KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Use of telehealth, which allows patients to see health care providers without being in the same location, has grown rapidly in recent years, among both privately-insured patients and Medicare beneficiaries. Prior to the COVID-19 pandemic, telehealth utilization in traditional Medicare was very low, but it rose dramatically in 2020 following temporary measures put in place at the start of the COVID-19 public health emergency that greatly expanded the scope of Medicare coverage of telehealth. Since early 2021 telehealth use has declined steadily, but it remains higher than pre-pandemic levels, with considerable variation by income level, race and ethnicity, and urban versus rural location, among other factors.

Congress has extended a number of pandemic-era flexibilities around Medicare coverage of telehealth beyond the COVID-19 public health emergency, which ended on May 11, 2023, but most of these flexibilities are due to expire in December 2024. There is bipartisan support for proposedlegislation to extend these provisions for another two years, and Congress is weighing the potential benefits, risks, and costs of permanently expanding Medicare coverage of telehealth services. Medicare beneficiaries are generally satisfied with their telehealth visits, and many health care providers are supportive of keeping these services accessible, but questions remain about the longer-term impact on patient care, Medicare spending, and program integrity.

These FAQs provide answers to key questions about the current scope of Medicare telehealth coverage, including both temporary and permanent changes adopted through legislation and regulation, and policy considerations that lie ahead.

What is the current scope of Medicare telehealth coverage and how did it change at the start of the COVID-19 pandemic?

Prior to the declaration of the COVID-19 public health emergency, Medicare coverage of telehealth was largely restricted to beneficiaries in rural areas and to certain types of providers, facilities, and services. At the time, beneficiaries were typically required to travel from their homes to approved clinical sites where they could receive care from providers at other locations. To make it easier and safer for beneficiaries to seek medical care during the pandemic, the Secretary of the Department of Health and Human Services (HHS) waived many of these restrictions in March 2020, enabling broader use of telehealth services for all Medicare beneficiaries. While the pandemic-related expansion of telehealth coverage under Medicare was initially due to expire at the end of the COVID-19 public health emergency, subsequent legislation extended many of these flexibilities through December 2024 and incorporated others into the program on a permanent basis (Figure 1).

The following list summarizes key provisions of current law related to coverage of telehealth in traditional Medicare, both temporary and permanent. (See section below for a discussion of telehealth coverage by Medicare Advantage plans.)

Temporary telehealth provisions (currently due to expire after December 31, 2024)

Waiver of geographic and “originating site” requirements: Telehealth is currently available to Medicare beneficiaries in both urban and rural areas, and patients can receive telehealth services from any location, including their home as the “originating site.” Prior to the expansion, telehealth coverage in traditional Medicare was limited to rural areas (with certain exceptions), and patients were required to travel to an approved originating site, such as a clinic or doctor’s office, when receiving telehealth services. (Providers participating in select accountable care organizations (ACOs) are permitted to waive these requirements under the Bipartisan Budget Act of 2018, and may continue to provide telehealth services without geographic restrictions, and to beneficiaries in their homes, should the current flexibilities expire.)

Expansion of covered telehealth services: Medicare currently offers coverage for an expanded set of telehealth services, including physical and occupational therapy, emergency department visits, and nursing facility care. Prior to the expansion, Medicare offered coverage for a more limited set of telehealth services, such as preventive health screenings, office visits, and psychotherapy. The Centers for Medicare & Medicaid Services (CMS) has the authority to expand the list of allowable telehealth services when there is a demonstrable clinical benefit and continues to evaluate select services for permanent inclusion on this list.

Coverage of audio-only services: Medicare currently allows a limited set of telehealth services to be provided to patients via audio-only platforms, such as a telephone or a smartphone without video. Prior to the expansion, Medicare required all telehealth services to be provided via a two-way audio/video connection, such as an interactive audio-video system or a smartphone with video enabled.

Expansion of eligible “distant site” telehealth providers: Currently, any health care provider who is eligible to bill for Medicare-covered services can provide and bill for telehealth as a “distant site” telehealth provider and may conduct an initial telehealth visit whether or not they have treated the beneficiary previously. Additionally, federally qualified health centers (FQHCs) and rural health clinics (RHCs) are now authorized to provide and bill for telehealth. Prior to the expansion, only physicians and certain other providers (e.g., physician assistants, clinical social workers, and clinical psychologists) were permitted to bill for telehealth services as the distant site provider and must have treated the beneficiary receiving those services within the last three years. FQHCs and RHCs were not authorized to serve as distant site providers but could serve as originating sites if located in a qualifying area.

Waiver of in-person visit requirement for behavioral health: Currently, Medicare beneficiaries receiving behavioral health services may opt to receive these services via telehealth with no in-person visit requirements. The Consolidated Appropriations Act of 2021 made numerous changes to Medicare coverage of behavioral telehealth (see below), including a provision that beneficiaries must have an in-person visit with their behavioral health provider no more than six months before their initial telehealth appointment and annually thereafter. Subsequent legislation delayed this requirement until January 2025.

Use of telehealth for hospice recertification: Patient recertification for the Medicare hospice benefit can currently be conducted via telehealth, provided there is a two-way audio/video connection that allows for real-time interaction between the patient and hospice provider. Prior to the expansion, only in-person encounters could be used for the purposes of hospice recertification.

Permanent telehealth provisions

Behavioral health: The Consolidated Appropriations Act of 2021 permanently removed geographic and originating site restrictions for any telehealth service used to diagnose, evaluate, or treat a mental health disorder. (These restrictions had already been lifted for treatment of substance use disorders and co-occurring mental health disorders in 2018). While many other provisions related to telehealth coverage expire at the end of 2024, Medicare beneficiaries may continue to receive behavioral health services from their homes, in both urban and rural areas, and may do so via audio-only platforms if they are unable to access a video connection or do not consent to video use. Additionally, FQHCs and RHCs are permanently allowed to serve as telehealth providers for behavioral health services.

What trends have emerged in Medicare beneficiaries’ use of telehealth services?

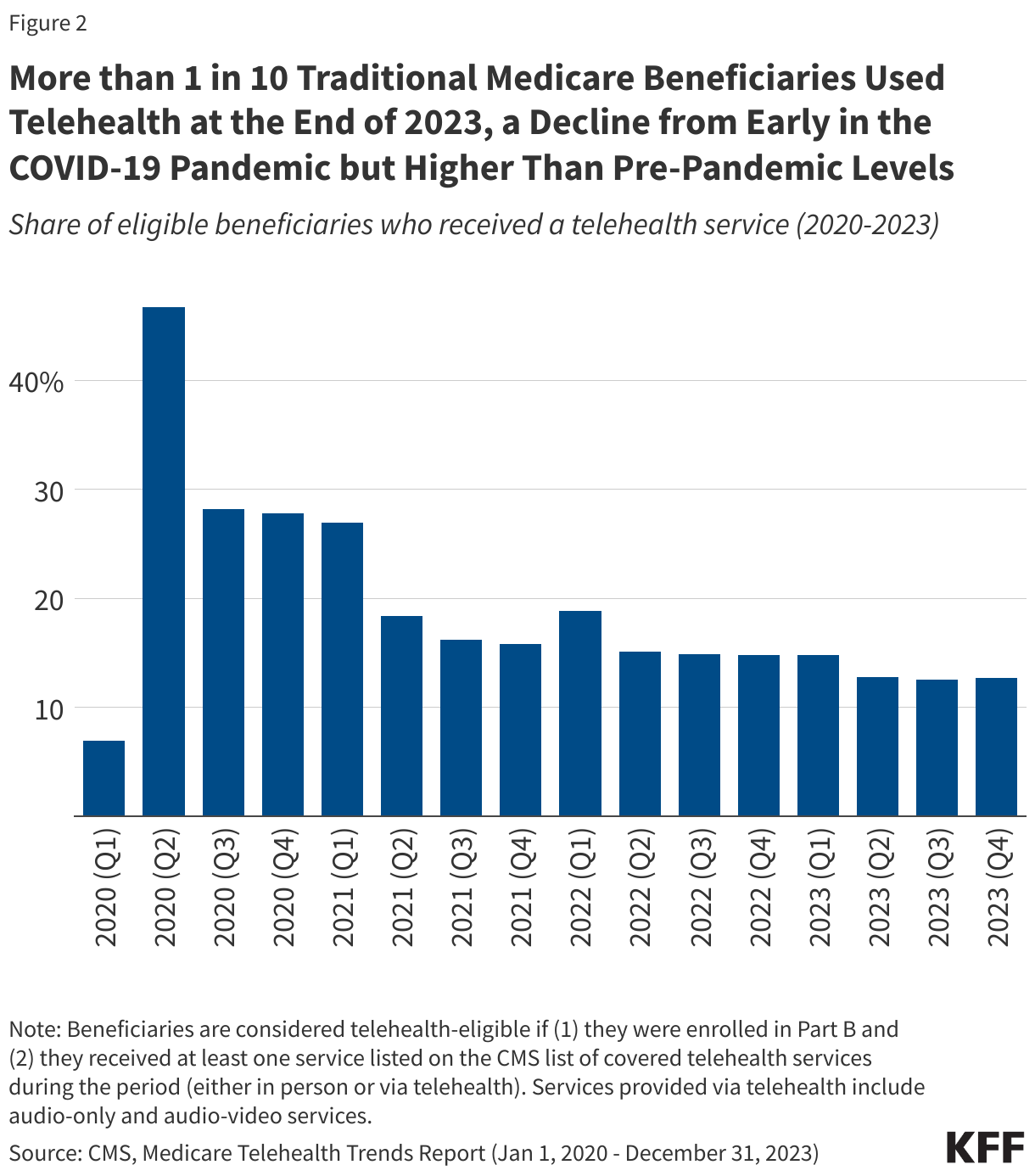

Telehealth use in traditional Medicare increased dramatically at the start of the COVID-19 public health emergency, with nearly half (46.7%) of all eligible beneficiaries receiving at least one telehealth service in the second quarter of 2020, compared to just 6.9% in the first quarter (Figure 2). While use has declined since that time, it remains nearly two times higher than pre-pandemic levels, with more than one in ten (12.7%) eligible beneficiaries receiving a telehealth service in the final quarter of 2023.

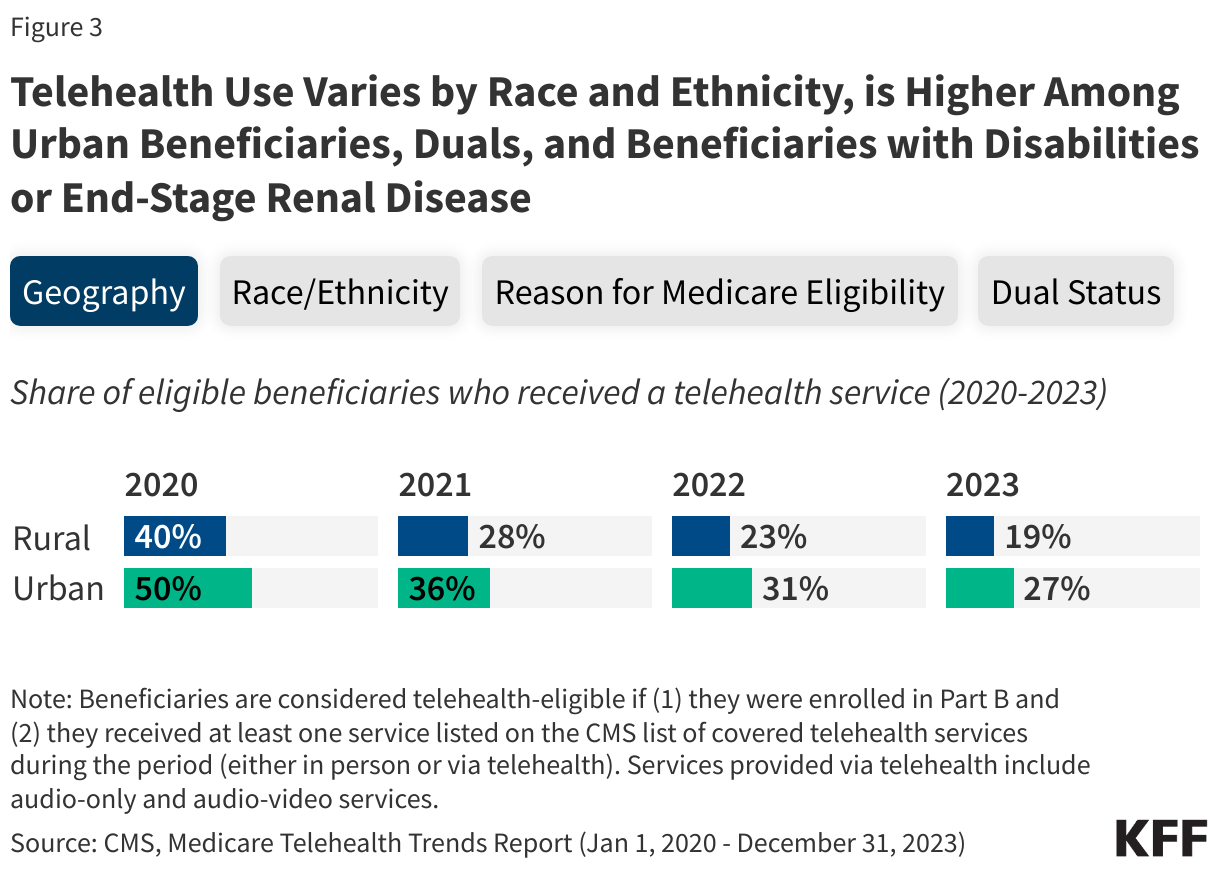

Use of telehealth services varies by geography, race and ethnicity, reason for Medicare eligibility, and dual enrollment in Medicare and Medicaid (Figure 3).

