2026 Medical Loss Ratio Rebates

The Medical Loss Ratio (MLR) provision of the Affordable Care Act (ACA) limits the share of premium income that insurers can keep for administration, marketing, and profits. Insurers that fail to meet the applicable MLR threshold are required to pay back excess profits or margins in the form of rebates to individuals and employers that purchased coverage.

In the individual and small group markets, insurers must spend at least 80% of their premium income on health care claims and quality improvement efforts, leaving the remaining 20% for administration, marketing expenses, and profit. The MLR threshold is higher for large group insurers, which must spend at least 85% of their premium income on health care claims and quality improvement efforts. MLR rebates are based on a three-year average, meaning that rebates issued in 2026 will be calculated using insurers’ financial data in 2023, 2024 and 2025 and will go to people and businesses who bought health coverage in 2025.

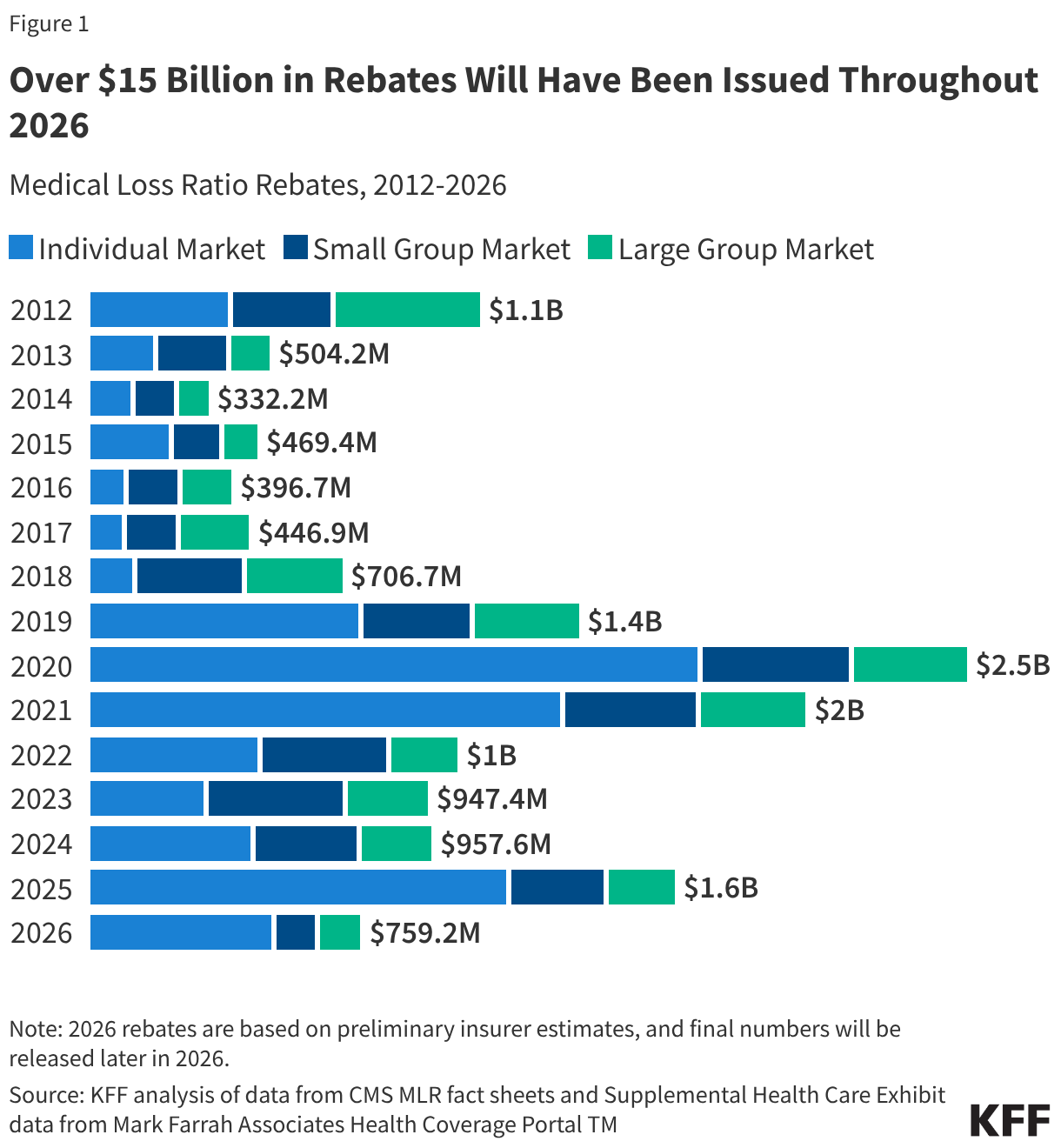

This analysis, using preliminary data reported by insurers to state regulators and compiled by Mark Farrah Associates, finds that insurers estimate they will issue a total of just over $759 million in MLR rebates across all commercial markets in 2026. Since the ACA began requiring insurers to issue these rebates in 2012, a total of $14.4 billion in rebates has already been issued to individuals and employers, and this analysis suggests the 2012-2026 total will rise to about $15.1 billion when rebates are issued later this year.

Estimated total rebates across all commercial markets in 2026 ($759 million) are less than total rebates issued in 2024 ($958 million) and in 2025 ($1.6 billion). In 2025, rebates were issued to 5.1 million people with individual coverage and 3.5 million people with employer coverage. In the individual market, the 2025 average rebate per person was $233, while the average rebates per person for the small group market and the large group market were $190 and $91, respectively (though enrollees could receive only a portion of this as rebates may be shared between the employer and employee or be used to offset premiums for the following year).

The estimated $759 million in rebates falls far short of record-high rebate totals of $2.5 billion issued in 2020 and $2.1 billion issued in 2021, driven largely by high margins in the 2018 ACA Marketplace following steep premium increases in response to the elimination of cost-sharing reduction payments, inflating the three-year average on which rebate calculations are based, as well as lower than expected utilization in 2020 due to the pandemic. In the years following 2018, insurers largely held premiums flat or reduced them as claims cost rose and caught up to premium levels, compressing margins and bringing rebate totals down significantly from those peaks. The current rebate environment reflects this period of margin normalization rather than continued insurer profitability stemming from the earlier CSR-related premium increases.

