The Affordability of Long-Term Care and Support Services: Findings from a KFF Survey

Findings

Millions of older adults in the U.S., as well as some younger people with disabilities, require assistance with activities of daily living that may be provided in residential facilities like nursing homes or assisted living facilities, or in their homes or other settings by paid or unpaid caregivers. It is estimated that 5.8 million people used paid long-term services and supports (LTSS) in 2020, while another 1.9 million used LTSS in institutional settings, according to CBO estimates1 . Despite the prevalence of the need for such services as people age, a KFF survey, conducted in 2022 as part of a broader reporting project by KFF Health News and The New York Times, finds that most adults do not feel prepared to handle the costs of such care, and most older adults have not taken financial or practical steps to plan for care needs that might arise in the future.2 For more about LTSS financing, policy, and the populations who use these services, see KFF’s reports on Long-Term Services and Supports (LTSS) and Medicaid’s role in financing these services.

Key Findings

- Fewer than half of adults say they have ever had a serious conversation with a loved one about who will take care of them if they need help with daily activities in the future (43%) or how the cost of such care would be paid for (39%). Four in ten adults (43%) say they are not confident that they will have the financial resources to pay for the care they might need as they age.

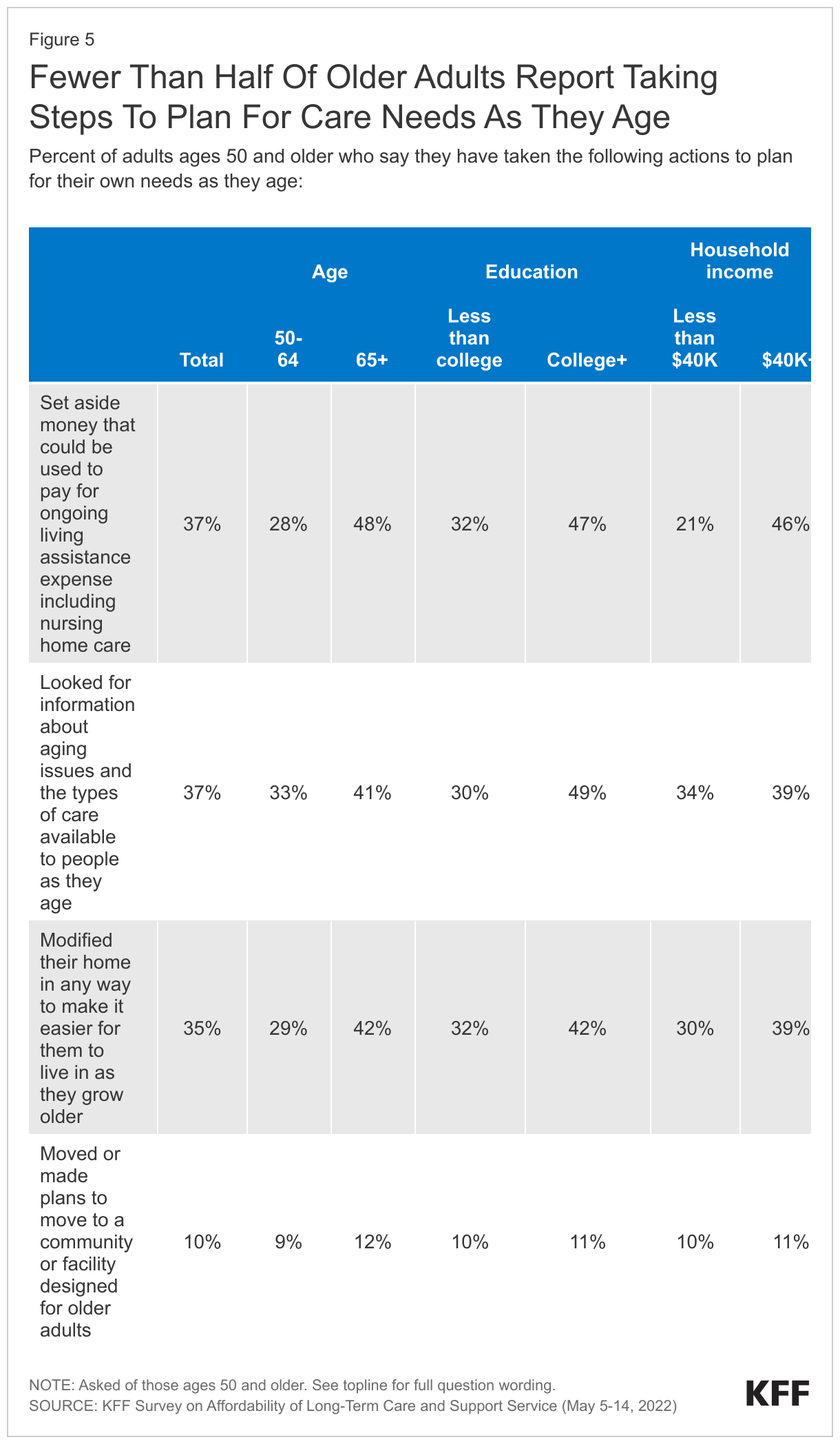

- Among those ages 50-64, many of whom are on the cusp of retirement, just under three in ten (28%) say they have set aside money that could be used to pay for future living assistance expenses. This share is higher among adults ages 65 and older (48%), but still half of adults in this age group say they have not put any money aside for this purpose.

- The overwhelming majority of adults say that it would be impossible or very difficult to pay the estimated $100,000 needed for one year at a nursing home (90%) or the estimated $60,000 for one year of assistance from a paid nurse or aide (83%).

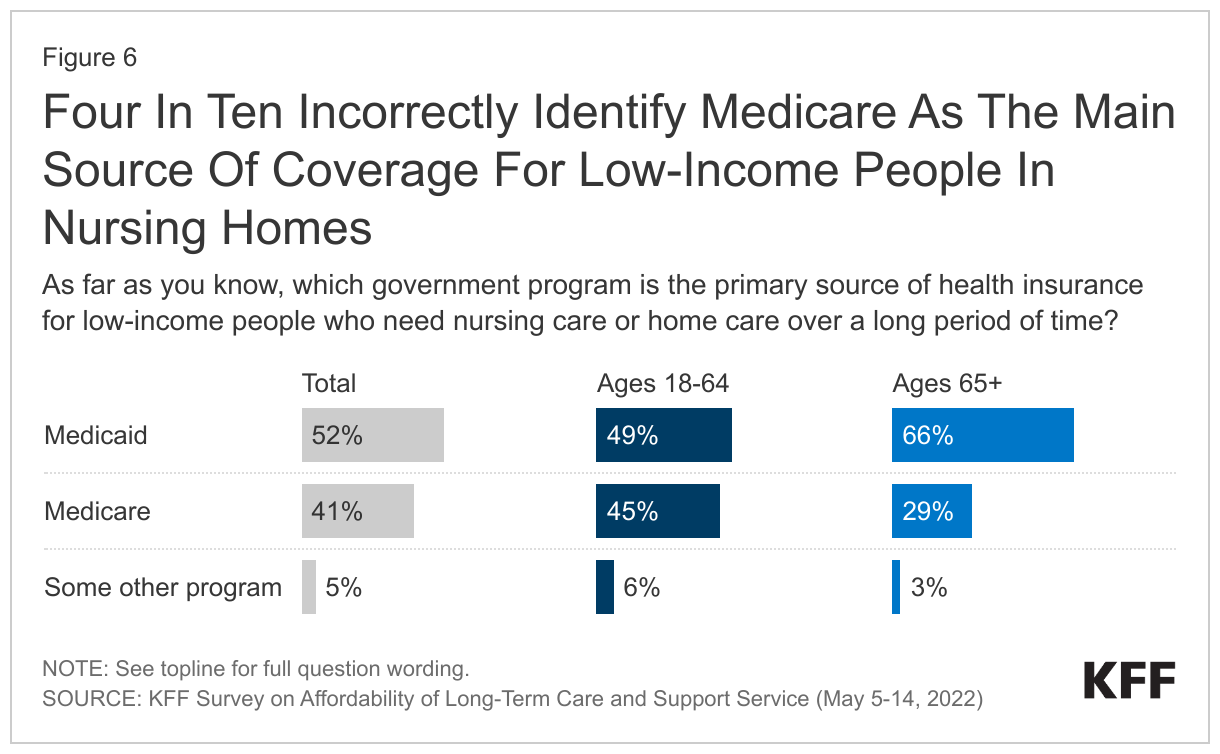

- There is also a fair amount of confusion about how long-term care is financed in the United States. Although Medicaid is the main source of coverage for these services and Medicare coverage of them is limited, 23% of adults – rising to 45% of those ages 65 and older – assume that Medicare would pay the bill for their own or a loved one’s time in a nursing home if they had a long-term illness or disability. Four in ten adults overall incorrectly believe that Medicare (rather than Medicaid) is the primary source of insurance coverage for low-income people who need nursing care or home care over a long period of time.

