Children of Immigrants: Key Facts on Health Coverage and Care

Note: This brief was updated on April 10, 2025 to update state take-up of Medicaid and CHIP options for immigrant children.

Introduction

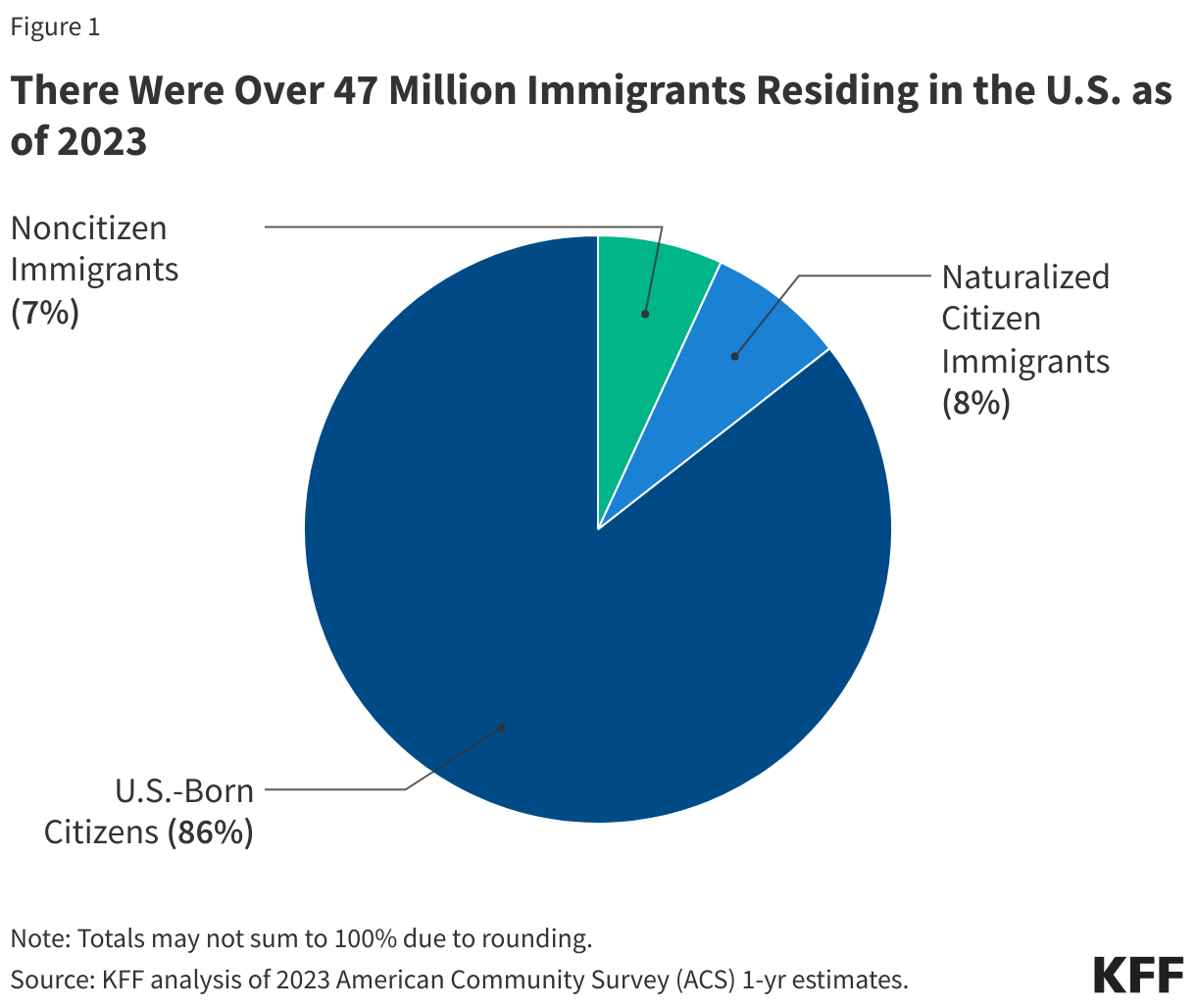

One in four children aged 18 and under living in the U.S. has at least one immigrant parent. Policies that may be implemented under the incoming Trump administration could have significant implications for these children, the vast majority of whom are citizens. These policies include potentially reinstating changes to public charge policy that were implemented during the first Trump administration, a proposal to end birthright citizenship for the children of some immigrants, and plans to carry out mass detention and deportations of immigrants, potentially including their citizen children and other family members. Birthright citizenship is a right guaranteed under the 14th amendment of the U.S. Constitution for children born in the U.S. regardless of their parents’ immigration status at the time of the child’s birth. Such actions could increase fears and confusion among children of immigrants and increase reluctance among parents to enroll them in programs for which they are eligible, including health coverage. They may also have long-term ramifications for the nation’s economy and workforce given the significant contributions immigrants and the adult children of immigrants make.

