KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Every Friday, we’re recapping the past week in the coronavirus pandemic from our tracking, policy analysis, polling, and journalism. This week, total deaths due to COVID-19 in the U.S. surpassed 100,000 on Wednesday, May 27. That day ended with approximately 100,400 total confirmed deaths. Total cases in the U.S. are still climbing, and this week increased by 144,000, bringing the cumulative total of cases past 1.7 million. Across 40 states reporting this data as of yesterday, 43% of deaths due to COVID-19 occurred in long-term care facilities.

Meanwhile, since last Thursday, restaurants have reopened to dine-in service in 4 more states, and 4 more states have eased or lifted their gatherings ban. All but two states have eased or lifted at least one social distancing requirement.

Here are more of the latest coronavirus stats from KFF’s tracking resources:

Global Cases and Deaths: This week, total cases worldwide passed 5.8 million – with approximately 707,000 new confirmed cases added between May 21 and May 28. There were approximately 29,300 new confirmed deaths worldwide between May 21 and May 28.

U.S. Cases and Deaths: Total confirmed deaths in the U.S. surpassed 100,000 this week. There have been over 1.7 million total confirmed cases in the U.S. There were approximately 145,000 new confirmed cases and 6,900 confirmed deaths in the United States between May 21 and May 28.

U.S. Tests: There have been over 15.6 million total COVID-19 tests with results in the United States —approximately 2.6 million were added since May 21. The seven-day rolling average rate of positive tests (between May 21 and May 28) was 10.7%. In the last seven days, 0.6% of the total U.S. population was tested.

Social Distancing: 49 states have eased at least one social distancing measure.

Stay At Home Order: Original stay at home order in place in 17 states, stay at home order eased or lifted in 28 states, no action in 6 states

Mandatory Quarantine for Travelers: Original traveler quarantine mandate in place in 16 states, traveler quarantine mandate eased or lifted in 8 states, no action in 27 states

Non-Essential Business Closures: Original non-essential business closures still in place in 2 states, some or all non-essential business permitted to reopen (some with reduced capacity) in 44 states, no action in 5 states

Large Gatherings Ban: Original gathering ban/limit in place in 28 states, gathering/ban limit eased or lifted in 22 states, no action in 1 states

State-Mandated School Closures: Closed in 7 states, closed for school year in 36 states, recommended closure in 1 state, recommended closure for school year in 6 states, rescinded in 1 state

Restaurant Limits: Original restaurant closures still in place in 18 states, restaurants re-opened to dine-in service in 32 states, no action in 1 state

Primary Election Postponement: Postponement in 14 states, cancelled in 1 state, no postponement in 36 states

Emergency Declaration: There are emergency declarations in all states and D.C.

Waive Cost Sharing for COVID-19 Treatment: 3 states require, state-insurer agreement in 3 states; no action in 45 states

Free Cost Vaccine When Available: 9 states require, state-insurer agreement in 1 state, no action in 41 states

States Requires Waiver of Prior Authorization Requirements: For COVID-19 testing only in 5 states, for COVID-19 testing and treatment in 6 states, no action in 40 states

Early Prescription Refills: State requires in 18 states, no action in 33 states

Premium Payment Grace Period: Grace period extended for all policies in 9 states, grace period extended for COVID-19 diagnosis/impacts only in 5 states, no action in 35 states, expired in 2 states

Marketplace Special Enrollment Period: Marketplace special enrollment period still active in 6 states, ended in 6 states, no special enrollment period in 39 states

Paid Sick Leave: 13 states enacted, 2 proposed, no action in 36 states

38 states overall have taken mandatory action expanding access to telehealth services through private insurers, including:

New Requirements for Coverage of Telehealth Services: Parity with in-person services in 6 states, broad coverage of telehealth services in 6 states, limited coverage of telehealth services in 6 states, no action in 33 states

Waiving or Limiting Cost-Sharing for Telehealth Services: Waived for COVID-19 services only in 7 states, waived or limited for all services in 9 states, no action in 35 states

Reimbursement Parity for Telehealth and In-Person Services: Required for all services in 17 states, no action in 34 states

Require Expanded Options for Delivery of Telehealth Services: Yes in 35 states, for behavioral health services only in 1 state, no action in 15 states

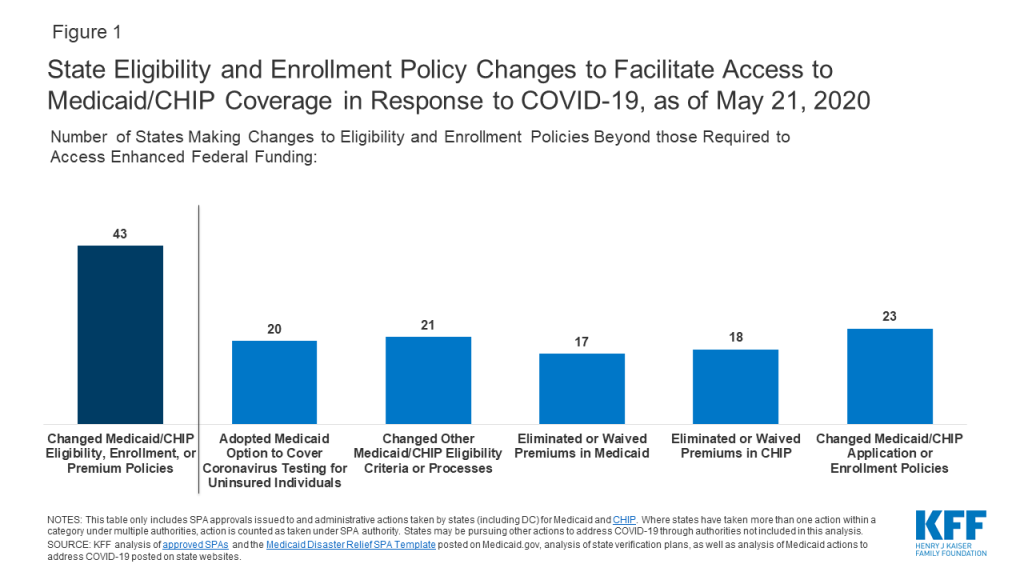

Approved Section 1115 Waivers to Address COVID-19: 1 state (Washington) has an approved waiver

Approved Section 1135 Waivers: 51 states have approved waivers

Approved 1915 (c) Appendix K Waivers: 45 states have approved waivers

Approved State Plan Amendments (SPAs): 38 states have temporary changes approved under Medicaid or CHIP disaster relief SPAs, 1 state has an approved traditional SPA

Other State-Reported Medicaid Administrative Actions: 51 states report taking other administrative actions in their Medicaid programs to address COVID-19

Adults at Higher Risk of Serious Illness if Infected with Coronavirus: 38% of all U.S. adults are at risk of serious illness if infected with coronavirus (92,560,223 total) due to their age (65 and over) or pre-existing medical condition. Of those at higher risk, 45% are at increased risk of serious illness if infected with coronavirus due to their existing medical condition such as such as heart disease, diabetes, lung disease, uncontrolled asthma or obesity. Among nonelderly adults — low-income, American Indian/Alaska Native & Black adults have a higher risk of serious illness if infected with coronavirus. In both cases – for race and household income – the higher risk of serious illness if infected with coronavirus is chiefly due to a higher prevalence of underlying health conditions and longstanding disparities in health care and other socio-economic factors.

Larry Levitt: COVID-19 and Massive Job Losses Will Test the US Health Insurance Safety Net (JAMA Forum)

Five Things to Know about the Cost of COVID-19 Testing and Treatment (Issue Brief)

N., Canada, Jamaica To Convene World Leaders In Effort To Boost Funding For Developing Countries; AP, Devex Examine Leadership, Key Development Players During Pandemic (KFF Daily Global Health Policy Report)

Trackers and Tools

COVID-19 Coronavirus Tracker – Updated as of May 29 (Interactive)

State Data and Policy Actions to Address Coronavirus – Updated as of May 28 (Interactive)

Medicaid Emergency Authority Tracker: Approved State Actions to Address COVID-19 – Updated as of May 28 (Issue Brief)

In this May 2020 post for The JAMA Health Forum, Larry Levitt explores how the massive and rapid job losses sparked by the COVID-19 pandemic will test the ACA’s coverage safety net – and how different policies could strengthen or weaken it.

In this May 2020 post for The JAMA Health Forum, Larry Levitt explores how the massive and rapid job losses of the past few months will test the ACA’s coverage safety net – and how different policies could strengthen or weaken it.

Other contributions to The JAMA Forum are also available.

The COVID-19 pandemic has upended the economy, causing massive job loss and disrupting health coverage for millions of people. KFF estimates that of 78 million people in families experiencing a job loss as of May 2, 26.8 million could have lost job-based coverage and could become uninsured.

Coverage loss during a pandemic is particularly concerning. In a previous analysis, we estimated that treatment costs for people who are hospitalized for COVID-19 could average $20,000, rising to more than $80,000 in more complex cases. Congress has not required access to free treatment of COVID-19 for the uninsured; however, the CARES Act established a Provider Relief Fund, an unspecified portion of which will be used to reimburse providers treating uninsured patients with COVID-19. Substantial loss of employer-sponsored insurance (ESI) also puts millions at risk of being unable to afford other health care. In late 2018, a KFF/LA Times survey found that 54% of adults with ESI reported someone in the household having at least one chronic condition, such as heart disease, serious mental illness, diabetes, or cancer.

Most of the 26.8 million who are at risk of losing their job-based coverage are eligible to remain in that coverage under a federal law, the Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA). COBRA requires that when individuals stand to lose job-based coverage due to a qualifying event – such as a layoff – they can continue enrollment in their existing group plan, usually at full cost to the enrollee.

Background on COBRA

COBRA applies to firms with 20 or more workers. When the qualifying event is termination of employment, individuals are generally eligible for up to 18 months of COBRA continuation coverage. (Other qualifying events, such as death of the covered employee or loss of dependent status, make people eligible for up to 36 months of COBRA continuation coverage.) Usually, individuals have 60 days to elect COBRA continuation, and another 45 days to pay the first premium, dating back to their qualifying event. However, a recent emergency regulation issued by the Trump Administration extends the amount of time people have to elect COBRA and pay premiums by 60 days after the national emergency period ends. For example, assuming the emergency period ends this summer on July 25, someone who received a COBRA notice on April 1 would have until late November to elect continuation coverage. The emergency regulation also extends the amount of time employers have to notify individuals of their right to elect COBRA continuation (usually 30 days) by the same amount of time.

For most people, particularly following job loss, the cost of COBRA continuation coverage is prohibitively expensive. Individuals must pay the total cost of the group health coverage (employee and employer share) plus a 2 percent administrative fee. On average, the total annual cost of employer-sponsored health coverage offered by firms of 20 or more in 2019 was $7,012 for single coverage and $20,599 for family coverage.

Looking at the Medical Expenditure Panel Survey, only about 130,000 unemployed nonelderly adults had health coverage through COBRA in 2017, a year when more than 11.5 million nonelderly adults were unemployed. The uninsured rate among the unemployed was close to 30% that year. This suggests that unsubsidized COBRA does little to prevent coverage loss among people who lose their jobs.

The high cost of COBRA also invites adverse selection – that is, the people with highest health costs and risks are most likely to elect it. Our analysis finds average annualized health spending for COBRA enrollees (out-of-pocket and plan spending together) in 2018 was nearly twice that for other large group plan enrollees ($11,695 vs $6,144).

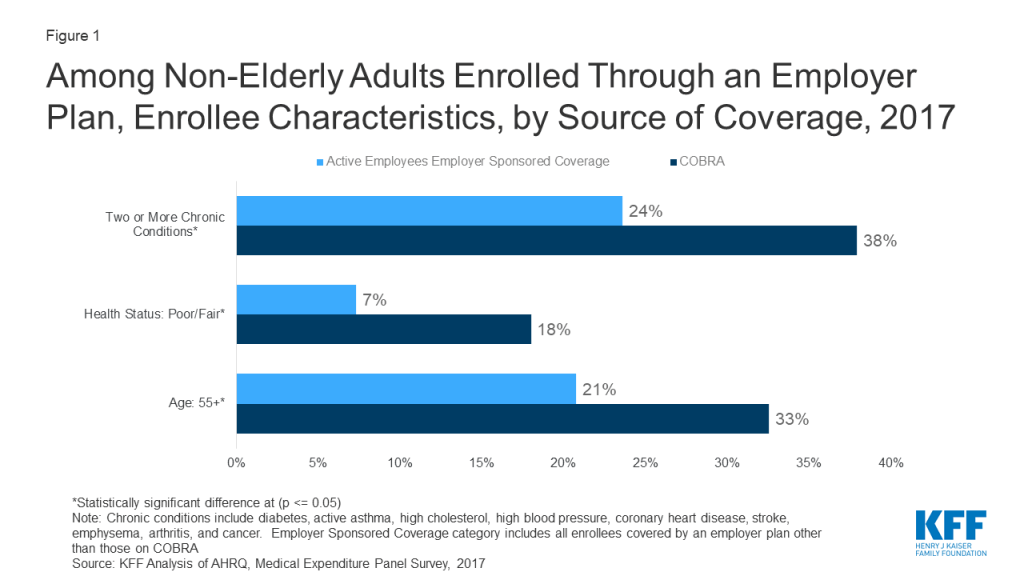

COBRA enrollees tend to be older than people enrolled in current job-based plans; on average 33% of COBRA enrollees are 55 or older, compared to 21% of active employees. In addition, COBRA enrollees are more likely to have multiple chronic conditions (38% vs 24%), and more than twice as likely to report poor health status (18% vs 7%) (Figure 1).

Figure 1: Among Non-Elderly Adults Enrolled Through an Employer Plan, Enrollee Characteristics, by Source of Coverage, 2017

COBRA subsidies: past and current proposals

At several times in the past, Congress provided for partial subsidy of COBRA premiums for displaced workers. The American Recovery and Reinvestment Act of 2009 (ARRA) provided COBRA premium subsidies of 65% to help unemployed workers afford to continue enrollment in health coverage offered by their former employer. The ARRA COBRA subsidy was available to eligible individuals for up to 9 months initially; the eligibility period was later increased to up to 15 months. Eligible individuals were required to pay no more than 35% of COBRA premiums. Their former employers paid the other 65%, which was reimbursed through a credit against their payroll tax liability. Eligibility for the COBRA subsidy was phased out for higher income individuals with adjusted gross income between $125,000 and $145,000 ($250,000 to $290,000 for joint returns). The final evaluation of the ARRA COBRA subsidy program found that 34% of eligible individuals opted for subsidized COBRA coverage. Participation rates were highest among individuals with higher incomes and higher education. Among eligible individuals who did not elect COBRA, 80% said cost was the most important factor in their decision, even with the substantial subsidy.

In addition, ARRA amended an earlier COBRA subsidy program enacted in 2002 – the Health Coverage Tax Credit (HCTC) – specifically for workers laid off due to international trade-related factors, and who received Trade Adjustment Assistance benefits and met other qualifications. When enacted, the HCTC subsidized 65% of premiums for COBRA and certain other qualified health coverage options; ARRA increased the HCTC subsidy to 80%. A U.S. General Accounting Office (GAO) review found that the partial subsidy and complex eligibility rules depressed take up of the HCTC. About 5% of potentially eligible individuals received the tax credit. After ARRA increased the HCTC subsidy, GAO found about 5.5% of potentially eligible individuals took the credit.