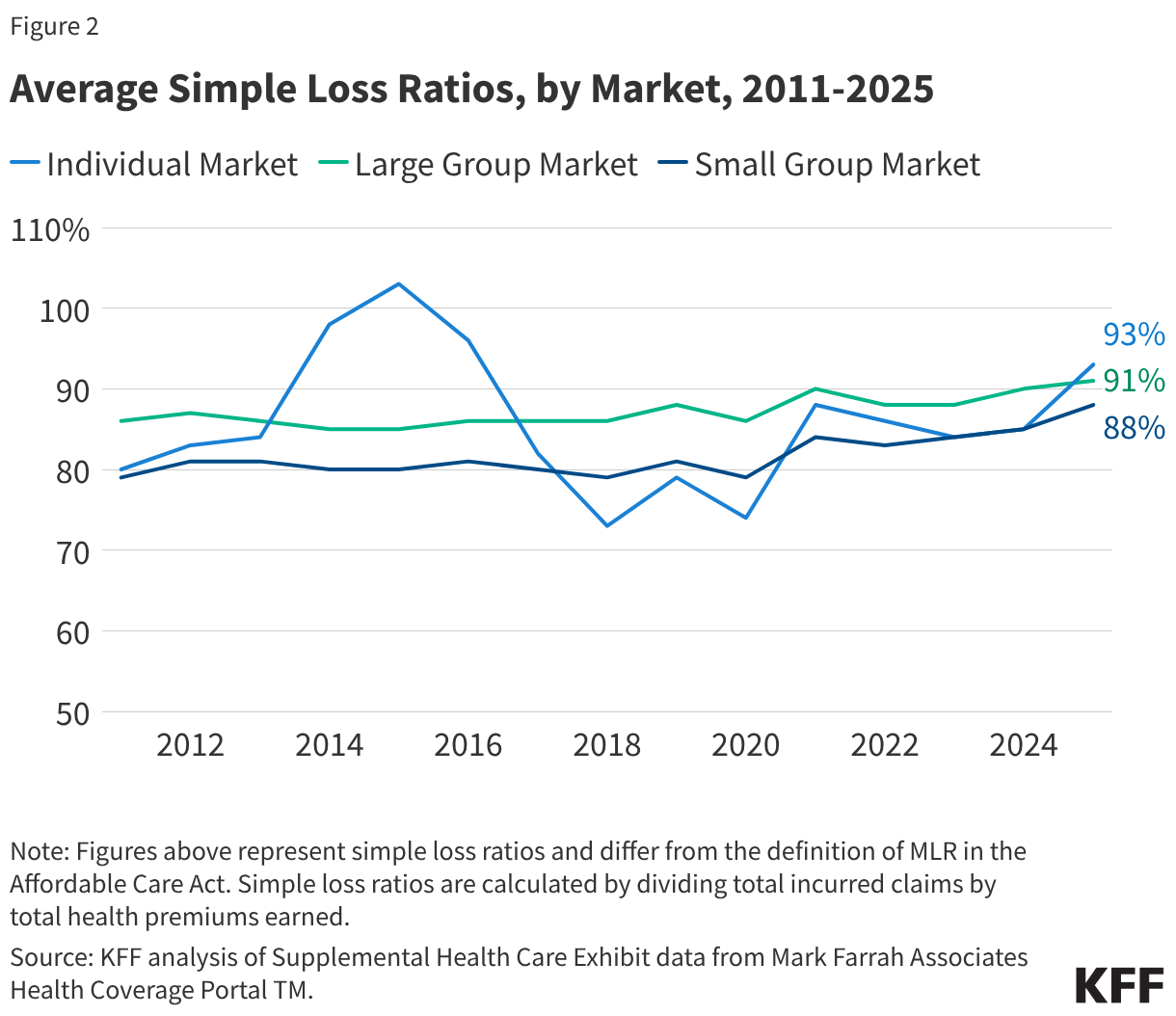

The chart above shows the average “simple loss ratio” in each market. Simple loss ratios differ from the ACA MLR used to calculate rebates because simple loss ratios do not include adjustments for quality improvement expenses or taxes. In 2025, the average simple loss ratio in the individual market was 93%, meaning these insurers spent an average of 93% of their premium income in the form of health claims in 2025. This is significantly higher than the previous year, suggesting that insurers were less profitable. However, rebates issued in 2026 are based not only on 2025 experience, but rather on a three-year average of insurers’ experience in 2023-2025. Consequently, even insurers with high loss ratios in 2025 may expect to owe rebates if they were highly profitable in the prior two years.

Going into 2026, ACA Marketplace premiums increased at the steepest rate (over 20%) since 2018, the last time policy uncertainty fueled premium increases. If it turns out insurers overpriced premiums compared to how much enrollees spend on claims in 2026 and fall short of MLR ratio targets, insurers would likely have to pay their enrollees rebates in the future.

In the small and large group markets, 2025 average simple loss ratios were 87% and 91%, respectively. Only fully-insured group plans are subject to the ACA MLR rule; about two-thirds of people with insurance through their work are in self-funded plans, to which the MLR threshold does not apply.

Rebate Payment Logistics

The 2026 rebate amounts in this analysis are still preliminary. Rebates or rebate notices are mailed out by the end of September and the federal government will post a summary of the total amount owed by each issuer in each state later in the year.

Insurers in the individual market may either issue rebates in the form of a check or premium credit. For people with employer coverage, the rebate may be shared between the employer and the employee depending on the way in which the employer and employee share premium costs.

If the amount of the rebate is exceptionally small (less than $5 for individual rebates and less than $20 for group rebates), insurers are not required to process the rebate, as it may not warrant the administrative burden required to do so.

Methods

This analysis is based on insurer-reported financial data from Health Coverage Portal TM, a market database maintained by Mark Farrah Associates, which includes information from the National Association of Insurance Commissioners. The Supplemental Health Care Exhibit dataset analyzed in this report does not include data from California HMOs regulated by California’s Department of Managed Health Care. Individual, Small, and Large Group Comprehensive plans were used for this analysis. All individual market figures in this analysis are for major medical insurance plans sold both on and off exchange. Health premiums earned and total incurred claims were set as zero if reported as a negative value. Simple loss ratios are calculated as the ratio of the sum of total incurred claims to the sum of health premiums earned. Only plans with an estimated unpaid current rebate value greater than zero were used to calculate the estimated total 2026 rebates.

Rebates for 2026 are based on preliminary estimates from insurers. In some years, final rebates are higher than expected and in other years, final rebates are lower.