This brief provides key data on socioeconomic characteristics and health coverage among children (aged 18 and under) of immigrants based on KFF analysis of the 2023 American Community Survey 1-year Public Use Microdata Sample. It also examines potential implications of policies and actions that may be implemented by the incoming Trump administration. Key takeaways from the analysis include the following:

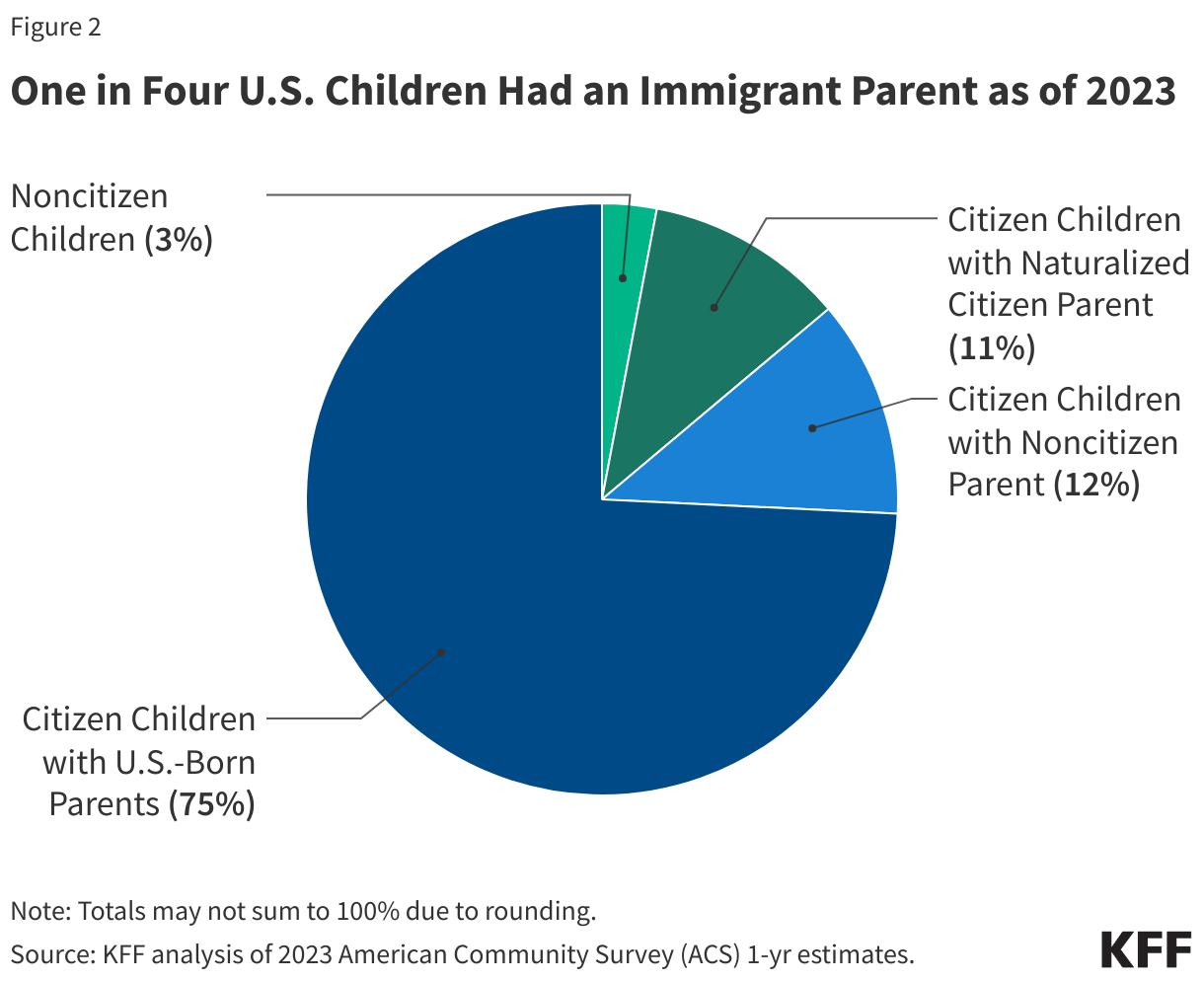

