Medicaid Arrangements to Coordinate Medicare and Medicaid for Dual-Eligible Individuals

Issue Brief

Introduction

There are 12.5 million people enrolled in both Medicare and Medicaid, known as “dual-eligible individuals.” Administered and financed by the federal government, Medicare is the primary source of health insurance for people ages 65 and older and covers people under 65 who qualify through the Social Security Disability Insurance program. Jointly financed by the federal and state governments, Medicaid is the nation’s largest public health insurance program for low-income Americans.

Dual-eligible individuals receive their primary health insurance coverage through Medicare and receive additional assistance from their state Medicaid program. They have low incomes and very modest savings but are otherwise a heterogenous group in terms of age, physical, and mental health. Among the 12.5 million dual-eligible individuals in 2020, most (73%) were “full-benefit” dual-eligible individuals meaning they were eligible for the full range of Medicaid benefits that are not otherwise covered by Medicare, such as long-term services and supports. “Partial-benefit” dual-eligible individuals are not eligible for full Medicaid benefits, but are eligible for assistance with Medicare premiums and, in many cases, cost sharing through the Medicare Savings Programs.

Separate eligibility requirements, benefits, and rules for Medicare and Medicaid sometimes contribute to what has been described as a “fragmented and disjointed system of care for dual eligibles.” In response to those challenges, policymakers have created several coverage arrangements aimed at improving the coordination of Medicare and Medicaid (see Glossary). Those arrangements often rely on managed care plans to coordinate Medicare and Medicaid. Such coordination is especially relevant for full-benefit dual-eligible individuals who use both Medicare- and Medicaid-covered services. Coordination needs are fewer for partial-benefit dual-eligible individuals but some may exist where Medicaid pays Medicare cost sharing.

This issue brief describes how state Medicaid programs are implementing arrangements aimed at coordinating Medicare and Medicaid for dual-eligible individuals. We use data from the 22nd annual budget survey of Medicaid officials in all 50 states and the District of Columbia conducted by KFF and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD). The District of Columbia is counted as a state for the purposes of this report. Given differences in the financing structure of their programs, the U.S. territories were not included in this analysis. We supplement the survey findings with administrative data from the Centers for Medicare and Medicaid Services (CMS). We find that nearly all states are leveraging strategies to coordinate care for dual-eligible individuals and many states are using multiple strategies. In 2022:

