the same as the FY26 final level. (Funding information provided to KFF via data request.)

The Minority AIDS Initiative (MAI)

As noted above, the MAI was created in 1998 to address the disparate impact of HIV on racial and ethnic minority communities and to build resources and organizational capacity within these communities. The status of the Minority AIDS Initiative is unclear. Funding that has been provided for MAI activities at the Substance Abuse and Mental Health Services Administration (SAMHSA) which the budget would move to AHA, aimed at “improving the health of people of color who have or are at risk for HIV” is eliminated in the proposal. In FY 2026 SAMHSA received $119 million for the MAI. Another $56 in MAI funding is eliminated from the Secretary’s Minority HIV/AIDS. In addition, as noted, Ryan White funding for Part F, which includes a funding line for MAI, is also eliminated in the proposal.

Housing Opportunities for Persons with AIDS (HOPWA)

The Department of Housing and Urban Development’s HOPWA Program is eliminated in the budget. In FY 2026, HOPWA was funded at $529 million. HOPWA, which was established in 1992, has provided housing assistance and supportive services to low-income people with HIV facing housing insecurity and is the only federal program centered on the housing needs of people with HIV. Its funding supports grants to localities, states, and community-based organizations.

The tables below compare federal funding levels for domestic HIV, where specified, in the FY 2027 request to the FY 2026 enacted levels. EHE funding is included in the overall table (Table 1) and in a dedicated table (Table 2).

Sources:

- HHS FY27 Budget in Brief: https://www.hhs.gov/sites/default/files/fy-2027-budget-in-brief.pdf

- HHS FY27 Budget Technical Appendix: https://www.whitehouse.gov/wp-content/uploads/2026/04/hhs_fy2027.pdf

- Indian Health Services Congressional Budget Justification: https://www.ihs.gov/sites/ofa/themes/responsive2017/display_objects/documents/IHS%20Draft%20CJ%20FY%202027.pdf

- Centers for Disease Control and Prevention Congression Budget Justification: https://www.cdc.gov/budget/documents/fy2027/fy-2027-cdc-cj.pdf

- Department of Housing and Urban Development Congressional Budget Justification: https://www.hud.gov/sites/dfiles/CFO/documents/2027-Congressional-Justifications.pdf

- Administration for a Healthy America Budget Justification (includes accounts formerly at HRSA, SAMHSA, and OASH, among others): https://www.hhs.gov/sites/default/files/fy-2027-aha-cj.pdf

- Departments of Labor, Health and Human Services, and Education, and Related Agencies Appropriations Act, 2026: https://www.congress.gov/bill/119th-congress/senate-bill/2587

- Transportation, Housing and Urban Development, and Related Agencies Appropriations Act, 2026: https://www.congress.gov/bill/119th-congress/house-bill/4552

Gary Claxton

Gary Claxton  Matthew Rae

Matthew Rae  Aubrey Winger

Aubrey Winger