How Will the Uninsured in Florida Fare Under the Affordable Care Act?

The 2010 Affordable Care Act (ACA) has the potential to extend coverage to many of the 47 million nonelderly uninsured people nationwide, including the 3.9 million uninsured Floridians. The ACA establishes coverage provisions across the income spectrum, with the expansion of Medicaid eligibility for adults serving as the vehicle for covering low-income individuals and premium tax credits to help people purchase insurance directly through new Health Insurance Marketplaces serving as the vehicle for covering people with moderate incomes. With the June 2012 Supreme Court ruling, the Medicaid expansion became optional for states, and as of December 2013, Florida was not planning to implement the expansion. As a result, many uninsured adults in Florida who would have been newly-eligible for Medicaid will remain without a coverage option. As the ACA coverage expansions are implemented and coverage changes are assessed, it is important to understand the potential scope of the law in the state.

How does the ACA Expand Health Insurance Coverage in Florida?

Historically, Medicaid had gaps in coverage for adults because eligibility was restricted to specific categories of low-income individuals, such as children, their parents, pregnant women, the elderly, or individuals with disabilities. In most states, adults without dependent children were ineligible for Medicaid, regardless of their income, and income limits for parents were very low—often below half the poverty level.1 The ACA aimed to fill in these gaps by extending Medicaid to nearly all nonelderly adults with incomes at or below 138% of poverty (about $32,500 for a family of four in 2013).