- Many find that long-term care and support services are difficult to find and afford. Among those who say they or a loved one has resided in a nursing home or other long-term care facility in the past two years, about six in ten (62%) say it was difficult to find a facility to meet their needs and a similar share say it was difficult to afford the cost of the facility. About half say the same about finding and affording support from paid nurses or aides.

- Although most people who say they or a loved one have used long-term care or support services report being at least somewhat satisfied with the quality of care received, the share reporting dissatisfaction with the quality of residential care is notably higher among those with lower household incomes (42% of those with incomes less than $40,000 vs. 28% of those with higher incomes).

- Providing or paying for long-term care and support services can also lead to financial consequences for families. For example, among those who contributed financially to their own or another’s long-term care or acted as a caregiver for a loved one, 56% say they cut back on spending on food, clothing or other basic household items as a result (rising to 67% among those in lower-income households) and one-third (rising to 49% of those with lower incomes) say they had trouble paying rent or other utilities.

Introduction

Millions of adults in the United States receive some form of long-term care services and supports, which encompasses a broad range of personal care assistance that people may need when they have difficulty with daily tasks due to aging, illness, or disability. Such supports include help with activities of daily living like eating, bathing, and dressing as well as other activities like preparing meals and managing medications. Such services and supports may be provided in facilities like nursing homes and assisted living facilities, or at people’s homes or other community-based settings. These services and supports are also often provided by family and friends on an unpaid basis.

In the U.S., Medicaid is the primary source of coverage for long-term care services and supports, financing over half of these services in 2020.3 Although Medicare is the primary source of health insurance coverage for Americans ages 65 and older and for some younger adults with disabilities, Medicare coverage of long-term care and support services is limited. Private long-term care insurance is expensive, and relatively few older adults are covered by such policies. This leaves many adults struggling to afford the cost of residential or home-based long-term care and supports or unprepared to handle these costs if they arise in the future.

As part of a broader investigative project by KFF Health News and The New York Times, KFF conducted this survey in 2022 to help shed light on the U.S. public’s awareness, attitudes, and experiences when it comes to long-term care services and supports.

Attitudes And Knowledge About Long-Term Care

Preparation For Future Long-Term Care Needs

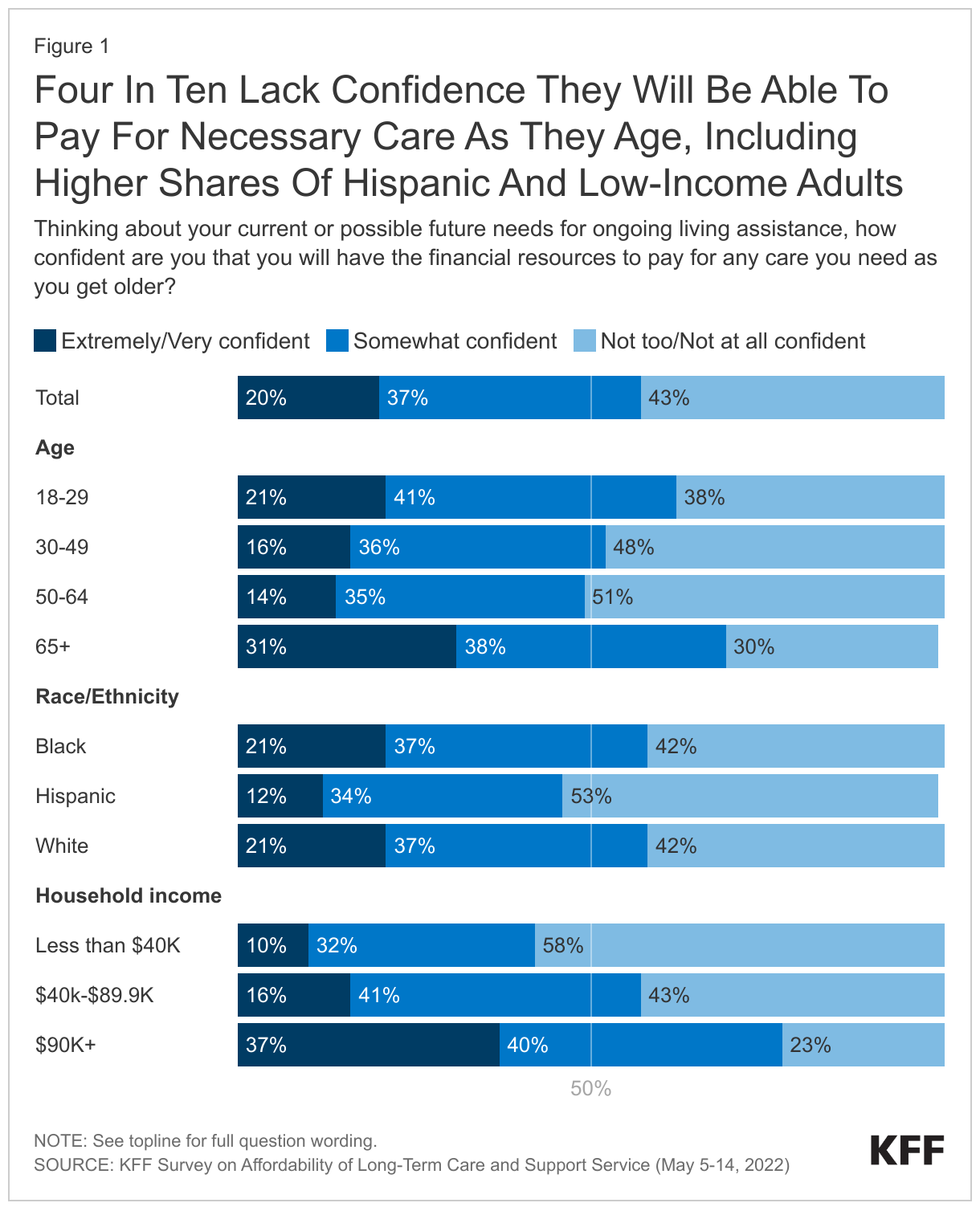

Although many adults in the United States know someone in their lives who receives long-term care assistance of some kind, many do not feel prepared for the cost of providing for that care for themselves if they may need it in the future. When asked about the prospect of needing living assistance as they age, four in ten adults (43%) say they are “not too” or “not at all confident” that they would have the financial resources to pay for such care, while 37% say they feel “somewhat confident” and a much smaller share – one in five – say they are “extremely” or “very confident”. The share that does not feel confident is larger among certain groups, including those with household incomes less than $40,000 (58% “not too” or “not at all confident”), Hispanic adults (53%), and those between the ages of 30-49 (48%) or 50-64 (51%). By contrast, among adults ages 65 and older (77% of whom report that they are retired), a smaller share (30%) say they are not confident about affording such care, while 31% say they are “extremely” or “very confident.”

