KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

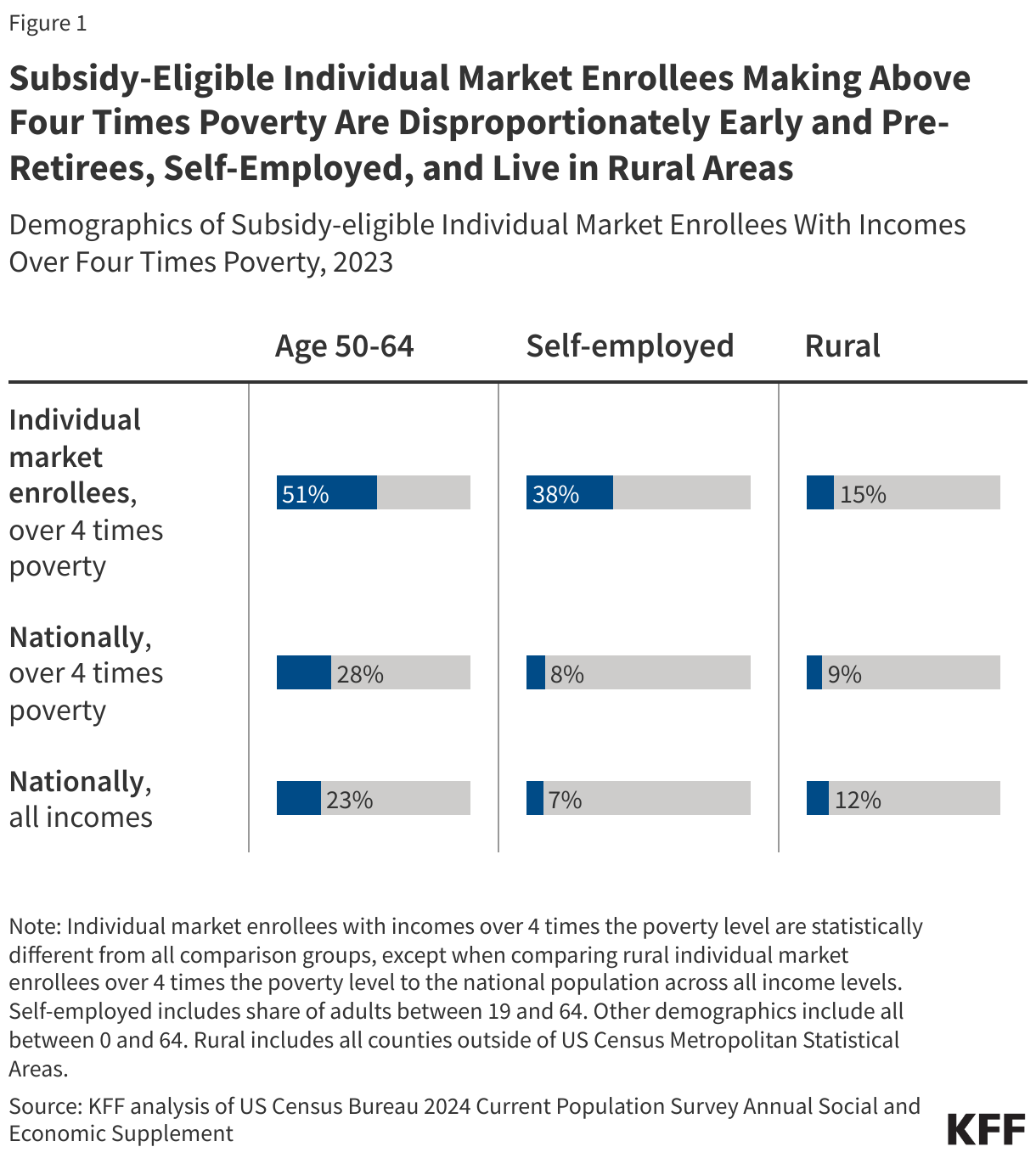

Enhanced subsidies for Affordable Care Act (ACA) Marketplace plans are set to expire at the end of 2025, unless they are renewed by Congress. Since 2021, these enhanced subsidies have lowered monthly premium payments for the vast majority of Marketplace enrollees, across incomes. For example, instead of a lower-income person paying 2% of their income on their premium, they pay nothing. Higher income people currently pay no more than 8.5% of their income on their premium, whereas they were originally ineligible for financial assistance.

While virtually all subsidized ACA enrollees can expect to see their premium payments rise substantially without extension of these subsidies, most will still be eligible for some financial assistance (with the original ACA subsidies). However, those who earn more than four times the federal poverty level ($62,600 for an individual or $128,600 for a family of four with 2026 coverage) would lose eligibility for subsidies altogether and would therefore have to pay full price for their health plans. Based on 2025 premiums, for example, a 60-year-old couple earning $85,000 annually (416% of the federal poverty level in the contiguous 48 states), would see their monthly premium payment increase by $1,507 per month (an increase in payments of over $18,000 for the year), on average.

Relative to other Americans, subsidy-eligible individual market enrollees with incomes over four times poverty (who would lose subsidy eligibility if enhanced tax credits expire) are disproportionately:

Early and pre-retirees: About half (51%) of enrollees with incomes over four times poverty who would lose subsidy eligibility are between the ages of 50 and 64, compared to 23% of the non-elderly U.S. population.

Self-employed: Among non-elderly adults (ages 19 to 64) with incomes over four times poverty who would lose ACA subsidy eligibility, 38% are self-employed, compared to 7% of non-elderly adults (19-64) nationally. Small business owners often rely on the ACA Marketplaces because they do not have employer-sponsored insurance.

Living in rural areas: 15% of people with individual market insurance who would lose subsidy eligibility live outside metropolitan areas, compared to 9% of Americans with incomes over four times poverty. (12% of all Americans live in rural area; this is not statistically different from the share of people who would lose subsidy eligibility living in rural areas.)

Relatively few Marketplace enrollees have incomes above four times poverty. According to administrative data, in 2024, 7% of Marketplace enrollees reported an income over four times poverty, with 3% having an income between four and five times poverty and another 4% with incomes over five times poverty (another 4% did not have a known income and may have also exceeded four times the poverty level, but most likely are not receiving an advanced premium tax credit). However, before the enhanced subsidies were introduced – and particularly in 2017 when there were large premium increases and debates about repealing the ACA – this group of people with incomes over four times poverty were the focus of a great deal of media attention because they were fully exposed to the underlying premiums. For those who were priced out of coverage before the enhanced subsidies, they often faced a choice of being uninsured, or – if they were healthy enough to qualify – buying a short-term (non-ACA-compliant) plan off of the Marketplace.

Note: The data above is based on KFF analysis of the 2024 Current Population Survey Annual Social and Economic Supplement. The analysis includes people under age 65 who buy individual market insurance, are subsidy eligible, and would receive a subsidy based on household income. Household offer units were imputed as described previously; enrollees were considered not subsidy eligible if a member of the unit reported being offered employer-sponsored insurance.

The U.S. health insurance system has become a “complex labyrinth” for consumers to understand and navigate. Whether public or private coverage, the information needed and the hoops the average health care consumer must go through to use their health coverage effectively is itself a public policy concern, exacerbating continued access and affordability challenges. The KFF 2023 Survey of Consumer Experiences with Health Insurance found that half of insured adults have some difficulty understanding at least some aspects of their insurance. This is the first of two Issue Briefs exploring specific survey findings about gaps in understanding health coverage, highlighting problems and federal consumer protections in place today designed to bridge the gap.

This brief discusses how consumers understand what their insurance covers, what to do when coverage for care is denied, and what protections exist to ensure that information is available and coverage determinations are fair, accurate, and timely. The second brief will discuss survey findings of consumer understanding of the cost of their coverage, existing consumer protections designed to assist with understanding how much they will have to pay for a covered service, and balanced billing and other federal consumer health insurance protections.

The Labyrinth

What does a consumer need to know in order to use their health coverage effectively? The U.S. insurance system of managed care networks, utilization review, and changing coverage options can result in a complicated maze for a patient to navigate on their own. Federal and state policymakers have developed a series of incremental reforms to address understanding and transparency for consumers, but these can differ considerably based on the type of coverage, the plan the consumer chooses (if they have a choice), and sometimes, the state where they live. For private coverage in particular, the current regulatory framework is a complicated system of overlapping state and federal standards, sometimes leaving consumers to sort through a barrage of questions in order to get the care they thought was covered by their insurance.

KFF Consumer Survey Findings

The KFF 2023 Survey of Consumer Experiences with Health Insurance (“Consumer Survey”) included a nationally representative sample of 3,605 U.S. adults ages 18 and older with health insurance. The survey asked consumers about their experiences with their health insurance, including questions regarding how well enrollees understood what was covered, insurance problems that arose when enrollees tried to use their insurance, and where they sought help when they experienced insurance problems.

Understanding What is Covered

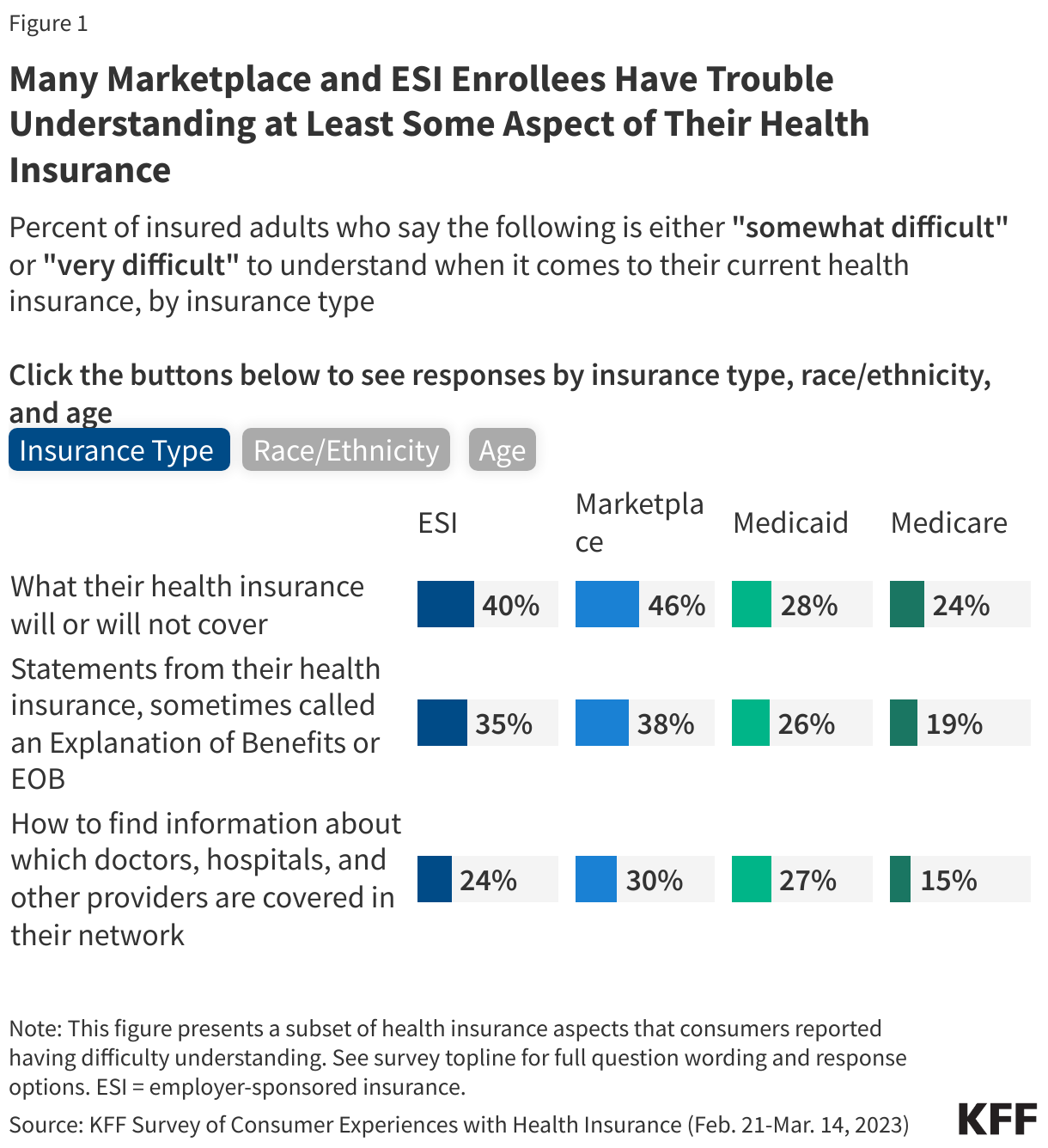

According to the 2023 KFF Consumer Survey, more than one-third (36%) of all insured adults said it was somewhat or very difficult for them to understand what their insurance will and will not cover. These shares vary by insurance type, with larger shares of those with Affordable Care Act (ACA) Marketplace plans (46%) and employer-sponsored plans (40%) reporting greater difficulty than those with Medicaid (28%) or Medicare (24%) (Figure 1). There were also differences in understanding certain aspects of insurance by demographic characteristics. Hispanic (36%) and White (36%) insured adults were more likely than insured Black adults (26%) to say it is somewhat or very difficult to understand what their insurance will and will not cover. Among insured adults, Hispanic adults (37%) were more likely than their Black (24%) and White (29%) counterparts to say it is at least somewhat difficult to understand their Explanation of Benefits (EOB). (An EOB is a written statement from a health insurance plan explaining what costs it will cover for medical care an enrollee has received and what the enrollee must pay, though it is not a bill). While the precise explanation for these demographic differences is not clear from the survey data, these trends are similar to those found in otherresearch that noted health insurance literacy challenges across consumers generally, but found racial and ethnic disparities. Additionally, about three in ten insured adults ages 18-29 (30%) and 30-49 (28%) found it somewhat or very difficult to understand how to find information about which doctors, hospitals, and other providers are covered in their plan’s network, compared to 13% of insured adults ages 65 and older. (For the full list of consumer items asked about in this question, see the survey toplines.)

Educational attainment does not necessarily explain lack of understanding. The KFF Consumer Survey found that a slightly higher share of college graduates (58%) had difficulty understanding some aspect of their health insurance coverage than those without a college degree (46%). College graduates (43%) were more likely to report that it was somewhat or very difficult to understand what their health insurance will or will not cover compared to those without a college degree (31%). It is not entirely clear why education does not seem to increase understanding of insurance, though one possible explanation is that those with higher educational attainment are more likely to have private insurance (employer-sponsored insurance or Marketplace), with variable and changing insurance designs that may be more difficult to understand generally.

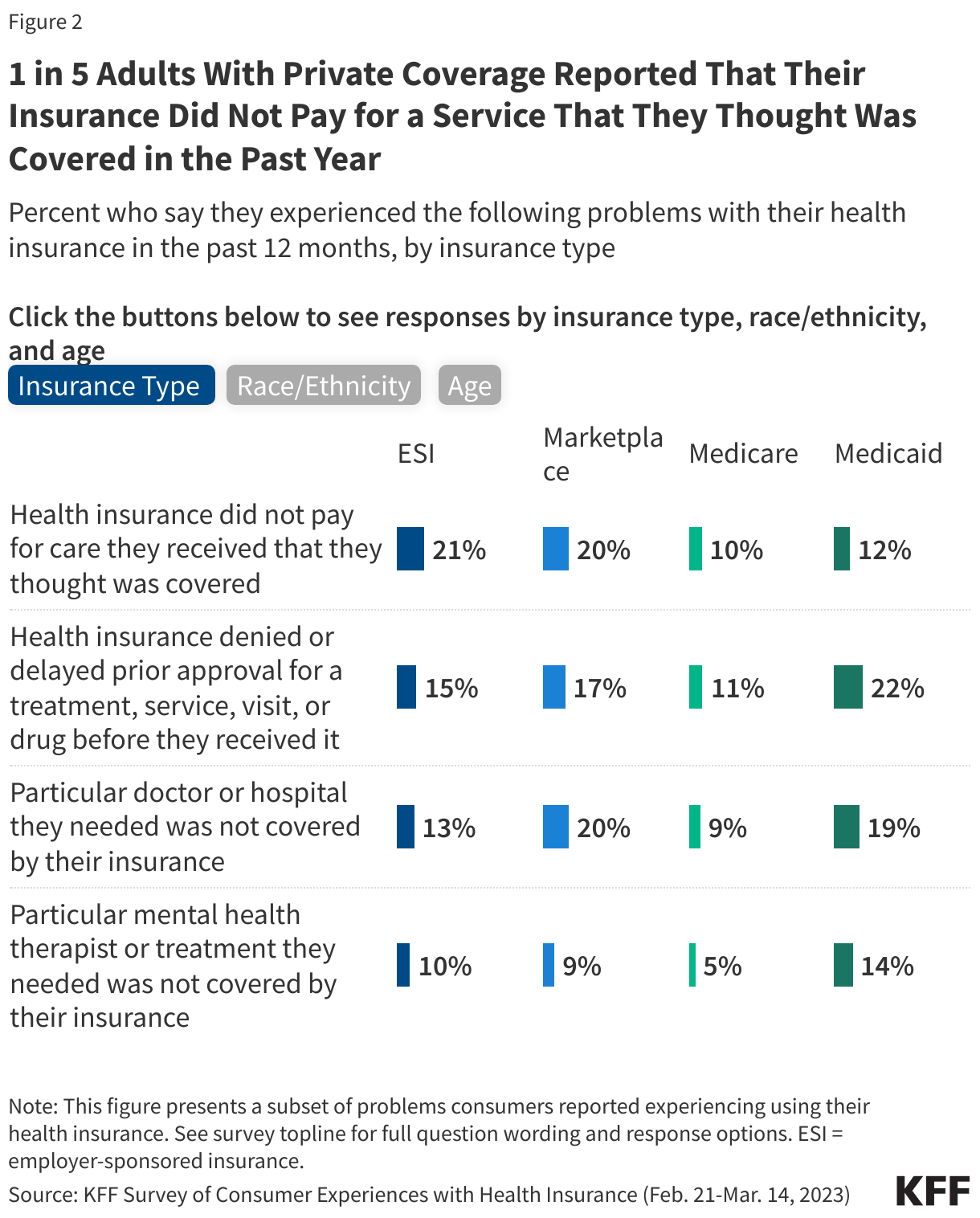

Areas where consumers note trouble with understanding insurance are often consistent with the top problems that consumers face with insurance. About six in ten (58%) insured adults reported experiencing a problem with their health insurance in the past year. This share is even higher (78%) among high utilizers of health care – those who had more than ten visits with a health care provider in the past year. While having a problem with health insurance does not necessarily indicate that a consumer had trouble understanding their insurance, determining what services are covered and what providers are in-network are items that cut across both topics. Several survey respondents reported problems related to using insurance that involved services or providers not covered by their plan. For example, 18% of insured adults indicated that their health insurance did not pay for a service that they thought was covered. Those with employer-sponsored (21%) and Marketplace (20%) coverage were more likely to report having this problem than those with Medicaid (12%) or Medicare (10%) (Figure 2). A somewhat larger share of insured Black (17%) and Hispanic (16%) adults reported that a doctor or hospital they needed was not covered by their insurance in the past 12 months compared to White adults (12%). Marketplace (20%) and Medicaid (19%) enrollees were more likely to encounter this problem than those with Medicare (9%) or employer-sponsored insurance (ESI) (13%). One in five (20%) insured adults ages 30-64 reported their health insurance denied or delayed a prior approval request in the past 12 months, relative to 11% of those ages 18-29 (11%) and 9% of those age 65 and older. (For the full list of consumer problems asked about in this question, see the survey toplines.)

Knowing Where To Go For Help

What actions, if any, consumers take when they encounter a problem with their health insurance might be instructive in addressing barriers to understanding coverage or best practices to assist consumers in navigating coverage questions.

