KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

Health Care Costs Tops the Public’s Economic Worries as the Runup to the Midterms Begins; Independent Voters Are More Likely to Trust Democrats than Republicans on the Issue

Two Thirds of Public Say Congress "Did the Wrong Thing" by Not Extending ACA Enhanced Tax Credits, But Republicans Largely Say Congress “Did the Right Thing”

Heading into this midterm election year, the cost of health care tops the public’s economic anxieties and more than 4 in 10 voters say the issue will have a major impact on their vote, a new KFF Health Tracking poll finds. Voters, including independents, currently trust Democrats more than Republicans to address the cost of health care and most other health care issues, though neither party has an advantage on addressing the overall cost of living, the poll finds.

The poll provides an early look at how the public and voters view health care issues, including costs, following a year of substantial debate and changes. Congress last year enacted major Medicaid changes expected to cut federal spending and increase the number of uninsured and allowed the Affordable Care Act’s enhanced tax credits to expire, sharply increasing the premium payments for most ACA Marketplace enrollees.

Across a range of measures, the poll finds significant concerns about health care costs:

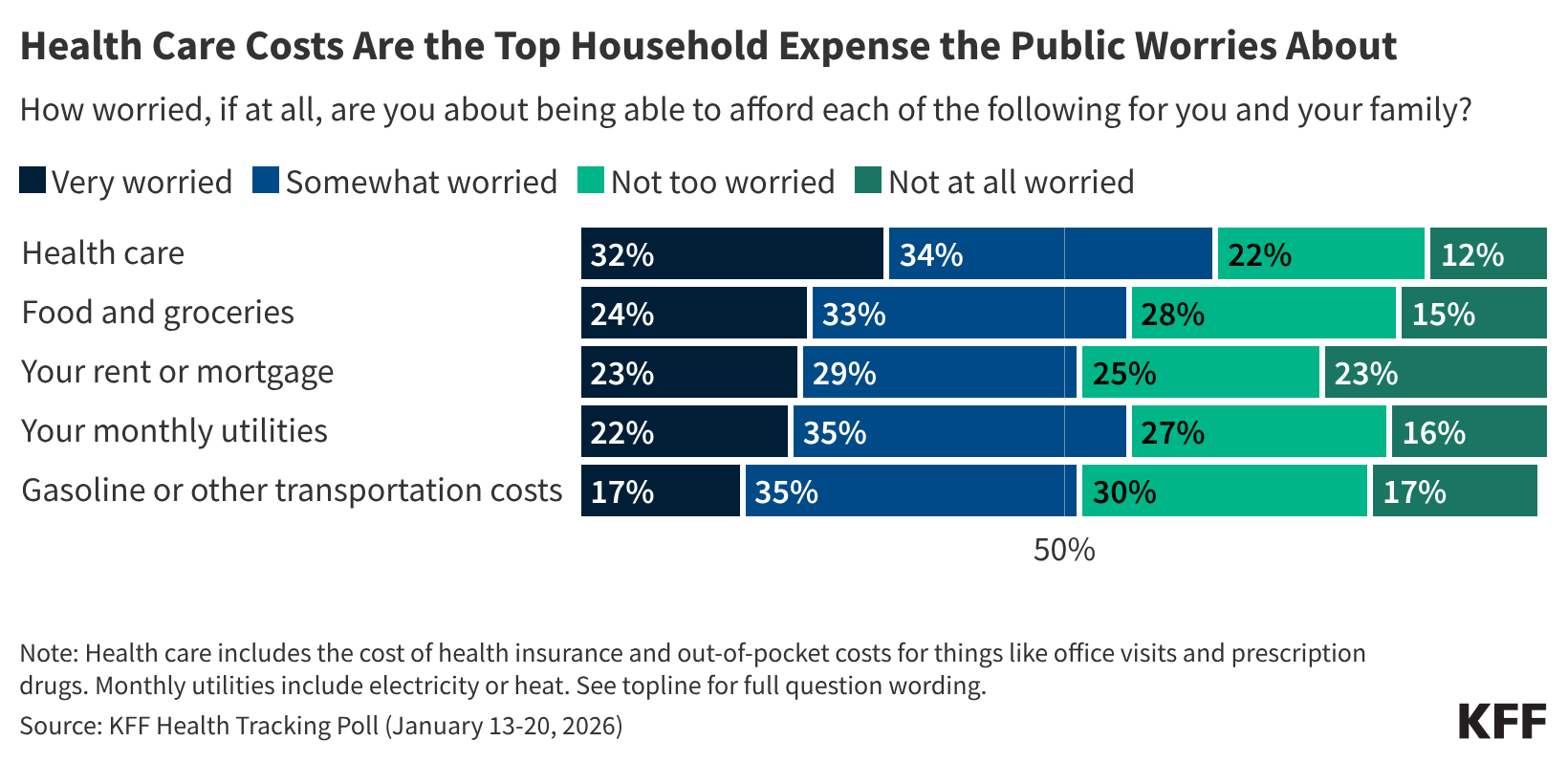

The public was given a list of household expenses families worry about. A third (32%) say that they are “very worried” about their ability to afford health care for them and their families – more than say the same about affording food and groceries (24%), rent or mortgage (23%), monthly utility bills (22%), or gasoline and other transportation costs (17%).

Health care costs are the top economic worry for Democrats, independents, Republicans, and supporters of President Trump’s “Make America Great Again” movement.

A majority (56%) of the public expect health care costs for their family to become less affordable in the coming year. About 1 in 5 say that their health care costs have increased more quickly than other necessities such as monthly utilities (23%) and food and groceries (21%).

Among independent voters, more trust the Democratic Party (35%) than the Republican Party (15%) to address health care costs. Independent voters also give Democrats an advantage over Republicans on Medicaid, the ACA, Medicare, and the cost of prescription drugs, though sizeable shares say they trust neither party. Among all voters, trust in Republicans (30%) is within 5 percentage points of Democrats (35%) on drug prices, an issue President Trump has championed.

More than 4 in 10 voters say that health care costs will have a “major impact” both on their decision to vote in the midterm elections (44%) and on which party’s candidates they will support (43%). This includes two thirds of Democrats, more than 4 in 10 independents, and about a fifth of Republicans.

“Republicans won the legislative battle to let the enhanced ACA tax credits expire, but that helped make health costs more of an economic worry and voting issue, and Democrats are well positioned to capitalize on that in the midterms,” KFF President and CEO Drew Altman said.

Most Continue to View ACA Favorably, But Support Falls Among Republicans After Debate

The poll also gauges the public’s views on the ACA after Congress allowed the law’s enhanced tax credits to expire after extensive debate.

Two thirds (67%) of the public say that Congress did “the wrong thing” by allowing the tax credits to expire, twice the share (33%) that says Congress did “the right thing.”

Large majorities of Democrats (89%) and independents (72%) say that Congress did the wrong thing. While most Republicans (63%) and MAGA supporters (64%) say Congress did the right thing, about a third of each group says that Congress did the wrong thing.

Most (58%) of the public continues to hold favorable views of the ACA, though support this month is down 6 percentage points since September (64%).

The shift reflects a drop in favorability among Republicans (22% now vs. 36% in September) and among MAGA supporters (16% now vs. 31% in September).

Designed and analyzed by public opinion researchers at KFF, this survey was conducted January 13-20, 2026, online and by telephone among a nationally representative sample of 1,426 U.S. adults in English and in Spanish. The margin of sampling error is plus or minus 3 percentage points for the full sample. For results based on other subgroups, the margin of sampling error may be higher.

Finding on other topics including prior authorization will be reported separately.

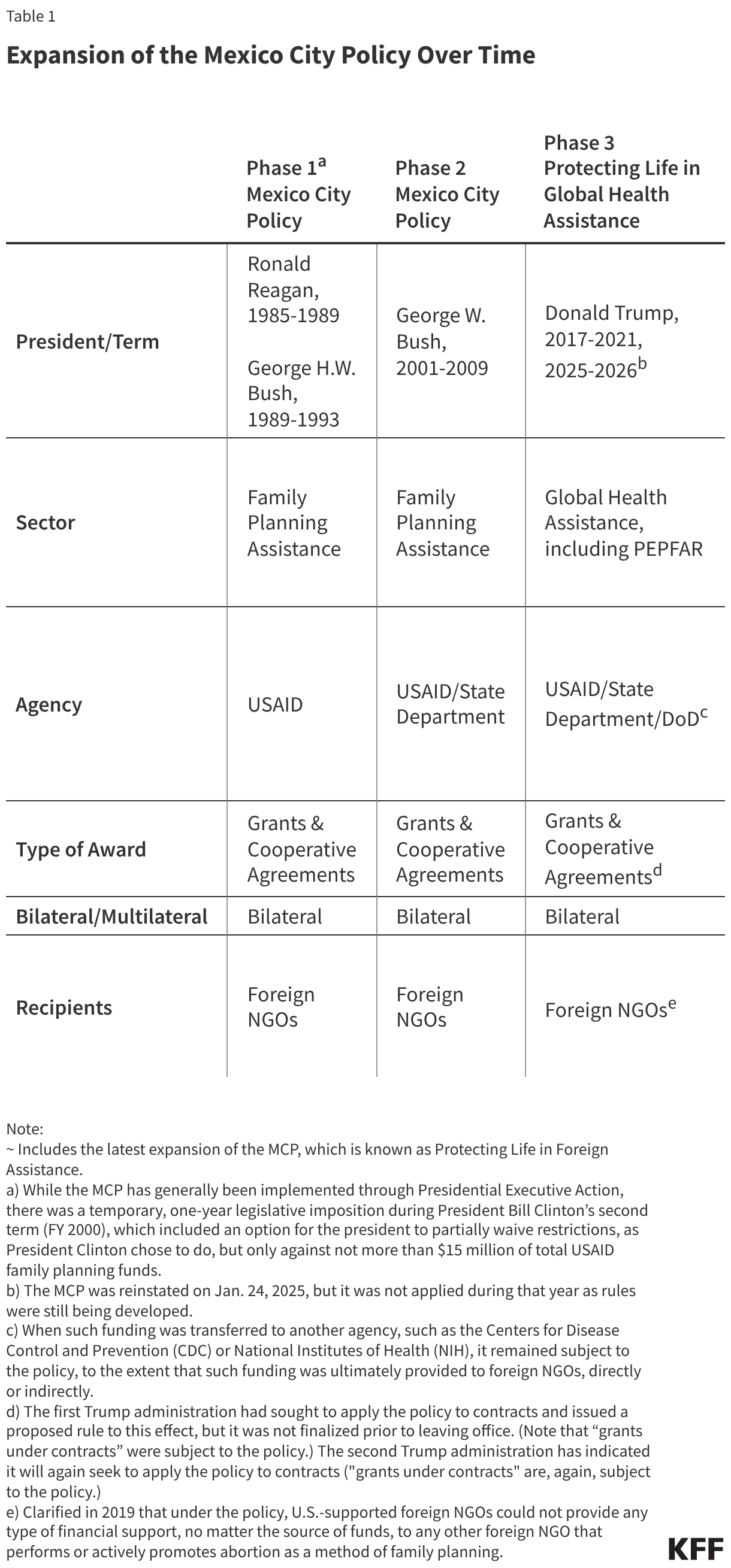

On January 27, 2026, the Trump administration released details of the latest expansion of the Mexico City Policy, a policy he reinstated in January of last year. The policy, which has been in effect, depending on the party of the President, since 1984, has required foreign non-governmental organizations (NGOs) to certify that they would not “perform or actively promote abortion as a method of family planning” using funds from any source (including non-U.S. funds) as a condition of receiving U.S. government global family planning funding. In 2017, President Trump reinstated the policy but also significantly expanded it to encompass the vast majority of U.S. bilateral global health assistance. The latest expansion, now part of a broader set of restrictions known as the “Promoting Human Flourishing in Foreign Assistance (PHFFA)” Policy, applies to significantly more funding, many more organizations, and new services and activities. Specifically, it now applies to most non-military foreign assistance and most recipients of foreign aid (not just foreign NGOs). And, in addition to abortion, it prohibits activities related to diversity, equity, and inclusion (DEI) and promoting or providing gender affirming care, legal protections based on gender identity, and other related services and activities. This analysis assesses the potential reach of the latest expansion of the policy by examining foreign assistance funding provided in FY 2024, the most recent year with complete information, to identify the amount of funding, number of organizations, and range of foreign assistance sectors that stand to be affected. The analysis looks at total funding that would be subject to restrictions, and although not all recipients are necessarily currently engaging in activities subject to the restrictions, all would have to decide whether they accept the policies’ terms. Among the key findings:

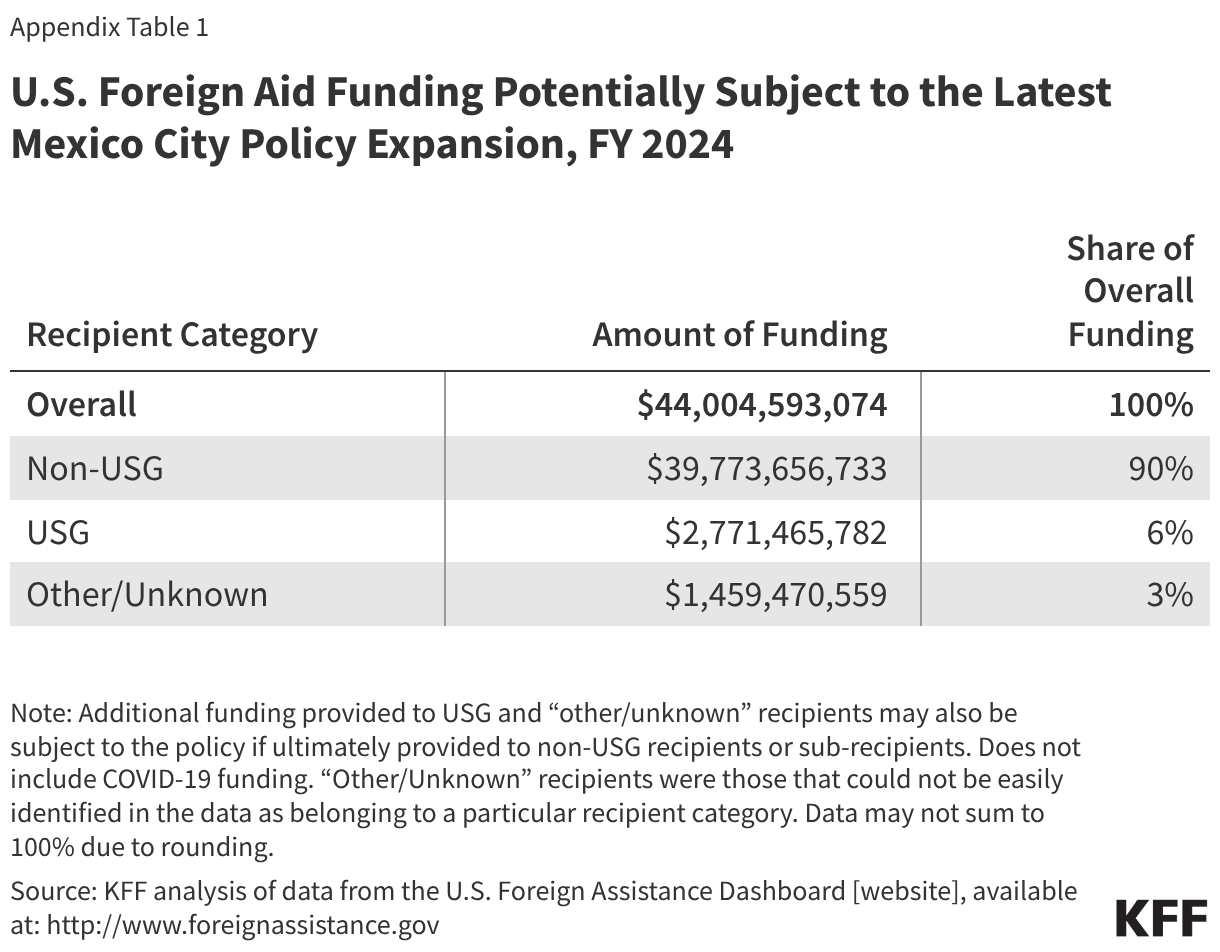

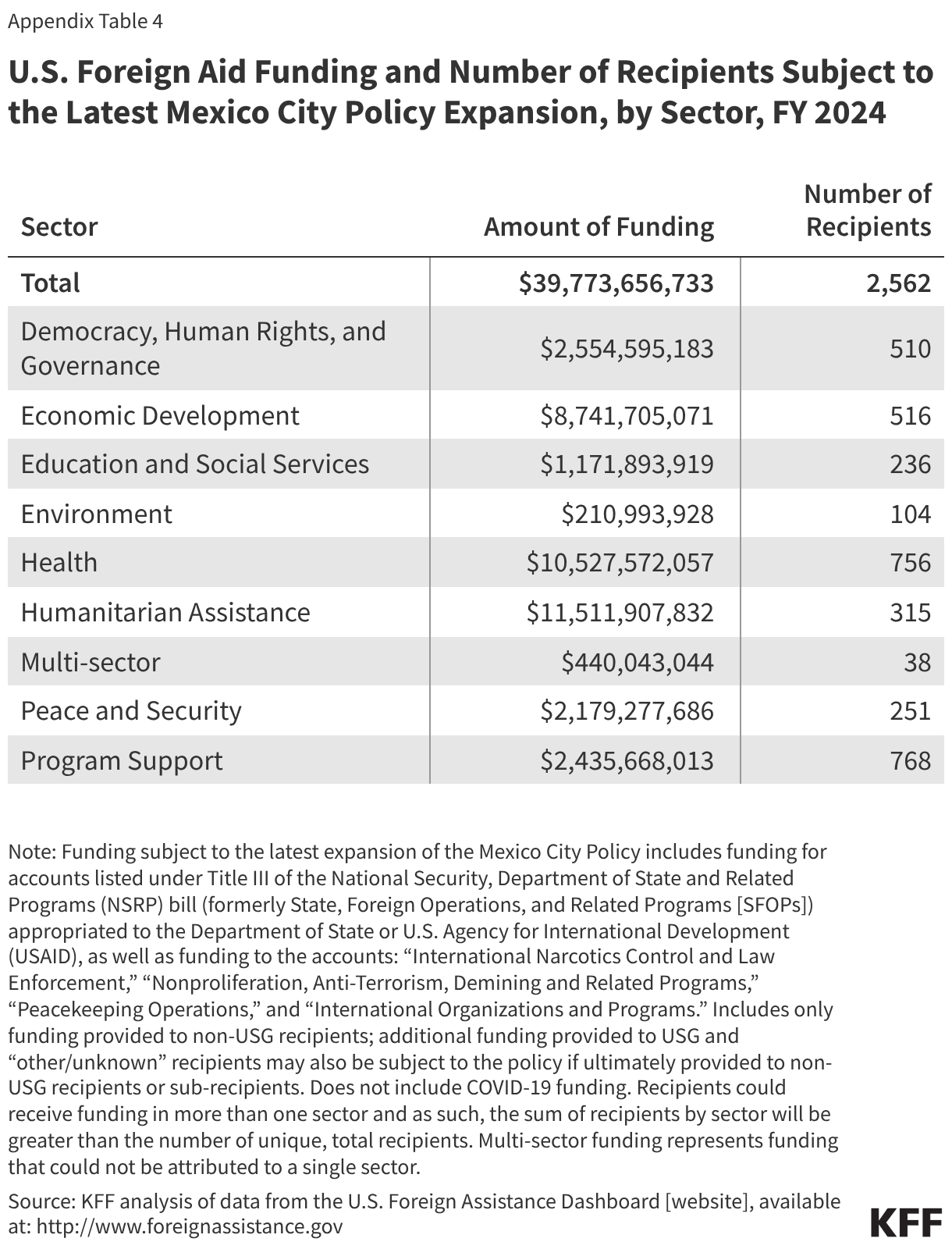

In FY 2024, $39.8 billion in U.S. foreign aid, spanning 160 countries, was obligated to prime recipients, funding that would be subject to the latest expansion (additional funding could be subject to the policy if it was ultimately provided, directly or indirectly, to recipients or sub-recipients).

Notably, this is tens of billions more than the amount of global health assistance subject to the policy under the Trump administration’s previously expanded policy ($7.3 billion in FY 2020), and significantly more than the amount of family planning assistance subject to the policy during earlier administrations (between $300-$600 million).

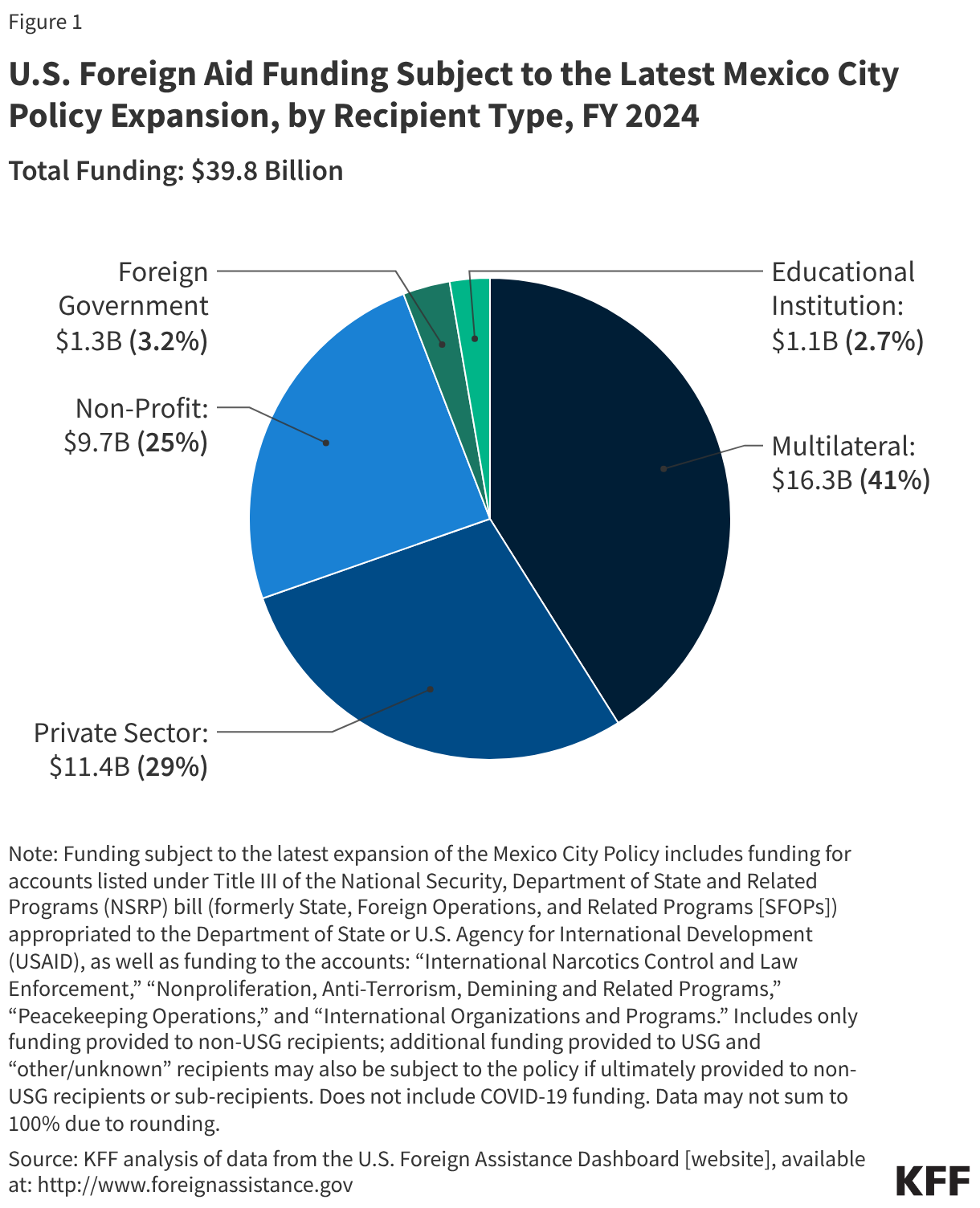

By recipient type, the largest share (41%) of the $39.8 billion was provided to multilateral organizations, recipients that are newly subject to the policy under the latest expansion. The second largest (29%) was provided to private sector organizations, including the newly-subject U.S. private sector.

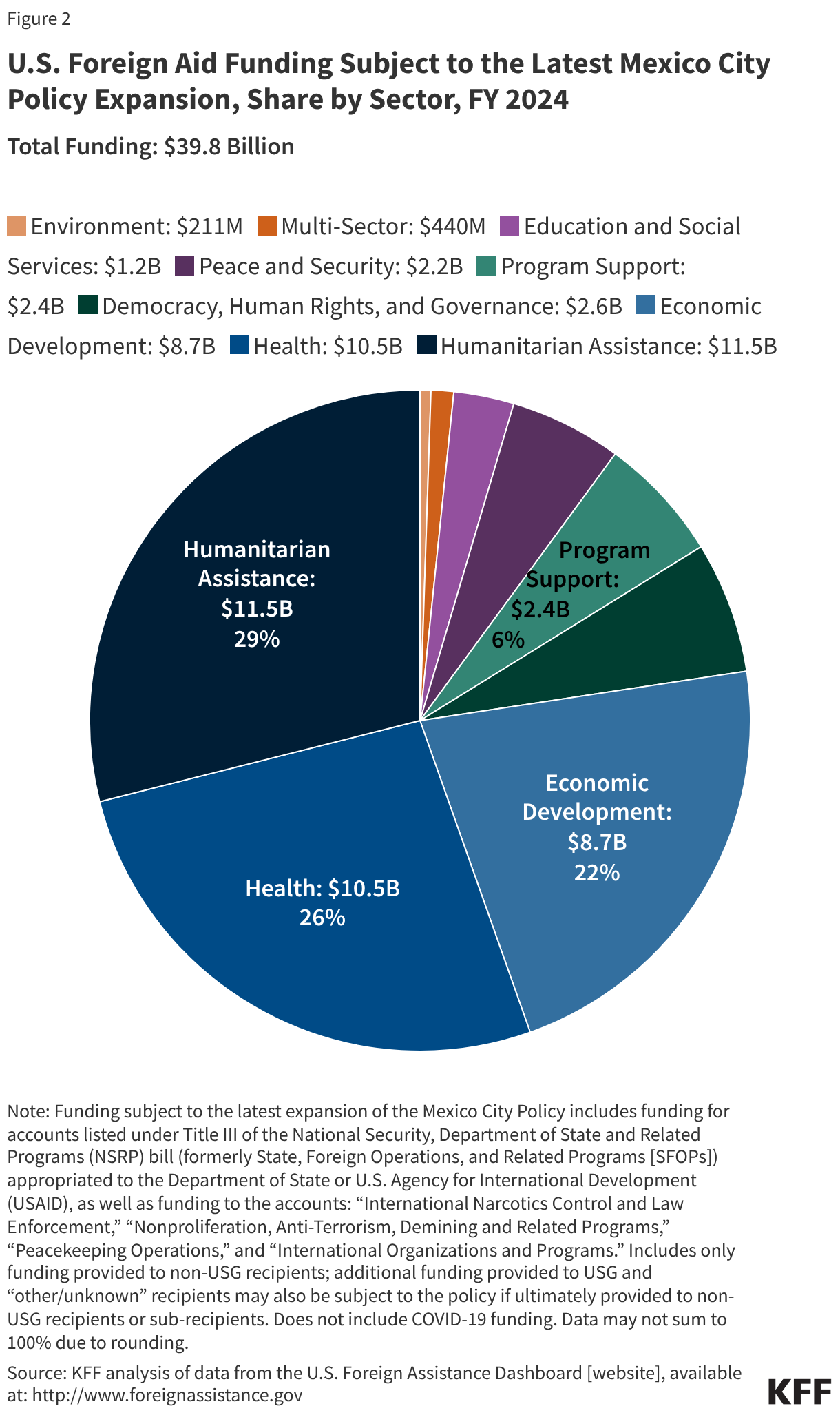

By sector, humanitarian assistance accounted for the largest share of funding (29%), followed by health (26%) and economic development (22%); two of these sectors (humanitarian assistance and economic development) are among the several sectors newly subject to the policy under the latest expansion.

There were almost 2,600 prime recipients of U.S. foreign aid in FY 2024, a significantly higher number than for health alone (756 prime recipients). This number should be considered a floor, since prime recipients must “flow-down” the policy to any sub-recipients. The majority of prime recipients were foreign entities (62%); U.S.-based entities accounted for 34%, with multilateral recipients accounting for 4%.

Whether or not the full extent of the expansion will be instituted (there are likely to be legal challenges to some aspects of the policy, which could limit its reach, and some additional rule-making has yet to occur), it represents a significant expansion in terms of funding, number of organizations, and content and services restricted, well beyond the reach of what was in place during the first Trump administration.

Background

The Mexico City Policy (MCP) is a U.S. government (USG) policy that – when in effect – has required foreign NGOs1 to certify that they will not “perform or actively promote abortion as a method of family planning” using funds from any source (including non-U.S. funds) as a condition of receiving U.S. global family planning assistance and, in 2017 under the first Trump administration, most other U.S. global health assistance. First announced in 1984 by the Reagan administration, the policy has been rescinded and reinstated by subsequent administrations along party lines since and has been in effect for 23 of the past 42 years. It has also been steadily expanded over time (see Table 1). Under the first Trump administration, the policy was renamed “Protecting Life in Global Health Assistance” (PLGHA). Among opponents, it has also been known as the “Global Gag Rule,” because among other activities, it prohibited foreign NGOs from using any funds (including non-U.S. funds) to provide information about abortion as a method of family planning and to lobby a foreign government to legalize abortion.

The second Trump administration reinstated the MCP through a Presidential Memorandum on January 24, 2025, noting that the policy would be expanded even further. On January 27, 2026, the policy details were released under three separate, but inter-related final rules (interim final rules were first posted on January 23), now called the “Promoting Human Flourishing in Foreign Assistance (PHFFA) Policy” (see Box 1).

Box 1: Promoting Human Flourishing in Foreign Assistance (PHFFA) Policy

The Trump administration released details of its new Promoting Human Flourishing in Foreign Assistance (PHFFA) Policy, which includes the latest expansion of the Mexico City Policy, via three separate, but related, final rules on January 27, 2026. Each rule applies to the same funding streams, types of organizations, and award mechanisms but restricts different activities and services:

Protecting Life in Foreign Assistance (PLFA): prohibits recipients from performing or actively promoting abortion as a method of family planning; the latest expansion of the Mexico City Policy.

Combating Gender Ideology in Foreign Assistance: prohibits recipients from providing or promoting gender affirming care, legal protections based on gender identity, and other related activities; defines sex as “person's immutable biological classification as either male or female.”

This marks the most significant expansion of the policy to date. Specifically, it:

expands to all non-military U.S. foreign assistance (not just global health) administered by the State Department2 (with an intention for the State Department to work with other agencies that administer foreign assistance to also incorporate these provisions);

expands the types of recipients, and consequently the number of organizations, subject to the policy to also include multilateral organizations, foreign governments, and U.S.-based NGOs (not just foreign NGOs);3

expands to prohibit additional content areas and services newly subject to the policy: DEI-related activities as well as support for gender affirming care and services, information, and legal protections based on gender identity, among other related activities (referred to as promoting “gender ideology”); and

expresses an intent to expand to include funding provided through contracts (not just grants and cooperative agreements), although this will be the subject of future rule-making.

Findings

To assess the potential reach of the latest expansion, this analysis looks at U.S. government foreign assistance obligation data for FY 2024 (the most recent year for which complete obligation data by sector are available) to quantify the amount of funding and number and type of prime recipients that could be affected. While not all recipients are necessarily currently engaging in activities subject to the restrictions, all would have to decide whether they accept the policies’ terms. Obligations were analyzed because the policy applies to funding once newly obligated to a recipient (either through an existing or a new award). Data were obtained from ForeignAssistance.gov, the U.S. government’s centralized data portal for budgetary and financial data provided by more than 20 federal agencies that manage foreign assistance programs. The analysis is based on the funding identified in the PHFAA rules, which includes all non-military foreign assistance4 appropriated to the State Department or U.S. Agency for International Development (USAID) under Title III and four other accounts under Department of State, Foreign Operations, and Related Programs (SFOPs)/National Security, State Department, and Related Programs (NSRP) appropriations acts (specifically, “International Narcotics Control and Law Enforcement,” “Nonproliferation, Anti-Terrorism, Demining and Related Programs,” “Peacekeeping Operations,” and “International Organizations and Programs”). The analysis also includes funding provided through contracts (not just grants and cooperative agreements) for two reasons: first, the rules indicate that further rule-making will be undertaken to add these policy restrictions to contracts; and second, it is not possible to disaggregate obligations by funding instrument in ForeignAssistance.gov (see Box 2 for key terms, Methodology for more detail, and Appendix for detailed data).

Box 2: Key Terms

Obligation: A binding agreement that will result in outlays of funds immediately or at a later date.

Prime Recipient: The main recipient, or those that receive funding directly from the U.S. government to carry out foreign assistance work.

Sub-Recipient: Those that receive funding indirectly from the U.S. government through an agreement with the prime recipient.