Recently, a fourth coronavirus relief measure, the Heroes Act, was passed in the House of Representative. It includes a provision to subsidize 100% of COBRA premiums for workers who would otherwise lose job-based coverage due to loss of employment or reduction in hours worked. People experiencing other COBRA qualifying events – such as death of the covered worker – would not be eligible for the subsidy. In addition, for furloughed workers whose health benefits continue while pay is suspended, the subsidy would also cover 100% of the employee’s portion of health premiums (employers would continue to pay their portion). Employers would cover the entire cost of health coverage for eligible individuals, then be reimbursed through a credit against their payroll tax liability or via a refund. The subsidy could be claimed for COBRA coverage months between March 1, 2020 and January 31, 2021. People would lose eligibility for the subsidy when they become eligible for other employer-sponsored health coverage or Medicare.

Other options and tradeoffs for people losing job-based coverage

The KFF analysis estimates that about 79% of people who have lost job-based coverage and could become uninsured are eligible for either Medicaid/CHIP (12.7 million, or 47%) or for subsidized marketplace plans (8.4 million, or 31%). Approximately 5.7 million will not be eligible for subsidized coverage for a variety of reasons.

Eligibility for coverage doesn’t always translate to enrollment. In 2018, there were more uninsured individuals eligible for subsidized marketplace plans that were enrolled in such plans — 9.2 million uninsured vs. 8.6 million enrolled. In addition that year 6.7 million uninsured adults and children were eligible for Medicaid or other public coverage.

In evaluating health coverage options, people would consider differences in premiums, cost sharing, and provider networks, among other factors. In addition, awareness of coverage options in the first place, as well as complexity of the application process affects enrollment outcomes. Subsidized COBRA would add a new coverage option, potentially changing the tradeoffs people face and their ability to remain insured.

Premiums and Cost Sharing

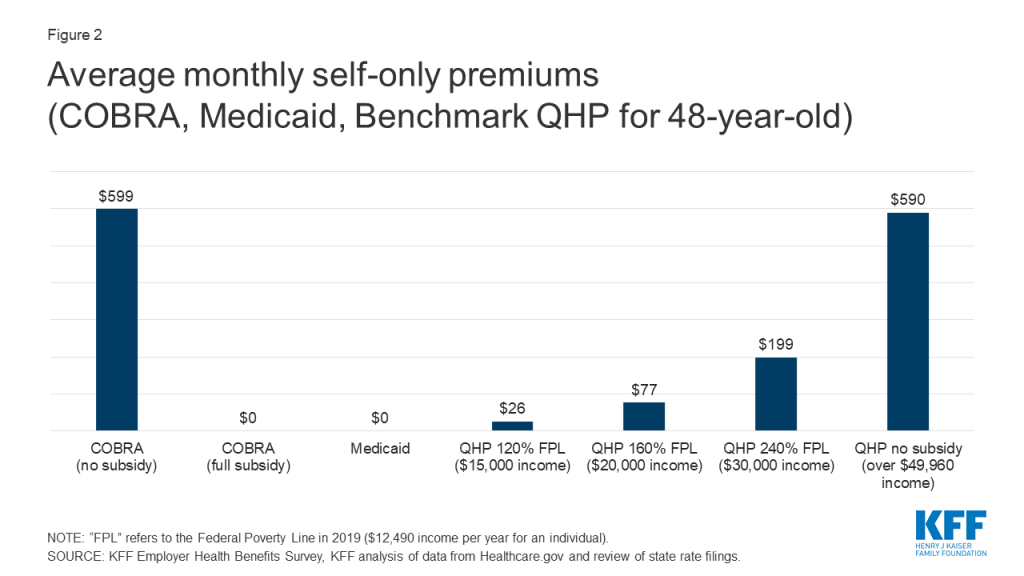

For the newly unemployed, unsubsidized COBRA generally will be the most expensive coverage option. Medicaid coverage in most states requires no premium. Marketplace plans are subsidized on a sliding scale for eligible individuals with income between 100% and 400% FPL; at every income level people must contribute at least a portion of the monthly premium for the benchmark plan, and the required premium contribution approaches 10 percent of gross income at 300% FPL. If fully subsidized, the premium cost of COBRA for individuals would be comparable to Medicaid, and would be less (far less, depending on income) than premium contribution required to purchase the average benchmark silver plan on the ACA Marketplace. (Figure 2)

Figure 2: Average monthly self-only premiums (COBRA, Medicaid, Benchmark QHP for 48-year-old)

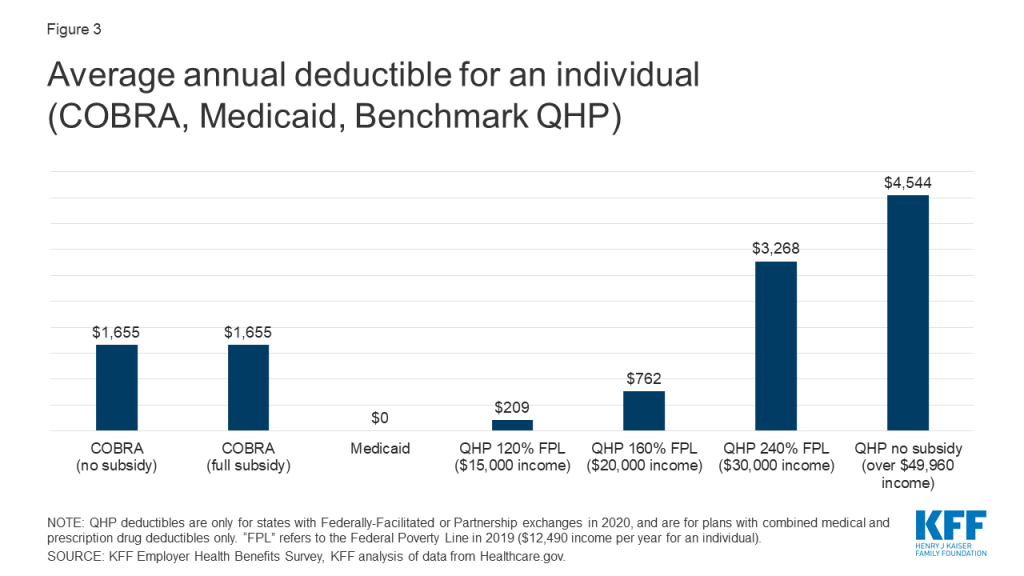

Under employer-based plans annual deductibles tend to be high. The average actuarial value of employment based plans in 2017 was about 85%, somewhat more generous than a gold-level marketplace plan. The average annual deductible for self-only coverage under job-based plans was $1,655 in 2019. Most employer plans do not vary deductibles based on income.

Under Marketplace plans, cost sharing is much higher. Benchmark silver plans have an actuarial value of roughly 70%, with deductibles averaging $4,544. However, cost sharing subsidies are available to lower-income enrollees on a sliding scale, and most marketplace enrollees receive them. For people with incomes of 100%-150% FPL, the silver plan AV is increased to 94% and the average annual deductible is reduced to $209. Between 150% and 200% FPL, the silver plan AV is increased to 87% and the average annual deductible is $762. Cost sharing subsidies are more modest between 200% and 250% FPL; the silver plan AV increases slightly to 74% and the average deductible is $3,268.

Medicaid generally does not impose deductibles; in 22 states, adults face limited copays for certain services (e.g., 13 states require copays that generally are up to $4 for physician visits, while 18 states require copays ranging from $0.50 to $4 for generic prescription drugs.) (Figure 2)

Proposed COBRA subsidies would not affect the level of cost sharing under continuation coverage. As a result, low income individuals (less than 200% FPL) could find cost sharing reduced if they transition to Medicaid or CSR marketplace plans; otherwise people would tend to face higher cost sharing under marketplace plans compared to COBRA continuation (Figure 3).

Figure 3: Average annual deductible for an individual (COBRA, Medicaid, Benchmark QHP)

Provider networks

Large employer health plans tend to offer broad choice of providers in their networks. In 2019, 79% of large firms characterized their largest plan option as having a “very broad” provider network, although six percent of large firms offered at least one narrow network plan option Only 2% of offering firms say they eliminated a hospital or health system from a provider network in the prior year to reduce plan costs. By contrast, marketplace plans rely heavily on narrow provider networks to control costs, and are dominated by plans with restrictive provider networks. This year 78% of qualified health plans (QHP) offered in healthcare.gov states are closed network plans (HMOs or EPOs), compared to 60% in 2016.

Though research indicates that, overall, most primary care providers and specialists accept Medicaid, provider participation in Medicaid is a subject of much debate. Providers are less likely to accept new Medicaid patients than new patients insured by other payers, and lower participation rates among some types of specialists remain an area of concern. However, gaps in access to certain providers including psychiatrists, some specialists, and dentists, are ongoing challenges in Medicaid and often in the health system more broadly due to overall provider shortages, and geographic maldistribution of health care providers. In most states, Medicaid coverage is provided through private managed care organizations (MCOs), and MCOs are responsible under their contracts with states for ensuring adequate provider networks.

Added enrollment barriers

In most states, people losing job-based coverage who are eligible to enroll in marketplace plans must do so within a limited period of time. Loss of other coverage is a qualifying event that triggers a 60-day special enrollment period (SEP), when people can sign up for marketplace coverage outside of the annual open enrollment period. (The recent emergency regulation extending the time people have to elect COBRA does not extend the duration of marketplace SEPs.) Complicating this process, new rules adopted in 2017 require applicants to document eligibility for the SEP before they can enroll in marketplace coverage. That appears to have made it harder for people to use the SEP. The federal marketplace resolved some 800,000 SEP verifications over 2018 and 2019. By contrast, prior to adoption of the more stringent verification requirements, there were nearly 950,000 SEP enrollments during the first half of 2015 alone.

The ACA establishing streamlined and modernized eligibility and enrollment systems for Medicaid across all states. To support states as enrollment in Medicaid grows and ensure enrollees maintain coverage, federal legislation provides states a temporary 6.2 percentage point increase in the federal matching rate and establishes conditions states must meet to access the enhanced funding. However, states may face capacity issues as demand for Medicaid grows. A number of states are taking actions to further streamline and simplify eligibility and processes and ease administrative burdens. However, many people who may be newly eligible for Medicaid may not know they can qualify and may not understand that they can apply anytime, without waiting for an open enrollment period.

In addition, new rules about what income to count toward eligibility for subsidized health care are complex and may be confusing for some consumers. In the CARES Act, Congress temporarily supplemented state unemployment insurance (UI) benefits, adding another $600 per week in federal benefits through the end of July, and specifying this supplement should be disregarded in determining eligibility for Medicaid and CHIP, but counted in determining eligibility for marketplace subsidies. To the extent consumers may not understand how to accurately report income under these rules, their ability to successfully apply for Medicaid, CHIP, or marketplace subsidies could be affected.

Recent federal cuts in outreach and enrollment assistance also could make it harder for people unfamiliar with either the marketplace or Medicaid to identify and understand these coverage options and successfully enroll.

In contrast, COBRA continuation coverage, by definition, does not require a transition to new coverage. People satisfied with their current coverage may be more likely to remain enrolled, if they can afford to. Overall, people with employer-sponsored health coverage view their health plan favorably, suggesting that, all other things equal, many might prefer to keep their current coverage. A late 2018 KFF/LA Times survey of adults with ESI found that overall, roughly seven in ten people with ESI give it a grade of either “A” or “B,” and about six in ten say they think their employer is offering them the best possible deal for coverage. However, satisfaction with job-based plans was lower for people in plans with higher deductibles.

Discussion

The availability of COBRA subsidies could help prevent health coverage loss for up to tens of millions of displaced workers. As proposed, COBRA subsidies would give workers the option to remain affordably in their current job-based plan. Subsidies could also reduce adverse selection against employer plans experienced today by unsubsidized COBRA enrollees.

Under current law, most displaced workers will also be eligible for other, subsidized, coverage options – marketplace plans and Medicaid/CHIP. Some might choose these current new coverage sources instead of subsidized COBRA. Premiums paid by individuals for fully subsidized COBRA would be comparable to Medicaid – that is, zero premiums. Marketplace plan premiums would generally be higher than subsidized COBRA, and much higher for individuals whose incomes make them ineligible for marketplace premium tax credits. On average, cost sharing under COBRA would be higher than under Medicaid, particularly if displaced workers had not yet satisfied their annual deductible. Cost sharing under marketplace plans could be much lower for individuals eligible for CSR; but could be much higher for people with income more than twice the poverty level. Finally, individuals losing their jobs and job-based coverage might not be aware of other Medicaid and marketplace coverage options, or successfully navigate the application and transition to other coverage. For them, COBRA continuation coverage could be more familiar and less administratively complex.

Beyond tradeoffs for individuals, COBRA subsidies raise other questions of cost-efficiency. Historical national data shows that employer plans generally are not as successful as public plans at controlling the rate of growth in health expenditures. On average, private health plans pay prices for hospital and medical services that are nearly twice that paid by Medicare. In addition, COBRA premium subsidies could generate a windfall for insurers and health plans whose 2020 premiums were established prior to the pandemic, At least in the short term, as patients delay elective procedures, major insurers have reported rising profits, some of which may need to be returned in rebates next year.

At $106 billion over two years, the federal cost of a 100% COBRA subsidy would be substantial, both because of the per person cost and because it is likely that most, even nearly all, of those eligible would take advantage of this option to maintain free health coverage.

Methods

This brief analyzes data from the 2017 Medical Expenditure Panel Survey (MEPS), a cross-sectional survey consisting of two-year longitudinal panels. The 2017 MEPS data set reflects data collected during both panel 21 (rounds 3, 4, and 5) and panel 22 (rounds 1, 2, and 3). The survey uses computer-assisted personal interview (CAPI) software to interview 19,351 households gathering information on 31,880 people. For this analysis, we looked a subset of people ages 18 to 64. Statistics are weighted using the MEPS person weight. Individual enrollment in COBRA was determined using the MEPS Person Round Plan file. We calculated a point-in-time cobra enrollment at panel 21 round 3 and panel 22 round 1. The MEPS Person Round Plan file was merged on to the MEPS Full Year consolidated file, which contained enrollment data by source of coverage. Each source of insurance was subset to the months January, February, March, and April to coincide with the point when the COBRA question was collected. The different sources of insurance are not mutually exclusive, so a hierarchy was created as follows: COBRA, Medicaid, Medicare, ESI, Non Group, Uninsured. The Unemployment rate was calculated by using the following categories: people who could not find work, people who were unable to work because of a disability, people unemployed because of temporarily layoff, and people who were waiting to start a new job.

Data on premiums and deductibles for 2020 QHP Marketplace plans come from Healthcare.gov and KFF review of state rate filings. Average QHP premiums were calculated as the average of premiums for the second-lowest cost silver plan (the benchmark plan) in each county in 2020 for a 48-year-old non-smoking individual, and are weighted by 2019 enrollment. Average QHP plan deductibles only include plans offered in federally-facilitated and partnership exchanges. Because many Marketplace plans are offered in multiple rating areas within a state, to calculate average deductibles we reduced the number of plans so that each benefit package was counted only once for each state. Average deductibles are simple averages of the plans that are available and are not weighted by enrollment.

