States are facing constrained budgets, putting pressure on HIV care and prevention programs, including the Ryan White HIV/AIDS Program. Ryan White, the nation’s HIV safety-net, is funded each year through discretionary federal appropriations, state dollars, and other sources. However, funding does not necessarily match the number of people who need support or the cost of services.

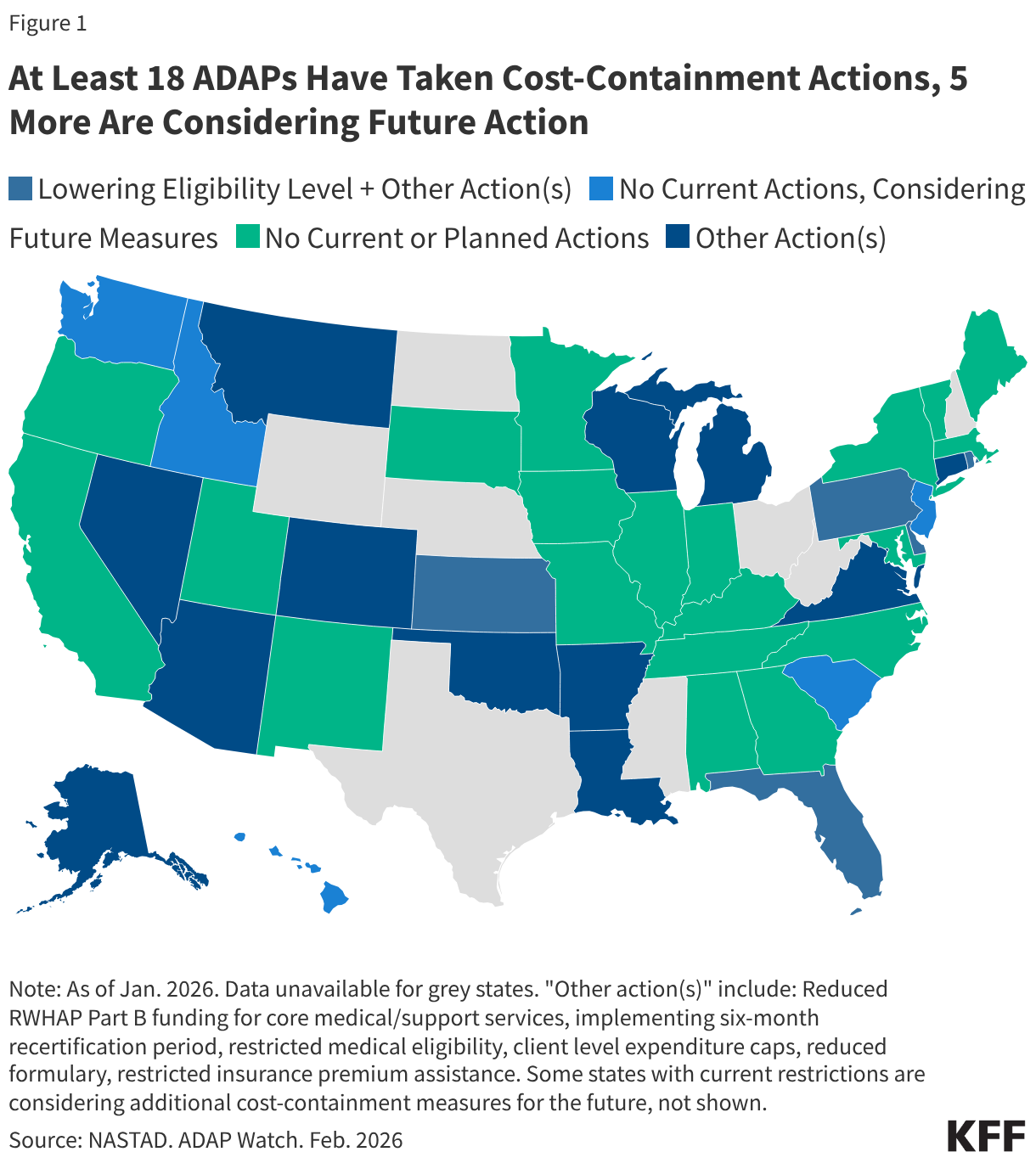

The largest component of Ryan White provides grants to states, including for their AIDS Drug Assistance Programs (ADAPs), which provide HIV treatment and insurance assistance for people with HIV. In the past, ADAPs have used waiting lists and other cost-containment measures when programs could not meet the needs of all those eligible, and in the early 2000s, waiting lists were common. Significant waiting lists were last cleared with an influx of emergency federal funding in 2013 and then were used occasionally for a few years. They have not been used for over a decade and, to date, have not returned. However, several states facing budget pressures have recently moved to institute other cost-containment measures, including restricting eligibility and scope of services, and some are considering waiting lists for the future. This represents the first time such broad cost-containment measures have been taken since the waitlist era.

Ultimately, such changes could result in people with HIV losing access to care and treatment, which could worsen health outcomes (increasing morbidity and mortality) and leading to new HIV infections (four in ten new HIV transmissions are associated with someone who is aware of their HIV status but not in care).

State ADAPs Respond to Strain by Limiting Enrollment and Services Offered

Florida recently announced changes to its ADAP, which would dramatically limit eligibility and scope of assistance. Specifically, the state plans to reduce income1 eligibility for the program from 400% of the federal poverty level (FPL) to 130% FPL (for an individual, which is the equivalent of eligibility decreasing from a maximum income of $63,840 to $20,748 annually).

Additionally, the state plans to remove Biktarvy from its formulary. Biktarvy is the most widely prescribed antiretroviral (ARV) medication nationally (accounting for 52% of the U.S. ARV market) and the only single tablet regimen (STR) included among the national HIV treatment guidelines list of recommended initial treatment regimens. Some studies have shown that STRs improve adherence by reducing pill burden.