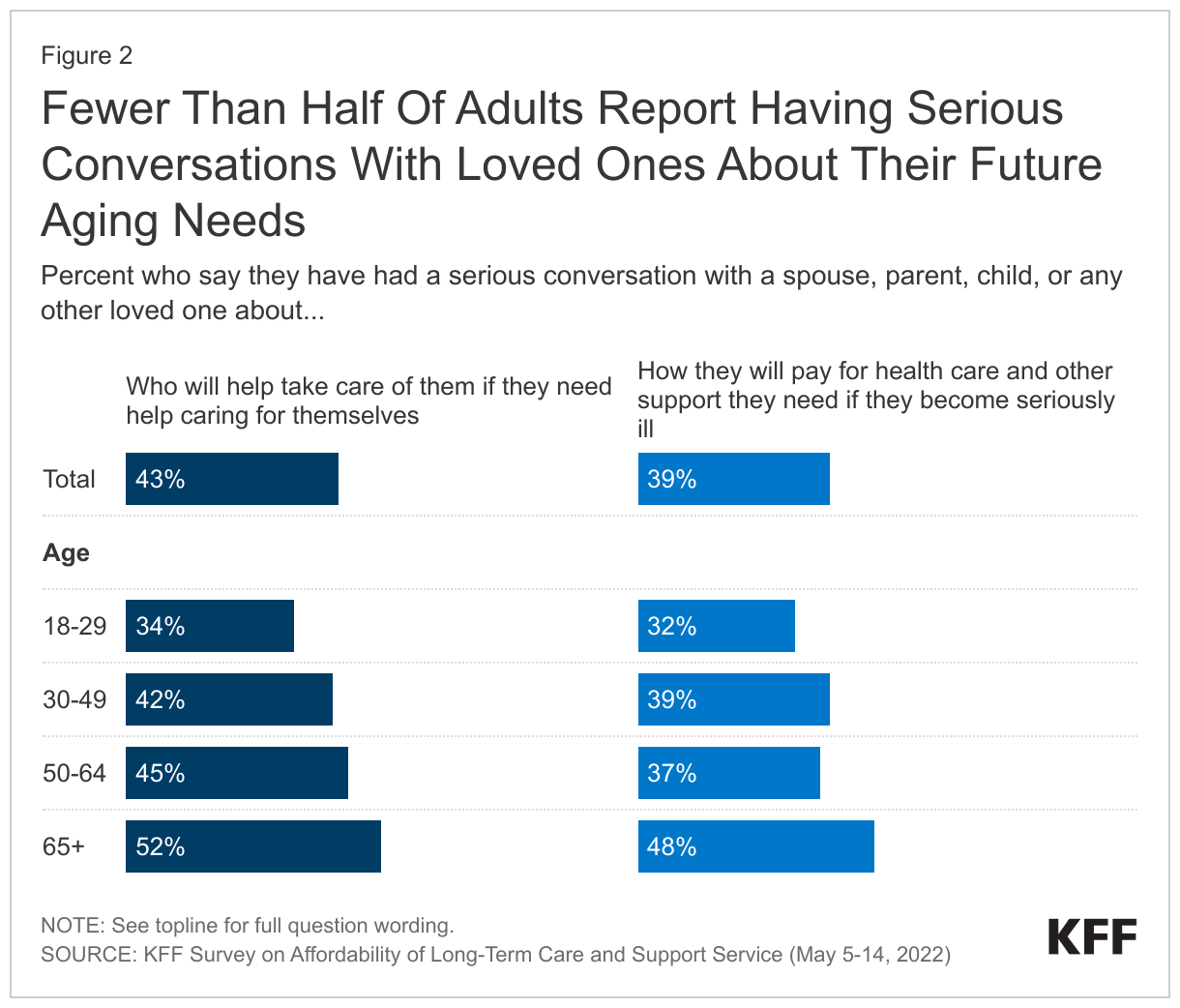

Fewer than half of adults in the United States say they have ever had a serious conversation with a loved one about who will take care of them if they need help doing so (43%) or how their health care and other support will be paid for if they fall seriously ill (39%). Adults who are 65 and older are most likely to have had these conversations, with approximately half saying they have had a serious discussion with a loved one about caretaking (52%) and paying for their care if they become very ill (48%). Still, that leaves about half of adults in this age range who say they have not had these conversations.

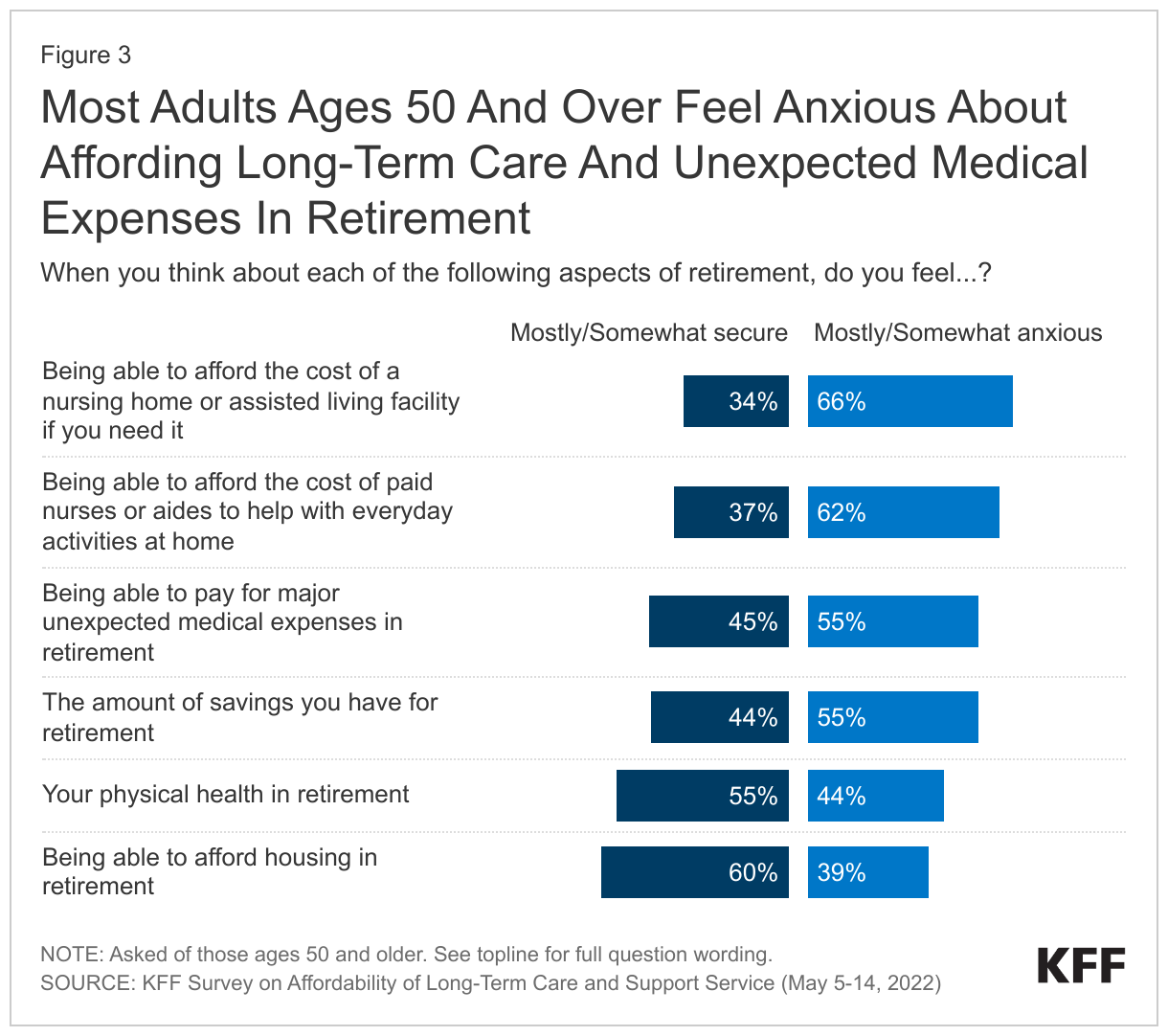

Among various issues that might be concerns for older adults in retirement, being able to afford long-term care is particularly likely to elicit feelings of anxiety, rather than security. At least six in ten adults ages 50 and older say they feel “mostly” or “somewhat anxious” about affording the cost of a nursing home or assisted living facility (66%) or paid nurses or aides to help with everyday activities (62%) if they need them. Over half also say they feel anxious about the amount of savings they have for retirement (55%) and being able to pay for major unexpected medical expenses in retirement (55%). On the other hand, most adults ages 50 and older say they feel “mostly” or “somewhat secure” about their physical health (55%) and being able to afford housing in retirement (60%), though about four in ten say they feel anxious about these aspects as well.