Unsubsidized premiums and deductibles for those with employer coverage are calculated as the average premiums (including both the employer and worker contributions) and average single-coverage deductible. Premium costs do not include a two percent administrative fee that enrollees may face. KFF conducted the annual Employer Health Benefits Survey between January and July of 2019. It included 2,012 randomly-selected, non-federal public and private firms with three or more employees, for more information see here.

Most Americans expect the coronavirus to upend summer vacation plans with few saying it is likely they will be staying in a hotel (32%), going on an airplane (23%), or going to a concert or sporting event (19%) in the next 3 months. Yet, majorities including most Republicans and independents, expect to be getting back to some usual activities in the coming months such as going to the doctor, going to a barber or salon, attending larger gatherings, or eating in a restaurant. Most Democrats say it is unlikely they will be doing any of these activities except for going to a doctor or health care provider.

In the midst of the coronavirus outbreak, the economy and health care rank solidly as the top two issues in the 2020 presidential election, with all other issues trailing far behind for voters. Yet, the issue most important to voters is largely driven by party identification. Four in ten Republican voters say the economy is their top voting issue while one-third of Democratic voters (32%) choose health care as the most important issue in their voting decision. The coronavirus outbreak itself ranks as among the top issues among Democratic voters (29%), but ranks as the third issue among total voters (17 percent) and swing voters (19 percent).

President Trump receives negative ratings on his job performance and handling of coronavirus and health care, but the public does not seem to be punishing him for the decline in the nation’s economy as a result of the coronavirus outbreak. A majority of the public (57%) and the crucial block of undecided voters known as “swing voters” (59%) continue to approve of President Trump’s handling of the nation’s economy. President Trump remains largely popular among Republicans with majorities approve of his handling of all national issues.

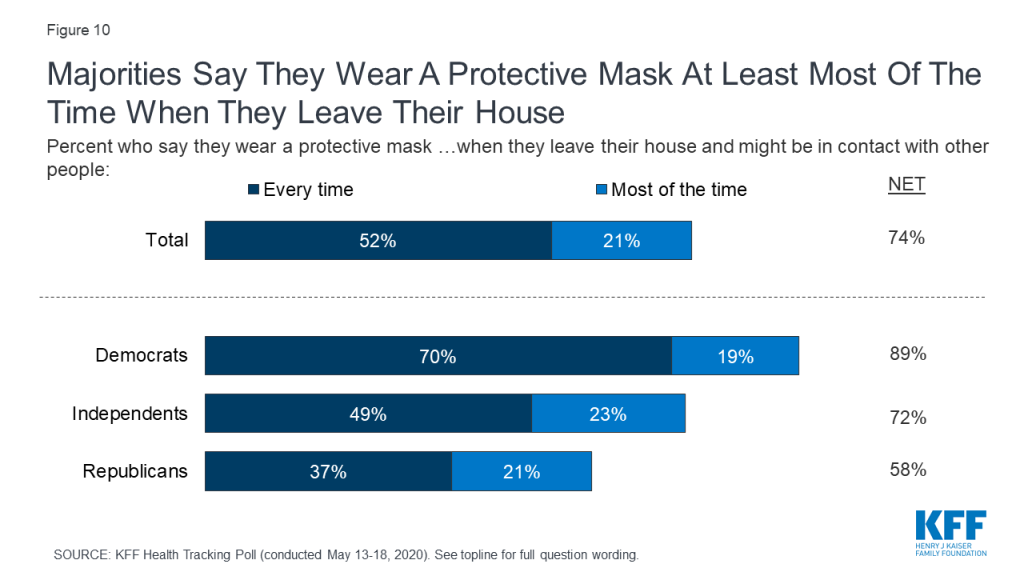

Democrats are almost twice as likely as Republicans (70% v. 37%) to say they wear a mask “every time” they leave their house and while most people (72%) think President Trump should wear a mask when meeting with other people, only about half of Republicans (48%) agree. The partisan difference in opinion and behavior regarding masks is largely driven by Republican men. About half of Republican men report wearing a protective mask at least most of the time when leaving their house to go someplace where they may come into contact with others (49%) and smaller shares say President Trump should wear a mask when meeting with other people (43%).

As Many States Are Re-Opening, Most U.S. Residents Don’t Expect To Get Back To Normal Soon

The coronavirus outbreak has had widespread effects across the U.S. bringing most Americans’ lives to a halt for the past couple months. But as states begin to re-open, Democrats and Republicans hold very different views of what the future holds. Most Republicans say the worst of the coronavirus is behind us or that the virus was never a threat, and they are likely to go back to usual activities in the coming months. Democrats, and to some extent independents, are more wary of the future and don’t think it is likely that their lives will be back to normal in the coming months.

Overall, half of U.S. adults still say that “the worst is yet to come” when it comes to the coronavirus outbreak in the U.S., which is considerably larger than the share (28%) who say “the worst is behind us.” The share who say “the worst is yet to come” remains relatively unchanged since last month’s KFF Health Tracking Poll, and the partisan divide remains. This month finds two-thirds of Republicans saying either “the worst is behind us” (45%) or that they don’t think the coronavirus is or was a major problem in the U.S. (20%).On the other hand, most Democrats (70%) and half of independents say “the worst is yet to come.”

Larger Shares of Republicans Report Going Back to Usual Activities

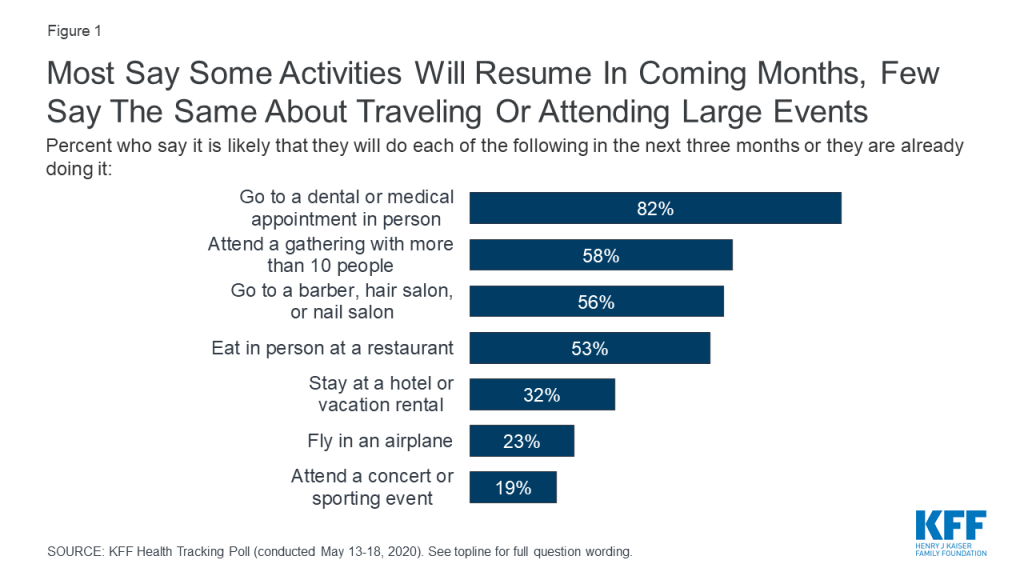

Most think that it is at least somewhat likely that they will resume some usual activities within the next three months, such as going to a dental or medical appointment in person (82%), attending gatherings with more than 10 people (58%), going to a barber or salon (56%), and eating in person at a restaurant (53%). Yet, while next week marks the official beginning to summer with observance of Memorial Day, few think it is “likely” they will be doing many typical summer activities such as staying at a hotel or vacation rental (32%), flying in an airplane (23%), or attending a concert or sporting event (19%) in the coming months.

Figure 1: Most Say Some Activities Will Resume In Coming Months, Few Say The Same About Traveling Or Attending Large Events

Majorities of Democrats (79%), independents (83%), and Republicans (91%) say it is likely they will go to a doctor, dentist, or other medical appointment in person in the next three months; but less than half of Democrats say the same about going to a barber or salon (43%), attending larger gatherings (43%), or eating in person at a restaurant (39%). Majorities of Republicans and independents say they are either already doing these activities or it is likely they will do them in the next three months.

Few – across party identification- say it is likely they will stay at a hotel or vacation rental, fly in an airplane, or attend a concert or sporting event in the coming months.

Table 1: Partisans Disagree On How Likely It Is They Will Be Back To Usual Activities

Percent who say it is likely they will do the following in the next three months or are already doing the following:

Party Identification

Democrats

Independents

Republicans

Go to a doctor, dentist, or other medical appointment in person

79%

83%

91%

Go to a barber, hair salon, or nail salon

43

55

74

Attend a gathering of family or friends with more than 10 people

43

58

73

Eat in person at a restaurant

39

52

75

Stay at a hotel or vacation rental

24

31

43

Fly in an airplane

21

25

25

Attend a concert or sporting event

8

20

31

Is Your State Opening Too Soon? Depends On Where You Live

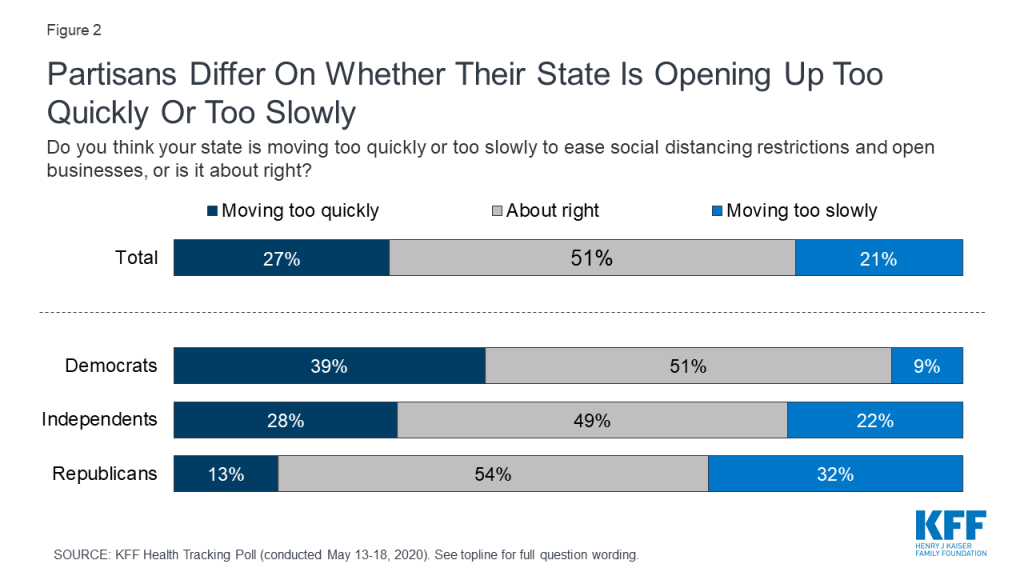

About half of adults – across party identification – say they think their state is moving at about the right speed in easing social distancing restrictions and opening businesses while one in four (27%) say their state is moving “too quickly” and one in five (21%) say their state is opening “too slowly.”

Figure 2: Partisans Differ On Whether Their State Is Opening Up Too Quickly Or Too Slowly

More than three times as many Republicans (32%) as Democrats (9%) say their state is opening “too slowly,” and one-fifth (22%) of independent say the same. Four in ten Democrats (39%) say their state is opening “too quickly” compared to 28% of independents and 13% of Republicans. About half, across party lines, say their state is doing things “about right.”

With all U.S. states taking some steps to re-open their economies, some states – most notably those with Republican governors like Texas and Arizona – have pushed to re-open their states sooner than many public health officials have advised. About four in ten (37%) of those living in states with a Republican governor say their state is moving “too quickly” compared to one in five of those living in states with a Democratic governor.

There are strong party divides with partisans more likely to support their state’s actions if their governor shares their party identification. Nearly two-thirds (64%) of Republicans living in a state with a Republican governor saying their state is doing things “about right,” while most Democrats (62%) and a slight majority of independents (51%) living in states with a Democratic governor saying their state is doing things at about the right speed.

Table 2: Partisans Living In Republican-Led States Have Different Views On Whether Their State Is Re-Opening Too Quickly Or Too Slowly

Do you think your state is moving too quickly or too slowly to ease social distancing restrictions and open businesses, or is it about right?

Living in a state with a Republican Governor

Total

Democrats

Independents

Republicans

Too quickly

37%

56%

40%

16%

Too slowly

15

9

15

20

About right

47

34

44

64

Do you think your state is moving too quickly or too slowly to ease social distancing restrictions and open businesses, or is it about right?

Living in a state with a Democratic Governor

Total

Democrats

Independents

Republicans

Too quickly

20%

27%

19%

11%

Too slowly

26

9

28

45

About right

52

62

51

43

Amidst Outbreak, Republican Voters Say Economy Is Top 2020 Issue While Health Care And Coronavirus Weighs Heavily On Democratic Voters

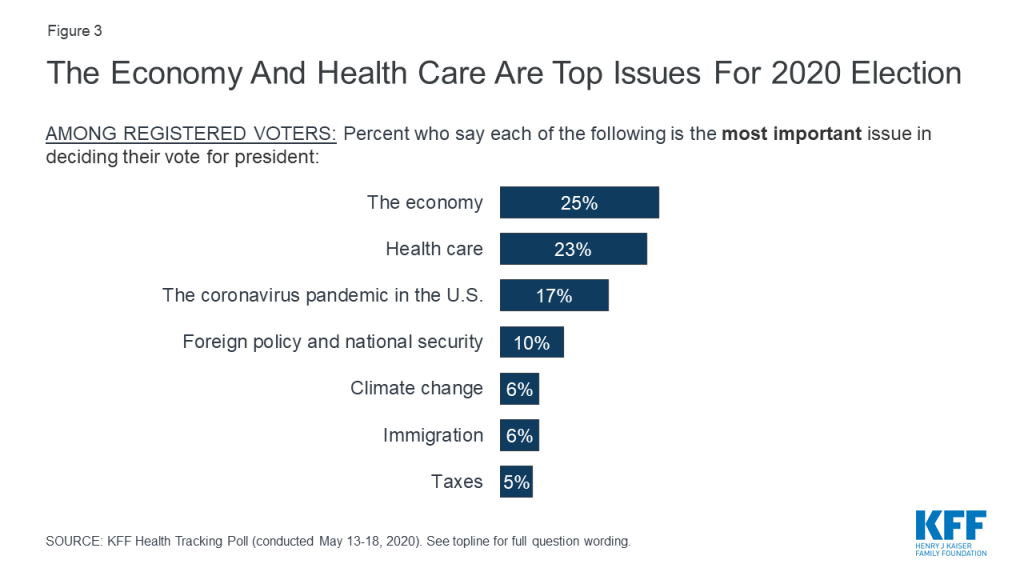

With less than six months before the 2020 presidential election, partisan voters are prioritizing different issues with the economy and health care rising to the top. Overall, both the economy (25%) and health care (23%) are the top issues for voters when deciding their vote for president in November. These two issues outrank all other issues including the coronavirus outbreak (17%), foreign policy and national security (10%), climate change (6%), immigration (6%), and taxes (5%).