Geography: Rates of telehealth use in 2023 were higher among beneficiaries living in urban areas than those in rural areas (27% vs. 19%), which may be due in part to disparities in access to broadband and other communication technologies. Beneficiaries in rural or underserved areas may lack the infrastructure to support reliable video telehealth visits or the means to afford internet access, which may further impede access to telehealth if coverage of audio-only services is reduced or eliminated.

Race and ethnicity: Rates of telehealth use in 2023 were highest among Asian and Pacific Islander (31%) and Hispanic (30%) beneficiaries, and somewhat lower among Black (26%), American Indian or Alaska Native (25%), and non-Hispanic White beneficiaries (24%). Given that beneficiaries of color are more likely than non-Hispanic White beneficiaries to report difficulty accessing needed health services, telehealth use may help to improve access to care for certain groups.

Reason for Medicare eligibility: Rates of telehealth use in 2023 were higher among beneficiaries who qualify for Medicare based on having end-stage renal disease (ESRD) (37%) or a long-term disability (37%), relative to those who qualify based on age (23%). This may be due in part to higher overall rates of service use among people with ESRD and disabilities (whether in-person or via telehealth) but may also reflect a preference for telehealth services among these populations, or a greater ease of accessing care via telehealth relative to in-person care. Beneficiaries under age 65 who qualify for Medicare based on having long-term disabilities are more likely than older beneficiaries to report having three or more limitations in activities of daily living, and may be more likely to benefit from the increased flexibility of receiving health care services from their home via telehealth.

Dual-eligible individuals: Rates of telehealth use in 2023 were higher among beneficiaries dually eligible for both Medicare and Medicaid compared to Medicare beneficiaries who were not Medicaid-eligible (34% vs. 23%). Dual-eligible individuals are four times more likely than other Medicare beneficiaries to live on incomes of less than $20,000. Prior studies have found that having lower income or living in a socioeconomically deprived neighborhood is associated with higher rates of telehealth use, suggesting that telehealth may have the potential to improve health care access for beneficiaries with limited access to in-person services.

How does Medicare pay providers for telehealth services?

Medicare currently pays providers for telehealth services, both video and audio-only, at the same rate that would be paid if the service were delivered in person. As with most services paid under the Medicare physician fee schedule, payment rates for telehealth services currently vary based on the location of the provider, with services furnished by providers based in a non-facility setting, such as a doctor’s office, reimbursed at a higher rate than services furnished by providers based in a facility setting, such as a hospital outpatient department.

Prior to the COVID-related temporary expansion, Medicare paid for all covered telehealth services at the lower facility rate, regardless of provider location. This means that providers in non-facility settings currently receive higher payment for telehealth services than they did before the temporary expansion. However, assuming no change to current law, Medicare will resume paying for most telehealth services (with the exception of behavioral health services) at the lower facility rate beginning in January 2025. The Consolidated Appropriations Act of 2021 permanently established payment parity between in-person and telehealth services in the context of behavioral health. Should the current flexibilities expire, Medicare will continue to pay providers for behavioral telehealth services at the same rate they would receive if the service were delivered in person.

CMS permanently authorized FQHCs and RHCs to provide and bill for behavioral telehealth services in 2022. As with other types of providers, clinicians in these settings are paid the same rate for behavioral telehealth services as they would receive if the service were delivered in person on a permanent basis. However, for all other types of telehealth services, FQHCs and RHCs are only eligible for reimbursement through December 2024. Medicare currently pays FQHCs and RHCs at rates comparable to those set under the physician fee schedule, which are lower than what they would receive for comparable in-person care, since Medicare typically pays more for clinician services provided by FQHCs and RHCs than those provided in other types of settings.

How do Medicare Advantage plans cover telehealth?

Medicare Advantage plans are required to cover all Part A and Part B benefits covered under traditional Medicare, and have some flexibility to offer additional benefits as well, including telehealth benefits not routinely covered by traditional Medicare (outside of the current telehealth expansion), such as telehealth services provided to enrollees in their own homes, services provided outside of rural areas, and services provided through audio-only platforms.

Since 2020, Medicare Advantage plans have been permitted to include the costs associated with select telehealth services in their basic Medicare Part A and B benefit package, and may continue to do so after December 2024 regardless of the status of the temporary telehealth expansions in traditional Medicare. Telehealth services may be included in a plan’s basic benefits package if they meet certain requirements, such as coverage under Medicare Part B when the same service is provided in person. When these requirements are not met, plans may continue to offer supplemental telehealth benefits via remote access technologies and/or telemonitoring services, but must cover the cost of these benefits using rebates or supplemental premiums.

What additional steps have been proposed to expand Medicare coverage of telehealth?

Options to extend or make permanent many of the current flexibilities around Medicare coverage of telehealth have been the subject of a number of hearings in both the U.S. Senate and the House of Representatives. Bipartisan bills such as the Preserving Telehealth, Hospital, and Ambulances Act and the Telehealth Modernization Act of 2024 include provisions that would temporarily extend the current flexibilities through December 2026. However, outside of select changes, such as permanently allowing FQHCs and RHCs to provide non-behavioral telehealth services, neither bill provides for a permanent expansion of Medicare telehealth coverage.

The Biden-Harris Administration has announced additional measures to preserve telehealth access for Medicare beneficiaries, such as a grant program to support the development of an interstate licensure compact that would make it easier for licensed social workers to practice across state lines, and provisions in a recent CMS proposed rule that would permanently extend certain telehealth flexibilities, such as coverage of audio-only services that meet all other conditions for Medicare telehealth coverage. However, in the absence of Congressional action, implementation of these provisions will be limited to the types of providers, services, and settings where telehealth was permitted before the current flexibilities were put in place (with the exception of behavioral health flexibilities, which have been made permanent).

Related to licensure, Medicare providers are generally required to be licensed in any state where they are practicing, and this requirement extends to telehealth. In most cases, a distant site telehealth provider must be licensed in the state where the beneficiary receiving services is located when the telehealth visit takes place. However, certain states have taken action to develop multi-state licensure compacts, which has allowed for additional flexibility related to licensure in participating states. These compacts are formed when states agree upon a uniform standard of care and enact state laws which allow qualified providers to practice across state lines while maintaining a single license or to maintain multiple licenses or which expedite the process of gaining additional licensure across member states. These compacts may be continued beyond December 2024, though other restrictions may limit their use if the current flexibilities are allowed to expire.

What are the implications of telehealth for Medicare program integrity?

As policymakers weigh whether to extend or make permanent current flexibilities around Medicare coverage of telehealth, several questions have been raised about the impact of telehealth services on patient care quality and program spending, as well as the potential for fraud and overuse.

Since the current flexibilities were introduced, state and federal agencies have filed several lawsuits regarding the submission of fraudulent claims by telehealth companies to Medicare and other insurers. However, investigations by the HHS Office of the Inspector General (OIG) into provider billing patterns during the first year of the COVID-19 pandemic found that just 0.2% of providers who billed for a telehealth service during the period engaged in excessive billing patterns that posed a high risk to the Medicare program, and clinicians generally complied with Medicare requirements when providing Evaluation and Management services through telehealth, suggesting little evidence of widespread misuse to date. MedPAC has recommended that CMS take certain precautions if the current telehealth flexibilities are extended, such as applying additional scrutiny to “outlier” clinicians who deliver more telehealth services than others and requiring in-person visits before high-cost tests and medical equipment are paid for.

What is the expected impact of telehealth use on Medicare spending and the estimated cost of expanding coverage?

Expanding telehealth coverage is expected to lead to an increase in Medicare spending, but the overall magnitude in the long term is uncertain. Some telehealth services may replace in-person care, as in the case of behavioral health visits, but easier access to telehealth may also lead to an overall increase in use of services and higher costs. Prior research has found modest increases in clinical encounters and spending per person among Medicare beneficiaries in geographic areas and health systems with higher rates of telehealth use. At the same time, there is evidence to suggest that beneficiaries with greater access to telehealth services may have fewer emergency department visits and improved adherence to certain medications. Additional research would help policymakers and other interested parties determine whether any increases in Medicare spending as a result of expanded telehealth coverage are offset by improvements in quality of care or decreases in other costs, such as spending on preventable hospital admissions and other types of acute care services.

As policymakers weigh the implications of legislation to maintain or broaden Medicare coverage of telehealth, a key consideration is how to set payment rates for telehealth services across different care settings and provider types. Payment parity between in-person and telehealth services may encourage providers to invest more time and resources into telehealth, but some have raised questions about how to ensure that this investment does not come at the expense of patient care quality or access to in-person services for beneficiaries who prefer them. MedPAC has recommended that CMS return to paying the lower facility rate for most telehealth services, including those furnished by FQHCs and RHCs, and collect data on practice costs in order to adjust telehealth payment rates in the future. Where policymakers end up on these issues would likely affect the overall cost of extending or making permanent Medicare coverage of telehealth beyond 2024.

While the implications of the election on the future of abortion access have received extensive attention, the stakes are also high for the future directions of Medicaid, a program that seven in ten women have a connection to. Vice President Harris and former President Trump hold vastly different views on abortion and Medicaid, key issues affecting women’s health, particularly for women in their reproductive years and with lower incomes. With regard to Medicaid, the Biden-Harris Administration policy proposals have generally focused on efforts to “protect and strengthen Medicaid and the Affordable Care Act (ACA)”, as well as repealing the Hyde Amendment, which limits federal spending on abortion; in contrast, Former President Trump supported plans to repeal or weaken the ACA, cap and reduce Medicaid financing, and restrict Medicaid eligibility while he was president. In a recent column, KFF President and CEO Drew Altman pointed out that Medicaid is the program most likely to be in the crosshairs if Republicans take control this November is Medicaid.

Changes related to Medicaid could have major consequences for health coverage of women with low incomes as well as pregnancy, postpartum and other reproductive health care for women. Here are the top five things to know about women and Medicaid ahead of the election.

