Donor Government Funding for HIV in Low- and Middle-Income Countries in 2024

Overview

This report, Donor Government Funding for HIV in Low- and Middle-Income Countries in 2024, tracks funding levels of the donor governments that collectively provide the bulk of international assistance for AIDS through bilateral programs and contributions to multilateral organizations. The new report, produced as a partnership between KFF and UNAIDS, provides the latest data available on donor funding disbursements based on data provided by governments. It includes their bilateral assistance to low- and middle-income countries and contributions to the Global Fund to Fight AIDS, Tuberculosis and Malaria as well as UNITAID.

Previous versions by publish date:

July 2023 (.pdf)

July 2022 (.pdf)

July 2021 (.pdf)

July 2020 (.pdf)

July 2019 (.pdf)

July 2018 (.pdf)

July 2017 (.pdf)

July 2016 (.pdf)

July 2015 (.pdf)

July 2014 (.pdf)

September 2013 (.pdf)

July 2012 (.pdf)

July 2011 (.pdf)

July 2010 (.pdf)

July 2009 (.pdf)

July 2008 (.pdf)

June 2007 (.pdf)

July 2006 (.pdf)

July 2005 (.pdf)

Key Findings

In 2025, the donor government funding landscape fundamentally changed. Under the new administration, the United States, the largest donor to HIV in the world, has instituted significant changes to global health programs including freezing, and then cancelling, most global HIV projects, restricting allowable activities, and seeking to cut HIV funding by at least 40%, actions which have collectively driven down disbursements. In addition, several other large donors to HIV – the United Kingdom, Germany and France – have also signaled reductions in their development assistance budgets. As such, this report, which focuses on both bilateral and multilateral funding for HIV provided by donor governments in 2024 and shows an increase over 2023, is likely the high watermark as funding will likely decline moving forward. While the U.S. has shouldered much of the burden of funding the HIV response, its abrupt reductions leave large gaps and could set back the HIV response, as some studies have already found. Key findings are as follows:

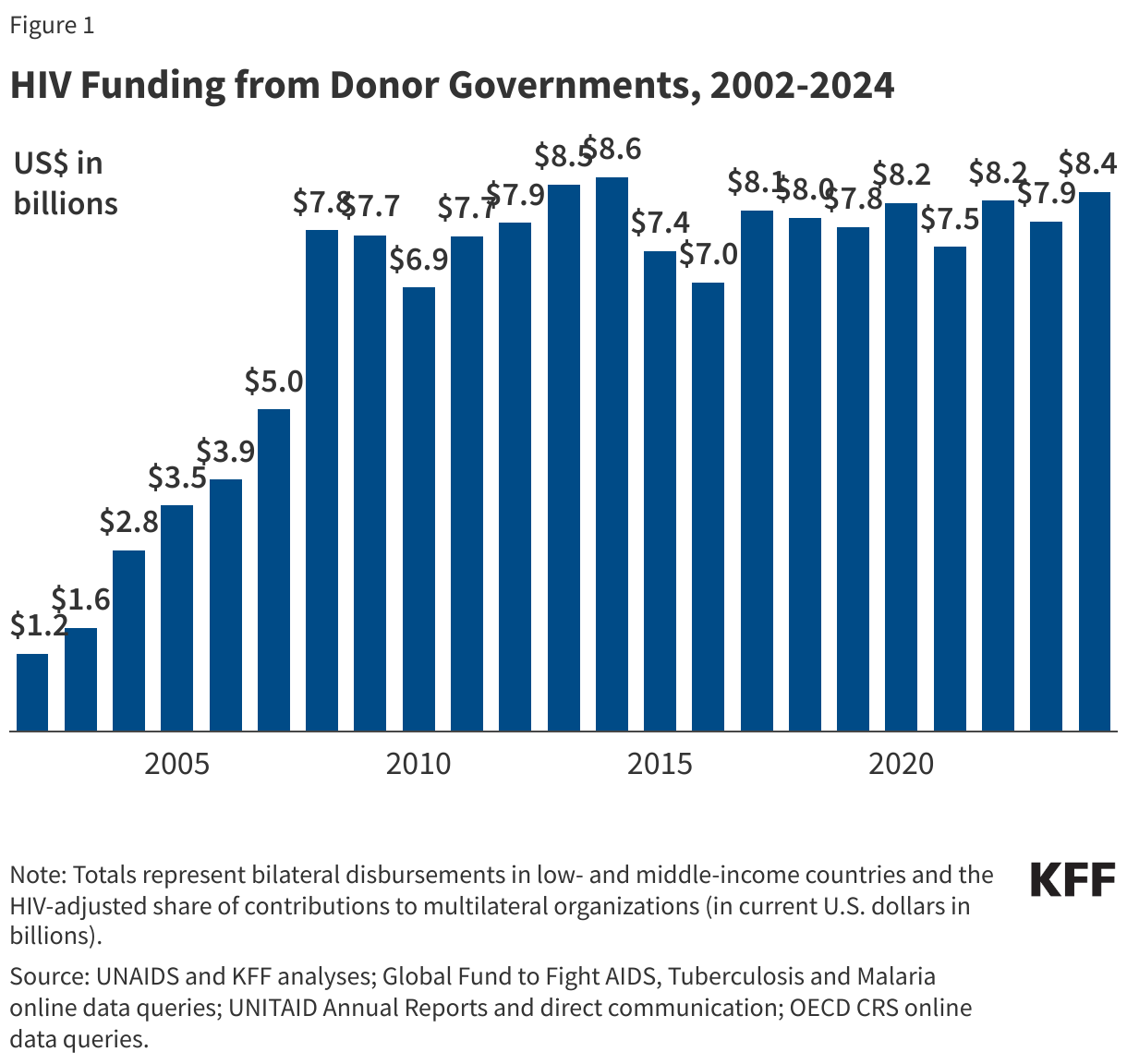

- Donor government funding for HIV increased in 2024 compared to the prior year. Disbursements for combined bilateral and multilateral support were US$8.37 billion in 2024, an increase of US$460 million compared to 2023 (US$7.91 billion), in current U.S. dollars (not adjusted for inflation).1 Funding increased even after accounting for exchange rate fluctuations. Looking more broadly, donor government funding for HIV in 2024 was at its highest level since 2014 (US$8.60 billion), but still below that peak.

