Most Medicare Advantage Markets are Dominated by One or Two Insurers

Enrollment in Medicare Advantage, the private plan alternative to traditional Medicare, has increased steadily since 2010. The average beneficiary has access to 34 Medicare Advantage plans with prescription drug coverage in 2025, double the number available in 2018. On average, Medicare beneficiaries have access to plans offered by 8 firms, a slight increase from 2018. One goal of offering Medicare coverage through private plans is to leverage competition with the idea that insurers will compete to provide better benefits and lower costs to attract and retain enrollees. However, recent analysis finds that Medicare Advantage markets are highly concentrated, suggesting that the growth in enrollment and plan availability has not occurred in the context of a competitive market.

Higher market concentration in Medicare Advantage insurance markets may lower the incentive for insurers to compete for potential enrollees by making plans more appealing through more comprehensive benefits or lower costs. However, the competitiveness, or lack thereof, of Medicare Advantage markets has not been a priority of policymakers or regulators, especially in recent years. The most recent activity at the federal level occurred in 2017 when the Department of Justice blocked a merger between insurers Aetna and Humana, arguing if it went through it would significantly raise market concentration in the Medicare Advantage market. More recently, the conversation regarding competition in health care has revolved around increased consolidation in provider markets, especially hospitals and health systems.

To examine the competitiveness of Medicare Advantage markets, this analysis uses publicly available, county-level Medicare Advantage plan information and enrollment data for all 50 states, D.C., and Puerto Rico, published by the Centers for Medicare and Medicaid, to calculate the Herfindahl-Hirshman Index (HHI) for each market (a county is considered a Medicare Advantage market because plans are offered at the county level). The HHI uses the relative market shares of all Medicare Advantage insurers offering plans in a county to create a measure of market concentration. Counties are then classified as unconcentrated, moderately concentrated, highly concentrated, or very highly concentrated markets. These categories align with guidelines published by the Federal Trade Commission and U.S. Department of Justice, except in that a fourth category (very highly concentrated) is added to further discern differences within the most concentrated markets. This analysis also examines how often one or two Medicare Advantage insurers enrolled at least half of all enrollees within a county, which provides an alternative illustration of market concentration (See Methods for more details).