The state also plans to roll back its insurance assistance program. ADAPs can help cover insurance costs in addition to directly purchasing medications. Ending insurance assistance poses unique challenges, as insurance coverage allows individuals to meet both HIV-related and other health care needs and helps protect clients in the face of unexpected medical costs (e.g. through out-of-pocket maximums).2 With expiration of enhanced Affordable Care Act premium tax credits, out-of-pocket premiums for people in ACA plans are increasing substantially this year.

The changes in Florida have received significant push back from advocates, patients, and providers, and the state was sued for proceeding with these changes without formal rule making. (The state then issued a proposed rule which it followed with emergency rulemaking. Litigation continues seeking to block implementation).

Florida, however, is not alone. New data from the National Association of State and Territorial AIDS Directors (NASTAD) indicate that 23 states (including Washinton, D.C.) have implemented or are considering ADAP cost-containment measures.3 Eighteen (18) ADAPs, including Florida‘s, have already made or are making changes and five additional states report that they are considering introducing such measures in the future. Further, 12 of the 18 states already implementing cost-containment measures are considering additional changes for the future.

For example, in addition to Florida, Pennsylvania, Kansas, Delaware, and Rhode Island have also reduced income eligibility for their programs (though to a lesser degree). Other changes states are exploring or implementing include reducing formularies (though, so far, none as consequential as removing Biktarvy), reducing funding for medical and support services, making recertification more stringent (which can create churn and lead to program disenrollment), implementing annual client spending caps, and restricting or ending health insurance assistance.

To date, no state has implemented a waiting list, a measure widely seen as a last resort. However, Arkansas, Louisiana, and New Jersey report considering implementing one as a future cost-containment measure.

Multiple Factors Are Exerting Budget Pressures on ADAP

There are a range of factors affecting ADAP budgets. These include, but are not limited to, the following:

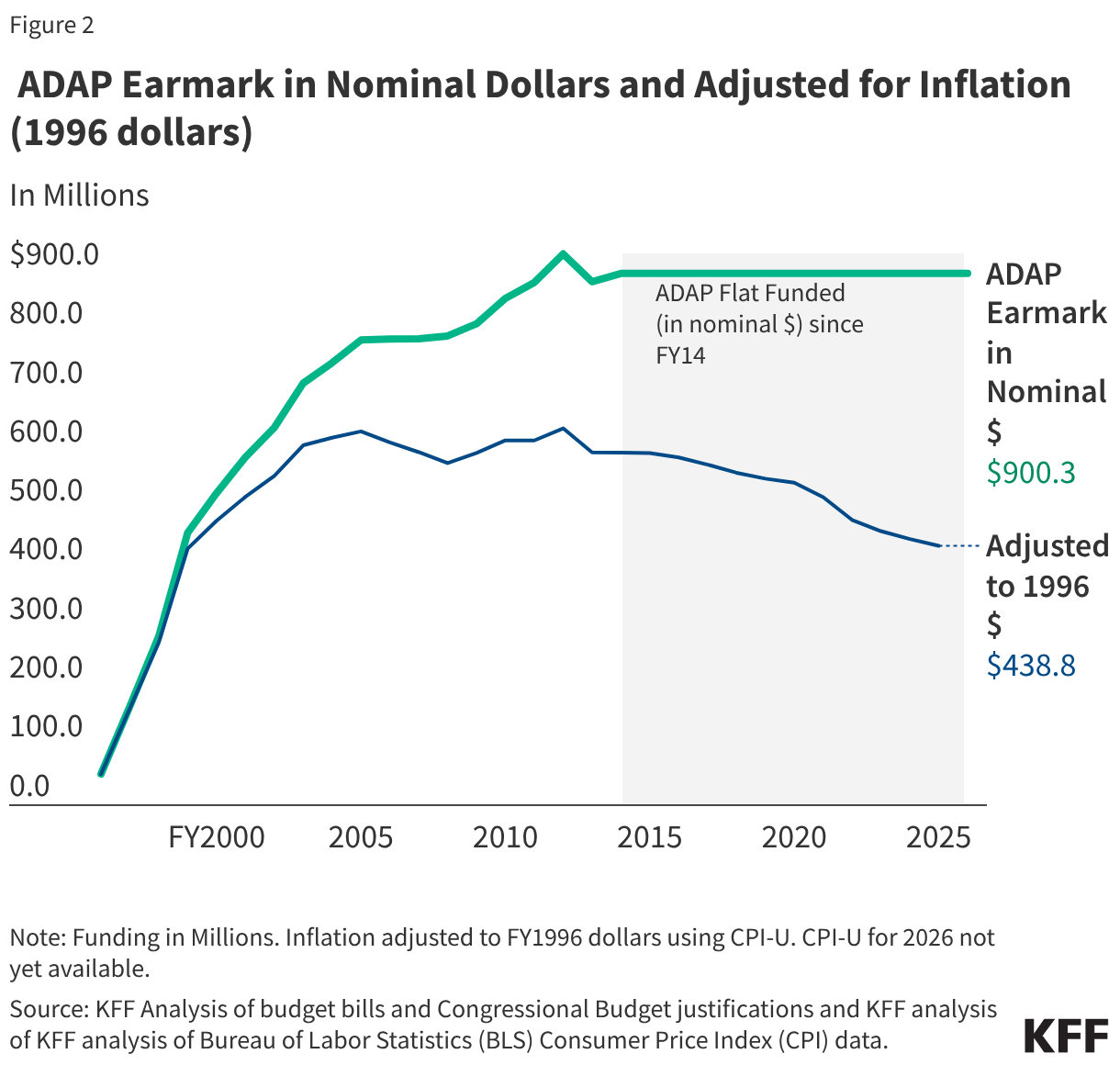

Federal ADAP Funding Not Keeping Pace With Inflation

Since 1996, Congress has allocated (or “earmarked”) a set amount of funding for ADAPs during the annual appropriations process. After modest funding levels in the late 1990s, followed by significant growth in the early 2000s, ADAP inflation-adjusted appropriations have declined by 31% since 2005.4 The decline is largely attributable to more than a decade of flat funding in nominal dollars. When adjusted to 1996 dollars, the FY25 appropriation ($438.8 million) has similar purchasing power as the program’s FY1999 funding level ($434.0 million).5 In other words, in the last 20 years, ADAP funding has not kept pace with inflation, even before accounting for enrollment growth and increased costs (discussed below).