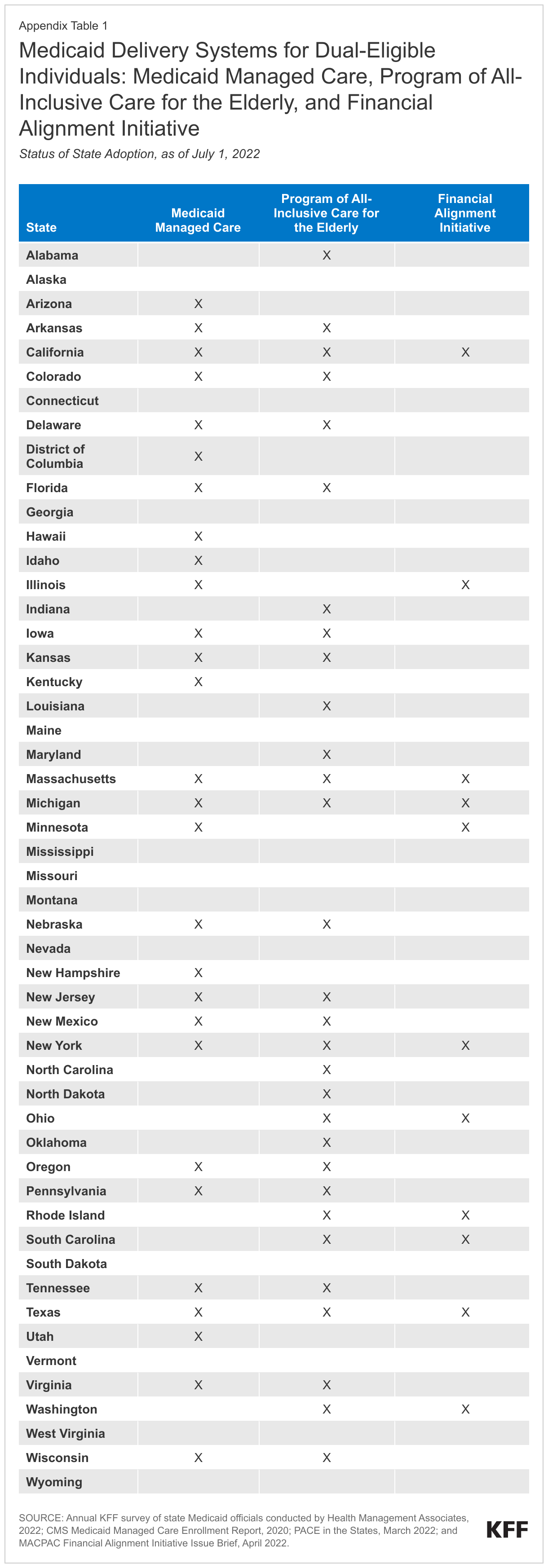

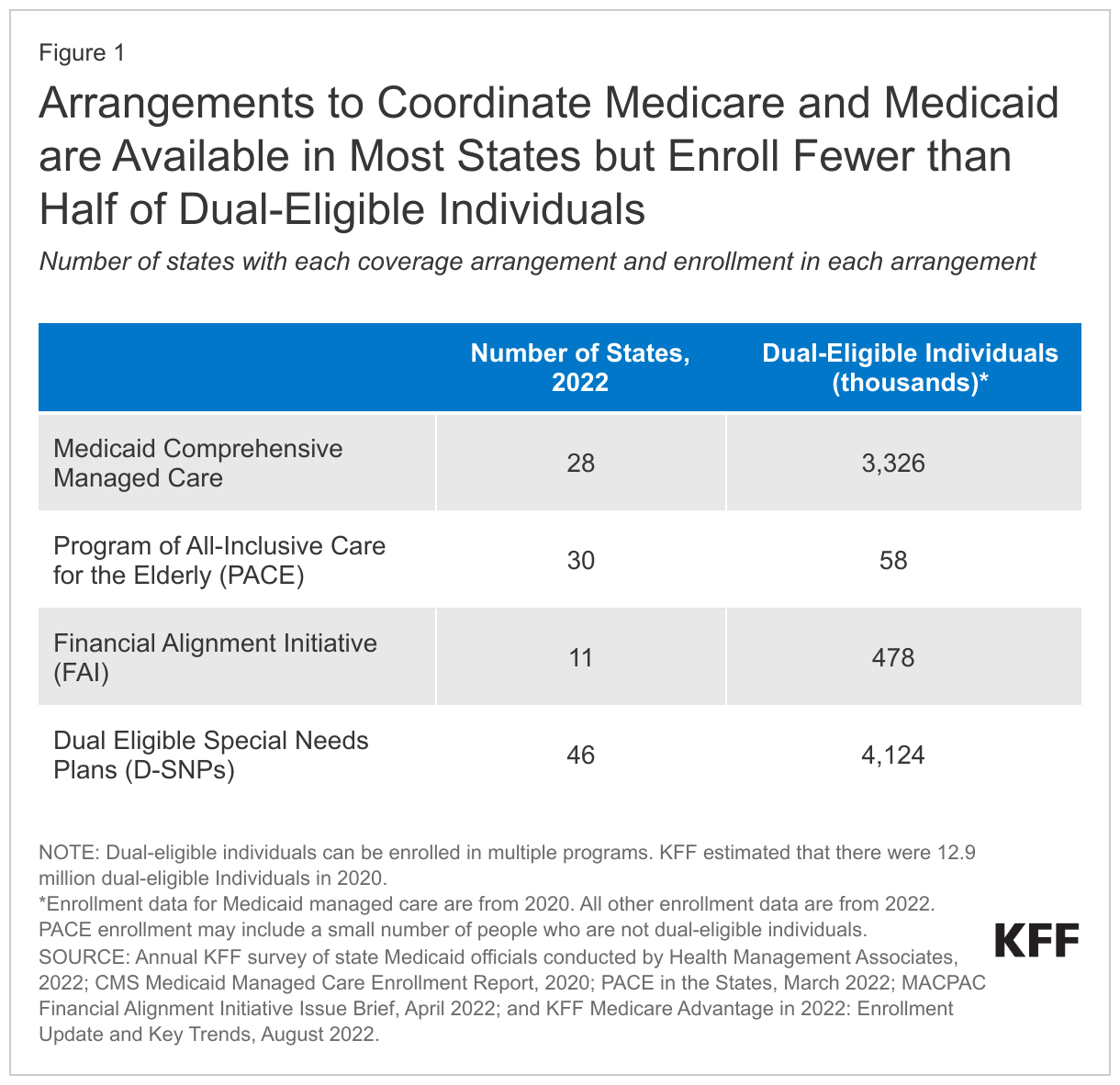

- 28 states use Medicaid managed care to cover some or all benefits for dual-eligible individuals. In Medicaid managed care, enrollees receive services through a health plan that is operated by either a private company or a local authority. States may include requirements for the plans to coordinate with Medicare. Such requirements could include paying Medicare cost sharing or providing a case manager to coordinate care. Dual-eligible individuals who are enrolled in Medicaid managed care can be enrolled in traditional Medicare or a private Medicare plan (e.g., Medicare Advantage).

- 30 states had Programs of All-Inclusive Care for the Elderly (PACE) available. PACE is a program that provides comprehensive medical and social services to individuals who are: (1) 55 years of age or older, (2) need a nursing home level of care but are able to live safely in the community, and (3) live in a PACE organization service area. Most enrollees are dual-eligible individuals, but Medicare beneficiaries who are not eligible for Medicaid may pay a monthly premium to enroll. Although PACE is only available in limited service areas, evaluations have shown favorable outcomes for participants.