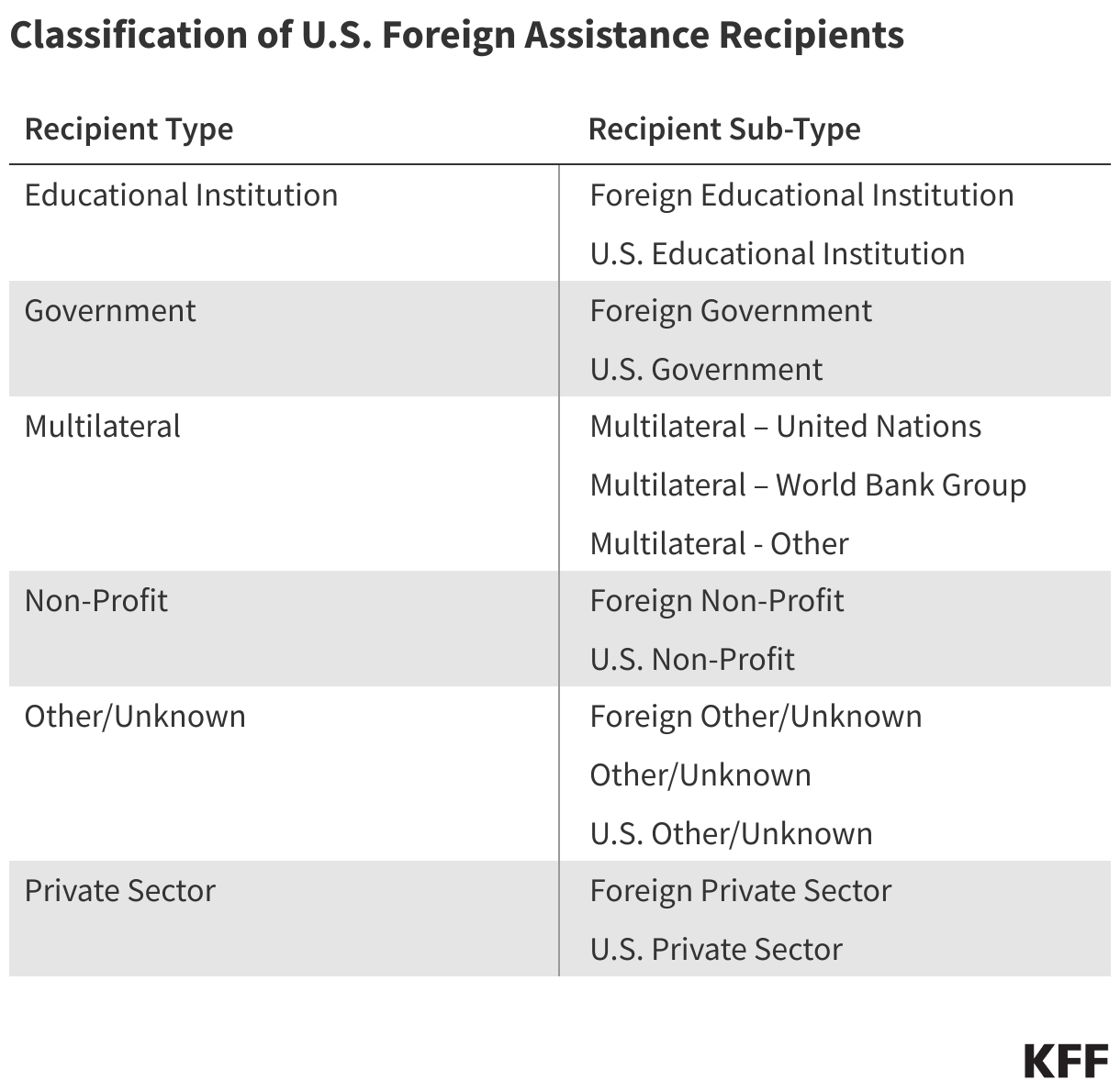

Non-Governmental Organization (NGO): a for-profit or not-for-profit organization that is not part of the U.S. government, a foreign government, or a multilateral organization; includes private sector organizations, non-profit organizations, and educational institutions.5

Multilateral Organization: an organization that is jointly supported by multiple governments and, often, other partners (versus bilateral efforts, which are carried out on a country-to-country basis); includes specialty agencies of the United Nations (U.N.) and international financing mechanisms that pool and direct resources from multiple public and private donors for specific causes.6

Foreign Government: any department, agency, independent establishment, or other entity of the government of a foreign country.

Parastatal: foreign-government-owned organization operated as a commercial company or other organization, including non-profits, or enterprises in which foreign governments or foreign government agencies have a controlling interest.

In FY 2024, $39.8 billion in U.S. foreign aid was obligated to prime recipients, funding that would be subject to the latest expansion. This includes funding provided to U.S. and foreign NGOs, international organizations, foreign governments, and parastatals (additional funding could be affected if it was ultimately provided, directly or indirectly, to recipients or sub-recipients subject to the policy).

Notably, this is tens of billions more than the amount of global health assistance subject to the policy under the first Trump administration’s previously expanded policy ($7.3 billion in FY 2020), and significantly more than the amount of family planning assistance subject to the policy during earlier administrations (between $300-$600 million). See Box 3.

Box 3: Funding Newly Subject under the Latest Expansion of the MCP

By Recipient Type:

Multilateral organizations: $16.3 billion

Foreign governments: $1.3 billion

U.S. NGOs: $16.5 billion^

Foreign NGOs: $3.5 billion in non-health sectors

By Sector:

Non-health sectors: $29.2 billion, including (for example):

Humanitarian assistance: $11.5 billion

Economic development: $8.7 billion

Democracy, human rights, and governance: $2.6 billion

Peace and security: $2.2 billion

Education and social services: $1.2 billion

Health sector: $8.3 billion in U.S. NGO,^ multilateral, and foreign government funding

Note: Amounts by recipient type and sector are not mutually exclusive categories. ^ Any foreign NGO that was a sub-recipient of U.S. global health assistance from a U.S. NGO would have been subject to the previously expanded MCP, PLGHA, when in place.

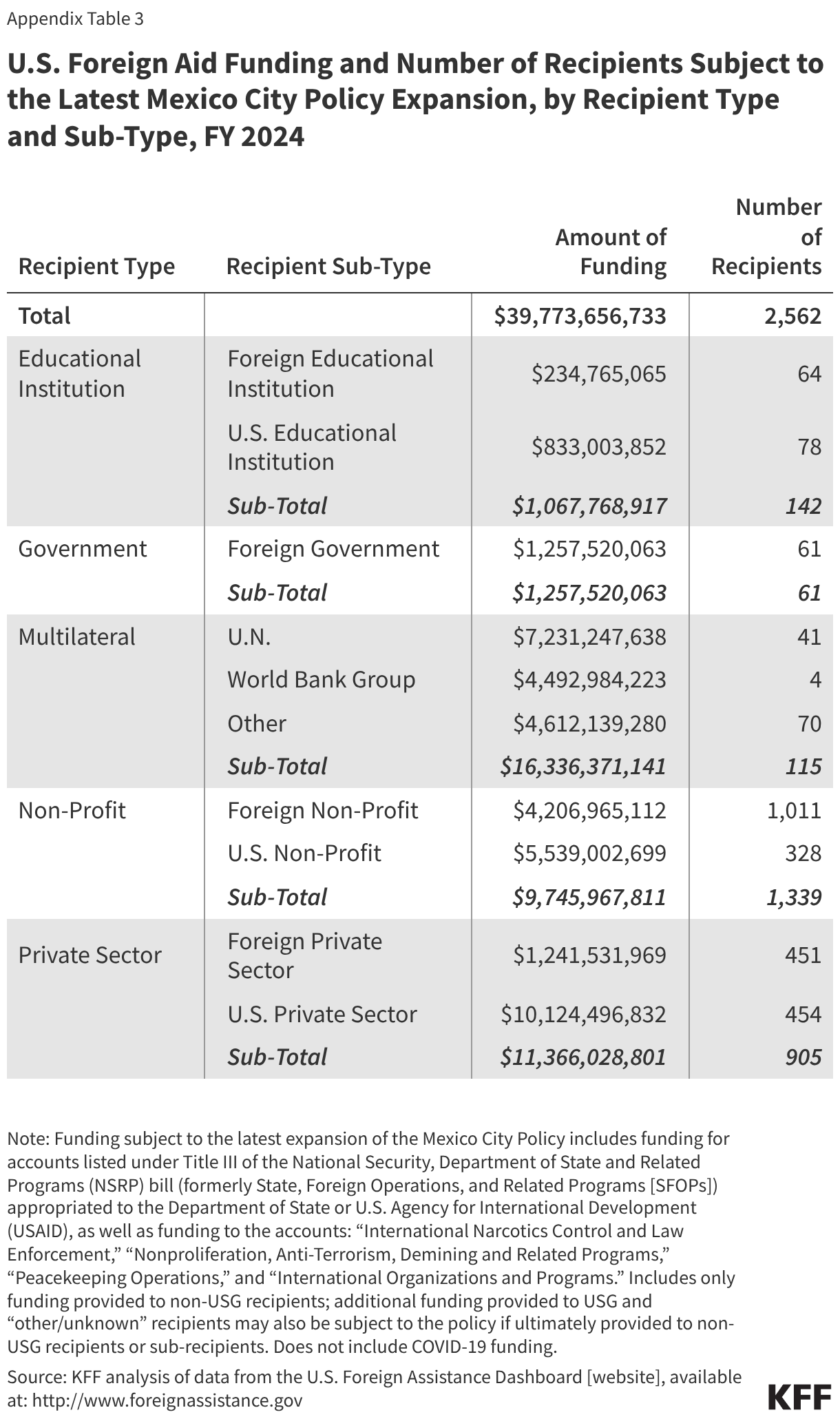

By recipient type, the largest share of funding was provided to multilateral organizations ($16.3 billion, or 41%), entities that are newly subject to the policy. The private sector received the next largest amount of funding ($11.4 billion, or 29%), followed by the non-profit sector ($9.7 billion, or 25%). Smaller amounts were provided to foreign governments ($1.3 billion, or 3.2%) and educational institutions ($1.1 billion, or 2.7%) (see Figure 1).

U.S.-based recipients received $16.5 billion (41%). These included U.S. NGOs, specifically U.S. non-profits, private sector organizations, and educational institutions (all newly subject to the policy). Foreign recipients, both governments and NGOs, received $6.9 billion (17%); foreign governments are also newly subject to the policy.

Collectively, the $39.8 billion in foreign assistance was provided to 160 countries, with more countries likely reached through “regional” and “worldwide” activities.7 This is significantly more countries than would be reached with global health assistance alone (87 countries).

By sector, humanitarian assistance accounted for the largest share of funding ($11.5 billion, or 29%) in FY 2024, followed by health ($10.5 billion, or 26%) and economic development ($8.7 billion, or 22%). Two of these sectors (humanitarian assistance and economic development) are newly subject to the policy (see Figure 2). The remaining sectors each accounted for approximately $3 billion (6%) or less.

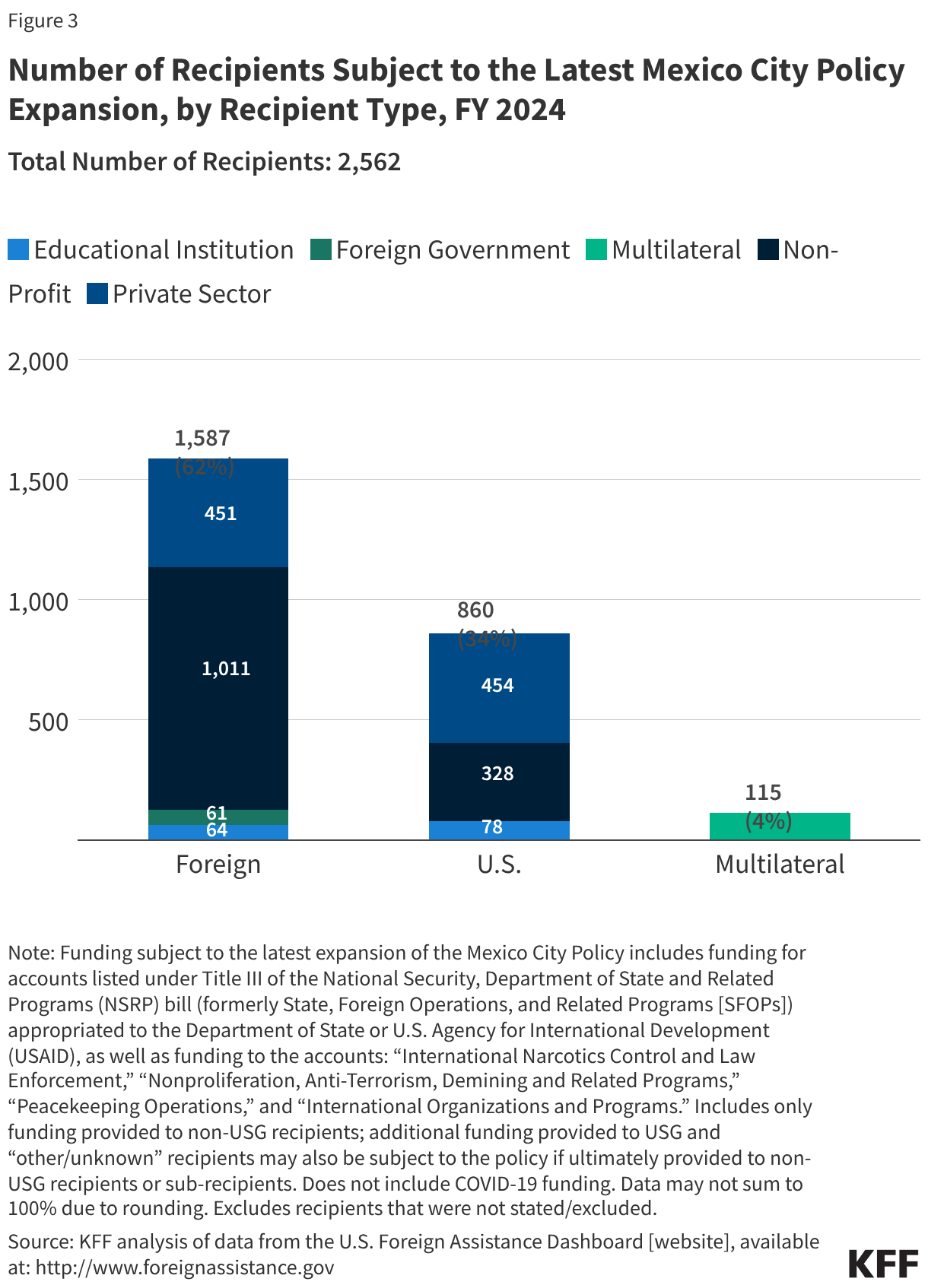

There were 2,562 non-USG prime recipients of U.S. foreign assistance in FY 2024, most8 of which (2,111 or 82%) would be subject to the policy for the first time. This number should be considered a floor, since any sub-recipients of U.S. foreign aid would also be subject to the policy.

Whereas most funding was provided to multilateral organizations, most recipients (62%, or 1,587) were foreign-based organizations. About a third (34%, or 860) were U.S.-based organizations. Multilateral organizations accounted for the remaining 4% (115) (see Figure 3).

NGOs (foreign- and U.S.-based) accounted for the vast majority (93%, or 2,386) of recipients. NGOs include:

non-profits (more than half – 52% - of all 2,562 recipients, or 1,339),

private sector organizations (more than a third – 35% - of all recipients, or 905), and

educational institutions (6% of all recipients, or 142).

Among the 2,386 NGO recipients, almost two-thirds (64%, or 1,526) were foreign NGOs, and the other third (36%, or 860) were U.S.-based NGOs.

The sectors with the largest numbers of recipients in FY 2024 were program support9 (768), health (756), and economic development (516). The next largest sector was democracy, human rights, and governance (510), followed by humanitarian assistance (315) (see Figure 4).

Methodology

This analysis uses FY 2024 foreign assistance obligation data, downloaded from ForeignAssistance.gov on November 20, 2025. ForeignAssistance.gov is the U.S. government’s centralized data portal for budgetary and financial data provided by more than 20 federal agencies that manage foreign assistance programs. Obligations are binding agreements that will result in outlays of funding, immediately or sometime in the future. The policy, when in place, is applied to funding that is obligated to recipients either as part of an existing award or as part of a new award. Data on funding amounts and recipients were analyzed by agency, sector, location, and type of entity. To the extent possible, COVID-19 emergency funding was excluded from this analysis, as it represented one-time funding for a particular event.

Recipients were categorized into the following groups (see table below) based on classifications already present in the ForeignAssistance.gov data as well as background research, where such classifications were not provided. Each recipient was reviewed, and the review sought to correct any mis-categorization in the original data and remove duplicates. “Other/Unknown” recipients were those that could not be easily identified as belonging to a particular recipient type/sub-type. Where it was not possible to identify a recipient as a single, implementing entity, they were excluded from analysis looking at the number of unique recipients.

Funding included in the analysis was based on the specifications in the final rules and includes Title III funding appropriated to the State Department and USAID (now administered by the State Department) as well as funding appropriated to four other accounts under Department of State, Foreign Operations, and Related Programs (SFOPs)/National Security, State Department, and Related Programs (NSRP) appropriations acts (specifically, “International Narcotics Control and Law Enforcement,” “Nonproliferation, Anti-Terrorism, Demining and Related Programs,” “Peacekeeping Operations,” and “International Organizations and Programs”), whether or not these data were listed as "Economic" or "Military" funding. The analysis excluded the funding in these accounts that was directed to U.S. departments or agencies as prime recipients, which totaled $2.8 billion in FY 2024, as well as funding directed to “Other/Unknown” recipients, which totaled $1.5 billion in FY 2024 (although to the extent that this funding is ultimately provided to a non-USG sub-recipient, it too would be subject to the policy). The U.S. government has also indicated that its intention is to apply the latest MCP expansion to additional non-military foreign assistance at other U.S. agencies and departments, which would also increase the amount of funding and number of organizations subject to the latest expansion.

