Beyond Rebates: How Much Are Consumers Saving from the ACA’s Medical Loss Ratio Provision?

Most of the conversation around the Affordable Care Act’s Medical Loss Ratio (MLR) provision has centered on the requirement that insurers issue consumer rebates when they fall short of spending a certain portion of premium dollars on health care and quality improvement expenses. This makes sense as rebates are one of the more tangible ways consumers have benefited from the law so far, and it likely contributes to the MLR provision being among the more popular aspects of the health reform law.

However, as we’ve written before, rebates represent only a portion, albeit the most concrete portion, of the MLR rule’s savings to consumers. The primary role of an MLR threshold is to encourage insurers to spend a certain percentage of premium dollars on health care and quality improvement expenses (80 percent in the individual and small group market and 85 percent in the large group market). The MLR rebate requirement operates as a backstop if insurers do not set premiums at a level where they would be paying out the minimally acceptable share of premiums back as benefits. Only if those thresholds are not met are insurers required to provide rebates to consumers or businesses. (You can read more about the MLR rule here).

Consumers and businesses, therefore, can realize savings in two ways as a result of the MLR requirement: by paying lower premiums than they would have been charged otherwise (as a result of lower administrative costs and profits), or by receiving rebates after the fact. So while insurers paid out considerable amounts for rebates – last year’s rebates totaled $1.1 billion – this is not the whole story for consumers.

Of course, it is hard to know with certainty what premiums would have been if the MLR rules were not in place: we cannot know for sure how insurers would have priced their products or what rates regulators would have allowed (to the extent that they reviewed rates prior to the ACA). It is also difficult to separate out the direct effects of the MLR provision from other aspects of the health reform law, particularly rate review, which works to moderate unreasonable premium increases and thus increase loss ratios. There are also data limitations. For example, prior to new reporting requirements put in place to enforce the MLR provision, there were not good data sources that break out premiums and claims on a consistent basis for major medical coverage by all types of carriers. In the initial years this data became available (2010 and 2011), there were some issues with the quality of the data, particularly regarding expenses for quality improvement and other new categories of administrative expenses that are reported on the exhibit.

Within these limitations, we constructed an analysis that looks at the basic proportion of premiums that health plans paid out as claims for medical care over the three years since the ACA was passed, both before and after the MLR requirement went into effect for coverage in 2011. These proportions do not include adjustments for quality improvement expenses, taxes or other factors that are used when determining whether or not rebates need to be paid; they simply represent the total payments for medical care as a proportion of premiums. This is the traditional way medical loss ratios have been calculated. Generally, if the proportion is rising, that means insurers are paying out more of each dollar they receive on enrollee health care, which in most cases would mean that enrollees are getting better value for the premiums they pay. We then quantify what the change in the traditional MLR means to enrollees by estimating how much they would have paid in premium if the observed MLR for 2010 (before the MLR requirement went into effect) were held constant for 2011 and 2012.1 This approach addresses the following question: If insurers had targeted the same claims to premium ratio for 2011 and 2012 as they achieved in 2010, would premiums have been higher or lower, and by how much? In other words, it addresses how much consumers may have saved in lower premiums as a result of the MLR threshold in addition to receiving rebates.

Our analysis uses insurer data filed to state regulators and compiled by Mark Farrah Associates. These data (filed on the Supplemental Health Care Exhibit) suggest that the main beneficiaries of the MLR rule’s upfront premium savings are people who purchase insurance on their own. The majority of plans sold to small and large businesses were already in compliance with their respective MLR thresholds before the law went into effect, and our analysis shows that traditional MLRs (claims divided by premiums) for group plans have stayed relatively flat over the past three years. In the individual market, by contrast, fewer than half of plans were in compliance with the ACA’s MLR thresholds in 2010, and the average traditional MLRs in this market have been steadily increasing since the requirement went into effect. This means that individual market insurers are devoting a greater portion of premium dollars to health care claims and less to administrative costs and profits compared to before the ACA’s MLR rule went into effect.

This pattern is consistent with the idea that some insurers needed to improve their MLRs to comply with the new rebate requirements. We know that the individual market MLR requirements in the ACA are higher than those that were in effect in many states, and there have been numerous reports that insurers worked to reduce their commissions and other administrative expenses to become more efficient.

