This analysis does not reflect recent changes that have been implemented by the Trump administration, including a foreign aid review and restructuring. For more information, see KFF’s Overview of President Trump’s Executive Actions on Global Health.

Key Facts

- Attention to and support for global health security efforts (activities to help countries prepare for and develop capacities to address epidemic and pandemic diseases) – also referred to as pandemic prevention, preparedness, and response – have grown over the past few decades, driven by emerging infectious diseases such as HIV, SARS, influenza, Ebola, Zika, and COVID-19.

- The U.S. government (U.S.) has supported global health security work for more than two decades and is the single largest government donor to such efforts, providing financial support and technical assistance to help build countries’ capacity to prevent, detect, and respond to infectious disease threats. The U.S. also was instrumental in launching the international “Global Health Security Agenda” (GHSA) initiative in 2014 and “The Pandemic Fund” financing mechanism in 2022.

- Historically, U.S. funding for global health security has waxed and waned over time, with spikes in funding driven almost entirely by specific disease events, often through emergency spending measures. For example, while funding for global health security in the years prior to COVID-19 typically ranged between $400 million and $500 million per year, it spiked to $1.34 billion in FY 2015 after the West Africa Ebola outbreak and again to $1.67 billion in FY 2021 after COVID-19, and it remains at higher than historical levels, with FY 2023 funding at $1.49 billion. The President requested $1.9 billion for global health security in FY 2024.

- COVID-19, in particular, increased attention to global health security among U.S. policymakers, with several bills introduced in Congress including one outlining a new U.S. global health security framework that became law in 2022. In addition, the Biden administration has taken several steps to bolster U.S. global health security efforts including reinstating the National Security Council’s Global Health Security and Biodefense Directorate, reversing the prior administration’s decision to withdraw the U.S. from membership in the World Health Organization (WHO), expanding country and regional partnerships, and supporting The Pandemic Fund.

- On September 20, 2023, the United Nations General Assembly, with WHO, will convene a high-level meeting on pandemic prevention, preparedness, and response that will include discussion of a new pandemic accord, which is currently being drafted and negotiated, and proposed amendments to the International Health Regulations, leading up to the World Health Assembly in May 2024.

Background

Global recognition of the threat of epidemic and pandemic diseases has grown over time, and concerns about such outbreaks has fueled efforts to improve local, national, and international capabilities to address emerging diseases. These efforts have been referred to as “global health security” and, more recently, “pandemic prevention, preparedness, and response” activities (see Box 1).

Box 1: Defining Key Terms: Global Health Security & Pandemic Preparedness and Response

Global Health Security (GHS) can be defined as activities supporting epidemic and pandemic preparedness and capabilities at the country and global levels, in order to minimize vulnerability to acute public health events that can endanger the health of populations across geographical regions and international boundaries. This includes efforts to improve countries’ capacity to prevent, detect, and respond to infectious disease threats.1 Over the past few years, the terms Pandemic Prevention, Preparedness and Response (PPPR) and Pandemic Preparedness and Response (PPR) have also been used frequently to refer to these types of activities as well.

This brief uses the term GHS to refer to activities, often supported by donors such as the U.S., that have the goal of building country-, regional-, and global-level capacities for infectious disease prevention, preparedness and response, but does not include research and development for countermeasures (such as diagnostics, drugs, and vaccines), nor support for acute epidemic response in other countries (such as funding for vaccine procurement and distribution during the COVID-19 pandemic or direct support to a country’s response to an Ebola outbreak).

While not every emerging infectious disease has major public health implications, some result in significant epidemics or global pandemics, such as HIV which emerged in the 1980s and marked a major turning point. Since then, multiple other new human infectious diseases have been identified (e.g., SARS, MERS, SARS-CoV-2 (COVID-19)), while other diseases have “re-emerged,” causing greater numbers of cases than before and/or affecting different populations and regions (e.g., dengue fever and Ebola). Still others have developed resistance to available treatment (e.g., multi-drug resistant tuberculosis) or been newly linked to adverse health outcomes (e.g., Zika).