The analysis also includes funding provided through contracts (not just grants and cooperative agreements) for two reasons: first, the rules indicate that further rule-making will be undertaken to add these policy restrictions to contracts; and second, it is not possible to disaggregate obligations by funding instrument in ForeignAssistance.gov data.

Appendix Tables

Per the interim rules, a foreign non-governmental organization is defined as “any non-governmental organization or entity, whether non-profit or profit-making (including any commercial firm and educational institution), not organized or existing under the laws of the United States, any State of the United States, the District of Columbia, the Commonwealth of Puerto Rico, or any other territory or possession of the United States.” ↩︎

Specifically, funding appropriated to the U.S. Agency for International Development (USAID) and the State Department; this funding is “administered” by the State Department. USAID was dissolved by the Trump administration in 2025, with its remaining programs transferred to other agencies, including mainly but not solely the State Department. ↩︎

The policies apply differently to U.S. NGOs and foreign governments/parastatals than to foreign NGOs and multilateral organizations. ↩︎

The analysis excluded approximately $82 million in FY 2024 foreign aid funding that was identifiable as emergency COVID-19 assistance since it was one-time emergency funding. ↩︎

Each rule of PHFFA defines a foreign NGO as “any non-governmental organization or entity, whether non-profit or profit-making (including any commercial firm and educational institution), not organized or existing under the laws of the United States, any State of the United States, the District of Columbia, the Commonwealth of Puerto Rico, or any other territory or possession of the United States,” and it defines a U.S. NGO as “any non-governmental organization or entity, whether non-profit or profit-making (including any commercial firm and educational institution), organized or existing under the laws of the United States, any State of the United States, the District of Columbia, the Commonwealth of Puerto Rico, or any other territory or possession of the United States.” ↩︎

Each rule of PHFFA defines an international organization as “(A) Any organization designated as being entitled to enjoy the privileges, exemptions, and immunities under the International Organizations Immunities Act; (B) Any organization treated as a public international organization pursuant to the regulations or policies of the Department of State; (C) Any organization established by international agreement and whose governing body is composed principally of representatives of national governments; or (D) Any other multilateral entity in which sovereign nations participate.” ↩︎

Number of countries represents countries that received funding directly from the U.S. government; additional countries may be reached through regional and worldwide programming. ↩︎

Includes number of foreign governments, multilaterals, and U.S. NGOs that received foreign assistance as well as the number of foreign NGOs that received non-health assistance only. ↩︎

Program support is “general management support required to ensure completion of U.S. foreign assistance objectives by facilitating program management, accounting and tracking for costs” according to the State Department, Standardized Program Structure and Definitions (SPSD) [Updated Foreign Assistance Standardized Program Structure and Definitions], June 2017, uploaded Feb. 2023, available at: https://www.state.gov/wp-content/uploads/2023/02/The-New-SPSD-June-2017-Accessible-2.16.2023.pdf. ↩︎

Virtually all enrollees in Medicare Advantage (99%) are required to obtain prior authorization for some services – most commonly, higher cost services, such as inpatient hospital stays, skilled nursing facility stays, and chemotherapy. This contrasts with traditional Medicare, where only a limited set of services, including certain outpatient hospital services, non-emergency ambulance transport, and durable medical equipment, require prior authorization (see Box 1). Insurers often use prior authorization requirements to assess whether health care services are medically necessary before they are covered and to reduce unnecessary costs. At the same time, prior authorization processes and requirements, including the use of artificial intelligence to review requests, may result in administrative hassles for providers, delays for patients in receiving necessary care, and in some instances, denials of medically necessary services, such as post-acute care.

Prior authorization practices have gotten a fair amount of attention in recent years. KFF polling shows that most people view delays and denials of care by health insurance companies as a problem, with about two-thirds of Medicare beneficiaries reporting that they consider it to be a major problem. Last summer, the Trump Administration announced that private health insurers, including those that comprise a majority of Medicare Advantage enrollment, agreed to a voluntary initiative to improve the prior authorization process. Lawmakers in Congress have also been active on the issue, with bipartisan legislation introduced in both the House and Senate. Additionally, on January 1, 2026, the Administration launched the Wasteful and Inappropriate Spending Reduction (WISeR) model to test the use of enhanced technology to conduct prior authorization for an additional set of select services in traditional Medicare in six states.

This analysis uses data submitted by Medicare Advantage insurers to the Centers for Medicare and Medicaid Services (CMS) to examine the trends in the number of prior authorization requests, denials, and appeals for 2019 through 2024, as well as differences across Medicare Advantage insurers with the largest enrollment. It does not include requests or denials by type of service or type of plan because CMS does not collect or report this information, though such data could help inform consumers in choosing among plans. It also presents data from CMS about the use of prior authorization in traditional Medicare, including the number of requests and denials for fiscal years 2021 through 2024.

Key Takeaways

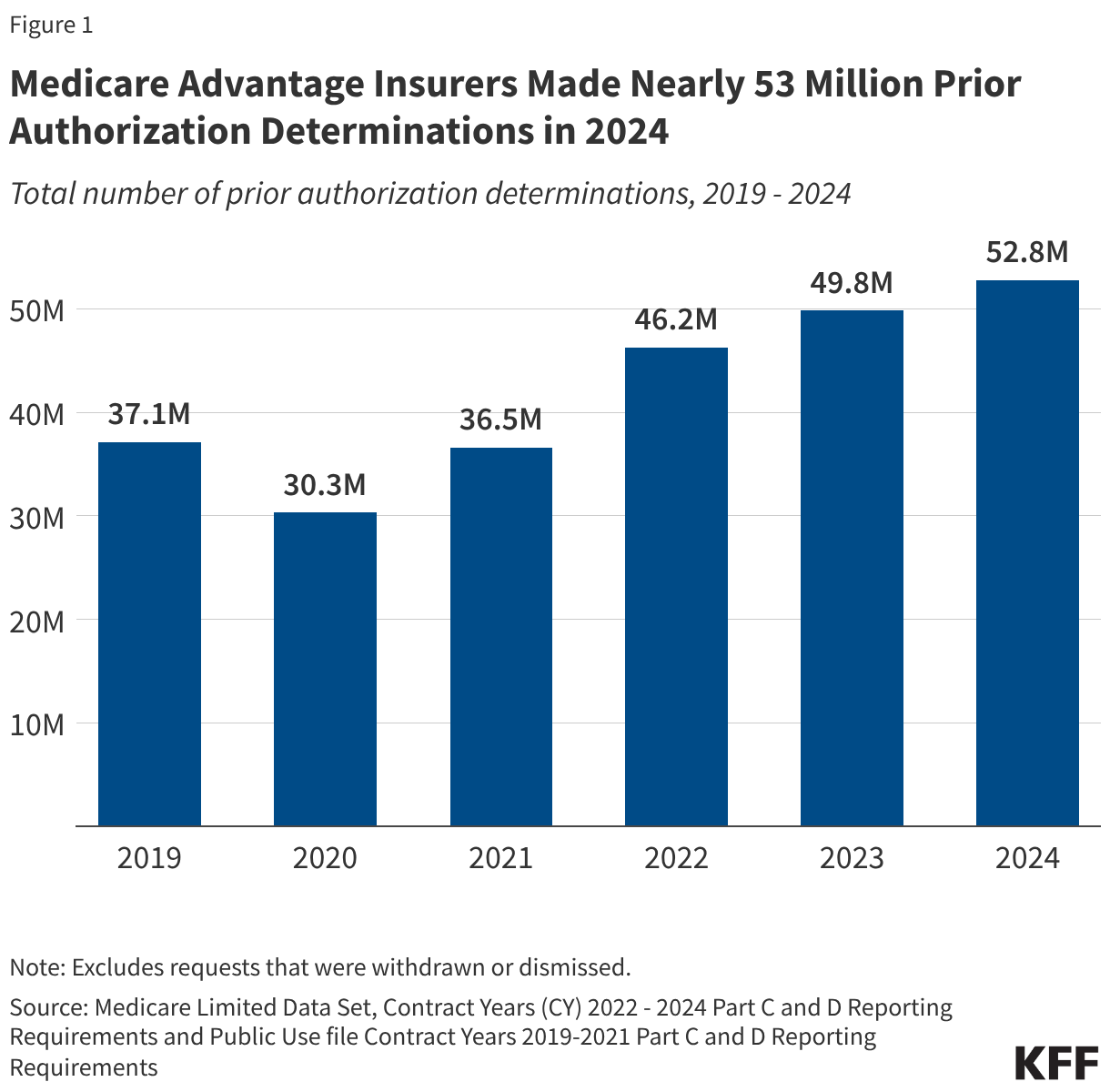

Nearly 53 million prior authorization requests were submitted to Medicare Advantage insurers on behalf of Medicare Advantage enrollees in 2024, an increase from 2023 (49.8 million) as the number of people enrolled in Medicare Advantage has grown. Substantially fewer prior authorization requests for traditional Medicare than Medicare Advantage beneficiaries were submitted to CMS – just over 625,000 in fiscal year 2024.

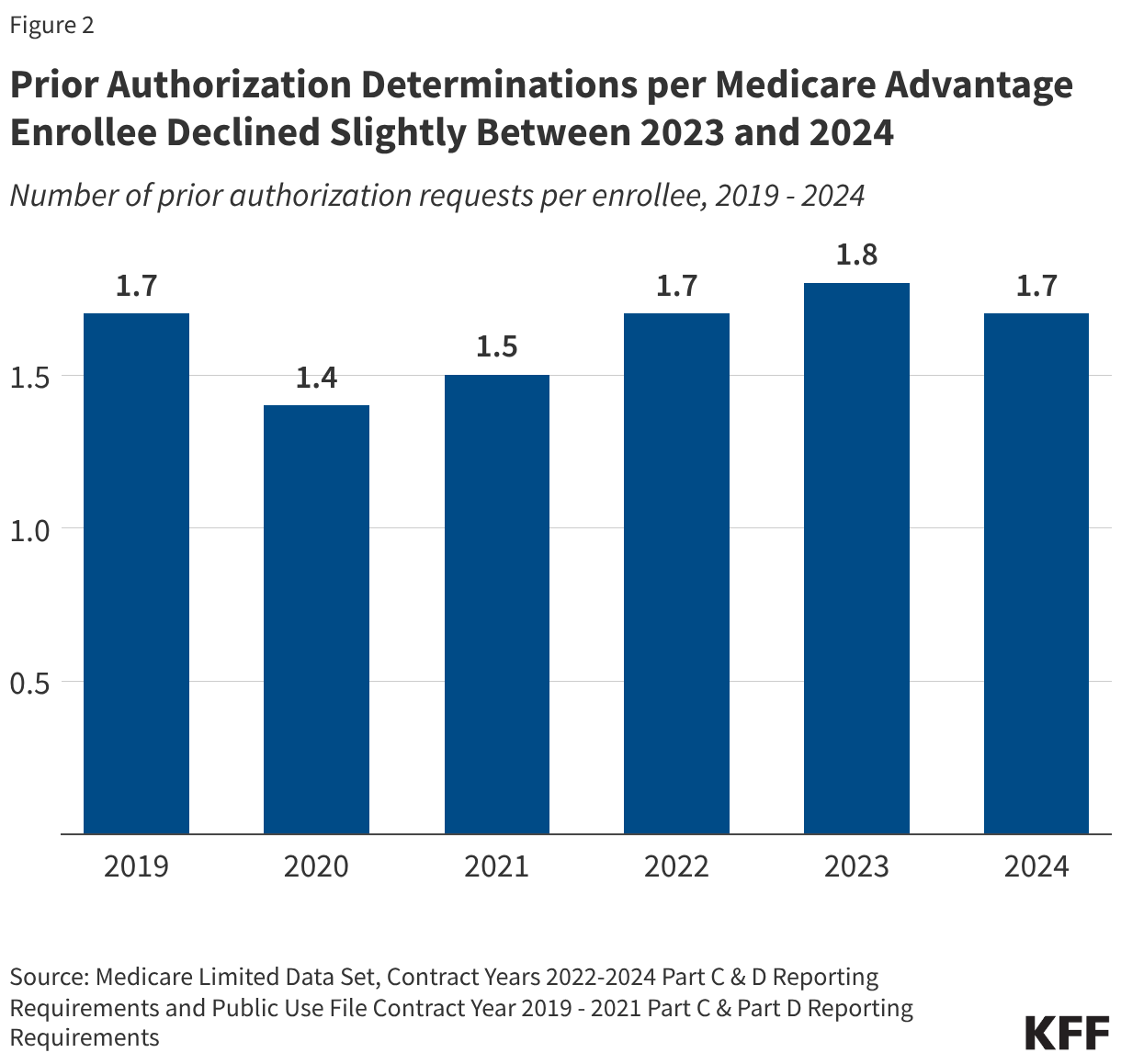

In 2024, there were 1.7 prior authorization requests on average per Medicare Advantage enrollee, a slight decline from 1.8 in 2023. In contrast, in 2024, about 2 prior authorization requests were submitted per 100 traditional Medicare beneficiaries – a rate of about 0.02 per enrollee – which reflects the limited set of services subject to prior authorization in traditional Medicare.

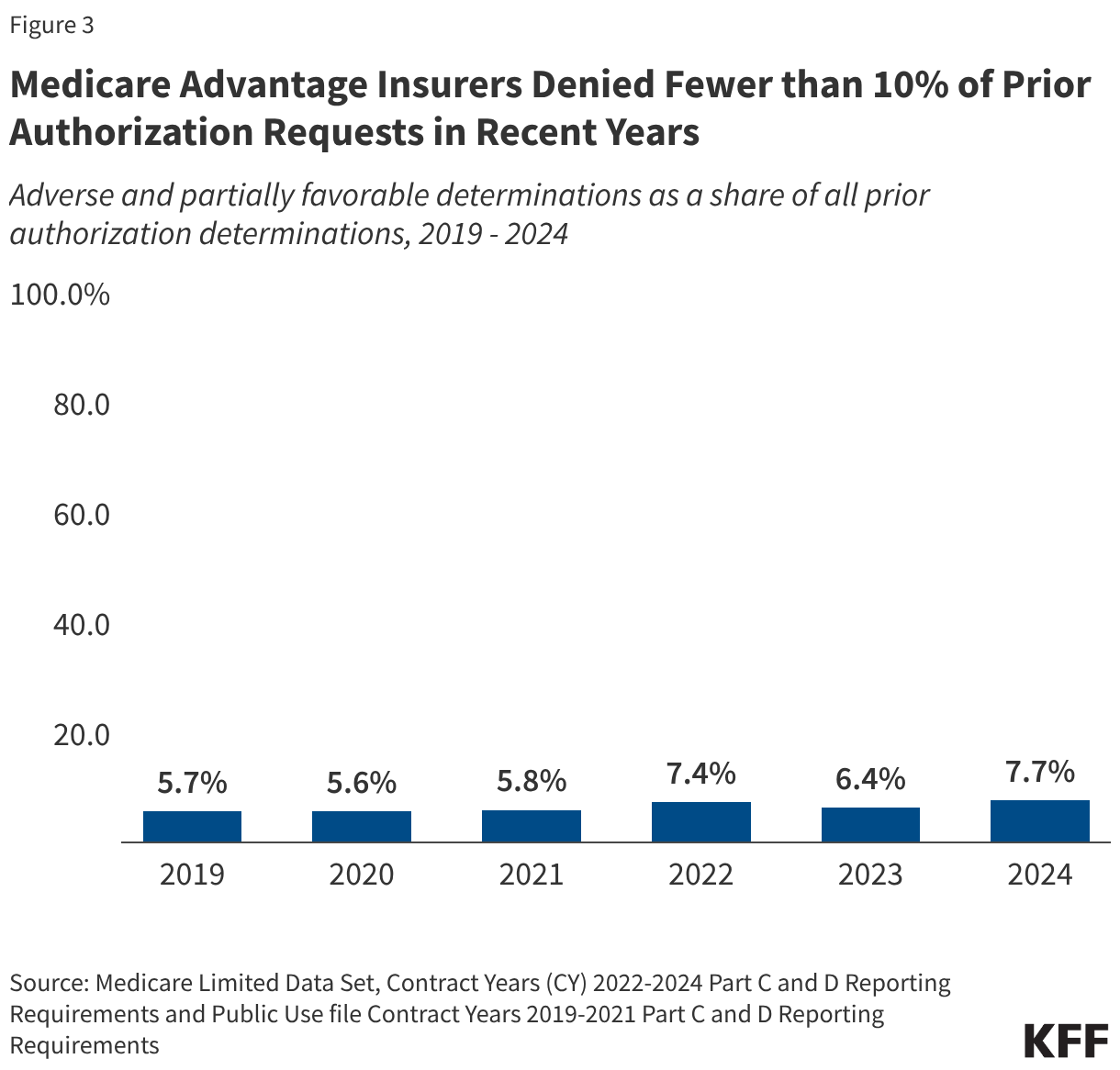

In 2024, Medicare Advantage insurers fully or partially denied 4.1 million prior authorization requests, which is a somewhat larger share (7.7%) of all requests than in 2023 (6.4%) and similar to 2022 (7.4%). Though there were substantially fewer prior authorization requests for traditional Medicare beneficiaries, a larger share was denied – 22.9% (less than 150,000) in 2024.