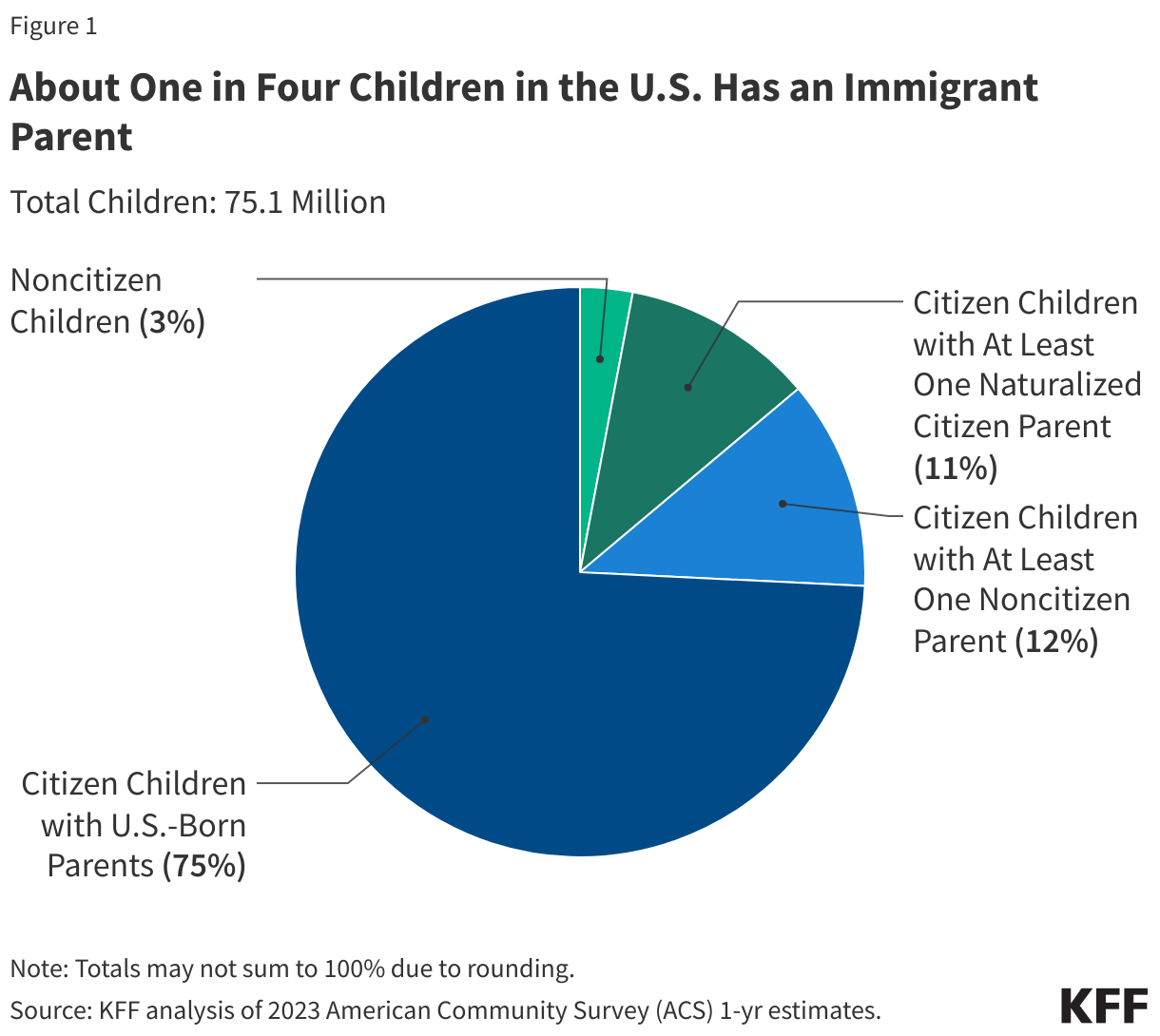

One in four children aged 18 and under in the U.S. has an immigrant parent, and the vast majority of these children are U.S. citizens. As of 2023, 19 million, or one in four, children in the U.S. had an immigrant parent. This includes one in ten (12%) who are citizen children with a noncitizen parent, a similar share (11%) who are citizen children with a naturalized citizen parent, and 3% who are noncitizen children.