- 9 states participated in the Financial Alignment Initiative (FAI) to coordinate care for dual-eligible individuals. The Financial Alignment Initiative is an initiative in which the Centers for Medicare and Medicaid Services (CMS) partners with states to test new models for their effectiveness in improving care for dual-eligible individuals and better aligning the financial incentives of Medicare and Medicaid. Most, but not all, the states that participated in the Initiative did so by offering Medicare and Medicaid benefits jointly in a single health plan. Such “Medicare-Medicaid Plans” have a 3-way contract between the state, federal government, and health plan. CMS recently announced its intent to end the Medicare-Medicaid plan model by the end of December 2025 and to transition those plans into D-SNPs. Evaluations of the Financial Alignment Initiative show mixed results in terms of spending, enrollment, and beneficiary experience across states.

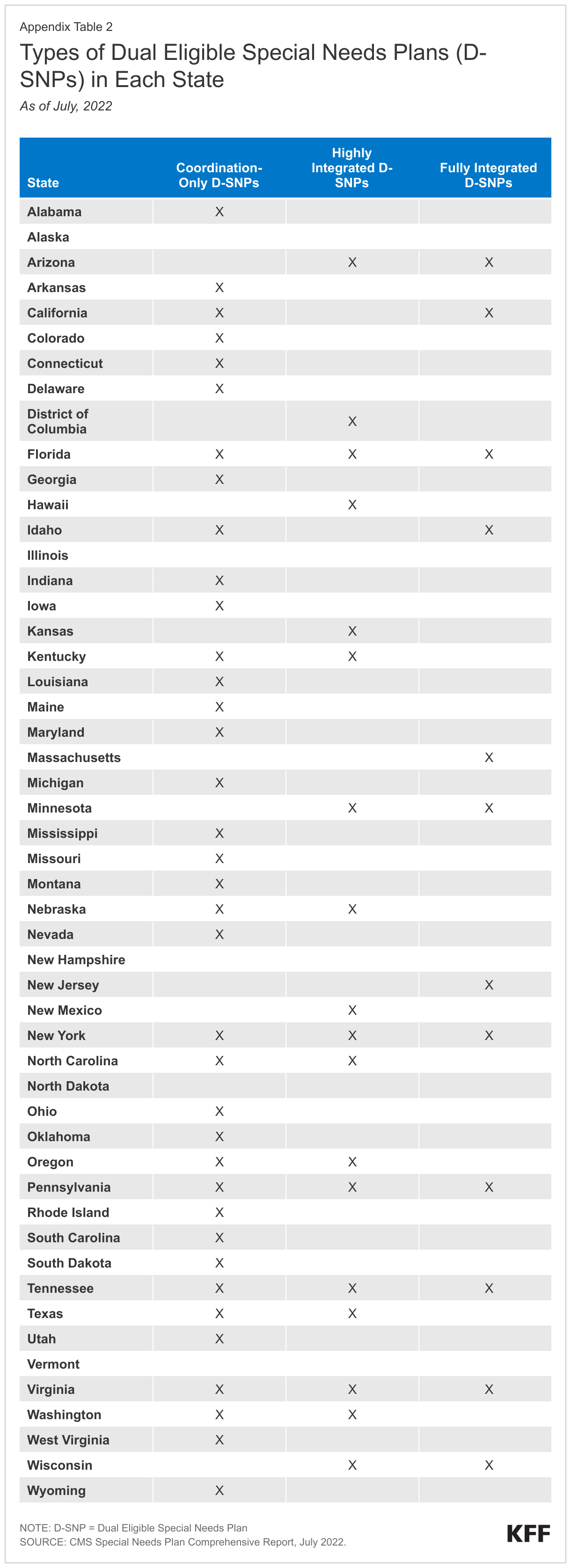

- 29 states leveraged their contracts with dual eligible special needs plans (D-SNPs) to require enhanced coordination between Medicaid and the D-SNP providing Medicare benefits. D-SNPs are Medicare Advantage plans that specialize in providing coverage for dual-eligible individuals. There are three types of D-SNPs:

- Coordination-Only D-SNPs provide Medicare-covered services and are required to coordinate the delivery of benefits with the Medicaid program, contract with state Medicaid programs, and notify states when enrollees are admitted to inpatient facilities.

- Highly Integrated D-SNPs must meet the requirements of coordination-only D-SNPs and must also have a Medicaid plan operating in the same counties as the D-SNP. The parent organization provides both Medicare and Medicaid services, but there is no requirement that people enroll in both plans.

- Fully Integrated D-SNPs must meet the requirements of coordination-only D-SNPs and must also offer an aligned Medicaid plan that integrates the Medicare and Medicaid benefits. Medicare pays the plan for Medicare-covered services and Medicaid pays the plan for Medicaid-covered services. Currently, dual-eligible beneficiaries may enroll in the D-SNP without also enrolling in the Medicaid-plan. Similarly, there may be Medicaid enrollees with coverage through the aligned Medicaid plan who are not also enrolled in the D-SNP. Starting in 2025, enrollment in fully integrated D-SNPs will be limited to those who are enrolled in both the Medicare and Medicaid plans.

How do Coverage Arrangements for Dual-Eligible Individuals Vary Across States?