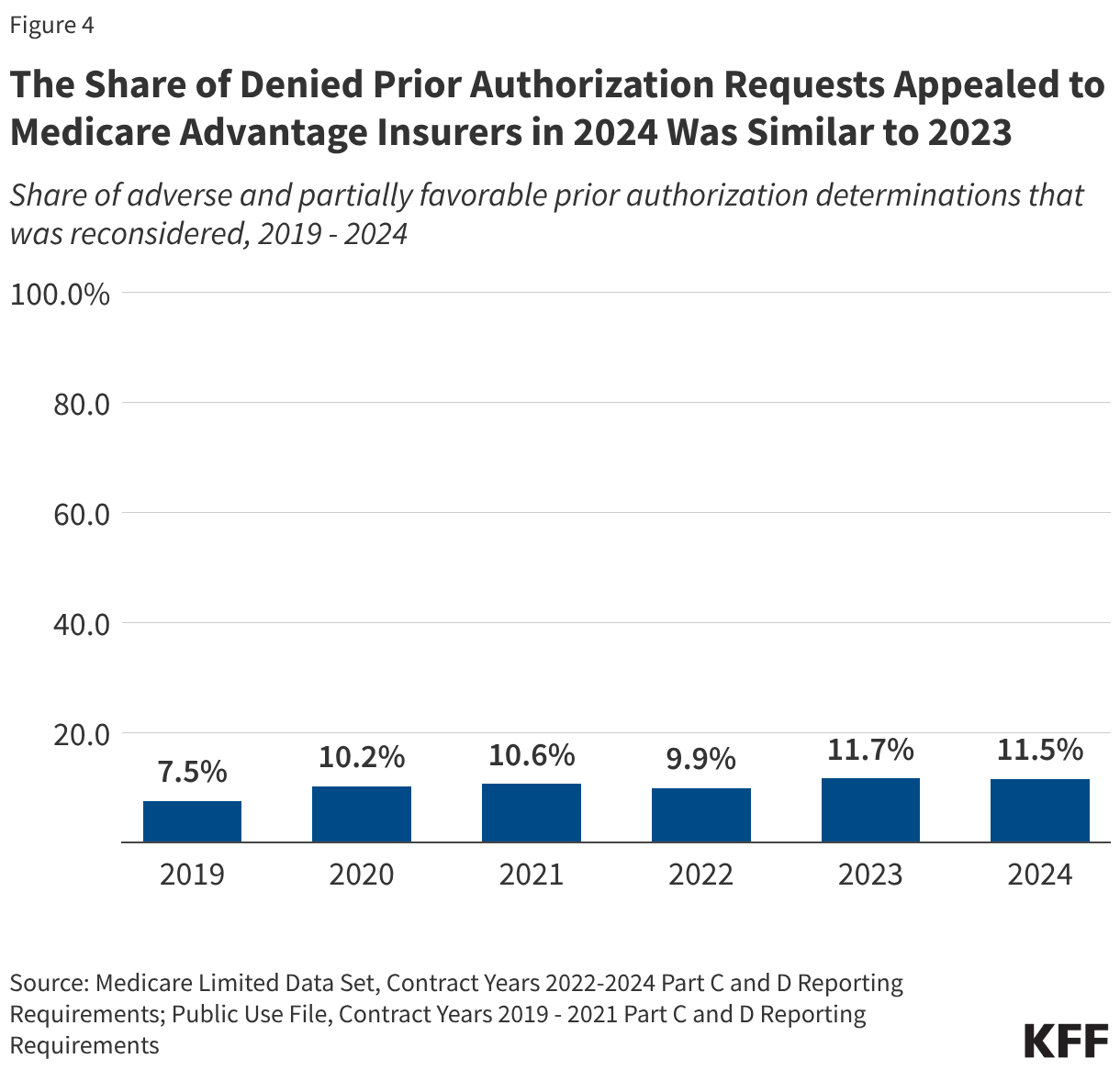

A small share of denied prior authorization requests was appealed in Medicare Advantage –11.5% in 2024, similar to 2023 (11.7%).That represents an increase since 2019, when 7.5% of denied prior authorization requests in Medicare Advantage were appealed. The traditional Medicare data do not include information on appeals for 2023 and 2024, but in 2022 a relatively small share of denied prior authorization requests was appealed in traditional Medicare (6.4% in 2022).

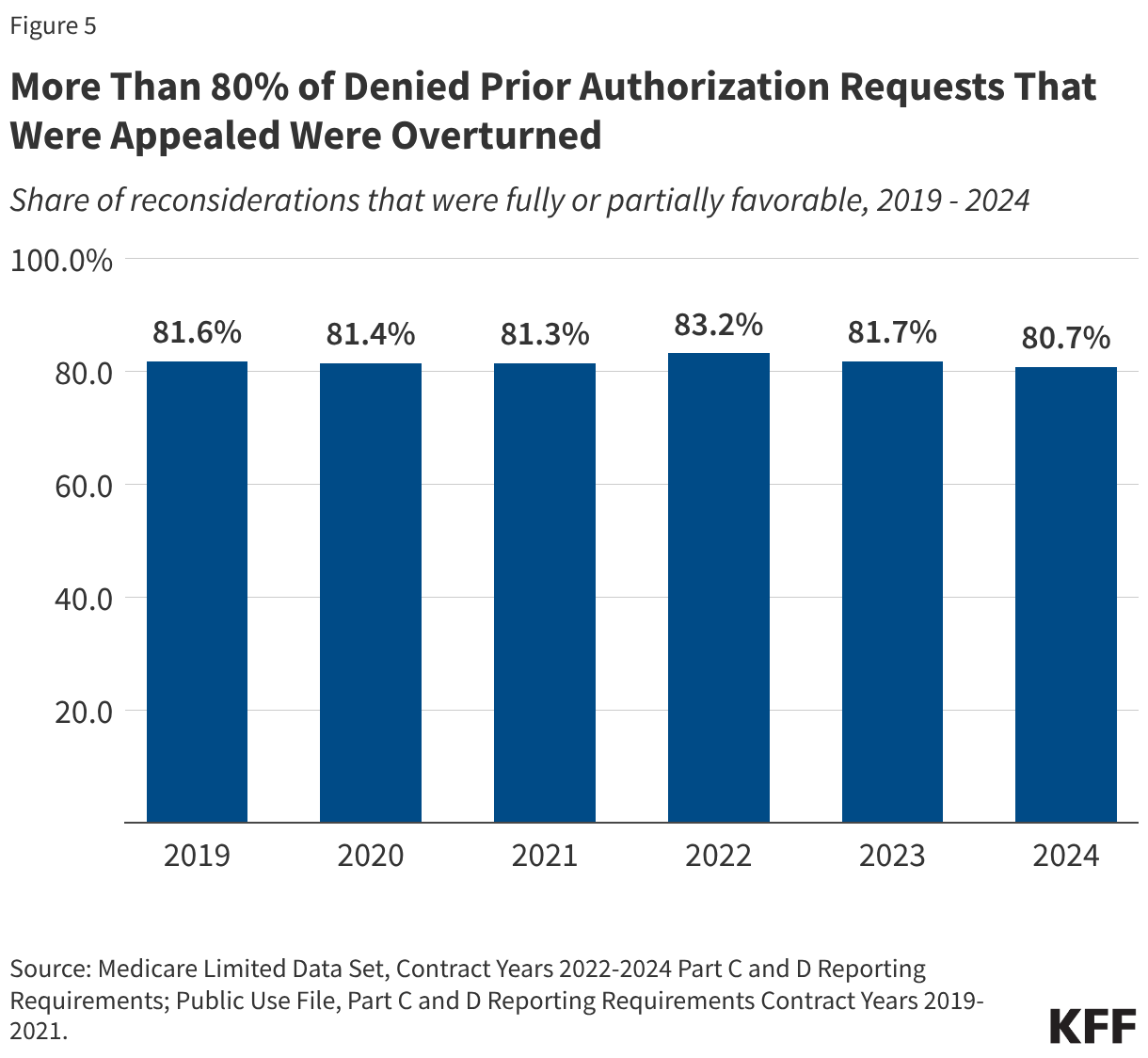

Though a small share of prior authorization denials were appealed to Medicare Advantage insurers, most appeals (80.7%) were partially or fully overturned in 2024. Across all years examined, more than eight in ten appeals overturned the initial denial. These requests represent medical care that was ordered by a health care provider and ultimately deemed necessary but was potentially delayed because of the additional step of appealing the initial prior authorization decision. Such delays may have negative effects on a patient’s health.

Use of Prior Authorization in Medicare Advantage

CMS requires Medicare Advantage insurers to submit data for each Medicare Advantage contract (which usually includes multiple plans) as part of its oversight of Medicare Advantage plans. Insurers are required to submit the number of prior authorization determinations made during a year and whether the request was approved. Insurers are additionally required to report the number of initial decisions that were appealed (reconsiderations) and the outcome of that process, including whether the initial decision was affirmed, partially overturned, or fully overturned. These data are useful for assessing overall trends and variations across insurers, but do not contain the information necessary to understand how the use of prior authorization varies by type of service or type of plan because they are aggregated to the contract level. CMS is implementing a pilot program to collect more detailed data at the plan and service level this year, which would help assess whether some enrollees bear a higher burden of prior authorization requirements or are more frequently denied requested services. CMS states that it anticipates expanding the requirement to all plans in 2027.

In 2024, nearly 53 million prior authorization requests were submitted to Medicare Advantage insurers.

After dropping in 2020 amid the initial phase of the COVID-19 pandemic, prior authorization requests increased steadily between 2021 and 2024 (Figure 1). The decline in 2020 was likely due to both a decline in utilization, as well as the option for insurers to temporarily pause prior authorization requirements during the public health emergency.

The increase in the total number of prior authorization requests since 2020 corresponds to an increase in Medicare Advantage enrollment. Between 2019 and 2024, the number of Medicare Advantage enrollees rose from 22 million people to 33 million people. Therefore, the number of prior authorization requests per enrollee has remained relatively constant in the past few years. In 2019, there were approximately 1.7 prior authorization requests per Medicare Advantage enrollee. That number dropped at the onset of the COVID-19 pandemic to 1.4 in 2020 and 1.5 in 2021, before returning to the pre-pandemic level of 1.7 requests per enrollee in 2022 and rising slightly to 1.8 in 2023. In 2024, Medicare Advantage enrollment growth outpaced the increase in the number of prior authorization requests, leading to a slight drop in the number of requests per enrollee to 1.7 (Figure 2).

The modest decline in the number of prior authorization determinations per enrollee corresponds with increased regulatory attention to prior authorization in Medicare Advantage which clarified the criteria that may be used by Medicare Advantage plans to establish prior authorization policies. In addition, certain Medicare Advantage insurers also announced changes to prior authorization practices in 2023 and 2024, such as UnitedHealth Group’s decision to reduce the number of services subject to prior authorization and launch a national “gold card” program that exempts certain providers from prior authorization requirements.

Medicare Advantage insurers denied 4.1 million (7.7%) prior authorization requests in 2024.

Of the 52.8 million prior authorization determinations in 2024, more than 90% (48.7 million) were fully favorable, meaning the requested item or service was approved in full. However, the remaining 4.1 million prior authorization requests (7.7%) were denied in full or in part by Medicare Advantage insurers. This is slightly higher than the 6.4% of requests that were denied in 2023 and similar to the share denied in 2022 (Figure 3). Across all years, most denials (73% in 2024, data not shown) were denied in full, while a minority of denials were determined to be partially favorable, meaning that only part of the request was approved. For example, the insurer may have approved 10 of 14 requested therapy sessions.

Just 11.5% of denied prior authorization requests were appealed to Medicare Advantage insurers in 2024.

As in previous years, the majority of the 4.1 million denied prior authorization requests were not appealed. Though the share of denied requests that are appealed is small at just 11.5%, similar to the share in 2023 (11.7%), it has risen over time, from 7.5% in 2019 (Figure 4). These include appeals of claims that were both fully and partially denied.

The vast majority of denied prior authorization requests that were appealed were subsequently overturned by Medicare Advantage insurers.

In each year from 2019 through 2024, more than eight in ten denied prior authorization requests that were appealed were overturned (Figure 5). This raises questions about whether the initial request should have been approved, although it could also indicate that the initial request was missing the required documentation to justify the service. In either case, patients potentially faced delays in obtaining services that were ultimately approved because of the prior authorization process.

Variation in Use of Prior Authorization Across Medicare Advantage Insurers in 2024

In 2024, the volume of prior authorization determinations varied across Medicare Advantage insurers, as did the share of requests that were denied, the share of denials that were appealed, and the share of decisions that were overturned upon appeal, meaning people may have different experiences depending on the Medicare Advantage plan in which they enroll.

Across most insurers, fewer prior authorization requests per enrollee were correlated with a higher share of requests being denied and vice versa. For example, prior authorization requests for UnitedHealth Group Inc. and Humana Inc., the two largest Medicare Advantage insurers, were among the lowest (UnitedHealth Group Inc., 1.0 requests per enrollee) and the highest (Humana Inc., 2.2 requests per enrollee) observed, and correspondingly, denial rates were above average (UnitedHealthcare, 12.8%) and below average (Humana, 5.8%) for these insurers.

While all Medicare Advantage insurers require prior authorization for at least some services, there is variation across insurers and plans in the specific services that are subject to these requirements. In addition, some insurers waive prior authorization requirements for certain providers, for example, as part of risk-based contracts or through “gold carding” programs that exempt providers with a history of complying with the insurer’s prior authorization policies.

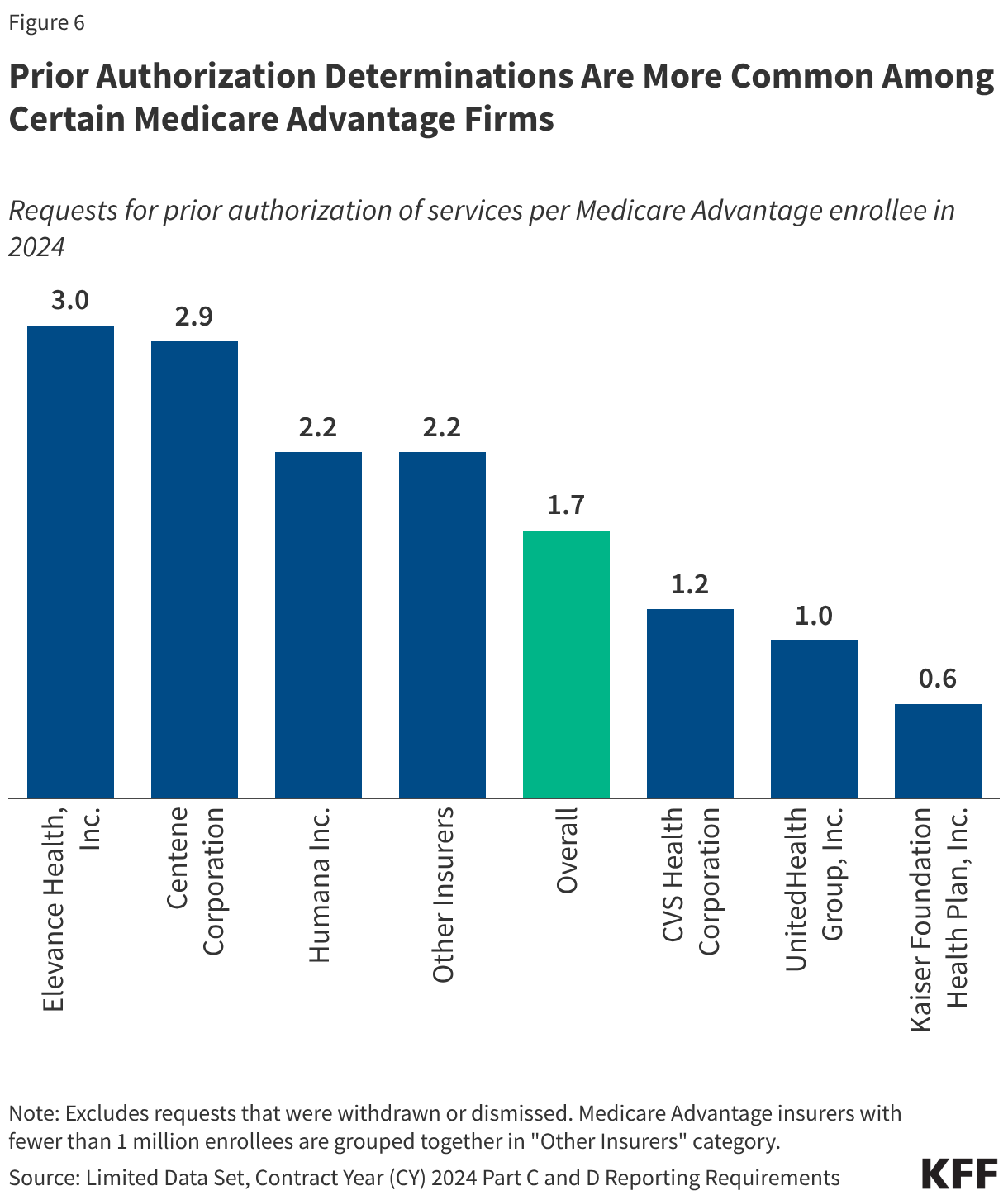

Prior authorization requests were most common among Elevance and Centene plans.