In the NASTAD report ADAPs identified growing client enrollment, growing drug costs, and rising insurance costs as the top three drivers of budget concerns. These concerns are explored further below:

Increased Client Enrollment

While modern era federal ADAP funding has not kept pace with inflation, the number of ADAP clients served has increased significantly. The number of clients served increased by 56% from 2007 (the first year with available data for the full year) to 2024 (the most recent year with available data), rising from 165,3826 to 257,644 clients served. Adjusted for inflation, appropriations per client served dropped from about $3,600 in 2007 to approximately $1,700 in 2024. Additionally, the national HIV treatment guidelines have evolved to recommend HIV treatment at the time of diagnosis -as opposed to starting at signs of disease progression- which has led to more people with HIV having an indication for treatment.

Rising HIV Drug Costs

Another factor impeding the reach of ADAP dollars is the increasing cost of drugs for HIV treatment. A recent analysis found that the average wholesale price (AWP) of recommended initial antiretroviral regimes in 2012 ranged from an AWP of $24,970 to $35,160, increasing to $36,080 to $48,000 in 2018. Costs have generally increased since then. Data in the treatment guidelines show that the AWP for Biktarvy (again the number one treatment regimen for people with HIV and only STR recommended by the treatment guidelines start list) was $61,000 in 2025. The 2025 AWP for other recommended (two-pill) regimens ranged from $34,320 to $65,196. While ADAPs do not pay the full AWP because they have access to price discounts through the 340B drug pricing program and supplemental manufacturer rebates, increasing drug prices may still affect them; it is a main concern cited by ADAPs regarding cost challenges. Additionally, ADAPs ability to generate rebates (which make up a growing share of their budgets) through Medicare have diminished due to programmatic changes, including adoption of the out-of-pocket cap in Part D – by introducing the cap, ADAPs and other 340B entities, have less opportunity to generate rebates on claims because they make fewer cost-sharing payments.

Increased Insurance Premium Costs and Expiration of Enhanced Tax Credits

As mentioned above, ADAPs can also purchase health insurance for eligible clients. However, the cost of individual market coverage is on the rise, with the expiration of the enhanced premium tax credits being a particular driver and premium increases also playing a role.