State Medicaid programs may deliver services on a fee-for-service basis in which states reimburse health care providers a fee for each service or through managed care plans, which provide Medicaid benefits to enrollees and receive a per member monthly payment for such services. States have increased their reliance on managed care delivery systems to help improve access and outcomes, enhance care management and coordination, and better control costs. For dual-eligible individuals, Medicaid managed care plans may provide coverage of services that Medicare does not cover (long-term services and supports and non-emergency transportation for example) or may pay enrollees’ required cost sharing for Medicare-covered services. Medicaid managed care plans may be “comprehensive,” which means that they cover most or all Medicaid benefits, or they may be “non-comprehensive,” which means that they only cover a specific subset of Medicaid benefits such as behavioral health or non-emergency medical transportation.

In 2022, 28 states enrolled dual-eligible individuals in comprehensive managed care and in 2020 (the most recent year for which data were available), an estimated 3 million people were enrolled (Figure 1). Enrollment in Medicaid managed care may be mandatory or voluntary for dual-eligible individuals and the enrollment process often varies within states by county or eligibility group. States with voluntary managed care enrollment may adopt “passive enrollment” in which enrollees are assigned to a managed care plan with the opportunity to opt-out or switch to another plan.

Other coverage arrangements provide Medicaid benefits through a single plan that integrates the Medicare and Medicaid benefits, although fewer dual-eligible individuals are enrolled in such programs. Those options include the Financial Alignment Initiative, which was available in 9 states, and PACE, which was available in 30 states in 2022. Total enrollment in these programs is just over 500,000.

Medicaid may also coordinate care for dual-eligible individuals by contracting with dual eligible special needs plans (D-SNPs), private Medicare Advantage plans that exclusively enroll beneficiaries with Medicaid. D-SNPs aim to better coordinate benefits and care covered under the two programs. In 2022, D-SNPs were available in 46 states and 4.1 million dual-eligible individuals were enrolled (Figure 1). D-SNPs may be paired with affiliated Medicaid managed care or managed long-term services and supports plans.

How are States Using Medicaid Managed Care to Coordinate Care for Dual-Eligible Individuals?

