New Reports Analyze Cost Sharing in 2015 ACA Marketplace Plans in 37 States

Charts Examine Savings from Subsidies at Stake in U.S. Supreme Court Case

Cost-sharing subsidies under the Affordable Care Act can substantially reduce deductibles and other cost sharing for people with low incomes purchasing coverage in the federally-facilitated insurance marketplace serving 37 states, a new analysis by the Kaiser Family Foundation finds. These government subsidies, which are also available in plans sold on state-run marketplaces, are different from premium tax credits. Both are at stake in the King v. Burwell case, the lawsuit which the U.S. Supreme Court will hear in March in which the federal government’s authority to provide financial assistance to people who buy insurance in federally-operated ACA marketplaces is being challenged.

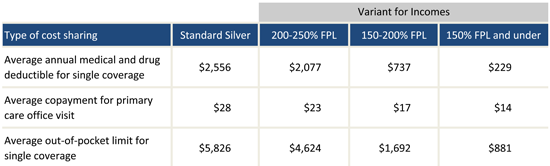

The health law requires insurers to offer enrollees with lower incomes variants of their standard silver plans with lower levels of cost sharing. People with incomes less than or equal to 150 percent of the federal poverty level can enroll in a plan with a 94 percent actuarial value; people with incomes between 150 and 200 percent of the FPL can get a plan with an 87 percent actuarial value, and people with incomes between 200 and 250 percent of the FPL can get a plan with a 73 percent actuarial value. A higher actuarial value means less cost sharing. Standard silver plans have an actuarial value of 70 percent.

In a new brief and collection of 36 charts, the Foundation compares cost sharing across standard silver plans and their variants in federally-facilitated ACA marketplaces, examining average deductibles and out-of-pocket limits, as well as copayments and coinsurance for hospital stays, physician visits, emergency room visits, and prescription drugs.

The comparisons show how average cost sharing declines for lower-income enrollees. Among the findings:

In an accompanying analysis with 65 charts, the Foundation examines cost sharing for plans across metal levels (platinum, gold, silver and bronze) for ACA marketplaces in 37 states. The analysis finds considerable variation in plan design, noting that plans offered in the same state and within the same metal level may have very different cost-sharing structures and still reach the same actuarial value.

The Cost of Care with Marketplace Coverage and Cost-Sharing Subsidies in Federal Marketplace Plans can be found at kff.org.