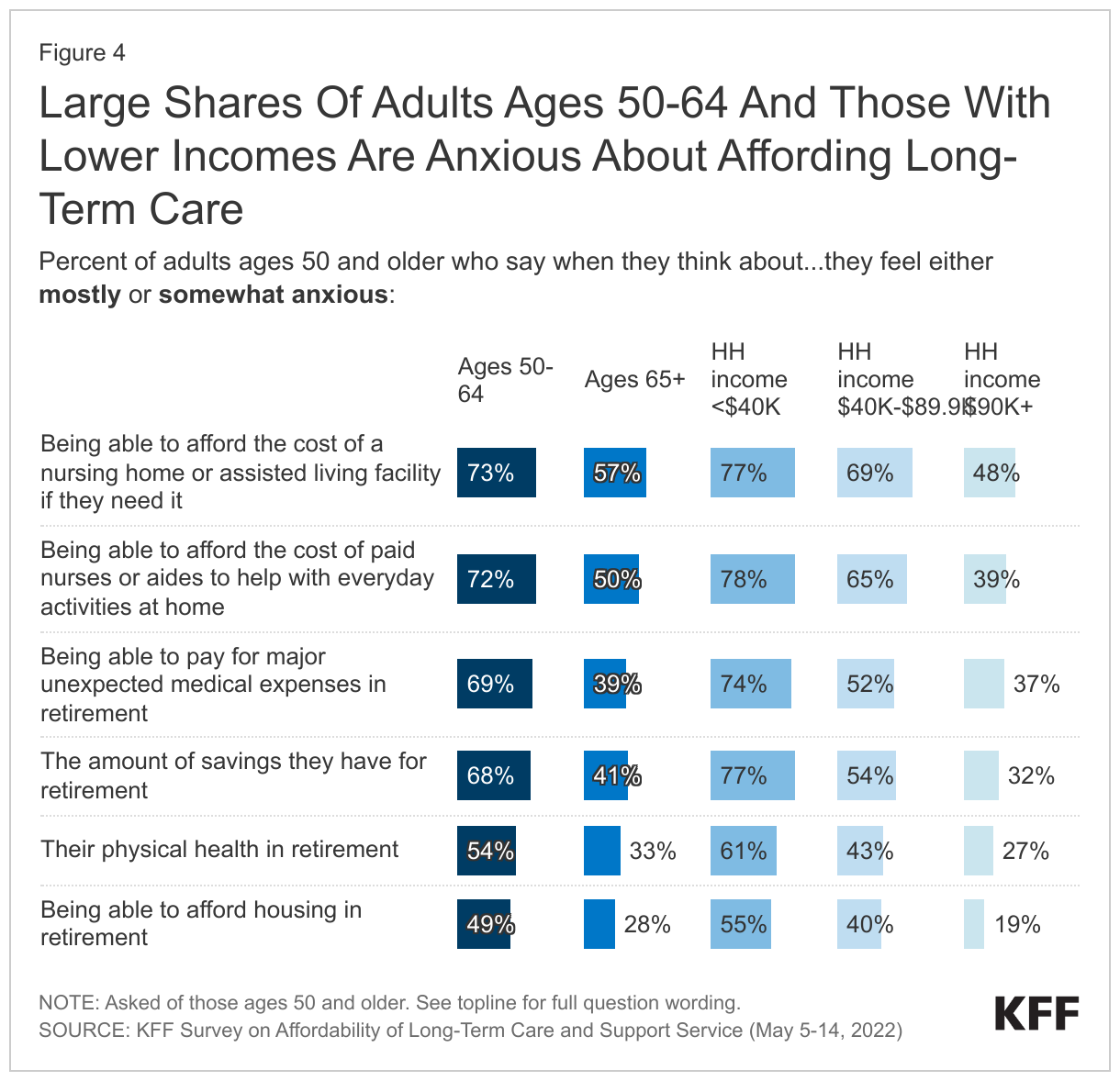

Among those who are 65 and older, three-fourths (77%) of whom say they are already retired, majorities say they feel at least “somewhat secure” about most aspects of retirement asked about in the survey, though almost six in ten (57%) say they feel at least “somewhat anxious” about affording the cost of a nursing home or assisted living facility and half say they feel anxious about being able to afford paid nurses or aides if they need them. Among those between the ages of 50 and 64, more than seven in ten feel anxious about affording residential care (73%) and care from paid nurses or aides (72%) in retirement, and nearly as many are anxious about affording unexpected medical expenses (69%).and their retirement savings (68%).

Not surprisingly, anxiety about retirement is also related to income. Among older adults with incomes under $40,000, roughly three-quarters say they feel anxious about affording support from paid nurses or aides (78%), residential long-term care (77%), and unexpected medical expenses in retirement (74%), while over half (55%) say they feel anxious about affording housing in retirement. Among older adults with annual incomes of $90,000 or more, most say they feel secure about various aspects of retirement, though about half (48%) say they are anxious about being able to afford the cost of a nursing home or assisted living facility if they need it.

While some older adults report taking concrete actions to plan for how their needs may change as they age, most have not. Among those ages 65 and older, about half say they have set aside money specifically for potential living assistance expenses (48%), four in ten have looked for information about the types of care available to people as they age (41%) or modified their homes to be easier to live in (42%), and 12% have moved or made plans to move to a community designed for older adults. The shares who report taking these steps are even smaller among those ages 50-64, some of whom may be approaching retirement: 28% have set aside money, 33% have looked for information about care options, 29% have modified their homes, and 9% have moved or made plans to move to a community designed for older adults. Among all adults 50 and older, the shares who report taking these steps are similar to those from a KFF survey in 2017.

Among all adults ages 50 and older, those from lower income households have not been able to plan as much for their aging needs as those with higher incomes, particularly when it comes to setting aside money. One in five (21%) older adults with household incomes less than $40,000 say they have set aside money specifically for ongoing living assistance, compared to nearly half (46%) of older adults with household incomes of at least $40,000. There are also differences in planning by education level. For example, nearly half (49%) of older adults with a college education say they have looked for information about aging issues and long-term care, compared to three in ten older adults with no college degree.

Another way to plan for future care needs is to purchase a long-term care insurance policy. One in ten adults (11%) say they have a private long-term care insurance policy, including 14% of those ages 65 and older.4 The share is slightly higher among those with higher household incomes (14% of those with household incomes of at least $40,000 vs. 6% of those with incomes under $40,000) and with college degrees (15% of college graduates vs. 9% of those with less than a college education).

Perceptions About How Long-Term Care Is Financed

There is a fair amount of confusion among the public about how the costs of long-term care are paid for different types of individuals. For example, while about half of adults (52%) correctly answer that Medicaid is the primary source of health insurance for low-income people who need nursing care or home care over a long period of time, a substantial four in ten (41%) incorrectly think that Medicare is the main source of this coverage. While those ages 65 and older (most of whom are covered by Medicare) are somewhat more knowledgeable than their younger counterparts, even among this group, 29% incorrectly believe Medicare provides this coverage.