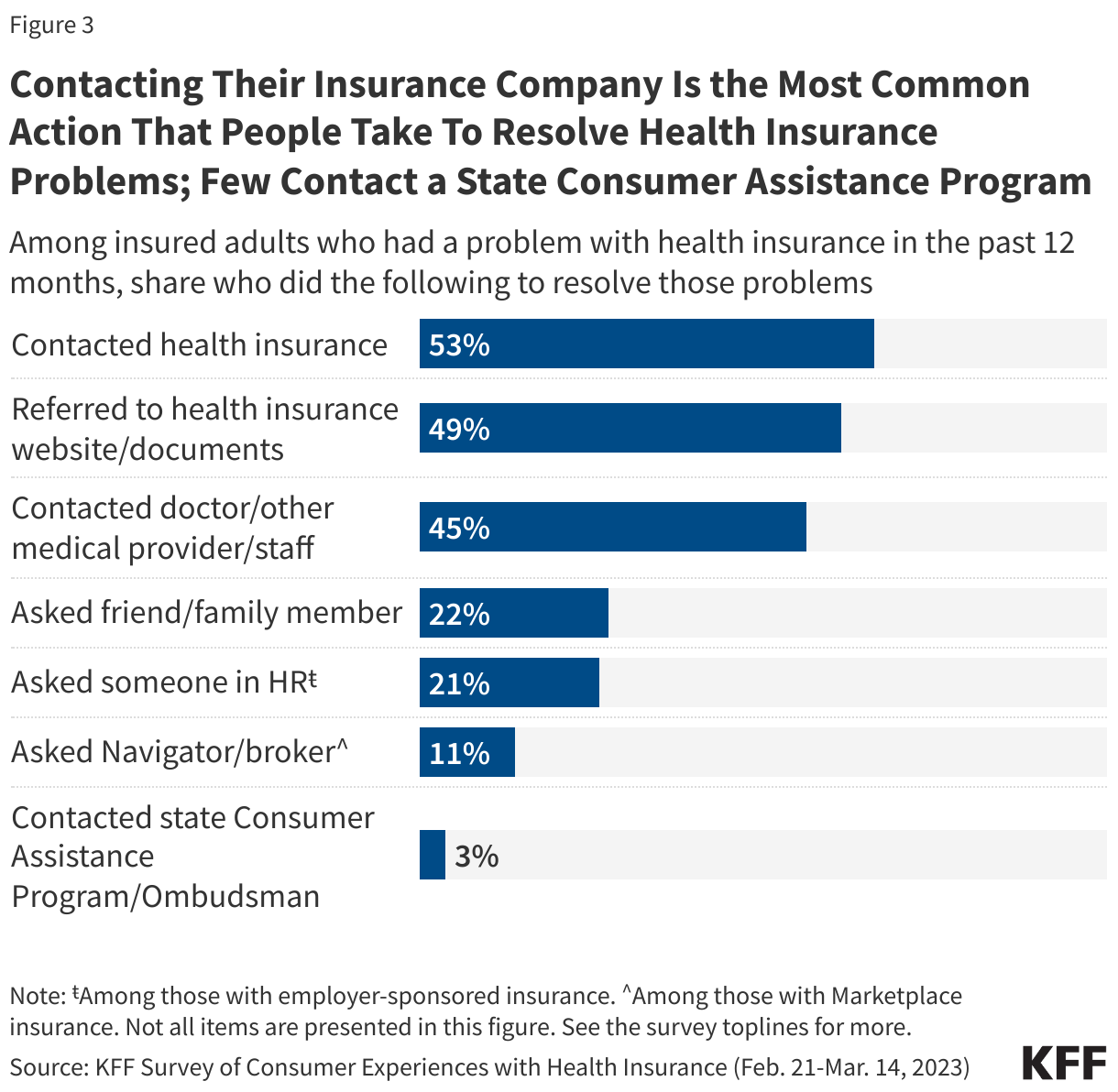

Among the nearly six in ten insured adults who reported experiencing problems with their health insurance in the past 12 months, more than half (53%) said they contacted their health insurance company to resolve the problem(s) (Figure 3). A similar share (49%) said that they referred to their health insurance website or documents. Fewer said they asked a Navigator or broker for help (11%) or contacted their state Consumer Assistance Program or Ombudsman (3%).

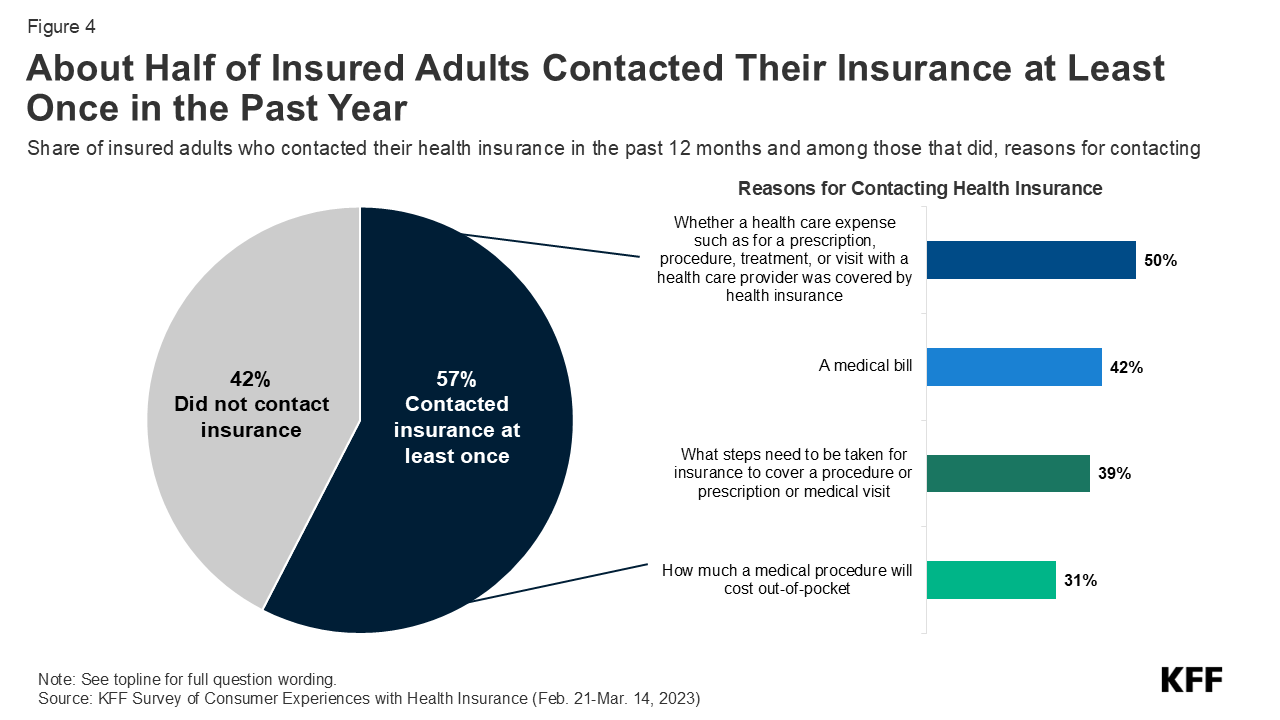

Nearly three in five (57%) of all insured adults reported contacting their insurance at least once in the past 12 months, either by phone, online, in-person, or in writing(Figure 4). Forty-two percent of insured adults did not contact their insurance company at all. Among those who did reach out to their insurance at least once, half (50%) inquired whether a health care expense (such as a prescription, procedure, treatment, or visit with a health care provider) was covered by their health insurance, making it the most common reason for contacting their insurance. Receiving a medical bill (42%) was another reason insured adults contacted their insurance, followed closely by finding out what steps needed to be taken for their insurance to cover a prescription, procedure, or medical visit (39%). Fewer (31%) contacted their insurance at least once in the past year to find out how much a medical procedure would cost out-of-pocket.

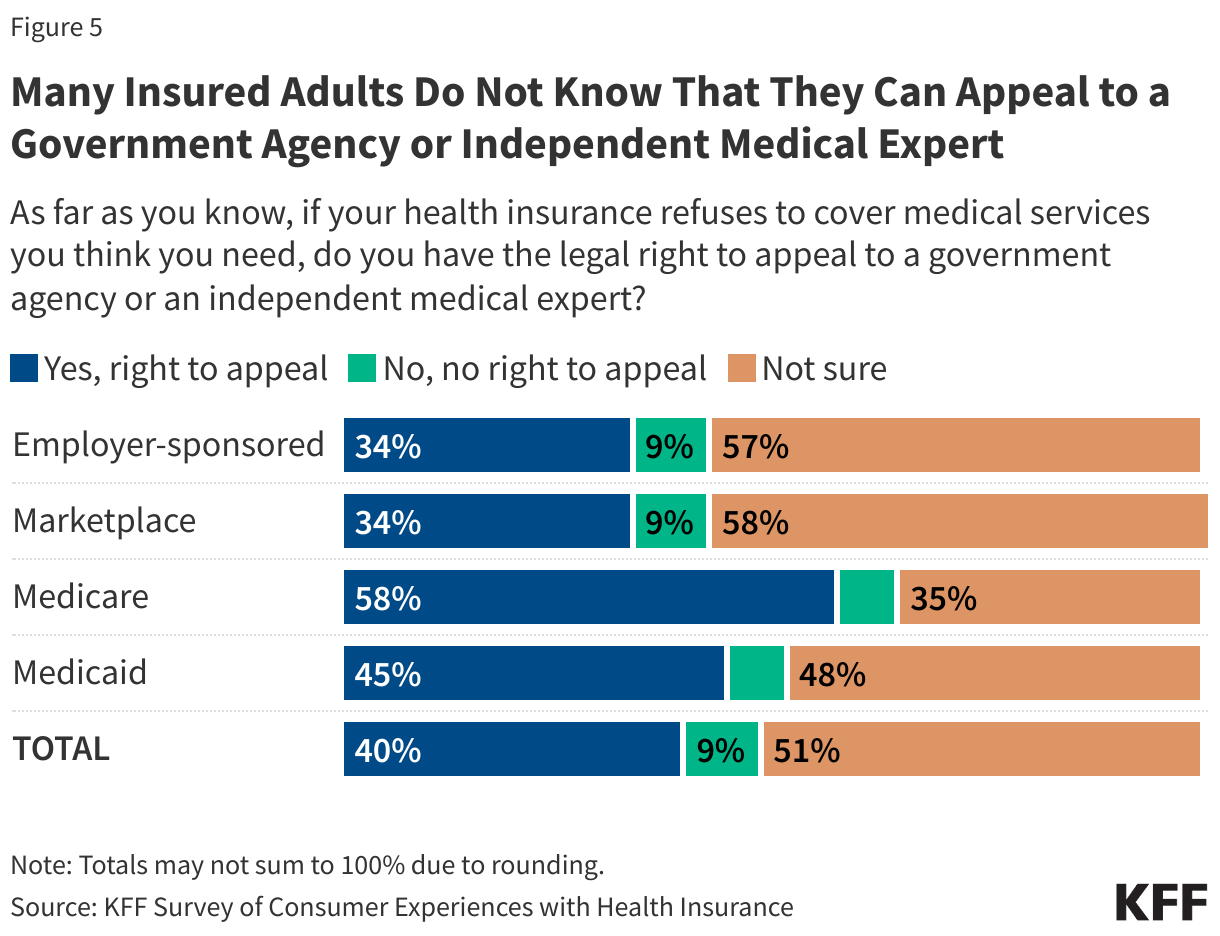

Most insured adults are unaware that they have the legal right to appeal to a government agency or independent medical expert if their health insurance refuses to cover needed medical services(Figure 5). Those with public insurance are more likely than those with private insurance to be aware of this right. Just one-third (34%) of those with ESI or Marketplace coverage know they have this right, compared to 58% of Medicare beneficiaries and 45% of those with Medicaid. Further, just one in ten (10%) insured adults who experienced a problem with their health insurance in the past year filed a complaint with their health insurance company (data not shown). This share is similar across all four coverage types.

Three-quarters (76%) of adults with insurance reported not knowing what government agency they would call for help if they wanted to. Adults with ESI (83%) or Marketplace (81%) coverage were more likely to report that they did not know which government agency to contact compared to Medicare (61%) and Medicaid (70%) enrollees. Among insured adults with ESI or Marketplace coverage who reported that they did know which government agency they would contact, 15% of those with ESI and 6% of those with Marketplace coverage reported that they would reach out to their state insurance department/commission(er), the lead agency that is responsible for regulating non-group health coverage and insured group coverage. No one reported that they would contact the Department of Labor (DOL), the government agency that regulates health plans sponsored by private employers, including self-insured employer health plans.

Federal Consumer Protections Seek to Address Barriers to Understanding Coverage

Many federal reforms have focused on providing consumers with better information about their plan, standardizing and simplifying information, and making sure notice is provided of key design features and reforms. While public programs such as Medicare and Medicaid also provide consumer protections, this section focuses primarily on federal protections for those with private health insurance coverage (individual and employer-sponsored).

Understanding What is Covered

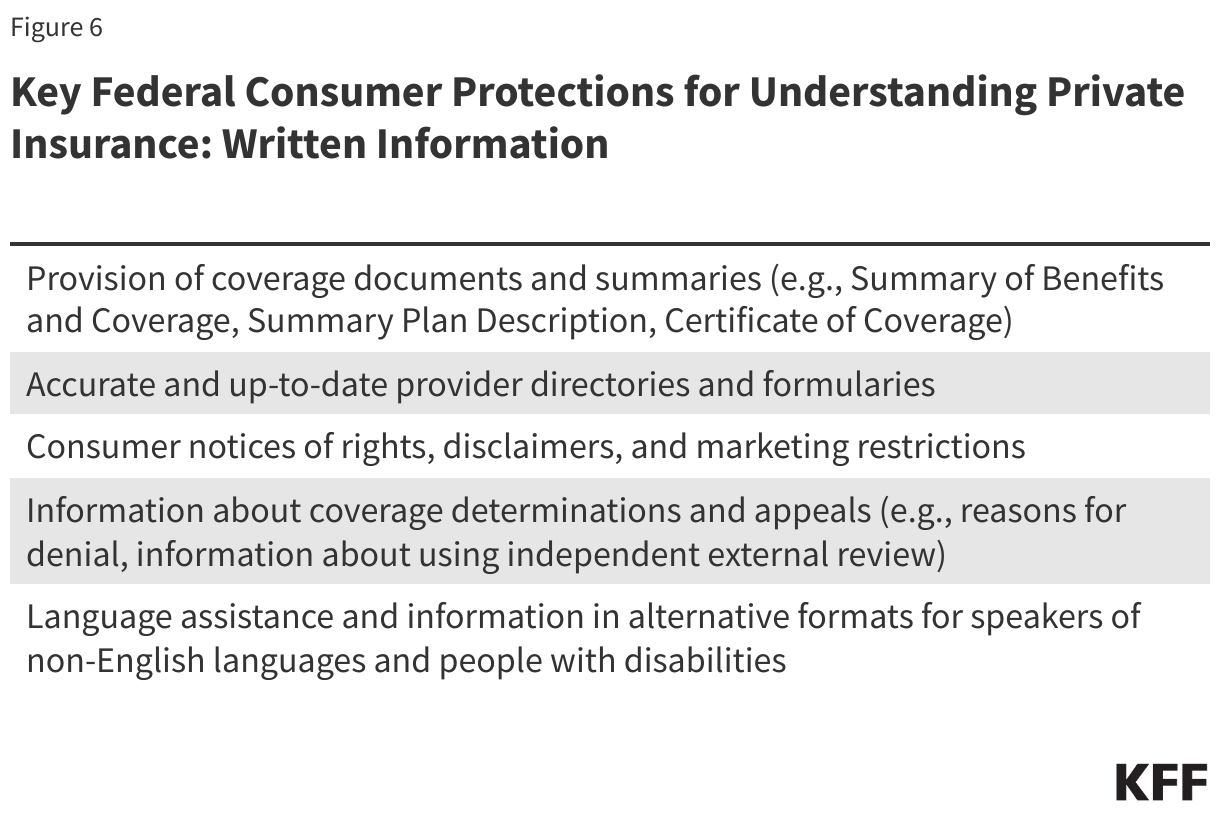

The ability to access accurate and easy-to-understand written information has long been a core consumer protection. Below is the landscape of written materials a consumer can access to get information to understand their coverage. Figure 6 is a snapshot of some key consumer protections for those with private insurance.

Coverage documents and summaries: All forms of coverage, whether Medicare, Medicaid, or private insurance available through an employer or a health insurance Marketplace, are required as a form of consumer protection to provide information about benefits and coverage, with varying content requirements, formats, and frequency of updates. Although there are fewer required standardized information formats across private coverage than in public programs such as Medicare, the ACA ushered in a standardized template across most private insurance through the Summary of Benefits and Coverage (SBC), with information on key coverage items and exclusions, cost-sharing, and rules for accessing care. All ACA-compliant plans in the individual and group insurance market and all employer-sponsored plans must provide consumers with an SBC.

More detailed coverage documents can extend to one hundred written pages or more; however, electronic formats and machine-readable files may make it easier to access information for those with the technology and ability to research this information. Examples in the private insurance market include state-regulated insurance documents (including Marketplace plans) sometimes called Certificates of Coverage, or plan documents and Summary Plan Descriptions that set out benefits for those in employer group health plans covered by ERISA.

Provider directories and formularies: Provider directories and formularies allow consumers to see what providers and medications are covered by their insurance. While these items might be easy to access online, severalresearchstudies have found that provider directories are often inaccurate. Federal consumer protections across public and private coverage include various features designed to ensure that plans maintain more accurate and up-to-date information. In some cases, these protections also require plans to meet minimum network adequacy standards and test that accuracy through “secret shopper” compliance programs.

Private coverage protections include the No Surprises Act (NSA) requirements, which apply to all private insurance (including employer coverage) and set standards for both plans and in-network providers to ensure accurate provider directory information. Consumers must be reimbursed for cost sharing in excess of in-network amounts when they rely on inaccurate directory information indicating that a provider was in-network. Plans must also continue to cover care from certain providers for a limited period of time after they leave an insurance network.

There is little research on prescription drug formulary accuracy and how consumers determine what medications are covered, but some public programs have model formulary templates to make it easier for consumers to review. There are no federal standards for private employer plans for formulary format, accuracy, and usability.

Consumer notice of rights, disclaimers, and marketing restrictions: Nearly every new consumer protection includes a requirement on an employer or insurance plan and/or provider to notify patients that the protection exists. For example, the NSA requires providers and facilities, as well as plans, to provide patients with information about the NSA’s balanced billing protections. Other federal reforms are meant to alert consumers about aspects of their coverage that might easily be misunderstood with a clear warning or disclaimer. For instance, federal rules for short-term limited duration coverage require a prominent statement that this coverage is “NOT COMPREHENSIVE COVERAGE.” This federally required warning on plan materials, as well as one for fixed indemnity plans, has been the subject of recent litigation questioning the need for and validity of these disclaimers. Another federal agency, the Federal Trade Commission, enforces protections against unfair or deceptive marketing or advertising to consumers that, for example, misrepresents certain limited coverage arrangements as comprehensive health insurance. Several recent investigations have been in collaboration with the federal health insurance agency Centers for Medicare and Medicaid Services (CMS).

Information about coverage determinations and appeals: Even if a consumer has located written information that an item, service, or provider visit is covered by their insurance, they could still face a denial of coverage (e.g., because the plan does not deem the care “medically necessary”), which can create frustrating hurdles for consumers. Medicare and Medicaid have longstanding processes for claims review and appeals. Private coverage also includes certain protections including:

Processes for reviewing claims: All private insurers and employer plans must ensure a “full and fair” review of enrollee claims. In addition, the ACA includes a “transparency in coverage” provision that requires all non-grandfathered private health plans to provide information and statistics about plan practices to the public and to federal and state agencies, including data on claims payment policies and procedures and the number of claims denied.

Prior authorization: The longstanding practice of health plans requiring patients to obtain approval for a health care service or medication before the care is provided has received renewed scrutiny in recent years. New federal protections issued in 2024 and effective in 2027 streamline the process and require aggregate reporting of the number of claims denials for federal Marketplace plans as well as Medicare Advantage and Medicaid managed care organizations.

Information about why a claim was denied: Health insurers and employer plans must clearly disclose to consumers the reason(s) their claim was denied, provide information on their right to appeal the decision, and include the name of any Consumer Assistance Program (CAP) in their state. Consumers can also request more specific information from their plan about the decision (e.g., policy provisions related to the denied claim, names of experts consulted for decision).

Internal appeal to the plan: If a consumer disagrees with a denied claim from their health plan, they can file an internal appeal with their plan. Plans are required to inform consumers of their appeal decision within 30 days for a service not yet received, within 60 days for a service that was already administered, and within 72 hours in urgent medical cases (sometimes less depending on the situation).

External independent review: Consumers whose claims denial is upheld at internal appeal may have the right to an external review by an entity independent of the plan for certain types of claims.

Language assistance and information in alternative formats: Requirements to provide some form of language assistance and auxiliary aids to help with understanding coverage exist across most forms of coverage. Private employer plans have long been required to offer assistance in a non-English language where the plan covers a specific percentage of participants in the plan who are “only literate” in the same non-English language. The ACA requires that the SBC and certain claims and appeal notices be provided in a “culturally and linguistically appropriate manner” by individual and group insurers and self-insured employer plans. This could include items such as oral language services and a notice in a certain non-English language provided to enrollees upon request if they live in a county where 10% or more of the population is literate only in the same non-English language.