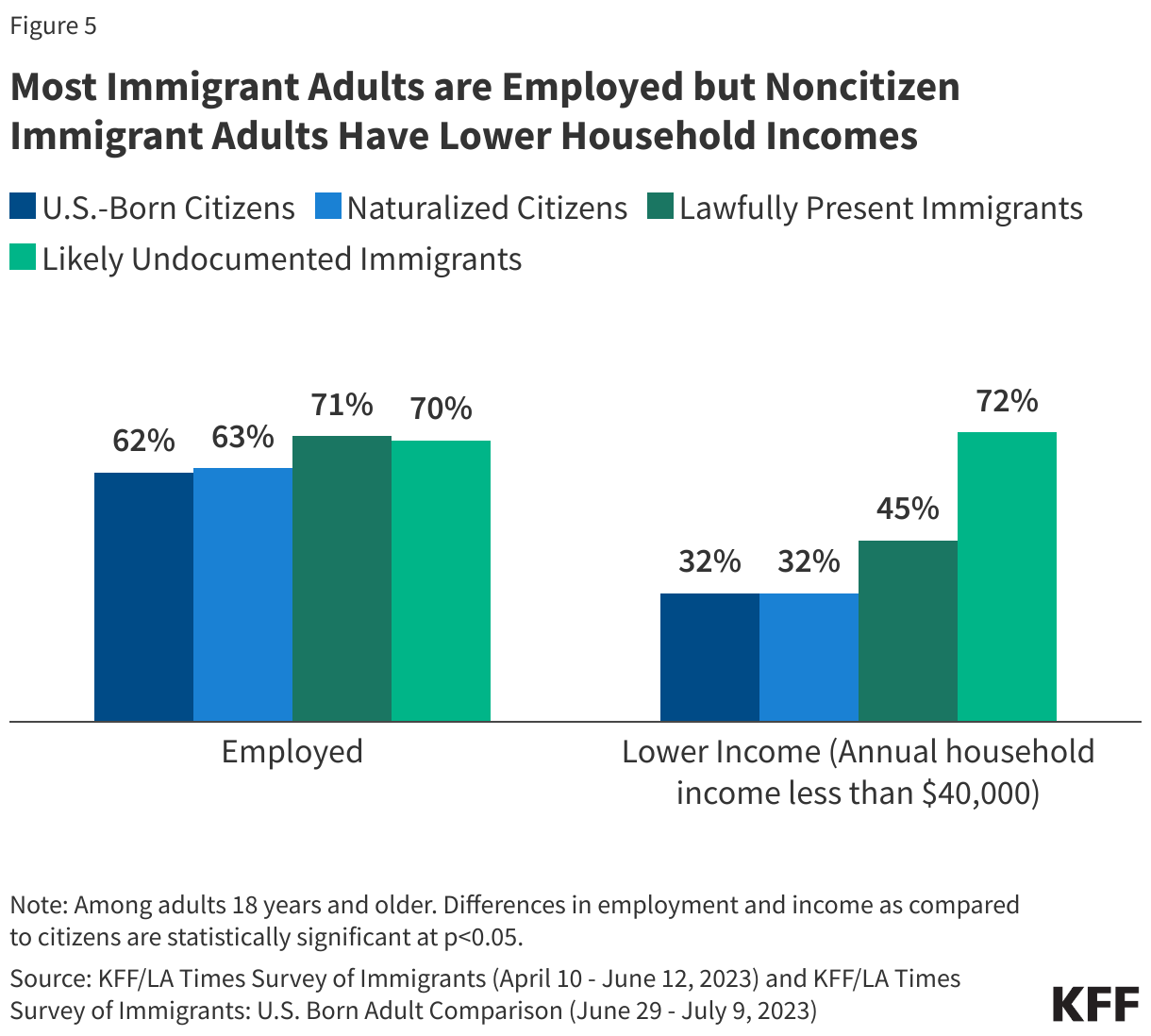

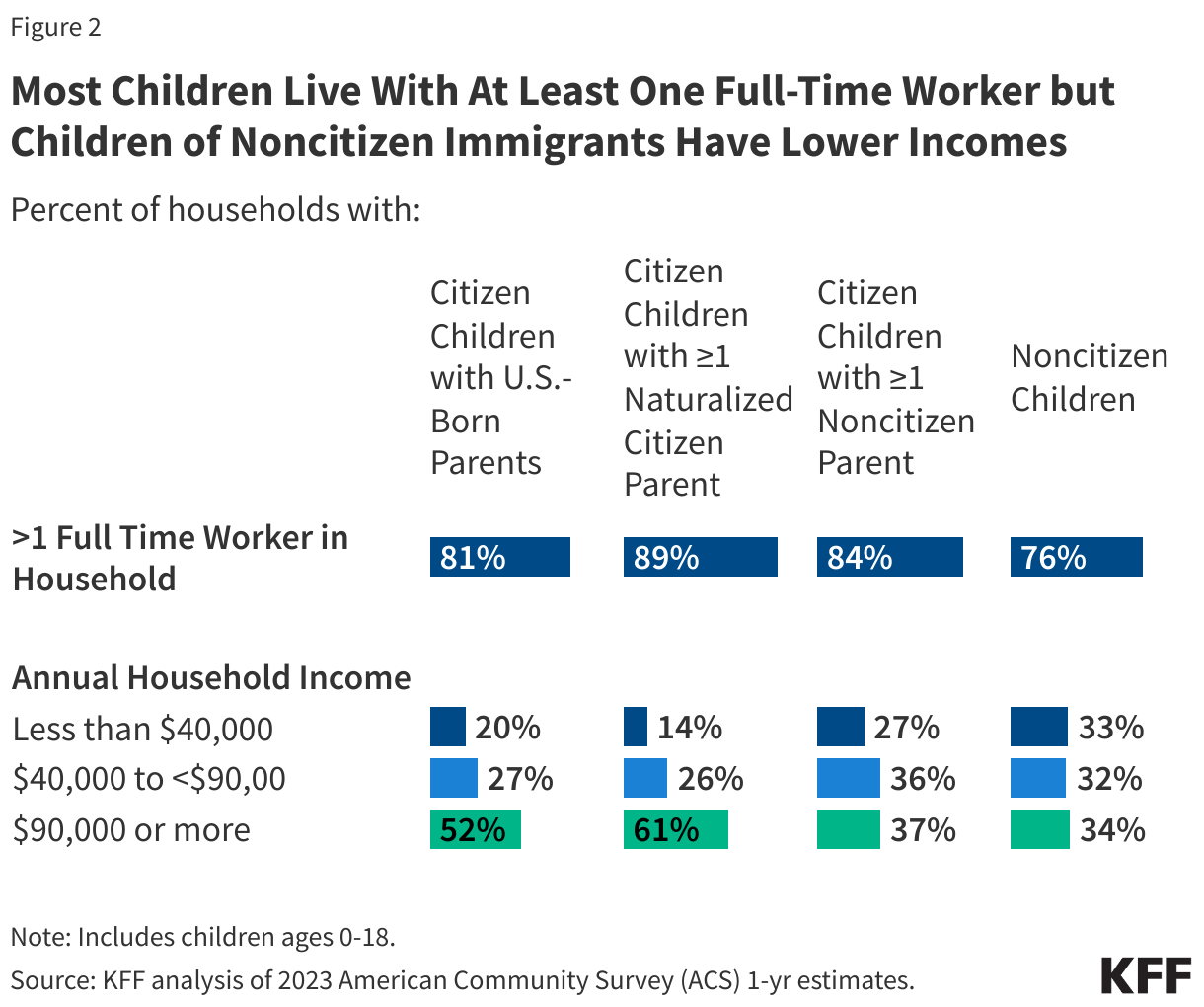

Most children of immigrants live in households with a full-time worker regardless of parental citizenship status; however, children with a noncitizen parent are more likely than children with citizen parents to live in lower income households. More than eight in ten citizen children live in a household with a full-time worker across parental citizenship statuses, and over three in four (76%) noncitizen children live in a household with a full-time worker. However, noncitizen children (33%) and citizen children with a noncitizen parent (27%) are more likely than those with U.S.-born parents (20%) and naturalized citizen parents (14%) to live in lower income households with annual incomes of less than $40,000.