Beyond their toll on health, these diseases can lead to severe societal and economic disruptions, even from smaller scale outbreaks. For example, the original SARS outbreak resulted in an estimated $30 billion in economic losses (over $3 million per case) in 2003, primarily from reduced commerce, travel and trade, while the 2014-2015 West Africa Ebola epidemic in Guinea, Liberia, and Sierra Leone resulted in an estimated $53 billion in economic losses. During a pandemic these effects are amplified even more, as was demonstrated during COVID-19, which the International Monetary Fund has recently called “the largest global economic crisis in more than a century” as national GDP levels fell by a median of 3.9% from 2019 to 2020 across all countries. In the U.S. alone, one estimate from late 2020 put the cost of the pandemic at $16 trillion – a number four times as large as the lost economic output from the ‘Great Recession’ of 2008.

At times, countries have worked together on international efforts and agreements to strengthen global health security and pandemic preparedness and response capacities. For example, in 2005, WHO member states agreed to revise the International Health Regulations (IHR), a long-standing international agreement that outlines roles and responsibilities for countries and international organizations in global health security. The revised IHR, among other things, requires countries to develop minimum capacities to detect, report, assess, and respond to outbreaks and other public health emergencies. In 2014, noting that progress on meeting the IHR requirements had been slow and unequal across regions, a group of governments – with the U.S. playing an instrumental role – and other stakeholders launched the Global Health Security Agenda (GHSA), a multilateral initiative to speed country progress in identifying and addressing gaps in basic global health security capacities (see Box 2). In addition, growing recognition of the importance of global health security to broader economic and social development has been reflected in the inclusion of a global health security objective under the U.N. Sustainable Development Goals (adopted in 2015) as well as by multiple recent endorsements of global health security by the leaders of the G7 and G20.

Despite such efforts, countries remained largely unprepared for outbreaks. According to a WHO review, in 2018 most countries still had “low to moderate” levels of national preparedness for emerging diseases and did not meet IHR core capacity requirements. An independent review of global health security in 2019 found “no country is fully prepared for epidemics or pandemics.” The world’s experience with COVID-19 has put the lack of preparedness and response capacity into stark relief, shining a spotlight on major gaps in financing for strong public health systems, social protection programs, international cooperation, and other aspects of global health security. It also, according to the Independent Panel for Pandemic Preparedness and Response, showed that existing measures of preparedness “failed to account sufficiently for the impact on responses of political leadership, trust in government institutions and country ability to mount fast and adaptable responses.”

Efforts are underway to identify not only the weaknesses exposed by the COVID-19 pandemic but also the steps that could be taken to address them. One proposal has already become a reality with the establishment of a new global funding mechanism known as The Pandemic Fund2 in September 2022, backed by strong U.S. support (see the KFF brief). A number of other proposals have also been put forward in light of COVID-19, including calls for a new “pandemic accord” (with drafting and negotiating underway) and more empowered leadership at national and international levels. Furthermore, discussions have begun on proposed amendments to the IHR. The ultimate impact COVID-19 will have made on re-shaping global health security efforts going forward remains to be determined, as debates and negotiations on these and other topics are likely to continue to play out for months and years to come.

U.S. Government Efforts

The U.S. has supported global health security efforts for over two decades.3 Specific policy guidance for federal agencies dates back to a 1996 Presidential Decision Directive on emerging diseases (PDD/NSTC-7), and each subsequent administration has updated or released new policy and strategic guidance. For example, the importance of U.S. support for global infectious disease surveillance and response capacities was emphasized in the Obama administration’s 2009 National Strategy for Countering Biological Threats and the Trump administration’s 2018 National Biodefense Strategy. The first U.S. Global Health Security Strategy (GHS Strategy), mandated by Congress, was released by the Trump administration in 2019. However, in parallel, the Trump administration made moves to pull back from some global health security engagement, including disbanding the National Security Council (NSC) Directorate on Global Health Security and Biodefense (first established during the Obama administration) and, in mid-2020, initiating the process of withdrawing the U.S. from WHO membership and halting U.S. contributions to WHO.