- The increase in 2024 was almost entirely due to the timing of disbursements by the U.S., not actual changes in funding commitments. The timing of disbursements, or payouts, by donor governments fluctuates each year and those fluctuations can affect overall levels of funding availability, independent of donor funding commitments. In 2024, the U.S. government’s disbursements for HIV increased significantly, while the U.K.’s payout declined, but both were due to the timing of payouts. Other donors had similar fluctuations. Because the U.S. is the largest donor, its fluctuations drove up overall funding levels in 2024.

- Bilateral funding increased in 2024, driven by payout timing. Bilateral funding totaled US$5.87 billion in 2024, an increase of US$241 million compared to 2023 (US$5.63 billion), with five donors providing increased disbursements. The increase was primarily the result of higher funding from the U.S., due to the timing of payouts, and the U.K., as well as slight increases from Australia, Japan, and Norway. Funding from eight donor governments decreased and two remained flat.

- Multilateral funding, which is the main channel of support for HIV used by most donor governments, also increased in 2024, similarly due to the timing of contributions. Multilateral funding totaled US$2.50 billion in 2024, an increase of US$218 million compared to 2023 (US$2.28 billion). Six donor governments increased multilateral support, while four remained flat, and five declined. Most multilateral funding for HIV was provided to the Global Fund (US$2.27 billion or 91%) with smaller amounts provided to UNAIDS (US$169 million or 7%) and UNITAID (US$59 million or 2%). The timing of payments to the Global Fund drove the multilateral increase in 2024.

- The U.S. has consistently been the largest donor to HIV. In 2024, the U.S. provided US$6.69 billion for HIV (bilateral and multilateral combined), accounting for 80% of total donor government support.2 France was the second largest donor (US$314 million, 4%), followed by Germany (US$226 million, 3%), the U.K. (US$218 million, 3%), and the Netherlands (US$192 million, 2%).3 ,4 Even when standardized by the size of its economy (per million GDP), the U.S. ranked first. The next largest donor, per million GDP, was the Netherlands, followed by Denmark, France, and Norway.

Looking ahead, donor government funding for HIV is expected to decline in 2025 and beyond. Due to the new administration’s actions targeting U.S. foreign assistance programs, including for global health and HIV, U.S. disbursements for HIV this year are well below prior year levels.5 In addition, the administration has asked Congress to rescind (formerly cancel) approximately US$400 million in bilateral HIV funding for 2025 and has proposed reducing the HIV budget by at least 40% in 2026. If these cuts were to materialize, other donor governments would have to more than double their HIV funding to maintain current levels. Given that the U.S. has already reduced HIV spending in 2025 and several other large donors have announced plans to reduce foreign assistance, funding for HIV in low- and middle-income countries is highly likely to decline.

Report

Introduction

This report provides the latest available data on donor government resources provided to address HIV in low- and middle-income countries, reporting on disbursements made in 2024. It is part of a collaborative tracking effort between UNAIDS and KFF that began almost 20 years ago, just as new global initiatives were being launched to address the epidemic. The analysis includes data from all 33 members of the Organisation for Economic Co-operation and Development (OECD)’s Development Assistance Committee (DAC), as well as non-DAC members who report data to the DAC. Data are collected directly from donor governments, UNAIDS, the Global Fund, and UNITAID, and supplemented with data from the DAC. Of the 33 DAC members, fifteen provide 98% of total disbursements for HIV; data for these donors are presented individually. For the remaining 18 DAC members, data are provided in aggregate. All totals are presented in current U.S. dollars (amounts are not adjusted for inflation). While totals include both bilateral and multilateral assistance for the entire period (2002-2024), detailed disaggregated bilateral and multilateral amounts for all donors are only available starting in 2011 (see Methodology for more detail).

Importantly, given that the donor government funding landscape fundamentally changed in 2025, the data provided here likely represent a high watermark for HIV funding. Under the new administration, the United States, the largest donor to HIV in the world, began instituting significant changes to global health programs in January 2025, including freezing, and then cancelling, most global HIV projects, restricting allowable activities, and seeking to cut HIV funding by at least 40%, actions which have collectively driven down disbursements. If U.S. reductions continue and future cuts were to be enacted, other donor governments would have to more than double their funding to maintain current levels. Yet several other large donors to HIV – the United Kingdom, Germany and France – have also signaled reductions in their development assistance budgets, making it highly likely that future funding will be reduced.

Findings

Total Funding

In 2024, donor government funding for HIV through bilateral and multilateral channels totaled US$8.37 billion in current USD (not adjusted for inflation) and accounted for approximately 44% of the US$18.7 billion estimated by UNAIDS to be available to address HIV.6 ,7 ,8 ,9 As per UNAIDS estimates, domestic resources accounted for 52%, and the remainder (4%) was from foundations, other multilateral organizations, and UN agencies.