The number of prior authorization requests per enrollee ranged from a low of 0.6 requests per enrollee in plans sponsored by Kaiser Foundation Health Plan, Inc. to a high of 3.0 requests per enrollee in Elevance Health, Inc. and Centene Corporation plans (Figure 6). Kaiser is atypical among insurers in that it generally operates its own hospitals and contracts with an affiliated medical group. Looking across other insurers that are more similar, the low end of the range was 1.0 prior authorization requests per enrollee in UnitedHealth Group, Inc. plans. Differences across Medicare Advantage insurers in the number of prior authorization requests per enrollee likely reflect some combination of differences in the services subject to prior authorization requirements, the frequency with which contracted providers are exempted from those requirements (which may be related to the extent to which providers are affiliated with the insurer), how onerous the prior authorization process is for a particular insurer relative to others, and differences in enrollees’ health conditions and the health care services they use.

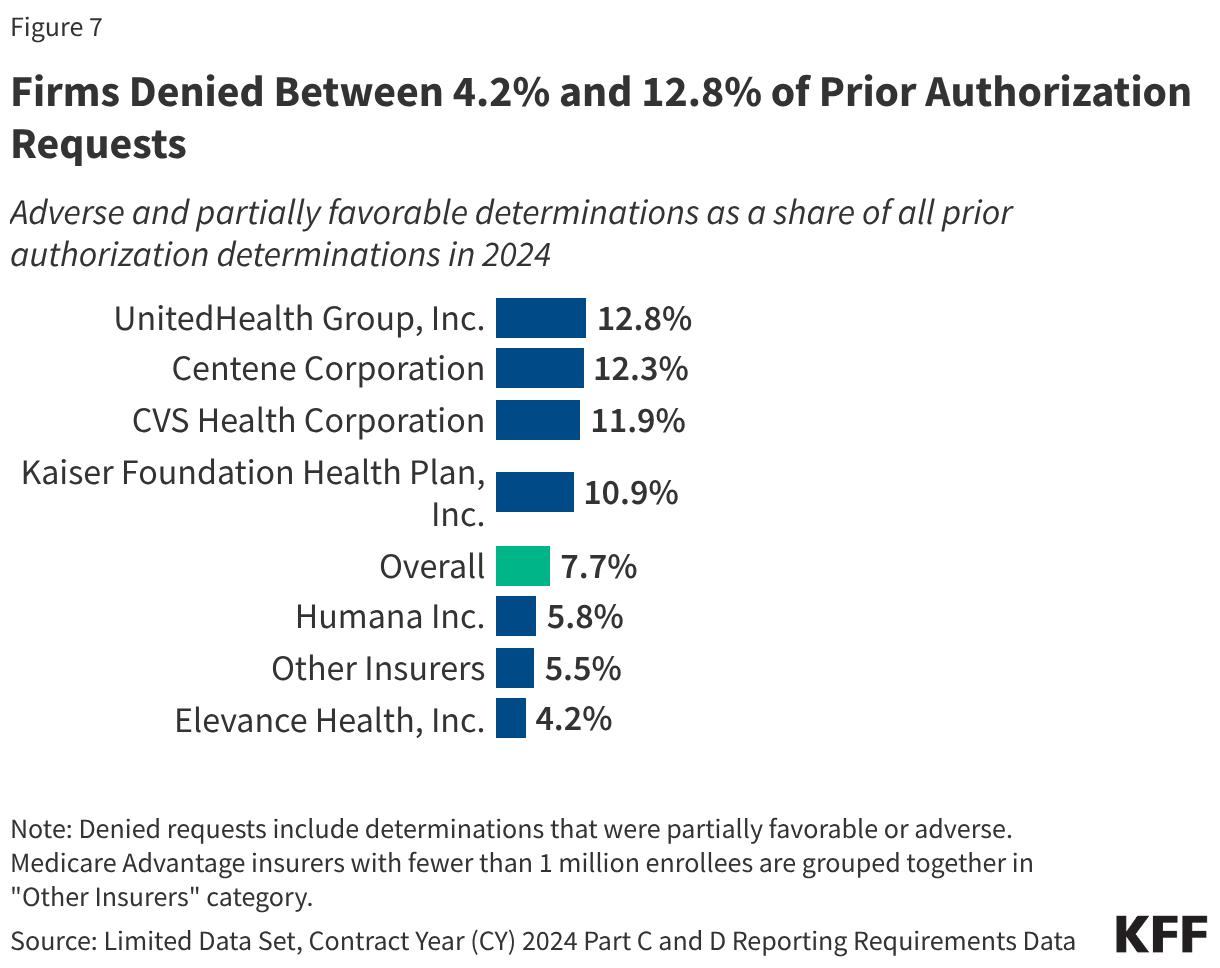

UnitedHealth Group denied the highest share of prior authorization requests while Elevance denied the fewest.

The denial rate ranged from 4.2% of prior authorization requests for Elevance Health plans to 12.8% of prior authorization requests for UnitedHealth Group plans (Figure 7). The overall denial rate includes requests that were both fully and partially denied (adverse and partially favorable determinations, respectively).

Most insurers that had more prior authorization requests per enrollee than average denied a smaller share of those requests than average, such as Elevance Health, which had 3.0 prior authorization requests per enrollee and a denial rate of 4.2%. Conversely, insurers with fewer prior authorization requests per enrollee denied a higher share of those requests, such as UnitedHealth Group, which had 1.0 prior authorization requests per enrollee and a denial rate of 12.8%. Centene Corporation was an exception with both a relatively high number of prior authorization requests (2.9 per enrollee) and a relatively high denial rate (12.3%).

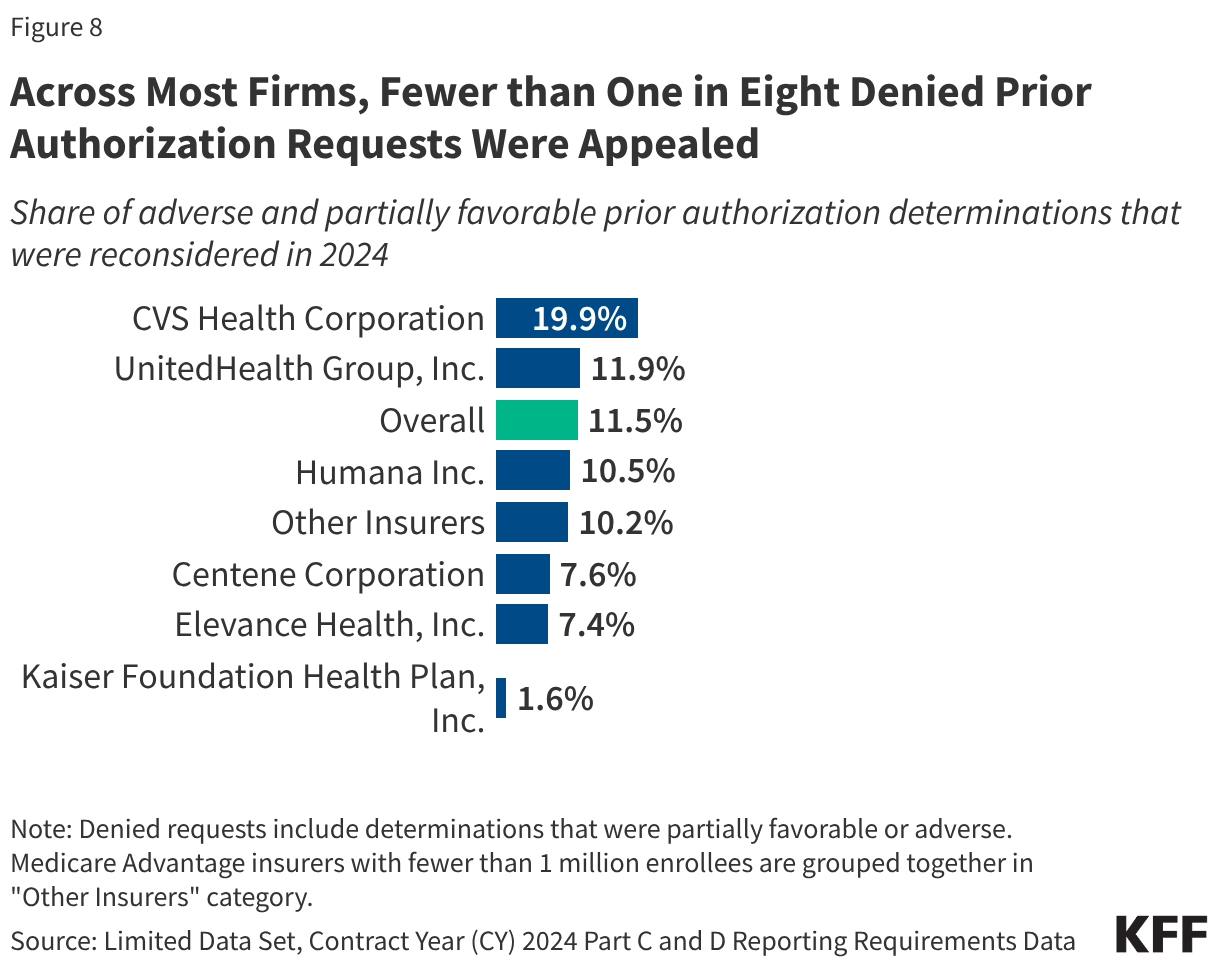

Across all insurers, a small share of denials was appealed.

Most denied prior authorization requests are not appealed to the Medicare Advantage insurer. The shares ranged from 1.6% for Kaiser Foundation Health Plan to 19.9% for CVS Health Corporation, with the appeal of fewer than one in twelve denials across all insurers except CVS Health Corporation (Figure 8).

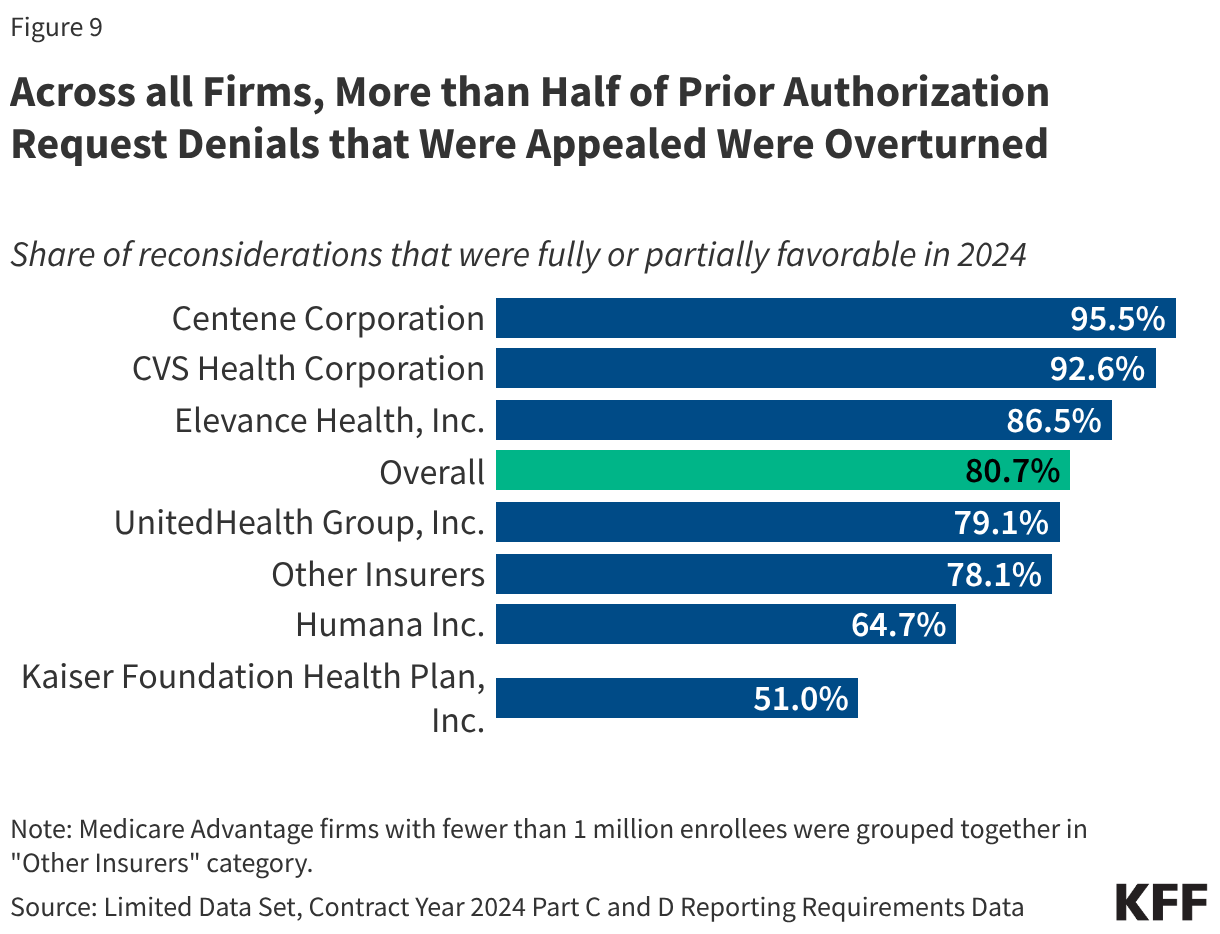

Across all firms, more than half of appeals were successful.

Even though most denials were not appealed, when they were, most of the initial decisions were partially or fully overturned. The share of appeals that resulted in favorable decisions overturning the initial denial was lowest for Kaiser Foundation Health Plan (51.0%) and highest for Centene Corporation (95.5%) (Figure 9), which also had the second highest share of requests initially denied.

The Use of Prior Authorization in Traditional Medicare

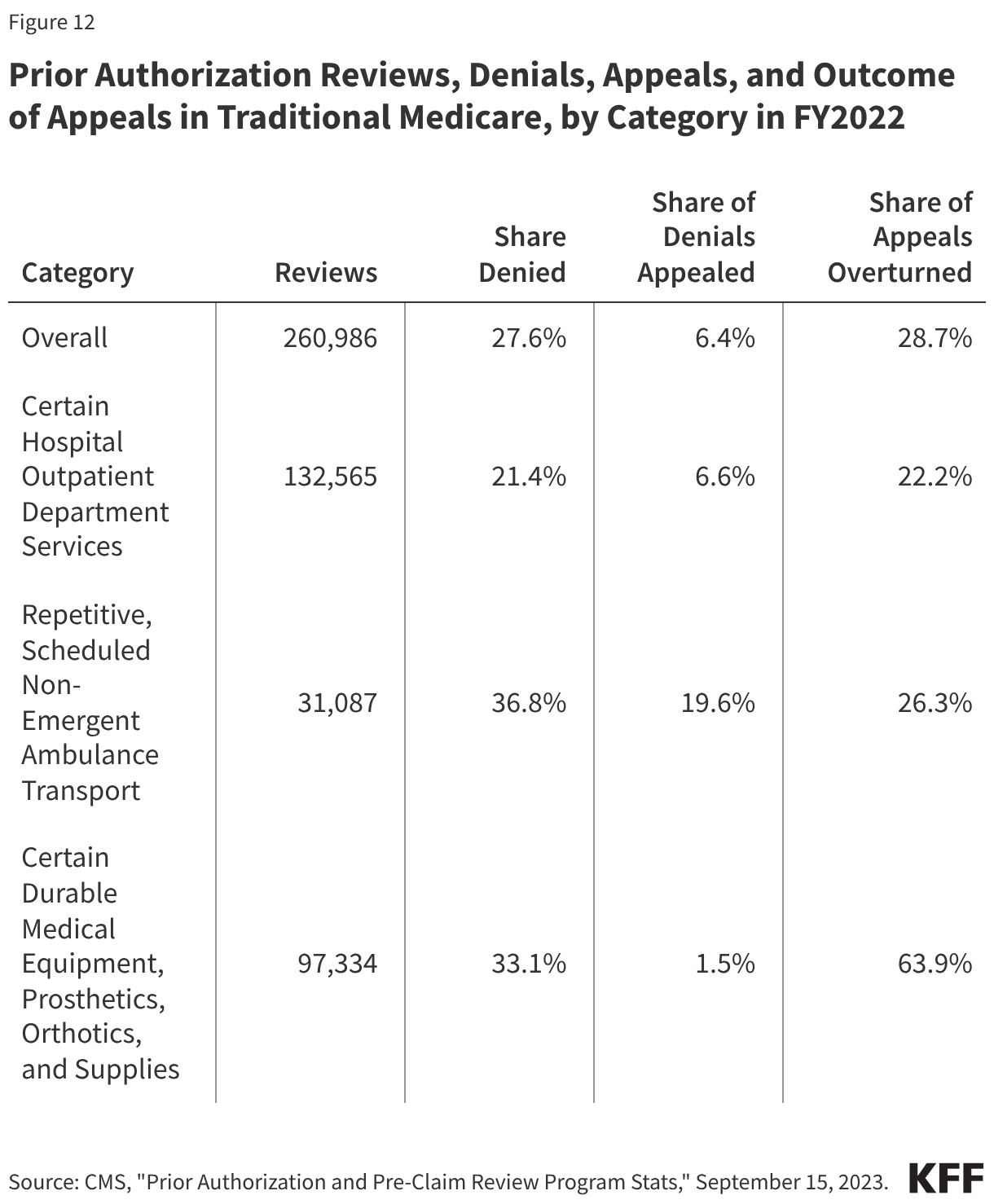

The use of prior authorization is relatively new to traditional Medicare and only used for a limited set of services, including certain outpatient hospital services, non-emergency ambulance transport, and durable medical equipment (see Box 1). The prior authorization process does not change any documentation requirements that are necessary for receiving Medicare payment – the confirmation that coverage requirements are met are required earlier in the review process. CMS has published reports presenting data on the use of prior authorization in traditional Medicare for fiscal years 2021, 2022, 2023, and 2024. These reports include information on the number of requests received, reviews completed, and the number and share of requests that were affirmed. For 2021 and 2022 only, the data also include information on appeals and the outcome of the appeal.