Separate language access standards apply to recipients of federal financial assistance, programs that HHS administers, and entities established under the ACA, such as health insurance Marketplaces. As a result, most private insurers participating in public and private insurance programs (including some who also provide insurance or administrative services to employer-sponsored coverage) must comply.

Effective communication for individuals with disabilities is also required under the ACA. Current regulations likely extend to information about health insurance coverage through the use of “auxiliary aids” for individuals with disabilities, such as sign language interpreters onsite or by video. Electronic information technology used to provide information about health coverage to enrollees must also be accessible for individuals with disabilities unless doing so creates an undue burden or fundamentally alters the program. Similar access standards for persons with disabilities might also apply to those who sponsor coverage and are also subject to the Americans with Disabilities Act or the Rehabilitation Act.

Direct Assistance

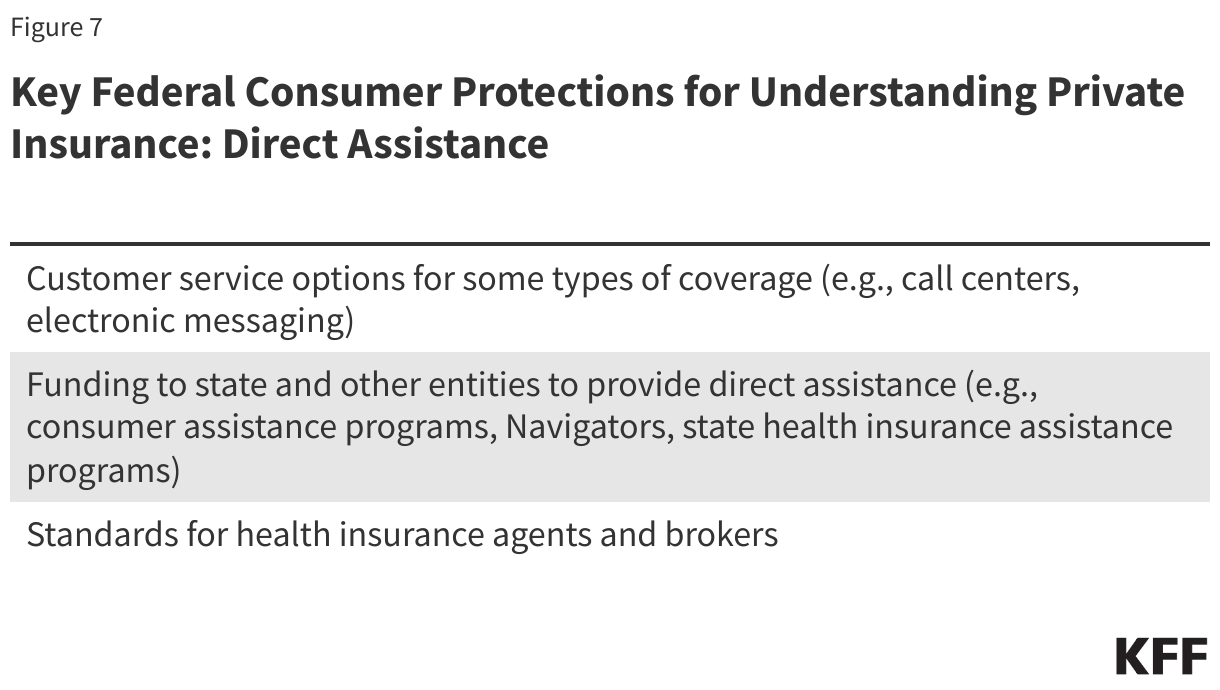

Some consumers may seek one-on-one communication to understand technical details in an insurance coverage document, to get more information about plan or provider policies and procedures, or to navigate the claims appeal process. The 2023 KFF Consumer Survey indicates that more insured adults reach out to their insurance company when encountering a problem than look to written plan material for resolution. Ensuring that consumers have access to effective and impartial one-on-one help has been the subject of federal consumer protection requirements. Figure 7 is a snapshot of key channels for direct consumer assistance.

Customer service options: Private insurers generally make certain customer services available to enrollees. Customer service provided by health plans is commonly offered via call centers, electronic messaging platforms, and increasingly, virtual chatbots. States may have specific customer service requirements for insurers selling state-regulated plans, such as call center wait time standards or staffing a minimum number of customer service representatives.

Health insurance marketplaces are required to provide consumer tools. Healthcare.gov operates a toll-free call center 24 hours a day, 7 days a week, for consumers with questions related to the federal health insurance Marketplace. The ACA also requires all state-based marketplaces to provide a live call center during their hours of operation. Call center representatives must assist consumers with inquiries related to qualified health plans, enrollment, cost-sharing reductions, and advanced premium tax credits (APTCs). Beyond relying just on insurers to provide this information, Congress also created the Navigator grant program to give enrollees access to an additional source of information from organizations other than health insurers to help navigate Marketplace coverage.

For those with private employer-sponsored coverage, there is no specific requirement under federal law to provide direct assistance to help covered employees and their families. Human resources staff sometimes perform this role if a consumer is unable to get answers from customer service personnel available from their insurer or third-party administrator. Some firms contract with third-party vendors to provide patient navigation or “concierge” services that help enrollees navigate plan services and advocate for enrollees as patients, among other services. According to the KFF Employer Health Benefits Survey, in 2024, 29% of firms with 200 or more employees that offered health benefits contracted with a vendor to provide “concierge” services to their enrollees. Separately, the DOL’s Employee Benefits Security Administration (EBSA) operates a toll-free phone number and an online message platform for consumers with questions or concerns related to federal legal requirements, obtaining health plan documents, and assistance getting claims paid.

Funding to state and other entities providing direct assistance: Before the ACA, some states had already established their own Consumer Assistance Programs (CAPs) or health insurance ombudsman programs to help all consumers explore coverage options or assist in resolving problems with their health insurance. Federal CAP grants as part of the ACA allowed for the improvement of existing programs and the creation of new CAPs in other states. In addition to assisting with consumer education and enrollment, the ACA listed one of the duties of CAPs as “assisting with the filing of complaints and appeals… of group health plans…and providing information about the external appeal process.” However, CAPs still operating today have not been supported by federal grant funding since 2012, effectively eliminating the only federally-funded assistance program available to consumers with employer coverage. Several have ceased operations due to lack of funding.

As referenced above, in addition to CAPs, Navigators were established under the ACA as a program to provide direct assistance to consumers in both HealthCare.gov states and in states that operate their own marketplace. Navigators offer support by conducting public education and outreach, helping consumers apply for financial assistance, assisting with enrollment and post-enrollment issues, and providing fair and impartial information about health plan options. Navigators cannot be insurers, nor can they receive any direct or indirect payment from an insurer. These programs in HealthCare.gov states are funded by federal grants, the amounts of which have fluctuated over the years depending on which political party is in power. In February 2025, the Trump administration announced it would cut funding for the Navigator program from its current $100 million to $10 million for 2026.

Standards for health insurance agents and brokers: Agents and (web)brokers play a large role in selling coverage in the individual and group insurance markets and can assist consumers in understanding their health insurance options and costs. While most agents and brokers are certified and regulated at the state level, federal requirements for those agents and brokers involved with Marketplace plans are meant to protect consumers from fraudulent activity and misleading information from agents and brokers, and to make sure consumers are aware of how they are paid and the possibility of conflicts of interest in steering consumers to certain products that financially benefit the agent/broker/web broker. Federal law also requires agents, brokers, and other service providers that work with private employer plans to disclose to employers how they are paid.

Looking forward

KFF 2023 Consumer Survey findings about how consumers understand and navigate the health insurance system reveal frustrating hurdles to determine what items and services and what providers are covered by their insurance. It presents the question of whether we have a system that is impossible for a consumer to navigate alone, leaving consumers vulnerable to exploitation and confusion as they are caught in the middle of health plan and provider interests and arbitrary boundaries of authority between state and federal agencies. Coming out of an election widely viewed to have turned on concerns about the economy, including health care costs, and following public outrage against insurers following the killing of the United Healthcare CEO at the end of 2024, expect that health care consumer issues will not go away, but perhaps will shift focus to include:

Use of digital technology such as artificial intelligence (AI) to assist consumers: Though imperfect and with some pitfalls, digital technology, including AI, can help consumers navigate the complexities of health insurance. These tools are increasingly being promoted to both companies and individuals and in 2024, nearly two-thirds (64%) of adults say they have used or interacted with AI. AI tools can be appealing to consumers looking for answers to health insurance-related questions without the need to make a phone call, wait on hold, or read through plan documents, and are often available 24/7. From guiding consumers through the insurance claims process, including filing appeals, to helping determine whether a plan that applies coinsurance or copayments for their prescription drugs will meet their needs, and identifying in-network doctors near a patient’s home, these tools have the potential to transform the ways in which people seek health information.

However, AI has also been in the spotlight following investigations and litigation in recent years related to health plans’ use of these tools in making coverage determinations, such as for prior authorization requests and in the claims review process. Much of the existing research and criticisms related to the use of AI in health care more broadly, such as clinical decision-making and claims processing, feature overarching concerns related to their accuracy, reliability, confidentiality, and accessibility that could also apply to consumers using AI and other digital technology to navigate their health insurance.

Patient input in coverage practices: Broader and different mechanisms to gather information about consumer experiences in real time could assist in determining the most pressing concerns for patients and engage more consumers in policy discussions about what structural changes and protections are most needed and impactful for them. One of the largest health insurers recently announced changes aimed at improving the patient experience in using their coverage, expanding consumer support, and improving transparency. Employers are making changes to better oversee and understand their benefit programs and provide consumer input and navigation services as plan sponsors face real scrutiny for the first time under longstanding federal fiduciary requirements.

For the federal government, while deregulation across health care, as well as federal agency upheaval, is likely to be the focus in the coming years, the Trump administration will be tasked with implementing key provisions of the No Surprises Act, which he signed into law, that requires upfront information about what services cost and more accurate provider directories. The Trump administration has already issued an Executive Order for agencies to “rapidly implement” price transparency regulations.

Promoting other forms of coverage: A reaction to the health insurance labyrinth has some promoting mechanisms to move away from traditional insurance to direct payment alternatives such as direct primary care arrangements and account-based arrangements where consumers use dollars available in a health savings account or other type of account to purchase care. The pros and cons of these arrangements will be up for debate, as well as whether consumers—especially those with lower incomes and/or chronic illnesses—are well served by the financial and coverage limitations that may be part of these arrangements, including existing problems with the price transparency data available to them and the rising cost of care due to provider consolidation. Patients might be faced with a different set of understanding challenges under these arrangements.

Understanding how health coverage works, what services are covered and by whom, and what rights consumers have is one piece of the health insurance labyrinth. The second brief in this series on consumer understanding will focus on the cost-related aspects and challenges of health insurance and health care.

This work was supported in part by a grant from the Robert Wood Johnson Foundation. The views and analysis contained here do not necessarily reflect the views of the Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism.

This is Irving Washington and Hagere Yilma. We direct KFF’s Health Information and Trust Initiative and on behalf of all our colleagues at KFF, we’re pleased to bring you this edition of our bi-weekly Monitor.

This volume discusses the spread of race-based vaccine myths amid measles outbreaks, along with shifts in health communication from fact-checking to fostering open dialogue. It also explains common misconceptions about heart attack treatment and prevention, a new scientific journal that questions established science, and gaps in research standards for AI chatbots used in healthcare.

As a measles outbreak in Texas worsens and other cases are reported in the country, misinformation about vaccines continues to spread, influencing public perception and fueling hesitancy. One recurring narrative falsely claims that Black children should follow a different vaccine schedule than children of other races because of alleged differences in immune systems. Some research has shown that people of African descent may demonstrate, on average, a stronger immune response to the rubella vaccine. However, the study’s authors state that the data does not support that there is a need for different vaccine schedules based on race. The claim spread in news and social media after it was brought up during Robert F. Kennedy Jr.’s Senate confirmation hearings, with social media posts both debunking and supporting this narrative.

One of the most popular social media posts on the topic came from Senator Angela Alsobrooks, who shared a video clip on X of her asking Kennedy about these claims during the confirmation hearing and expressing her concern about the dangers of this narrative. The post received approximately 164,000 likes and 30,000 reposts, and 15,000 comments as of February 19. While many commenters shared Alsobrooks’ concern, some perpetuated the misconception that biological differences in vaccine safety are supported by evidence. In some instances, commenters cited cases in which race-based medicine is used in other domains as justification for biological differences in medication effectiveness. But scientists have emphasized that race is a social construct, not a biological category, and using it as a proxy for genetics has led to harmful medical practices.

Despite decades of credible research showing that vaccines are not associated with autism, narratives linking vaccines to autism in Black children have also gained traction, sometimes citing a retracted study of 2004 CDC data. The study, which claimed that Black boys who received the MMR vaccine on schedule were diagnosed with autism at higher rates than other children who did not receive the vaccine on time, was retracted due to flawed methods and the lead author’s undisclosed ties to the anti-vaccine group, Children’s Health Defense. Other claims that vaccines cause autism cite a debunked study, commonly referred to as the “Mawson Study”, which is not about race-related risk but reports an alleged connection between vaccines and autism. However, the study was not published in a peer-reviewed journal, was funded by an anti-vaccine group, and authored by researchers with a history of publishing vaccine-related research that was later retracted. This belief, alongside other unfounded concerns about vaccine safety, may be fueling the decline in childhood vaccination rates, which has led to outbreaks of vaccine-preventable diseases like measles.

Polling Insights:

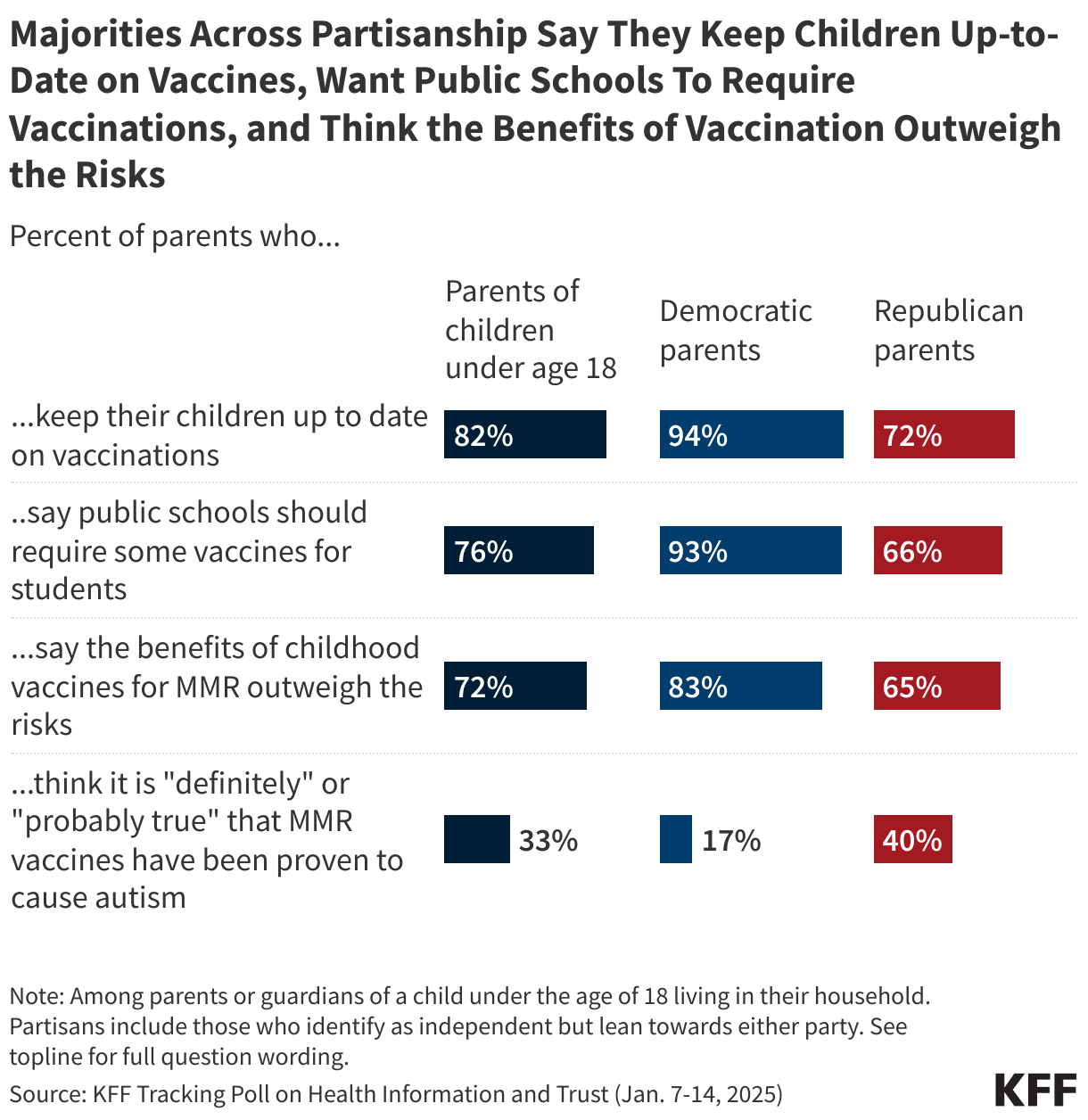

KFF’s January 2025 Tracking Poll on Health Information and Trust found that majorities of parents say they keep their children up to date on vaccinations (82%), support public schools requiring vaccines for students (76%), and believe the benefits of childhood MMR vaccines outweigh the risks (72%). While majorities of parents across partisanship express each of these views, the shares answering in the pro-vaccine direction are notably larger among parents who identify as Democrats or lean that way, compared to their Republican and Republican-leaning counterparts.

The Field of Health Communication Explores Moving Beyond Fact-Checking to Foster Dialogue

Blue Images / Getty Images

Some health communication professionals are shifting their approach to promoting accurate health beliefs, moving beyond reactive fact-checking to open conversations that help people weigh benefits and risks more accurately. One emerging strategy, known as bypassing, focuses on presenting relevant facts rather than directly debunking misinformation. For example, instead of stating that “aluminum in vaccines causes bone problems” is false, bypassing highlights that “the aluminum in vaccines enhances their effectiveness in preventing disease.” Research suggests this approach may be more effective at changing personal attitudes, though its impact on policy views is less clear. Fostering open conversations may also allow health professionals to share nuances of scientific information in an accessible manner. For topics like vaccines, simply emphasizing their safety and effectiveness may not be enough as it fails to address public concerns and skepticism. Members of the Council for Quality Health Communication argue that the phrase “safe and effective” should be replaced with a more nuanced, empathetic approach that explains vaccine benefits in relatable terms, acknowledges uncertainties, and engages with people in ways that resonate with their real-world experiences and values.

New Public Health Journal Co-Founded by Nominee for NIH Director Questions Widely Accepted Science

Mordolff / Getty Images

A new scientific journal, the Journal of the Academy of Public Health, has drawn attention for its potential bias and questioning of scientific consensus. The journal has ties to the news site RealClearPolitics and was co-founded by Dr. Jay Bhattacharya, President Trump’s nominee for NIH director. Another Trump nominee, Dr. Marty Makary, nominee for FDA commissioner serves on the editorial board, although both Makary and Bhattacharya are currently listed as “on leave” from the journal. Its first edition included articles that questioned COVID-19 vaccine trials, suggested a link between DTaP vaccines and childhood asthma, and argued school mask mandates were ineffective. Co-founder Dr. Martin Kulldorff, known for opposing COVID-19 lockdowns and child vaccination, also published a paper claiming that established journals suppress dissenting viewpoints and fail to address public health biases. While the journal’s critiques may appeal to those questioning the prevailing public health consensus, some question its objectivity. The journal is open-access and peer reviewed, but it operates on a membership model where only invited members of the Academy of Public Health can submit articles, which may raise additional questions about how this exclusivity may impact credibility. However, the journal’s divergence from scientific consensus may increase its credibility among Republicans who are less likely than Democrats to list scientific research studies among their top trusted sources for public health information, according to the Rollins-Gallup Public Health Priorities Survey.