Donor government funding for HIV in 2024 increased by US$460 million compared to 2023 (US$8.37 in 2024 compared to US$7.91 billion in 2023) and reached the highest level since 2014 (US$8.60 billion), though it is still below that highpoint (See Figure 1 and Table 1).10

The increase in 2024 was almost entirely due to the timing of disbursements, or payouts, by donor governments, which can fluctuate from year-to-year, not actual changes in funding commitments. For instance, U.S. disbursements increased significantly in 2024 while funding from the U.K. declined, but both were due to the timing of payouts. As two of the world’s largest donors, these fluctuations can have an outsized impact on the overall amount of available funding in a given year.

The U.S. continued to be the largest donor to HIV efforts, providing US$6.69 billion and accounting for 80% of total donor government funding in 2024.11 The second largest donor was France (US$314 million, 4%), followed by Germany (US$226 million, 3%), the U.K. (US$218 million, 3%), and the Netherlands (US$192 million, 2%).12 ,13 In 2024, 91% of total donor government funding for HIV was provided by these five donors.

Bilateral Disbursements

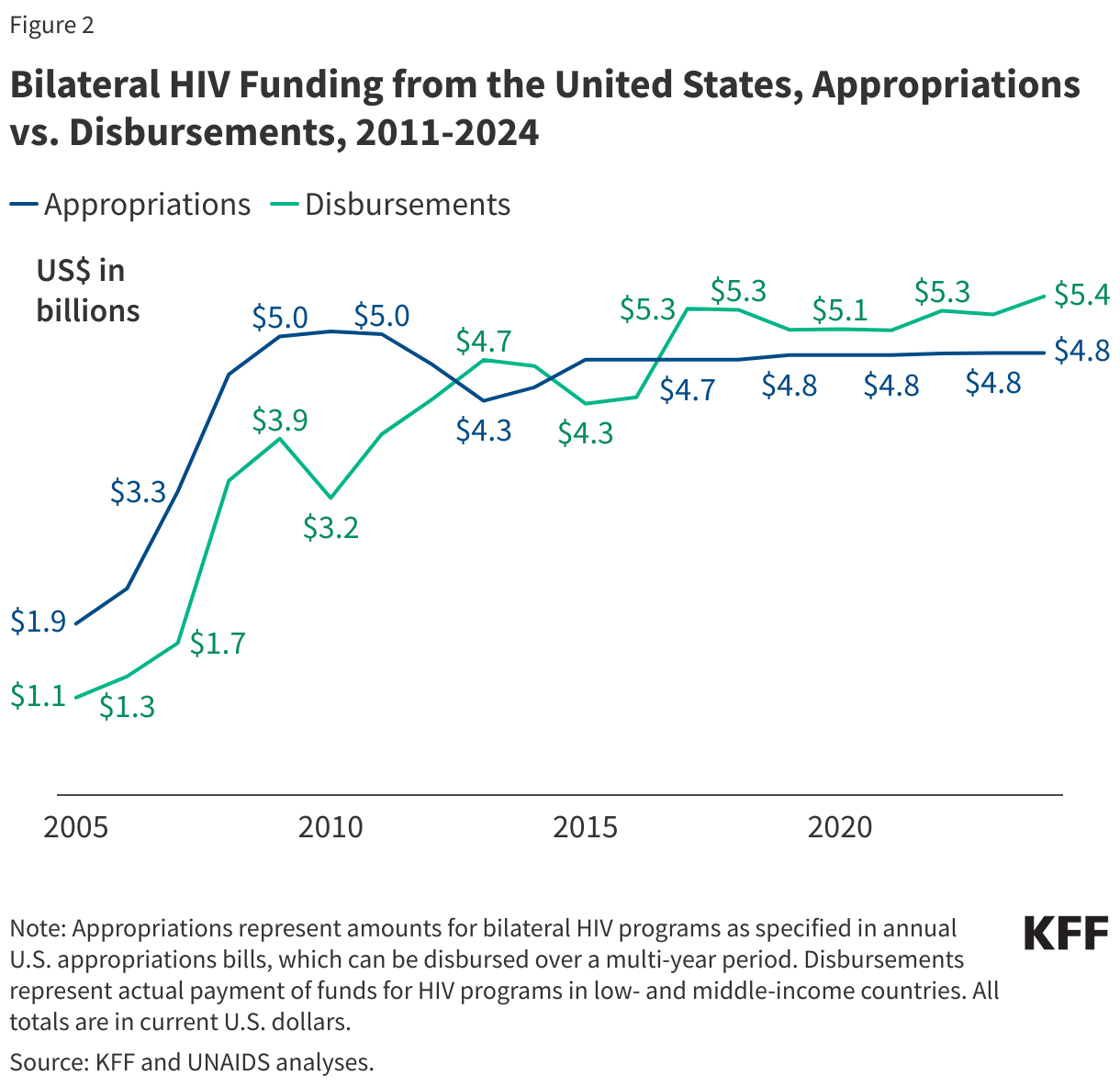

Bilateral disbursements for HIV from donor governments – that is, funding disbursed by a donor on behalf of a recipient country or region – totaled US$5.87 billion in 2024, an increase of US$241 million compared to 2023 (US$5.63 billion). Despite the increase, bilateral funding from most donor governments decreased or remained flat and most of the overall increase was attributable to the U.S. and the U.K. When the increases from the U.S. and U.K. are removed, bilateral funding from all other donor governments declined by US$49 million in 2024 (US$237 million) compared to 2023 (US$286 million). These trends were the same after accounting for exchange rate fluctuations.