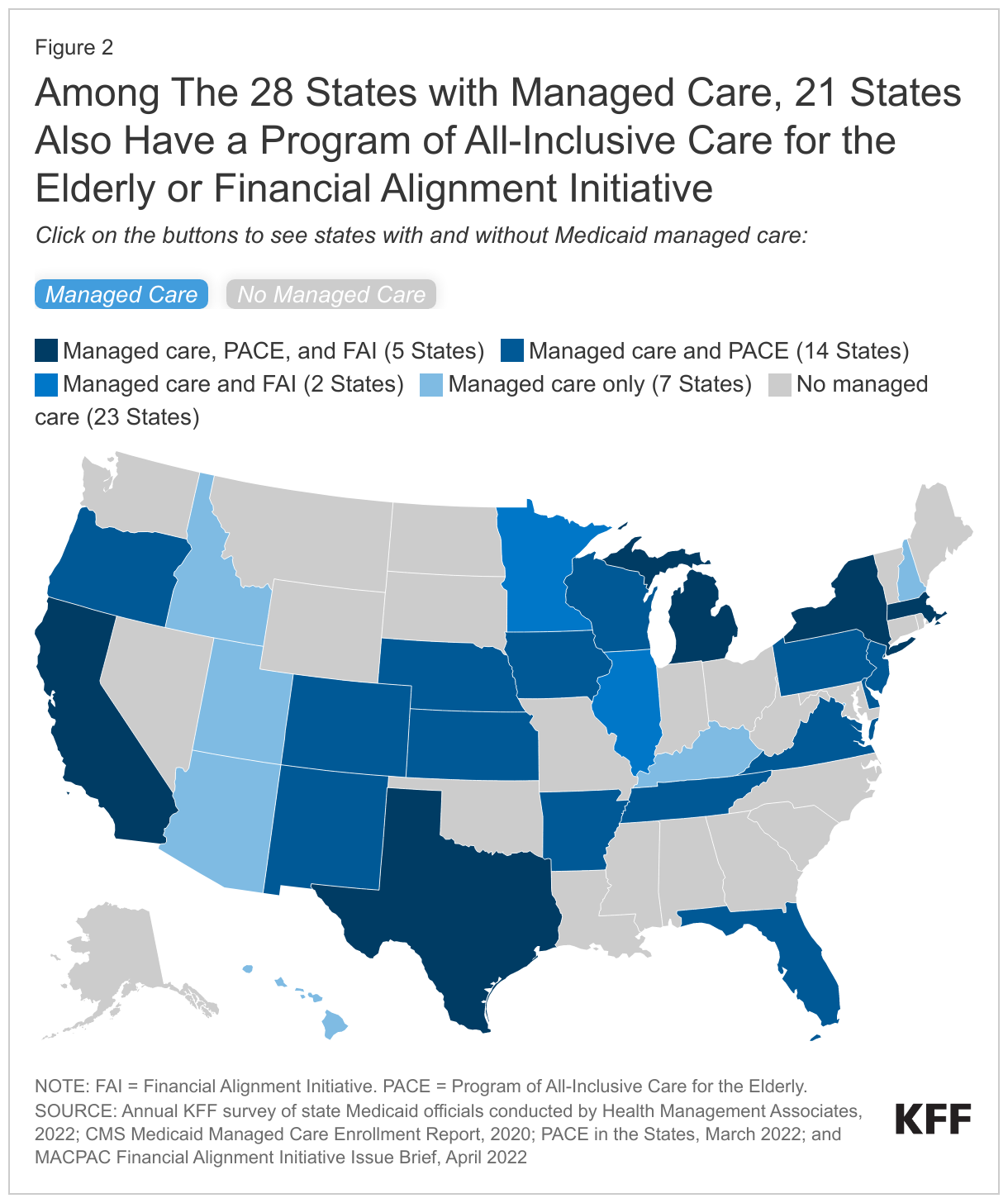

Over half of states (28) use Medicaid comprehensive managed care to deliver Medicaid benefits to dual-eligible individuals (Figure 2, Managed care tab). Among those states, 7 states only had managed care, 14 states had managed care and PACE, 2 states had managed care and a Financial Alignment Initiative, and 5 states had managed care, PACE, and a Financial Alignment Initiative (Appendix Table 1). Among the states with comprehensive Medicaid managed care and the Financial Alignment Initiative, all used private plans to implement the Financial Alignment Initiative. Although many states have more than one Medicaid coverage arrangement in place, those arrangements are often not available statewide. States may choose to make Medicaid managed care and the Financial Alignment Initiative statewide or to limit them to certain counties. PACE is only available in specific “service areas,” which are defined by counties or zip codes and agreed to by the PACE provider, the state, and CMS.

The remaining 23 states do not use comprehensive managed care to cover dual-eligible individuals but may coordinate care using other strategies (Figure 2, No managed care tab). Among states without comprehensive managed care, 7 states had PACE and 4 states had both PACE and a Financial Alignment Initiative. The remaining states did not have PACE or a Financial Alignment Initiative. Among the 7 states without comprehensive managed care that had a Financial Alignment Initiative, all but Washington used private plans to implement the Initiative. Washington uses a managed fee-for-service model where health homes receive payments from the Medicaid agency to coordinate care for dual-eligible individuals. (Health homes are organizations such as community-based organizations or managed care organizations that contract with care coordination organizations to provide comprehensive care management, care coordination, health promotion, transitional care, individual and family support, and referral to community and social support services to participants.)

How are States Leveraging their Contracts with D-SNPs to Coordinate Care for Dual-Eligible Individuals?