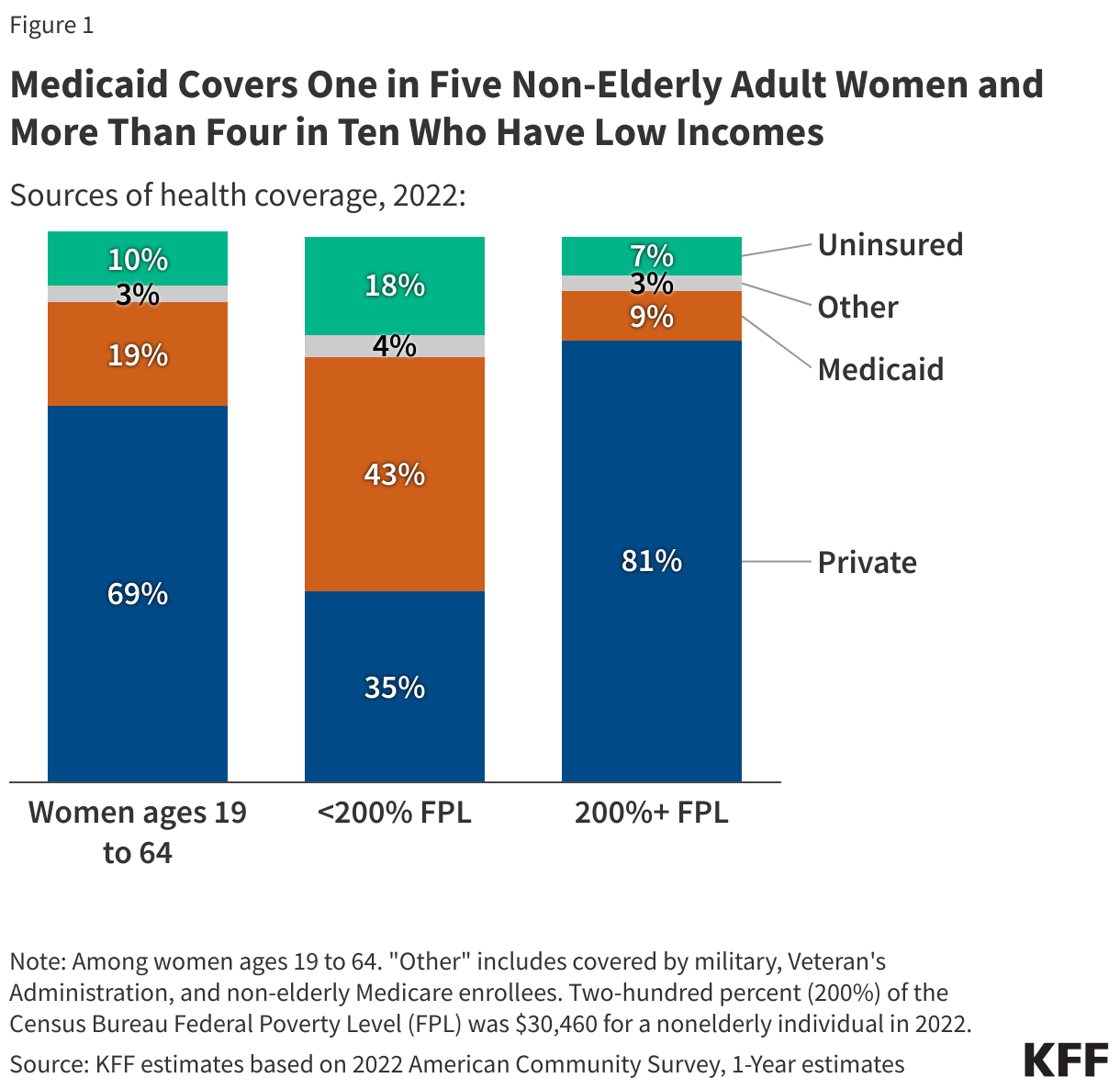

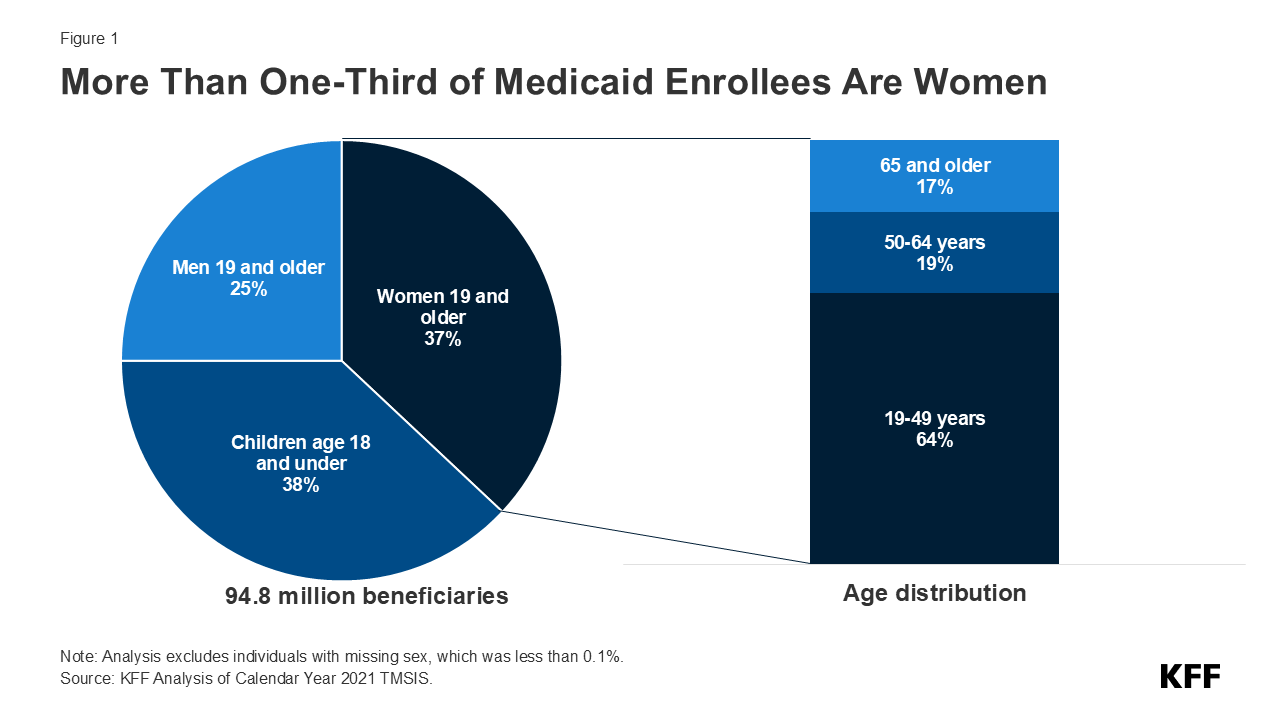

Medicaid is a major source of coverage for women with low incomes (and their children). Medicaid provides coverage to one in five non-elderly adult women, the largest source of coverage after employer coverage (Figure 1). Medicaid covers 43 percent of non-elderly women with low incomes (income below 200% FPL) and over half (52%) of poor women (income below 100% FPL). Medicaid also covers four in ten children and eight in ten poor children..

Medicaid provides coverage to women across the lifespan, including women who are older and those with chronic disabilities. Medicaid provides coverage to women with low incomes who qualify because they meet one of the eligibility categories (pregnancy, parent, disability, or age 65+), or have income less than 138% of poverty through the ACA expansion pathway. Nearly two-thirds (64%) of adult women who are covered by Medicaid are of child-bearing age. Medicaid also covers over four in ten (44%) nonelderly women with a broad range of physical and mental disabilities, including physical impairments and severe mental illnesses. Medicaid finances over half (54%) of all long-term care spending, which is critical for many frail elderly women and women who qualify on the basis of disability. In 2021, 20% of women with Medicare were also enrolled in Medicaid. For these women, Medicaid helps to pay Medicare premiums, deductibles and cost-sharing as well as pay for services not typically covered by Medicare such as long-term care..

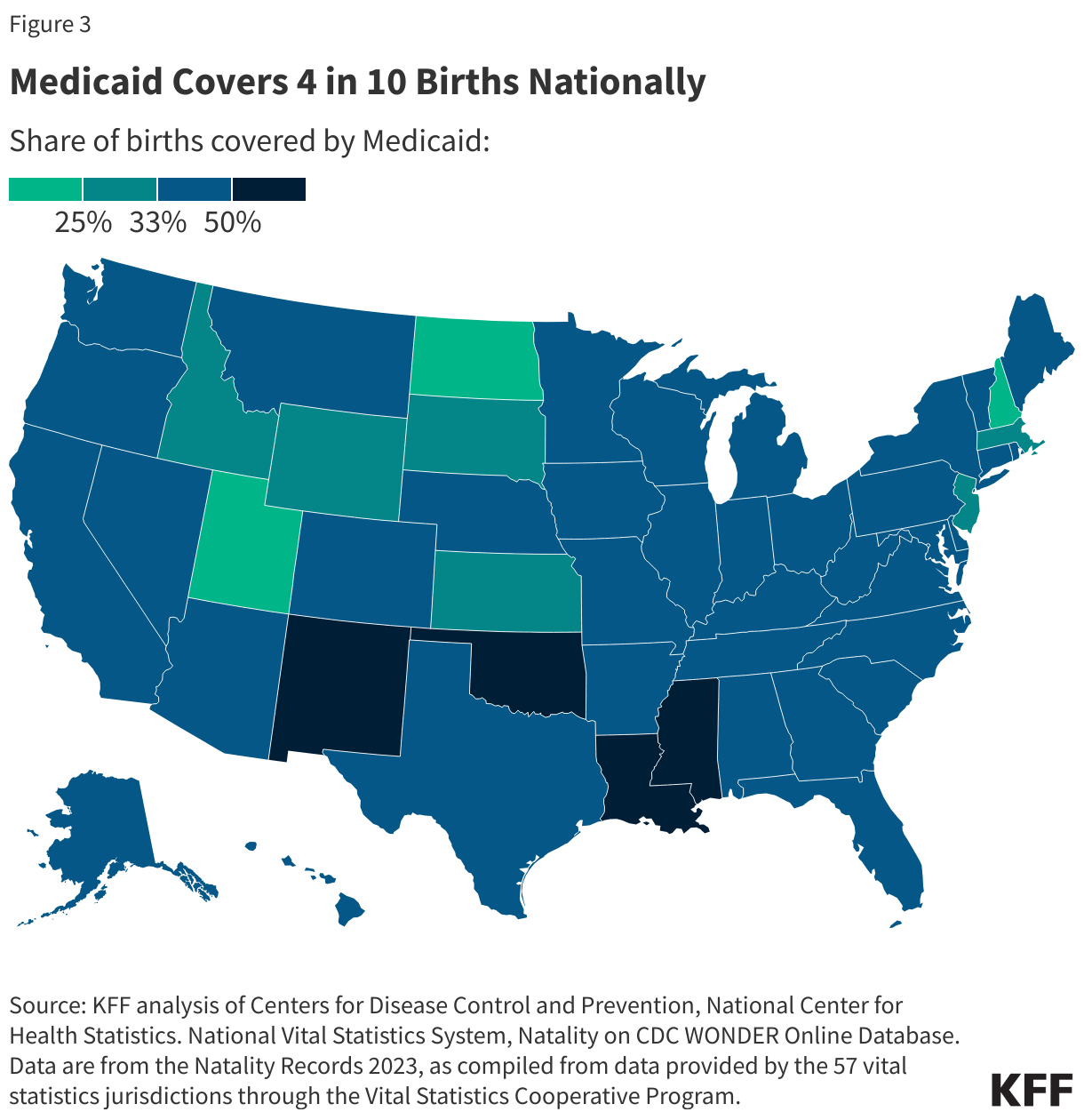

Medicaid is a key source of coverage for pregnant and postpartum women and births as well as access to family planning and preventive services. Medicaid covers over 4 in 10 births nationally and the majority of births in many states. Medicaid has also been used as a lever to help address disparities in access and outcomes in maternal and infant health. KFF research has found that the ACA’s Medicaid expansion promotes continuity of coverage in both the prenatal and postpartum periods. Furthermore, as a result of a provision in the American Rescue Plan Act of 2021, nearly all states now allow pregnancy-related coverage to continue through one year postpartum. Over half of the states have established programs that use Medicaid funds to cover the costs of family planning services for low-income women who remain uninsured and Medicaid accounts for 75% of all publicly funded family planning. Most states have limited scope Medicaid programs to pay for breast and cervical cancer treatment for certain low-income uninsured women..

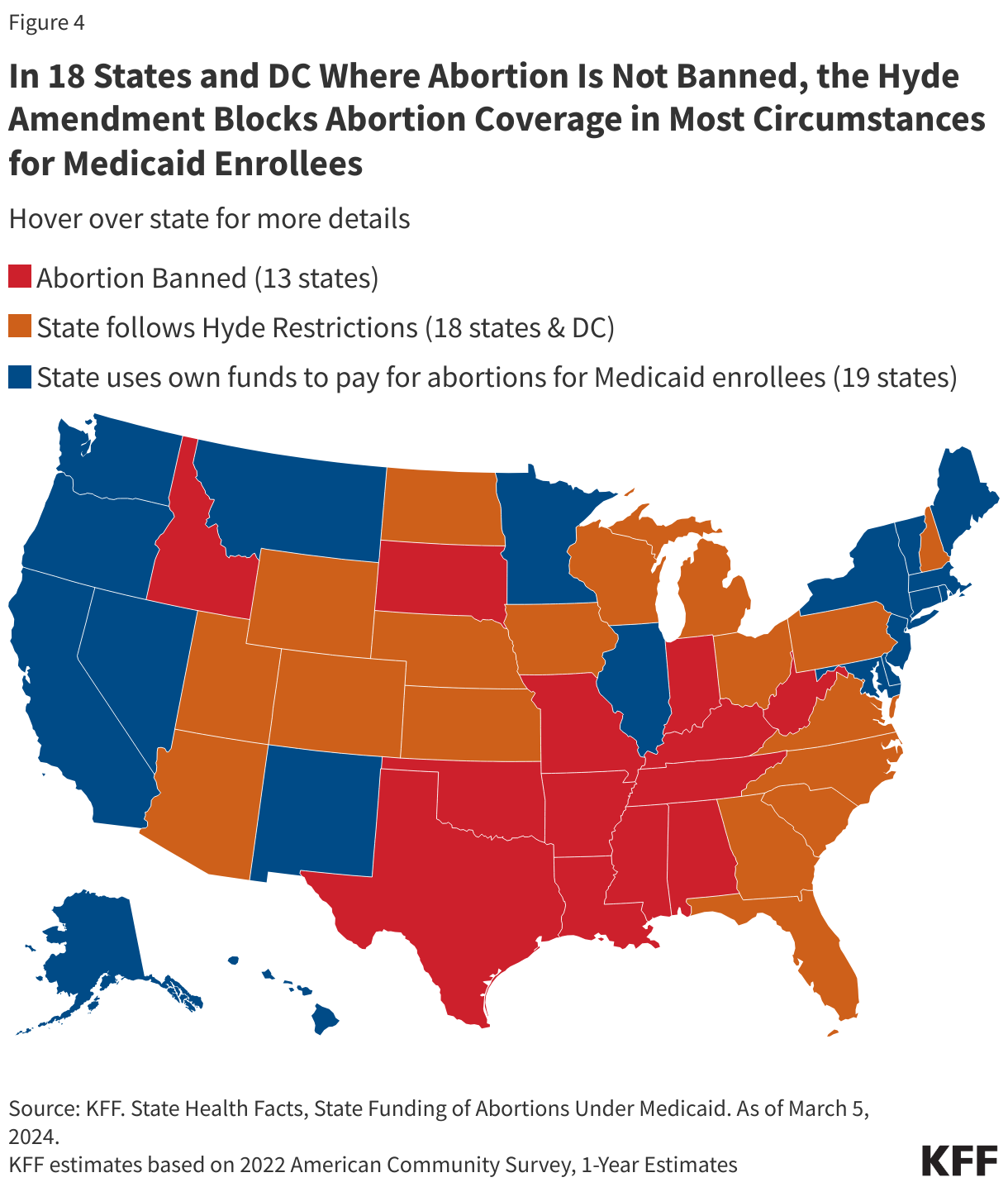

Medicaid provides very limited access to abortion services. The federal Hyde Amendment prohibits federal spending on abortions, except when the pregnancy is a result of rape or incest, or when it jeopardizes the life of the pregnant person. However, states may use their own unmatched funds to pay for abortions for Medicaid enrollees in other circumstances and 19 states currently do so..