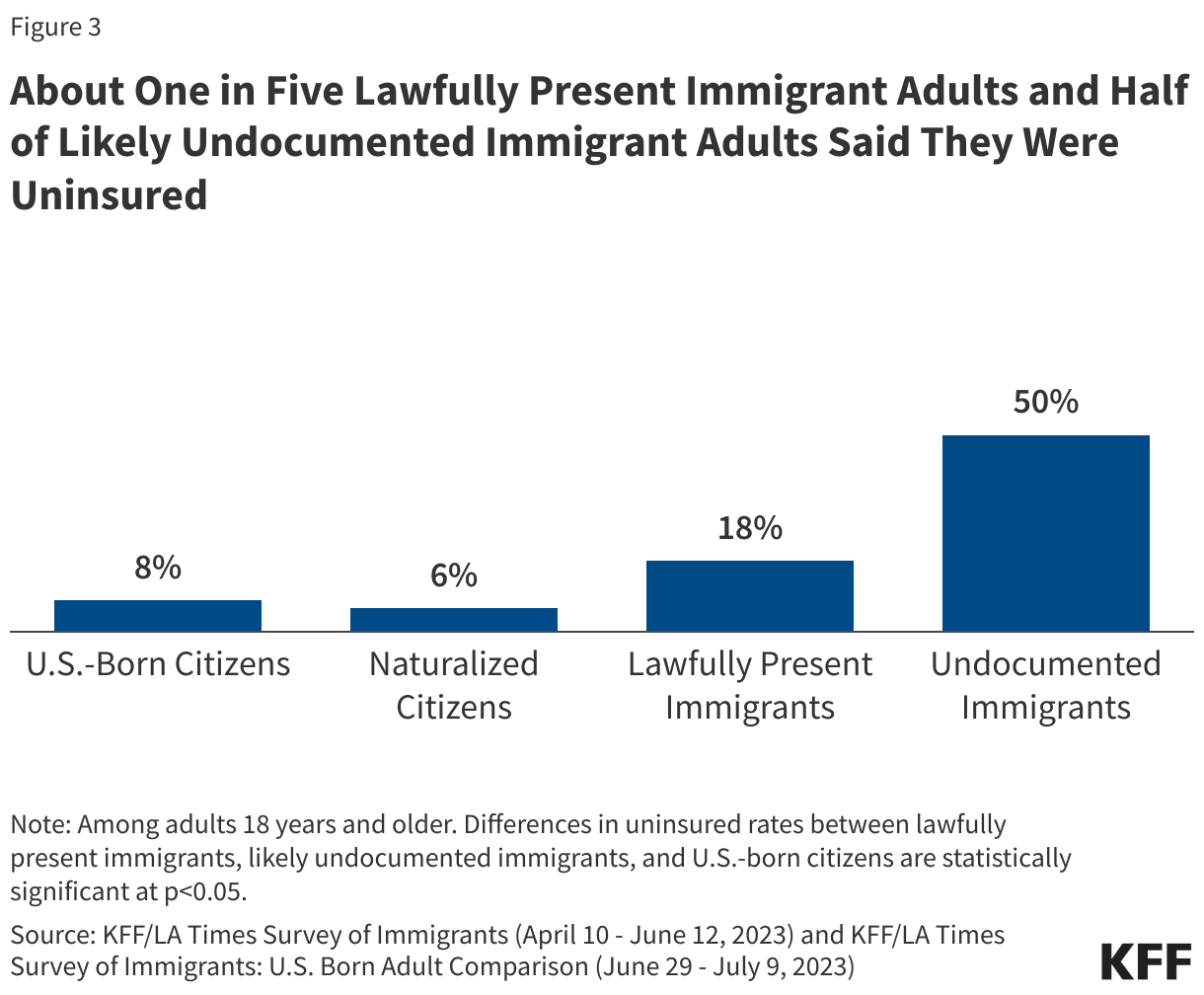

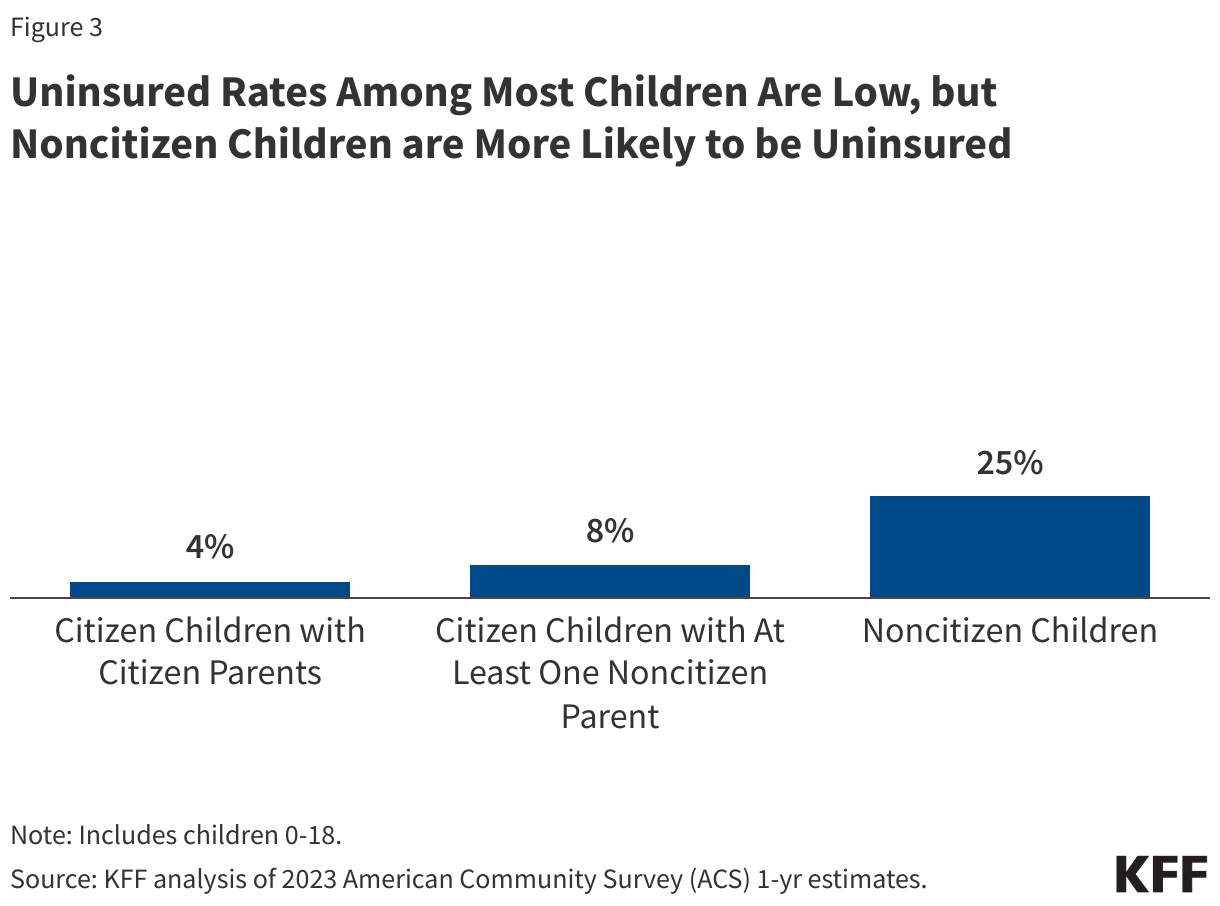

Uninsured rates among most children of immigrants remain low reflecting that most are citizens and broad coverage options are available for low-income children. As of 2023, fewer than one in ten citizen children with U.S.-citizen parents (4%) and citizen children with noncitizen parent(s) (8%) were uninsured. The small share of children who are noncitizens had a higher uninsured rate (25%). Low uninsured rates among most children reflect broad coverage for lower income children through Medicaid and the Children’s Health Insurance Program (CHIP), including state take-up of options to cover immigrant children and some state-funded coverage programs that cover children regardless of immigration status. However, coverage gaps remain for noncitizen children.

Policies that may be implemented under the incoming Trump administration could negatively affect the health and well-being of children of immigrants and have long-term negative consequences for the nation’s economy and workforce. During the first Trump administration, uninsured rates among children in immigrant families increased and immigrant families experienced negative impacts on health due to changes in public charge policy and enhanced enforcement actions. Potential immigration policies and actions that may be taken under the incoming Trump administration such as mass detention and deportation efforts, ending birthright citizenship, and/or reinstating changes to public charge policy would likely increase fears among immigrant families and negatively impact the health of children in immigrant families. The proposed policies would also likely have broader ramifications for the economy and workforce, given the major role immigrants and their adult children play, particularly in certain industries, including health care.

Overview of Children of Immigrants

As of 2023, 19 million or one in four children aged 18 and under in the U.S. had an immigrant parent. These include one in ten (12%) or 9 million who are citizen children with a noncitizen parent, a similar share (11%) or 8.3 million who are citizen children with a naturalized citizen parent, and 3%, or about 2.3 million, who are noncitizens themselves (Figure 1).