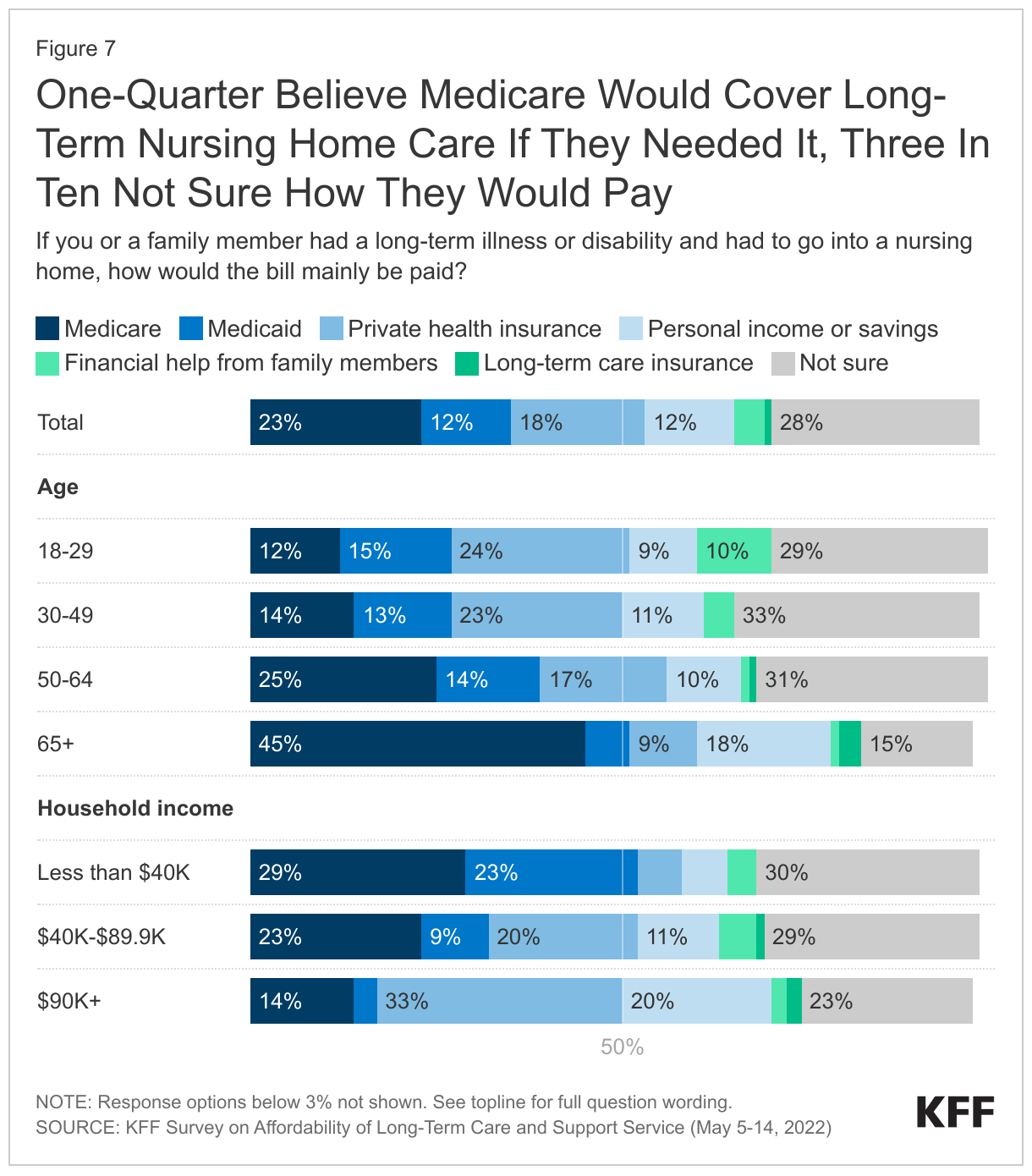

Confusion about how long-term care is financed is also evident when adults are asked to think about their own or a loved one’s potential long-term care needs. Nearly one in four adults (23%) incorrectly assume that Medicare would pay the bill for their own or a loved one’s time in a nursing home if they had a long-term illness or disability. Nearly half (45%) of adults ages 65 and older say that Medicare would cover these costs, compared to smaller shares of younger adults. Just over one in ten adults (12%) believe Medicaid would be the main payment source if they or a family member needed long-term nursing home care, including roughly one in four (23%) with household incomes less than $40,000 a year (some of whom might qualify for Medicaid in their state).

About one in five adults (18%) say private health insurance would be the main payment source if they or a family member needed nursing home care and another one in six say they would rely on personal income or savings (12%) or financial help from family members (4%). In fact, nearly three in ten adults (28%) are simply not sure how the bill for long-term nursing home care would be paid if such a need ever arose.

Perceived Affordability Of Long-Term Care

Despite the confusion about how long-term care is paid for, nearly nine out of ten (87%) adults say that they think that the cost of long-term care causes many or most of the people who need this care serious financial difficulties.

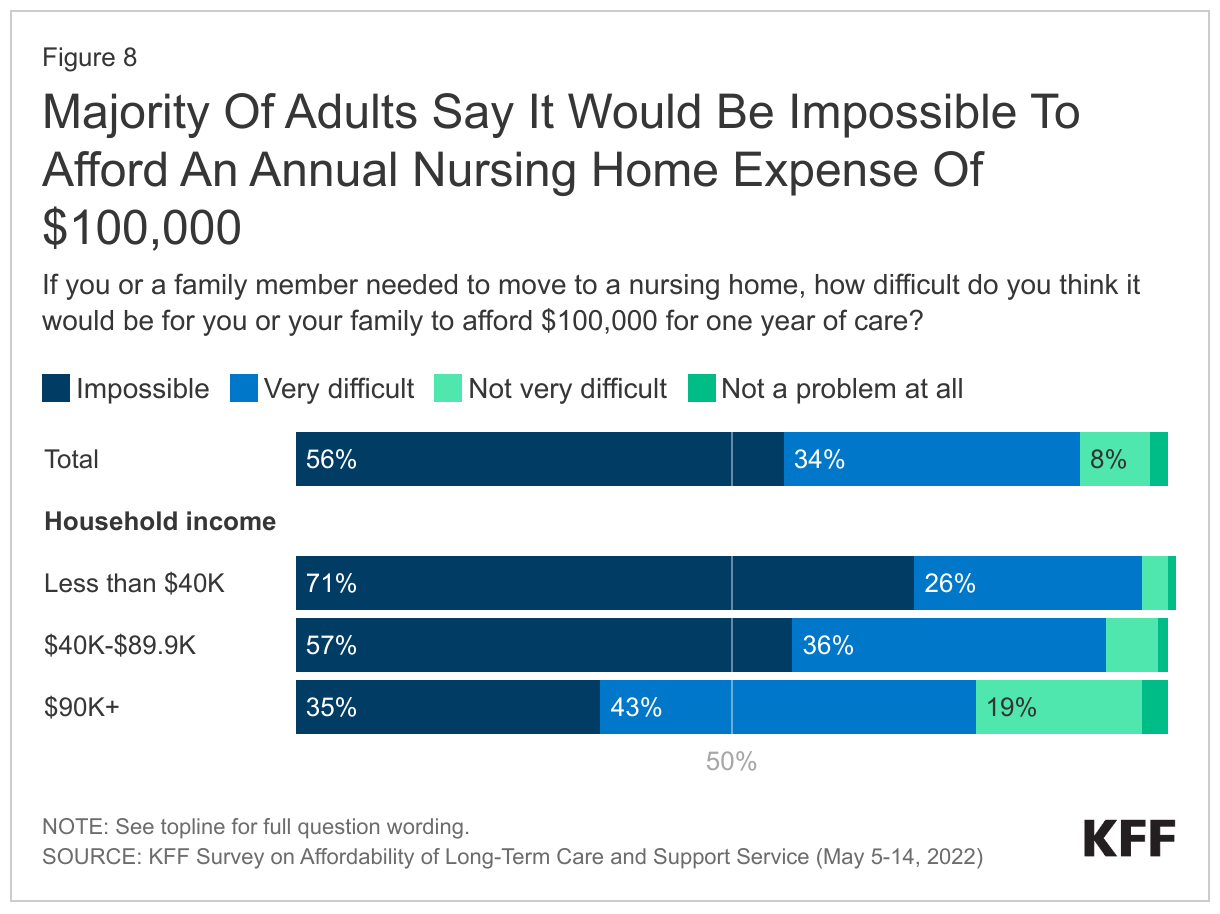

In fact, the overwhelming majority of adults (90%) say that it would be impossible or very difficult for them or their families to pay $100,000 for one year of nursing home care, which is a rough estimate of the median cost of such care in the United States.5 Responses were similar in a 2001 survey, when 92% of adults said it would be impossible or very difficult for them to pay $60,000 for a year of nursing home care, the median cost at that time. While large majorities across the income spectrum say affording nursing home care would be at least “very difficult,” the share who would find such care “impossible” to afford is higher among those with lower incomes. Those with household incomes under $40,000 a year are twice as likely to say that it would be impossible for them to afford a year of nursing home care compared to those with incomes of at least $90,000 (71% vs. 35%).