False Beliefs About Heart Attack Treatment and Prevention Persist as Heart Disease Remains Leading Cause of Death

Peter Dazeley / Getty Images

Heart disease is the leading cause of death in the U.S. and ongoing research continues to examine new factors like COVID-19 that influence cardiovascular risk. However, misinformation about heart attack treatment and prevention persists. One misconception that has re-emerged is that coughing during a heart attack, sometimes called ‘cough CPR,’ can help maintain blood flow to the heart. Health experts have debunked this, explaining that CPR is used for cardiac arrest, not heart attacks, and that by the time CPR is necessary, a person is typically unable to cough. Additionally, coughing cannot restart a heart that has stopped beating. The confusion likely stems from the use of coughing as a temporary measure during certain arrhythmias in monitored medical settings, leading to the misconception that it can improve heart function during a heart attack and potentially delaying care.

Outdated guidelines may also contribute to misconceptions about heart attack prevention. Daily aspirin use was once widely recommended for healthy adults to reduce heart attack and stroke risk, however, guidelines from the American College of Cardiology and the American Heart Association (AHA) issued in 2019 only recommend aspirin as an option among adults ages 40-70 who have elevated risk of cardiovascular disease. The guidelines also advise against routine aspirin use for healthy adults over 70 due to the risk of gastrointestinal bleeding. Despite this, a survey by the Annenberg Public Policy Center found that this misconception persists, particularly among older adults. The survey found that 18% of people without a personal or family history of heart attack or stroke reported regularly taking low-dose aspirin, and nearly 43% believed its benefits outweigh the risks. Those ages 60 and over were especially likely to take aspirin daily for prevention and to believe in its benefits, despite updated guidance.

AI & Emerging Technology

Gaps in Research Standards for AI Chatbots in Healthcare

Laurence Dutton / Getty Images

As artificial intelligence (AI) continues to shape healthcare, large language models (LLMs) are increasingly consulted for medical advice. However, concerns persist regarding their accuracy, transparency, and safety. A systematic review of 137 studies evaluated the reporting quality of research assessing LLMs’ ability to offer health guidance. Findings revealed that nearly all studies examined closed-source models without disclosing sufficient details about the LLM version or parameters. Most studies relied on subjective measures to assess chatbot performance, and fewer than a third considered ethical, regulatory, or patient safety implications. The variability in study design and reporting highlights a gap in standardized assessment frameworks which may be useful for conducting reliable evaluations of LLMs used in healthcare.

About The Health Information and Trust Initiative: the Health Information and Trust Initiative is a KFF program aimed at tracking health misinformation in the U.S., analyzing its impact on the American people, and mobilizing media to address the problem. Our goal is to be of service to everyone working on health misinformation, strengthen efforts to counter misinformation, and build trust.

The Monitor is a report from KFF’s Health Information and Trust initiative that focuses on recent developments in health information. It’s free and published twice a month.

Support for the Health Information and Trust initiative is provided by the Robert Wood Johnson Foundation (RWJF). The views expressed do not necessarily reflect the views of RWJF and KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities. The Public Good Projects (PGP) provides media monitoring data KFF uses in producing the Monitor.

Managed care is the dominant delivery system for people enrolled in Medicaid. The latest national Medicaid managed care enrollment data (from 2022) show 75% of Medicaid beneficiaries were enrolled in comprehensive managed care organizations (MCOs). While managed care is the dominant Medicaid delivery system, states decide which populations and services to include in managed care arrangements, which leads to considerable variation across states. Additionally, while state requirements for Medicaid managed care plans can be tracked, plans have flexibility in certain areas, including in setting provider payment rates, and plans may choose to offer additional benefits beyond those required by the state.

Early in 2025, there are many factors at play that could have implications for Medicaid managed care plans and the people they serve. At the state level, states and plans have faced considerable rate setting uncertainty after millions of people were disenrolled during the unwinding of the pandemic-era Medicaid continuous enrollment provision. Some firms report that current capitation rates do not align with higher member risk and utilization patterns. Many states have sought federal approval to adjust rates to address these changes amid shifts and uncertainty in state fiscal conditions. At the federal level, talks in Congress about cutting federal Medicaid spending could have implications for coverage as well as plans and providers. Finally, major Medicaid regulations designed to promote quality of care and advance access to care for Medicaid enrollees finalized under the Biden administration could be repealed by Congress or delayed or rewritten by the Trump administration. In this context, this brief describes 10 themes related to the use of comprehensive, risk-based managed care in the Medicaid program.

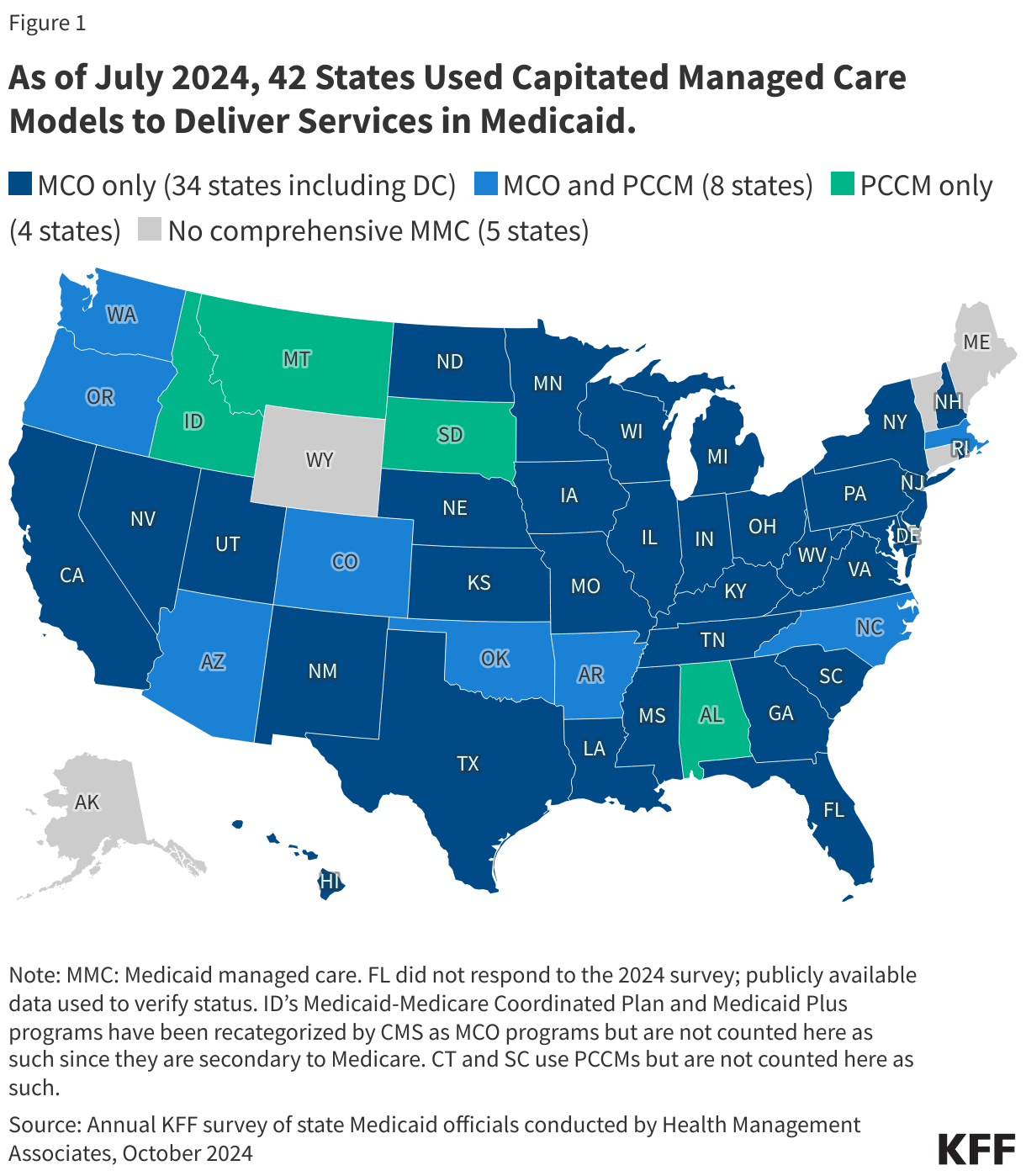

1. Today, capitated managed care is the dominant way in which states deliver services to Medicaid enrollees.

States design and administer their own Medicaid programs within federal rules. States determine how they will deliver and pay for care for Medicaid beneficiaries. Nearly all states have some form of managed care in place – comprehensive risk-based managed care and/or primary care case management (PCCM) programs.1,2 As of July 2024, 42 states (including DC) contract with comprehensive, risk-based managed care plans to provide care to at least some of their Medicaid beneficiaries (Figure 1). Oklahoma is the latest state to be included in this count, having implemented capitated, comprehensive Medicaid managed care (for most children and adults) on April 1, 2024. Medicaid MCOs provide comprehensive acute care (i.e., most physician and hospital services) and, in some cases, long-term care to Medicaid beneficiaries and are paid a set per member per month payment for these services. For more than three decades, states have increased their reliance on managed care delivery systems with the aim of improving access to certain services, enhancing care coordination and management, and making future costs more predictable. While the shift to MCOs has increased budget predictability for states, the evidence about the impact of managed care on access to care and costs is both limited and mixed.3,4,5

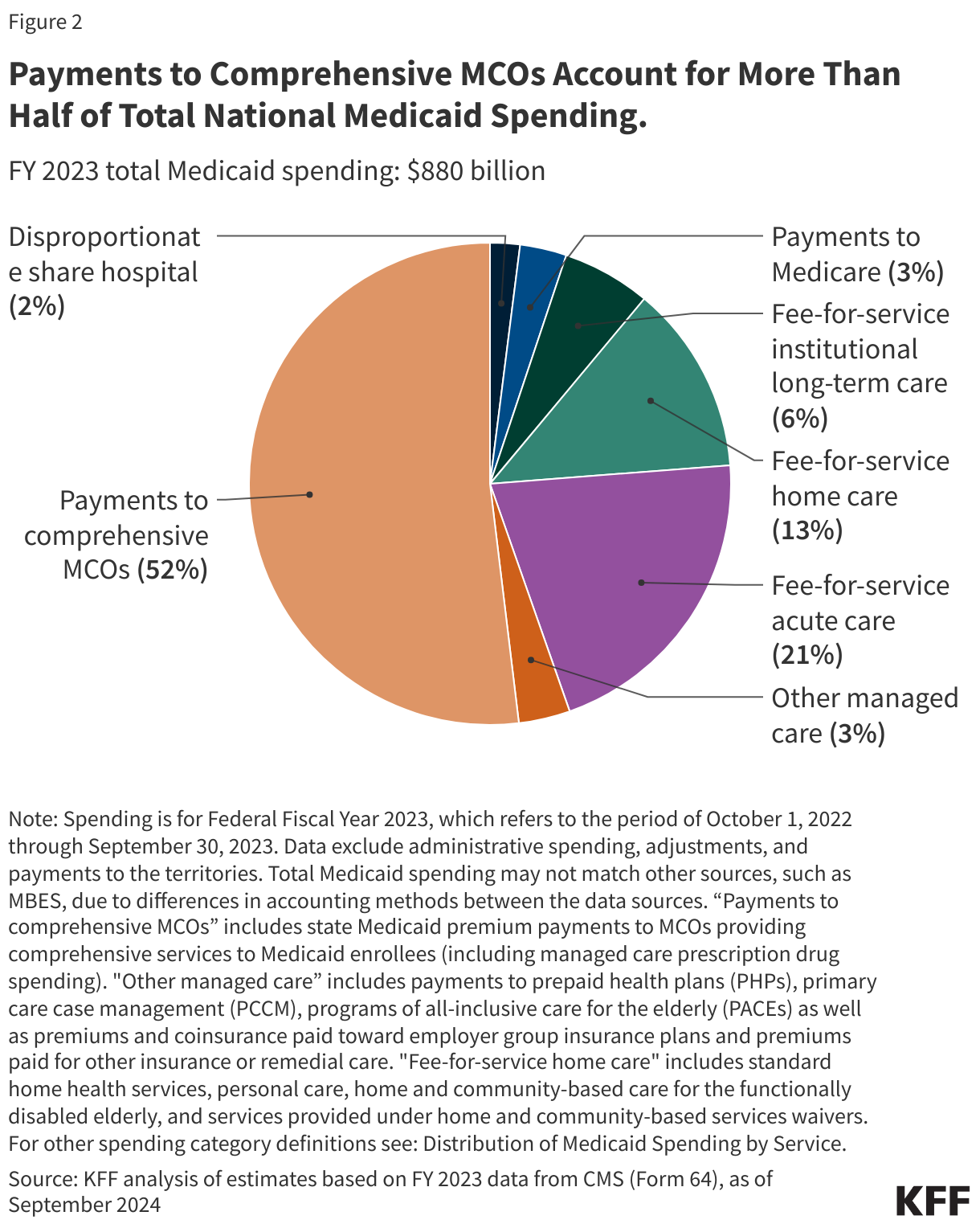

2. In FY 2023, payments to comprehensive risk-based MCOs accounted for over half of Medicaid spending.

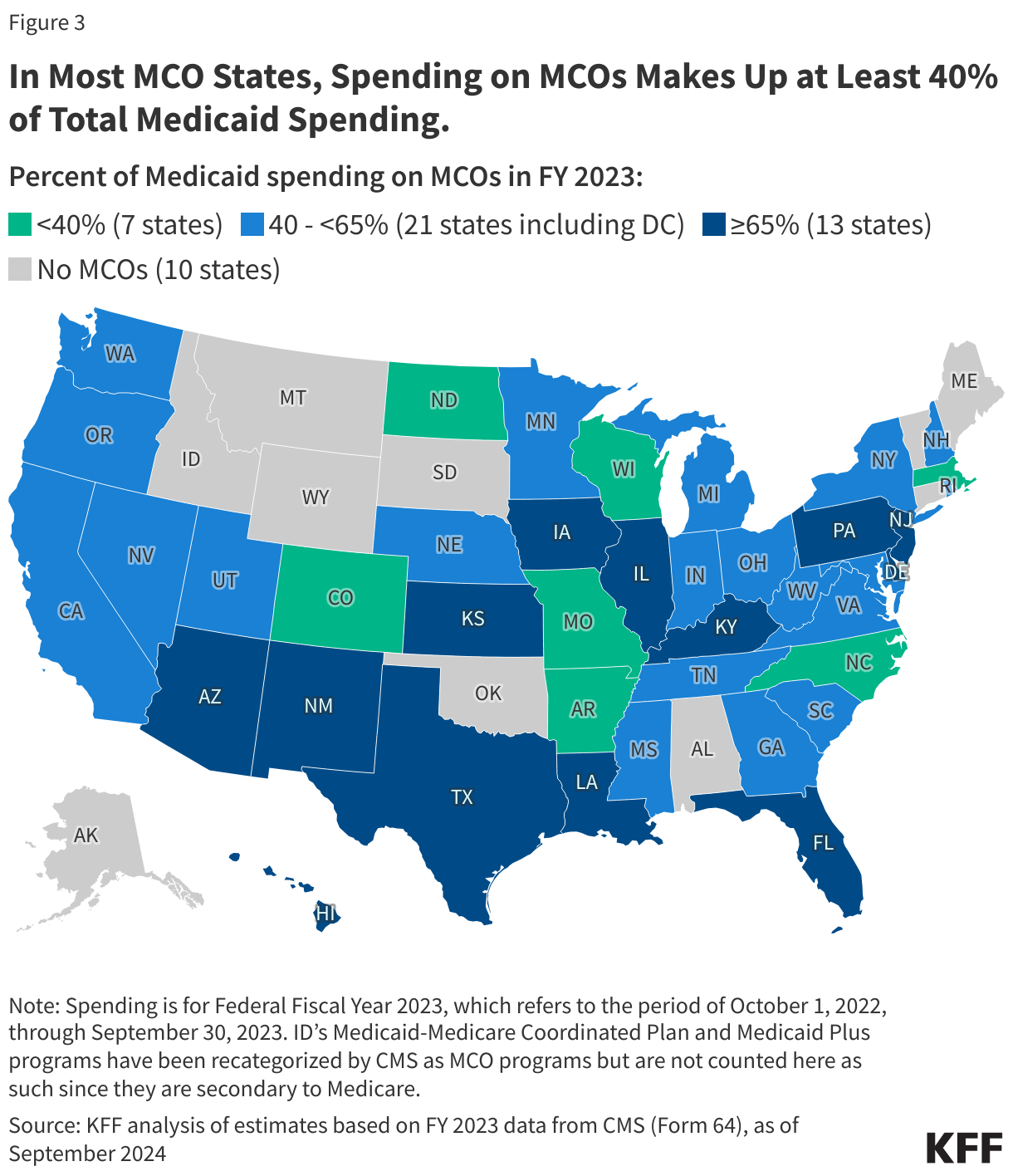

In FY 2023, state and federal spending on Medicaid services totaled over $880 billion. Payments made to MCOs accounted for about 52% of total Medicaid spending (Figure 2), unchanged from the previous fiscal year. The share of Medicaid spending on MCOs varies by state, but over three-quarters of MCO states directed at least 40% of total Medicaid dollars to payments to MCOs (Figure 3). State-to-state variation reflects many factors, including the proportion of the state Medicaid population enrolled in MCOs, the health profile of the Medicaid population, whether high-risk/high-cost beneficiaries (e.g., people with disabilities, dual eligible beneficiaries) are included in or excluded from MCO enrollment, and whether long-term care services are included in MCO contracts. As states expand Medicaid managed care to include higher-need, higher-cost beneficiaries, expensive long-term care, and adults newly eligible for Medicaid under the ACA, the share of Medicaid dollars going to MCOs could continue to increase.

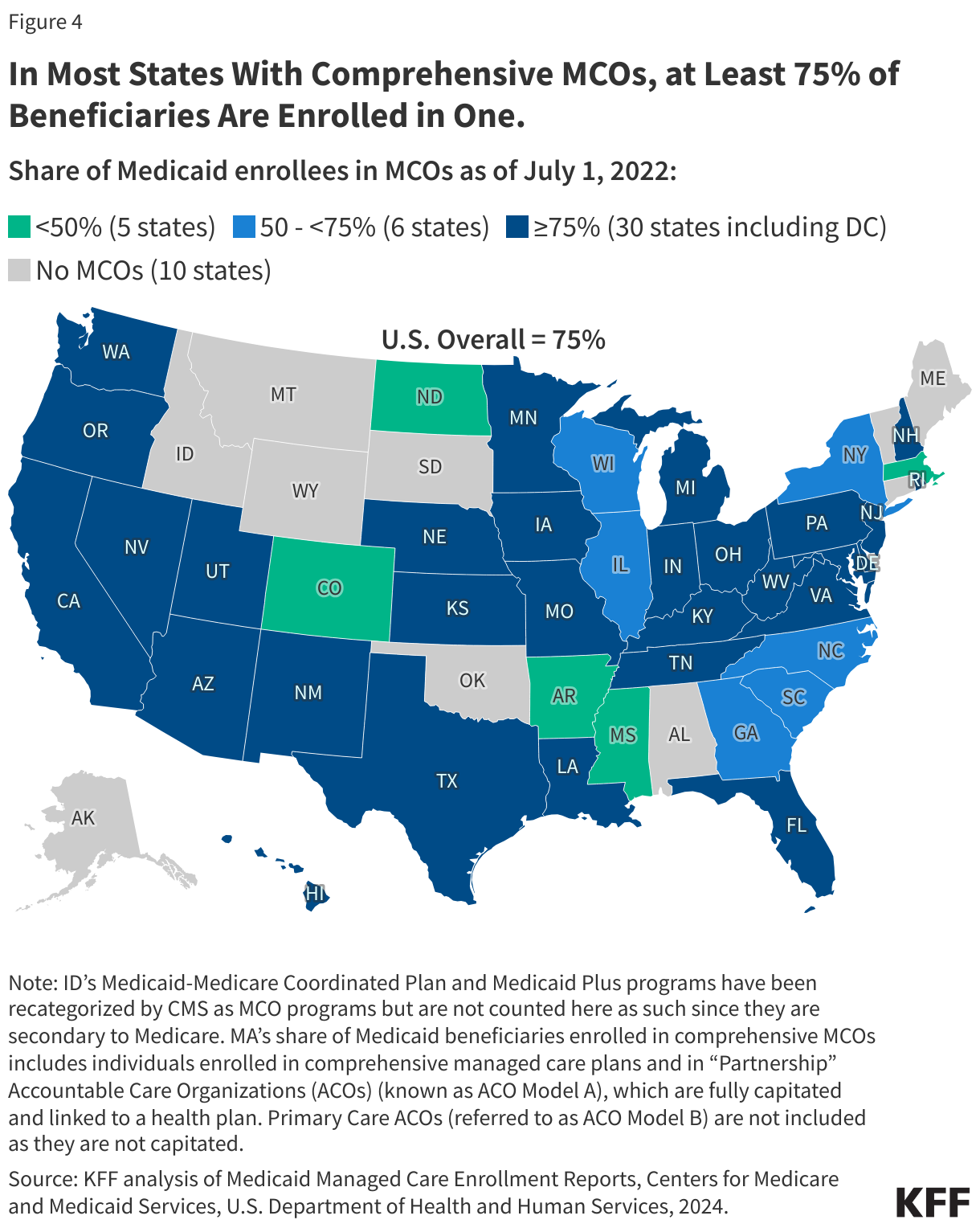

3. Three-quarters (75%) of all Medicaid beneficiaries received their care through comprehensive risk-based MCOs.

As of July 2022, nearly 72 million Medicaid enrollees received their care through risk-based MCOs. Thirty MCO states covered at least 75% of Medicaid beneficiaries in MCOs (Figure 4).

