Is The U.S. Stepping Up In The Fight Against Ebola?

Editorial Note: Originally published on May 21, this Policy Watch was updated on May 23 to incorporate additional information and developments.

The recently announced Ebola outbreak in the Democratic Republic of the Congo (DRC), which is quickly escalating in the region, emerges at a time when the larger fiscal and programmatic environment for global health efforts faces particular hurdles, and international cooperation has been significantly challenged. This is in large part due to policy decisions made by the Trump administration and presents the first real global outbreak test following those changes.

On May 15, news broke of a large, ongoing Ebola outbreak concentrated in northeastern DRC. Two days later, the Director-General of the World Health Organization (WHO) declared the outbreak to be a “public health emergency of international concern” (PHEIC) given its size and because Ebola cases were already reported across the border in Uganda, making the outbreak a regional threat. Despite only recently being detected and reported, this already appears to be one of the largest Ebola outbreaks to date, with almost 746 suspected cases and over 176 suspected deaths as of May 21st.

National and international health authorities have recent experience responding to Ebola outbreaks, such as in West Africa in 2014-2015 (the largest since the virus was discovered in 1976) and in DRC between 2018 and 2020. However, this outbreak presents particular challenges. These include:

- First, the species of Ebola virus circulating in the current outbreak is different from that which caused most prior major outbreaks, which means countermeasures such vaccines and treatments are not available, and even testing for this species can only be done at more specialized labs currently.

- Second, the outbreak is happening in a geographic area with ongoing insecurity, multiple concurrent humanitarian crises, high population mobility, and limited access to health services. These factors played a role in the delayed identification of the outbreak and pose difficulties for the response.

- Third, the international environment of health cooperation and financial support has changed significantly since the last big outbreak, driven in large part by the U.S. withdrawal from WHO and international cooperation more broadly as well as its reductions in foreign aid and health programming, but also by larger financial constraints due to aid cuts by other donors.

Even so, the public health effort has already started to ramp up, with DRC and Ugandan health authorities leading responses in their respective countries, supported by WHO, United Nations humanitarian agencies, the Africa CDC, and a network of other local, regional, and international non-governmental organizations.

For its part, the U.S. government has reported that it has already taken a number of steps in response to the outbreak, including:

- Providing some financial support to national Ebola responses in DRC and Uganda. Within two days of learning of the outbreak, the State Department announced it had mobilized $23 million in emergency funding to support DRC and Ugandan government health responses. The State Department also announced it would direct U.S. humanitarian funding to assist with the broader humanitarian response in these countries. By comparison, this initial funding amount is larger than the $8 million the U.S. provided through USAID in the weeks following the identification of the 2018 Ebola outbreak in Equateur province in DRC, though the 2026 outbreak is already much larger and affects a wider geographic area. It is unclear at this point how much funding will ultimately be necessary for the current Ebola response, with authorities still trying to understand the true scope of the outbreak and community needs. The State Department expects the U.S. will increase its financial support for the current outbreak response over time. Over the course of the series of DRC Ebola outbreaks from 2018-2020, which ultimately caused over 2,300 deaths, USAID contributed $324 million, and CDC $37 million, to country response efforts, with these funds drawn entirely from prior emergency Ebola appropriations provided by Congress during the 2014-2015 West Africa Ebola epidemic.

- Activating CDC emergency operations and mobilizing CDC staff and resources. CDC held a press conference within two days of the outbreak announcement, reporting that the agency has begun to assist DRC and Ugandan officials and connect with other partners via CDC offices in each country. CDC and State Department have begun supporting partner organizations in procuring and deploying needed supplies, such as personal protective equipment (PPE). CDC says it has a “long-standing” team of 30 staff in its DRC country office (primarily located in the capital, Kinshasa, which is hundreds of miles from the affected areas in northeastern DRC) and about 100 in Uganda, with more expected to be mobilized in the coming days, including experts from Atlanta who will travel to the affected countries. According to reports, CDC is taking the lead role for the U.S. government in the Ebola response in affected countries. For some context, during the response to Ebola outbreaks in DRC that began in 2018 and eventually grew to thousands of cases, CDC had 187 staff members complete 278 deployments through June 2019.

- Committing to help stand up Ebola isolation and treatment units. In a May 19 announcement, the State Department says it will be financing the deployment of “up to 50” Ebola Treatment Units and “associated frontline costs” to assist further with the response. These units will provide emergency Ebola screening, triage, and isolation capacity in affected areas. According to the State Department, the U.S. funding will be delivered via “pooled funding vehicles administered by the United Nations Office for the Coordination of Humanitarian Affairs (OCHA).”

- Deploying a Disaster Assistance Response Team (DART) to the region. The State Department reports it will be deploying a DART to DRC, which is a mechanism meant to align and coordinate resources from various U.S. agencies under a single organizational structure. The State Department expects the DRC DART will allow CDC, State, and other U.S. agencies to be located together, fostering unified communications with host country governments and other partners.