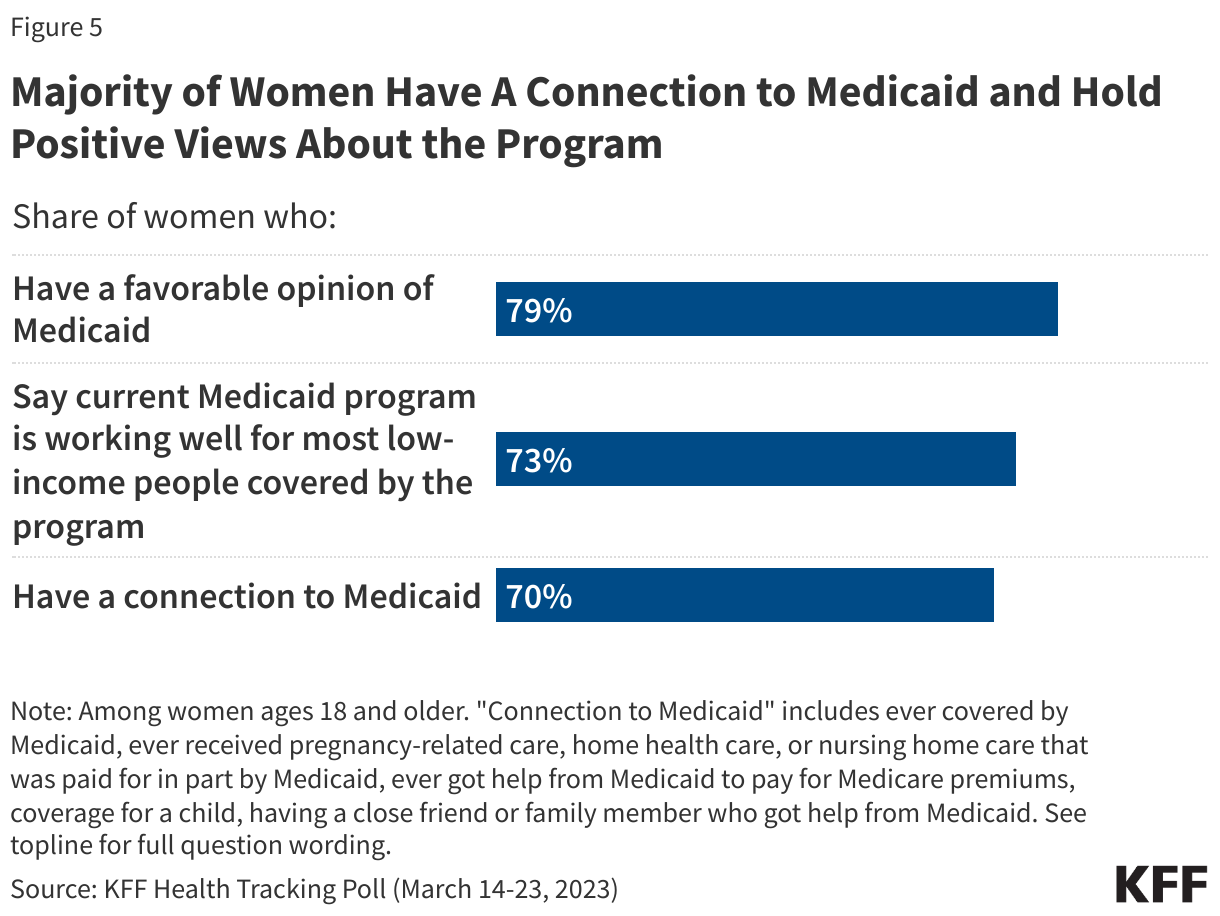

Medicaid has broad support and the majority of enrollees prefer to keep it as it is today. The public’s views of Medicaid are also largely positive. KFF public opinion polling shows Medicaid has broad support across political parties, with majorities of Democrats, independents, and Republicans expressing a favorable view of the program. In addition, the majority of the public and Medicaid enrollees prefer to keep Medicaid as it is today, with the federal government guaranteeing coverage for low-income people, setting standards for who states cover and what benefits people get, and matching state Medicaid spending as the number of people on the program goes up or down. Seven in ten women have a personal connection to Medicaid (including health insurance, pregnancy-related care, home health care, or nursing home care, coverage for a child, or to help pay for Medicare premiums for themselves, a family member or close friend). Eight in ten adult women (79%) have a favorable opinion of the program (Figure 5)..

Major outbreaks of mpox – the infectious disease previously called monkeypox – are ongoing in a number of African countries, in particular the Democratic Republic of the Congo (DRC). In addition, several mpox cases linked to the DRC outbreak have now been identified in some non-African countries, including Sweden and Thailand. Due to these circumstances, in mid-August 2024, the World Health Organization (WHO) and the Africa Centres for Disease Control and Prevention (Africa CDC) each declared mpox to be a public health emergency requiring a globally coordinated response.

This is the second time mpox has been declared an international emergency, with the first spanning 2022-2023. The current mpox outbreak centered in the DRC is being driven by the “clade I” strain of the virus, with a clade Ia variant that is primarily affecting children and a more recently identified clade Ib variant that is spreading primarily via sexual contact among adults. The previous international emergency was driven by a “clade II” strain, and primarily affected adult gay and bisexual men. Currently, there is ongoing transmission of both clades affecting mostly different geographic areas.

The U.S. government has provided technical and financial assistance for mpox response in DRC and elsewhere for years. Following the emergency declarations it has increased this support, including by delivering 50,000 doses of mpox vaccine to the DRC and 10,000 doses to Nigeria, as well as providing $10 million in mpox response-specific funding. On September 24, President Biden also pledged to donate up to 1 million more vaccine doses and an additional $500 million in funding to support mpox response across Africa.

Since the emergency declarations, the Africa CDC, WHO, and governments of affected countries have accelerated efforts to respond to the situation by developing updated response plans, mobilizing more funds and attention from policymakers, and working to obtain more mpox vaccine doses. Still, the response faces a number of challenges including an uncertain path to delivering mpox vaccines at scale, lack of access to prevention tools, poor health infrastructure in many affected areas along with ongoing conflicts and instability, and high levels of distrust and misinformation in affected communities.

No cases of clade I mpox have been identified in the U.S. as of September 26, 2024, and the CDC estimates the risk to the general public in the U.S. from the current outbreak in African countries is very low. However, clade II mpox infections continue to occur in the U.S. primarily among adult gay and bisexual men, though case numbers have declined since the previous mpox emergency in 2022-2023.

Introduction

Major outbreaks of mpox are again raising significant international concern. The DRC in particular has reported a large increase in cases driven by the “clade I” strain of the mpox virus, including a “clade Ia” variant that is primarily affecting children and a more recently identified “clade Ib variant” that is spreading primarily via sexual contact among adults. Clade I cases are also being reported in some other African nations, and several cases of the clade Ib variant have now been identified in non-African countries. At the same time, there continue to be mpox cases caused by “clade II” mpox, which was the variant that led to an earlier public health emergency in 2022-2023 in many different regions and countries around the world, including in the U.S. The recent circumstances led to two public health emergency declarations: the Africa Centres for Disease Control and Prevention (Africa CDC) declared mpox to be a “public health emergency of continental security” (PHECS) for Africa on August 13, 2024, and the WHO Director-General declared the mpox outbreaks a “public health emergency of international concern” (PHEIC) on August 14, 2024.

This explainer answers key questions about the international response to date, including the U.S. government’s role globally, and identifies issues and challenges that may affect the response going forward. It also discusses how the global emergency might affect the U.S. and the current status of mpox circulation within the U.S. It will be updated as needed.

Key Questions

What is mpox?

Mpox is a disease caused through infection with the mpox virus (MPXV). The first human case of mpox was identified in 1970, and since then, the virus has caused intermittent outbreaks. It is considered endemic in several Central, East, and West African countries, where infections have traditionally occurred through exposure to rodents or other animals carrying the virus. Human-to-human spread is also possible, primarily through close contact such as skin-to-skin contact and sexual or other contact with infected body fluids. Mpox can also pass from mother to fetus during pregnancy and during or after birth. Mpox infections can lead to symptoms such as fever, headaches, and body aches, and the development of a rash with lesions. Some infections can cause severe illness and even death, and there is a higher risk for severe outcomes in those with weaker immune systems such as people with HIV who are not virally suppressed and children. In areas with poor health care infrastructure and a lack of access to prevention tools, testing, treatment, and supportive care, mpox can be more difficult to identify, treat, and contain.

In recent years, more sustained human-to-human transmission and larger mpox outbreaks have been recorded from two genetic families of mpox virus (known as clade I and clade II mpox viruses; see Box 1). Most notably, in 2022, an outbreak of clade II mpox virus emerged from West Africa and spread globally, eventually affecting more than 100 countries and causing over 100,000 reported cases, including over 30,000 cases in the U.S. alone. That global outbreak was declared a PHEIC by WHO between July 2022 and May 2023 , and also declared a public health emergency in the U.S. in August 2022, marking the first time mpox had become a significant public health threat in non-endemic countries. Adult gay and bisexual men, especially men of color, made up the vast majority of cases during that outbreak in the U.S.

Strains of mpox virus (MPXV) from both clades have continued to circulate in largely geographically separate sets of endemic African countries, with clade II mpox infections primarily found in West African and Southern African countries and clade I infections found in Central African countries, the DRC in particular. In addition, clade II infections continue to be identified in many countries outside endemic regions, including in the U.S., primarily in gay and bisexual men, though the number of reported cases has declined significantly since the 2022 global outbreak.

Box 1: Epidemiology of Mpox Virus (MPXV) Clades I and II

There are two main genetic families of MPXV, known as clade I and clade II, and each clade is divided into sub-clades (clade Ia, clade Ib, clade IIa, and clade IIb) based on genetic similarities and differences.

Historically, clade I MPXV infections have been identified primarily in Central African countries, the DRC in particular, while clade II MPXV infections have been identified primarily in West African countries. In 2022, clade II MPXV emerged from West Africa to cause a global outbreak, primarily spread via sexual contact among adult gay and bisexual men. While that outbreak subsided following its 2022 peak, new cases of clade II MPXV infection continue to be reported in a number of countries worldwide, including African countries and the U.S.

In recent years, clade Ia and clade Ib MPXV have been circulating concurrently in the DRC and in Africa, and some clade Ib infections have also been identified outside of Africa:

Clade Ia MPXV: Infections continue to occur mostly in central DRC, affecting children exposed to infected animals with some additional ongoing human-to-human transmission due to close contact among family members or caregivers.

Clade Ib MPXV: Firstdescribed in 2023; infections have been found primarily in eastern DRC and neighboring African countries. This includes several countries reporting mpox cases for the first time ever, such as Burundi, Kenya, Rwanda, and Uganda. In areas affected by clade Ib, the majority of cases have occurred in adults and transmission appears to be sustained “largely, but not exclusively, through transmission linked to sexual contact and amplified in networks associated with commercial sex and sex workers.”

Available data suggest clade Ia MPXV infections are more likely to be severe cases and cause deaths than infections from clade IIa or clade IIb MPXV. While there is limited data on the severity of clade Ib, early indications are that it may not be as severe as clade Ia. Still, more data and studies are needed to fully understand the extent of biological and epidemiological differences across mpox sub-clades.

Why has mpox again been declared a public health emergency this year?

WHO and Africa CDC issued the emergency declarations due to the recent rapid rise in case numbers and expanded geographic reach of mpox. Of primary concern has been mpox in the DRC. In 2023, the DRC reported more than 14,000 suspected cases (three times as many as in 2022) and over 500 deaths from mpox. In 2024, these trends have accelerated, and in only the first half of this year, the country has reported over 14,000 suspected cases across 23 different provinces, with over 450 deaths. Children have been heavily affected in the DRC outbreaks, with an estimated 70% of mpox cases and 85% of mpox deaths in the country since 2022 occurring in children under 15.