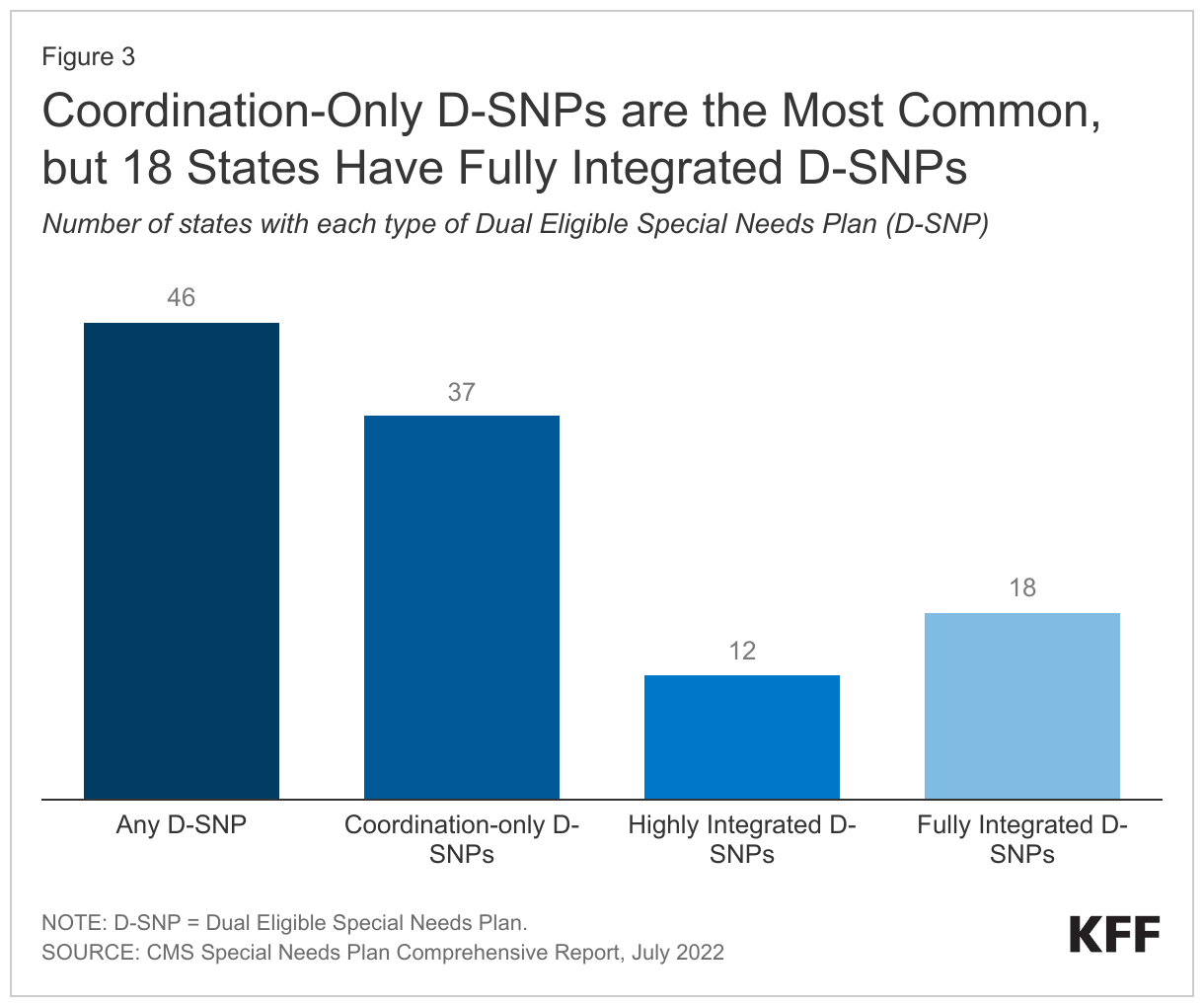

D-SNPs are available in almost all states, but D-SNPs with lower levels of federally-required integration are much more widely available than those with higher levels of integration (Figure 3). Medicare Advantage insurers that would like to offer D-SNPs must have a contract with each state in which they intend to offer coverage, in addition to having a contract with the federal government for providing Medicare-covered services. Federal regulations describe minimum contract elements, which differ across the three categories of D-SNPs and change from year-to-year. There are more required contract elements for D-SNPs with higher levels of integration. Of the 46 states offering a D-SNP (Appendix Table 2), 37 offer coordination-only D-SNPs, which have the fewest requirements for integrating Medicare and Medicaid. There are 12 states with highly integrated D-SNPs and 18 states with fully integrated D-SNPs. Roughly a third of states with D-SNPs have more than one type available (16).