Starting in January 2021, the Biden administration took immediate steps to reorient and increase U.S. support for the global COVID-19 response and to reinvigorate and revamp U.S. global health security efforts. On his first day in office, President Biden issued an executive order that, among other things, restored the NSC Directorate on Global Health Security and Biodefense and also directed that the NSC Principals Committee coordinate the government’s efforts to address biological threats and pandemics and advise the president on global response to and recovery from COVID-19, including matters related to global health security and WHO. At that time, President Biden issued a national security memorandum on U.S. leadership regarding the global COVID-19 response and global health security, which states that the current administration “will treat epidemic and pandemic preparedness, health security, and global health as top national security priorities” and reversed the Trump administration’s earlier decision to begin withdrawing the U.S. from WHO membership. The administration also released the National Strategy for the COVID-19 Response and Pandemic Preparedness, which states that it is a U.S. goal to “restore U.S. leadership globally, advance health security, and build better preparedness for future threats;” it also affirmed that the U.S. would restore its funding to WHO, which the prior administration had halted, and work to strengthen and reform the agency, including through its role as a member of the WHO Executive Board (see the KFF fact sheet on the U.S. government and WHO and KFF brief on the Biden administration’s global health agenda for more information).

More recently, in October 2022, the administration issued another national security memorandum, directing the National Security Advisor and relevant agencies to recommend, within a year, updated goals and objectives for inclusion in the GHS strategy incorporating lessons from the COVID-19 pandemic, and outlining U.S. support for the global health security architecture internationally. The 2019 GHS strategy – the first national strategy focused specifically on U.S. global health security efforts and developed at the direction of Congress – guided U.S. government activities aimed at “accelerating capacities of targeted countries to prevent, detect, and respond to infectious disease outbreaks protect populations at home and abroad.” Such a strategy is also a requirement of a global health security bill that became law late last year; it also outlined a new framework for these efforts, requires periodic reporting, and allows U.S. contributions to The Pandemic Fund.

Approach

The U.S. approach centers on bilateral financial and technical support for capacity-building programs in certain partner countries as well as multilateral support and cooperation. In FY 2021, the U.S. focused its bilateral efforts in 19 GHSA “partner countries” and supported additional efforts in other countries, reaching more than 40 countries overall and, in some cases, regional efforts.4 U.S. multilateral efforts include playing leading roles in the negotiations for the 2005 revision of the IHR, the development and launch of the GHSA (see Box 2) in 2014, and the launch of The Pandemic Fund in 2022. The U.S. also participates in and supports international responses to outbreaks. For example, it was the largest donor to and supporter of the response to the 2014-2015 West Africa Ebola epidemic, the largest Ebola outbreak in history. It also provided support to the Global Fund to Fight AIDS, Tuberculosis and Malaria and Gavi, the Vaccine Alliance to address COVID-19. As mentioned earlier, in 2021, under the Biden administration the U.S. re-engaged with and restored funding to WHO and stated that it would take steps to strengthen U.S. leadership in the global COVID-19 response and elevate U.S. efforts in support of GHSA.5

Box 2: The Global Health Security Agenda (GHSA)

The U.S. played the leading role in developing the Global Health Security Agenda (GHSA), a multilateral initiative that aims to serve as “a catalyst for progress toward the vision of attaining a world safe and secure from global health threats posed by infectious diseases.” Launched in 2014 for an initial 5-year period (2014-2019), it has been extended for a second five-year period through 2024. Among the strategic objectives of the GHSA are to:

- promote international initiatives, instruments, and frameworks relevant for health security; and

- increase domestic and international partner financial support for strengthening and maintaining capacities to prevent, detect and respond to infectious disease outbreaks, including health system strengthening.

There are 70 member countries of the GHSA, including the U.S. The initiative incorporates several multilateral institutions as partners, such as WHO, the United Nations Food and Agriculture Organization (FAO), the World Organization for Animal Health (OIE), the World Bank, and World Trade Organization (WTO). Private sector and non-governmental partners also engage the initiative through forums such as the Private Sector Roundtable on Global Health Security and GHSA Consortium.

GHSA members have agreed to coordinate efforts and mutually work toward goals in defined areas of global health security, known as “action packages.” To assist in this process, the GHSA helped develop a tool for independent evaluation of countries’ preparedness levels, known as the Joint External Evaluation (JEE); these scores are used as benchmarks for country and global progress in global health security. Over 100 countries, including the U.S., have undergone such an evaluation since 2014.

GHSA and the IHR are meant to be complementary, with GHSA action packages designed to support countries’ progress toward meeting IHR core capacity requirements. While the GHSA and the IHR facilitate cooperative efforts among countries, ultimately country governments are responsible for ensuring capacity to prevent, identify, and respond to emerging diseases within their own borders.