Figure 3: The Economy And Health Care Are Top Issues For 2020 Election

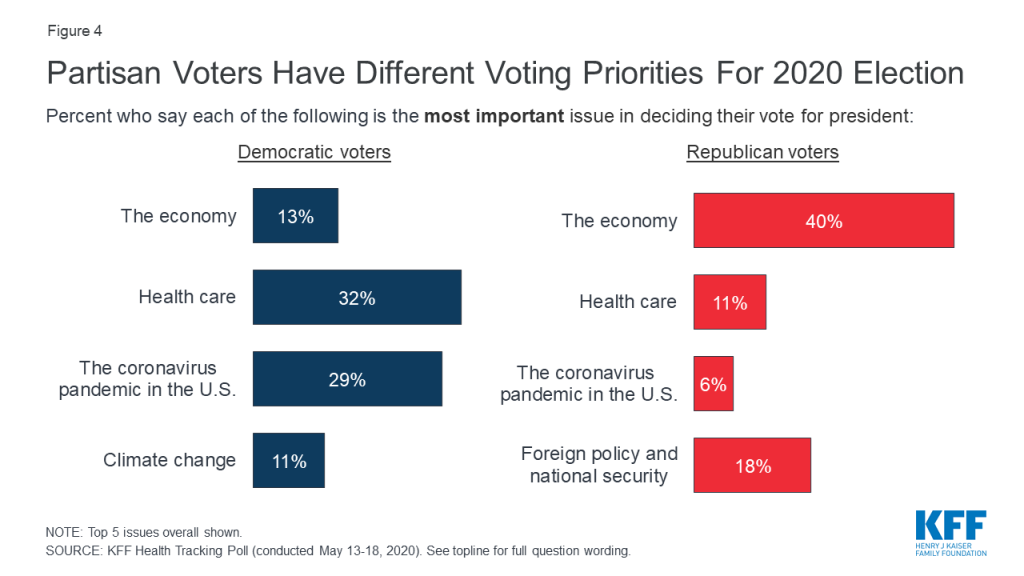

Throughout the 2020 Democratic presidential primary, Democratic voters said health care was their most important issue. In fact, in all of the 17 states in which KFF has analyzed AP VoteCast survey data of primary voters and caucus-goers, health care was either the top issue (15 states), or among the top issues (2 states). Health care remains a top issue for Democratic voters with one-third (32%) choosing health care as the most important issue to their vote decision, followed closely by the coronavirus pandemic in the U.S. (29%). Fewer Democratic voters (13%) say the economy is the most important issue. Republican voters, on the other hand, are prioritizing the economy over all other issues with four in ten saying it is “the most important issue” followed by foreign policy and national security (18%). Fewer Republican voters say either health care (11%) or coronavirus (6%) is the most important issue to their vote. Independents are split with similar shares prioritizing health care (25%) and the economy (25%).

Figure 4: Partisan Voters Have Different Voting Priorities For 2020 Election

Swing Voters Say Issues, Not Trump, Will Drive Their 2020 Decision

With former Vice President Joe Biden now the presumptive nominee for the Democratic candidate for president, the latest KFF Health Tracking Poll examines the views of voters who have not yet made up their minds about who to vote for.

Defining Swing Voters

A similar share of voters say they are either “definitely going to vote for President Trump” (30%) as say they are “definitely going to vote for Joe Biden” (28%), while nearly four in ten voters either say they are undecided in their 2020 vote choice (11%) or are probably going to vote for President Trump (11%) or Democratic nominee Joe Biden (15%) but have not made up their minds yet.

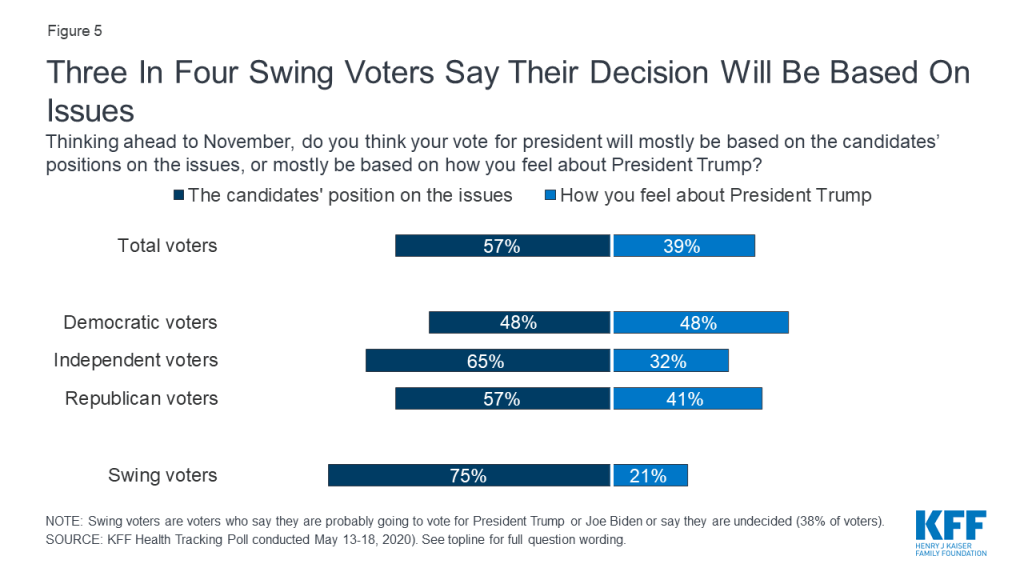

Swing voters are more likely than voters, overall, as well as voters across party identification to say their vote for president will “mostly be based on the candidates’ position on the issues” (75%) rather than based on “how they feel about President Trump” (21%).

Figure 5: Three In Four Swing Voters Say Their Decision Will Be Based On Issues

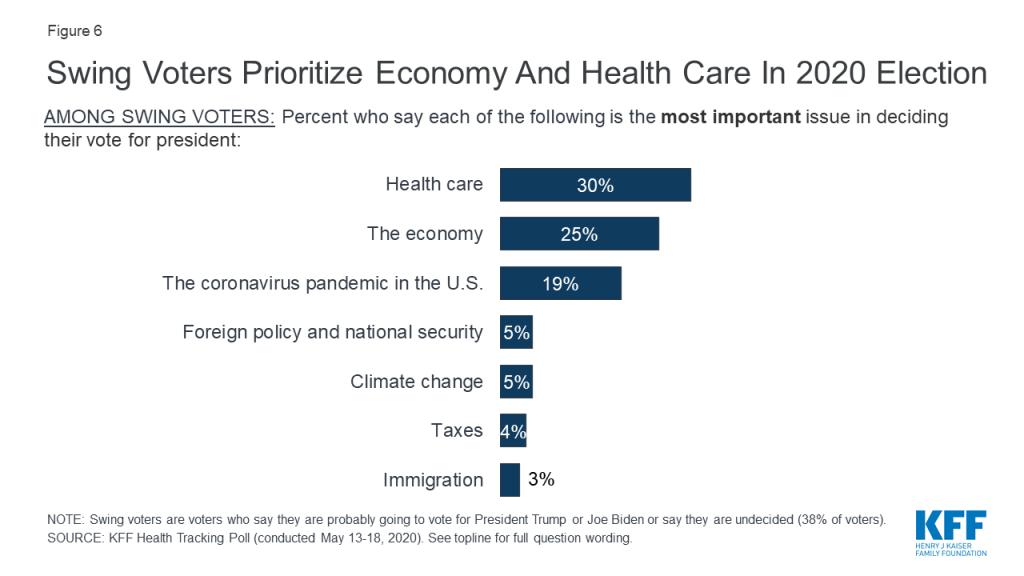

Swing voters’ priorities in their 2020 vote choice are similar to the rankings among all voters, with three in ten swing voters saying health care is their top issue and one-fourth choosing the economy as their top issue. About one in five (19%) say the coronavirus pandemic in the U.S. is the most important issue in deciding their vote.

Figure 6: Swing Voters Prioritize Economy And Health Care In 2020 Election

Is Trump’s Handling of Coronavirus Impacting Voters’ 2020 Decision?

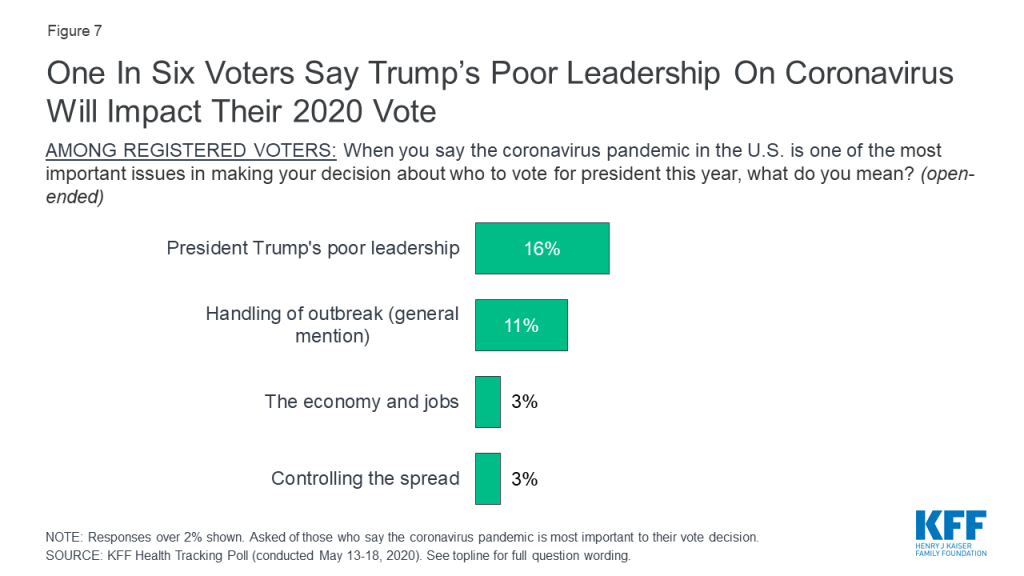

Nearly one in five voters overall (17%) and three in ten Democratic voters (28%) say the coronavirus pandemic in the U.S. is going to be “the most important issue” when deciding their vote for president. When voters who said coronavirus was going to be very important to their vote are asked to say in their own words what about the outbreak is going to impact their vote, larger shares offer negative responses about President Trump’s handling of the virus than any other response. About one-third of voters who say coronavirus is important to their vote (16% of all voters) offer responses related to President Trump’s poor leadership, four times as many who offer any other response including the impact on the economy and jobs (3% of all voters). An additional one in ten (11%) mention general responses related to the handling of the outbreak.

Figure 7: One In Six Voters Say Trump’s Poor Leadership On Coronavirus Will Impact Their 2020 Vote

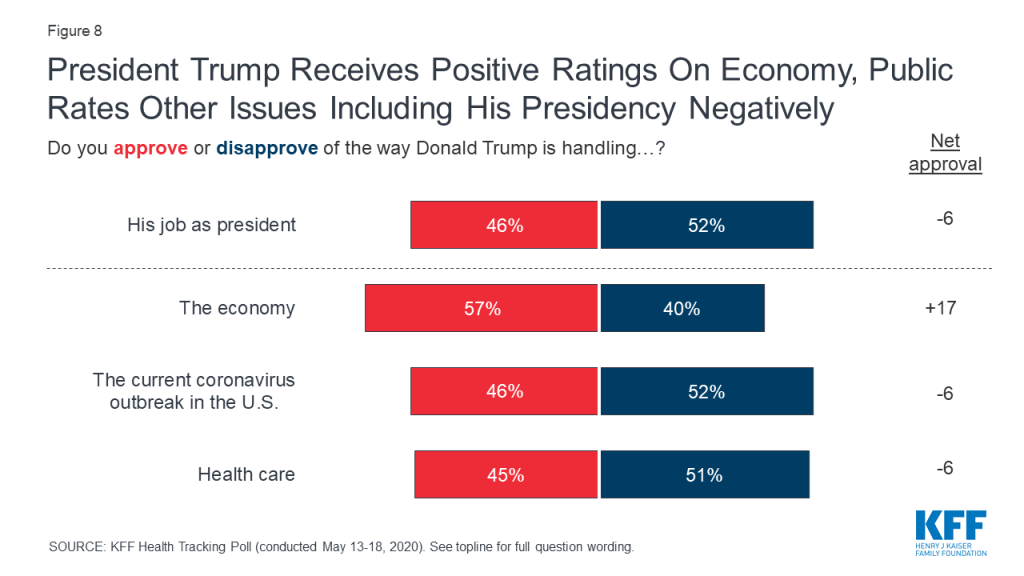

This is consistent with how the public rate the job President Trump is doing with the current coronavirus outbreak in the U.S. President Trump now receives negative ratings for his handling of the coronavirus outbreak with a slightly smaller share approving (46%) than disapproving (52%) of his handling of this issue (-6 percentage points net approval). This marks a decline in the public’s evaluation of his handling of the coronavirus outbreak from six weeks ago when 50% of the public approved of his response and he had a net positive rating (+3 percentage points net approval).

Figure 8: President Trump Receives Positive Ratings On Economy, Public Rates Other Issues Including His Presidency Negatively

Partisans continue to be strongly divided in their assessment of President Trump’s job performance, with at least eight in ten Republicans approving of the way he is handling the economy (91%), his job as president (89%), the current coronavirus outbreak in the U.S. (87%), and health care (84%). Democrats, on the other hand, largely disapprove of his job as president (87%), as well as the way he is handling health care (86%), the current coronavirus outbreak (84%), and the economy (71%). Independents are divided in their assessments of his job performance overall but give him negative assessments on his job approval overall (-10 percentage point net approval), as well as his handling of health care (-10 percentage point net approval) and the current coronavirus outbreak (-6 percentage point net approval), but positive ratings on his handling of the economy (+20 percentage point net approval).

Table 3: President Trump Job Approval By Party Identification

Do you approve or disapprove of the way Donald Trump is handling…?

Party ID

Democrats

Independents

Republicans

His job as president

Approve

12%

44%

89%

Disapprove

87

54

10

The economy

Approve

25

59

91

Disapprove

71

39

9

Health care

Approve

12

41

84

Disapprove

86

51

12

The current coronavirus outbreak in the U.S.

Approve

15

46

87

Disapprove

84

52

12

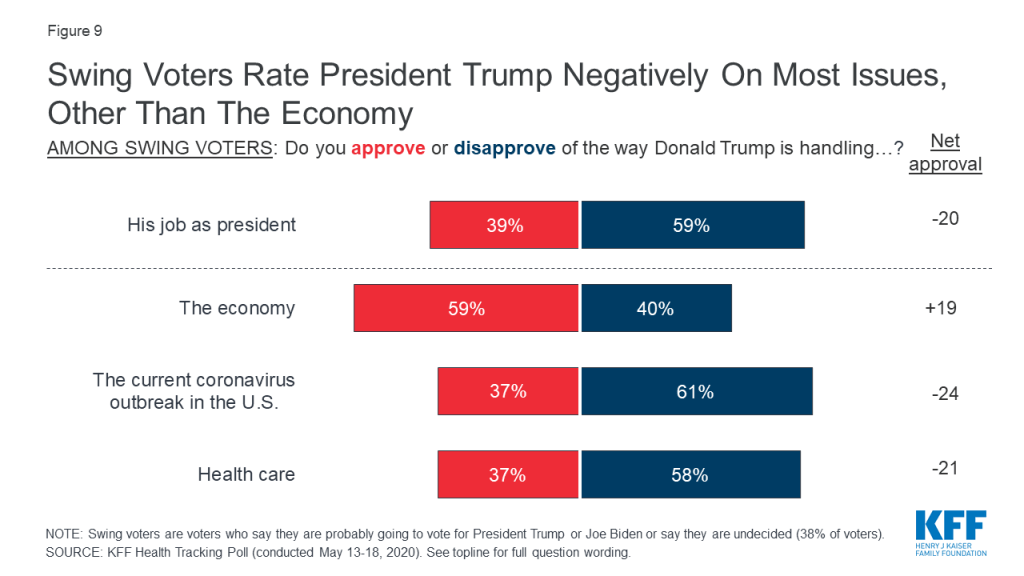

Swing voters are also negative in their assessments of President Trump’s presidency and his handling of most national issues. Swing voters (who comprise 38% of all voters) largely disapprove (59%) of the way President Trump is handling his presidency and are also negative in Trump’s handling of both the coronavirus outbreak (-24 percentage point net approval) and health care (-21 percentage point net approval). Swing voters, like the overall public, remain positive in their assessments of his handling of the economy (+19 percentage point net approval).