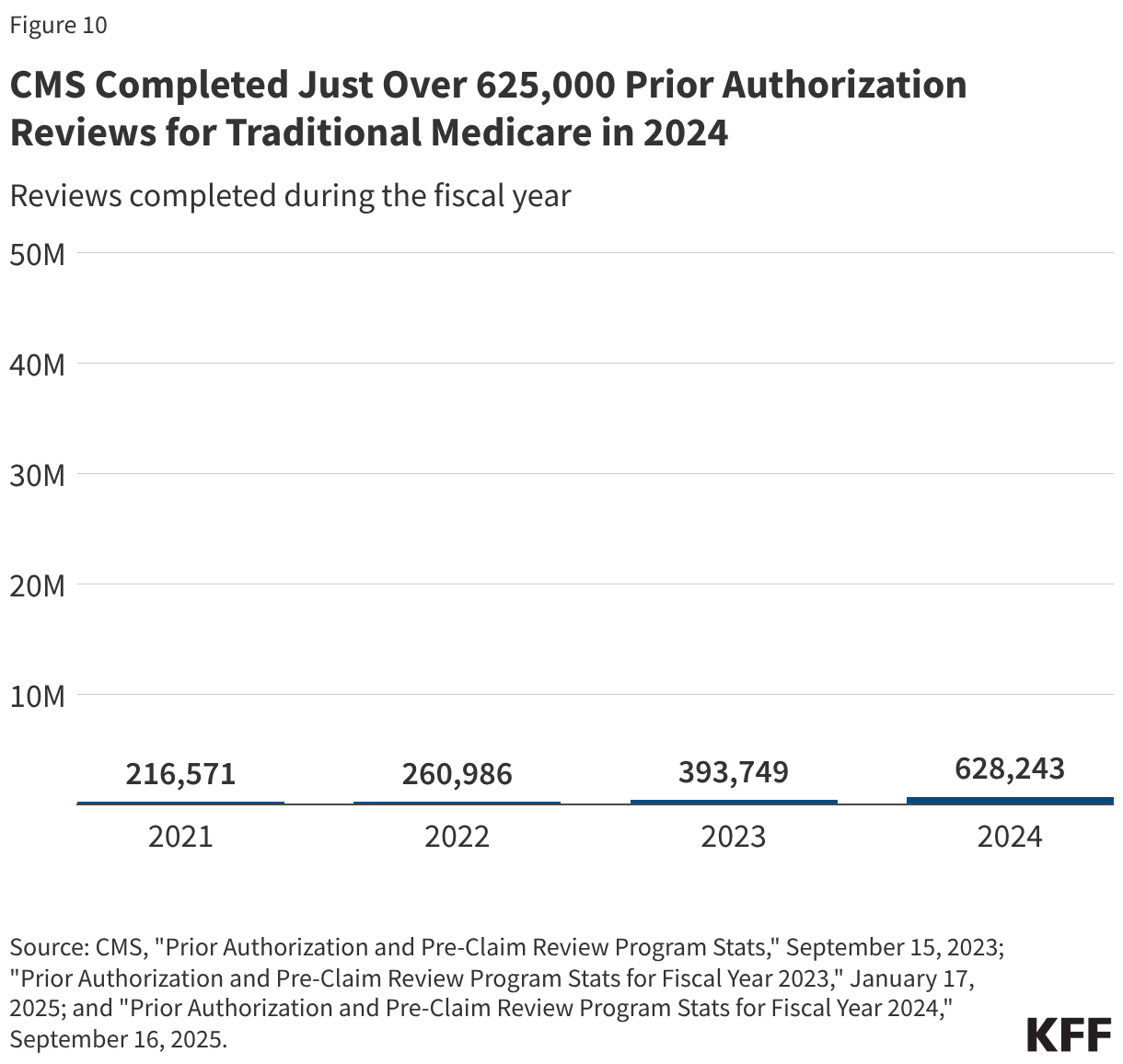

Just over 625,000 prior authorization reviews were completed by CMS for traditional Medicare in 2024.

Across the three categories of services that required prior authorization, there were 216,571 reviews completed in 2021, 260,986 reviews completed in 2022, 393,749 reviews completed in 2023, and 628,243 reviews completed in 2024 (Figure 10). This translates to about 2 prior authorization reviews per 100 traditional Medicare beneficiaries in 2024.

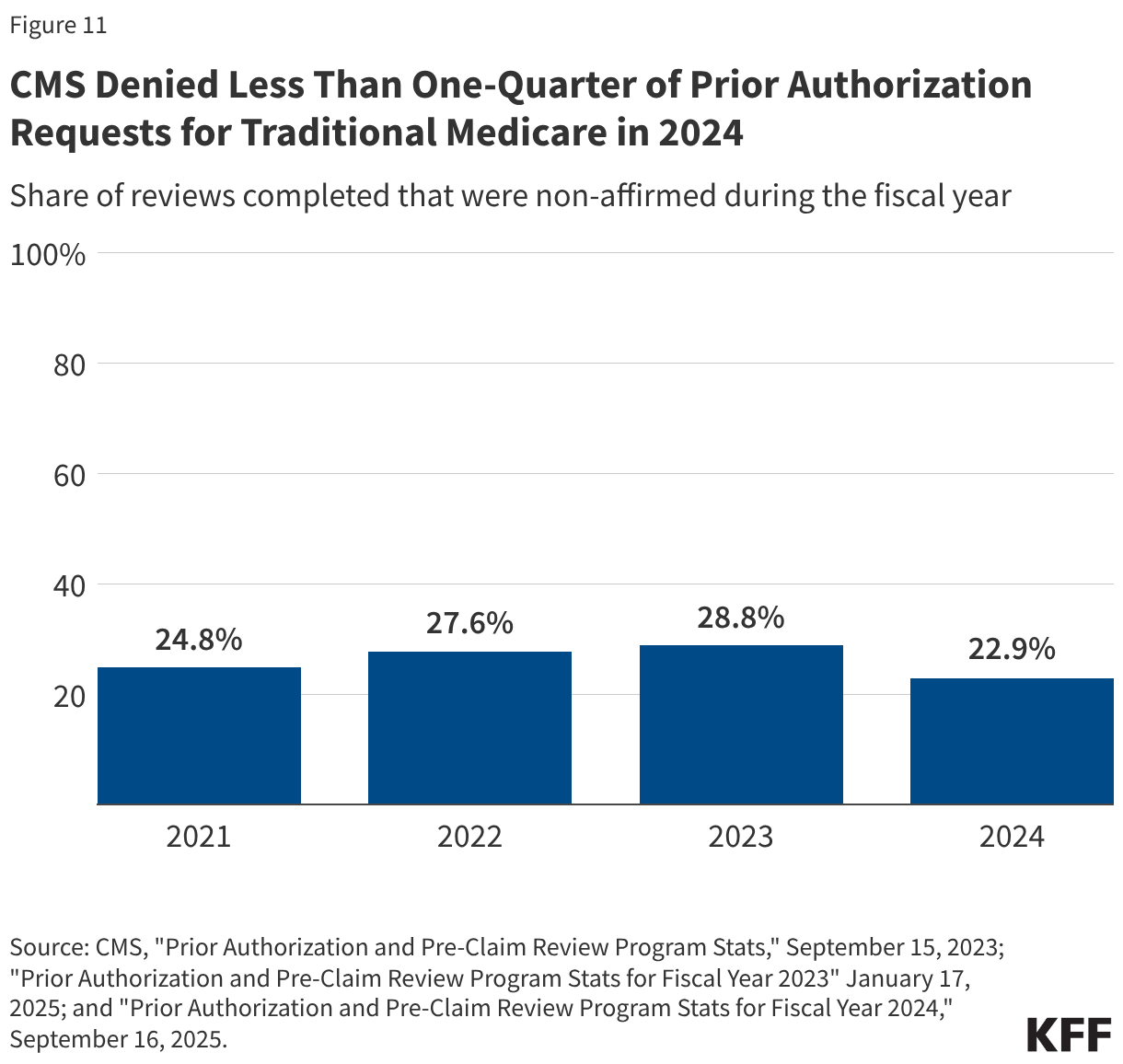

Less than one-quarter of prior authorization requests in traditional Medicare were denied.

CMS approved (or affirmed) the majority of prior authorization requests it reviewed. CMS reported that 24.8% of requests were denied (or non-affirmed) in 2021, 27.6% of requests were denied in 2022, 28.8% of requests were denied in 2023, and 22.9% of requests were denied in 2024 (Figure 11). This reflects 53,680 denied requests in 2021, 72,029 denied requests in 2022, 113,448 denied requests in 2023, and 143,705 denied requests in 2024.

In traditional Medicare, a small share of denied prior authorization requests was appealed to CMS and the share of prior authorization requests that were appealed and overturned upon appeal varied across service type.

In 2022, fewer than 5,000 denied prior authorization requests in traditional Medicare were appealed to the first level. As a share of all denied requests that translates to 6.4% appealed in 2022. Of the denied requests, 1,323 prior authorization denials were overturned upon appeal, which represents 28.7% of all first level appeals (Figure 12). Appeals data in traditional Medicare are presented differently across the CMS reports. Specifically, the 2023 and 2024 reports include a separate claims and appeals section for each category of service, which appears to include a broader universe of reviews by Medicare Administrative Contractors, including those for payment of services rendered, than what is presented in the report for 2021 and 2022. Given the differences in the data reported, we present appeals and whether the decision was overturned on appeal for 2022 only.

Denied requests for the ambulance transport services were most often appealed (19.6%); just 6.6% of denials for certain hospital outpatient services and 1.5% of certain durable medical equipment, prosthetics, orthotics and supplies requests were appealed.

The share of appeals that resulted in overturning the initial decision also varied widely. Nearly two-thirds (63.9%) of appeals for durable medical equipment, prosthetics, orthotics and other supplies were successful. That compares to 26.3% of appeals for the ambulance transport services and 22.2% of appeals for certain hospital outpatient services.

Box 1: Prior Authorization Requirements in Traditional Medicare

In 2015, CMS issued a final rule that established a prior authorization process for certain Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) items, with the goal of reducing the use of items that had been frequently subject to unnecessary utilization. Initial implementation began March 20, 2017, and items have been added and subtracted to the list over the following years through subsequent rulemaking. As of January 13, 2026, the DMEPOS items prior authorizations list includes over 70 items, including for pressure reducing support surfaces, power mobility devices, and lower limb prosthetics. Additionally, in December 2025, CMS issued a rule which establishes a prior authorization exemption process for certain DMEPOS items, allowing qualifying suppliers, such as those who show an affirmation rate of 90% or higher, to be exempt from prior authorization.

In a 2019 final rule (effective July 1, 2020), CMS established national prior authorization requirements for a set of hospital outpatient department services which had experienced significant increases in utilization and that are likely to be cosmetic procedures and not covered by Medicare, but may be combined with other therapeutic services, including blepharoplasty, botulinum toxin injections, panniculectomy, rhinoplasty, and vein ablation. In further rulemaking (effective July 1, 2021), CMS added implanted spinal neurostimulators and cervical fusion with disc removal to the list of services requiring prior authorization, and another rule (effective July 1, 2023) added facet joint interventions.

On January 1, 2026, the Center for Medicare and Medicaid Innovations (CMMI) launched the Wasteful and Inappropriate Service Reduction (WISeR) Model that establishes new prior authorization requirements in traditional Medicare for select services in six states (New Jersey, Ohio, Oklahoma, Texas, Arizona, and Washington). These services include skin substitutes (synthetic products used in the treatment of severe or chronic wounds), orthopedic pain management services, electrical nerve stimulator implants, incontinence control devices, and services related to the diagnosis and treatment of impotence. According to CMS, the model will test the use of enhanced technologies, such as artificial intelligence, to conduct prior authorization for services vulnerable to fraud or abuse.

Box 2: Recent Administrative Actions and Proposed Legislation on Prior Authorization

The Administration recently finalized three rules related to prior authorization.

The first rule (effective date: June 5, 2023) issued by the Biden Administration clarifies the criteria that may be used by Medicare Advantage plans in establishing prior authorization policies and the duration for which a prior authorization is valid. Specifically, the rule states that prior authorization may only be used to confirm a diagnosis and/or ensure that the requested service is medically necessary and that private insurers must follow the same criteria used by traditional Medicare. That is, Medicare Advantage prior authorization requirements cannot result in coverage that is more restrictive than traditional Medicare. The rule also describes how private insurers may consider additional information when traditional Medicare does not have fully established coverage criteria. The rules apply to coverage beginning with plan year 2024.

The second rule (effective date: April 8, 2024) issued by the Biden Administration is intended to improve the use of electronic prior authorization processes, as well as the timeliness and transparency of decisions, and applies to Medicare Advantage and certain other insurers. Specifically, it shortens the standard time frame for insurers to respond to prior authorization requests from 14 to 7 calendar days starting in January 2026 and standardizes the electronic exchange of information by specifying the prior authorization information that must be included in application programming interfaces starting in January 2027. It also requires that beginning in 2026, insurers post all items and services subject to prior authorization and the share of prior authorization requests that were approved, denied, and approved after appeal. A bipartisan bill has also been introduced to codify pieces of this rule.

The third rule (effective date: June 3, 2024) also issued by the Biden Administration would have required Medicare Advantage plans to evaluate the effect of prior authorization policies on people with certain social risk factors (“health equity analysis”) starting with plan year 2025, but the Trump Administration announced in June 2025 that it would not enforce these requirements.

Additionally, lawmakers in Congress have introduced several bills aimed improving the prior authorization process, including codifying changes made through recent rulemaking, and requiring written clinical criteria for prior authorization requirements, which were both introduced on a bipartisan basis. Other legislation would penalize insurers when initially denied requests are overturned upon appeal too often, require plans to include prior authorization information in plan advertisements, and one proposal would prohibit the use of prior authorization altogether.

Methods

The analysis of Medicare Advantage uses organization determinations and reconsiderations – Part C data from the Centers for Medicare and Medicaid Services (CMS) Part C and D reporting requirements public use file for contract years 2019 – 2021 and the limited data set for contract years 2022 through 2024. Medicare Advantage insurers submit the required data at the contract level to CMS and CMS performs a data validation check.

Data for Medicare Advantage contracts is aggregated to the parent company level. Insurers with less than 1 million enrollees into “other insurers”.

This analysis reflects data on service determinations and does not include claims determinations (for payment for services already provided). We also do not include withdrawn or dismissed determination requests in this analysis.

The enrollment data are from the CMS Medicare Advantage enrollment file for March of each year at the contract-plan-county level. We then sum up to the contract level to merge with the determination and reconsideration data. Contract-plan-county combinations are not included if there are fewer than 11 enrollees. The traditional Medicare analysis uses data included “Prior Authorization and Pre-Claim Review Program Stats,” published by CMS on September 15, 2023, which reflects prior authorization reviews completed in fiscal years 2021 and 2022, “Prior Authorization and Pre-Claim Review Program Stats for Fiscal Year 2023,” published on January 17, 2025, and “Prior Authorization and Pre-Claim Review Program Stats for Fiscal Year 2024,” published on September 16, 2025. The total number of traditional Medicare beneficiaries is from the Medicare Monthly Enrollment Dashboard for 2021 through 2024. While CMS published data on the use of prior authorization in traditional Medicare for FY2023 and FY2024, the information for appeals are not comparable to FY2021 and FY2022 data and are therefore not included in this analysis.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

At the start of 2026, many issues are at play that could affect Medicaid coverage, financing, and access to care. Medicaid, which is administered by states within broad federal rules, provides comprehensive health and long-term care coverage to one in five low-income Americans. A more tenuous fiscal climate in 2026 coupled with implementation of the 2025 reconciliation law will put pressure on state Medicaid programs. While major legislative changes to Medicaid at the federal level are unlikely in 2026, key areas to watch include federal policy actions such as new regulations or guidance related to work requirements, implementation guidance for other components of the 2025 reconciliation law, and states’ policy actions in response to federal policy changes and state budget pressures.