Organization

Multiple U.S. agencies are engaged in global health security efforts. The National Security Council (NSC) is responsible for overall coordination and review of U.S. strategy and activities in global health security, including its international response; its Global Health Security and Biodefense Directorate, which was first established during the Obama administration but disbanded during the Trump administration, has been restored under the Biden administration. The U.S. Agency for International Development (USAID), the Centers for Disease Control and Prevention (CDC), and the Department of Defense (DoD) are the primary agencies involved in implementing global health security programs in partner countries. The Department of State (State), the Department of Health and Human Services (HHS), and the U.S. Department of Agriculture (USDA) also support global health security-related activities.

USAID

The USAID Global Health Bureau’s global health security program helps countries build capacity to identify and respond to dangerous pathogens in animals and humans and to be prepared for outbreaks, including pandemics. Other USAID global health programs support health systems strengthening, including building surveillance and laboratory capacities that have applications for global health security. In addition, the Office of Foreign Disaster Assistance (OFDA) has often been involved when the U.S. engages in large-scale international outbreak responses.

CDC

The CDC Center for Global Health’s Division of Global Health Protection provides capacity-building, training, and educational support to other countries through its Global Disease Detection Operations Center (GDD), Emergency Response and Recovery Branch (ERRB), and Field Epidemiology Training Program (FETP). Other CDC global health programs help build surveillance, laboratory, and other capacities relevant to global health security. CDC has also created a cross-agency rapid response team for international deployment, and CDC staff are often involved in international outbreak response efforts.

DOD

The Department of Defense (DoD) Defense Threat Reduction Agency’s Biological Threat Reduction Program (BTRP), previously known as the Cooperative Biological Engagement Program (CBEP), funds capacity-building efforts to strengthen partner countries’ biosecurity, surveillance, and response capabilities and is a component of the DoD’s broader Cooperative Threat Reduction (CTR) program. The DoD’s Global Emerging Infections Surveillance System (GEIS) provides technical and funding support for DoD and partner organizations’ surveillance, research and development, outbreak response, and local capacity-building and helps support Army and Navy laboratories that are located in multiple foreign countries.

STATE

The Department of State engages in diplomacy and coordination in support of global health security and is home to the Biological Engagement Program (BEP), a biological security assistance and capacity building effort. The Coordinator for Global COVID-19 Response and Health Security, a role created within the department during the Biden administration, is charged with leading the U.S. response to the pandemic overseas and ensuring that U.S. global health security efforts adequately equip partner countries for future global health threats.6 In late 2022, the Secretary of State announced plans to consolidate the department’s efforts in this area under a new Bureau of Global Health Security and Diplomacy, expected to launch in July 2023; it will bring together the functions of several Coordinators and offices, including that of the COVID-19 Response Coordinator as well as PEPFAR’s Office of the U.S. Global AIDS Coordinator and Global Health Diplomacy.

HHS

HHS is the official U.S. point of contact with WHO for IHR purposes and often represents the U.S. at multilateral meetings on emerging disease topics and helps coordinate U.S. global health security efforts. HHS also supports research and development for emerging disease countermeasures (e.g., drugs and vaccines) through the National Institutes of Health (NIH) and the Biodefense Advanced Research and Development Authority (BARDA), while the Food and Drug Administration (FDA) is responsible for regulatory review and approval.

In addition, the USDA, particularly through its Animal and Plant Health Inspection Service (APHIS), supports global capacity building for food safety and animal health surveillance, as well as research on animal diseases overseas.