Bilateral disbursements from the U.S. increased by almost US$200 million in 2024 (US$5.43 billion) compared to 2023 (US$5.23 billion), due to the timing of payouts, but not actual increases in funding commitments. In fact, bilateral HIV funding as specified by the U.S. Congress in annual appropriations bills has been flat for several years (see Figure 2).14 ,15

Multilateral Contributions

Multilateral contributions from donor governments to the Global Fund, UNITAID, and UNAIDS for HIV – funding disbursed by donor governments to these organizations which in turn use some (Global Fund and UNITAID) or all (UNAIDS) of that funding for HIV – totaled US$2.50 billion in 2024 (after adjusting for an HIV share to account for the fact that the Global Fund and UNITAID address other diseases). This represents an increase of US$218 million compared to 2023 (US$2.28 billion).16 ,17 The Global Fund accounted for most of the multilateral funding for HIV in 2024 (US$2.27 billion or 91%), followed by UNAIDS (US$169 million or 7%) and UNITAID (US$59 million or 2%).

The increase in 2024 disbursements was due to the timing of payments to the Global Fund, particularly from the U.S., which is required by law not to exceed 33% of total contributions to the Global Fund from all donors and results in significant year-to-year differences depending on the amounts other donors have provided.18 In addition, funding from donor governments to the Global Fund often fluctuates reflecting different Global Fund pledge periods. For instance, some donors choose to “front-load” contributions (e.g., the U.K. fulfilled almost its entire pledge for 2023-2025 in 2023 resulting in a significant decrease in 2024), while others choose to fulfill pledges towards the end of the pledge period (e.g., Australia and Denmark did not provide any contribution in 2023, but both fulfilled more than half their pledges in 2024).