Key Takeaways

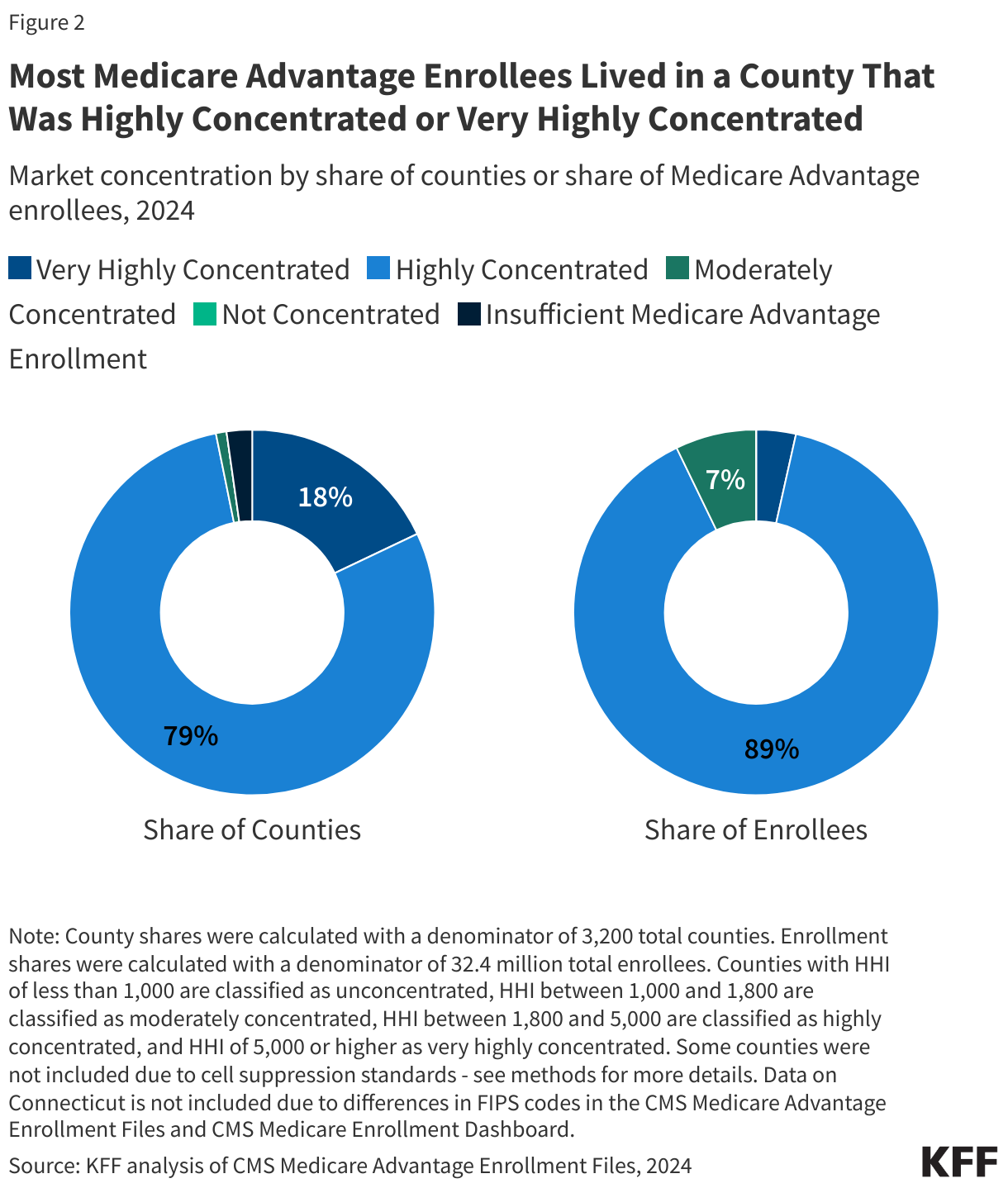

- Virtually all counties were highly concentrated (79%) or very highly concentrated (18%) in 2024. Less than 1% were moderately concentrated and 0% of counties were unconcentrated. (2% of counties had low or no Medicare Advantage enrollment.)

- Most (89%) Medicare Advantage enrollees were in highly concentrated markets, with another 4% of Medicare Advantage enrollees in very highly concentrated markets.