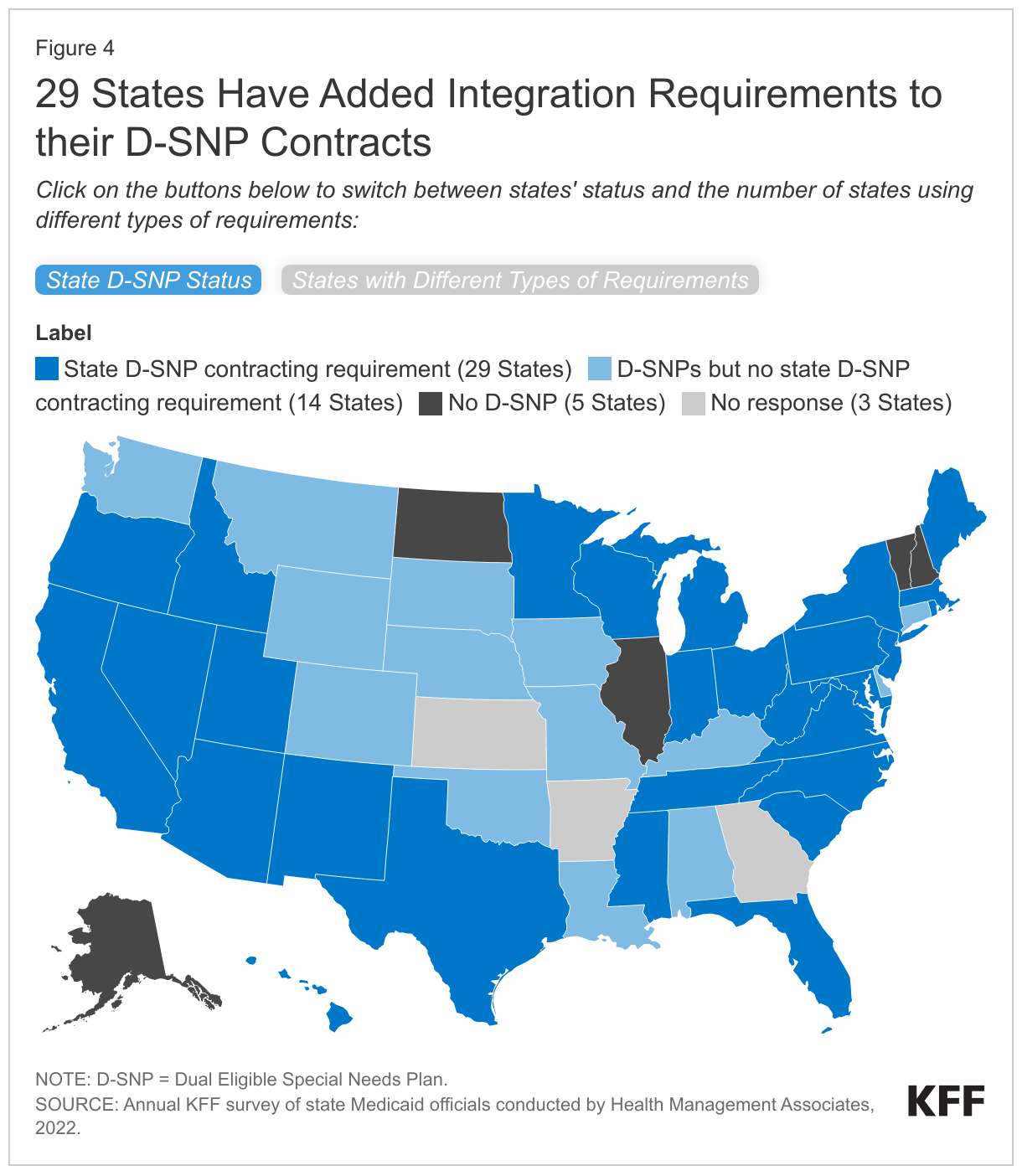

States are able to include additional requirements for D-SNPs in their contracts to enhance the integration between Medicare and Medicaid and 29 states reported doing so (Figure 4, States with Different Types of Requirements tab). In the survey, states reported whether they included several elements in their contracts with D-SNPs that were designed to increase Medicare and Medicaid integration. For the 16 states with multiple types of D-SNPs, it is unknown whether the contract requirements apply to all D-SNPs within the state or only to the most integrated type of D-SNP. However, among the 29 states with additional requirements for D-SNPs, over half (16) do not have any contracts with fully integrated D-SNPs.

- 17 states reported requirements related to coverage of supplemental benefits under either Medicare or Medicaid (Figure 4, States with Different Types of Requirements tab). As with other Medicare Advantage plans, D-SNPs may offer supplemental benefits beyond what is covered by traditional Medicare. Some of those benefits such as non-emergency medical transportation or dental care may overlap with Medicaid benefits. To avoid duplicative coverage, 9 states reported requiring the D-SNP to provide supplemental Medicare benefits that complement (rather than duplicate) the benefits dual-eligible individuals receive through Medicaid. (The benefits would be provided under the Medicare supplemental benefit package).

Other states reported requiring D-SNPs to offer Medicaid managed care plans that included coverage of either long-term services and supports (8 states) or behavioral health services (9 states) (Medicaid pays the costs of Medicaid-covered benefits). Long-term services and supports and behavioral health are the largest components of Medicaid spending for dual-eligible individuals and are services that often require significant coordination with Medicare-covered services. Requiring D-SNPs to offer a Medicaid plan that covers those benefits ensures that the same parent organization is familiar with the major set of services used by dual-eligible individuals.

- 15 states reported administrative integration requirements including integrating the member materials or the grievance and appeals system (13 states each). Integrated member materials provide information to dual-eligible individuals about all Medicare and Medicaid benefits and applicable cost sharing in unified documents (such as a combined summary of benefits and single enrollee handbook). Without the unified documents, dual-eligible individuals receive separate materials for Medicare and Medicaid and need to find the relevant information in both to determine what is covered under the two plans combined. Unifying the grievance and appeals system means that if enrollees want to file a complaint or request reconsideration of denied services, they can do so once for the plan, rather than doing so separately for their Medicare and Medicaid coverage.

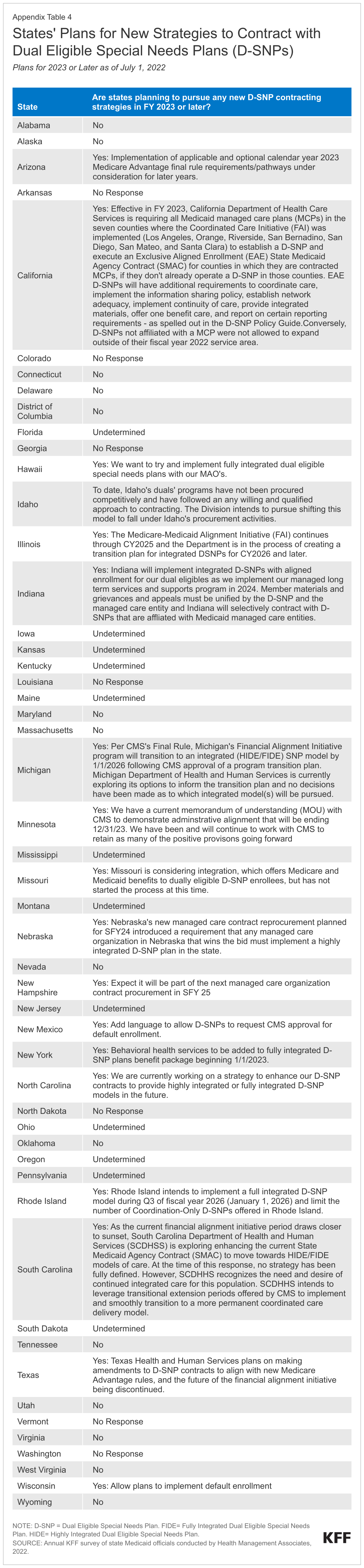

In addition, 12 states reported other types of requirements beyond those that multiple states are implementing (Appendix Table 3) and 18 states reported pursuing new strategies in FY 2023 or beyond (Appendix Table 4). Future changes include contracting with D-SNPs that have a higher level of integration than their current D-SNPs, enhancing integration requirements among existing D-SNPs, and making changes that would facilitate compliance with the final rule, Medicare Program; Contract Year 2023 Policy and Technical Changes to the Medicare Advantage and Medicare Prescription Drug Programs. That rule makes several changes to D-SNPs that will take effect between 2023 and 2025.