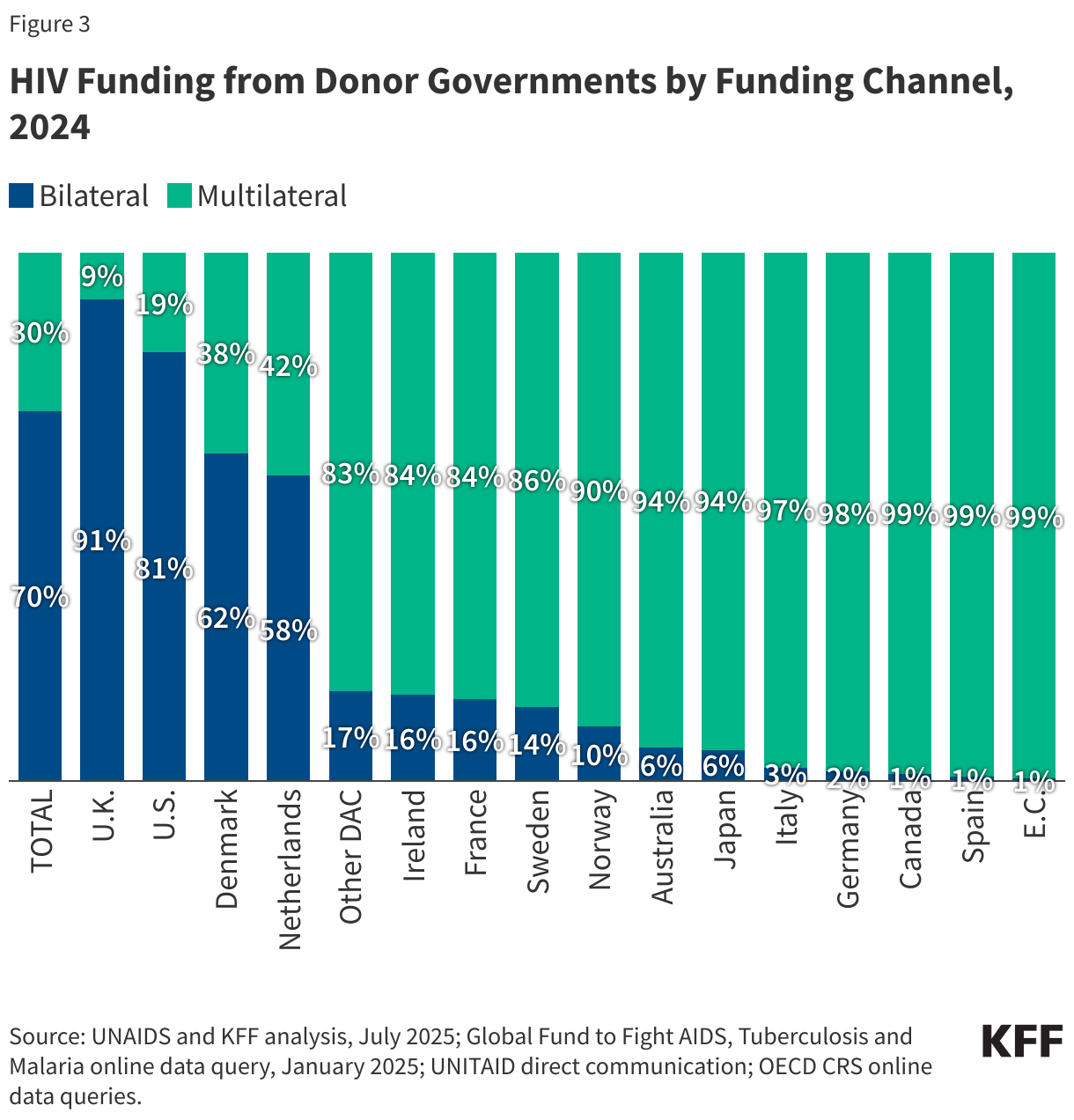

Most donor governments provide the majority of their HIV funding through multilateral organizations. In 2024, eleven provided more than 80% of their HIV funding multilaterally; only Denmark, the Netherlands, the U.K., and the U.S. provided a larger share bilaterally (Figure 3). While the U.K. provided most of its HIV funding bilaterally in 2024, this was entirely due to the timing of payments to the Global Fund. The U.K. fulfilled almost its entire pledge to the Global Fund for 2023-205 in 2023 resulting in significantly lower levels of multilateral funding in 2024. In fact, between 2019-2023, most HIV funding from the U.K. was provided through multilateral channels.

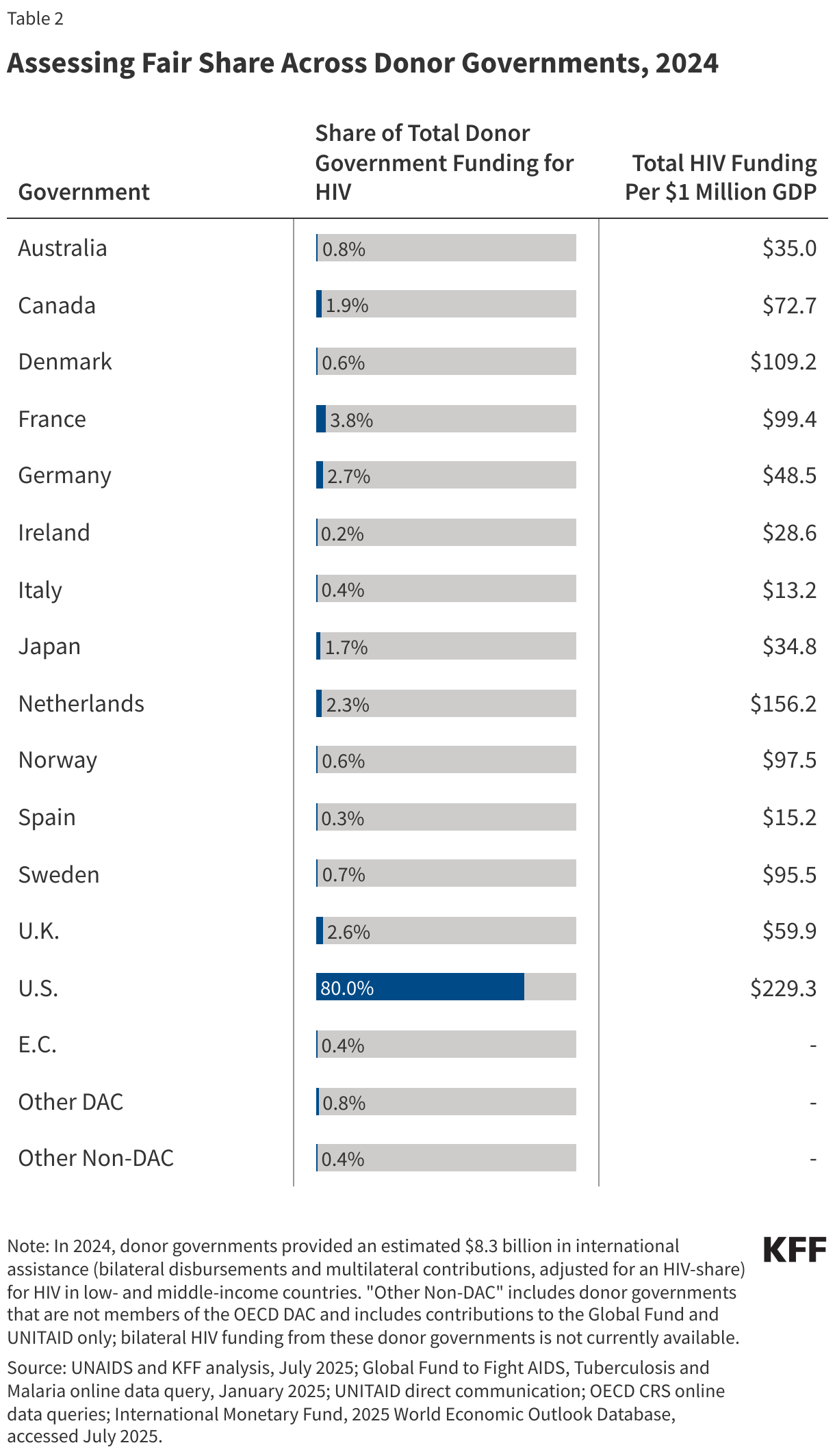

Fair Share

There are different ways to measure donor government contributions to HIV, relative to one another. While the U.S. government provides the largest amount of funding for HIV, for example, it also has the largest economy in the world. To assess relative contributions, or “fair share”, two measures were used: ranking by overall funding amount and ranking by funding for HIV per US$1 million GDP, to adjust for the size of donor economies (See Table 2):

- Rank by share of total donor government funding for HIV: By this measure, the U.S. ranked first in 2024, followed France, Germany, the U.K., and the Netherlands. The U.S. has ranked #1 in absolute funding amounts since tracking efforts began.