While most children of noncitizen immigrants are U.S. citizens and live in a family with at least one full-time worker, they are more likely to live in lower income households than the children of U.S.-citizen parents. As of 2023, eight in ten or more of citizen children of U.S.-born citizen parents (81%), naturalized citizen parent(s) (89%), and noncitizen parent(s) (84%) lived in a family with at least one full-time worker (Figure 2). Three-quarters of noncitizen children (76%) also lived in a family with at least one full-time worker in 2023. However, citizen children with at least one noncitizen parent (27%) and noncitizen children (33%) were more likely to live in a lower income household (annual household income of less than $40,000) than citizen children with U.S.-born citizen parents (20%) or those with at least one naturalized citizen parent (14%) (Figure 2). Lower household income among children of noncitizen immigrants reflects noncitizen immigrants’ disproportionate employment in lower-wage jobs in industries such as construction, agriculture, and transportation, which are less likely to provide employer-sponsored insurance.

Access to Health Coverage and Care Among Children of Immigrants

Overall, uninsured rates among most children of immigrants remain low reflecting that the majority are citizens and broad-based coverage options are available for low-income children. Among children with citizen parents, 4% are uninsured, while this share rises to 8% among children with at least one noncitizen parent. Among the small group of children who are noncitizens, uninsured rates are significantly higher at 25% (Figure 3). Medicaid and/or CHIP provide broad eligibility for children with a median eligibility level of 255% of the federal poverty level across states. Higher uninsured rates among citizen children with a noncitizen parent and noncitizen children reflect enrollment barriers such as fears and confusion and language access challenges and eligibility restrictions for federally-funded health coverage, including Medicaid and CHIP, for noncitizen immigrants.