Figure 9: Swing Voters Rate President Trump Negatively On Most Issues, Other Than The Economy

Is The Use Of Masks Partisan?

Three-fourths (74%) of adults say they wear a protective mask either “every time” or “most of the time” when they leave their house and might be in contact with people, which is consistent with the Centers for Disease Control and Prevention (CDC) recommendations that people wear a mask anytime they may be unable to maintain safe social distancing. But there are strong partisan differences with Democrats almost twice as likely as Republicans (70% v. 37%) to say they wear a mask “every time” they leave their house. Majorities across partisans say they wear a mask at least most of the time.

Figure 10: Majorities Say They Wear A Protective Mask At Least Most Of The Time When They Leave Their House

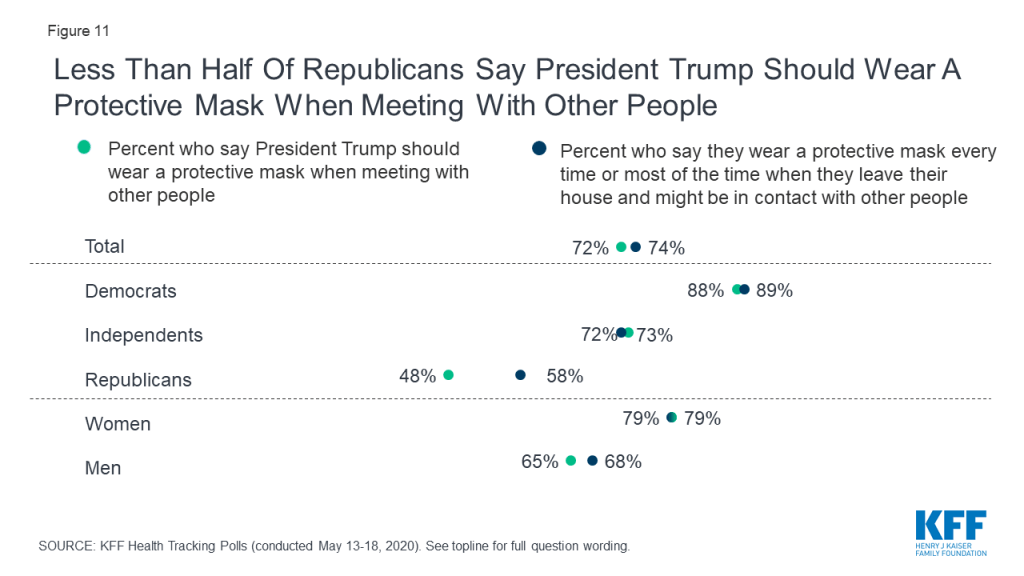

There have been recent news reports about people protesting the requirement of wearing masks in order to limit contact and reduce the spread of coronavirus including some recent criticism of President Trump for not wearing a mask when making public appearances. Most people (72%) think President Trump should wear a mask when meeting with other people, but only about half of Republicans (48%) agree.

Figure 11: Less Than Half Of Republicans Say President Trump Should Wear A Protective Mask When Meeting With Other People

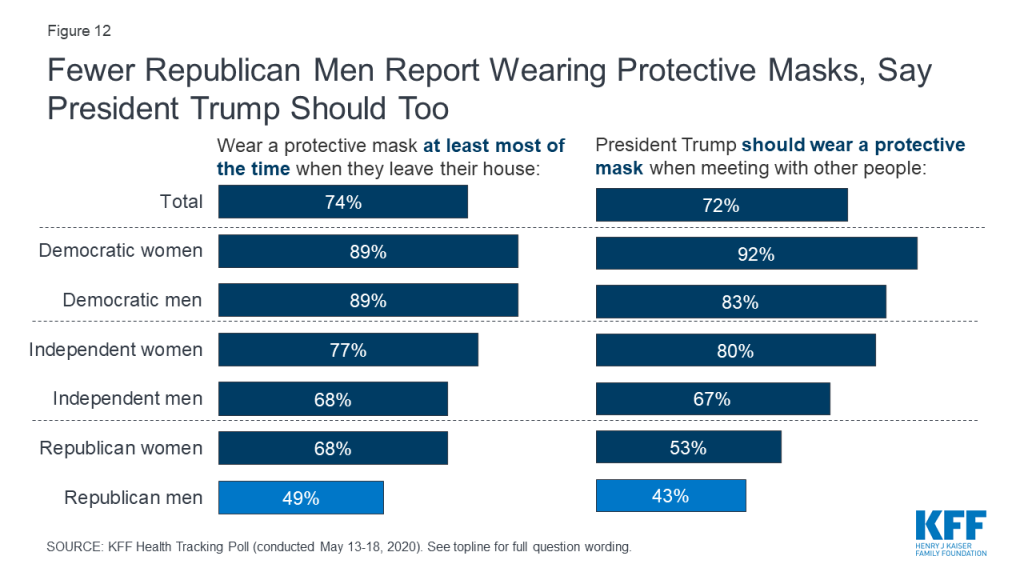

The partisan difference in opinion and behavior regarding masks is largely driven by Republican men. Republican men are both less likely to report wearing a protective mask when leaving their house to go someplace where they may come into contact with others and smaller shares say President Trump should wear a mask when meeting with other people. About half (49%) of Republican men say they wear a mask at least most of the time, compared to 68% of Republican women and more than two-thirds of independent men (68%) and a large majority of Democratic men (89%). Slightly more than four in ten Republican men (43%) say President Trump should wear a mask compared to 53% of Republican women, and large majorities of both independent men (67%) and Democratic men (83%).

Figure 12: Fewer Republican Men Report Wearing Protective Masks, Say President Trump Should Too

Health And Economic Impacts

Impact of Coronavirus on Personal Health,Economic and Food Security, and Medicaid

Key Findings:

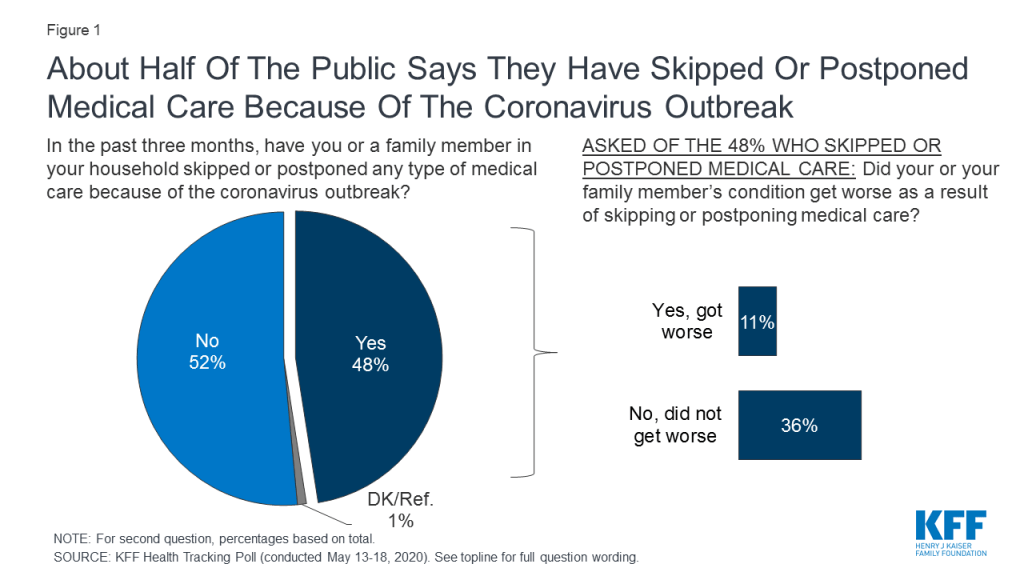

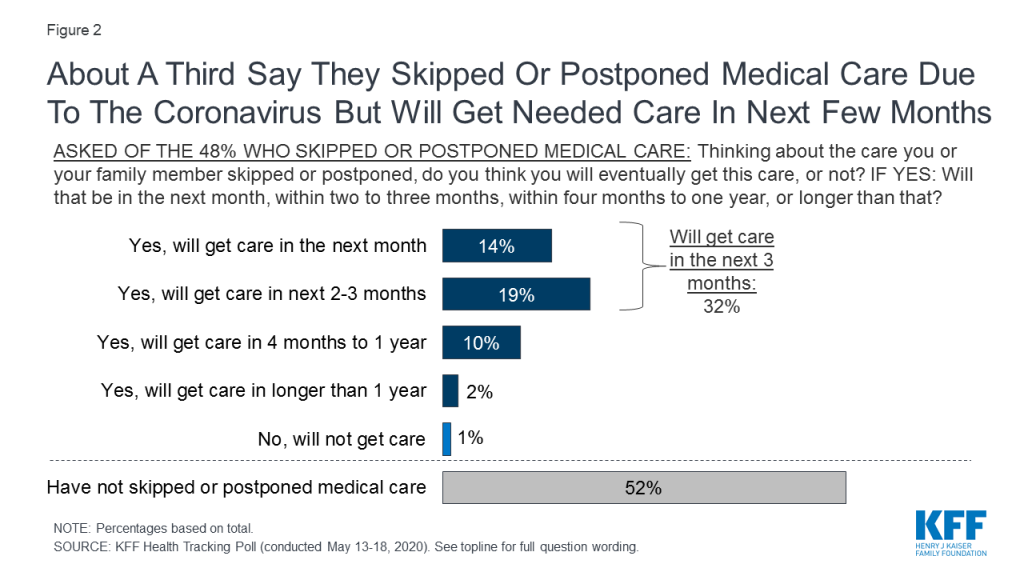

Amidst the coronavirus pandemic, Americans are deferring medical care. Nearly half of adults (48%) say they or someone in their household have postponed or skipped medical care due to the coronavirus outbreak. However, as stay-at-home restrictions ease, most (68% of those who delayed care, or 32% of all adults) expect to get the delayed care in the next three months.

About four in ten U.S. adults (39%) say worry or stress related to coronavirus has had a negative impact on their mental health, including 12% who say it has had a “major” impact. This is down slightly from early April when 45% reported a negative mental health impact. Yet, women continue to be more likely than men to say it is has negatively impacted their mental health (46% vs 33%) and urban (46%) and suburban (38%) residents are more likely than those in rural areas (28%) to say coronavirus has had a negative impact on their mental health. Among adults in households that experienced income or job loss due to the coronavirus outbreak (who make up one-third of adults overall), 46% say the pandemic has had a negative impact on their mental health.

Three in ten adults (31%) say they have fallen behind in paying bills or had problems affording household expenses like food or health insurance coverage since February due to the coronavirus outbreak. Additionally, one in four Americans (26%) say they or someone in their household have skipped meals or relied on charity or government food programs since February, including 16% who say this was due to the impact of coronavirus on their finances. The share who say they have skipped meals or relied on charity or government food programs due to coronavirus is higher among those in households that have lost a job or income due to coronavirus (30%) and among Black adults (30%) and Latinos (26%).

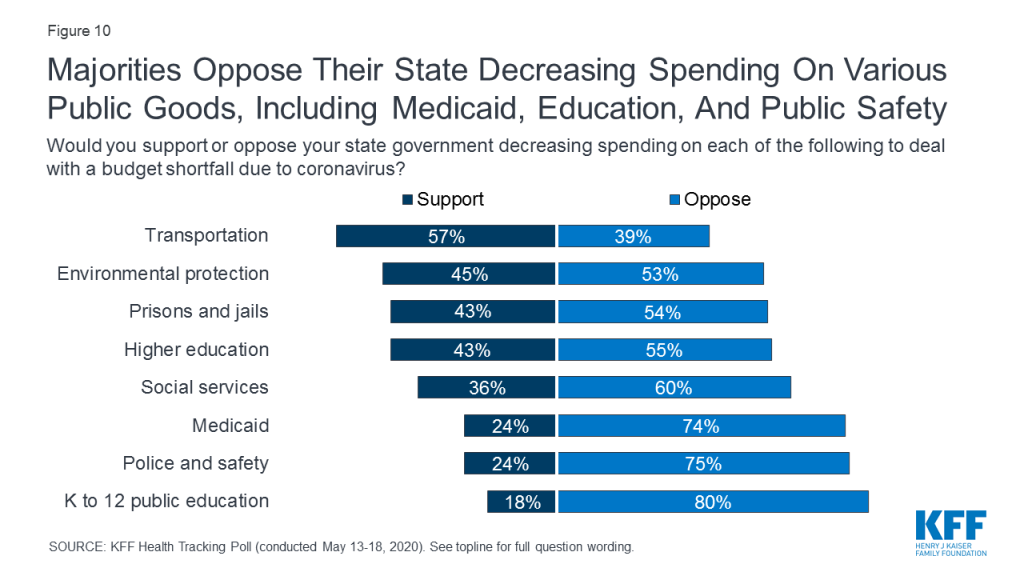

As states consider spending cuts to address budget shortfalls caused or exacerbated by the coronavirus pandemic, it appears that many potential cuts will be unpopular among the public. At least three-quarters of adults oppose decreasing spending on K-12 public education (80%), police and safety (75%), and Medicaid (74%). Moreover, majorities oppose cutting spending on social services (60%), higher education (55%), prisons and jails (54%), and environmental protection (53%). Transportation is the only area which garners majority support for state budget cuts. Majorities of Democrats (85%), independents (73%), and Republicans (62%) oppose their state government decreasing spending on Medicaid.

At a time when many newly unemployed Americans may turn to Medicaid for health insurance coverage, a majority of adults (55%) say the Medicaid program is personally important to them and their families and about one in four adults (23%) who are not currently on Medicaid say it is likely they or a family member will turn to Medicaid for health insurance in the next year. This share rises to 31% among those who lost income or whose spouse lost income due to the coronavirus outbreak. Two-thirds of adults in states that have not expanded Medicaid say their state should expand the program, including seven in ten adults (72%) in those states whose household experienced a job or income loss due to coronavirus.

Nearly Half Of Adults Say They Or A Family Member Have Deferred Medical Care Due To The Coronavirus Outbreak

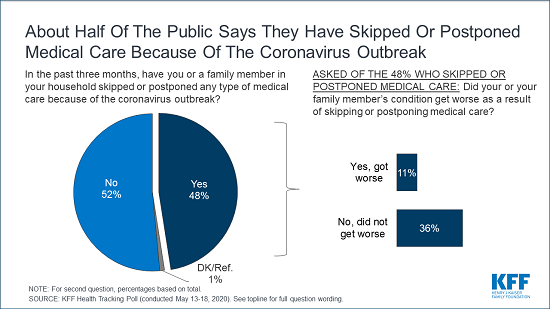

The recent stay-at-home orders instituted by most states to help curb the spread of coronavirus impacted most industries, including the health care sector. Many hospitals and medical care providers closed for non-emergency services and many patients with non-emergency conditions postponed or cancelled appointments.1 2 The latest KFF Health Tracking Poll finds that nearly half of adults (48%) say they or someone in their household have postponed or skipped medical care due to the coronavirus outbreak, including a higher share of women than men (54% vs. 42%). Notably, 11% of adults overall say their or their family member’s condition got worse as a result of postponing or skipping medical care due to coronavirus.