- Investigating potential monoclonal antibody treatments. According to a spokesperson for the Department of Health and Human Services (HHS), the Biomedical Advanced Research and Development Authority (BARDA) is working with a biotechnology company to make available an experimental Ebola treatment based on monoclonal antibodies for potential use in high-risk individuals. It is unclear how much may be made available and under what circumstances the treatment may be used.

Still, given all of the changes made by the U.S. to its foreign assistance and global health response, U.S. support is taking shape under very different circumstances and through different organizational mechanisms compared to past Ebola responses. For example:

- The absence of USAID. USAID supported Ebola prevention and detection activities in DRC, Uganda, and elsewhere for many years, employing dozens of staff members with outbreak surveillance and response expertise. However, much of that expertise and the underlying network of organizations was lost when USAID was dissolved and almost all its staff was fired last year. Historically, USAID was the lead agency representing the U.S. government during major Ebola response and was home to interagency DARTs. Now, the newly created State Department Bureau of Global Health Security and Diplomacy (GHSD) and State’s Bureau of Disaster and Humanitarian Response (DHR) are responsible for overseeing diplomatic and coordinating with CDC on technical aspects of an Ebola response for the first time, including through the newly announced DART, despite having fewer personnel than USAID had and limited prior experience overseeing an operational response. Ultimately, staffing for the U.S. response could be scaled up over time, as it was during prior outbreaks, such as during the 2014-2015 West Africa Ebola response, which ultimately consisted of a large U.S. government interagency presence that included the deployment of thousands of U.S. military personnel, hundreds of CDC and HHS staff, and representatives from other agencies.

- Ongoing effects of foreign assistance funding freeze and cuts. Alongside the dissolution of USAID, in early 2025 the Trump administration implemented a freeze on all foreign assistance funding for a period last year. As a consequence, partner organizations report that they had to fire staff and cease many disease prevention and detection activities, including Ebola-focused activities in Uganda and DRC. . Eventually, the State Department issued “waivers” to allow funding for existing “life-saving” assistance programs to continue, which included infectious disease outbreak detection and response programs. While certain activities resumed, the underlying system itself was affected.

- Withdrawal of U.S. membership in WHO. During past response to major Ebola outbreaks, WHO played important coordinating and financing roles, and is poised to serve a leading role in bringing international resources to bear in DRC and Uganda. WHO has already mobilized almost $4 million funding from its Contingency Fund for Emergencies (CFE), the mechanism created after the 2014-2015 West Africa Ebola outbreak to rapidly channel donor funding to support public health emergency response efforts. In the past, the U.S. had always been a major supporter of WHO’s responses and the CFE, including as one of the largest donors to the CFE, and to the multilateral Ebola response, during the 2018-2020 DRC Ebola outbreaks. However, given the U.S. withdrawal from WHO and more limited formal communications between U.S. government officials and WHO officials, the U.S. does has not indicated an interest in directly supporting a WHO-led response this time, a departure from past practices. With just $5.4 million in total donor contributions to the fund in 2026, CFE is already close to being exhausted, with other donors so far unable to fill the funding gaps left by the U.S. absence. While some formal communications between the U.S. and WHO have been limited, CDC has explicit permission to coordinate as necessary with international organizations involved in the response on the ground, including staff from WHO.