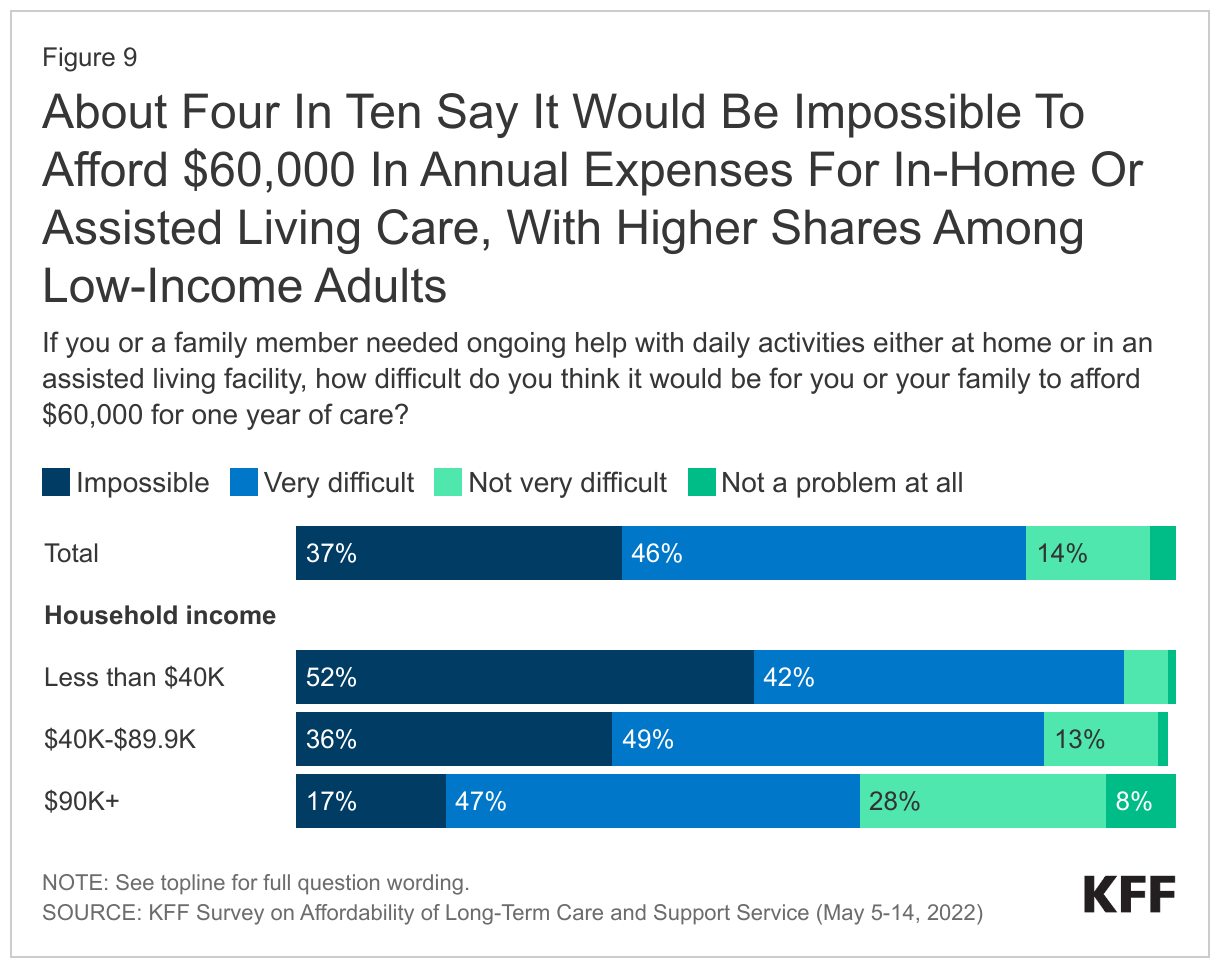

Similarly, eight out of ten adults (83%) say it would be impossible or very difficult to pay $60,0006 for one year of ongoing help with daily activities at home or at an assisted living facility. However, the 37% of adults overall who say paying $60,000 would be impossible is a notably smaller share than the 56% who say it would be impossible to pay $100,000 for nursing home care. Income remains an important indicator of how “impossible” it feels to afford such an expense, as adults with lower incomes are three times as likely to say “impossible” compared to those with higher incomes (52% of those with household incomes less than $40,000 vs. 17% of those with incomes of $90,000 or more).

Personal Experiences With Long-Term Care

Nearly half of adults in the U.S. (47%) report some level of personal connection to paid or unpaid long-term care in the past two years. This includes roughly one in four (27%) who have personally resided in or had a loved one who was a resident in a nursing home or assisted living facility, three in ten (30%) who have personally or had a loved one who received ongoing support for daily activities from a paid nurse or aide, and nearly four in ten (38%) who have personally or have a loved one who received such support from a friend or family member. In total, 38% say they or a loved one received paid long-term care support either in a facility or at home, including 4% who say they personally received such support and 36% who say a loved one did (there is some overlap in these figures since some people say both they and a loved one used paid services). Nearly one in five (18%) say they personally acted as a caregiver for a loved one in the past two years.

Difficulties Finding And Affording Care

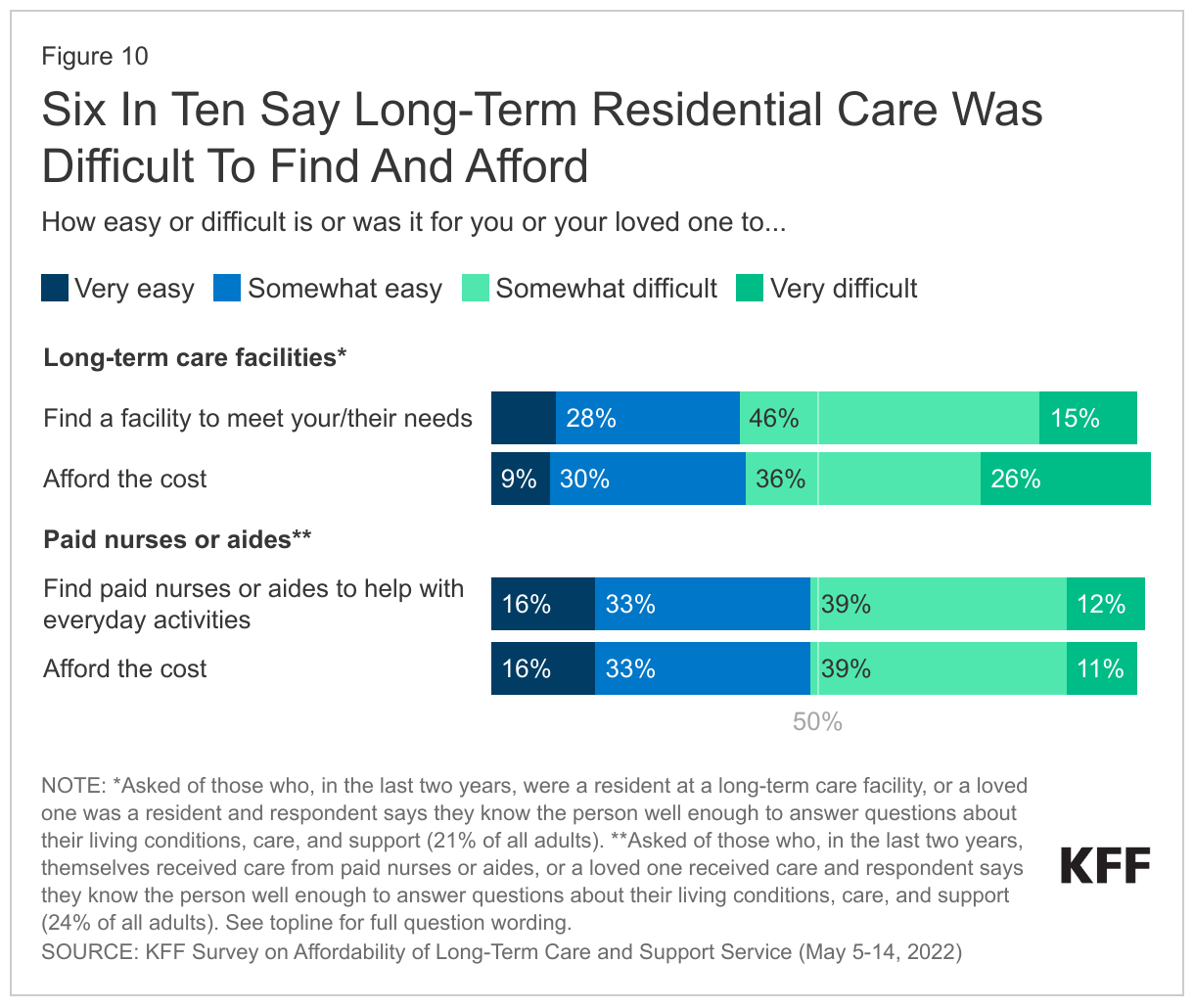

Many adults report difficulty finding and affording long-term care, particularly when it comes to residential facilities. Among those who personally stayed in a long-term care facility or knew enough about a loved one’s experience in such a facility to answer questions about their living conditions, care, and support, approximately six in ten (62%) say it was “somewhat difficult” or “very difficult” to find a facility that met their or their loved ones’ needs, and the same share report that it was difficult to afford that care, including one-quarter (26%) who say it was “very difficult.” Moreover, nearly half (45%) say that after they or their loved one moved into a long-term care facility, they encountered unexpected costs for things they thought were included but were added on as extra charges by the facility.