Figure 1: About Half Of The Public Says They Have Skipped Or Postponed Medical Care Because Of The Coronavirus Outbreak

Among those who say they or a family member have postponed or delayed medical care because of coronavirus, almost all say they will eventually get the care that has been postponed, including 68% (32% of adults overall) who expect to get the care within the next 3 months.

Figure 2: About A Third Say They Skipped Or Postponed Medical Care Due To The Coronavirus But Will Get Needed Care In Next Few Months

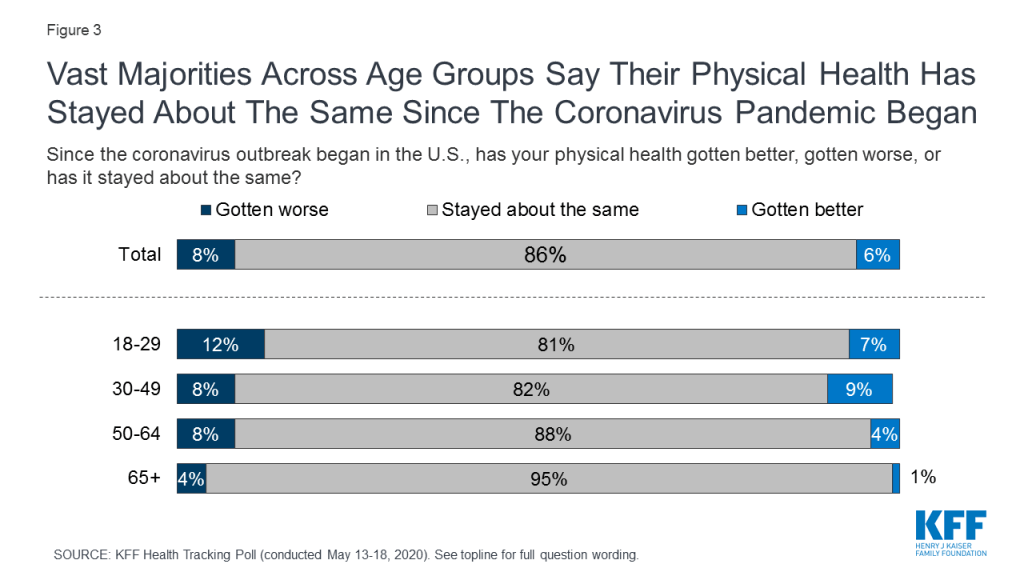

Despite nearly half of adults saying that they or a member of their household has deferred medical care due to coronavirus, most adults (86%) and at least eight in ten across age groups, say their physical health has “stayed about the same” since the outbreak began. Few adults say their physical health has gotten better (6%) and a similar share say their physical health has gotten worse (8%) since the coronavirus outbreak began in the U.S.

Figure 3: Vast Majorities Across Age Groups Say Their Physical Health Has Stayed About The Same Since The Coronavirus Pandemic Began

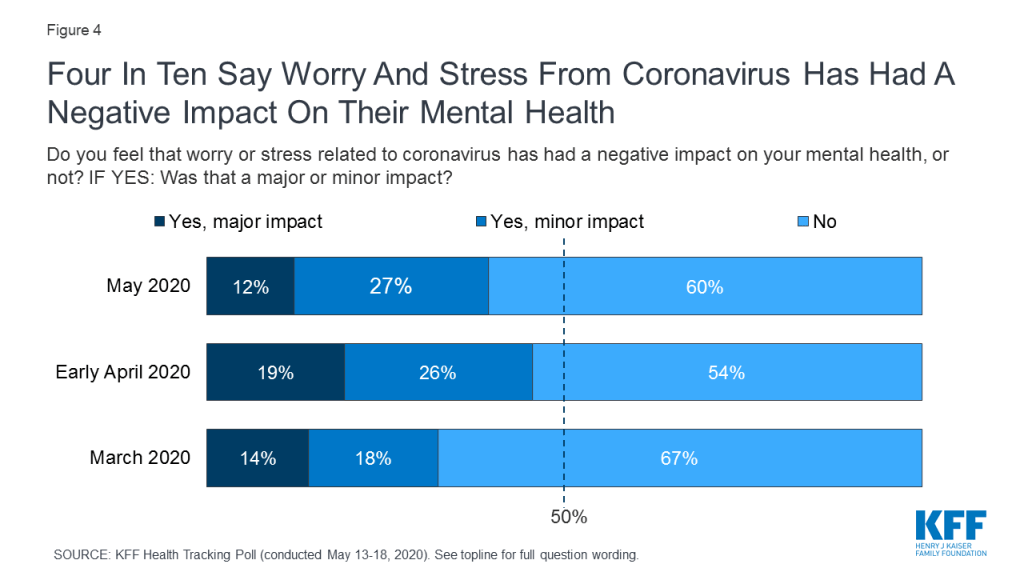

Though few Americans say their physical health has worsened, nearly four in ten (39%) say that worry or stress related to coronavirus has had a negative effect on their mental health. The share of adults who say coronavirus has had a “major” impact on their mental health (12%) has decreased slightly from early April (19%).

Figure 4: Four In Ten Say Worry And Stress From Coronavirus Has Had A Negative Impact On Their Mental Health

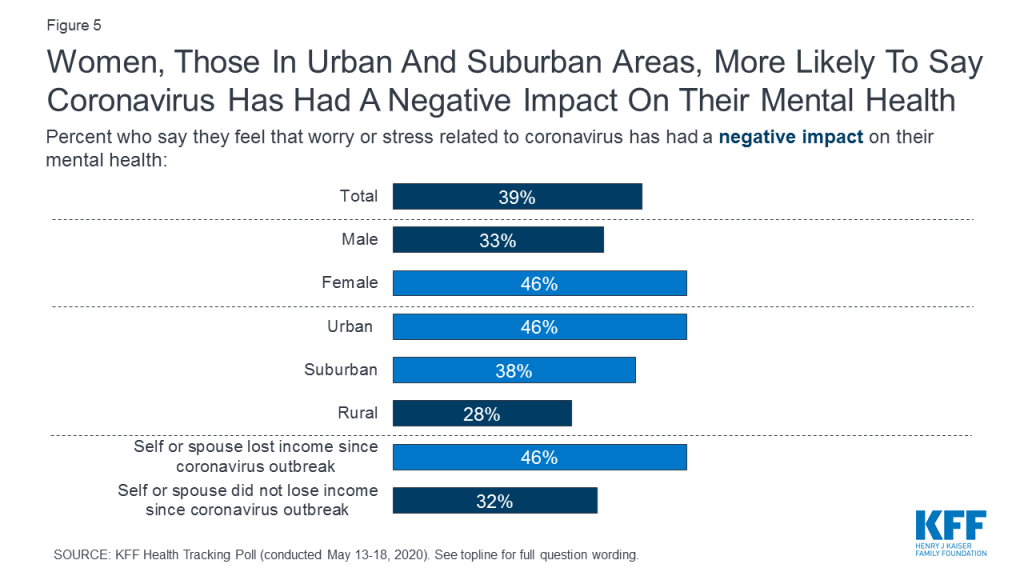

Consistent with findings in our earlier surveys, women continue to be more likely than men to say coronavirus has had a negative impact on their mental health (46% vs 33%). Similarly, those who live in urban (46%) and suburban (38%) areas are more likely than those who live in rural areas (28%) to say coronavirus has had a negative impact on their mental health. Among those living in households that experienced income or job loss since the coronavirus outbreak, 46% say the pandemic has had a negative impact on their mental health, including 13% who say it has had a “major impact.”

Figure 5: Women, Those In Urban And Suburban Areas, More Likely To Say Coronavirus Has Had A Negative Impact On Their Mental Health

One In Four U.S. Adults Say Their Families Have Skipped Meals Or Relied On Charity Or Government Food Programs Since The Coronavirus Outbreak Began

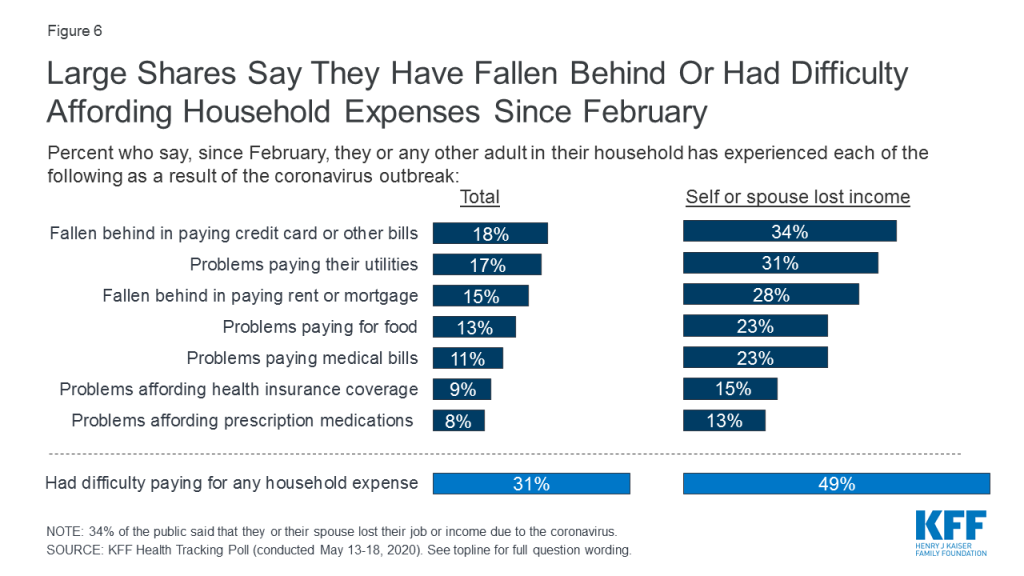

As the economic downturn continues, about three in ten adults (31%) have had difficulty paying household expenses, including about one in six who say they have fallen behind in paying credit card or other bills (18%), have had problems paying their utilities (17%), or fallen behind in paying their rent or mortgage (15%) since the coronavirus outbreak in the U.S. began. An additional 13% say they have had problems paying for food while about one in ten say they have had problems affording their health insurance coverage (9%) or their prescription medications (8%) or have had problems paying medical bills (11%). Among those living in households that experienced a job loss or had their income reduced due to the coronavirus outbreak, about half (49%) have had difficulty paying household expenses as a result. This includes about a third who say they have had problems paying credit cards bill (34%) or utilities (31%), 28% who say they have fallen behind on their rent or mortgage, and about one in four who say they have had trouble paying medical bills (23%) or affording food (23%).

Figure 6: Large Shares Say They Have Fallen Behind Or Had Difficulty Affording Household Expenses Since February

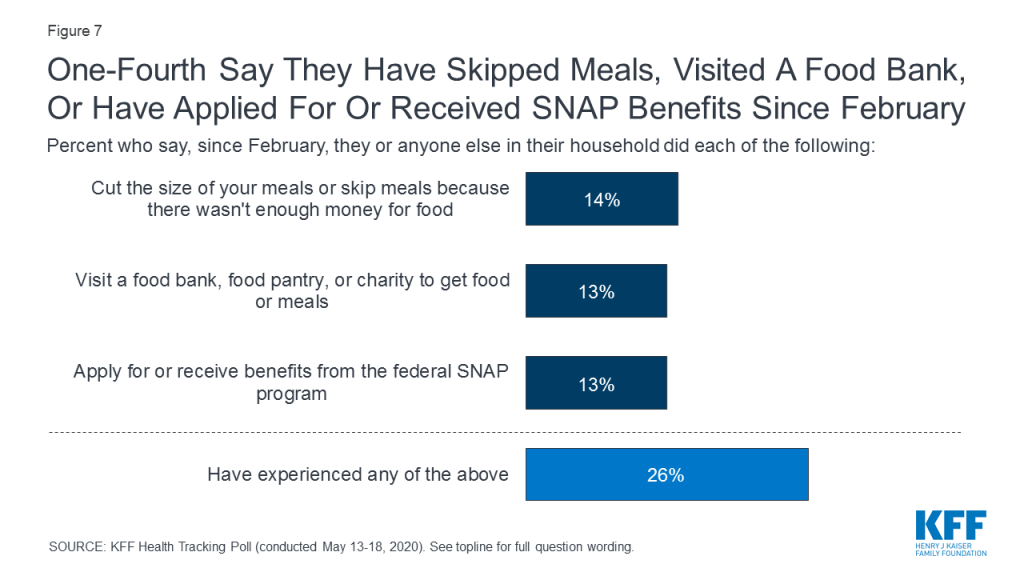

One in four Americans (26%) say they or a member of their household have skipped meals or relied on charity or government food programs since February, including 14% who say they have reduced the size of meals or skipped meals because there wasn’t enough money for food, 13% who have visited a food bank or pantry for meals, and 13% who have applied for or received SNAP benefits.

Figure 7: One-Fourth Say They Have Skipped Meals, Visited A Food Bank, Or Have Applied For Or Received SNAP Benefits Since February

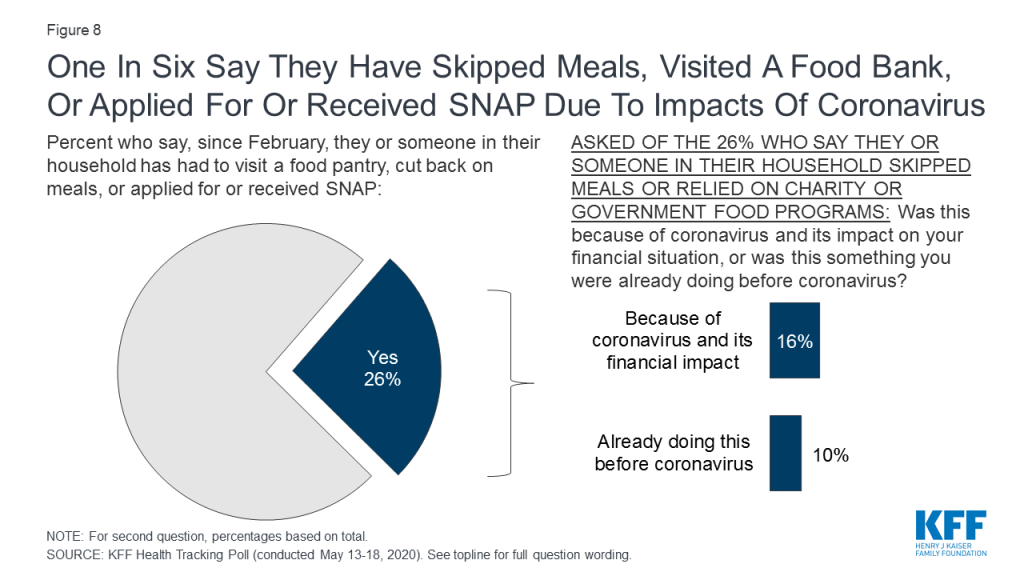

Overall, one in six Americans say that their experiences skipping meals or relying on charity or government food programs was because of coronavirus and its impact on their financial situation. A further 10% say they were already experiencing problems affording food before the coronavirus outbreak.