Moreover, the emergence and rapid spread of a new strain of the mpox virus (known as clade Ib; see Box 1) that “appears to be spreading mainly through sexual networks” was first identified in eastern DRC in 2023 has not only caused a growing number of cases in the DRC, it has been found in a number of other countries in the region and outside Africa with one case detected in Sweden and one in Thailand. There are concerns that clade Ib virus may be more readily transmissible (including via sexual contact) compared to clade Ia, which could be contributing to the increased numbers of cases and the cross-border spread of the disease.

What has been the global response to the current mpox emergency?

Alongside its PHEIC declaration on August 14, WHO released $1.45 million from its Contingency Fund for Emergencies to help scale up the response in affected countries. On August 26, WHO issued a Global Mpox Strategic Preparedness and Response Plan (SPRP) that outlined a set of global, regional, and country level response steps and needs to address the spread of clade Ib in eastern DRC and to control outbreaks of clades I and II in the DRC and other African countries. The plan emphasized the need for better mpox surveillance, strengthening clinical care for the disease, more global cooperation to increase vaccine access, implementation of strategic vaccination efforts in populations at highest risk, and public health communication efforts and community empowerment.

Along with its declaration on August 13, Africa CDC requested $20 million for immediate mpox response needs (and reported it had been granted $10.4 million) from the African Union, and initially requested an additional $16 million from WHO and other international partners for a continent-wide response. The Africa CDC and WHO also launched a joint plan, the Mpox Continental Preparedness and Response Plan for Africa, covering the September 2024 through February 2025 period identifying the following:

10 “pillars” for the continental response including coordination and leadership, case management, vaccination, and logistics and financing;

roles and responsibilities for the primary international organizations involved in the response, including Africa CDC, WHO, Gavi, the Vaccine Alliance, and UNICEF;

the need for approximately $600 million to address the outbreak on the continent during the plan period (with 55% to be allocated to the mpox response in 14 affected countries and to boost readiness in 15 other countries at risk and 45% to be allocated to operational and technical support through partners), calling on donor governments, philanthropic organizations, and the private sector to provide this funding. Recent pledges from the U.S. and other donors totalled

In addition, Africa CDC activated its Public Health Emergency Operations Centre (PHEOC), initiated negotiations with pharmaceutical manufacturers and others to obtain mpox vaccines for use in outbreak response on the continent (see Box 2 for more on mpox vaccines), began supporting laboratory testing capacity building for mpox, and deployed epidemiologists to affected areas, among other activities.

Are mpox vaccines available, and are they getting to affected countries quickly?

There are several vaccines that can be used to prevent mpox (see Box 2). Africa CDC and WHO consider vaccines to be a key prevention tool for the response, and the joint Africa CDC and WHO continental response plan calls for enough vaccine doses to vaccinate 10 million people in African countries from September 2024 through February 2025. However, there are a limited number of vaccine doses available other than those already stockpiled by high-income countries.

Some high-income countries have agreed to donate vaccine doses from their existing stockpiles in support of the global response. For example, the European Commission announced a donation of 175,000 doses to Africa CDC, and Japan agreed to donate up to 3.5 million doses for response in the DRC. The U.S. has pledged to provide 1 million doses for the response, and has already delivered 50,000 doses to the DRC and 10,000 doses to Nigeria (see more on the U.S. role in mpox response below). In addition, Bavarian Nordic, the company that manufactures one of the mpox vaccines, pledged to donate 40,000 of the doses it has on hand to the DRC and to ramp up production of more doses for use in African countries in the coming months. Taken together, donors have pledged to provide a total of over 5.4 million doses of mpox vaccine for this response, according to WHO.

UNICEF and Gavi are also assisting in the process of acquiring vaccine doses and implementing vaccination in affected areas. Gavi announced it would redirect $2.9 million in funding to support mpox vaccinations in the DRC, and also is talking with vaccine manufacturers to help purchase doses directly, using funds drawn from its First Response Fund. Gavi is also helping coordinate the delivery of donated vaccines to countries in need. UNICEF reports that it is providing vaccination supplies and logistics support, health worker trainings, transportation, storage, and vaccine administration in the country.

As of September 24, 2024, 250,000 doses – 200,000 doses from the European Commission and Bavarian Nordic, along with the 50,000 doses from the U.S. – have arrived in the DRC. However, this is just a small fraction of the over 3 million doses that health authorities say are needed in the country in the near term. The DRC government announced it expects mpox vaccinations to begin in the country in the first week of October.

In other nearby countries reporting recent clade I mpox cases (such as Burundi, Rwanda, and Uganda), there is little information so far about if mpox vaccines will be provided in-country and when vaccinations may begin.

Box 2: Mpox vaccines and the international response

There are three vaccines, initially developed for smallpox prevention, that are considered effective in preventing mpox infection:

MVA-BN: Also known under the brand names Jynneos, Imvamune, and Imvanex, it is manufactured by Bavarian Nordic in Denmark and licensed by a number of countries for use in adults for the prevention of mpox.1 The MVA-BN vaccine is administered in a two-dose series.

ACAM2000: Manufactured by Emergent in the U.S., it has been made available for mpox prevention in adults under expanded access by the FDA in the U.S. The ACAM2000 vaccine is administered as a single dose.

LC16m8: Manufactured by KM Biologics in Japan, it has been licensed by Japan for smallpox prevention in children and adults and authorized by Japan for use against mpox since 2022. The LC16m8 vaccine is administered as a single dose.

Africa CDC has primarily focused on acquiring MVA-BN and LC16m8 doses for African countries, and estimates that enough doses to vaccinate 10 million people on the continent are needed.1 In the U.S., a 2022emergency use authorization issued by the FDA allows for the use of MVA-BN (JYNNEOS) vaccine in children and adolescents under some circumstances. WHO representatives have stated that the same vaccine could be used “off label” to vaccinate children and adolescents on the African continent during the current emergency response.

What assistance has the U.S. provided to the DRC for mpox response?

The U.S. government has long provided support to help DRC address mpox. For example, CDC has supported mpox research and response efforts in country for decades. Over the last few years, U.S. support for mpox response has included efforts to build laboratory testing capacity in-country, conduct mpox vaccine research, and training health care workers.

With the growth in mpox cases in the DRC and the emergency declarations from Africa CDC and WHO, the U.S. government has announced a number of additional actions. This includes a U.S. commitment to provide over $55 million in emergency health assistance through USAID and the U.S. CDC for mpox response in DRC and other affected countries in Africa, including $10 million in additional funding announced in August specifically for clade I mpox response efforts. Also, the U.S. donated 10,000 doses of mpox vaccine to Nigeria in August and delivered 50,000 doses of mpox vaccine to the DRC in September, along with additional support for vaccine delivery.

On September 24, President Biden stated the U.S. would increase its support over the coming months, and expects to provide over $500 million in additional assistance for the mpox response in African countries as well as donate as many as 1 million mpox vaccines in support of the response.

Besides its mpox-specific support, the U.S. government has also long provided significant amounts of global health and humanitarian assistance to the country, and recently stated it would be expanding assistance for broad humanitarian efforts in the DRC.

What are key challenges in responding to the current mpox emergency?

Addressing the current mpox emergency in the DRC and other affected countries in Africa poses a number of challenges, including:

Limited testing, surveillance, and epidemiological capacity. There is a lack of point of care testing and laboratory capacity in many affected areas, which means many suspected cases of mpox may be undiagnosed and suspected cases unconfirmed. This is particularly true in regard to genomic sequencing. This hampers epidemiological investigations and leaves many questions unanswered about the current state of mpox in the DRC and elsewhere. More testing and epidemiological information on modes of disease transmission, risk factors, and disease severity associated with the different MPXV clades, as well as outcomes of pregnancy in women infected with different MPXV clades, would help authorities target response efforts.

Difficulties with obtaining and distributing mpox vaccines at scale. There is currently a limited global supply of mpox vaccines, with many of the existing doses found only in national stockpiles of high-income countries so the response relies in large part on donations. Also, there is a lack of formal authorization to use these vaccines in a number of the affected countries in Africa and little data on the effectiveness of these vaccines against clade I mpox or their effectiveness in children. A new, large-scale vaccination campaign to reach the populations at greatest risk for mpox is also a challenge.

Stigma and overlapping risks of mpox and HIV infection. There are relatively high rates of HIV infection in some mpox-affected countries in Africa, which raises concerns about the potential overlap in risks between these infectious diseases. Unsuppressed HIV infection could raise the risk for mpox transmission, especially in the context of sexual contact, and for development of more severe outcomes from mpox infection. In addition, both infections can lead to stigma for those affected, making the response more challenging. Therefore, ensuring public health authorities plan to address HIV and mpox in a coordinated fashion will be important.

Health systems and health care workforce. Lack of access to health care and a limited health care workforce increase risks from mpox for individuals and communities. Linking mpox cases to health care services as early as possible and ensuring the health care workforce is adequately trained and supplied to address mpox improves outcomes.

Travel restrictions. To date, countries have not put into place harsh restrictions on travel to and from areas affected by this mpox emergency. However, if the outbreak worsens and spreads to more countries, there is the potential for countries to impose travel bans or other restrictions, as has occurred during past outbreaks. There is little evidence to support the effectiveness of such restrictions in interrupting international transmission of mpox.

Competing priorities amid instability, conflict, and community distrust. Many of the affected countries – the DRC in particular – face multiple simultaneous humanitarian crises, health emergencies, and other urgent issues in addition to mpox. This makes focusing attention on and implementing a response to mpox more challenging, especially in the context of limited resources. For example, in some affected areas in the DRC, there is a history of instability and conflict and an ongoing lack of trust in authorities in many communities, which complicates response and risk communication efforts particularly those focused on reaching the most at-risk populations.

How might this latest outbreak affect people in the U.S.?

Although cases of mpox due to clade II infections continue to occur in the U.S. (see below), so far no cases of mpox due to clade I infections – the genetic family linked to the current DRC outbreak – have been identified in the U.S. The U.S. CDC estimates that the risk to the general public from the current mpox outbreak in African countries remains very low. The CDC also estimates there is a low to moderate risk from the current DRC-based clade I outbreak for U.S. gay, bisexual and other men who have sex with men (MSM) who have more than one sexual partner as well as for people who have sex with MSM, regardless of gender, particularly if there is a history of travel to any of the African countries affected in the current mpox emergency.

In light of the evolving mpox situation in parts of Africa and the potential risk of imported cases, CDC has issued a travel warning for the DRC and has issued severalhealth alerts for U.S. clinicians, which provide guidance on prevention strategies and also suggest a “heightened index of suspicion” for mpox in patients recently arriving from affected areas in Africa who demonstrate signs and symptoms consistent with the disease.

Given the rise in anti-immigrant rhetoric and a history of charged debates about travelers entering the U.S. during health emergencies, there is the potential for mpox to become politicized this election year, especially if cases linked to the ongoing outbreaks in Africa are eventually identified in the U.S.

What is the status of ongoing mpox circulation in the U.S.?

As mentioned above, in 2022-2023, the U.S. had over 30,000 mpox cases during the global outbreak of clade II mpox, which had initially emerged from West African countries. While case numbers have declined in the U.S. since 2022, some clade II mpox cases continue to be identified, with CDC reporting 1,968 mpox (clade II) cases so far this year nationwide as of September 1, 2024. These cases have primarily occurred among adult gay, bisexual and other men who have sex with men (MSM) who have multiple sexual partners, especially men of color and with people with HIV being disproportionately impacted. According to CDC, during the peak of the epidemic in 2022 over 99% of mpox clade II cases in the U.S. occurred among men, and of those, 94% were among men who had sexual contact with other men.