Funding7

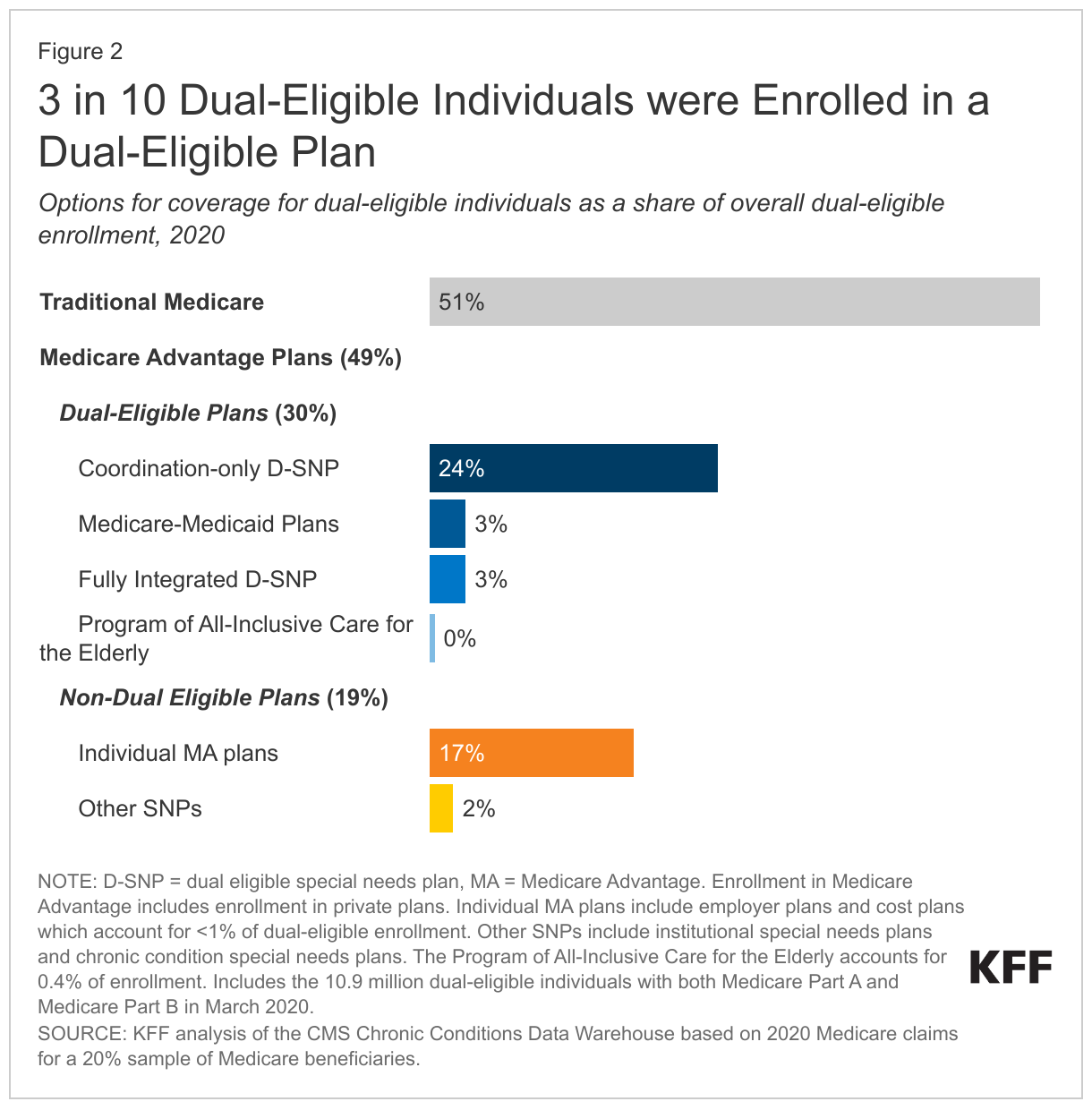

U.S. funding for its main global health security programs has waxed and waned over time, with occasional spikes driven by supplemental funding connected to specific disease events. For example, while funding generally ranged between $400 million and $500 million in the years just prior to the COVID-19 pandemic, it spiked to $1.34 billion in FY 2015, due to an influx of emergency funding provided to address the Ebola outbreak in West Africa and support future preparedness efforts. In the wake of the COVID-19 pandemic, it reached $1.67 billion in FY 2021 (($674 million through regular appropriations and $1 billion through emergency supplemental funding), $1.24 billion in FY 2022, and $1.49 billion in FY 2023 due to increased funding levels (see Figure 1).8 The administration’s FY 2024 budget request includes approximately $1.9 billion: $1.26 billion via USAID/the Department of State, an increase of $360 million compared to FY 2023; $353 million via CDC, an increase of $60 million compared to FY 2023; and an estimated $290 million via DoD, essentially level to FY 2023.9