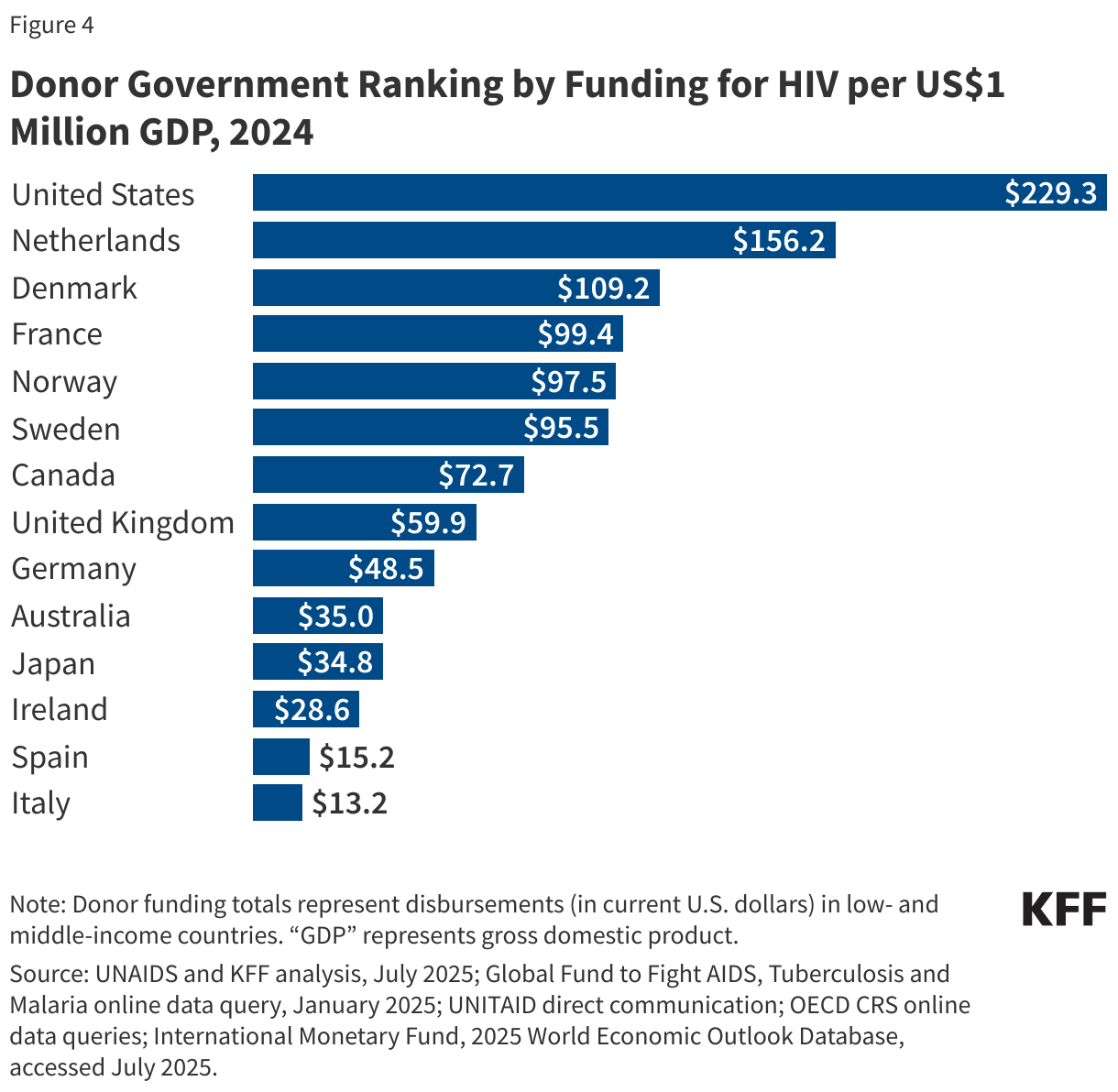

- Rank by funding for HIV per US$1 million GDP: By this measure, the U.S. ranks first, followed by the Netherlands, Denmark, France, and Norway (See Figure 4).19

Looking Forward

Donor government funding for HIV in low and middle-income countries is likely to decline in 2025. While the anticipated decline is largely due to actions by the new administration, which have already resulted in lower disbursements in 2025, other donor governments have also indicated plans to reduce foreign assistance. Looking beyond 2025, the new administration has proposed to reduce HIV funding by at least 40% in 2026. Since the U.S. is the world’s largest donor to the global HIV response, a cut in funding of this size would require other donor governments to more than double their funding to fill the gap, an increase that seems unlikely. While final funding amounts are determined by the U.S. Congress, the administration’s actions may continue to have the effect of reducing HIV funding from the U.S.

This work was supported in part by the Joint United Nations Programme on HIV and AIDS (UNAIDS) and the Bill & Melinda Gates Foundation. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Adam Wexler and Jen Kates are with KFF. Eric Lief is an independent consultant. Joint United Nations Programme on HIV and AIDS (UNAIDS).

Methodology

This project represents a collaboration between the Joint United Nations Programme on HIV/AIDS (UNAIDS) and KFF. Data provided in this report were collected and analyzed by UNAIDS and KFF.

Totals presented in this analysis include both bilateral funding for HIV in low- and middle-income countries, core contributions to UNAIDS, and the estimated share of donor government contributions to the Global Fund and UNITAID that are used for HIV. Amounts are based on analysis of data from the 32 donor government members of the Organisation for Economic Co-operation and Development (OECD) Development Assistance Committee (DAC) in 2024 who had reported Official Development Assistance (ODA). Bilateral and multilateral data were collected from multiple sources. Disaggregated bilateral and multilateral data are only available starting from 2011.