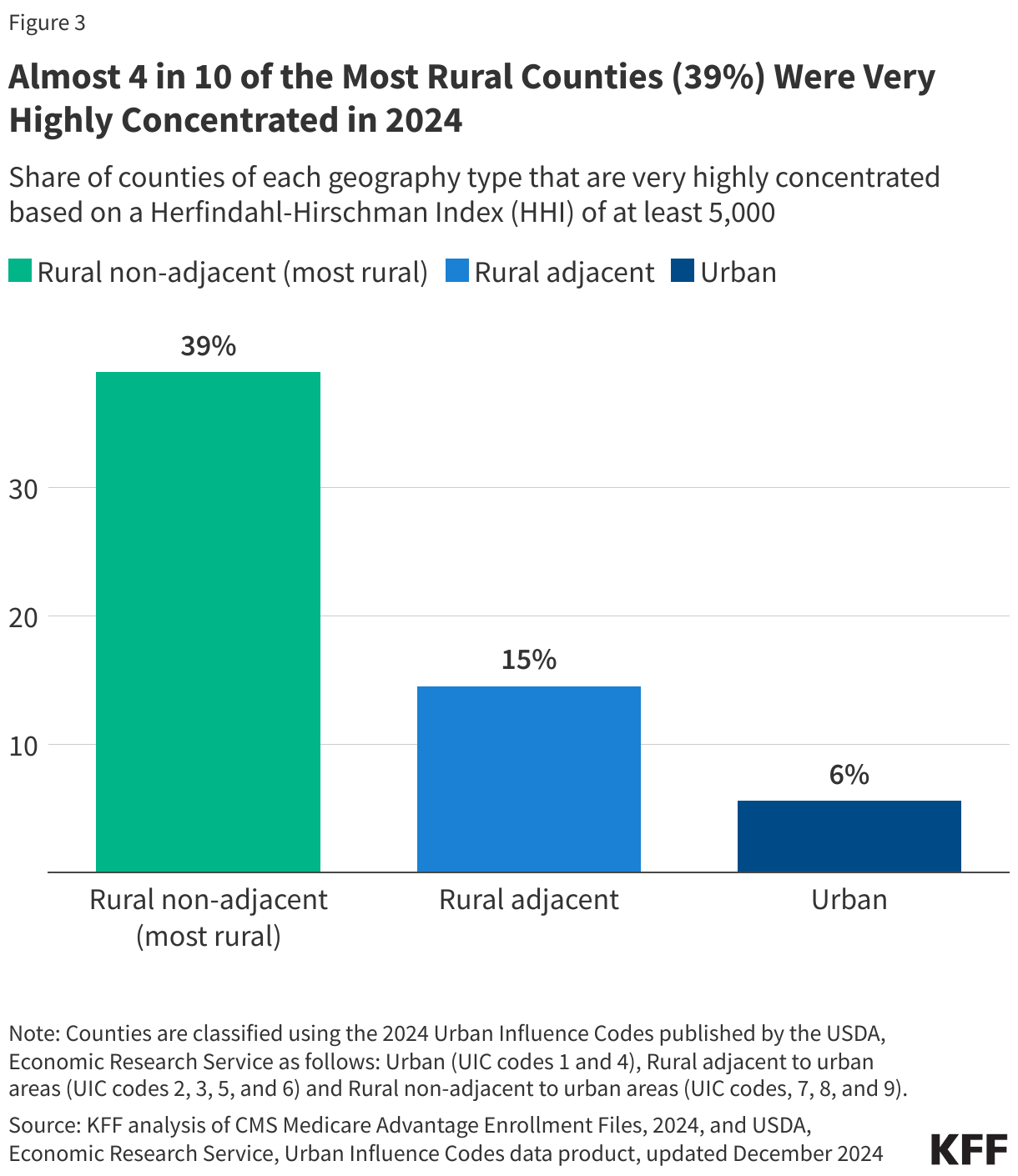

- Medicare Advantage markets were more concentrated in rural counties than in urban counties: 39% of the most rural counties were very highly concentrated in 2024 compared with 15% of rural counties that were near urban areas and 6% of urban counties.