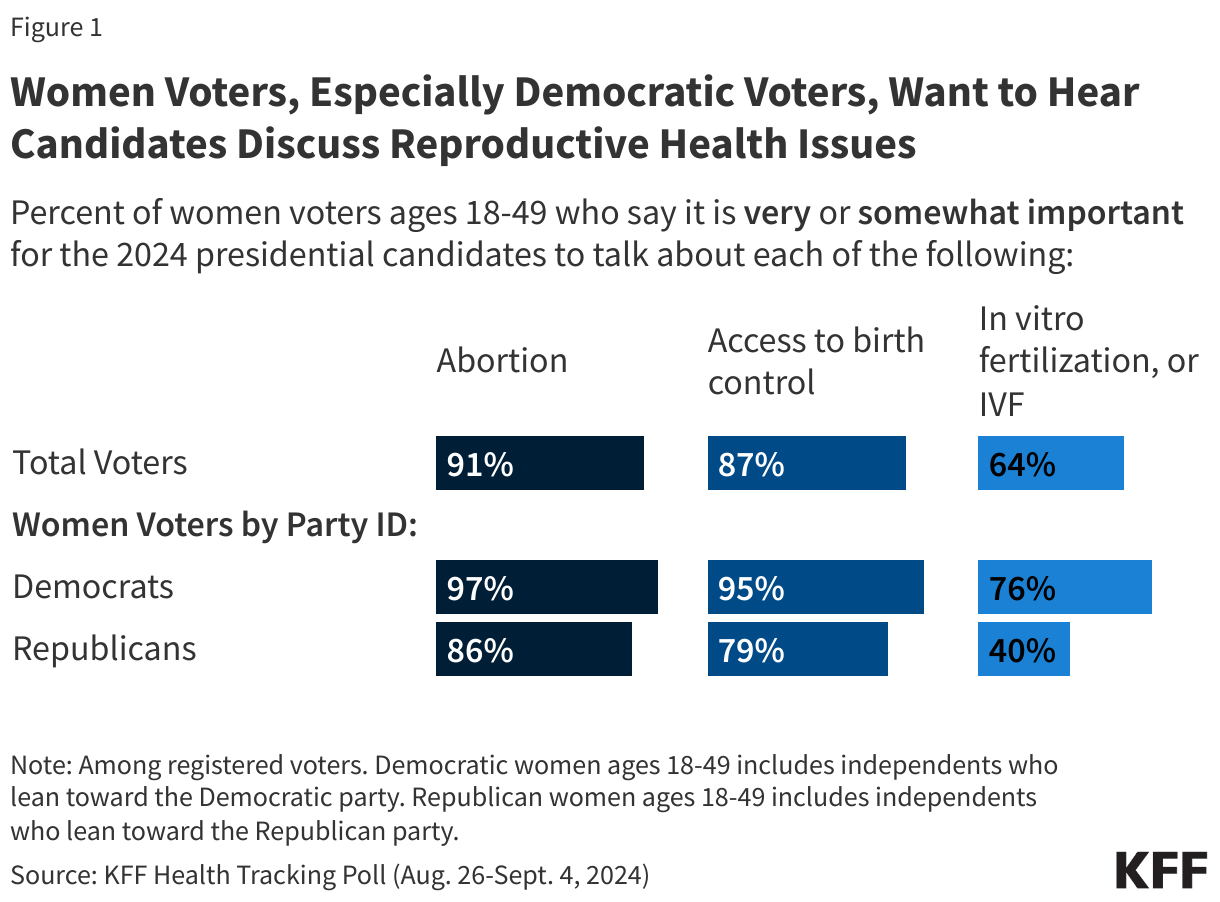

The 2024 election is the first Presidential election since the Supreme Court’s ruling in Dobbs v. Jackson Women’s Health Organization, and abortion access and reproductive health more broadly, are front and center in this election (Figure 1). The two candidates, Vice President Kamala Harris (D) and former President Donald Trump (R) have widely different positions on reproductive health. Vice President Harris has been and is an outspoken leader and advocate for reproductive freedom, while former President Trump celebrates the overturning of Roe v Wade, which ended the constitutional right to abortion and allowed states to completely ban or severely restrict abortion access. The candidates’ Vice-Presidential running mates, Governor Tim Walz (D) and Senator JD Vance (R) also have divergent records on reproductive health issues. Governor Walz points to his support for Minnesota’s Protect Reproductive Freedom Act, which codified abortion rights in the state, as well as his family’s own experience with fertility care. Senator Vance has expressed support for a national abortion ban via the Comstock Act and voted against a Senate bill that would have established a national right to IVF, a position that his running mate, Donald Trump, has said he supports.

While abortion is the most prominent health care campaign issue, the election could also have large implications for contraceptive care and maternal health. This brief summarizes the positions, records, and potential priorities of the two major party candidates for the 2024 Presidential election on three major issues in women’s health policy – abortion, contraception, and maternal health. The information presented is derived from the candidates’ records from their time as elected officials, their proposals or statements, and the Democratic and Republican party platforms. We have also included discussion of proposals from the Heritage Foundation’s Project 2025. While former President Trump has distanced himself from this proposal, its authors are influential in Republican circles and include several individuals who served in the Trump Administration. A separate side-by-side from KFF compares the candidates’ positions across a broad range of health care issues.

Abortion

Abortion access is one of the most prominent issues in the 2024 election, and the candidates have widely divergent records and positions. Vice President Harris has been an outspoken advocate for reproductive freedom and has endorsed the restoration of the prior federal standard under Roe v. Wade, which would guarantee a right to abortion until the point of fetal viability. In contrast, Trump expresses his support for letting states set their own abortion policy, including banning abortion, as allowed under the Dobbs Supreme Court ruling.

Vice President Harris has been vocal in her disagreement with the Supreme Court’s 2022 decision in Dobbs v. Jackson Women’s Health Organization, which overturned Roe v. Wade and allowed states to set their own policy on abortion legality. In stark contrast, Trump has repeatedly taken credit for the overturning of Roe and giving states decision-making authority on abortion because he appointed three conservative justices to the Supreme Court with the explicit goal of overturning Roe. Since the Dobbs ruling, 14 states have banned abortion with very few exceptions and several other states have limited abortion availability to very early in pregnancy.

Abortion Access

Vice President Harris has been the leading voice for the Biden/Harris Administration on reproductive health and has said she supports restoring the protections of Roe v. Wade and eliminating the filibuster to do so. In the wake of the Dobbs ruling, the Biden-Harris administration has tried to limit the impact of the bans through executive actions as well as in the courts. This includes reiterating federal protections for abortion care under EMTALA in cases of pregnancy-related emergencies, reinforcing requirements for pharmacies to fulfill their obligation to provide access to reproductive health pharmaceuticals, enforcement of non-discrimination policies for health care providers, promulgating policies to strengthen data privacy to protect those seeking reproductive health care, and defending the FDA decision to approve mifepristone (one of the drugs used in the medication abortion regimen) and changes in how the drug can be dispensed. Vice President Harris opposes the Hyde Amendment, which limits federal spending on abortions to cases of rape, incest, or life of the pregnant person.

In 2016, Trump ran on the promise that he would appoint Supreme Court judges that would overturn Roe v. Wade, a promise he kept. Most recently, he has stated that he believes that abortion regulation should be left up to states and tweeted that he would veto a federal ban. At times earlier in the campaign he has suggested that he would support some type of federal standard, such as 15 or 16 weeks gestation, that would apply in all states. He has said that he believes in exceptions for cases of rape, incest, and life of the mother. Despite stating that he believes that abortion bans or limits at 6 weeks are “too early,” he also said he will vote against the ballot initiative that would expand abortion legality in Florida, where he resides (currently limited to six weeks of pregnancy). In terms of penalties for violation of bans or gestational limits, he has said that they should be also decided by states, even leaving open the possibility of allowing states to prosecute people in states with bans if they obtain abortions.

Trump has repeatedly stated that Democrats support abortion up to and after birth, which is false. There are no abortions at birth or after. During the 2016 campaign, he pledged to make the Hyde Amendment abortion funding ban a permanent law.

Medication Abortion

Medication abortion pills account for the majority of abortions in the U.S. The Biden-Harris Administration has implemented policies that expand access to medication abortion, particularly via telehealth, and has been fighting lawsuits brought by anti-choice clinicians and policymakers to further restrict abortion access. Former President Trump’s statements about medication abortion have been inconsistent, at times suggesting he would not block their availability and at other times suggesting the opposite. His support for leaving abortion policy to the states allows states to prohibit access to all abortions, including medication abortion. Project 2025—the detailed conservative policy treatise that was spearheaded by many former Trump Administration leaders—is clear in its opposition to the FDA’s approval of mifepristone and endorses the Comstock Act, which would effectively prohibit the mailing and distribution of abortion pills.

The Comstock Act is an existing 1873 anti-vice law banning the mailing of obscene matter and articles used to produce abortion. The Biden-Harris Administration’s Department of Justice maintains that the Comstock Act should not be interpreted literally and therefore has not enforced it. Based on over a century of Federal Court rulings, they determined the Comstock Act only applies when the sender intends for the material or drug to be used for an illegal abortion, and there are legal uses of abortion drugs in every state and no way to determine the intent of the sender. However, that would not preclude an Administration that is hostile to abortion from doing so. Former President Trump has not articulated his stance on enforcement of the Comstock Act, but some Republican leaders, including his running mate Senator Vance, have called for enforcement of the law and a halt on the mailing of all abortion medications and supplies within the country (which would be a de facto national ban) and even limiting access in states that currently allow abortion without restrictions.

Pregnancy-Related Emergency Care

Health exceptions to abortion bans is an issue that Vice President Harris has spoken about extensively. In addition to reiterating the federal EMTALA requirements for hospitals to provide health-stabilizing emergency care that includes abortion in cases of pregnancy-related emergencies, the Biden-Harris administration defended their policy in a case that reached the Supreme Court. This challenge was spearheaded by Republican-led states that ban emergency abortion care, even when it is the standard of care to preserve or stabilize health. President Trump says he believes in exceptions for “life of the mother.” Project 2025 authors say that emergency abortion denials are not a problem and call for the reversal of the Biden-Harris Administration’s EMTALA guidance and withdrawal of lawsuits challenging state abortion bans without health exceptions.

Access to contraception has emerged as another health care issue in this year’s election where Vice President Harris and former President Trump have different records. Vice President Harris’ call for reproductive freedom includes access to contraception, and her support on this issue extends back to her time before she became Vice President. Since the Dobbs decision, the Biden-Harris Administration issued executive orders reiterating support for contraception and directing various federal agencies and regulators to assure that access to the full range of contraceptive services and supplies is safeguarded. Trump’s Administration issued multiple regulations that placed restrictions on the availability of funding for contraception. During his campaign, he initially expressed that states could restrict access to contraceptives, but shortly afterwards, also said that he would not support this.

Right to Contraceptives

Vice President Harris is a strong supporter of contraceptive care, including coverage of over-the-counter methods, encouraging broader access under Medicare and at colleges and universities, and for the proposed federal Right to Contraception Act, which is pending in Congress. Although Trump has not spoken extensively about contraception during this campaign, the Republican party platform states support for “access to birth control;” however, there is no detail on the policies that they would implement to promote access. The majority of the Republican members of Congress (including Senator Vance) either opposed or abstained from voting on the Right to Contraception Act. Project 2025 characterizes some emergency contraception pills—a contraceptive that prevents pregnancy after sex by preventing or delaying ovulation, as a “potential abortifacient.”

Title X Federal Family Planning Program

While in office, Trump’s Administration rewrote the rules governing the federal Title X program, the federal family planning program that supports contraceptive access for people with lower incomes. Title X funds have never been used to pay for abortion services, but Trump’s Administration rewrote the regulations to disqualify family planning clinics from participating in the program if they also offered abortion services (with separate funding); additionally, they prohibited participating clinics from offering referrals to abortion services at other clinics to pregnant patients seeking abortion information. These changes resulted in a reduction of about 1,300 of the 4,000 sites participating in the network of clinics receiving federal support from the Title X program. His Administration also provided federal family planning funding through Title X funds to clinics that did not provide contraceptive methods, which had been a requirement of the program until that time. The Biden-Harris Administration reversed the Trump Administration changes to the program. Project 2025 calls for the restoration of the Trump-era rules and focusing the program on fertility-awareness based methods (FABM).

Medicaid and Family Planning

For decades, the Medicaid program has required coverage for family planning services, including contraceptives. The Biden–Harris Administration has reiterated support for this policy as well as the program’s “free choice of provider” policy which commits to inclusion of all qualified providers (including Planned Parenthood) that offer both contraception and abortion services, although federal Medicaid funds are not used for abortion care. Former President Trump allowed federal Medicaid funds to be used in a Texas Medicaid program that excluded Planned Parenthood and did not cover the full range of contraceptives, excluding emergency contraception. Eliminating Planned Parenthood from Medicaid provider networks has long been a priority of some Republican lawmakers and conservative organizations and is reiterated by Project 2025.

Contraceptive Coverage and the ACA

Private insurance coverage for contraceptives and other evidence-based preventive services such as cancer screenings and prenatal care is required under the ACA and has been championed and expanded by the Biden-Harris Administration. While President, Trump issued regulations that expanded facilitated employer claims to an exemption from the contraceptive coverage requirement, allowing employers with religious or moral objections to completely exclude contraceptives from their employee health plans.

The outcome of a pending federal lawsuit, Braidwood Management Inc v Becerra, which specifically challenges the ACA preventive services requirements, could put contraceptive coverage at risk. The Biden-Harris Administration is defending the ACA requirement and fighting the case. Former President Trump has not publicly voiced an opinion on the case, but Project 2025 calls for the federal government to issue new requirements for contraceptives and other women’s preventive services because of the pending case.

In recent years, there has been increased awareness and attention to the poor state of maternal health in the U.S., particularly stark racial and ethnic disparities in mortality and morbidity, as well as limited access and coverage for fertility assistance, particularly in vitro fertilization (IVF), under private insurance and Medicaid. While in the Senate and as Vice President, Harris has been a champion on improving maternal health, with a particular focus on eliminating persistent racial and ethnic disparities. Recently, has called for insurance coverage of IVF.

