KFF Analysis: Average Health Insurance Tax Credit for Consumers Would Be at Least a Third Lower Under Currently Discussed Replacement Plans than the ACA

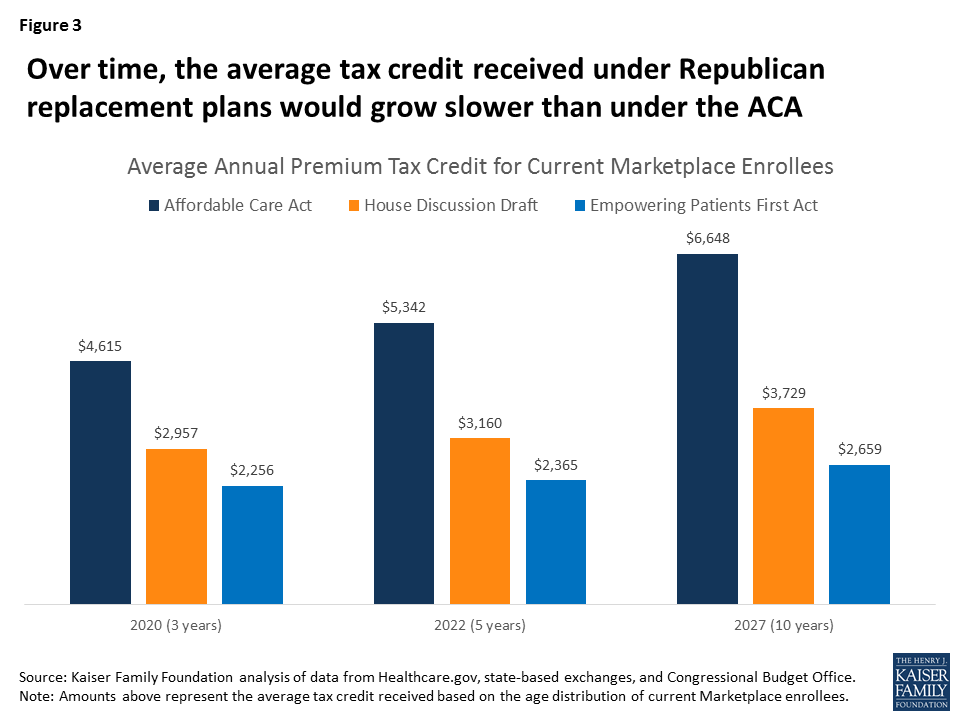

Tax Credits in Proposals Also Would Increase More Slowly Over Time Than Under ACA

A new analysis from the Kaiser Family Foundation estimates that the average health insurance premium tax credit received by consumers in 2020 would be at least 36 percent lower under replacement proposals being discussed by Republicans in Congress than under the Affordable Care Act.

The average tax credit also would increase more slowly under replacement proposals, the analysis finds: In the House Discussion Draft alternative to the ACA, which has been recently discussed in media reports, the average tax credit for current ACA marketplace enrollees would rise from an estimated $2,957 in 2020 to $3,729 in 2027. By comparison, the average tax credit under the ACA would be $4,615 in 2020, increasing to $6,648 in 2027.

The new analysis provides estimates of average 2020 tax credits for people who were enrolled in ACA marketplace plans as of 2017, including average credits for those with low, middle, and high incomes at ages 27, 40, and 60, and in markets with low-, average, and high-cost health insurance premiums.

It finds that people with lower incomes, who are older, or who live in markets with higher premiums would receive larger tax credits under the ACA than under replacement proposals. By contrast, people with higher incomes, who are younger, or who live in areas with lower premiums would benefit more from alternative plans.

Both the Affordable Care Act and leading alternative proposals rely on refundable tax credits – reductions in what is owed in federal income tax — to help people pay premiums for health insurance plans in the individual market. However, proposals such as the House Discussion Draft and the “Empowering Patients First Act,” introduced by Rep. Tom Price before he became U.S. Secretary of Health and Human Services, calculate credit amounts differently than the health law.

The ACA takes family income, local cost of insurance, and age into account; and tax credit increases are based on premium growth over time. People with incomes over 400 percent of the federal poverty level are ineligible for financial assistance under the ACA. Under replacement proposals, tax credits vary only with the enrollee’s age, and increases are based on inflation.

How Affordable Care Act Repeal and Replace Plans Might Shift Health Insurance Tax Credits is available on kff.org