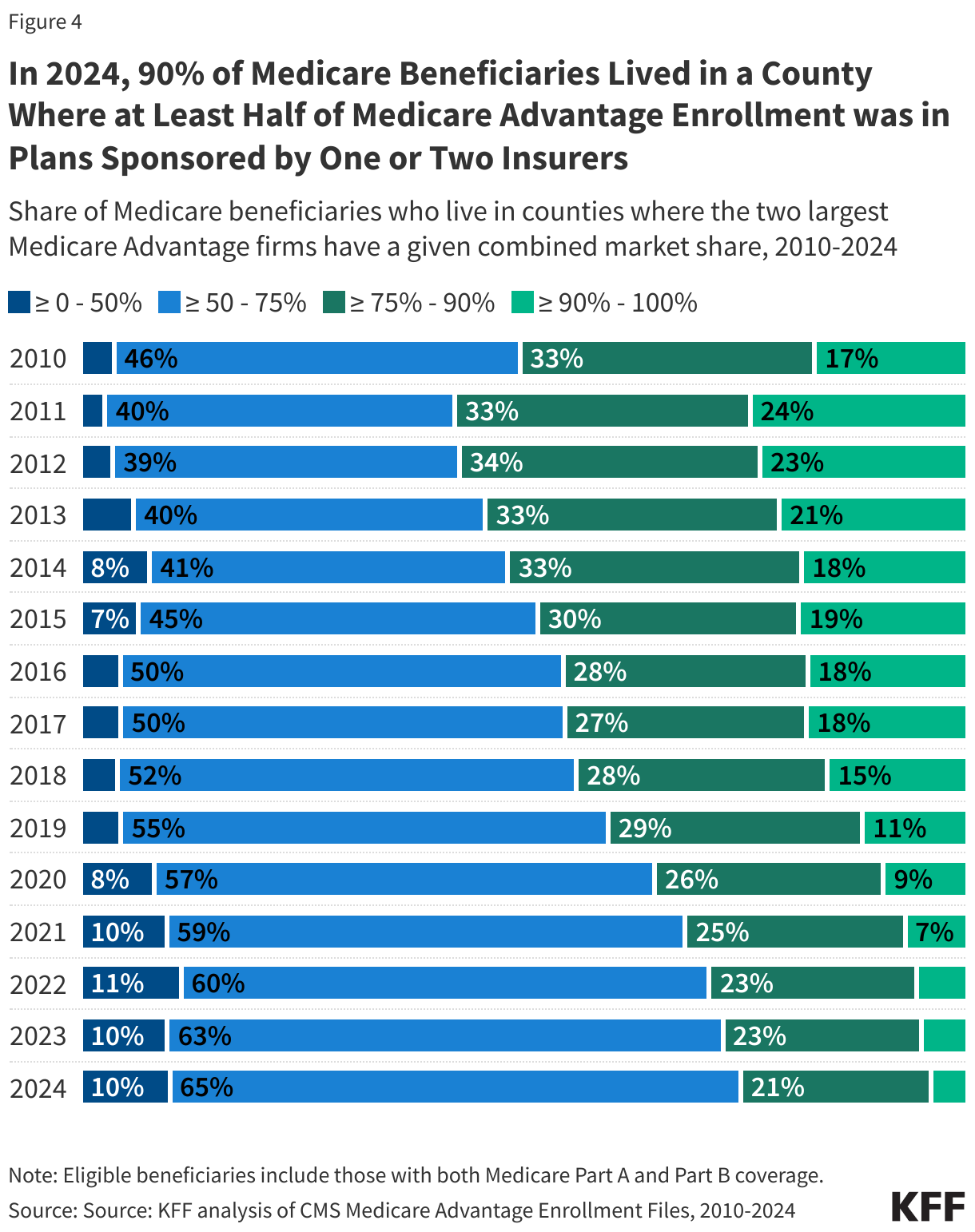

- Nine in ten (90%) Medicare beneficiaries lived in a county where at least half of all Medicare Advantage enrollees were in plans sponsored by one or two insurers in 2024.

- UnitedHealthcare (41%) or Humana (25%) had the highest enrollment in two-thirds of counties, which comprised 59% of all Medicare Advantage enrollment, in 2024. Among all Medicare Advantage insurers, UnitedHealthcare was the dominant insurer in the largest share of highly concentrated markets (41%) and very highly concentrated markets (50%) in 2024.

- In more than four in ten counties (44%), comprising 22% of all Medicare Advantage enrollment, a single Medicare Advantage insurer had at least 50% of enrollment in 2024, including 22% of counties where UnitedHealthcare had at least 50% of enrollment and 10% of counties where Humana had at least 50% of enrollment. Some large counties where one insurer had at least 50% of enrollment include Dallas County, Texas (55%), Salt Lake County, Utah (52%), and Milwaukee County, Wisconsin (64%).

Virtually all Medicare Advantage insurance markets were highly concentrated (79%) or very highly concentrated (18%) in 2024.