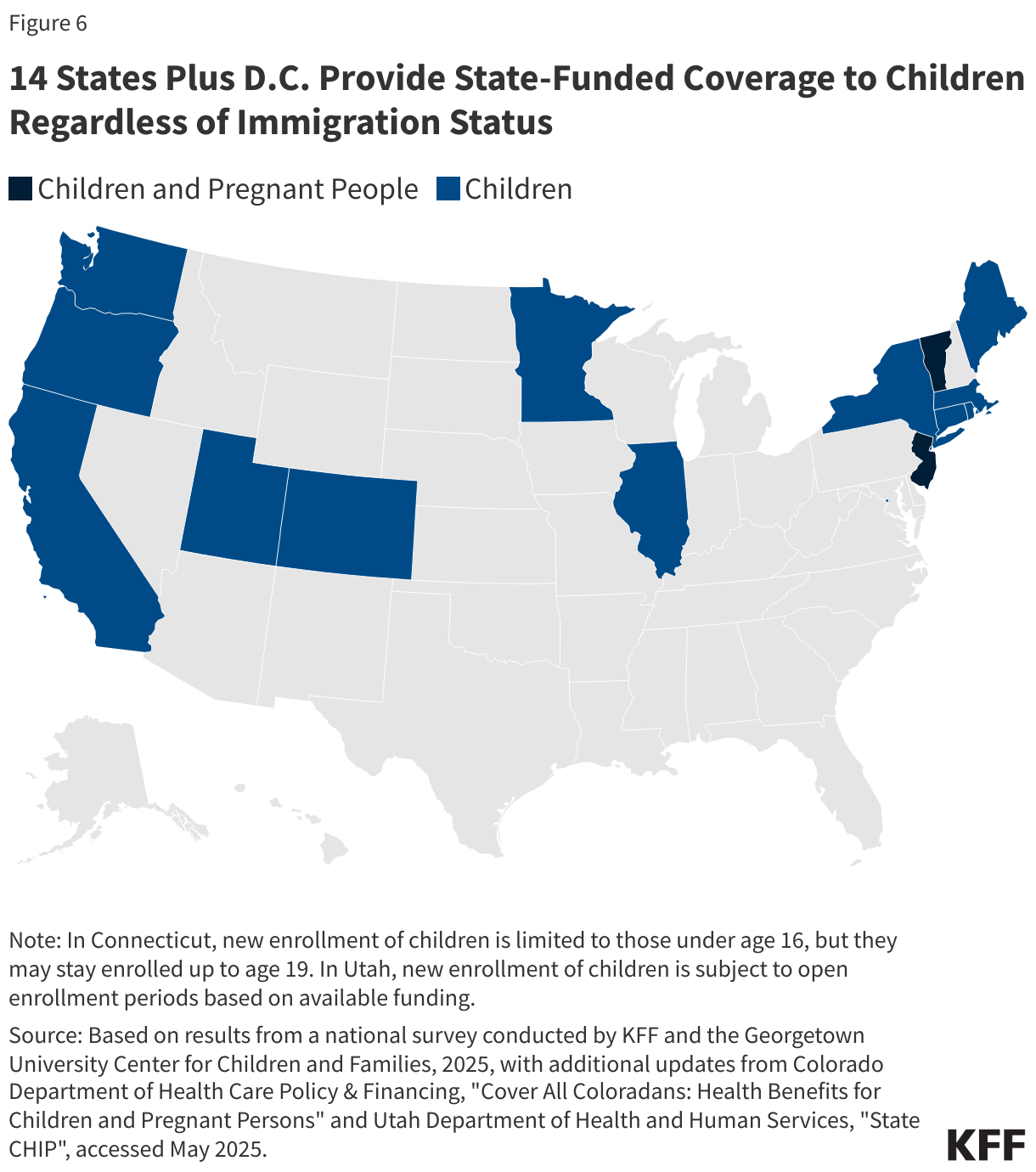

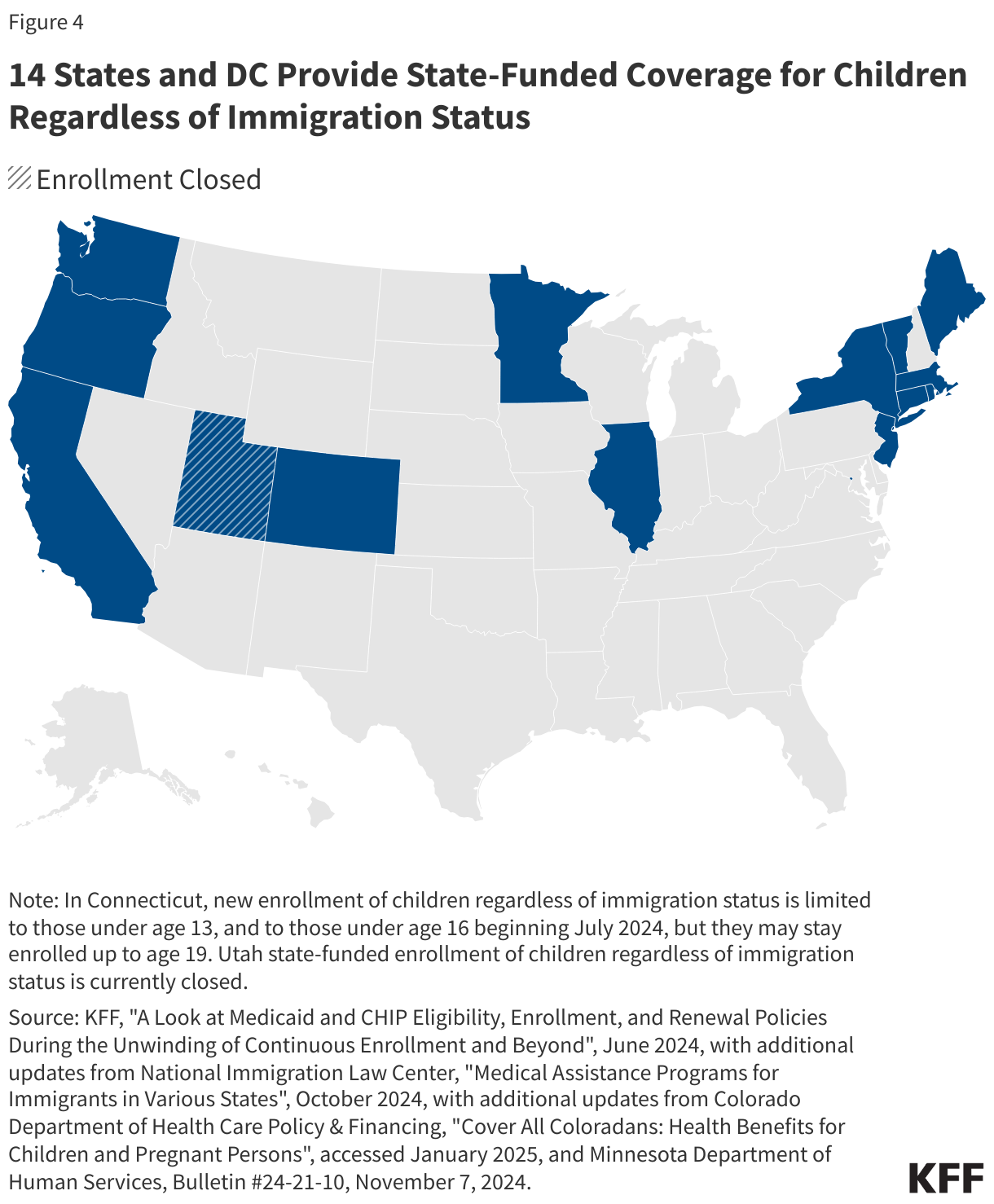

Most states have taken up options to expand coverage for immigrant children. As of April 2025, 37 states plus D.C. cover lawfully residing immigrant children without a five-year waiting period in Medicaid and CHIP. As of April 2025, 14 states and D.C. provide comprehensive fully state-funded coverage for children regardless of immigration status (Figure 4).

While public coverage increases spending by states and the federal government, coverage helps ensure children can access needed care and promotes long-term positive outcomes for children. States have taken steps to expand Medicaid and CHIP coverage, reduce enrollment barriers, and implement continuous eligibility for children in face of rising child poverty and uninsured rates. Children without health coverage are more likely than those with coverage to delay or forgo care because of costs. Coverage expansions to immigrant children also increase access to health care and are associated with improved health outcomes. California’s 2016 expansion to cover low-income children regardless of immigration status was associated with a 34% decline in uninsured rates. Similarly, a study found that children who reside in states that have expanded coverage to all children regardless of immigration status were less likely to be uninsured, to forgo medical or dental care, and to go without a preventive health visit than children residing in states that have not expanded coverage. Research suggests that more expansive health coverage for noncitizens does not increase migration of immigrant children from other states.

Potential Implications of Incoming Trump Administration Policies

During the first Trump administration, uninsured rates among children in immigrant families increased and immigrant families experienced negative impacts on health. During his first term, President Trump implemented changes to public charge policies and enforcement actions that increased fears and uncertainty among immigrant families. Uninsured rates increased among citizen children with a noncitizen parent between 2015 to 2019, which reflected an overall decline in use of public benefits. From 2016-2019, participation in public programs such as Medicaid, CHIP, and the Supplemental Nutrition Assistance Program among citizen children with noncitizen household members fell twice as fast as those with only U.S. citizen household members. Research also shows that enrollment in Medicaid among immigrant mothers fell and newborn birth weight declined following the public charge rule changes. Immigrant families also reported increasing mental health issues among their children related to immigration-related fears and stress during the first Trump administration. There was also decreased use of health care among Hispanic children and fewer well-child visits among children of immigrant mothers following actions on immigration during the first Trump administration.