Data on gross domestic product (GDP) were obtained from the International Monetary Fund’s World Economic Outlook Database and represent current price data for 2024 (see: https://www.imf.org/en/Publications/WEO/weo-database/2025/April).

Bilateral Funding:Bilateral funding is defined as any earmarked (HIV-designated) amount, including earmarked non-core (“multi-bi”) contributions to multilateral organizations, such as UNAIDS. Data included in this report represent funding assistance for HIV prevention, care, treatment and support activities, but do not include funding for international HIV research conducted in donor countries (which is not considered in estimates of resource needs for service delivery of HIV-related activities).

The research team collected the latest bilateral funding data directly from twelve governments: Australia, Canada, Denmark, France, Germany, Ireland, Japan, the Netherlands, Norway, Sweden, the United Kingdom, and the United States during the first half of 2025, representing the fiscal year 2024 period. Direct data collection from these donors was desirable because they represent the preponderance of donor government assistance for HIV and the latest official statistics – from the Organisation for Economic Co-operation and Development (OECD) Creditor Reporting System (CRS) (see: http://www.oecd.org/dac/stats/data) – are from 2023 and do not include all forms of international assistance (e.g., certain funding streams provided by donors, such as HIV components of mixed-purpose grants to non-governmental organizations). Data for all other member governments of the OECD DAC – Austria, Belgium, the Czech Republic, the European Commission, Estonia, Finland, Greece, Hungary, Iceland, Italy, Korea, Lithuania, Luxembourg, New Zealand, Poland, Portugal, the Slovak Republic, Slovenia, Spain, and Switzerland – which collectively accounted for less than 5 percent of bilateral disbursements in each of the past several years, were obtained from the OECD CRS database and are from calendar year 2023.

In 2025, France provided data revising prior year amounts to account for “set-aside” funding (adjusted for an HIV-share) that supports Global Fund related activities. While this funding is considered part of France’s pledge to the Global Fund, it is not counted by the Global Fund as a direct contribution and is instead included under bilateral totals in this analysis. Due to this update, amounts presented in this report will differ from prior reports.

Where donor governments were members of the European Union (EU), the research team ensured that no double-counting of funds occurred between EU Member State reported amounts and European Commission (EC) reported amounts for international HIV assistance. Figures obtained directly using this approach should be considered as the upper bound estimation of financial flows in support of HIV-related activities.

Reflecting deliberate strategies of integrating HIV activities into other activity sectors, some donors use policy markers to attribute portions of mixed-purpose projects to HIV. This is done, for example, by the Netherlands and the U.K. The bilateral figures submitted by the UK Foreign, Commonwealth & Development Office (FCDO) for the financial year 2024/25 are based on an existing FCDO ‘HIV policy marker’. Ireland and Denmark also attribute percentages of multipurpose projects to HIV. Canada breaks its mixed-purpose projects into components by percentage. Germany, Norway, and Sweden provided data much more conservatively, consistent with DAC constructs and purpose codes. Apart from targeted HIV/AIDS programs, bilateral health programs mainly focusing on health systems strengthening are also designed to contribute to the HIV response in partner countries.

Bilateral assistance data represent disbursements. A disbursement is the actual release of funds to, or the purchase of goods or services for, a recipient. Disbursements in any given year may include disbursements of funds committed in prior years and in some cases, not all funds committed during a government fiscal year are disbursed in that year. In addition, a disbursement by a government does not necessarily mean that the funds were provided to a country or other intended end-user.

Amounts presented are for the fiscal year period, which varies by country. The U.S. fiscal year runs from October 1-September 30. The fiscal years for Canada, Japan, and the U.K. are April 1-March 31. The Australian fiscal year runs from July 1-June 30. The European Commission, Denmark, France, Germany, Italy, Ireland, the Netherlands, Norway, and Sweden use the calendar year. The OECD uses the calendar year, so data collected from the CRS for other donor governments reflect January 1-December 31. Most UN agencies use the calendar year, and their budgets are biennial.

All data are expressed in current US dollars (USD), unless otherwise noted. Where data were provided by governments in their currencies, they were adjusted by average daily exchange rates to obtain a USD equivalent, based on foreign exchange rate historical data available from the U.S. Federal Reserve (see: http://www.federalreserve.gov/) or the OECD.

Funding totals presented in this analysis should be considered preliminary estimates based on data provided and validated by representatives of the donor governments who were contacted directly.

Multilateral Funding:Multilateral funding includes core contributions to UNAIDS, as well as contributions to the Global Fund (see: http://www.theglobalfund.org/en/) and UNITAID (see: http://www.unitaid.org/#end). All Global Fund contributions were adjusted to represent 52% of the donor’s core contribution, reflecting the Fund’s reported grant approvals for HIV-related projects to date and includes funding for HIV/TB activities. UNITAID contributions were adjusted to represent 46% of the donor’s core contribution, reflecting UNITAID’s reported attribution for HIV-related projects.

Data obtained from UNAIDS, the Global Fund, and UNITAID were already adjusted to represent a USD equivalent based on date of receipts.

UNAIDS core contributions reflect amounts received in 2024. In 2024, the Netherlands provided two core contributions to UNAIDS; the first payment was provided for the 2024 contribution, while the second was a prepayment of the 2025 contribution. Global Fund and UNITAID contributions from all governments correspond to amounts received during the 2024 calendar year, regardless of which contributor’s fiscal year such disbursements pertain to.