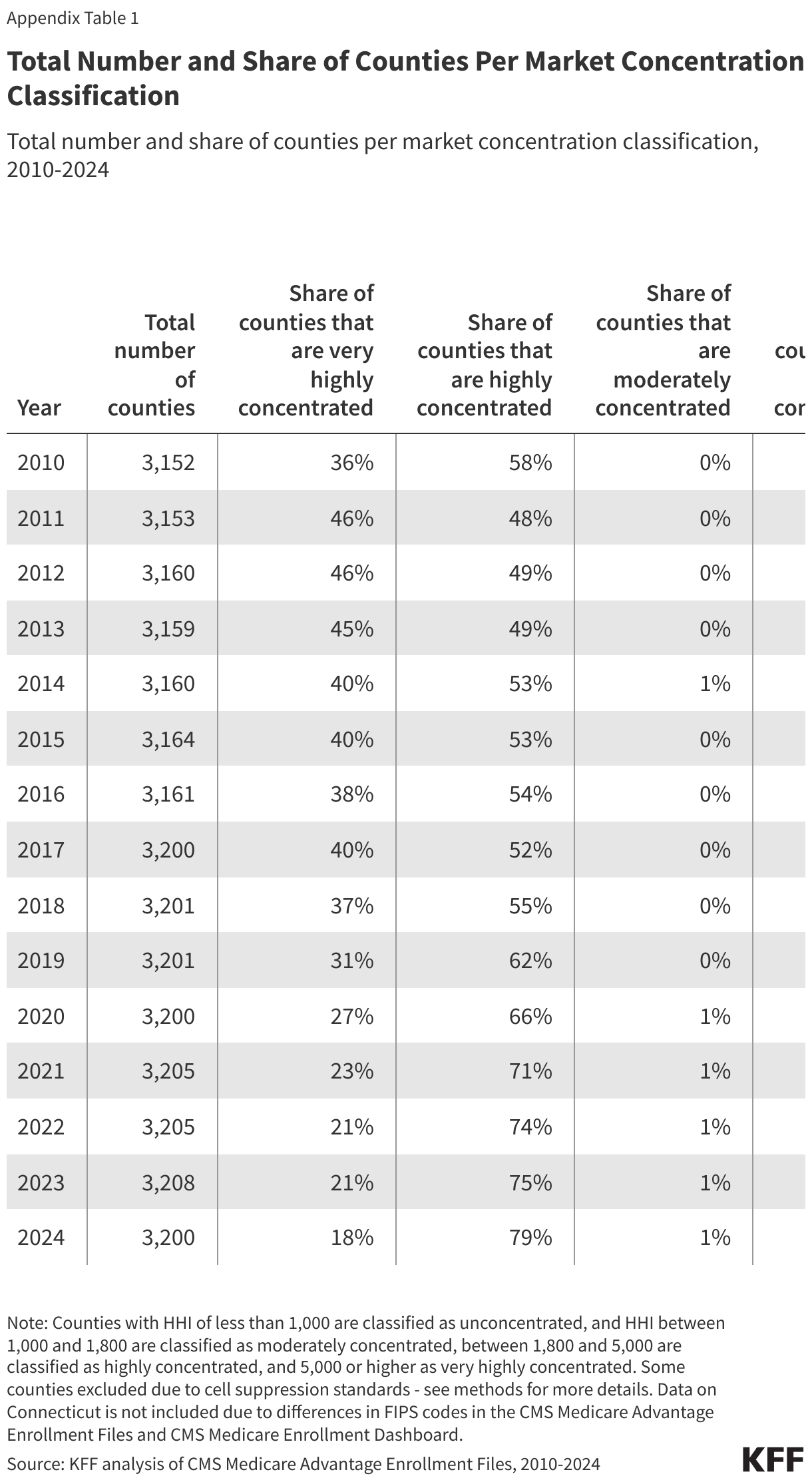

In 2024, virtually every county was a highly concentrated or very highly concentrated market for Medicare Advantage (Figure 1). A total of 2,524 counties (79%) were highly concentrated markets and 574 counties (18%) were very highly concentrated markets (Figure 2). Just 30 counties (<1%) were moderately concentrated markets. No counties were unconcentrated. (In 2024, 72 counties (2%) did not have sufficient Medicare Advantage enrollment to have a market concentration classification.)