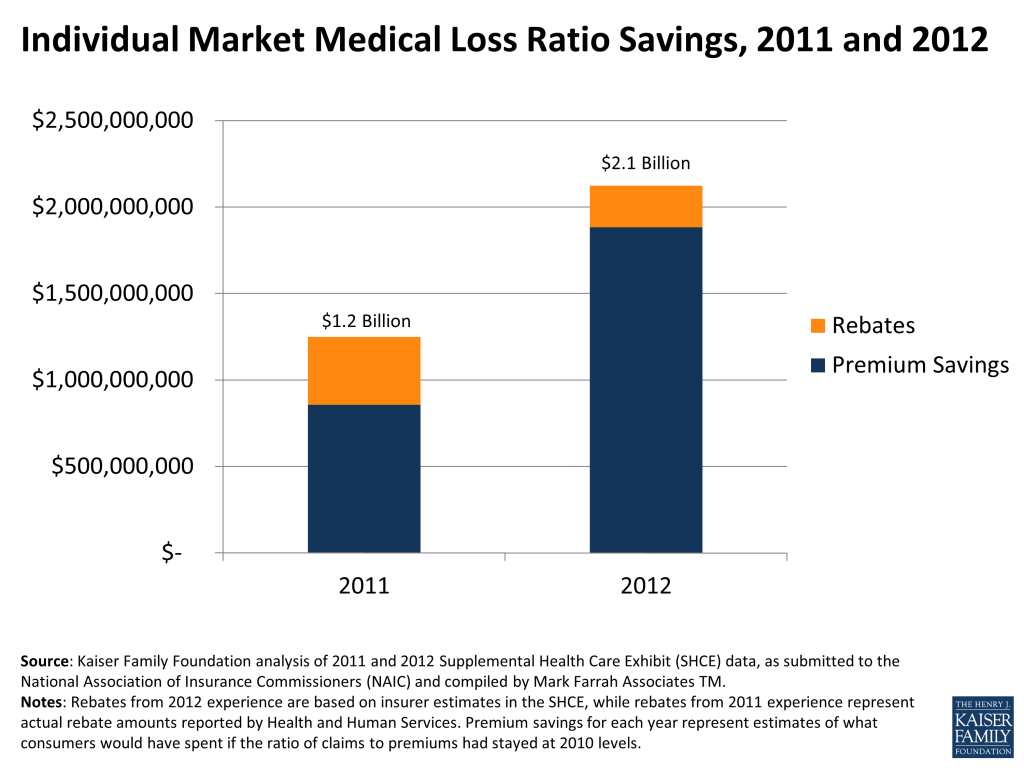

So how might these changes have affected premiums? As noted above, one way to address this question is to compute what these consumers would have paid in premiums in 2011 and 2012 had traditional individual market MLRs stayed at 2010 levels (the year before the provision went into effect). Looked at this way, premiums would have been $856 million higher in 2011, and premiums would have been $1.9 billion higher in 2012.

Adding to the premium savings the amount individual market consumers received in rebates yields a total savings of $1.2 billion for 2011. This year, individual market insurers are expecting to issue $241 million in rebates (based on our analysis of early estimates from insurers filed with state insurance departments), bringing the total estimated savings for 2012 to $2.1 billion. While this savings was not distributed evenly (with more going to people enrolled in plans that had low MLRs prior to the law), when averaged across all individual market enrollees, this amounts to a savings of $204 per person ($181 in premium savings and $23 in rebates) in 2012. Taking into account both premium savings and estimated rebates, people purchasing insurance on their own in 2012 spent 7.5% less on average on insurance than they might otherwise have in the absence of the law.

There are some potential limitations to this approach. While the pattern of increasing MLRs over the three years makes sense given the incentives under the ACA and reports of insurer behavior, we do not have comparable data from earlier years to tell us whether or not the 2010 MLR was typical for the pre-ACA period (though the available evidence suggests that it was).2 Also, MLRs in 2011 and 2012 might be overstated because insurers simply underestimated how much health care expenses would rise following the recession, though increasing MLRs still means that consumers have been getting better value for their premium dollars. Finally, rebate amounts for 2012 are based on preliminary estimates filed on the Supplemental Health Care Exhibit to state insurance departments, and actual rebate amounts will be based on insurer filings with the Department of Health and Human Services, which were due June 1.

If insurers’ preliminary estimates hold true, this year’s rebates (at a total of $571 million across all markets) are expected to be about half the amount of last year’s $1.1 billion in insurer rebates. Smaller rebates, however, are not an indication that consumers are now saving less money as a result of the MLR provision, but rather that insurers are coming closer to meeting the ACA’s MLR requirements and that this provision is having its intended effect of consumers getting more value for the money they spend on premiums. In fact, in the individual market, the $241 million consumers are expected to receive in rebates for 2012 represents roughly one tenth of our estimate of the overall savings from the provision in that year. Perhaps ironically, when the MLR provision is working as intended and insurers set premiums to meet the thresholds, consumers save money but are less likely to get a check in the mail as tangible demonstration of those savings.

Updated June 6, 2013 11:30 AM PT

- See methodology attached ↩︎

- Based on our analysis of the Accident and Health Experience Exhibit submitted to state regulators, which has been required of all insurance entities since 2006 but is not directly comparable to newer and more precise data, the weighted average traditional loss ratio in 2010 was slightly higher (80%) than the average of previous years (79%). Our premium savings estimates for 2012 and 2011 are thus likely conservative compared with estimates that used MLRs in prior years. ↩︎