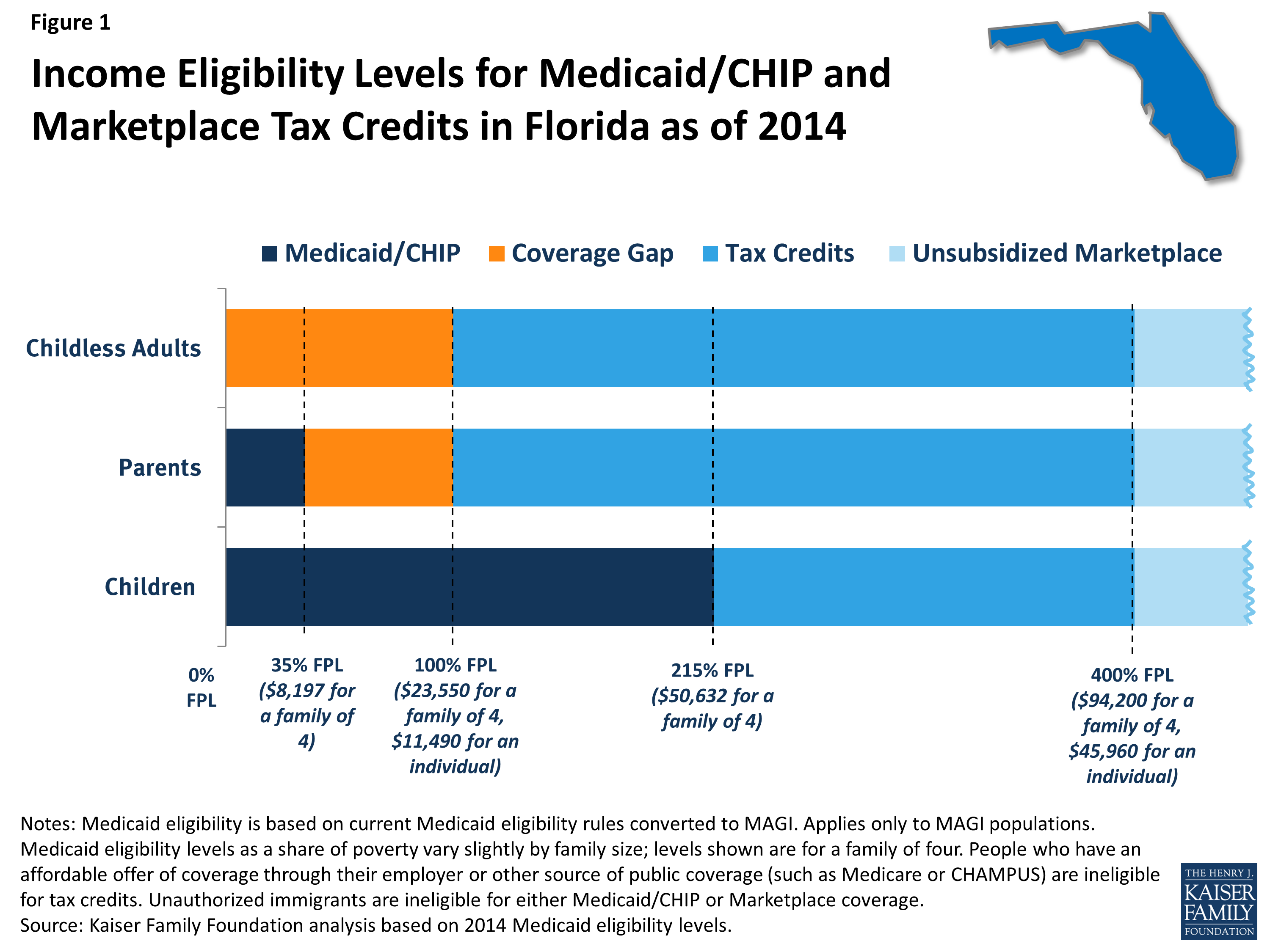

In states that do not implement the expansion (such as Florida), Medicaid eligibility for adults will remain quite limited, as shown by the dark blue shading in Figure 1. As of January 2014, in Florida, Medicaid eligibility for non-disabled adults is limited to parents with incomes below 35% of poverty, or about $8,200 a year for a family of four, and adults without dependent children remain ineligible regardless of their income. All states previously expanded eligibility for children to higher levels than adults through Medicaid and the Children’s Health Insurance Program (CHIP), and in Florida, children with family incomes up to 215% of poverty (about $50,600 for a family of four) are eligible for Medicaid or CHIP. As was the case before the ACA, undocumented immigrants remain ineligible to enroll in Medicaid, and recent lawfully residing immigrants are subject to certain Medicaid eligibility restrictions.2

Under the ACA, people with incomes between 100% and 400% of poverty may be eligible for premium tax credits when they purchase coverage in a Marketplace, as indicated by the bright blue shading in Figure 1. The amount of the tax credit is based on income and the cost of insurance, and tax credits are only available to people who are not eligible for other coverage, such as Medicaid/CHIP, Medicare, or employer coverage, and who are citizens or lawfully-present immigrants. Citizens and lawfully-present immigrants with incomes above 400% of poverty can purchase unsubsidized coverage through the Marketplace. Because the ACA envisioned low-income people receiving coverage through Medicaid, people below poverty are not eligible for Marketplace subsidies. Thus, some adults in Florida fall into a “coverage gap” of earning too much to qualify for Medicaid but not enough to qualify for premium tax credits, as shown by the orange shading in Figure 1. People in the coverage gap are ineligible for financial assistance under the ACA, while people with higher incomes are eligible for tax credits to purchase coverage.

How Many Uninsured Floridians Are Eligible for Assistance Under the ACA?