Looking ahead

Although coverage arrangements aimed at integrating Medicare and Medicaid are available in most states, fewer than one million dual-eligible individuals are estimated to be enrolled in either a fully-integrated D-SNP or Medicare-Medicaid Plan. Policymakers at the federal and state levels are discussing ideas to increase coordination between Medicare and Medicaid. A bipartisan group of Senators led by Bill Cassidy (R-LA) -- and including Tom Carper (D-DE), John Cornyn (R-TX), Bob Menendez (D-NJ), Tim Scott (R-SC), and Mark Warner (D-VA) – recently solicited feedback from health care providers and patient communities about improving care for dual-eligible beneficiaries.

Responses to the request for information note the problems that arise from the current Medicare and Medicaid systems, which include fragmented care and poorer health outcomes for dual-eligible individuals, higher health spending, and the incentives for health care providers and states to shift costs to the Medicare program. Several responses to the request for information—including those by the Medicare Payment and Access Commission—recommend strengthening integration requirements for D-SNPs. Those recommendations reflect the fact that there is already significant and growing enrollment in D-SNPs, whereas other types of integrated delivery systems (such as PACE) have been characterized by limited participation. However, the level of integration achieved by D-SNPs is highly varied and over half of the states with D-SNPs only have plans with the lowest level of integration. Other responses —such as one by the Medicaid and CHIP Payment and Access Commission—highlight the value of maintaining state flexibility when creating federal programs and recognizing the variation in how states are currently integrating care for dual-eligible individuals.

The tension between retaining state flexibility and ensuring that more highly integrated arrangements are available in all states is one of many challenges of developing new approaches to coordinating care. Other challenges include the heterogeneity of dual-eligible individuals, their need for varied but often quite complex or costly health and social services, and differing financing streams from which these programs are funded.

Glossary: Coverage Models for Dual-Eligible Individuals

Medicaid Managed Care covers some or all Medicaid benefits through a health plan that is operated by either a private company or a local authority. States may include requirements for the plans to coordinate with Medicare. Such requirements could include paying Medicare cost sharing or providing a case manager to coordinate care. Dual-eligible individuals who are enrolled in Medicaid managed care can be enrolled in traditional Medicare or a private Medicare plan (e.g., Medicare Advantage).

The Program of All-Inclusive Care for the Elderly (PACE) is a program that provides comprehensive medical and social services to individuals who are: (1) 55 years of age or older, (2) need a nursing home level of care but are able to live safely in the community, and (3) live in a PACE organization service area. Most enrollees are dual-eligible individuals, but Medicare beneficiaries who are not eligible for Medicaid may pay a monthly premium to enroll. Although PACE is only available in limited service areas, evaluations have shown favorable outcomes for participants.

The Financial Alignment Initiative is an initiative in which the Centers for Medicare and Medicaid Services (CMS) partners with states to test new models for their effectiveness in improving care for dual-eligible individuals and better aligning the financial incentives of Medicare and Medicaid. Most, but not all of the states that participated in the Initiative, did so by offering Medicare and Medicaid benefits jointly in a single health plan. Such “Medicare-Medicaid Plans” have a 3-way contract between the state, federal government, and health plan. CMS recently announced its intent to end the Medicare-Medicaid plan model by the end of December 2025 and to transition those plans into D-SNPs. Evaluations of the Financial Alignment Initiative show mixed results in terms of spending, enrollment, and beneficiary experience across states.

Dual Eligible Special Needs Plans (D-SNPs) are Medicare Advantage plans that specialize in providing coverage for dual-eligible individuals. There are three types of D-SNPs:

- Coordination-Only D-SNPs provide Medicare-covered services and are required to coordinate the delivery of benefits with the Medicaid program, contract with state Medicaid programs, and notify states when enrollees are admitted to inpatient facilities.

- Highly Integrated D-SNPs must meet the requirements of coordination-only D-SNPs and must also have a Medicaid plan operating in the same counties as the D-SNP. The parent organization provides both Medicare and Medicaid services, but there is no requirement that the same people enroll in both plans.

- Fully Integrated D-SNPs must meet the requirements of coordination-only D-SNPs and must also offer an aligned Medicaid plan that integrates the Medicare and Medicaid benefits. Medicare pays the plan for Medicare-covered services and Medicaid pays the plan for Medicaid-covered services. Currently, dual-eligible beneficiaries may enroll in the D-SNP without also enrolling in the Medicaid-plan. Similarly, there may be Medicaid enrollees with coverage through the aligned Medicaid plan who are not also enrolled in the D-SNP. Starting in 2025, enrollment in fully integrated D-SNPs will be limited to those who are enrolled in both the Medicare and Medicaid plans.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

This brief draws on work done under contract with Health Management Associates (HMA) consultants Kathleen Gifford, Aimee Lashbrook, Mike Nardone, and Matt Wimmer.

Appendix Tables