Although 2022 data are the most current national data available, enrollment in Medicaid overall grew substantially during the COVID public health emergency when states paused disenrollments, resulting in growth in MCO enrollment as well. At the start of the “unwinding” period, in April 2023, Medicaid enrollment (overall) peaked at 94.5 million, an increase of 23 million or 32% from before the pandemic. Despite millions of disenrollments during the unwinding, nationally, nearly 8 million more people were enrolled in Medicaid/CHIP in October 2024 than in February 2020 (pre-pandemic).

4. Children and adults are groups most likely to be enrolled in MCOs; however, states are increasingly including enrollees with complex needs in MCOs.

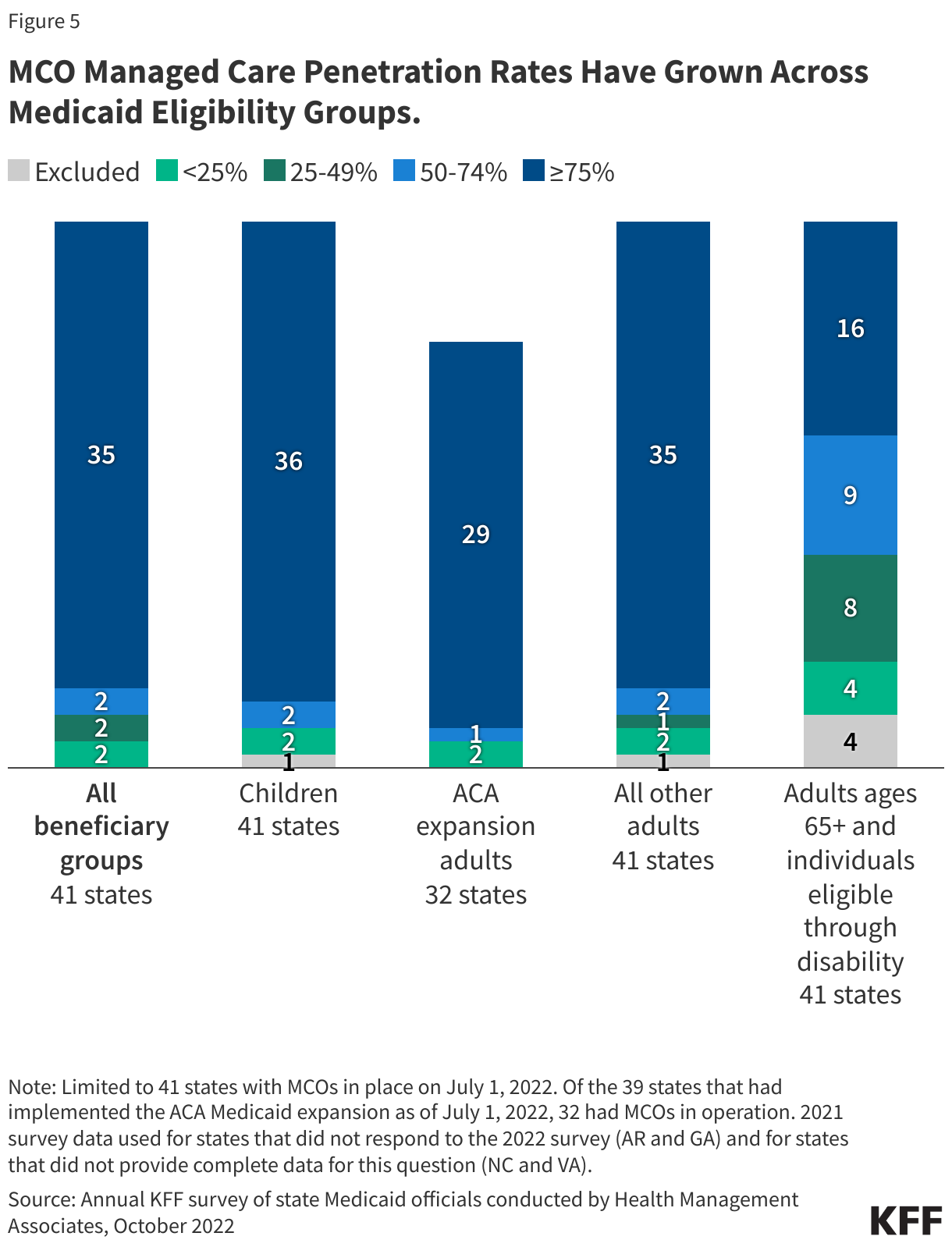

As of July 2022, 36 MCO states reported covering 75% or more of all children through MCOs (Figure 5). Of the 39 states that had implemented the ACA Medicaid expansion as of July 2022, 32 states were using MCOs to cover newly eligible adults and most covered more than 75% of beneficiaries in this group through MCOs. Thirty-five MCO states reported covering 75% or more of low-income adults in pre-ACA expansion groups (e.g., parents, pregnant women) through MCOs. Fewer MCO states reported covering 75% or more adults ages 65+ and people eligible through disability. Although this group is still less likely to be enrolled in MCOs than children and adults, over time, states have been moving to include adults ages 65+ and people eligible through disability in MCOs.

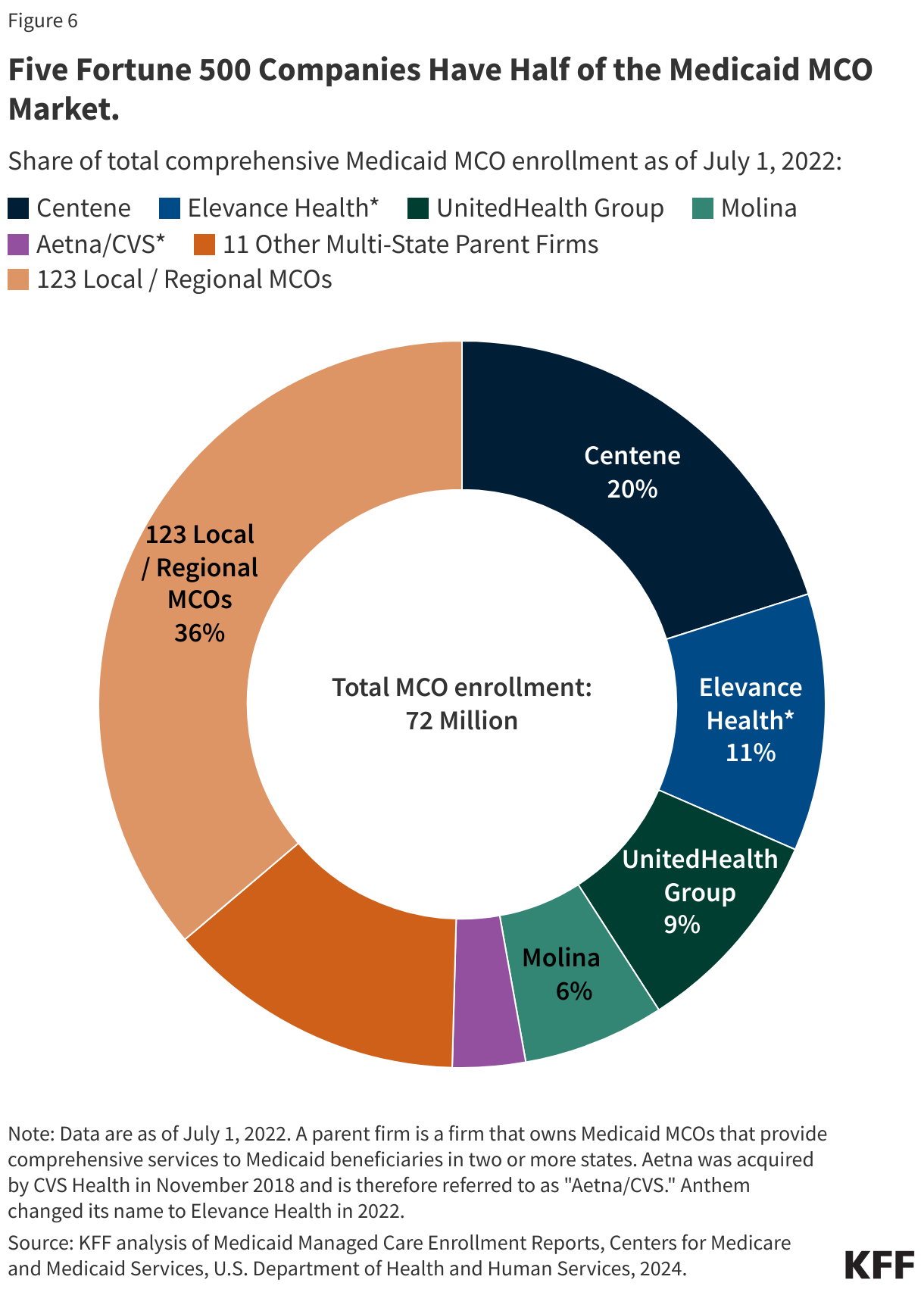

5. Five publicly traded firms account for half of MCO enrollment.

States contracted with a total of 282 Medicaid MCOs as of July 2022. MCOs represent a mix of private for-profit, private non-profit, and government plans. As of July 2022, a total of 16 firms operated Medicaid MCOs in two or more states (called “parent” firms), and these firms accounted for over 63% of enrollment in 2022 (Figure 6). Of the 16 parent firms, six are publicly traded, for-profit firms while the remaining ten are non-profit companies. Five firms – Centene, UnitedHealth Group, Elevance (formerly Anthem), Molina, and Aetna/CVS – account for 50% of all Medicaid MCO enrollment (Figure 6). All five are publicly traded companies ranked in the Fortune 500, and four are ranked in the top 100.

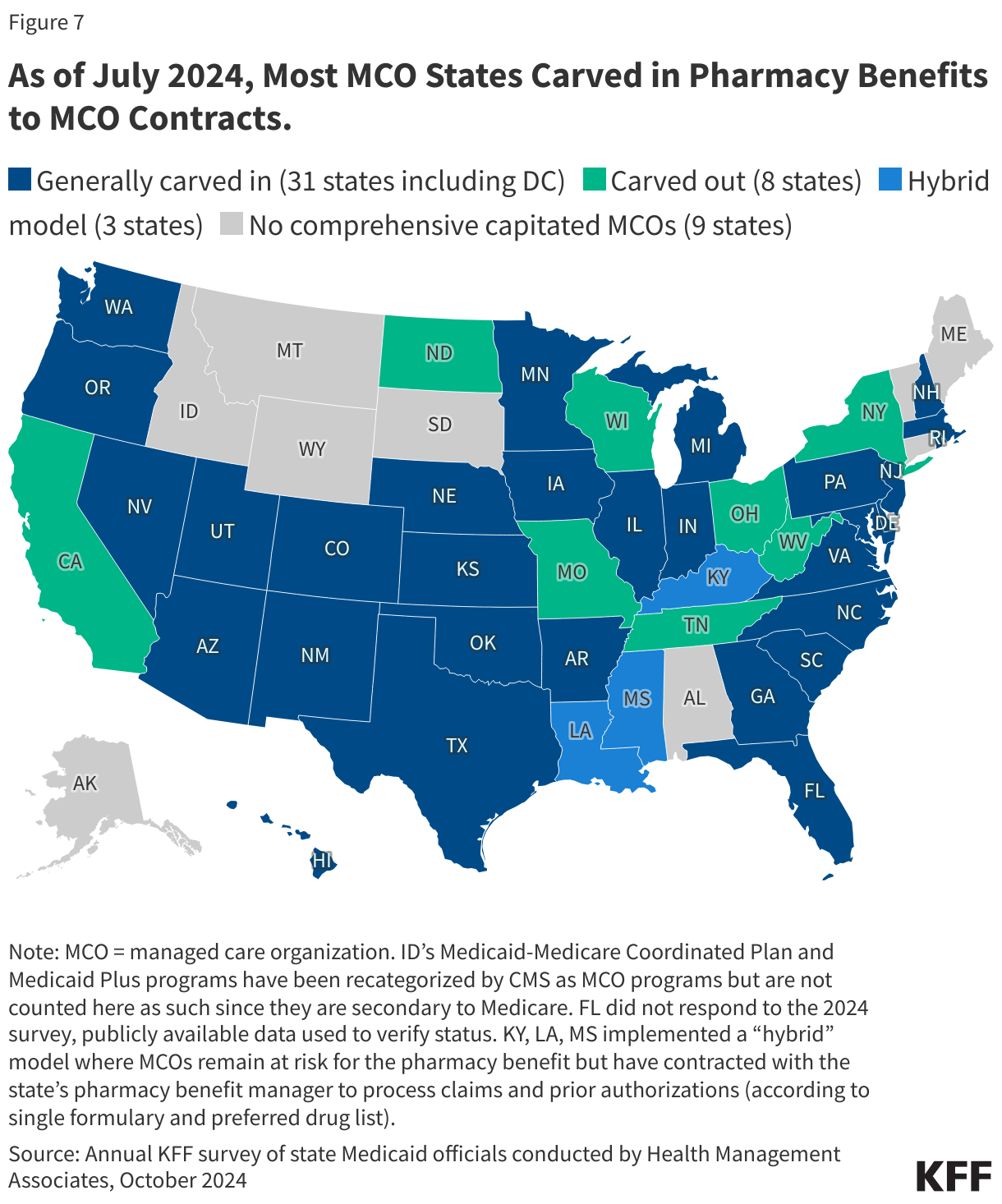

6. States make decisions about which services to carve in and out of MCO contracts.

Although MCOs provide comprehensive services to beneficiaries, states may carve specific services out of MCO contracts to fee-for-service systems or limited benefit plans. Services frequently carved out include behavioral health, pharmacy, dental, and long-term care services. However, there has been significant movement across states to carve these services into MCO contracts. While the vast majority of states that contract with MCOs report that the pharmacy benefit is carved into managed care (31 of 42), eight states report that pharmacy benefits are carved out of MCO contracts as of July 2024 (Figure 7). An additional three states (Kentucky, Louisiana, and Mississippi) now contract with a single PBM for the managed care population instead of implementing a traditional carve-out of pharmacy from managed care. (Under this “hybrid” model, MCOs remain at risk for the pharmacy benefit but must contract with the state’s pharmacy benefit manager to process pharmacy claims and pharmacy prior authorizations according to a single formulary and preferred drug list.)

7. Each year, states develop MCO capitation rates that must be actuarially sound and may include risk mitigation strategies.

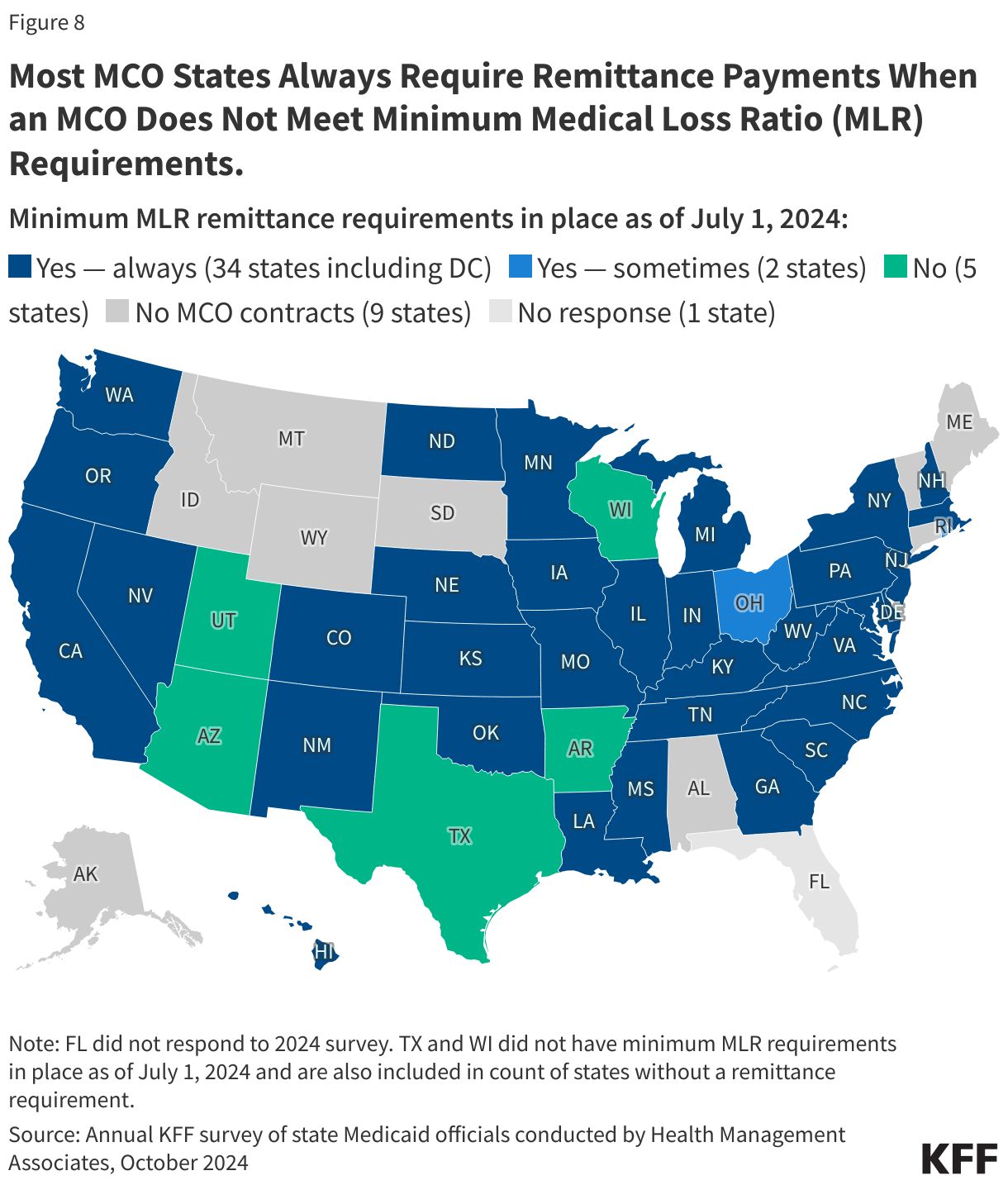

States pay Medicaid managed care organizations a set per member per month payment for the Medicaid services specified in their contracts. While plans set rates in the commercial and Medicare Advantage markets, Medicaid managed care rates are developed by states and their actuaries and reviewed and approved by CMS. Under federal law, payments to Medicaid MCOs must be actuarially sound.Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Unlike fee-for-service (FFS), capitation provides upfront fixed payments to plans for expected utilization of covered services, administrative costs, and profit. Plan rates are usually set for a 12-month rating period. States may use a variety of mechanisms to adjust plan risk, incentivize plan performance, and ensure payments are not too high or too low, including risk sharing arrangements, risk and acuity adjustments, medical loss ratios (MLRs, which reflect the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement), or incentive and withhold arrangements.

To limit the amount that plans can spend on administration and keep as profit, states are required to develop capitation rates for Medicaid to achieve an MLR of at least 85% in the rate year; 6 however, there is no federal requirement for Medicaid plans to pay remittances to the state if they fail to meet the MLR standard.7 As of July 2024, 34 MCO states reported they always require remittance payments when an MCO does not meet state minimum MLR requirements, while two states indicated they sometimes require MCOs to pay remittances (Figure 8).

8. In 2024, CMS finalized rules to strengthen access standards, but the future of the rules is uncertain.

The Biden administration finalized major Medicaid regulations designed to promote quality of care and advance access to care for Medicaid enrollees. The 2024 Managed Care rule addresses Medicaid managed care access, financing, and quality, including strengthening standards for timely access to care (e.g., through the establishment of national maximum wait time standards for certain “routine” appointments) and states’ monitoring and enforcement efforts. These rules are complex and are set to be implemented over several years. However, Congress may seek to overturn these rules, or the Trump administration could delay implementation or issue new regulations that would undo them. During the first Trump administration, CMS took action to change Medicaid managed care rules, including relaxing rules around network adequacy and beneficiary protections.