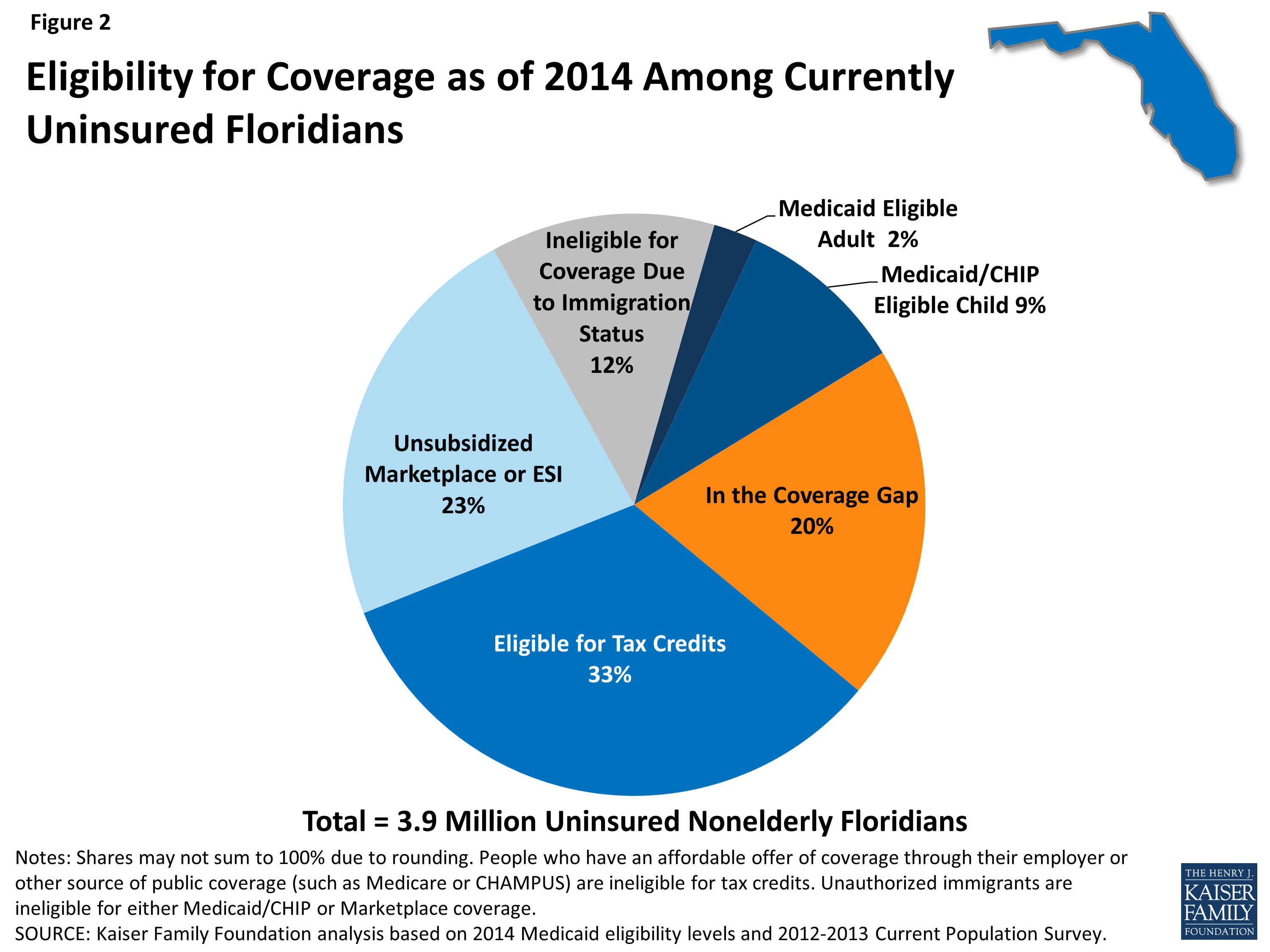

Under the ACA, in Florida, nearly half (44%) of currently uninsured nonelderly people are eligible for financial assistance in gaining coverage (Figure 2). The main pathway for the currently uninsured to gain coverage is the Marketplace, the new coverage option in the state: nearly 1.3 million (a third) uninsured Floridians are eligible for premium tax credits to help them purchase coverage in the Marketplace.

Even though the state is not expanding Medicaid eligibility, some currently uninsured people are eligible for Medicaid in 2014. Reflecting higher eligibility levels for children than for adults, the majority (79%) of uninsured Floridians eligible for Medicaid are children who are already eligible but not yet enrolled in coverage. A small number of uninsured adult parents (2% of the uninsured in the state) are eligible for Medicaid in Florida under eligibility pathways in place before the ACA. Not all eligible individuals are enrolled in the program due to lack of knowledge about their eligibility and historic enrollment barriers. As the ACA coverage expansions are implemented, it is likely that broad outreach efforts and new streamlined enrollment processes will lead to increased enrollment of eligible individuals into Medicaid.

In Florida, 764,000 uninsured adults (20% of the uninsured in the state) who would have been eligible for Medicaid if the state expanded fall into the coverage gap. These adults are all below the poverty line and thus have very limited incomes. Because they do not gain an affordable coverage option under the ACA, they are most likely to remain uninsured.

Two other groups of uninsured Floridians are outside the reach of financial assistance for health coverage under the ACA. First, the 23% of the uninsured with incomes too high to be eligible for premium tax subsidies or who have an affordable offer of coverage through their employer are ineligible for financial assistance. Some of these people are still able to purchase unsubsidized coverage in the Marketplace, which may be more affordable or more comprehensive than coverage they could obtain on their own through the individual market. Second, uninsured undocumented immigrants (about 12% of uninsured Floridians) are ineligible for assistance under the ACA and barred from purchasing coverage through the Marketplace. This group is likely to remain uninsured, though they will still have a need for health care services.

***

The ACA will help many currently uninsured Floridians gain health coverage, but many who could have obtained financial assistance through the Medicaid expansion will remain outside its reach. Further, the impact of the ACA will depend on take-up of coverage among the eligible uninsured, and outreach and enrollment efforts will be an important factor in determining how the law affects the uninsured rate in the state. The ACA includes a requirement that most individuals obtain health coverage, but some people (such as the lowest income or those without an affordable option) are exempt and others may still remain uninsured. Notably, there is no deadline for state decisions about implementing the Medicaid expansion, and open enrollment in the Marketplaces continues through March 2014. Continued attention to who gains coverage as the ACA is fully implemented and who is excluded from its reach—as well as whether and how their health needs are being met—can help inform decisions about the future of health coverage in Florida.

- Some states had expanded coverage to parents at higher income levels or provided coverage to adults without children. See http://modern.kff.org/medicaid/fact-sheet/medicaid-eligibility-for-adults-as-of-january-1-2014/ for more detail on pre- and post-ACA Medicaid eligibility for adults. ↩︎

- For more detail on Medicaid coverage for immigrants, see: http://modern.kff.org/disparities-policy/fact-sheet/key-facts-on-health-coverage-for-low/. ↩︎