Fears persist among immigrant families. Although President Biden rescinded public charge and other policy changes implemented by President Trump during his first term, KFF survey data show that as of 2023, about a quarter (27%) of likely undocumented immigrant adults said they avoided applying for government programs that help pay for food, housing, or health care for themselves or a family member in the past year due to immigration-related fears. In addition, a majority of immigrant adults regardless of immigration status remain unsure about whether the use of non-cash assistance programs like Medicaid and CHIP can be used to make public charge determinations or incorrectly believe that to be the case.

Policies under the incoming Trump administration could negatively affect the health and well-being of children of immigrants and have long-term negative consequences for the nation’s economy and workforce. Potential immigration policies and actions that may be taken under the incoming Trump administration such as mass detention and deportation efforts, ending birthright citizenship, and/or reinstating changes to public charge policy would likely increase fears among immigrant families and negatively impact the health of children in immigrant families. For example, research shows that workplace raids to carry out enforcement actions can lead to family separations, poor physical and mental health outcomes for immigrant families, negative birth and educational outcomes for the children of immigrants, and financial hardship due to employment losses. Ending birthright citizenship would limit access to health coverage and care for the children of immigrants given eligibility restrictions for noncitizen immigrants. The proposed policies would also likely have broader ramifications for the economy and workforce given the major role immigrants and their adult children play, particularly in certain industries, including health care. Adult children of immigrants have higher educational attainment and incomes than their parents as well as the adult children of U.S.-born parent(s) and play an outsized role in the U.S. health care workforce. Moreover, immigrants and their adult children contribute billions of dollars in federal, state, and local taxes each year and help to create jobs for U.S.-born people. Research further shows that adult children of immigrants contribute more in taxes on average than their parents or the rest of the U.S.-born population and that their fiscal contributions exceed their costs associated with health care, education, and other social services.