Most Medicare Advantage enrollees were in a highly concentrated (89%) or very highly concentrated market (4%) in 2024.

Most Medicare Advantage enrollees lived in a highly concentrated or very highly concentrated market: 28.9 million out of 32.3 million Medicare Advantage enrollees (89%) lived in a highly concentrated market, while 1.1 million lived (4%) lived in a very highly concentrated market in 2024 (Figure 2). Of the remaining Medicare Advantage enrollees, 2.3 million (7%) lived in moderately concentrated markets. No Medicare Advantage enrollees were in unconcentrated markets.

Since 2010, the share of counties that were either highly concentrated or very highly concentrated Medicare Advantage markets has changed little (94% of counties in 2010 compared to 97% in 2024). However, there have been shifts within markets at the highest levels of concentration. Specifically, the share of counties that are very highly concentrated markets declined from 36% in 2010 to 18% in 2024, while the share of counties that are highly concentrated has increased from 58% in 2010 to 79% in 2024 (Appendix Table 1).

Medicare Advantage markets were more concentrated (and less competitive) in rural than urban counties.

On average, Medicare Advantage markets in rural areas were more concentrated than those in urban areas in 2024 (data not shown). Consistent with this finding, substantially more counties were very highly concentrated in the most rural areas (39%), compared with rural counties near urban areas (15%), and counties in urban areas (6%) (Figure 3).

A much larger share of Medicare Advantage enrollees living in the most rural counties were in very highly concentrated markets than either rural adjacent or urban counties: 16% of Medicare Advantage enrollees in the most rural counties lived in very highly concentrated markets, compared to 6% of Medicare Advantage enrollees in rural counties near urban areas and approximately 3% of Medicare Advantage enrollees in urban areas.

Nine in ten (90%) Medicare beneficiaries lived in counties where more than half of all Medicare Advantage enrollees were in plans sponsored by one or two firms in 2024.

In 2024, 90% of eligible Medicare beneficiaries – 54.3 million out of 60.5 million – lived in a county where at least 50% of Medicare Advantage enrollees in that county were in plans sponsored by one or two insurers (Figure 4). This represents a small decrease since 2010, when 96% of eligible beneficiaries – 41.4 million out of 43.5 million – lived in a county where at least half of Medicare Advantage enrollees were in plans sponsored by one or two insurers.

There has been a sharper decline in the share of Medicare beneficiaries living in counties where at least 75% of Medicare Advantage enrollment was in plans sponsored by one or two insurers. In 2010, 50% of Medicare beneficiaries lived in counties where the two largest firms comprised at least 75% Medicare Advantage enrollment compared with 25% in 2024.

UnitedHealthcare or Humana was the largest Medicare Advantage insurer in over half of counties in 2024.

UnitedHealthcare had the highest market share in more counties (41%) than any other Medicare Advantage insurer in 2024 – meaning that for 38% of all Medicare Advantage enrollees nationwide, UnitedHealthcare was the largest insurer in their county (Figure 5). Humana was the largest insurer in 25% of all counties in 2024; for 21% of all Medicare Advantage enrollees nationwide, Humana was the largest insurer in their county. UnitedHealthcare and Humana have consistently been the two largest insurers in the Medicare Advantage market, and comprised nearly half (47%) of all Medicare Advantage enrollment across the country in 2024.

UnitedHealthcare and Humana’s dominance was especially prominent in the least competitive markets: UnitedHealthcare was the largest Medicare Advantage insurer in 50% of all very highly concentrated counties and in 41% of highly concentrated counties in 2024, while Humana was dominant in 22% of very highly concentrated counties and in 26% of highly concentrated counties.

Other insurers enrolled the largest number of Medicare beneficiaries in a smaller number of counties. BlueCross BlueShield (BCBS) affiliates were the largest Medicare Advantage insurer in 11% of all counties, followed by CVS Health (8%), and Elevance Health (4%). In 2% of counties there was not sufficient Medicare Advantage enrollment to examine enrollment by insurer.