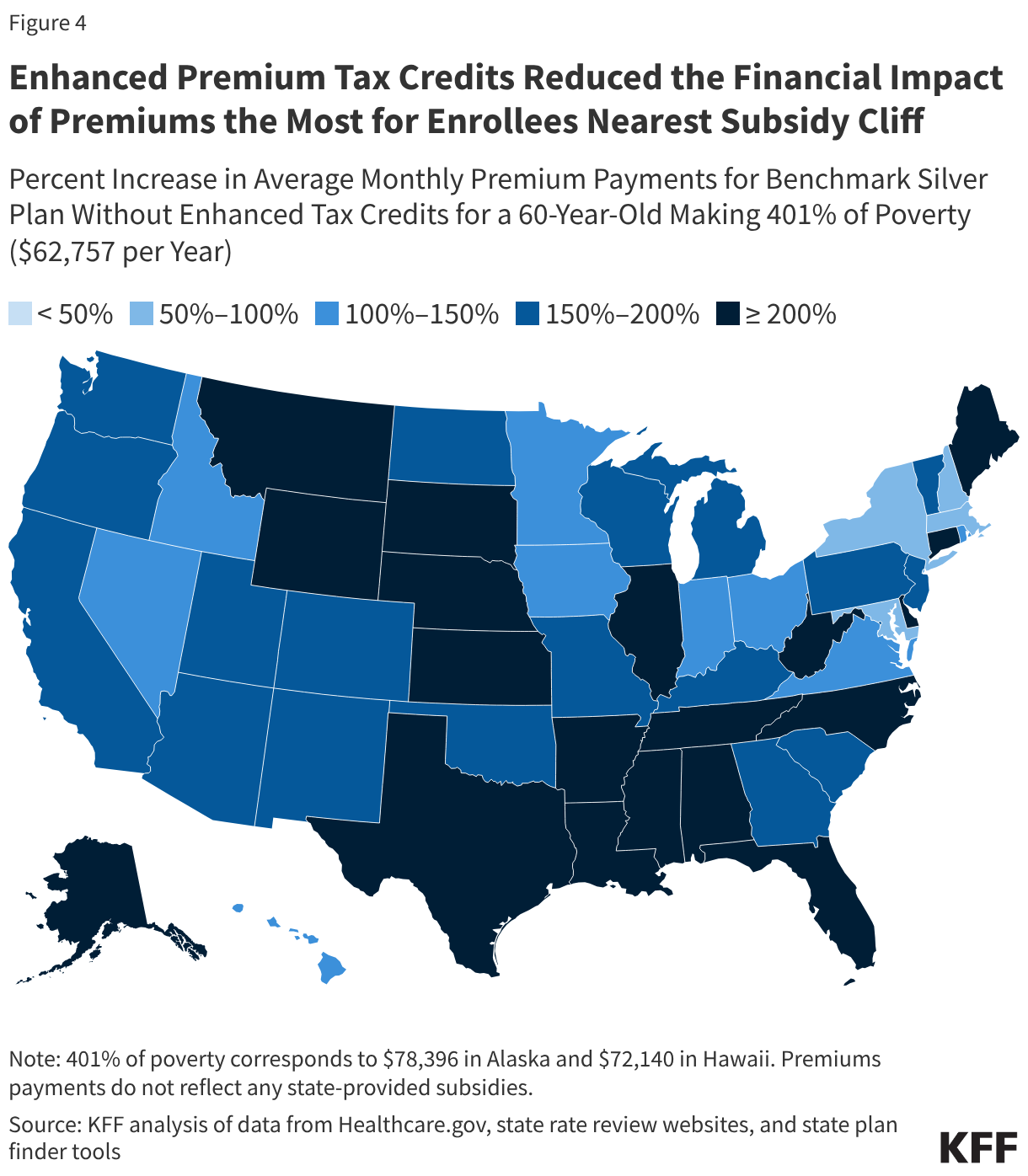

ACA premium tax credits help make marketplace plans more affordable for people with low to moderate incomes. They were first enhanced as part of the American Rescue Plan Act in 2021 and extended by Congress through 2025, but have since expired due to the lack of a bipartisan Congressional agreement to continue them. The enhanced tax credits had improved insurance affordability for ADAPs purchasing coverage on behalf of clients, including for those previously eligible for the less generous ACA subsidies and, newly, for those with incomes over 400% FPL, a group for whom premium costs were limited to 8.5% of income. Without the enhanced credit those 100-400% FPL revert to the original, less generous, ACA tax credits and those over 400% FPL have lost financial assistance altogether. For enrollees keeping the same plan, expiration of the enhanced premium tax credits is estimated to more than double what subsidized enrollees previously paid annually for premiums—a 114% increase from an average of $888 in 2025 to $1,904 in 2026.

Additionally, after holding relatively steady since 2020, premiums increased steeply between 2025 and 2026, with the average premium cost for benchmark plans increasing by 26%7, with significant variation across states. Some southern states with high HIV prevalence saw especially large average increases (e.g. 33% in Florida and 35% in Texas). These premium increases occurred for a range of reasons including, but not limited to, higher health care costs, use of expensive GLP-1 drugs, the threat of tariffs, and the expiration of the enhanced premium tax credits. While the vast-majority of ADAP clients have modest incomes, these costs will be borne out most acutely for the 7% of clients served by insurance purchasing who have incomes over 400% FPL, a group who lost the enhanced tax credits that previously capped premium costs as a share of their income. ADAPs covering individuals in this higher income group face a two-fold setback – loss of enhanced tax credits and no protections against rising premiums.

Additionally, individuals who lose ADAP insurance coverage due to cost-containment measures may find financing coverage independently more challenging due to reduced tax credit generosity and increases in premiums.

Looking Ahead

While ADAPs have sought to leverage additional state funds, drug rebates, and capture limited emergency and supplemental funding, these efforts have not remedied budget shortfalls, leading many to institute cost-containment measures. ADAPs may increasingly face budget pressures that could lead to additional such measures in the future. This could leave growing numbers of people with HIV ineligible for safety-net services, particularly if states further lower income eligibility limits or institute waiting lists. The expiration of enhanced tax credits amplifies these challenges, both increasing costs for programs and leaving those who are ineligible for ADAPs with fewer affordable alternatives. Limiting access to Ryan White services will in turn affect the ability of people with HIV to stay engaged in HIV treatment, a cornerstone of national efforts to address the HIV epidemic.

Endnotes