U.S. funding for global health security is provided primarily through accounts at USAID, CDC, and DoD (also see the KFF budget fact sheet):

- USAID: USAID funding for global health security activities has generally risen each year over the past 10 years, from $55.2 million in FY 2013 to $900 million in FY 2023, with occasional spikes in connection with outbreak events or reprogrammed funding from such events. For example, the agency received $385 million in FY 2015, including $72.5 million through regular appropriations and $312 million through emergency funding in connection with Ebola; $218 million in FY 2016, including $72.5 million through regular appropriations and $145.5 million through emergency funding in connection with Zika; and some reprogrammed unspent FY 2015 Ebola funding in FY 2018 and FY 2019.10 ,11 More recently it has seen a large increase in base and overall funding in the wake of COVID-19, rising from about $441 million in FY 2021 (including about $191 million through regular appropriations and $250 million through emergency funding in connection with COVID-19) to $700 million in FY 2022 to a peak of $900 million in FY 2023. (Also see discussion of U.S. contributions to The Pandemic Fund below).

- CDC: CDC funding for global health security activities has also generally risen over the past 10 years, from $54 million in FY 2013 to $293 million in FY 2023, with occasional spikes. For example, the agency received $652 million ($55 million through regular appropriations and $597 million through emergency funding in connection with Ebola) in FY 2015, which was made available for use through FY 2019. Partly in response to the anticipated decline in program funding upon expiration of this emergency funding, base funding at CDC rose in FY 2020 (from $108 million in FY 2019 to $183 million in FY 2020). Additionally, $750 million in FY 2021 emergency funding for the COVID-19 response was ultimately designated for global health security at CDC, and base funding rose from $203 million in FY 2021 to $293 million in FY 2023.12 ,13

- DoD: BTRP received $235 million in FY 2023, down from a peak of $320 million in FY 2014 – after which it decreased for several years before beginning to increase steadily since FY 2019. GEIS received between about $43 to $60 million each year from FY 2013 through FY 2023.14

In addition to these key accounts, other funds may be used for global health security activities, though public information about them is often limited. For example, DoD provides some funding to support Army and Navy overseas labs, and the Department of State, USDA, and other agencies’ budgets support additional global health security activities.

| U.S. Funding for Global Health Security, FY 2013 – FY 2024 Request(in $ millions) |

| Agency/Program | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 Req |

| TOTAL | 366.2 | 498.5 | 1,341.6 | 552.1 | 364.1 | 512.3 | 503.5 | 537.8 | 1674.5 | 1241.0 | 1486.9 | 1900.3 |

| USAID Global Health Security^ | 55.2 | 72.6 | 384.5 | 218.0 | 72.5 | 172.6 | 138.0 | 100.0 | 440.8 | 700.0 | 900.0 | 760.3 |

| Global Health Programs | 55.2 | 72.5 | 72.5 | 72.5 | 72.5 | 72.6 | 100.0 | 100.0 | 190.8 | 700.0 | 900.0 | 745.0 |

| Of which, Pandemic Fund | | | | | | | | | | Of which, 200.0 | Of which, 250.0# | |

| Economic Support Fund | 0.1 | — | — | — | — | — | — | — | — | — | — | 13.3 |

| AEECA | — | — | — | — | — | — | — | — | 0.8 | — | — | 2.0 |

| Emergency Ebola | — | — | 312.0 | — | — | 100.0 | 38.0 | — | — | — | — | — |

| Emergency Zika | — | — | — | 145.5 | — | — | — | — | — | — | — | — |

| Emergency COVID-19 | — | — | — | — | — | — | — | — | 250.0 | — | — | — |

| Of which, Pandemic Fund | | | | | | | | | Of which, 250.0 | | | |

| State Global Health Security | — | — | — | — | — | — | — | — | — | — | — | 500.0 |

| Global Health Programs | — | — | — | — | — | — | — | — | — | — | — | 500.0 |

| Of which, Pandemic Fund | | | | | | | | | | | | Of which, 500.0 |

| CDC Global Health Protection^ | 54.3 | 62.6 | 652.1 | 55.2 | 58.2 | 108.2 | 108.2 | 183.2 | 953.2 | 253.2 | 293.2 | 353.2 |