Among those who personally or had a loved one who received help with everyday activities from paid nurses or aides, about half (51%) say they found the process of finding such help difficult, and a similar share (50%) say it was difficult to afford this kind of support. In both finding and affording the care provided by paid aides, 49% say they found it to be easy.

Satisfaction With The Quality And Cost Of Care

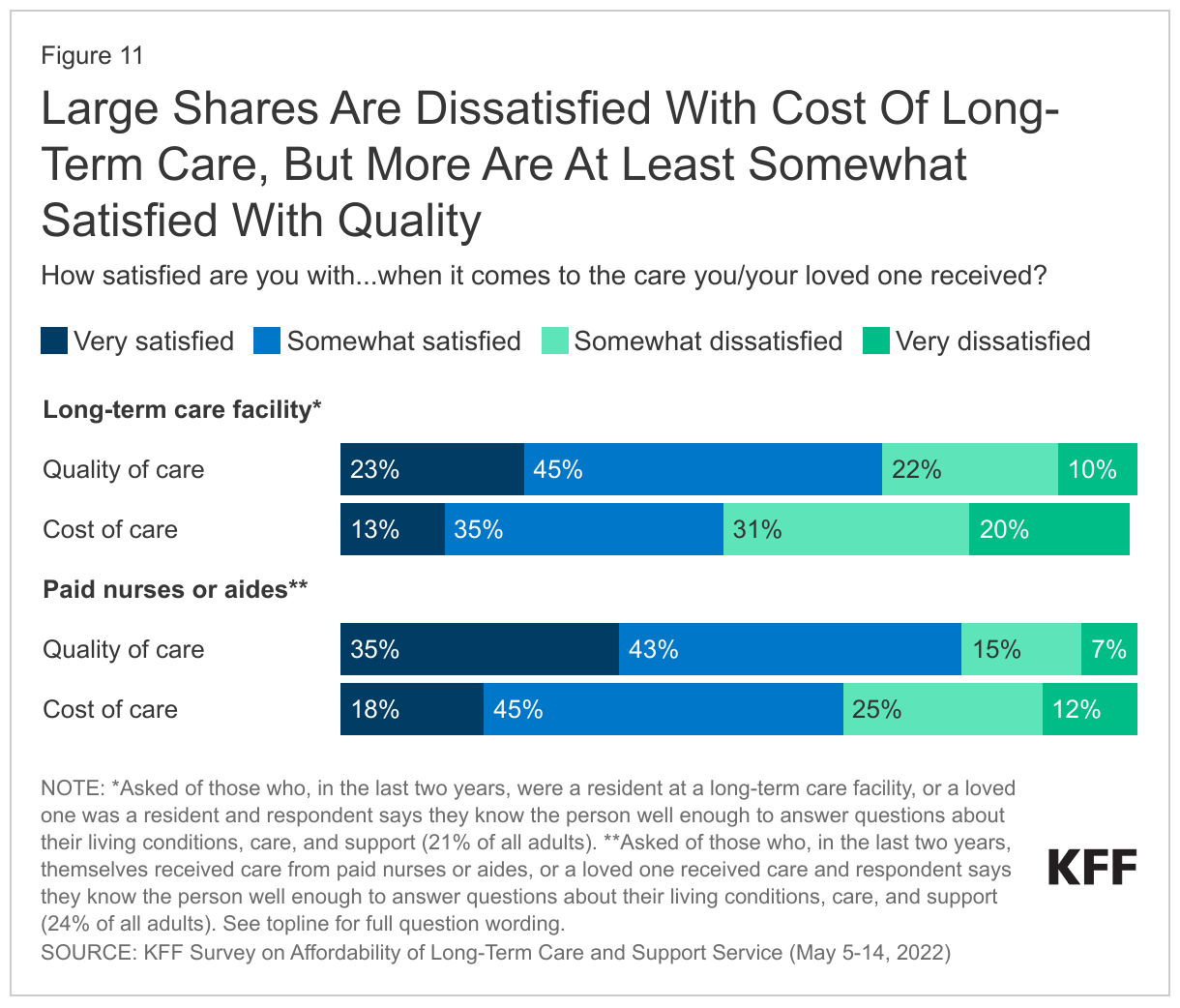

Many adults are dissatisfied with the cost of long-term care, particularly when it comes to residential facilities, but most are at least somewhat satisfied with the quality of the care they or their loved ones received. Among those with personal experience or sufficient knowledge of a loved one’s time in a long-term care facility, about half (51%) say they are “somewhat dissatisfied” or “very dissatisfied” with the cost of their or their loved one’s residential long-term care facility, while the other half (49%) say they are “very” or “somewhat” satisfied. Among those with personal experience or knowledge of a loved one’s care from paid nurses or aides, a majority (63%) say they are satisfied with the cost of such care, but a substantial share (37%) is dissatisfied.

When it comes to the quality of the long-term care, majorities say they are at least “somewhat” satisfied, with about a quarter saying they are “very” satisfied with the quality of care they or their loved one received in a long-term care facility (23%) and about a third saying the same about the quality of care from paid nurses or aides (35%). Meanwhile, one third (33%) say they are dissatisfied with the quality of residential care and one in five (22%) say the same about the quality of care from paid aides. Notably, those with household incomes under $40,000 are somewhat more likely than those with higher incomes to be dissatisfied with the quality of care in residential facilities (42% vs. 28% dissatisfied).