A single insurer comprised at least half of Medicare Advantage enrollment in 44% of counties in 2024.

In 44% of counties, comprising 22% of all Medicare Advantage enrollment, a single insurer enrolled at least 50% of all Medicare Advantage enrollees in 2024. In half of these counties (22%), UnitedHealthcare was the single insurer with a market share of at least 50%, including in Dallas County, Texas (55%), Salt Lake County, Utah (52%), Milwaukee County, Wisconsin (64%), Boulder County, Colorado (52%), and the District of Columbia (64%) (Appendix Table 2).

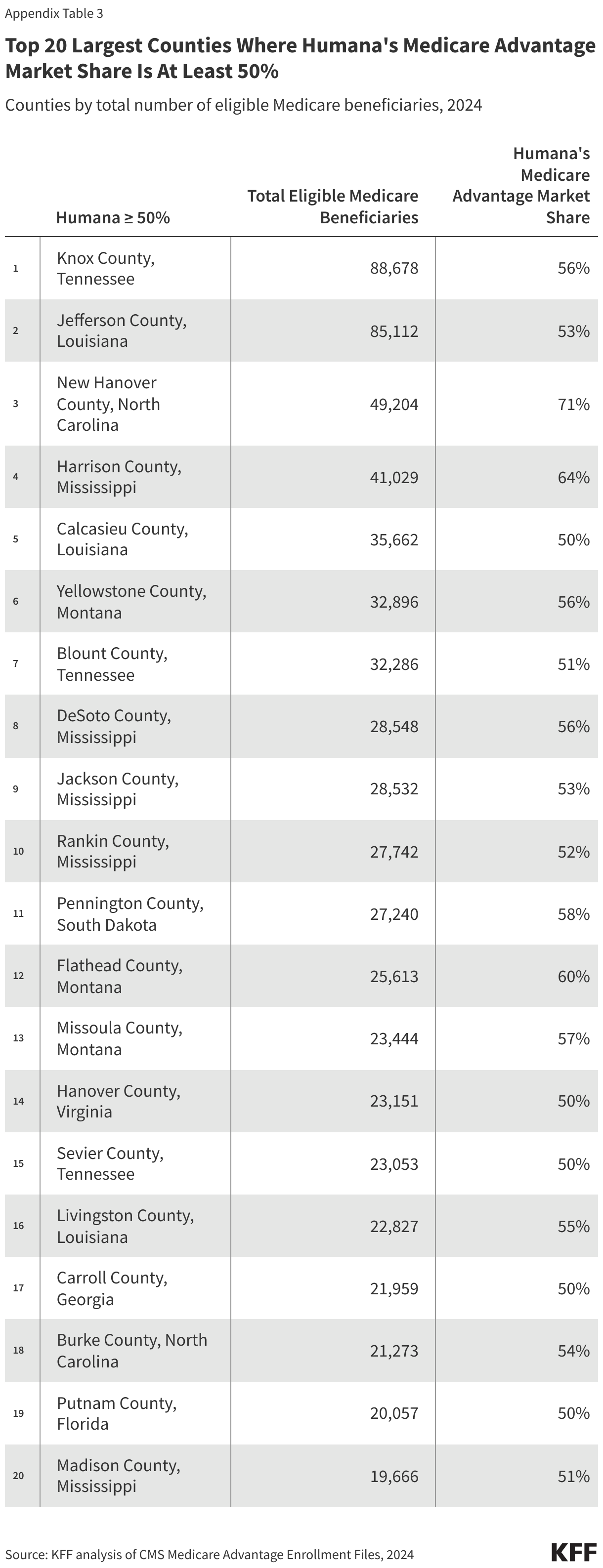

Humana enrolled at least half of all Medicare Advantage enrollees in 10% of counties, BCBS affiliates in 5% of counties, CVS Health in 3% of counties, and Elevance Health in less than 1% of counties (Appendix Table 3). Other insurers had at least 50% of Medicare Advantage enrollment in 3% of counties.

Appendix

This work was supported in part by Arnold Ventures and AARP. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.