States are generally prohibited from contractually directing how a managed care plan pays its providers.8 Subject to CMS approval, however, states may implement certain “state directed payments” (SDPs) that require managed care plans to adopt minimum or maximum provider payment fee schedules, provide uniform dollar or percentage increases to providers (above base payment rates), or implement value-based provider (VBP) payment arrangements.9 In creating state directed payments (in 2016), CMS aimed to help states ensure access to adequate provider networks and to increase use of VBP arrangements. Many states that contract with MCOs use SDPs to make uniform rate increases that are like FFS supplemental payments. State directed payments must meet federal requirements (e.g., must be tied to utilization and delivery of services, be distributed equally to specified providers, and not be conditioned on participation in intergovernmental transfer (IGT) agreements).10 The managed care rules finalized in 2024 permit states to pay hospitals and nursing facilities at the average commercial payment rate (ACR) when using directed payments (higher than the Medicare payment ceiling used for other Medicaid FFS supplemental payments). The 2024 rules also tightened SDP requirements to improve oversight, evaluation, and transparency (e.g., states will be required to report provider level directed payment data) and to ensure state directed payments are tied to actual utilization. Recent reports indicate state directed payments have been a major driver of Medicaid expenditure growth in recent years, and CBO Medicaid projections for 2025-2034 attribute further increases in SDPs (partially tied to the changes in rule) as a factor increasing spending.

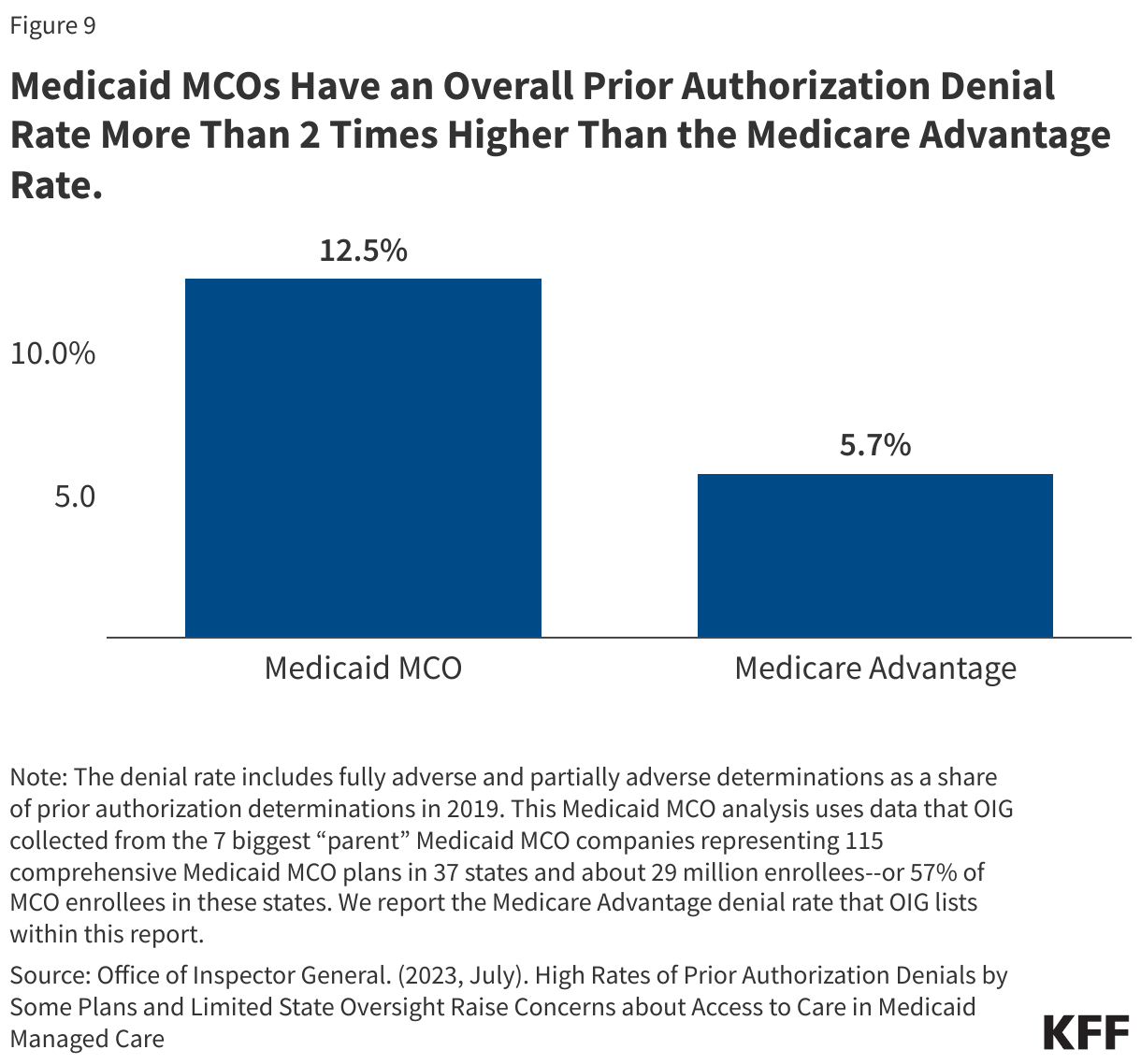

In 2024, CMS also finalized a rule focused on improving the prior authorization process including reducing approval wait times and improving transparency. A 2023 KFF survey of consumer experiences with health insurance found that about one in five Medicaid enrollees say they’ve had issues with prior authorization—higher than for most other types of insurance. A July 2023 OIG report found that Medicaid MCOs had an overall prior authorization denial rate of 12.5%–more than 2 times higher than the Medicare Advantage rate (Figure 9), raising concerns about prior authorization and access in Medicaid managed care. OIG recommendations (to CMS) include strengthening state monitoring of denials. Recent MACPAC analysis of denials and appeals in Medicaid managed care resulted in the inclusion of seven recommendations in the March 2024 Report to Congress focused on improving the appeals process and enhancing monitoring and oversight of MCOs.

9. States link financial incentives to quality measures and use contract requirements to advance priorities, including addressing social determinants of health.

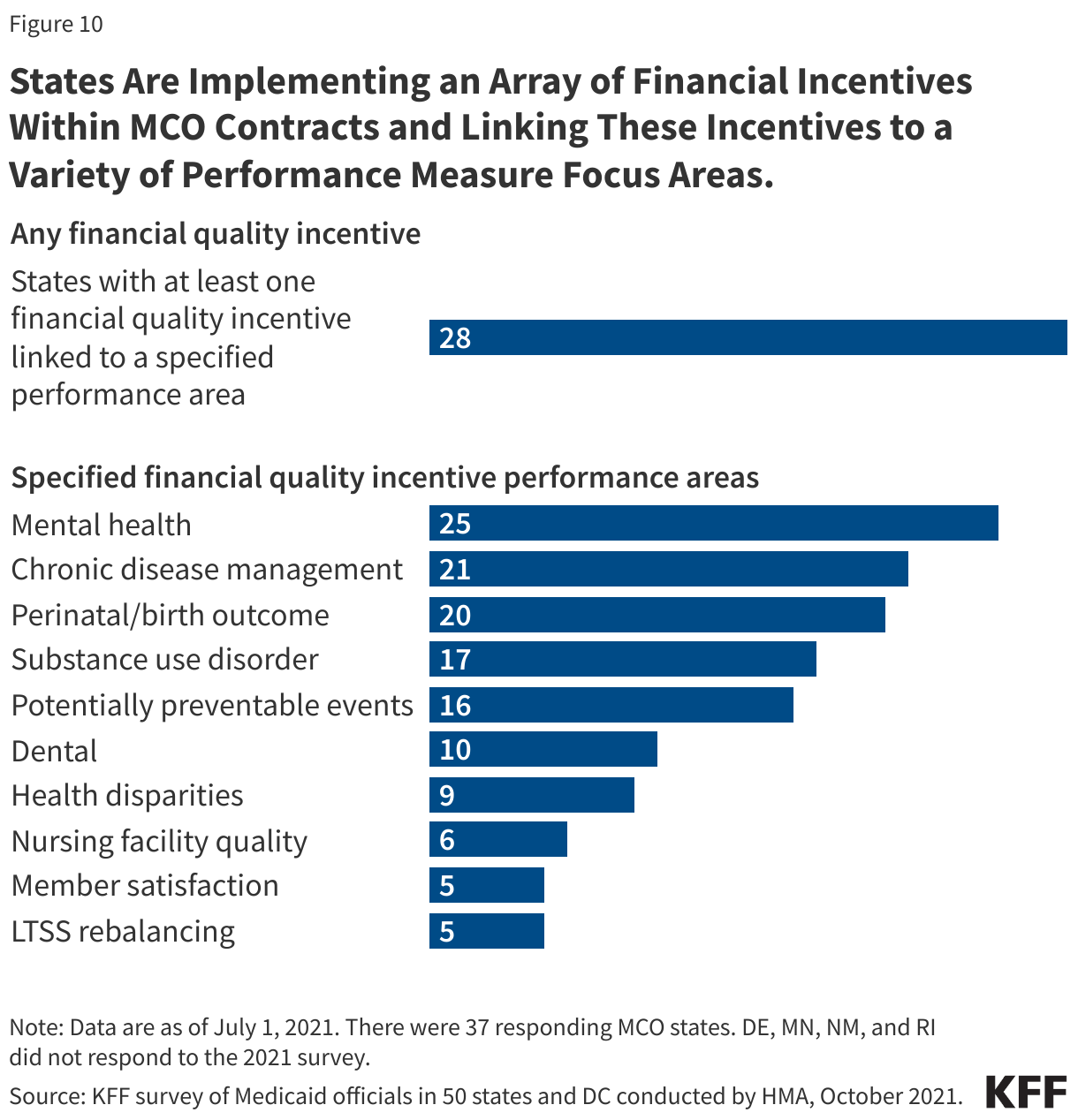

States incorporate quality metrics into the ongoing monitoring of their programs, including linking financial incentives like performance bonuses or penalties, capitation withholds, or value-based state directed payments to quality measures. Over three quarters of MCO states reported using at least one financial incentive to promote quality of care as of July 2021 (Figure 10). Financial incentive performance areas most frequently targeted by MCO states include behavioral health, chronic disease management, and perinatal/birth outcomes. Despite activity in this area, detailed performance information at the plan-level frequently has not been made publicly available by state Medicaid agencies, limiting transparency and the ability of Medicaid beneficiaries (and other stakeholders) to assess how plans are performing on key indicators related to access, quality, etc.

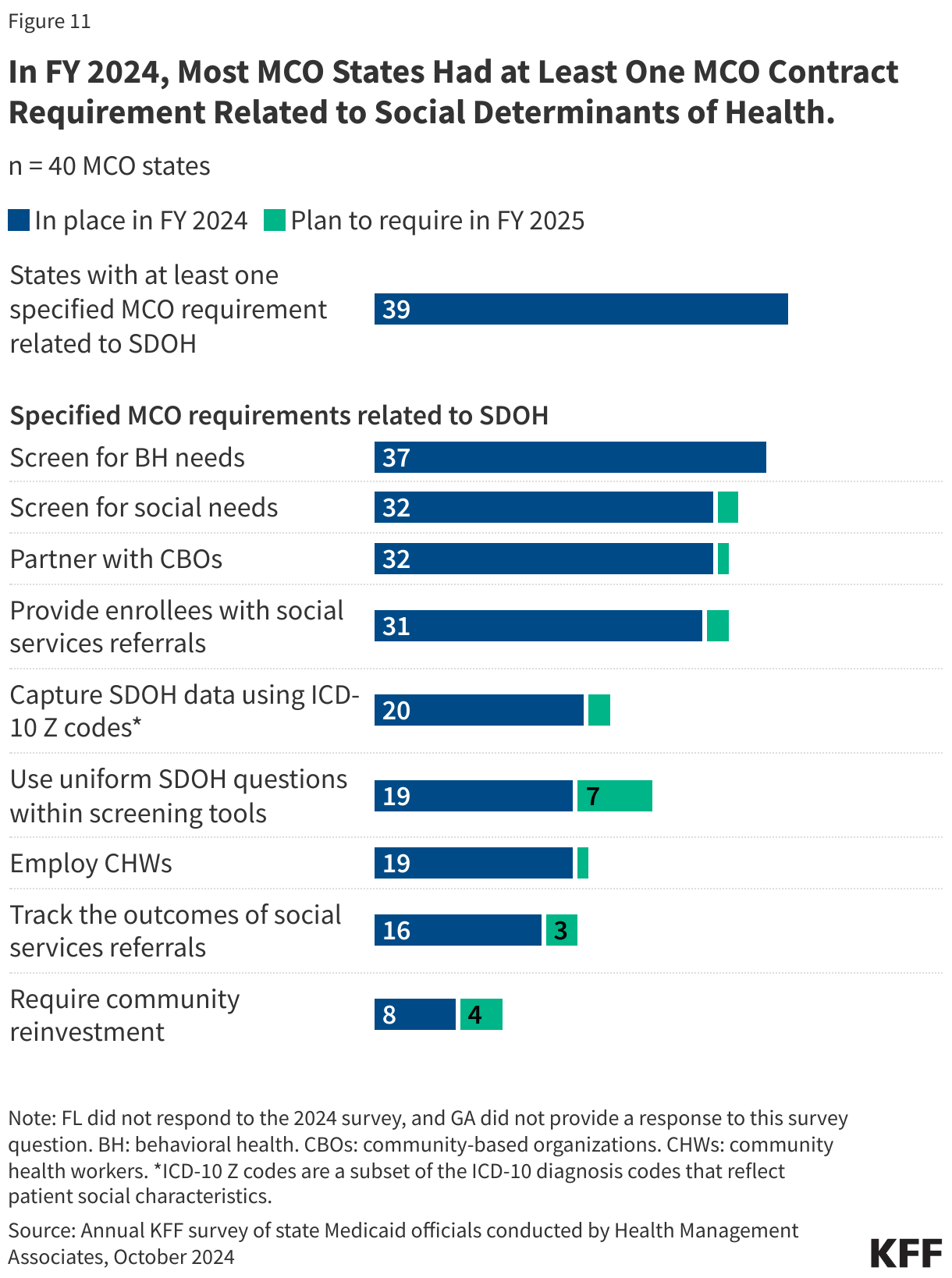

In FY 2024, most MCO states reported leveraging Medicaid MCO contracts to promote at least one specified strategy to address social determinants of health (Figure 11). States can also leverage managed care contracts to help reduce health disparities.

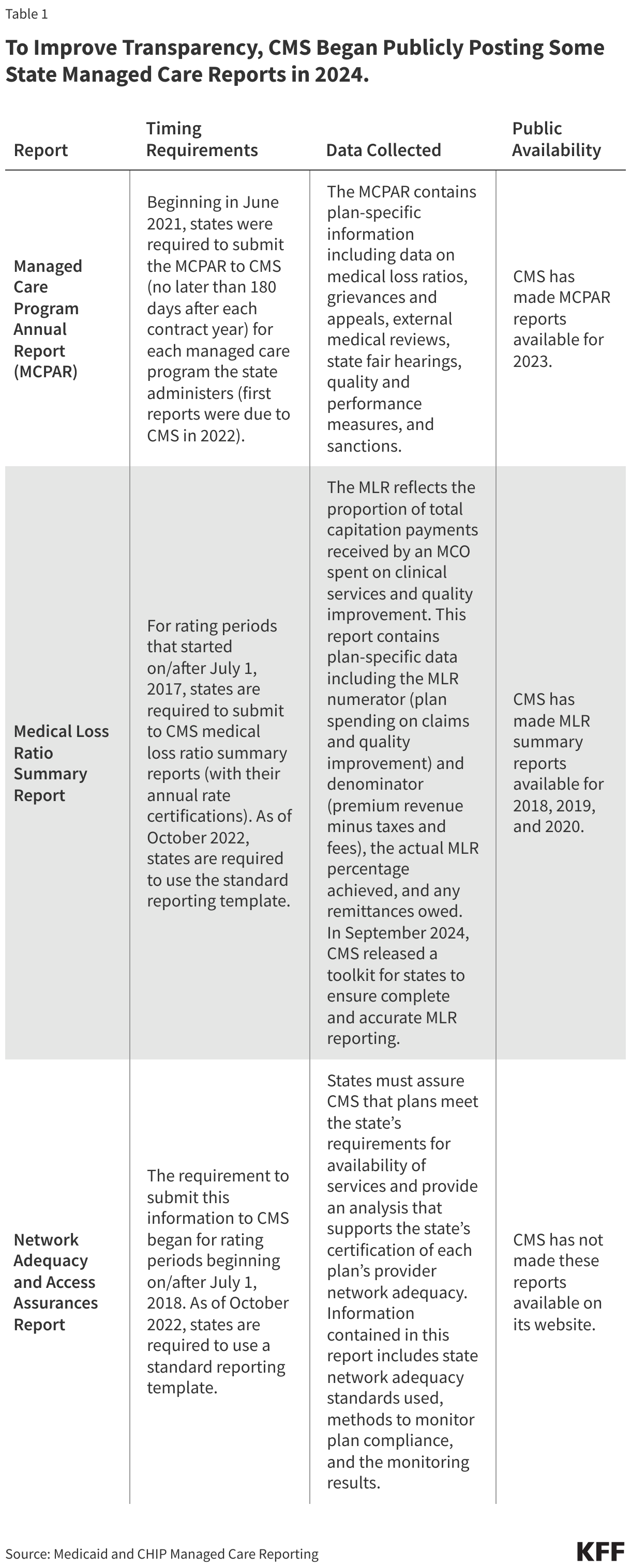

10. CMS has taken steps to improve managed care program monitoring and transparency.

The 2016 Medicaid managed care final rule created new managed care reporting requirements for states. CMS, under the Biden administration, developed standard reporting templates (Table 1) and a variety of toolkits and released a series of informational bulletins (2021, 2022, 2023, 2024) to help states improve their monitoring and oversight of managed care programs. Transparency has the potential to promote accountability. To improve transparency, CMS began publicly posting the Managed Care Program Annual Report (MCPAR) and the MLR Summary Reports on Medicaid.gov in 2024. Managed care rules finalized in 2024 include provisions aimed at further strengthening managed care transparency and monitoring, though the fate of these rules remains uncertain.

Posting data relating to the performance of individual MCOs may allow for comparison within and across states. However, limitations and challenges may exist including posting lags and incomplete data (e.g., GAO found 6 states had not submitted required MCPARs for 2022, OIG found MLR reports prepared by plans were missing required data). (States are required to post the MCPAR and Network Adequacy and Access Assurances Report on their websites but some states may not yet be in compliance with these requirements.) It is unclear whether the Trump administration will continue efforts to strengthen managed care oversight and transparency.

