Some Can Get Marketplace Plans With No Premiums,Though With Higher Deductibles and Cost-Sharing

Many low-income consumers who are eligible for federal financial help under the Affordable Care Act can get a bronze-level plan and pay nothing out-of-pocket in premiums in more than 2,000 counties next year, depending on their annual income, according to a new analysis from KFF (the Kaiser Family Foundation). Such plans come with higher deductibles and out-of-pocket maximums, however.

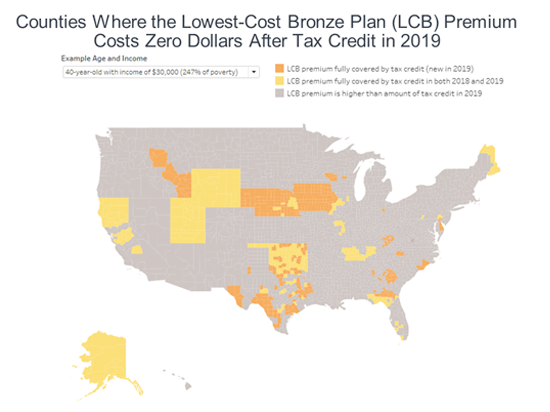

The analysis finds that the ACA’s premium tax credits would cover the full premium of the lowest-cost bronze marketplace plan in 2,532 counties in 2019 for a 40-year-old with an annual income of $20,000. Going up the income ladder, the figure is 2,014 counties for a 40-year-old making $25,000; 659 counties for a person the same age who makes $30,000; 417 counties for someone making $35,000; and 120 counties for a 40-year-old making $40,000.

The analysis examines how ACA marketplace premiums are changing in 2019. It features interactive maps with county-level data illustrating changes in premiums for the lowest-cost bronze, silver and gold plans in counties across the U.S.

Nationally, the average unsubsidized premium for the lowest-cost bronze plan is decreasing by 0.3 percent in 2019. Unsubsidized premiums for the lowest-cost silver and gold plans are falling by one percent and two percent, on average, respectively. Costs often will be even lower for consumers who receive premium tax credits, although these tax credits will be smaller than in 2018 for many consumers.

The availability of bronze plans for no or low premiums is in large part the result of insurers increasing silver premiums following the termination cost-sharing payments to insurers by the Trump administration in late 2017. Insurers are still required to provide reduced cost-sharing to low-income consumers in silver plans, and those eligible for those reductions should shop around and consider their options carefully as bronze plans come with high deductibles. For example, a single individual making between 100-200% of the poverty level can qualify for a silver plan with an out-of-pocket maximum of no more than $2,600, and the deductible would likely be much lower than that. For a bronze plan, the out-of-pocket maximum and deductible could be upwards to $7,900. Zero- or low-premium plans may not be cheaper overall if the enrollee is sick or has high health spending.

Also available is KFF’s Health Insurance Marketplace Calculator, which allows users to enter their income, age, and family size and get estimates of premiums and available subsidies for insurance purchased on the ACA exchanges.

Filling the need for trusted information on national health issues, the Kaiser Family Foundation is a nonprofit organization based in San Francisco, California.