In addition to contributions supporting the Global Fund’s and UNITAID’s core activities, some donor governments provided significant funding to these multilateral organizations for COVID-related efforts between 2020-2023. These COVID-specific contributions were not included in totals in this analysis. The U.S., for example, provided almost US$1.9 billion in such funding to the Global Fund during 2022.

Other than contributions provided by governments to the Global Fund and UNITAID, un-earmarked general contributions to United Nations entities, most of which are membership contributions set by treaty or other formal agreement (e.g., the World Bank’s International Development Association or United Nations country membership assessments), are not identified as part of a donor government’s HIV assistance even if the multilateral organization in turn directs some of these funds to HIV. Rather, these would be considered as HIV funding provided by the multilateral organization, as in the case of the World Bank’s efforts, and are not considered for purposes of this report.

Appendix

Endnotes

- Between 2020-2023, some donor governments provided COVID-specific emergency contributions to the Global Fund and UNITAID in addition to their contributions for core activities. For the purposes of this report, these COVID-specific amounts have been excluded as they cannot be attributed to a specific area, such as HIV. ↩︎

- U.S. totals represent funding amounts provided through regular appropriations only. In 2021, the U.S. Congress appropriated additional emergency supplemental funding for bilateral HIV activities and for the Global Fund to address the impacts of the COVID-19 pandemic. These emergency supplemental funding amounts are not included in overall U.S. totals. ↩︎

- In 2025, France provided data revising prior year amounts to account for “set-aside” funding (adjusted for an HIV-share) that supports Global Fund related activities. While this funding is considered part of France’s pledge to the Global Fund, it is not counted by the Global Fund as a direct contribution and is instead included under bilateral totals in this analysis. Due to this update, amounts presented in this report will differ from prior reports. ↩︎

- Total HIV funding from the Netherlands in 2024 includes two core contributions to UNAIDS; the first payment was provided for the 2024 contribution, while the second was a prepayment of the 2025 contribution. ↩︎

- KFF analysis of data from USAspending.gov and Treasury.gov. ↩︎

- Donor government disbursements are a subset of overall international assistance for HIV in low-and-middle-income countries, which also includes funding provided by other multilateral institutions, UN agencies, and foundations. ↩︎

- UNAIDS, “UNAIDS Global AIDS Update 2025: AIDS, Crisis and the Power to Transform”, July 2025. ↩︎

- UNAIDS estimates that US$18.7 billion was available for HIV from all sources (domestic resources, donor governments, multilaterals, and philanthropic organizations) in 2024. In addition, while the amounts presented in this analysis include donor contributions to multilateral organizations, the UNAIDS estimate of total available resources for HIV includes the actual disbursements made by multilateral organizations in 2024 rather than the donor government contributions to these entities. ↩︎

- The donor share of total available resources includes bilateral disbursements as well as an adjusted share of Global Fund and UNITAID disbursements (the donor government share of contributions to each of the multilaterals in 2024 is applied to the disbursements from these multilaterals for the same year). ↩︎

- KFF & UNAIDS, “Donor Government Funding for HIV in Low- and Middle-Income Countries in 2023”, July 2024. ↩︎

- U.S. totals represent funding amounts provided through regular appropriations only. In 2021, the U.S. Congress appropriated additional emergency supplemental funding for bilateral HIV activities and for the Global Fund to address the impacts of the COVID-19 pandemic. These emergency supplemental funding amounts are not included in overall U.S. totals. ↩︎

- In 2025, France provided data revising prior year amounts to account for “set-aside” funding (adjusted for an HIV-share) that supports Global Fund related activities. While this funding is considered part of France’s pledge to the Global Fund, it is not counted by the Global Fund as a direct contribution and is instead included under bilateral totals in this analysis. Due to this update, amounts presented in this report will differ from prior reports. ↩︎

- Total HIV funding from the Netherlands in 2024 includes two core contributions to UNAIDS; the first payment was provided for the 2024 contribution, while the second was a prepayment of the 2025 contribution. ↩︎

- KFF, “The U.S. President’s Emergency Plan for AIDS Relief (PEPFAR)”, May 2025. ↩︎

- U.S. totals represent funding amounts provided through regular appropriations only. In 2021, the U.S. Congress appropriated additional emergency supplemental funding for bilateral HIV activities and for the Global Fund to address the impacts of the COVID-19 pandemic. These emergency supplemental funding amounts are not included in overall U.S. totals. ↩︎

- Between 2020-2023, some donor governments provided COVID-specific emergency contributions to the Global Fund and UNITAID in addition to their contributions for core activities. For the purposes of this report, these COVID-specific amounts have been excluded as they cannot be attributed to a specific area, such as HIV. ↩︎

- In 2024, 52% of the Global Fund’s disbursements and 48% of UNITAID’s disbursements were directed to HIV activities. These percentages were applied to the full donor government contributions to these multilateral organizations to calculate the “HIV-share” (see Methodology for additional details). ↩︎

- The U.S. has had a long-standing legislative requirement that total U.S. contributions to the Global Fund could not exceed 33% of all contributions (see “KFF – The U.S. & The Global Fund to Fight AIDS, Tuberculosis and Malaria”), which results in year-to-year fluctuations in U.S. payouts to the Global Fund depending on when other donors provide funds. However, this requirement technically expired in March when the authorization legislation ended (see “KFF – PEPFAR Reauthorization: Side-by-Side of Legislation Over Time”). ↩︎

- GDP estimates are from the International Monetary Fund’s (IMF) World Economic Outlook (WEO) Database (accessed July 2025). ↩︎