PCCM is a managed fee-for-service (FFS) based system in which beneficiaries are enrolled with a primary care provider who is paid a small monthly fee to provide case management services in addition to primary care. ↩︎

While MCOs are the predominant form of Medicaid managed care, millions of other beneficiaries receive at least some Medicaid services, such as behavioral health or dental care, through limited-benefit risk-based plans, known as prepaid inpatient health plans (PIHPs) and prepaid ambulatory health plans (PAHPs). ↩︎

Sparer M. 2012. Medicaid managed care: costs, access, and quality of care. Res. Synth. Rep. 23, Robert Wood Johnson Found., Princeton, NJ ↩︎

Daniel Franco Montoya, Puneet Kaur Chehal, and E. Kathleen Adams, “Medicaid Managed Care’s Effects on Costs, Access, and Quality: An Update,” Annual Review of Public Health 41:1 (2020):537-549 ↩︎

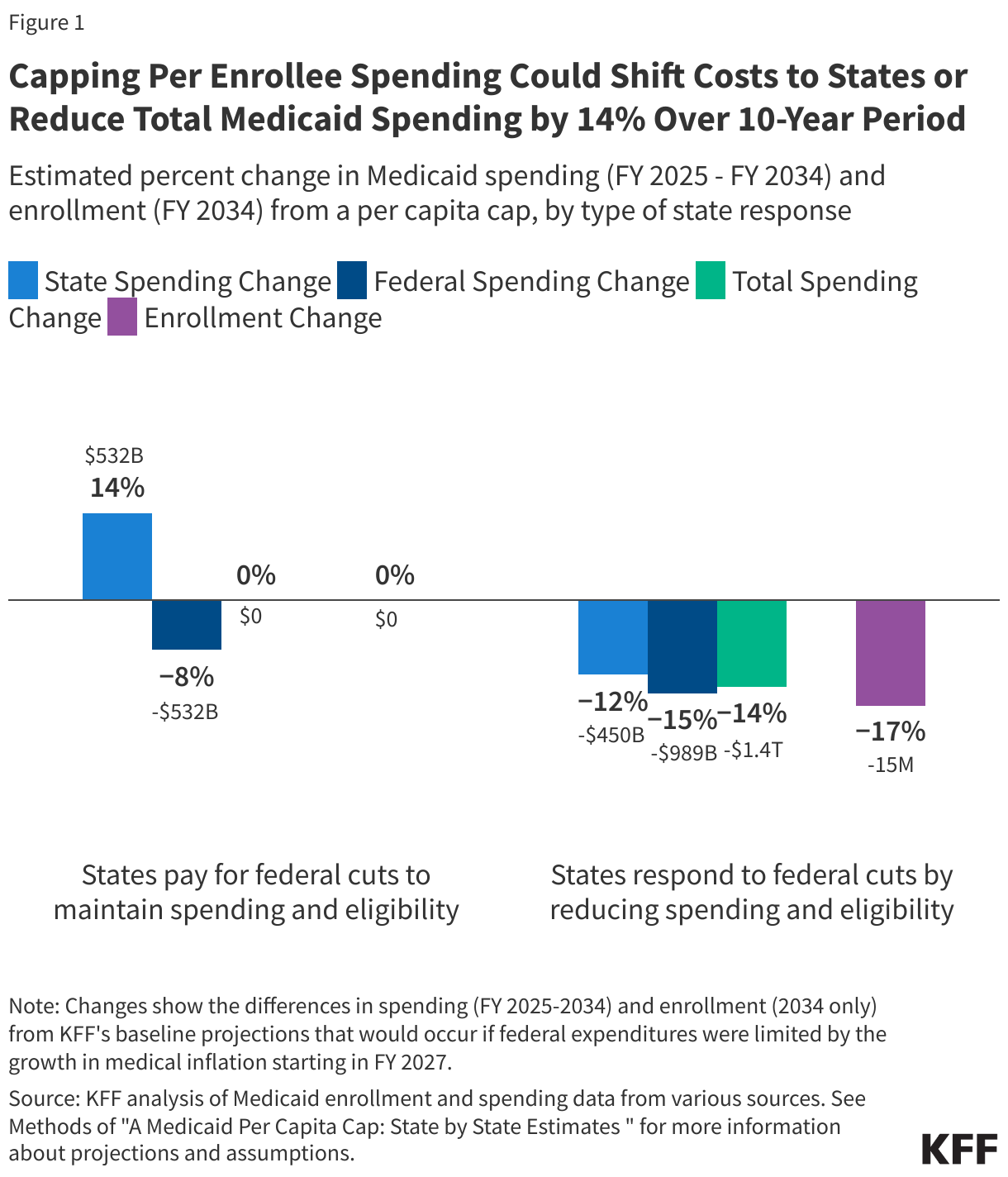

Capping Per Enrollee Spending Could Reduce Federal Medicaid Expenditures by $532 billion to Nearly $1 Trillion Over 10 Years Depending on How States Respond and Result in as Many as 15 Million People Losing Medicaid Coverage by 2034

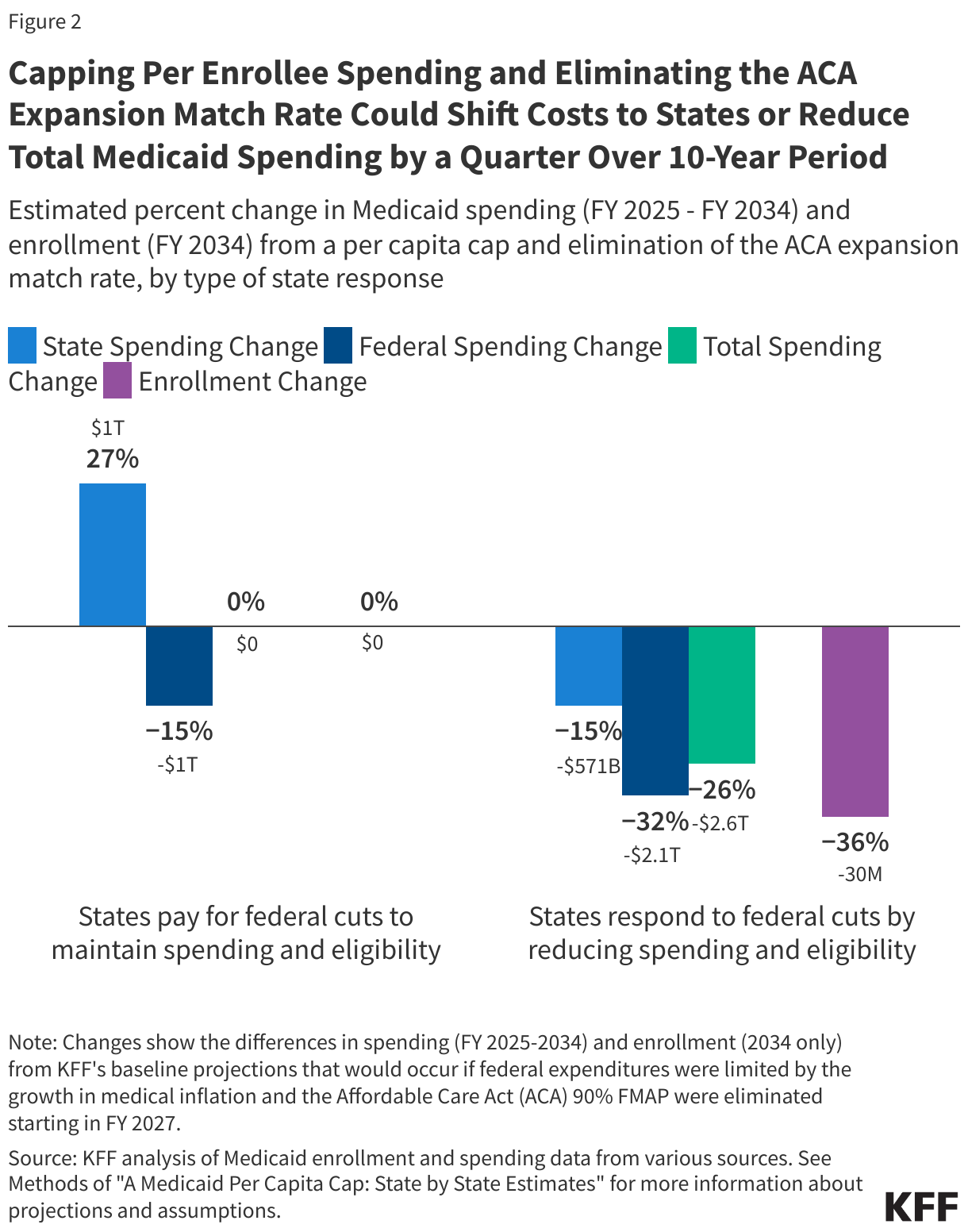

Eliminating the Medicaid Expansion Match Rate at the Same Time Could Push Federal Medicaid Spending Declines to as Much as $2.1 Trillion and Cause 30 Million to Lose Medicaid Coverage

As Congress considers ways to cut Medicaid spending to help finance the extension of federal tax cuts, a new KFF analysis finds that imposing a cap on federal spending per Medicaid enrollee—known as a “per capita cap”—could trigger a decrease in federal Medicaid spending over a 10-year period of $532 billion to almost $1 trillion, depending on how states respond to the cuts. An estimated 15 million people could lose Medicaid coverage by 2034, if states were to respond to the change by reducing their own Medicaid spending and curtailing eligibility.

The size of the cuts and which states would be hit hardest would depend on how states respond, and also whether the policy is combined with other changes, such as ending the 90% federal match for the Affordable Care Act’s Medicaid expansion.

The analysis shows that if states choose to increase their own Medicaid spending to offset federal reductions and maintain coverage and benefits, federal Medicaid spending would fall by $532 billion and state costs would increase by the same amount. State responses to federal cuts may vary.

However, if Congress at the same time eliminates the enhanced federal matching rate for the Medicaid expansion (another significant policy being discussed, and which was examined by a previous KFF analysis), the impact would be bigger. Federal Medicaid spending cuts could range from $1 trillion–if states offset costs–to $2.1 trillion–if states respond by cutting state spending and eligibility over 10 years, with 30 million people losing Medicaid coverage by the end of the period.

In a party-line vote, the Republican-controlled House last night passed a budget resolution that would target cuts to Medicaid of up to $880 billion or more over a decade to help pay for tax cuts.

“The current proposals being discussed by Congress would lead to the largest Medicaid spending cuts and enrollment declines in the program’s history with an unprecedented cut in federal Medicaid funding to states,” said KFF President and CEO Drew Altman. “As our polling and focus groups with voters show, Americans, including many Trump voters, are not expecting, nor would they want, cuts to Medicaid, which would be felt across the country.”

The analysis examines the potential impacts of two of the Medicaid proposals being discussed that would generate significant federal savings. It looks at the combination of them because lawmakers may pursue multiple, simultaneous changes to the program that would have interacting effects. Other proposals being discussed reportedly include imposing Medicaid work requirements, reducing the minimum federal matching rate, restricting states’ use of provider taxes to finance their share of Medicaid spending, and repealing certain Medicaid regulations. Future KFF analyses will examine these proposals as well.

Under the current system, the federal government reimburses states for a share of Medicaid enrollees’ costs, with no upper limit on expenditures, and states pick up the rest. Capping the federal contribution would force states to choose how to offset the funding reductions and could lead to increases in the uninsured rate and reduced revenue for health plans, hospitals and nursing homes.

Other key takeaways of the analysis include:

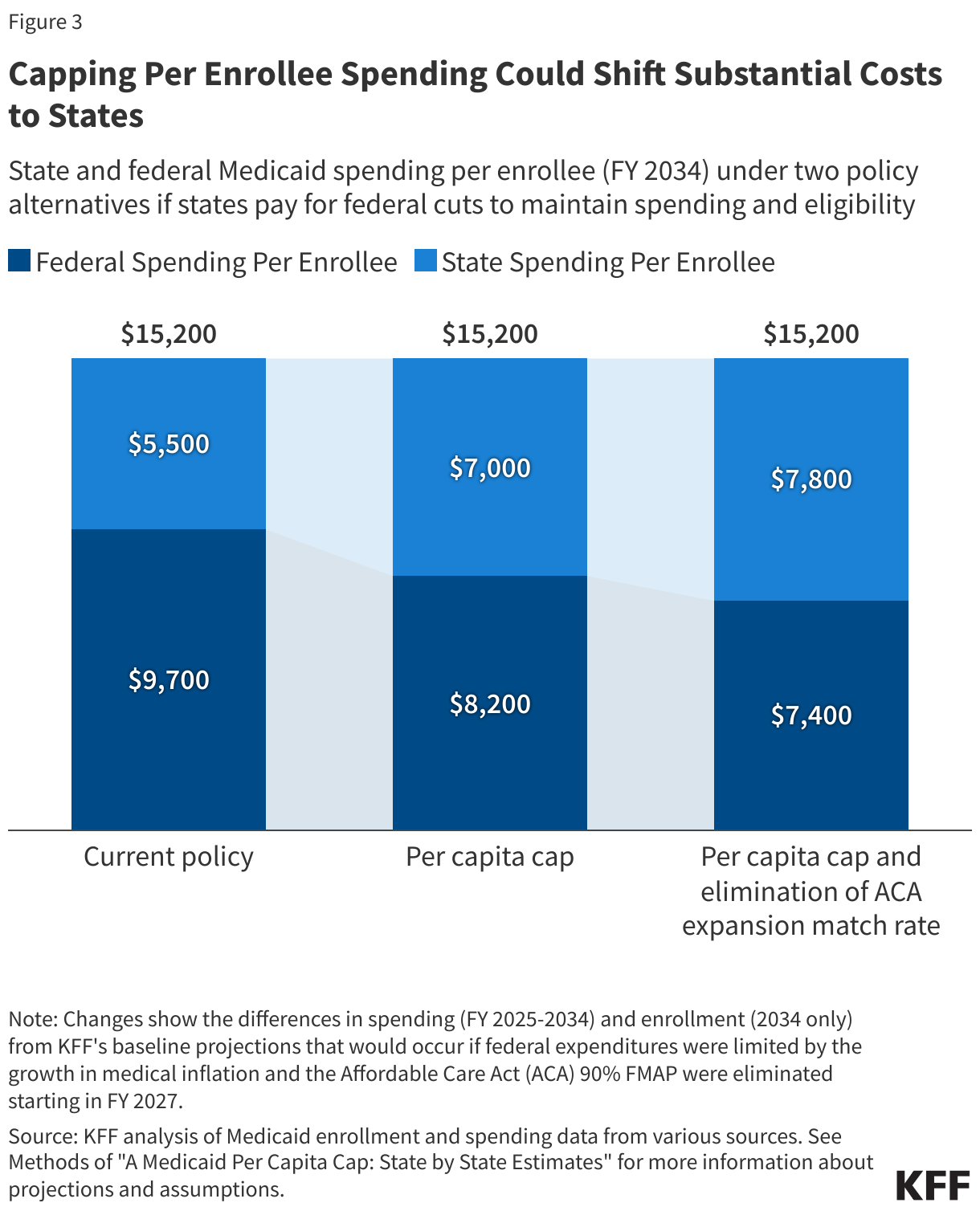

Maintaining current Medicaid benefit levels and enrollment would require states to pay $1,500 more per enrollee under a per capita cap, or up to $2,300 more per enrollee under a per capita cap that is combined with the elimination of the enhanced Medicaid expansion match rate, by FY 2034.

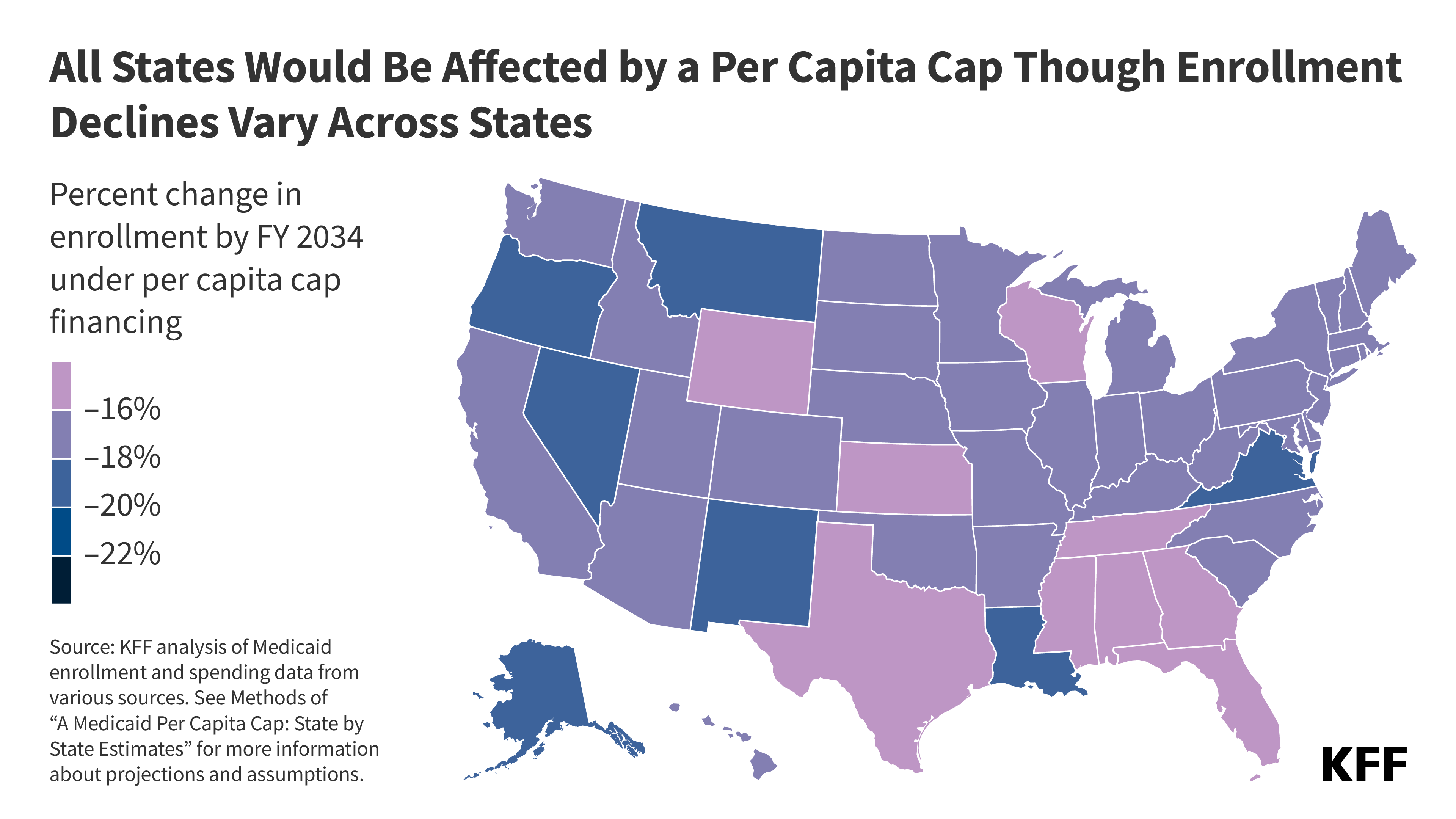

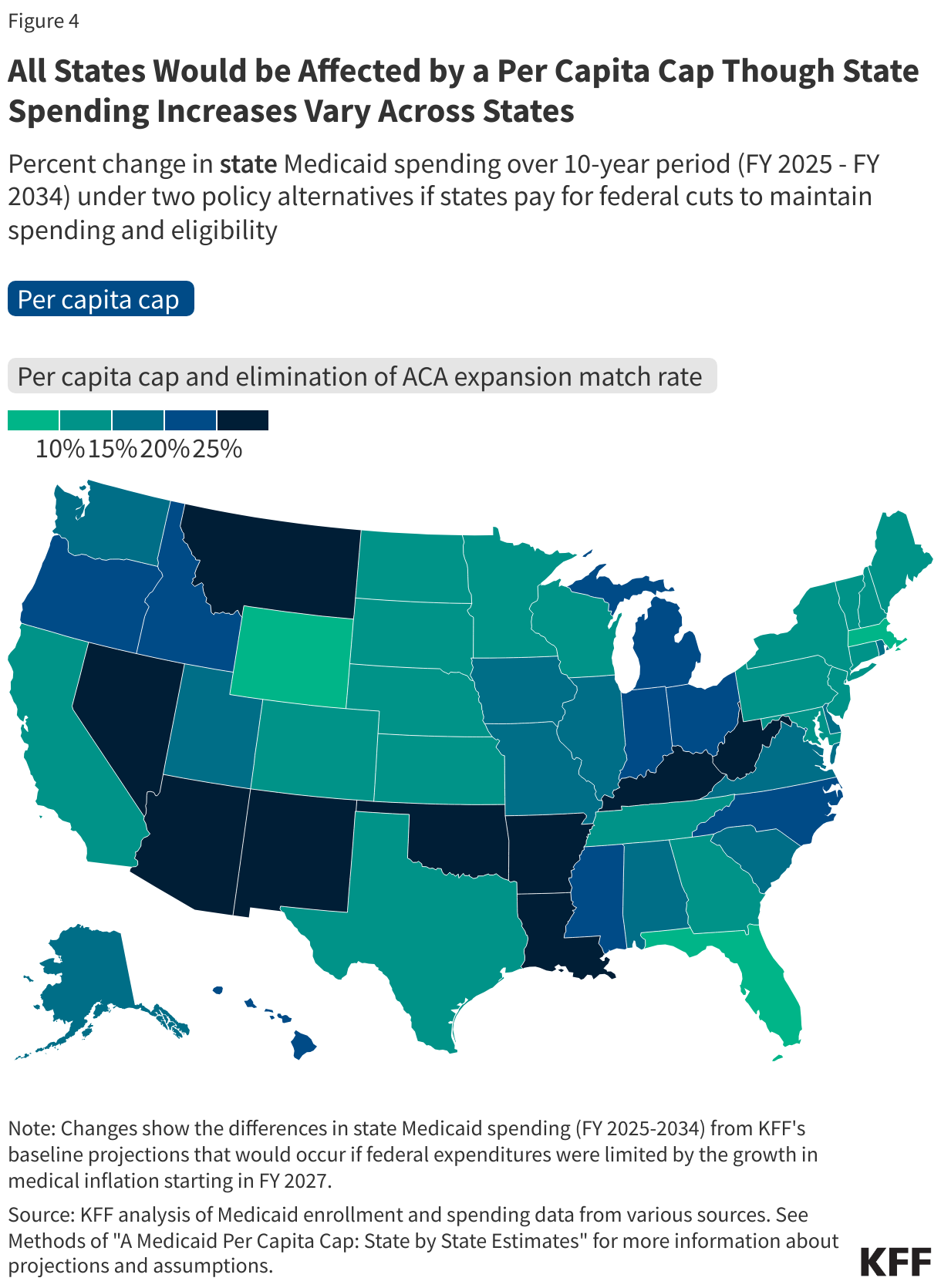

Decreases in Medicaid enrollment would vary by state and could be as high as 57% in some states if Congress implements both per capita cap financing and the elimination of the Medicaid expansion match.