| Global Public Health Protection | 54.3 | 62.6 | 55.1 | 55.2 | 58.2 | 108.2 | 108.2 | 183.2 | 203.2 | 253.2 | 293.2 | 353.2 |

| Emergency Ebola | — | — | 597.0 | — | — | — | — | — | — | — | — | — |

| Emergency COVID-19 | — | — | — | — | — | — | — | — | 750.0 | — | — | — |

| DoD | 256.6 | 363.4 | 305.0 | 278.9 | 233.4 | 231.5 | 257.3 | 254.6 | 280.5 | 287.8 | 293.7 | 286.8 |

| BTRP | 211.0 | 320.0 | 256.8 | 222.0 | 175.7 | 172.8 | 197.6 | 203.6 | 225.4 | 229.0 | 235.0 | 228.0 |

| GEIS | 45.6 | 43.4 | 48.2 | 56.9 | 57.7 | 58.7 | 59.8 | 50.9 | 55.2 | 58.7 | 58.7* | 58.7* |

| NOTES: Totals include base and supplemental funding. — means $0/not applicable. Totals may not sum due to rounding. FY13 includes the effects of sequestration. BTRP is the Biological Threat Reduction Program, formerly known as the Cooperative Biological Engagement Program (CBEP). GEIS is the Global Emerging Infections Surveillance system.^ In FY15, Congress provided $5.4 billion in emergency funding to address the Ebola outbreak, of which $909.0 million was specifically designated for global health security at USAID and CDC. In FY16, Congress provided $1.1 billion in emergency funding to address the Zika outbreak, of which $145.5 million was specifically designated for global health security at USAID. In FY18, Congress provided $100 million in unspent Emergency Ebola response funding for “programs to accelerate the capabilities of targeted countries to prevent, detect, and respond to infectious disease outbreaks” at USAID. In FY19, Congress provided $38 million in unspent Emergency Ebola response funding for “programs to accelerate the capacities of targeted countries to prevent, detect, and respond to infectious disease outbreaks” at USAID. In FY20 and FY 21, Congress provided emergency COVID-19 funding to address the COVID-19 pandemic globally.# For FY23, $250 million is planned, pending congressional approval, for such a contribution. * GEIS funding for FY23 and FY24 request assumes level funding based on FY22 level.SOURCES: KFF analysis of data from the Office of Management and Budget, Agency Congressional Budget Justifications, Congressional Appropriations Bills, U.S. Foreign Assistance Dashboard [website], available at: http://www.foreignassistance.gov, GEIS and AFHSC/AFHSB annual reports, and personal communication with DoD and CDC. See also KFF, Global Funding Across U.S. COVID-19 Supplemental Funding Bills. |