Equity, Quality, and Access to Care

Vice President Harris has a history of advocating for improvements in maternal health and care. As Senator, she sponsored the MOMNIBUS, a package of bills aimed at improving quality of and access to maternity care. After becoming Vice President, the American Rescue Plan Act (ARPA) of 2021, which the Administration supported, allowed states to extend postpartum coverage under Medicaid from 60 days to 12 months. Since it took effect, nearly all states have adopted the extension.

The Biden-Harris Administration has also taken other actions, including the launch of a maternal mental health hotline and a new Medicaid payment model for better coordinated maternity homes. Their Maternal Health Blueprint presents future priorities, such as coverage for a broader range of services, improving data collection, diversifying the maternity workforce (including with midwives and doulas), and improving treatment of pregnant people, particularly communities of color.

Trump also issued a maternal health plan near the end of his term that called for action on many of the same issues, including more research and technological investments in maternal health. The former President signed federal legislation that provided funding for maternal mortality review committees. The Project 2025 document supports broader access to doulas, as long as no federal funds support training related to abortion care.

Fertility Assistance and IVF

In February 2024, the Alabama Supreme Court ruled that embryos created through in vitro fertilization (IVF) are “unborn children” under the state’s law. Since the state court’s ruling, both Vice President Harris and former President Trump have expressed their support for IVF care. Trump has also said that if elected, his administration would provide access to full coverage of IVF services by requiring insurance companies or the government to pay, but he has not provided any details on how this would be funded or operationalized.

Both party platforms express support for IVF, however the Republican platform also invokes the 14th Amendment, which can be used to promote fetal personhood policies that could threaten and criminalize IVF care. Additionally, the Project 2025 authors refer to embryos as “aborted children” and oppose research using embryonic stem cells (which can be derived from the IVF process). Senators in both parties introduced federal legislation related to IVF. The Democratic-sponsored proposal would have established a federal right to IVF as well as other fertility assistance services, while the Republican-backed bill would have prohibited states from banning IVF care. Both bills failed to pass.

Paid Leave

Despite strongpublicsupport, the U.S. is one of the few industrialized nations that does not have national requirements for paid family leave for most workers. Vice President Harris supports guaranteeing 12 weeks of paid leave for new parents, caregivers, cases of domestic violence, or military deployment. The Republican Party platform does not address paid leave. During former President Trump’s time in office, he signed the 2020 National Defense Authorization Act, which provided 12 weeks paid parental leave to federal employees for the birth or arrival of a child.

National health spending totaled $4.5 trillion in 2022—17% of gross domestic product (GDP)—and is projected to grow faster than GDP through 2032, contributing to higher costs for families, employers, states, and the federal government. As policymakers consider a variety of strategies to make health care more affordable, they have been increasingly attentive to the effects of consolidation in health care markets and the potential implications for cost and quality of care. Hospital consolidation has been a subject of particular focus in part because nearly one third of all health spending goes towards hospital care. Consolidation may allow providers to operate more efficiently and help struggling providers keep their doors open in underserved areas, but often reduces competition. A substantial body of evidence has found that consolidation can contribute to higher prices, with unclear effects on quality.

This analysis examines the competitiveness of markets for hospital care, based on RAND Hospital Data—a cleaned and processed version of cost reports from Medicare-certified hospitals—and American Hospital Association (AHA) survey data. This piece describes competition among independent hospitals and health systems, referring to both as “health systems” throughout for brevity. Competition is measured in three ways: the share of metropolitan statistical areas (MSAs) controlled by a small number of health systems, the level of market concentration in MSAs based on the Herfindahl-Hirschman Index (HHI), and the share of hospitals affiliated with health systems over time. Using hospital data from 2022 (the most recent year available), this analysis focuses on general short-term or general medical or surgical hospitals depending on the dataset and excludes federal hospitals (see Methods for more details).

Key Takeaways

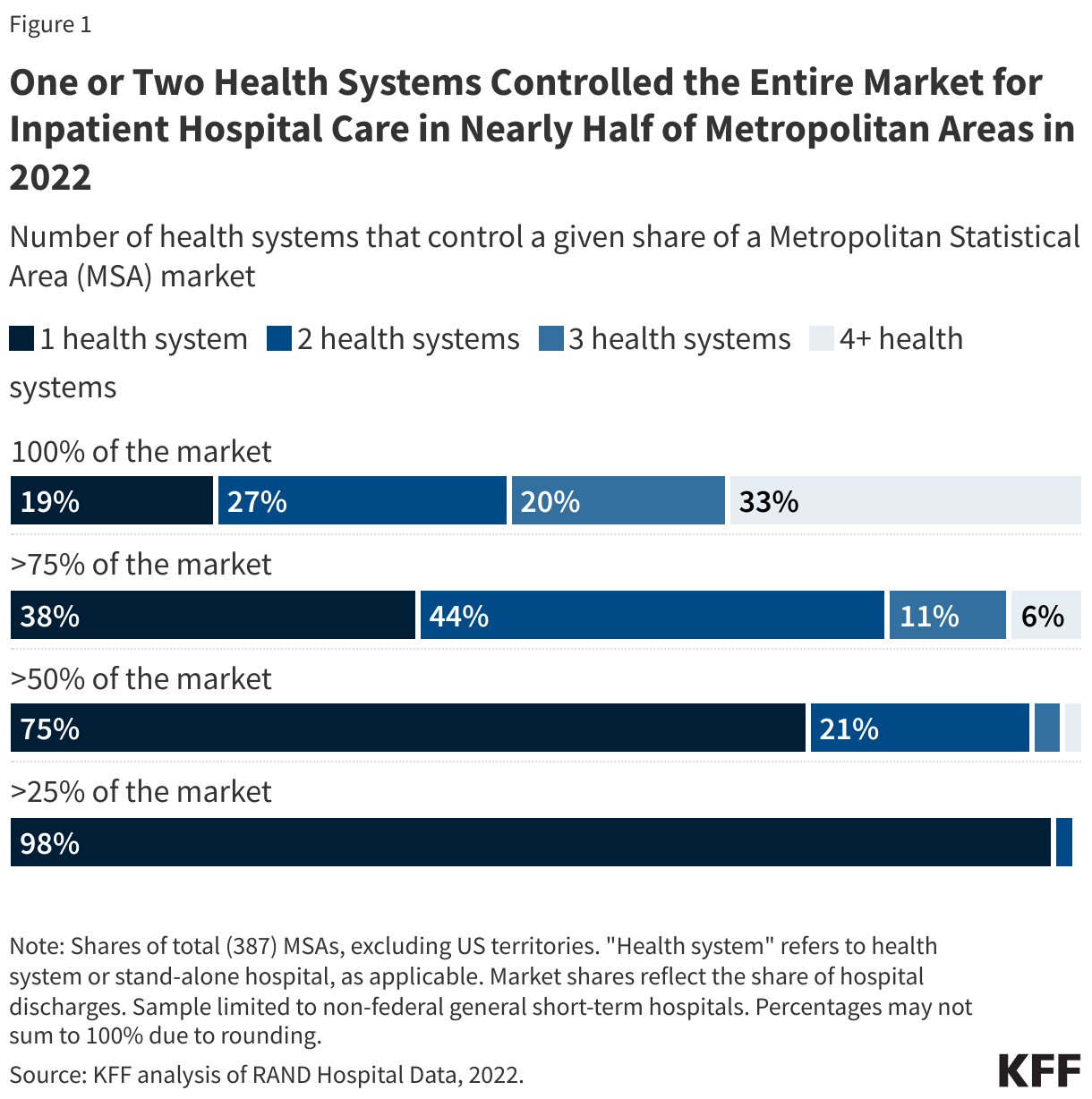

One or two health systems controlled the entire market for inpatient hospital care in nearly half (47%) of metropolitan areas in 2022.

In more than four of five metropolitan areas (82%), one or two health systems controlled more than 75 percent of the market.

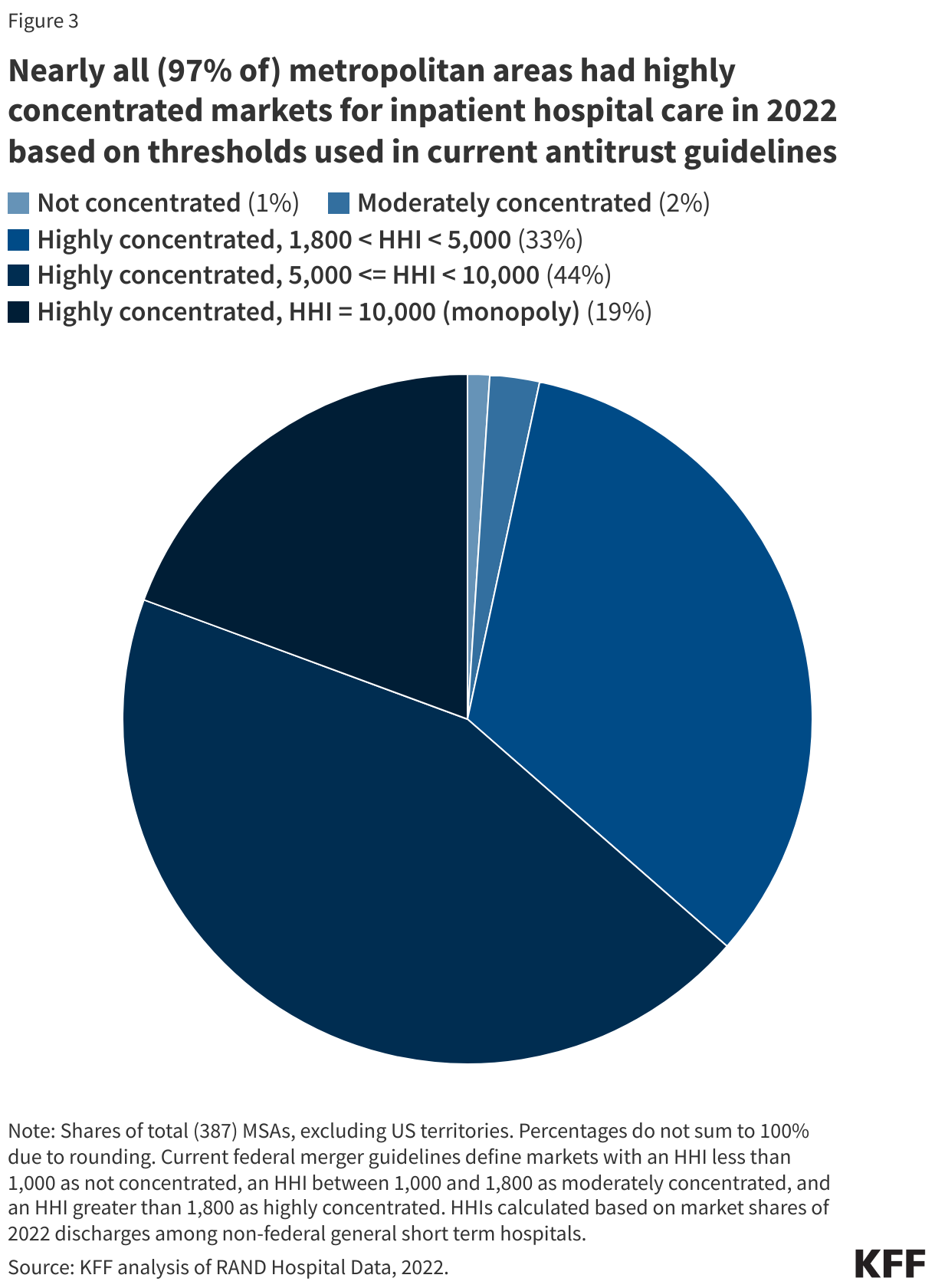

Nearly all (97% of) metropolitan areas had highly concentrated markets for inpatient hospital care when applying HHI thresholds from antitrust guidelines to MSAs.

One or Two Health Systems Controlled the Entire Market for Inpatient Hospital Care in Nearly Half (47%) of Metropolitan Areas in 2022

Nearly one in five (19%) metropolitan statistical areas (MSAs) were controlled by a single health system, and more than one in four (27%) markets were controlled by two systems in 2022 (see Figure 1). In more than four of five metropolitan areas (82%), one or two health systems controlled more than 75 percent of the market. These markets all met the definition of highly concentrated markets based on thresholds in current antitrust guidelines (see below). One health system controlled at least half of the market in three out of four MSAs (75%) and at least a quarter of the market in nearly every MSA (98%).