Spending reductions under a per capita cap would compound in future years as the per enrollee cap levels diverge further from spending levels expected without the cap, limiting states’ ability to meet changing program needs.

All states would be affected by a per capita cap, but the magnitude would vary due to differences in the mix of the types of Medicaid enrollees in each state. The effects would vary across eligibility groups because spending for different groups is expected to grow at different rates over time. Also, the elimination of the enhanced Medicaid expansion match rate would only affect the 40 states and the District of Columbia that have adopted the expansion.

For detailed state-by-state impacts of the proposed Medicaid financing changes on spending and enrollment, see Appendix Tables 1 and 2.

A related report released this week highlights the experiences and opinions of Medicaid enrollees who participated in five virtual focus groups that KFF conducted in January with enrollees who voted for President Trump or for Vice President Harris. Despite differences in political leanings, participants reported having favorable experiences with Medicaid and concerns about potential cuts to the program. While some Trump voters enrolled in Medicaid believed there is fraud in the program and were open to work requirements, they also didn’t think that President Trump would follow through on cuts to Medicaid because they believed he understood their financial struggles.

Medicaid covers one in five people in the U.S., and accounts for nearly $1 out of every $5 spent on health care. It covers 41% of all births, nearly half of children with special health care needs, and five in eight nursing home residents.

There are several options under consideration in Congress to significantly reduce Medicaid spending to help pay for tax cuts, with the recently passed House budget resolution targeting cuts to Medicaid of up to $880 billion or more over a decade. Medicaid is the primary program providing comprehensive health and long-term care to one in five people living in the U.S and accounts for nearly $1 out of every $5 spent on health care. Medicaid is administered by states within broad federal rules and jointly funded by states and the federal government, meaning restrictions in federal Medicaid spending could leave states with tough choices about how to offset reductions through cuts to Medicaid, cuts to other programs, or tax increases.

This analysis examines the potential impacts on states, Medicaid enrollees, and providers of implementing a per capita cap on federal Medicaid spending, which is one proposal that has been discussed in Congress. The analysis assumes, based on proposals floated in Congress, that the plan would cap federal Medicaid spending growth per enrollee for each of the five major eligibility groups at medical inflation. Given the likelihood of multiple, simultaneous changes to Medicaid and the interactive nature of those changes, the analysis also illustrates the effects of a per capita cap on Medicaid if implemented jointly with the elimination of the 90% federal match rate for the Affordable Care Act (ACA) expansion, another significant policy change that has been discussed in Congress and which was examined by a previous KFF analysis. Other proposals to reduce federal Medicaid spending have also been reportedly raised, including work requirements, a reduced federal matching rate, limits on provider taxes to finance the state share of Medicaid spending, and repeal of certain Medicaid regulations issued by the Biden administration. Future KFF analyses will examine these proposals as well.

Key takeaways

The estimated effects of a per capita cap depend highly on what assumptions are made about policy specifications, future growth in Medicaid spending, and states’ responses to federal cuts.

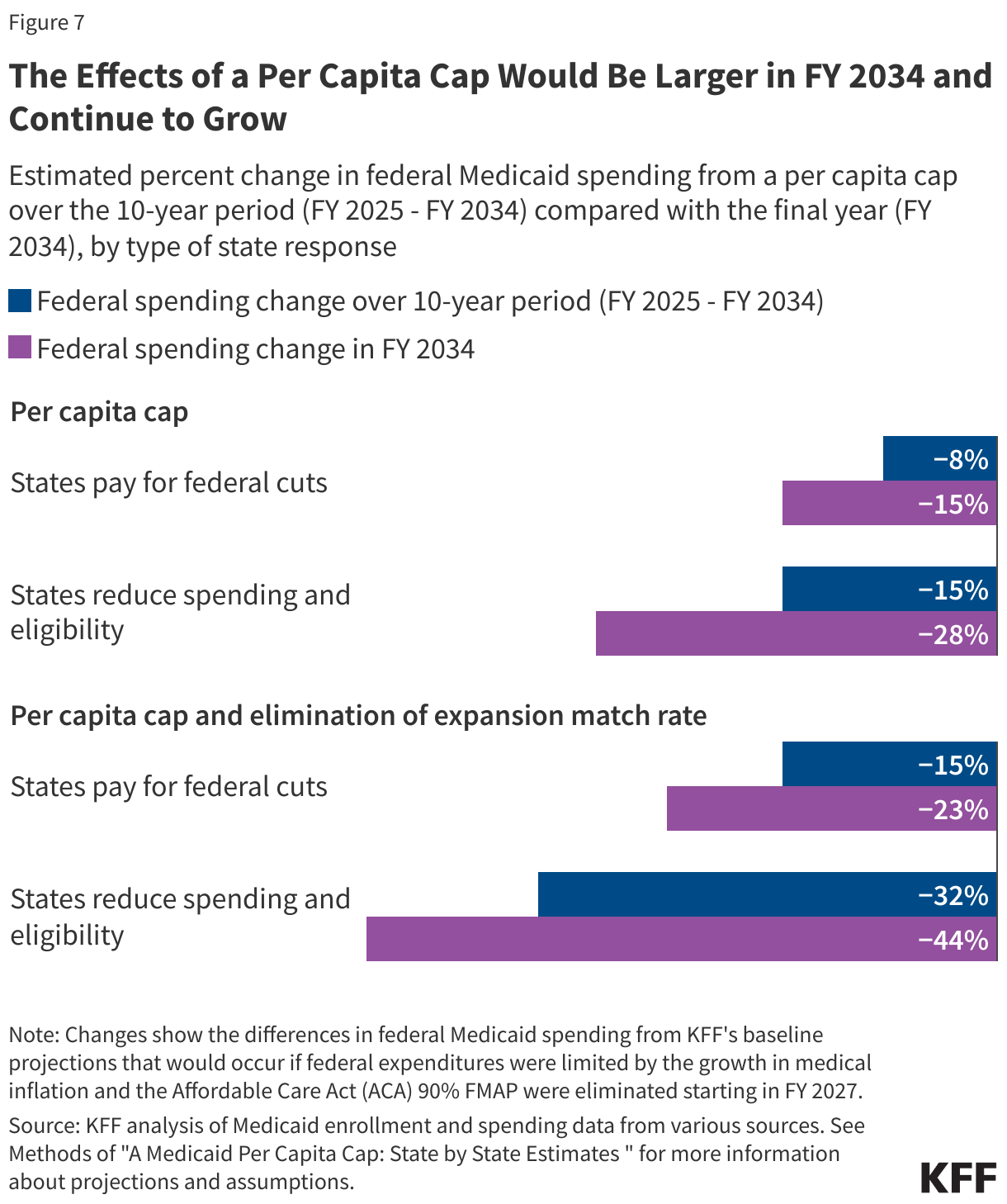

Capping per enrollee spending could reduce federal spending by $532 billion to nearly $1 trillion dollars between FY 2025 and FY 2034. Depending on how states respond, the policy could shift costs to states by $532 billion and leave total Medicaid spending unchanged or total Medicaid spending could decline by 14% (or $1.4 trillion).

If per capita caps were implemented jointly with the elimination of the enhanced ACA expansion match rate, federal Medicaid spending could decline by $1 trillion to $2.1 trillion dollars between FY 2025 and FY 2034. Depending on how states respond, this combination of policies could shift costs to states by $1 trillion and leave total Medicaid spending unchanged or total Medicaid spending could decline by a quarter (or $2.6 trillion).

If states reduced Medicaid eligibility proportionally to the cuts in federal spending, 15 million enrollees could lose Medicaid coverage under a per capita cap by the final year of the analysis, with that figure doubling to 30 million when combined with elimination of the ACA expansion match rate.

States would face tough choices about Medicaid’s future under a per capita cap: maintaining current Medicaid benefit levels and enrollment would require states to pay $1,500 to $2,300 more per enrollee in the final year of the analysis.

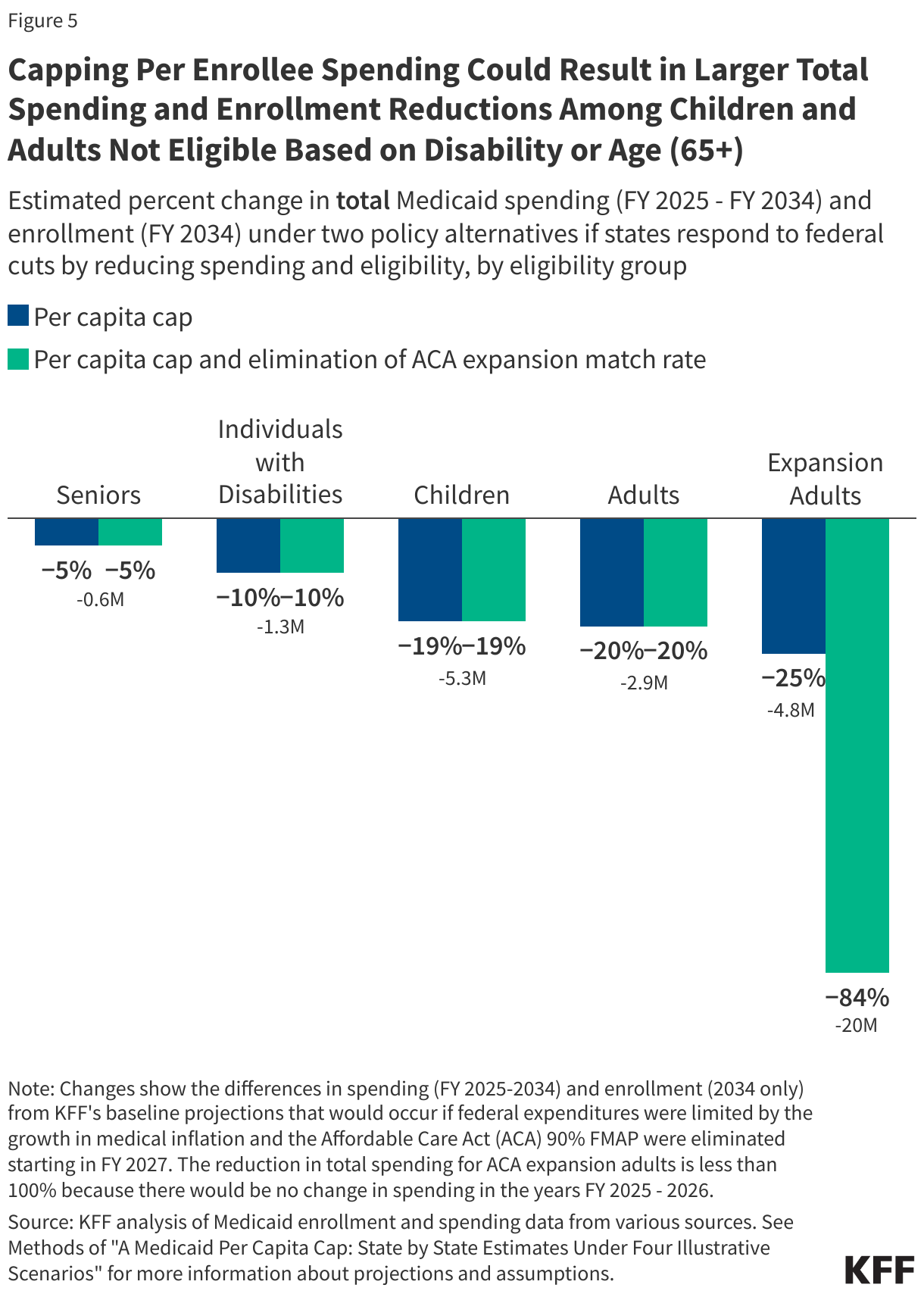

The effects of a per capita cap differ across eligibility groups because spending for different eligibility groups is expected to grow at different rates, with larger estimated effects among children and adults who are not eligible because they have a disability or are ages 65 and older.

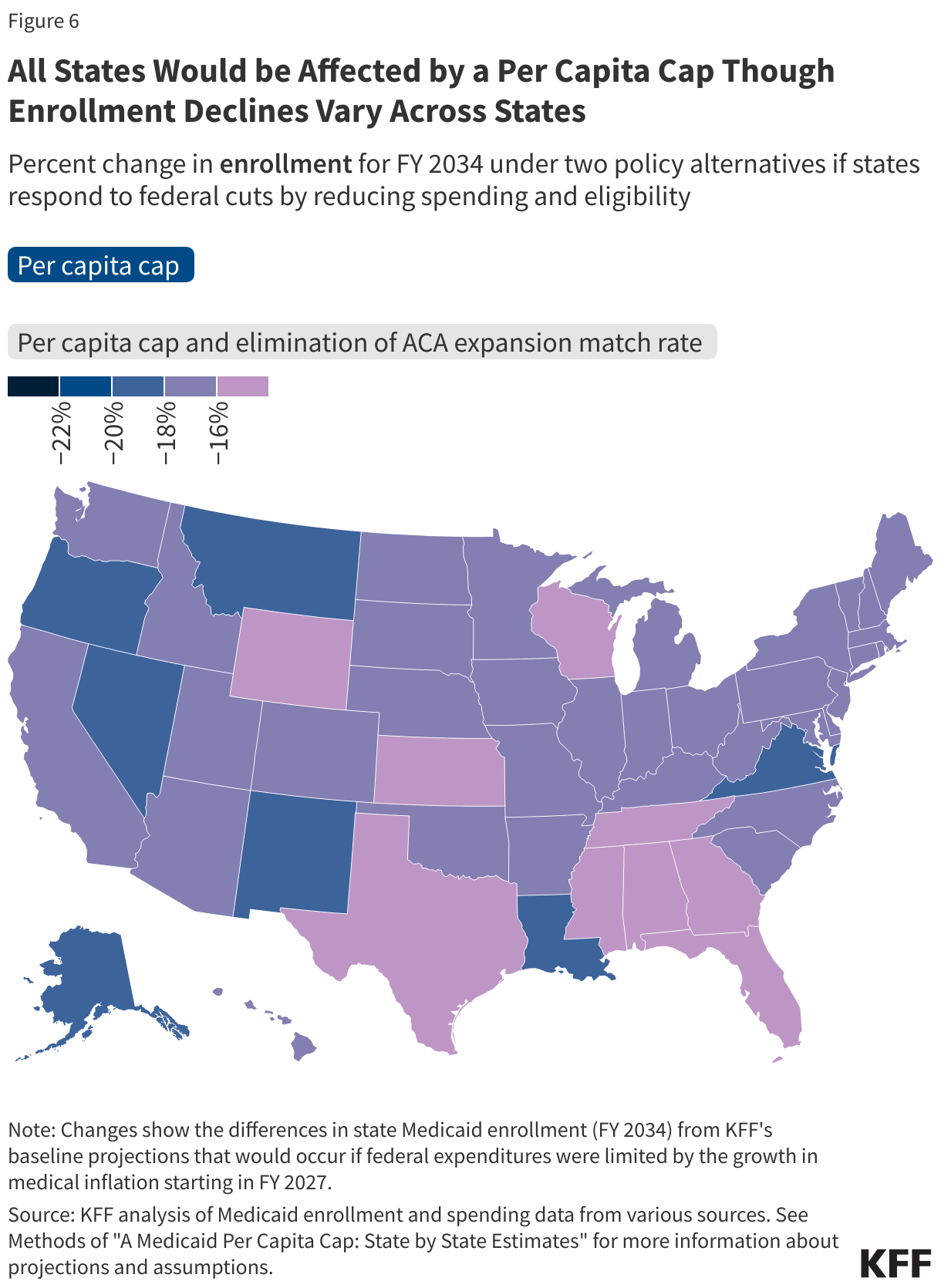

All states would be affected by a per capita cap, but the size of the effects vary due to differences in the mix of enrollees. Depending on state responses, state spending could increase up to 57% in some states if they chose to pay for the cuts. Enrollment could decrease by similar levels if states chose to restrict eligibility in response to the federal funding cuts.

Spending reductions under a per capita cap would compound over time as expected increases in Medicaid spending diverge from the caps. The effects would be smaller immediately following implementation, larger in FY 2034, the final year of this analysis, and continue to grow in the years after 2034. A per capita cap can provide lower and more predictable federal costs over time, but it would also fundamentally change the Medicaid federal-state partnership by eliminating the federal guaranteed match and transferring new financial risk to states. States would face significant challenges in efforts to pay for federal cuts and there would be pressure to reduce benefits and eligibility, with even larger effects if a per capita cap were paired with other Medicaid cuts. Beyond reduced Medicaid spending and enrollment, there could be increases in the number of people who are uninsured, fewer covered benefits for future Medicaid enrollees, and reduced revenues available for health plans and providers such as hospitals and nursing facilities.

What is the proposed policy change?

Medicaid spending is currently shared by states and the federal government with a guarantee to states for federal matching payments without a cap on federal expenditures. The percentage of costs paid by the federal government (known as the federal medical assistance percentage or “FMAP”) for most Medicaid enrollees is determined by a formula set in law designed to provide a higher federal match rate for states with lower per capita incomes. There are also higher match rates for certain services and populations like the ACA expansion group (90%). This leads to variation in the federal share of Medicaid spending across states. There is also considerable variation in per enrollee spending across states, due to state flexibility to determine eligibility levels, benefits, and provider payment, and across eligibility groups,reflecting differences in health care needs and utilization.

This analysis estimates the impact of implementing a per capita cap on the federal share of Medicaid spending. One proposal under consideration would “establish a per capita cap [on federal Medicaid expenditures] for each of the different enrollment populations set to grow at medical inflation.” While specifics on the implementation of this policy would be included in a legislative proposal, further details have yet to be released, and assumptions made here may differ from details included in proposed legislation. To estimate a per capita (i.e., per enrollee) cap policy, this analysis first establishes FY 2025 per enrollee spending as the base year estimate; then, starting in FY 2027, the analysis limits federal spending growth for the five major eligibility groups (children, adults, expansion adults, people with disabilities and aged 65+) to the consumer price index (CPI-U) plus 0.4 percentage points, which is KFF’s estimate of the difference between CPI-U and medical inflation (CPI-M) over the past 20 years (see Methods).

The analysis also estimates the combined impact of implementing a per capita cap and eliminating the ACA expansion federal match rate. The combined policy would include the same per capita caps on federal spending and also assumes that, starting in FY 2027, expenditures for people eligible through Medicaid expansion would be matched at each state’s traditional FY 2026 FMAP rate. This part of the analysis accounts for the interactive effects of these two policy changes; therefore, savings are lower than if each policy was modeled separately and the totals were added together (see Methods). There are a number of other Medicaid policy changes that have been suggested, and policy estimates would likely differ depending on the combination of policies and their interactive effects.

What is the potential impact on Medicaid spending?

This analysis does not make assumptions about specific state behavioral responses and instead examines how the impacts of the two policy alternatives vary based on two types of state responses to the cuts. The state responses are designed to illustrate the spectrum of potential policy change effects. However, in practice, each state is likely to respond to the policy change differently and spending impacts overall would likely fall within the range. While some states may choose to increase state spending to maintain current programs with substantially reduced federal funding, many would likely need to make programmatic cuts, making both the lower end and higher end estimates unlikely. The analysis does not explore people’s insurance coverage after losing Medicaid; some may enroll in another source of coverage, but many others would likely become uninsured. The estimates presented here are not directly comparable to the estimates of federal savings from the Congressional Budget Office (CBO) because CBO’s estimates account for people enrolling in other coverage and make assumptions about how states would respond in the aggregate. While the estimates assume that spending per enrollee by eligibility group would grow uniformly across states based on CBO’s national projections, it is likely that growth rates would vary by state, and that a cap would therefore have varying effects

Per Capita Cap

In analyzing the effects of a per capita cap on Medicaid spending, KFF considered the following two types of state responses.