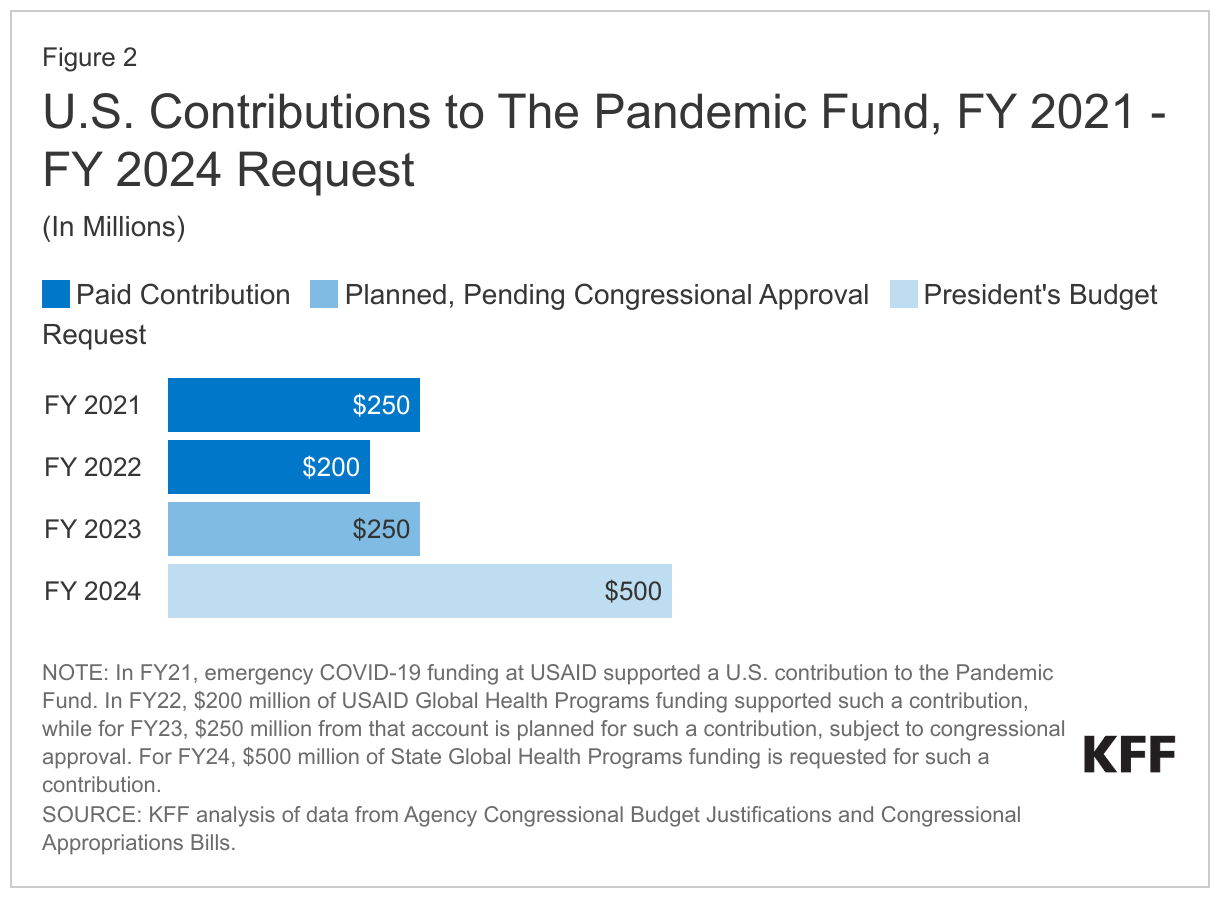

U.S. Contributions to The Pandemic Fund

U.S. global health security funding also includes U.S. contributions to the recently created “The Pandemic Fund” as follows: $250 million in FY 2021 from COVID-19 emergency funding at USAID, $200 million for FY 2022 from the global health programs (GHP) account at USAID, $250 million (planned, subject to congressional approval) for FY 2023 from GHP at USAID, and $500 million requested for FY 2024 from the Department of State. See Figure 2.

Key Issues for the U.S.

While the U.S. has supported global health security activities for decades and remains the single largest contributor to international capacity building, U.S. attention to and funding for global health security have waxed and waned over time. In addition, despite efforts by the U.S. and others, global preparedness for epidemics and pandemics remains weak, as evidenced by the degree to which countries, including the U.S., and global response systems exhibited significant vulnerabilities to COVID-19 over the past several years. This has led to an intensified U.S. and global focus on the importance of global health security and new efforts to bolster preparedness, though the extent to which these will have lasting impact remains to be seen. Among key issues to watch include:

- the funding levels the Biden administration proposes for global health security efforts (including an additional $500 million requested for FY 2024 for U.S. support to The Pandemic Fund) and the amounts ultimately appropriated for these efforts by Congress and whether more consistent and sustained funding is made available instead of the episodic funding patterns of the past;

- the implementation of the new global health security law as well as congressional oversight of this process and how the adoption of the law’s requirements affects the organization, coordination, leadership, strategy, and reporting of U.S. efforts;

- the impact of other changes in the U.S. approach to and organization of its global health security efforts including the launch of the new Bureau of Global Health Security and Diplomacy at the Department of State;

- the extent of U.S. engagement with partners and multilateral organizations, including WHO, on global health security through various avenues, such as GHSA, the World Health Assembly and the WHO Executive Board and specifically related to negotiations on a new pandemic accord and proposed amendments to the IHR; and

- the implications of a greater focus on U.S. global health security for the “unfinished business” of global health, including core U.S. programs such as PEPFAR and PMI, and whether U.S. global health security efforts are able to effectively coordinate with other program areas to better leverage their efforts to collectively strengthen health system resilience to future shocks such as pandemics.