Figure 8: One In Six Say They Have Skipped Meals, Visited A Food Bank, Or Applied For Or Received SNAP Due To Impacts Of Coronavirus

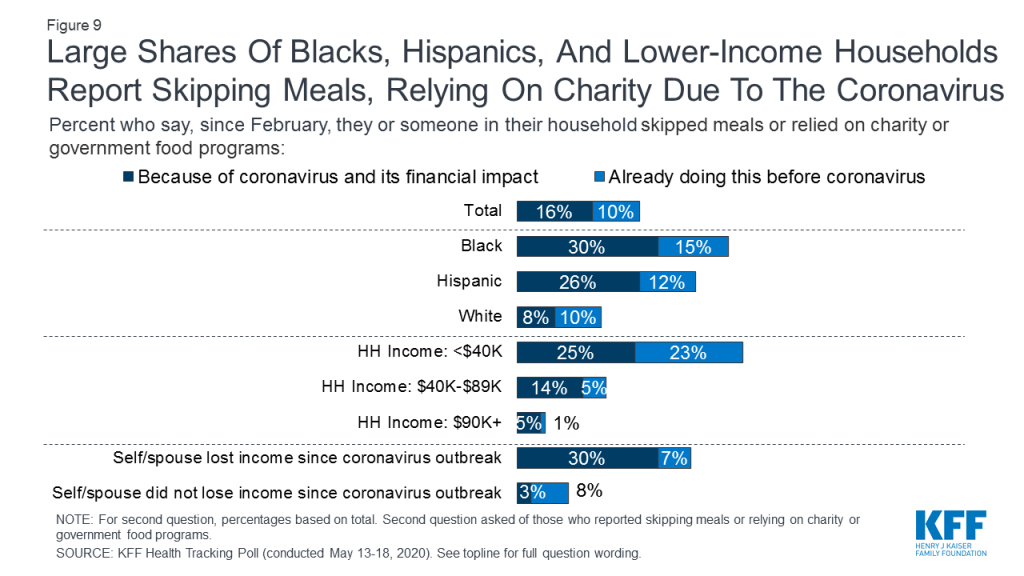

Some groups are more likely than others to report difficulty affording food as a result of coronavirus. About a third (34%) of all adults say they or their spouse lost a job or had their hours or income reduced as a result of the coronavirus outbreak. Among this group, about four in ten (38%) say they have skipped meals or relied on charity or government food programs since February, most of whom (30%) say coronavirus was the cause.

In addition, Black and Latino adults and those with lower incomes appear to be harder hit. About four in ten Black adults (45%) and Latinos (39%) say they have skipped meals or relied on charity or government food programs since February, including three in ten Black adults and about a quarter (26%) of Hispanics who say their experiences were directly related to the financial impact of coronavirus. Among those in households with an annual income under $40,000, nearly half (48%) say they have skipped meals or relied on charity or government food programs, including one-quarter who attribute this to coronavirus and a similar share (23%) who say they were already skipping meals or relying on food programs before the pandemic hit.

Figure 9: Large Shares Of Blacks, Hispanics, And Lower-Income Households Report Skipping Meals, Relying On Charity Due To The Coronavirus

Table 1: Skipping Meals Or Relying On Charity Or Government Food Programs By Demographic Groups

Percent who say they or someone in their household has done each of the following since February:

Total

Race/ethnicity

Household income

HH lost job/income due to coronavirus

Black

Hispanic

White

<$40K

$40 to <$90K

$90K+

Yes

No

Skipped or cut the size of meals because there wasn’t enough money for food

14%

27%

20%

8%

23%

12%

4%

24%

4%

Visited a food bank, food pantry, or charity for food

13

28

19

8

27

6

2

20

6

Applied for or received SNAP assistance

13

34

13

10

30

8

1

16

6

NET: Yes to any item above

26

45

39

18

48

19

7

38

11

Due to coronavirus and its impact on their financial situation

16

30

26

8

25

14

5

30

3

As States Face Budget Shortfalls, Public Opposes State Budget Cuts To Most Areas

Due to the recent economic downturn, many states may need to decrease spending in order to address projected budget shortfalls. Notably, eight in ten adults oppose their state government cutting spending on K-12 public education (80%) while about three in four oppose decreasing spending on police and safety (75%) and Medicaid (74%). Six in ten oppose their state government cutting spending on social services and slight majorities oppose cutting spending on higher education (55%), prisons and jail (54%), and environmental protection (54%). Notably, a majority of adults support their state decreasing spending on transportation (57%) in order to address budget shortfalls.

Figure 10: Majorities Oppose Their State Decreasing Spending On Various Public Goods, Including Medicaid, Education, And Public Safety

Across partisans, majorities of Democrats (85%), independents (73%), and Republicans (62%) oppose their state government decreasing spending on Medicaid. Similarly, majorities across partisans oppose decreasing spending on K-12 public education and on police and safety. Partisan splits are larger when it comes to state spending on higher education, social services, environmental protection.

Table 2: Majorities across partisans oppose their state government decreasing funding for K-12 education, police, and Medicaid

Percent who oppose their state government decreasing spending on each of the following:

Democrats

Independents

Republicans

K-12 public education

89%

79%

76%

Police and safety

71

72

91

Medicaid

85

73

62

Higher education

72

47

43

Social services

70

58

46

Prisons and jails

53

54

53

Environmental protection

73

47

37

Transportation

44

39

35

With the sudden rise in unemployment following the coronavirus outbreak, many Americans have not only lost their jobs, but have also lost the health insurance coverage provided by their former employers. A recent KFF analysis estimates that since the coronavirus outbreak began in the U.S., nearly half of adults who lost their health insurance coverage due to job loss are eligible for Medicaid, the government health insurance and long-term care program for low-income adults and children,.

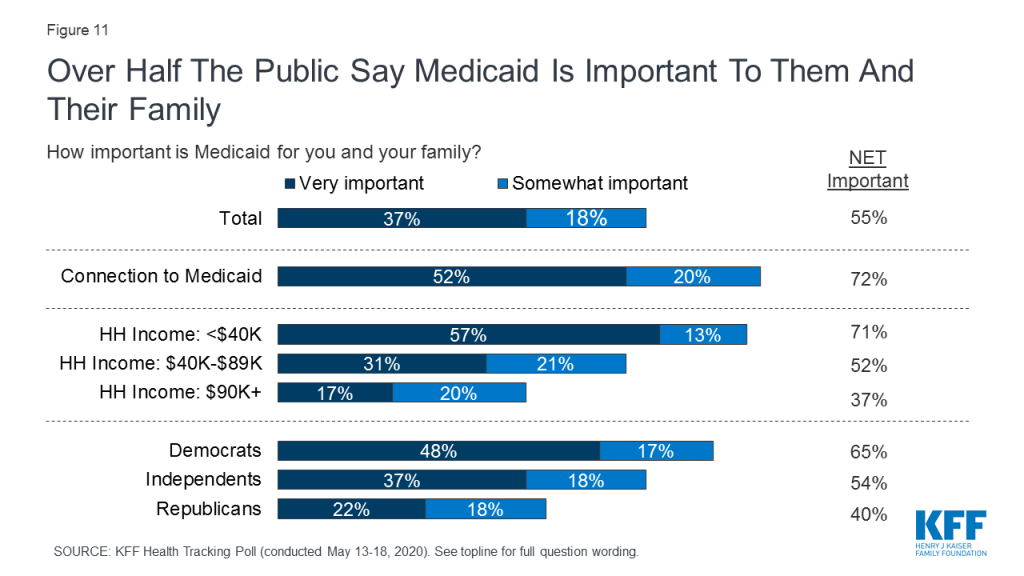

A majority of Americans (55%) say the Medicaid program is important to them and their family including 37% who say it is “very important”. Seven in ten adults with a household income under $40,000 (71%) say Medicaid is important to them and their family. Across partisans, Democrats (65%) and independents (54%) are more likely than Republicans (40%) to say Medicaid is important to them.

Figure 11: Over Half The Public Say Medicaid Is Important To Them And Their Family

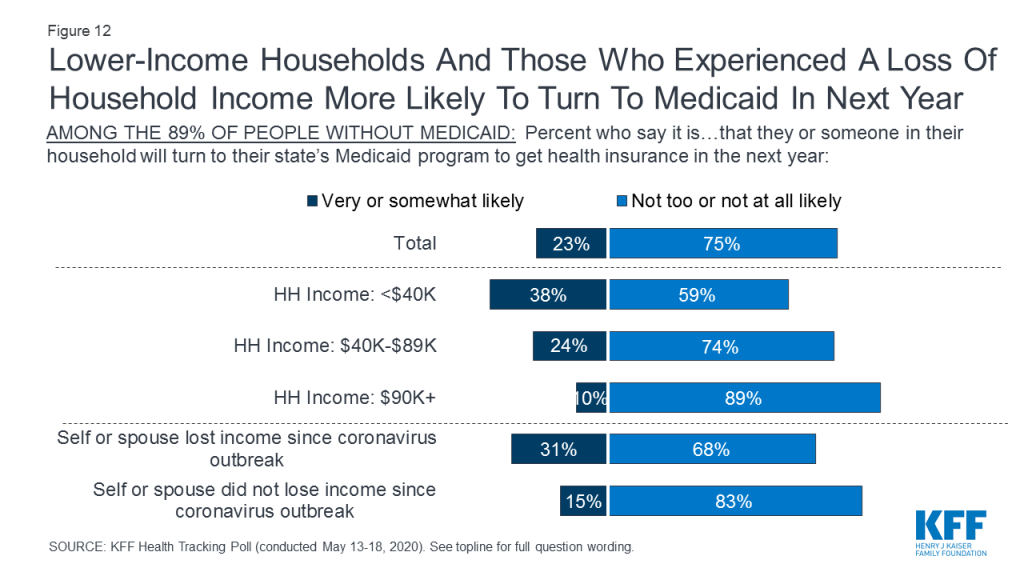

Amid rising unemployment, about one in four (23%) adults who are not currently covered by Medicaid say they or a family member are likely to rely on Medicaid for health care coverage in the next year. Notably, about four in ten (38%) adults with a household income under $40,000 who are not currently on Medicaid, say it is very or somewhat likely that they or someone in their household will turn to Medicaid in the next year. Among households who have lost income due to the coronavirus outbreak, 31% say it is very or somewhat likely that they will turn to Medicaid for health insurance coverage in the next year.

Figure 12: Lower-Income Households And Those Who Experienced A Loss Of Household Income More Likely To Turn To Medicaid In Next Year

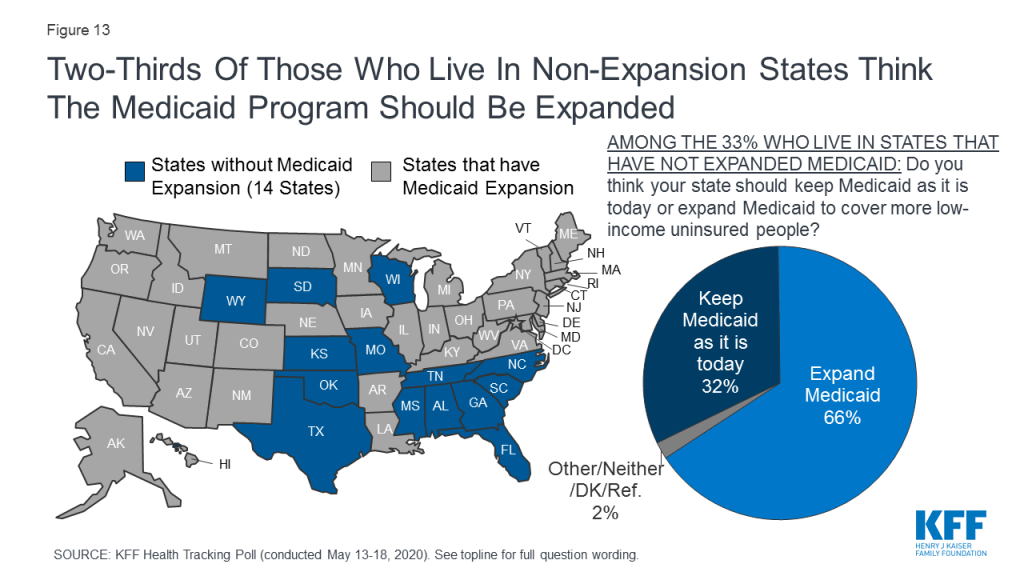

Under the 2010 Affordable Care Act (ACA), a number of states have expanded their Medicaid program. Among those who live in the 14 states that have not yet expanded their Medicaid program, two-thirds (66%) say they want their state to expand Medicaid to cover more low-income uninsured people, while about one-third (32%) want to keep Medicaid as it is today. However, within these states that have not yet expanded Medicaid, there is a large partisan gap on this issue with 89% of Democrats and 72% of independents preferring their state expand the program to cover more low-income uninsured people, while a majority of Republicans (58%) prefer to keep Medicaid in their state as it is now. In states that have not expanded their Medicaid programs, seven in ten adults whose household experienced a job or income loss due to coronavirus say their state should expand the program, while fewer adults who have not experienced a job or income loss say the same (72% vs. 52%).

Figure 13: Two-Thirds Of Those Who Live In Non-Expansion States Think The Medicaid Program Should Be Expanded

2010 Affordable Care Act

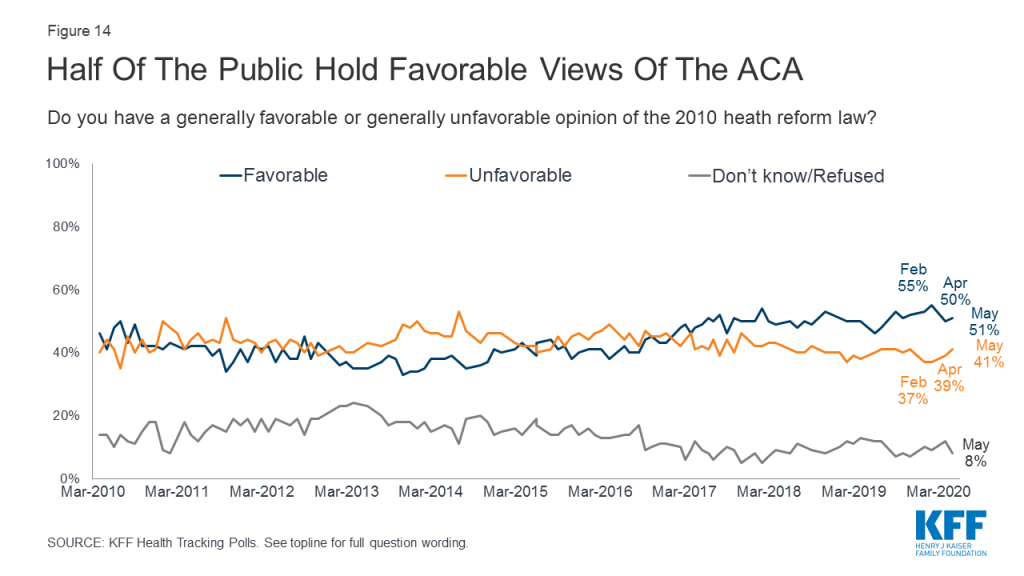

The most recent KFF Health Tracking Poll finds about half of the public (51%) have a favorable view of the ACA while 41% view it unfavorably, similar to the split in opinion since 2019. A majority of Republicans (76%) continue to hold unfavorable views towards the law, while eight in ten Democrats (80%) and a majority of independents (55%) hold favorable views of the ACA.