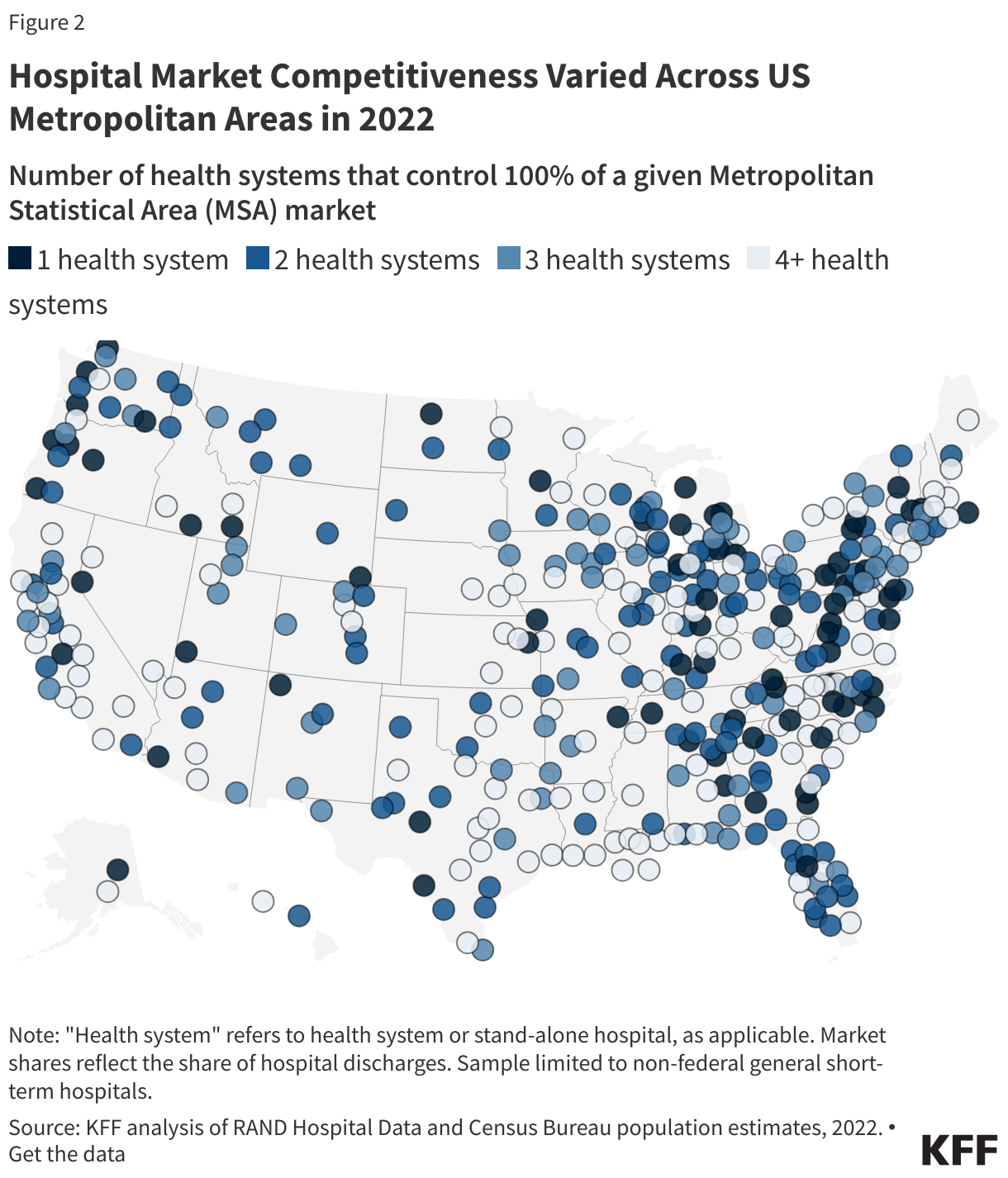

The number of health systems in a given MSA tends to increase with the population of the region. For example, in 79% of MSAs with a population of less than 200,000, one or two health systems controlled the entire market for inpatient hospital care in 2022, as in the Muncie, IN; Napa, CA; and Amherst Town-Northampton, MA MSAs (Figure 2). MSAs with one or two health systems account for nearly half (47%) of all MSAs but 12% of the U.S. population living in metropolitan areas.

Conversely, virtually all (53 of 54) MSAs with a population of at least one million people had at least four health systems, as in the MSAs encompassing Detroit, Miami, and Phoenix. MSAs with four or more health systems accounted for 35% of all MSAs but 79% of the U.S. population living in metropolitan areas.

However, in nine of these relatively large MSAs with four or more health systems, the two largest health systems controlled at least 75% of the market, and in 37 of these areas, they controlled at least 50% of the market. For example, in the MSA encompassing Austin, TX, with 2.4 million residents, two systems (HCA Healthcare and Ascension Health) controlled 85% of the inpatient hospital care market, though Austin is home to more than four health systems. The metropolitan area encompassing Portland, OR, with 2.5 million residents and more than four health systems, is a less concentrated market than Austin’s, but the two largest systems (Legacy Health and Providence) still control a combined 56% of the market. (See Methods for discussion about MSAs as geographic hospital markets).

Nearly all (97% of) metropolitan areas had highly concentrated markets for inpatient hospital care in 2022 based on thresholds used in current antitrust guidelines

Another way to assess market competitiveness is to evaluate a measure of concentration known as the Herfindahl-Hirschman Index (HHI), which is based on the number of participants in a market and their respective shares. The measure runs from 0 (perfectly competitive) to 10,000 (monopoly market). Based on current merger guidelines from the Federal Trade Commission (FTC) and Department of Justice (DOJ), markets can be grouped into three categories: not concentrated (HHI < 1,000), moderately concentrated (1,000 – 1,800), and highly concentrated (HHI > 1,800). This analysis calculates HHIs for MSAs and groups these regions accordingly, though there are other ways of defining the boundaries of hospital markets (see Methods).

Nearly all (97% of) MSAs had highly concentrated markets for inpatient hospital care in 2022 based on thresholds used in current merger guidelines (Figure 3). These guidelines reflect updates in 2023 that lowered the HHI thresholds for moderately concentrated and highly concentrated markets. Based on the thresholds used in prior guidelines, a large majority but somewhat smaller share (93%) of MSAs were highly concentrated markets for inpatient hospital care in 2022, closer to an estimate from an earlier study (90%) that used data from 2016.

As was the case when looking at counts of health systems in MSAs, larger metropolitan areas tended to be less concentrated and more competitive than less populated metropolitan areas, although this was not always the case. All 13 MSAs that were identified as either not concentrated or moderately concentrated had more than one million residents, such as the MSAs encompassing Cincinnati, Oklahoma City, and Miami. However, 41 MSAs with more than one million residents—including the MSAs encompassing Houston, Denver, and Atlanta—had highly concentrated hospital markets. Overall, 70% of people living in metropolitan areas lived in highly concentrated hospital markets.

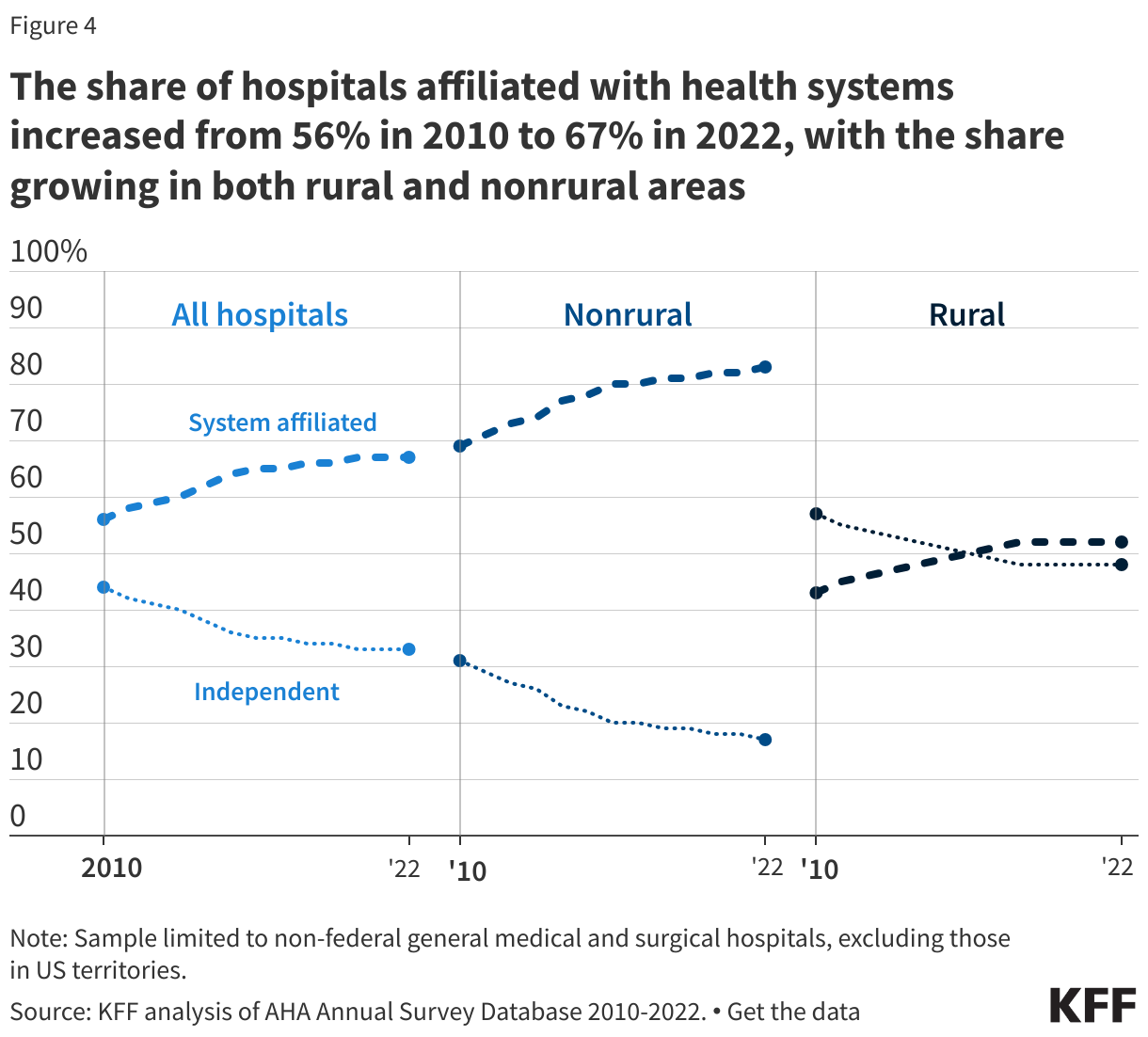

The share of hospitals affiliated with health systems increased from 56% in 2010 to 67% in 2022, with the share growing in both rural and nonrural areas

About two thirds of hospitals (67%) are now part of a larger system, an increase from 56% in 2010 (Figure 4). A smaller share of rural than nonrural hospitals were part of a health system in 2022 (52% versus 83%), though shares have increased over time for both rural and nonrural regions: from 43% in 2010 to 52% in 2022 among rural hospitals and from 69% in 2010 to 83% in 2022 among nonrural hospitals.

Most system-affiliated hospitals in 2022 (53%) were part of a system with at least 15 hospitals, and 22% were in a system with at least 50 hospitals. Systems with at least 100 hospitals accounted for 13% of system-affiliated hospitals.

Hospitals joining larger systems may not always reduce local market competition, for example, if an independent hospital is acquired by a larger system that does not own facilities in the same market. However, mergers between hospitals that operate in different geographic markets for patient care—also known as “cross-market” mergers—may nonetheless lead to higher prices in some cases.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Methods

Analyses of market shares and HHI (e.g., Figures 1 through 3) were based on RAND Hospital Data. RAND Hospital Data are a cleaned and processed version of annual cost reports that Medicare-certified hospitals are required to submit to the federal government. Although limited to Medicare-certified hospitals, in 2022, our analysis of RAND data included the vast majority (97%) of non-federal general medical and surgical hospitals in US metropolitan areas included in our analysis of the AHA Annual Survey Database (see below). Cost reports were assigned to years based on the end of the reporting period and were scaled up or down to reflect a 365-day period, as necessary.

Analyses of market shares and HHI were restricted to non-federal, general short-term hospitals. Market shares were calculated as the share of inpatient discharges in an MSA that occurred within a given health system or independent hospital. One percent of hospitals that met our other sample restrictions had missing values for inpatient discharges and were excluded. Hospitals were grouped into health systems, as applicable, based on the 2022 AHRQ Compendium of US Health Systems. MSAs reflect 2023 geographic definitions from the Census Bureau calculated based on data from the 2020 decennial census. HHIs were calculated as the sum of squared market shares for all health systems in a given MSA (e.g., an MSA divided evenly between two systems would have an HHI of 502 + 502 = 5,000). We obtained 2022 MSA population estimates from the Census Bureau.

We used MSAs as a proxy for hospital markets, which is one approach used by other studies summarizing hospital market competition across the country. There are other ways of defining markets that would yield different results when calculating the level of competition. For example, one relatively recent report also evaluated MSAs but focused on where residents received their care, including at hospitals outside of a given MSA. As another example, some have defined markets based on Hospital Referral Regions (HRRs) and USDA Commuting Zones. More precise market definitions, such as those used to define competition in antitrust cases, were not feasible. This study did not exclude MSAs with populations of at least three million as some others have done, because the analysis sought to describe competition across all metropolitan areas.

Analyses of the share of hospitals affiliated with systems are based on the AHA Annual Survey Database, which includes its own measure of system affiliation. We restricted this analysis to nonfederal, general medical and surgical hospitals. Hospitals were designated as rural if they were located in a ZIP code that is eligible for Rural Health Grants through the Federal Office of Rural Health Programs.