Financial Challenges Faced By Those Paying For Long-Term Care

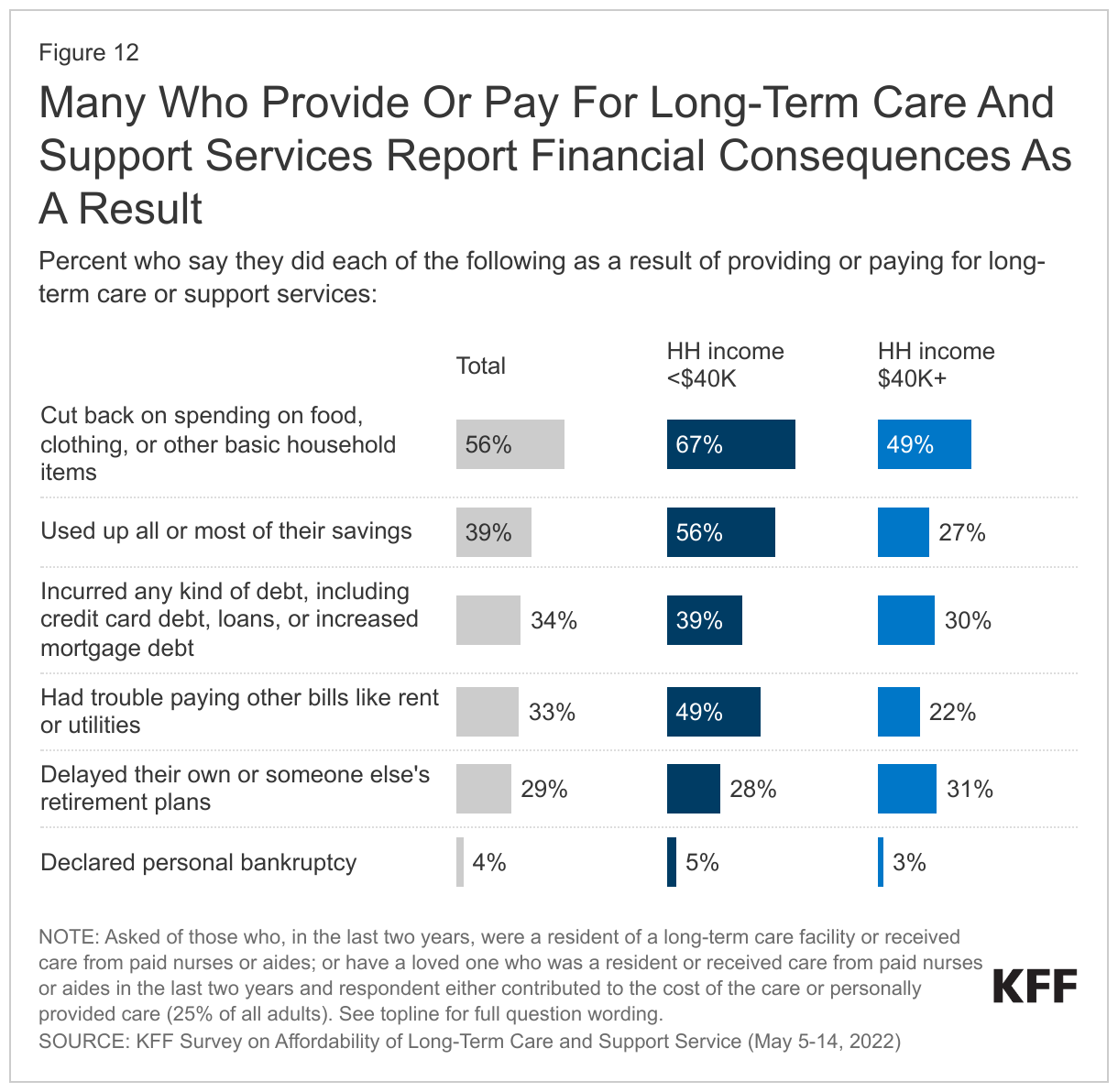

In addition to reporting difficulty affording long-term care and support services, many of those who contribute financially to their own or a family member’s care report experiencing financial consequences as a result. Among those who say they contributed financially to their own or another’s long-term care or acted as a caregiver for a loved one,7 more than half (56%) say they cut back spending on food, clothing or other basic household items as a result of providing or paying for care, and about four in ten (39%) say they used up all or most of their savings. Roughly three in ten say they incurred any kind of debt (34%), had trouble paying other bills like rent or utilities (33%), or delayed their own or someone else’s retirement (29%) as a result of providing or paying for long-term care or support services, while a very small share (4%) report declaring personal bankruptcy.

People in lower-income households are more likely than their higher-income counterparts to report many of these financial effects of providing or paying for long-term care and supports. Among those who provide or help pay for such care, two-thirds (67%) of those from lower-income households report cutting back spending on household items as a result, compared to about half (49%) of those from higher-income households. Nearly half of those in households earning less than $40,000 (49%) say they had trouble paying rent or other utilities as a result of providing or paying for long-term care, compared to roughly one in five (22%) of those with incomes of at least $40,000.

In a separate question asked of people who report that they provide care or contribute financially to their own or another person’s long-term care, a third (33%, or 8% of all adults) say they have experienced any financial challenges directly as a result of paying for or providing these services. When asked to describe the nature of these challenges, respondents detailed a variety of circumstances that the obligation of long-term care precipitated, such as taking a leave of absence from their own careers or leaning on loans or family generosity to make up for the financial shortfall.

In Their Own Words: How Contributing Long-Term Care to Those Who Need it Affects Individual Finances

“My income barely met the requirements for a home facility, and it broke my bank” – 28-year-old woman from California whose loved one resided in a long-term care facility

“Took out loans to cover some of the costs not covered by insurance” – 60-year-old man from Ohio whose loved one received support from paid nurses or aides

“Had to rely on family for food and help with bills some months. Terrible times” – 36-year-old man from California whose loved one resided in a long-term care facility

“Having to decide which things not to pay for in monthly costs in order to pay for the long-term care” – 26-year-old woman from Kentucky whose loved one resided in a long-term care facility

“Had to take a leave of absence from my employer in order to care for my 85-year-old mother.”- 63-year-old woman from Mississippi who provided care for a loved one

Methodology

The KFF Survey on Affordability of Long-term Care and Support Service was designed and analyzed by public opinion researchers at the KFF. The survey was conducted May 5th-14th, 2022 online and by telephone among a nationally representative sample of 1,573 U.S. adults, in English (1,502) and in Spanish (71). The sample includes 1,422 adults reached through the SSRS Opinion Panel online. The SSRS Opinion Panel is a nationally representative probability-based panel where panel members are recruited randomly in one of two ways: (a) Through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS) provided by Marketing Systems Groups (MSG) through the U.S. Postal Service’s Computerized Delivery Sequence (CDS); (b) from a dual-frame random digit dial (RDD) sample provided by MSG. For the online panel component, invitations were sent to panel members by email followed by up to four reminder emails. An additional 151 interviews were conducted by telephone with respondents who previously interviewed as part of the SSRS RDD Omnibus poll and indicated they do not access the internet. Web-panelists received a modest incentive for participation in the form of an electronic gift card for the SSRS Opinion Panel. For the callback sample, a $10 incentive was offered to all respondents.

A series of data quality checks were run on the final data. This included a review of the following: all grids straight-lined (i.e., providing the same response to every item in a grid); cases with more than 25% question non-response; cases with a length less than one third of the mean length from respondents who experienced long term care or had a loved one who received long-term care; and open-ended responses that were unintelligible, nonsensical, or seemed suspicious. Based on this criterion, 7 cases were removed.

The combined telephone and online panel samples were weighted to match the sample’s demographics to the national U.S. adult population using data from the Census Bureau’s 2021 Current Population Survey (CPS). Weighting parameters included gender by age, gender by education, age by education, race by education, race by age, race by gender, detailed race/ethnicity, detailed education, census region, internet frequency, population density and party ID. The gender, age, education, race/ethnicity, and census region benchmarks were derived from 2021 Current Population Survey (CPS) data. The population density came from Census Planning Database 2020. The internet frequency and party ID were derived from the National Public Opinion Reference Survey (NPORS) for Pew Research Center - May 29 to Aug 25, 2021. The weights take into account differences in the probability of selection for each sample type (SSRS Probability Panel or via the callback sample). For the SSRS Probability Panel, this includes adjustment for within household probability of selection and the design of the panel recruitment procedure. For the callback sample, this includes propensity for nonresponse.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Sampling error is only one of many potential sources of error and there may be other unmeasured error in this or any other public opinion poll. KFF public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

| Group | N (unweighted) | M.O.S.E. |

| Total | 1,573 | ± 3 percentage points |

| . | ||

| Self or loved one has been a resident in a long-term care facility or received support from paid nurses or aides in past two years (NET) | 586 | +5 percentage points |

| Self or loved one has been a long-term care resident | 402 | ± 6 percentage points |

| Self or loved one has received support from paid nurses or aides | 445 | ± 6 percentage points |

Endnotes

- For more details about LTSS, including the populations who use LTSS, cost estimates and policy, see KFF’s reports on Long-Term Services and Supports (LTSS) and Medicaid’s role in financing these services. ↩︎

- This survey, like most public opinion surveys, excludes responses from the institutionalized population, so findings may not fully represent the views of all individuals who currently use long-term services and supports. To help account for this, some questions in the survey ask respondents questions about the experiences of their loved ones who have used these services in the past two years. ↩︎

- As of 2020, KFF estimates that Medicaid paid 54% of the approximately $400 billion spent on LTSS in the U.S. See KFF’s issue brief, 10 Things About Long-Term Services and Supports (LTSS), for more information. ↩︎

- The American Association for Long-term Care Insurance estimates that 7.5 million Americans have some long-term care insurance in place, suggesting there is some level of over-reporting on this survey question. Given the level of confusion around how long-term care is paid for, one possible explanation is that some people may wrongly assume that their existing private health care insurance will also cover long-term care support services if needed, and so may answer yes to this question even if they have not purchased a separate long-term care insurance plan. ↩︎

- The $100,000 estimate for one year of nursing home costs is derived from Genworth’s estimates of the monthly median costs of a nursing home facility in the United States. Roughly averaging the monthly cost of a semi-private room ($7,908) and a private room ($9,034) in a nursing home facility resulted in an estimated annual cost of $102,000, which was simplified to $100,000 for the purposes of the survey questionnaire. ↩︎

- The $60,000 estimate for one year of in-home care or assisted living facility costs is derived from Genworth’s estimates of the monthly median costs of a home health aide and an assisted living facility in the United States. Roughly averaging the monthly cost of homemaker services ($4,957), a home health aide ($5,148), and an assisted living facility ($4,500) resulted in an estimated annual cost of $60,000. ↩︎

- This question was asked of adults who said they received paid long-term care at a residential facility or from paid nurses or aides in the last two years, those who said they financially contributed to the cost of the long-term care that a loved one received in the last two years, and those who said they personally provided unpaid care to a loved one in the last two years. ↩︎