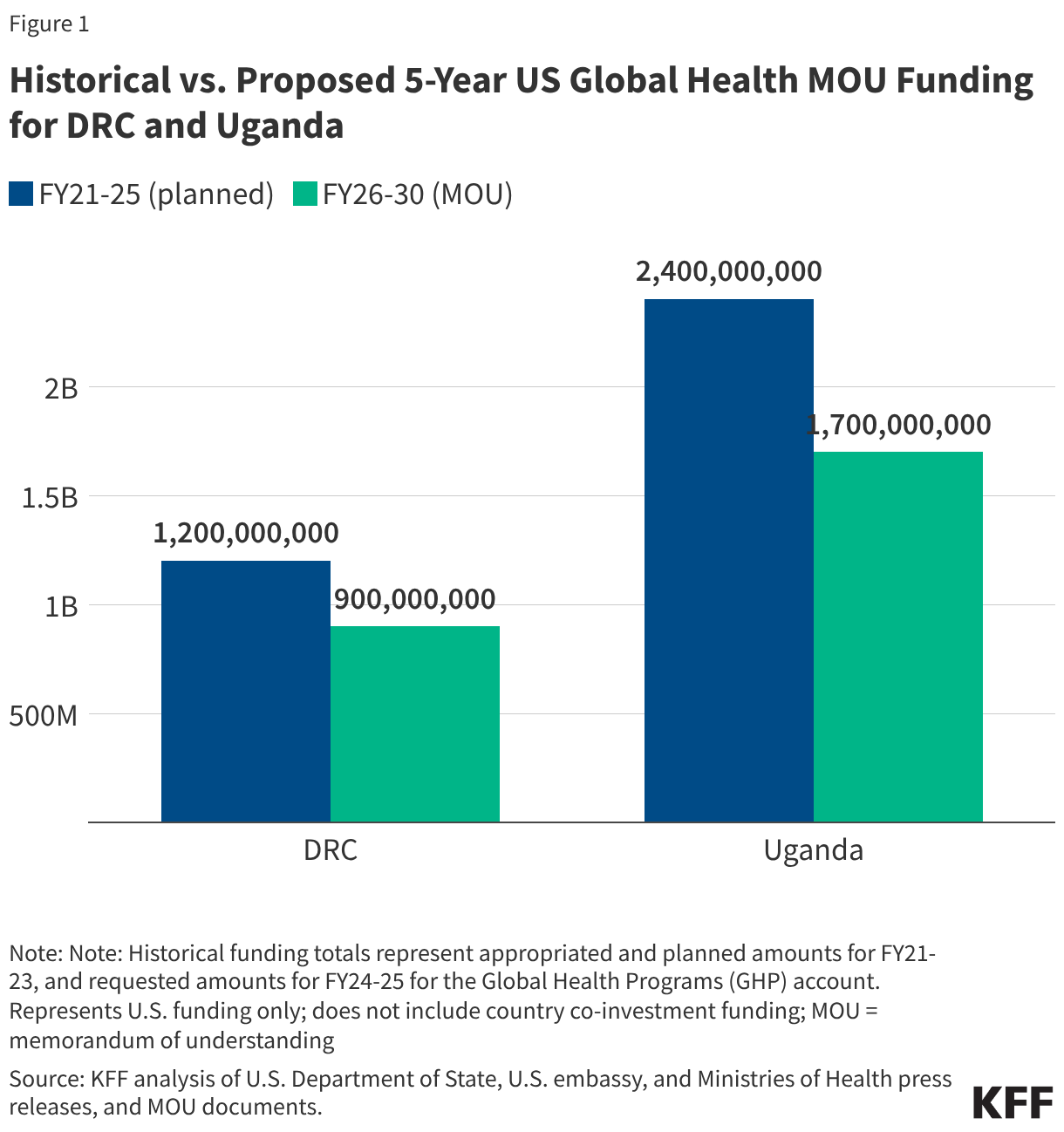

- Reduced funding for global health in new U.S. agreements with DRC and Uganda. As referenced above, the dissolution of USAID and the foreign assistance funding freeze last year created de facto cuts to global health assistance in the Ebola-affected countries, affecting country programs. U.S. pledges of assistance over the next few years do represent a cut in funding compared to previous years. The new U.S. approach to global health assistance relies on negotiating country-specific agreements (memoranda of understanding, or MOUs), and such agreements have already been reached with Uganda (signed December 2025) and DRC (signed February 2026). However, the amount of funding pledged by the U.S. for the next 5 years represents a 27% cut compared to that provided over the past five years (see Figure). The MOUs also outline priorities for the US and the partner countries for global health assistance, with disease surveillance and response being a key aspect for both the DRC and Uganda agreements. For example, the MOU with Uganda states the U.S. wishes to “advance its bilateral relationship with the Government of Uganda and prevent the spread of emerging and existing infectious disease threats globally”, and outlines the funding amounts the U.S. intends to provide the country each year to advance these priorities. However, it is not exactly clear how this new mechanism will shape the programs and outcomes from U.S. global health funding in these priority areas going forward.

While these are still early days in a response that could last months (and facing an outbreak that appears to be escalating quickly), there are several key questions regarding the U.S. response going forward:

- If the needs on the ground increase significantly, will the Trump administration request additional emergency funding from Congress, as previous administrations have done? In addition to the United Nations OCHA funds the U.S. is tapping into, are there other, as of yet untapped existing resources that could be mobilized?

- If the outbreak worsens significantly, will the U.S. scale up its on the ground presence? Because the outbreak is occurring in an area with active conflict, direct deployment of CDC staff to affected areas in eastern DRC is unlikely, which is similar to the situation during the 2019 outbreaks of Ebola in DRC, where CDC provided support from afar but was not directly stationed in the field in affected areas. Could military personnel once again be called on to assist with the response, echoing the role they played in the 2014-2015 response?

- How far have U.S., WHO, and other disease response capacities been stretched now that officials are responding to two international emerging disease events in a short span – hantavirus and Ebola? And what might happen if yet another strain is placed on the already strained global response system?

- Will the Ebola outbreak and response affect other U.S. global health programs operating in the affected countries, and how might the U.S. government address any temporary interruptions or changes in services delivered through those programs?

Given its scale, the urgent messaging, and a rapid series of actions taken by national and international health authorities already, it appears that this Ebola outbreak will be a significant regional public health emergency ideally requiring a sustained, coordinated response. It also presents as the first real test of U.S. government commitment to supporting a major global outbreak response effort since the beginning of this administration, not unlike how hantavirus has been a test of sorts for U.S. domestic public health response to an emerging disease threat.