Figure 14: Half Of The Public Hold Favorable Views Of The ACA

Medicare-for-all and Public Option

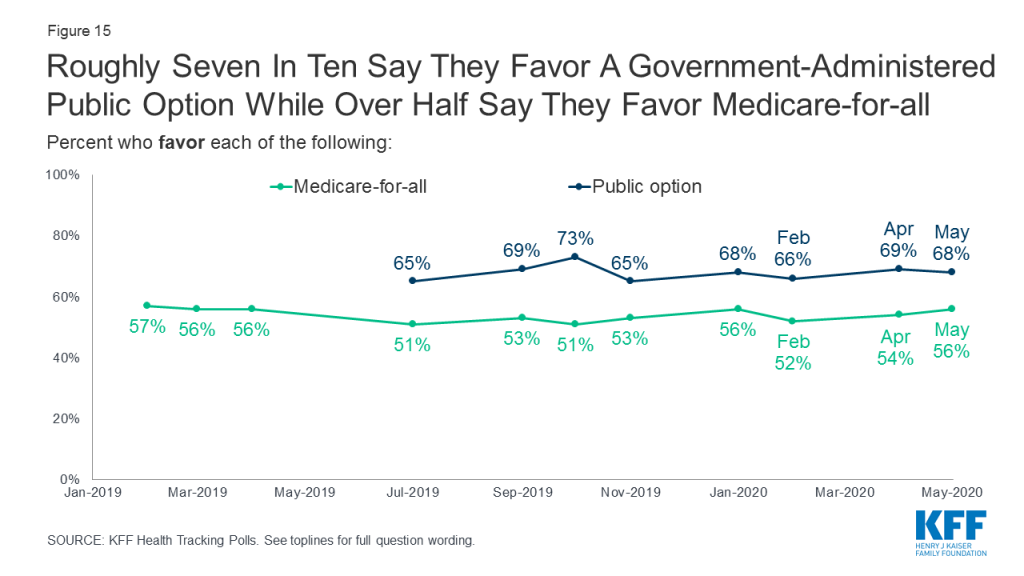

Though the 2020 Democratic presidential primary campaign has largely concluded, the policy discussions on the how to best expand public health insurance in this country have continued as the nation faces a deadly public health crisis. KFF continues to track public opinion on both a national health plan, sometimes called Medicare-for-all, as well as more incremental changes such as an optional government-administered health plan, sometimes called a public option. A majority (56%) of the public favors a Medicare-for-all plan in which all Americans would get their insurance from a single government plan (41% oppose), though a government administered public option continues to garner more support with two-thirds (68%) in favor a public option that would compete with private health plans and be available to all Americans (28% oppose).

Figure 15: Roughly Seven In Ten Say They Favor A Government-Administered Public Option While Over Half Say They Favor Medicare-for-all

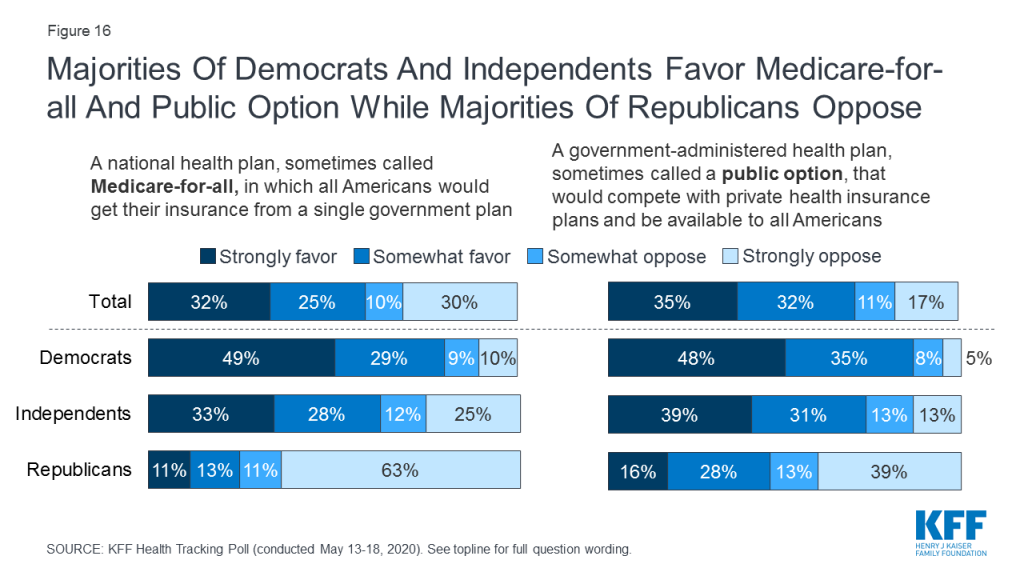

Large majorities of Democrats favor both Medicare-for-all (78%) and a public option (84%), as do majorities of independents (60% favor Medicare-for-all, 70% favor a public option). Among Republicans, one in four (24%) support a national Medicare-for-all plan while more than four in ten (44%) favor a public option.

Figure 16: Majorities Of Democrats And Independents Favor Medicare-for-all And Public Option While Majorities Of Republicans Oppose

This KFF Health Tracking Poll was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). The survey was conducted May 13th – 18th, 2020, among a nationally representative random digit dial telephone sample of 1,189 adults ages 18 and older, living in the United States, including Alaska and Hawaii (note: persons without a telephone could not be included in the random selection process). The sample included 290 respondents reached by calling back respondents that had previously completed an interview on the KFF Tracking poll at least nine months ago. Computer-assisted telephone interviews conducted by landline (283) and cell phone (906, including 634 who had no landline telephone) were carried out in English and Spanish by SSRS of Glen Mills, PA. To efficiently obtain a sample of lower-income and non-White respondents, the sample also included an oversample of prepaid (pay-as-you-go) telephone numbers (25% of the cell phone sample consisted of prepaid numbers) as well as a subsample of respondents who had previously completed Spanish language interviews on the SSRS Omnibus poll (n=9). Both the random digit dial landline and cell phone samples were provided by Marketing Systems Group (MSG). For the landline sample, respondents were selected by asking for the youngest adult male or female currently at home based on a random rotation. If no one of that gender was available, interviewers asked to speak with the youngest adult of the opposite gender. For the cell phone sample, interviews were conducted with the adult who answered the phone. KFF paid for all costs associated with the survey.

The combined landline and cell phone sample was weighted to balance the sample demographics to match estimates for the national population using data from the Census Bureau’s 2018 American Community Survey (ACS) on sex, age, education, race, Hispanic origin, and region along with data from the 2010 Census on population density. The sample was also weighted to match current patterns of telephone use using data from the July-December 2018 National Health Interview Survey. The weight takes into account the fact that respondents with both a landline and cell phone have a higher probability of selection in the combined sample and also adjusts for the household size for the landline sample, and design modifications, namely, the oversampling of prepaid cell phones and likelihood of non-response for the re-contacted sample. All statistical tests of significance account for the effect of weighting.

The margin of sampling error including the design effect for the full sample is plus or minus 3 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Note that sampling error is only one of many potential sources of error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

Nearly One in Four Expect a Family Member to Turn to Medicaid in the Coming Year, and Majorities across Party Lines Oppose Medicaid Cuts to Address State Budget Shortfalls

Amid the threat of coronavirus, nearly half (48%) of Americans say someone in their family has skipped or delayed getting some type of medical care due to the pandemic, the latest KFF Health Tracking Poll finds. This includes 11% who say the person’s condition worsened due to the missed care.

The findings come as many states move to relax some restrictions on businesses, including health care providers, aimed at limiting the spread of COVID-19, which has already caused about 100,000 deaths nationwide.

Among those who say they or a family member skipped care, most say they expect to get the care within the next three months (68% of the group, or 32% of all adults). Few say they do not expect to get the care for at least a year or at all.

“Most of those who have put off care due to coronavirus expect to get it soon,” KFF President and CEO Drew Altman said. “If they do, health care utilization may bounce back more quickly than the rest of the economy.”

Most adults (86%) say their physical health has stayed about the same since the outbreak began, but the crisis continues to take a toll on people’s mental health. Four in 10 adults (39%) this month say worry and stress related to coronavirus has had a negative impact on their mental health. This includes one in eight (12%) who say it has had a “major” negative impact, a slight dip from six weeks ago (19%).

Majorities across Party Lines Oppose Cuts to Medicaid Spending to Address State Budget Shortfalls

With unemployment rising and employer coverage at risk, nearly one in four (23%) adults who are not currently covered by Medicaid also say they or a family member likely will turn to the program in the next year. This includes about three in 10 (31%) of those who have lost a job or income recently due to coronavirus.

Three-quarters (74%) of the public say they would oppose state Medicaid cuts to address budget shortfalls spurred by the coronavirus pandemic and economic downturn, while a quarter (24%) say they would favor them. Most Democrats (85%), independents (73%), and Republicans (62%) say they oppose decreasing Medicaid spending.

Majorities across partisan identification also say they would oppose cuts to balance their state’s budget affecting public schools, police and public safety, and jails and prisons. Most across parties would support cuts to transportation spending, while partisans are split over cuts to higher education, social services and environmental protection with majorities of Democrats opposing all of these cuts.

Most states have expanded their Medicaid programs under the Affordable Care Act to cover low-income childless adults. In the 14 states that haven’t, two-thirds (66%) of residents say they favor their state expanding Medicaid to cover more low-income uninsured people, while one-third (32%) want to keep Medicaid as it is today.

Economic Turmoil is Making it Harder for Many to Pay Bills and Afford Routine Expenses

The poll also examines the crisis’ economic impact on families. Overall about three in 10 (31%) people report at least some difficulties paying their bills or affording routine expenses because of coronavirus.

This includes about one in six who say they have fallen behind in paying credit card or other bills (18%), have had problems paying their utilities (17%), or fallen behind in paying their rent or mortgage (15%). About one in ten report problems paying for food (13%), paying medical bills (11%), affording health coverage (9%), or paying for prescription drugs (8%).

Among those living in households that experienced a job or income loss due to coronavirus (who make up one-third of all adults), about half (49%) report at least one of those difficulties paying household expenses.

In addition, one in four (26%) Americans also say they or someone in their household has skipped meals or relied on charity or government programs to get enough to eat. Most of those skipping meals or relying on assistance attribute their need to the coronavirus pandemic and its impact on their financial situation (59%, or 16% of the overall public). A smaller share (39%, or 10% of the overall public) say they were already experiencing problems affording food before the outbreak.

Those most likely to struggle with getting enough food specifically because of coronavirus include those in families who have lost a job or income (30%), as well as Blacks (30%) and Hispanics (26%).

Views of Medicare-for-all, a Public Option, and the ACA Largely Unchanged since Coronavirus

While the COVID-19 crisis has renewed attention on health coverage and cost issues, it has had little impact on the public’s views toward two main Democratic approaches to expanding coverage debated during the 2020 primary season – Medicare-for-all, championed by Sen. Bernie Sanders, and a voluntary “public option” plan, promoted by former Vice President Joe Biden.

While majorities of the public support both approaches, more people continue to say they favor a public option (68%) than say they favor Medicare-for-all (56%) – the same shares that favored each proposal in January before coronavirus became a major concern in the U.S.

About half the public (51%) now holds favorable views toward the Affordable Care Act, while 41% hold unfavorable views – similar to the results in January (53% favorable, 39% unfavorable).

Designed and analyzed by public opinion researchers at KFF, the poll was conducted May 13-18 among a nationally representative random digit dial telephone sample of 1,189 adults. Interviews were conducted in English and Spanish by landline (283) and cell phone (906). The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

Filling the need for trusted information on national health issues, KFF (Kaiser Family Foundation) is a nonprofit organization based in San Francisco, California.

Sweden’s response to the novel coronavirus has been simultaneously praised and criticized by public health experts. In an article for Foreign Affairs, KFF’s Josh Michaud discusses the merits and risks associated with Sweden’s hands-off approach to the pandemic.

“While there is some debate about what the ‘Swedish model’ actually is, many would likely agree there are two primary differences between that country’s response and responses of other Western countries. One is that the Swedish government has taken a remarkably hands-off approach to managing the pandemic—an approach from which other countries could learn as they prepare for the long haul. The other characteristic that distinguishes Sweden’s response is its undeclared but widely acknowledged objective of achieving herd immunity. Here, other governments would do well to heed warning signs and be wary of following Sweden’s lead.”

The coronavirus pandemic and resulting economic downturn is hitting the United States at a time when unexpected medical bills were already a primary concern for many Americans. Throughout the crisis, states, Congress, the Trump Administration, and private insurance plans have taken various actions to mitigate some affordability challenges that could arise from, or prevent timely access to, COVID-19 testing and treatment. In this brief, we answer key questions on affordability of COVID-19 testing and treatment for people who are uninsured and those insured through private coverage, Medicare, and Medicaid. We also explore broader concerns around deductibles, assets, and job loss.

1. How much will patients pay for COVID-19 testing?

Since the passage of the Families First Coronavirus Response Act (FFCRA) on March 18, most people should not face costs for the COVID-19 test or associated costs. Starting on March 18 and lasting for the duration of the public health emergency, all forms of public and private insurance, including self-funded plans, must now cover FDA-approved COVID-19 tests and costs associated with diagnostic testing with no cost-sharing, as long as the test is deemed medically appropriate by an attending health care provider. This includes high-deductible health plans and grandfathered plans, but does not apply to short-term, limited duration plans. As outlined by CMS in a series of FAQs, there is no limit on the number of COVID-19 tests that an insurer or plan is required to cover for an individual, as long as each test is deemed medically appropriate and the individual has signs or symptoms of COVID-19 or has had known or suspected recent exposure to SARS-CoV-2. Federal guidance does not require coverage of routine tests that employers or other institutions may require for screening purposes as workplaces reopen.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act, enacted on March 27, 2020, expanded protections by requiring private plans to also fully cover out-of-network tests. The CARES Act requires health plans to reimburse out-of-network COVID-19 test claims at up to the cash price that the provider has posted on a public web site. The CARES Act is silent as to the amount private plans should reimburse out-of-network COVID test providers that do not post their cash price online, though the law does require a civil money penalty of up to $300 per day for providers that fail to post prices. The CARES Act also does not prohibit out-of-network providers from billing patients directly for the COVID-19 test; if that happens, and if the up-front expense is unaffordable, it could deter some patients from getting a test. Otherwise, when providers charge cash up front, it falls to the patient to submit the bill to the health plan for reimbursement.

Medicare, Medicaid, and private plans also must cover serology tests that can determine whether an individual has been infected with SARS-CoV-2, the virus that causes COVID-19, and developed antibodies to the virus.

As background, the Centers for Medicare and Medicaid Services has announced that Medicare will reimburse providers up to $100 per test, depending on the test. Newer COVID-19 tests that give results more quickly may cost providers more than the early tests. A number of private providers, including some that take no insurance, are charging substantially more than $100 for COVID-19 tests.

2. How much will patients pay for COVID-19 treatment?

In contrast to federal law for coverage of testing, there has not yet been comprehensive federal legislation to limit cost-sharing for treatment of COVID-19, such as hospitalization for those who become very ill.