Medicaid issues are likely to intersect with broader health care coverage and affordability debates, including the expiration of the enhanced premium tax credits for Affordable Care Act (ACA) coverage and efforts by the administration to control drug prices and hold insurance companies accountable, leading up to the mid-term elections in November 2026. At the federal level, these elections could affect the make-up of Congress and at the state level, they could affect control of state legislatures and governors’ offices. There will be 39 gubernatorial elections (18 incumbent governors running for reelection and 21 incumbent governors who are either term-limited or not seeking reelection).

Medicaid Coverage

In 2026, states will begin implementing Medicaid policy changes that are estimated to increase the number of people without health insurance by 7.5 million in 2034. Over half (5.3 million) of people newly uninsured from Medicaid changes would come from new work requirements for Medicaid enrollees in the ACA Medicaid expansion group or enrollees in partial expansion waiver programs (Georgia and Wisconsin) starting January 1, 2027. Beyond work requirements, the 2025 reconciliation law made other Medicaid eligibility changes, including pausing implementation of some provisions in two Biden-era eligibility and enrollment rules (that aimed to streamline complex processes), restricting Medicaid eligibility for certain lawfully-present immigrants, and requiring states to conduct more frequent eligibility redeterminations for ACA expansion adults.

States will need to make major policy decisions and systems upgrades, likely in advance of formal federal guidance, to be ready to implement work requirements in January 2027. Operationalizing new Medicaid work requirements will require changes to state eligibility systems and processes, enhanced data sharing infrastructure, and targeted enrollee outreach and education, all of which will demand staff resources and funding that will limit attention to other Medicaid priorities. The short timeline for making these changes means states will need to move forward with key decisions before formal guidance from the Centers for Medicare and Medicaid Services (CMS) may be available, increasing the risk that they will have to make adjustments to align with federal policy, which could increase costs. Despite these challenges, some states have indicated a desire to implement work requirements before the January 2027 deadline. To date, Nebraska is the first to announce it will begin enforcing federal work requirements early, starting May 1, 2026.

Federal immigration policies and state policy choices could have implications for Medicaid coverage in 2026. In addition to federal legislative changes, broader immigration policies, such as changes to the public charge rules, new agreements for CMS to share Medicaid data with Department of Homeland Security (DHS) and Immigration and Customs Enforcement (ICE), and continued public immigration enforcement activity could result in fewer legal immigrants obtaining or maintaining Medicaid coverage. In the face of increasing fiscal pressure, several states have announced they are rolling back state-funded coverage for immigrants who are not eligible for federally-funded Medicaid, which will further limit coverage options for immigrants. States may also adopt other eligibility restrictions in an effort to reduce state costs.

Medicaid Financing

Cuts to federal Medicaid spending will exacerbate the fiscal challenges states are experiencing because of slowing revenue growth and increasing spending demands. The 2025 reconciliation law made historic cuts to federal Medicaid financing, which are estimated to reduce federal Medicaid spending by $911 billion over 10 years. Although the most significant changes to federal Medicaid financing don’t take effect until October 2027 or later, some states will experience more immediate effects resulting from changes to federal requirements governing provider taxes. One of the most immediate effects is that states are prohibited from establishing any new provider taxes or increasing existing taxes. Historically, states have used provider taxes as a means of sustaining Medicaid funding in times of slowing revenue growth or increasing spending demands, but that tool is no longer available because of the new prohibition.

Some states may also face reductions to states’ budgeted revenues for 2026 because of more immediate changes to federal provider tax rules. This would occur in two types of cases:

States that had adopted new provider taxes for state fiscal year (FY) 2026 may not be able to implement those taxes if they had not done so by July 4, 2025, and

States that have implemented provider taxes with a special waiver from CMS known as a “uniformity waiver,” may need to revise their taxes as early as April 1, 2026 because of new limits on the use of such waivers (estimated to affect at least seven states including California, Illinois, Massachusetts, Michigan, Ohio, New York, and West Virginia).

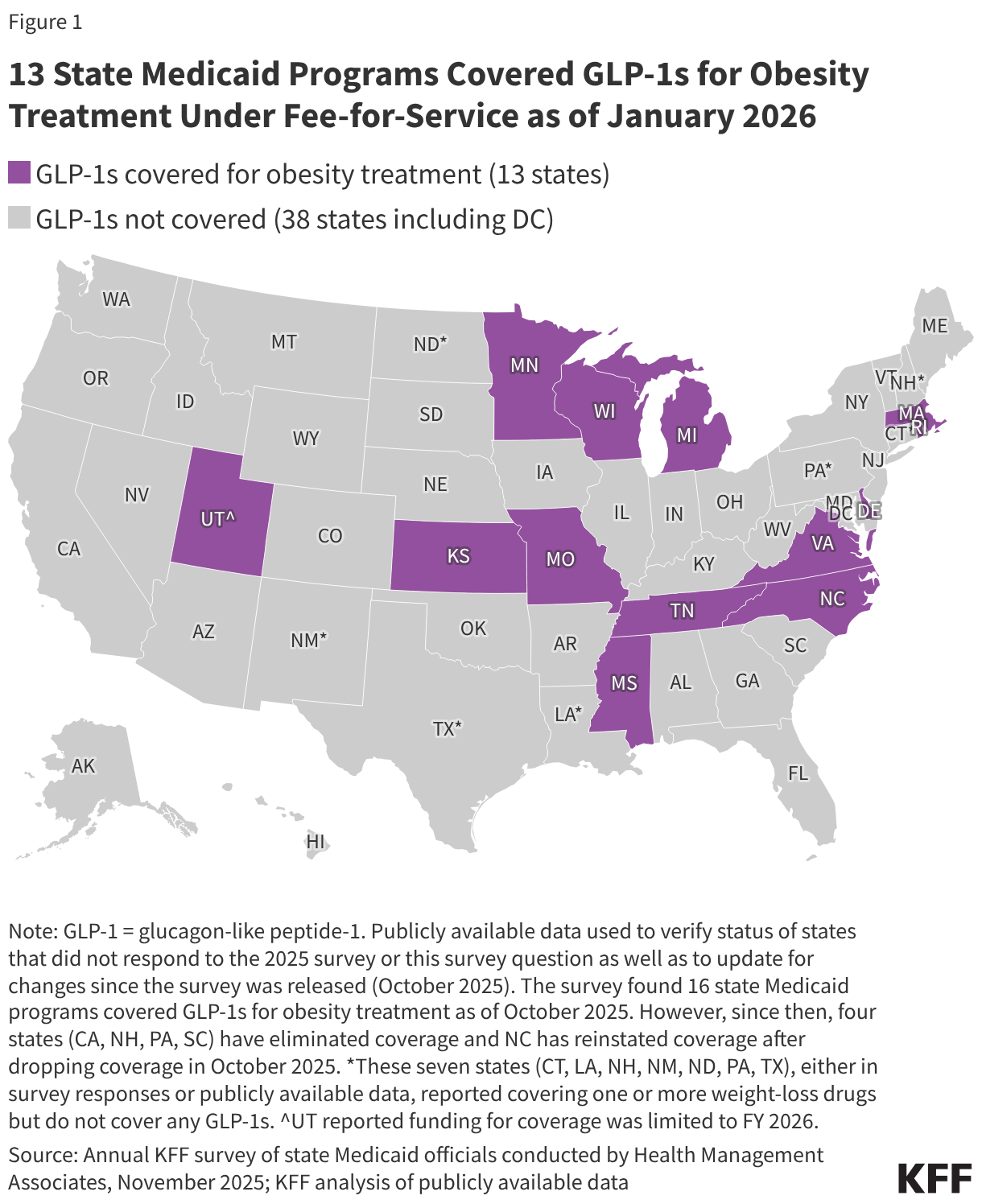

To address slowing revenue growth and increasing spending demands, states may seek to restrict Medicaid provider reimbursement rates, benefits, or eligibility to reduce state Medicaid spending. For example, four states eliminated GLP-1 coverage for obesity treatment in late 2025 likely reflecting recent state budget challenges and fiscal uncertainty. While state Medicaid programs must cover nearly all drugs, a long-standing statutory exception allows states to choose whether to cover weight-loss drugs under Medicaid, resulting in limited state coverage of GLP-1s for obesity treatment. Recent governors’ budgets have included restrictions for other Medicaid benefits including dental and home care. States’ fiscal challenges in 2026 stem from factors other than the 2025 reconciliation law, but the law may exacerbate such challenges. Beyond limiting revenues in states affected by the provider tax provisions, states will need to spend more to implement the law’s requirements, most notably the new work requirements that start January 1, 2027. While the 2025 reconciliation law included some resources to implement policy changes, states may need to make additional investments in systems or workforce to comply with multiple and complex policy changes. Because states pay less than 50% of total Medicaid costs, reductions in state funding will have even larger effects on total Medicaid spending. For example, on average, states accounted for 35% of total Medicaid spending in federal fiscal year 2024. At that rate, a decrease of $100 million in state Medicaid spending would decrease total Medicaid spending by $286 million.

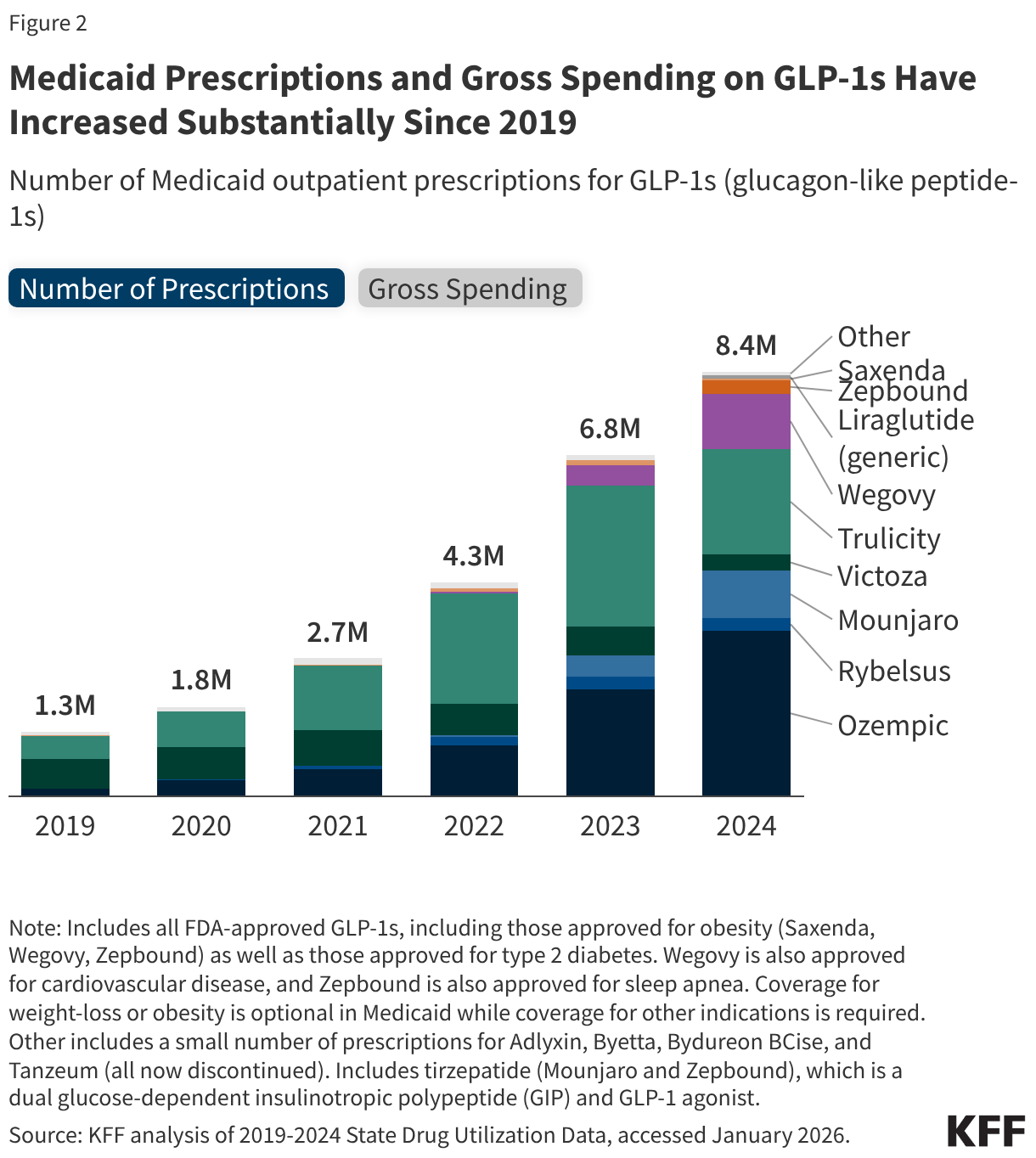

Recent Trump administration prescription drug initiatives could result in savings for state Medicaid programs, though questions remain about the implementation and impact of the deals. In fall 2025, the Trump administration announced reaching agreements with some drug manufacturers, including Pfizer and AstraZeneca, to provide most-favored nation (MFN) prescription drug pricing in Medicaid. MFN prices will be available to state Medicaid programs through the GENEROUS (GENErating cost Reductions fOr U.S. Medicaid) Model, a voluntary drug payment model through which CMS will negotiate supplemental drug rebates based on prices paid in other countries. The Trump administration also recently announced the BALANCE (Better Approaches to Lifestyle and Nutrition for Comprehensive hEalth) Model, another voluntary model that intends to expand access to obesity drugs in Medicaid and Medicare by negotiating lower GLP-1 prices with manufacturers. While lower prices for state Medicaid programs through the recently announced models could result in reduced Medicaid prescription drug spending and potentially expanded coverage of obesity drugs, how the new lower costs under the models compare to the net prices state Medicaid programs currently pay and how states or manufacturers will respond remain unclear. Due to the design of the Medicaid Drug Rebate Program (MDRP), Medicaid programs already typically pay lower prices, net of rebates, than other payers. Further, the recent announcements will not impact costs for Medicaid enrollees as they already pay little or no copays for prescription drugs.

Medicaid Access to Care

State decisions to restrict provider reimbursement rates or benefits in response to federal Medicaid spending cuts could limit access to care for some Medicaid enrollees in 2026. Changes to Medicaid financing will make it difficult for states to increase payment rates to providers and may create pressure for states to restrict payment rates. Reduced or stagnant payment rates to providers coupled with rising costs and increases in the number of people who are uninsured (from Medicaid and Marketplace coverage changes) could pressure providers to reduce staff, services or potentially close. Some providers already struggling financially, such as rural hospitals or hospitals serving a high share of Medicaid enrollees, could face more challenges. An influx of funding from the Rural Health Transformation Program may help to mitigate some challenges in the near term, but those funds are temporary and not expected offset the full magnitude of Medicaid funding cuts over the next ten years. Restricting Medicaid coverage of “optional” services (like behavioral health or home care) could result in less access to care for people with complex health conditions. This may be particularly likely for home care services, where existing tools for managing spending such as caps on total spending or enrollment make it easier for states to limit spending in the future.

The administration may shape Medicaid access through actions to curtail or approve new Section 1115 Medicaid demonstration waivers. Such waivers allow states an avenue to test new approaches in Medicaid if the Department of Health and Human Services (HHS) Secretary determines the waiver is likely to “promote the objectives of the Medicaid program.” Waiver priorities may shift from one presidential administration to another. For example, the Trump administration has rescinded Biden-era 1115 waiver guidance on covering health-related social needs (HRSN) services, indicated plans to phase out certain waiver financing tools (related to use of “Designated State Health Programs” (DSHP), notified states that it does not anticipate approving or extending waivers with continuous eligibility provisions for children and adults or workforce initiatives. While the Trump administration has indicated the phase out or rescission of certain Biden-era waiver policies, the administration has not provided details about its priorities for the use of 1115 waivers. The 2025 reconciliation law included a new provision that requires the Chief Actuary at CMS to certify that 1115 waivers are not expected to result in an increase in federal expenditures compared to federal expenditures without the waiver. While “budget-neutrality” for waivers has been required under long-standing policy and practice, typically the calculations are determined on a per enrollee basis over the course of the waiver and are negotiated between states and the administration.

Workforce challenges tied to reimbursement rate policies and changes in immigration policy could also exacerbate access challenges. KFF survey data finds that 13% of immigrants have avoided going to work since January 2025 because of concerns about drawing attention to someone’s immigration status, a number which rises to 40% among people who are likely to be undocumented immigrants. Such concerns are most significant for the long-term care workforce because Medicaid is the dominant payer for care and more than one in four long-term care workers are immigrants. Beyond long-term care, immigrants constitute a large share of workers in other health care fields, including over one in four physicians in US hospitals.

What to Watch

The issues identified in this policy watch could have major implications for Medicaid coverage, financing, and access to care. Key questions for each of these areas will be important to monitor as debates evolve leading up to the mid-term elections, which will have significant implications for Medicaid and health policy in general in the years ahead.

Medicaid coverage changes:

How will federal guidance shape implementation of work requirements and other eligibility changes in the reconciliation law?

How will states implement Medicaid work requirements? How many states will implement work requirements ahead of the January 2027 deadline? Will any states be granted good faith waivers to delay implementation?

Will states adopt additional eligibility restrictions in budgets for FY 2027?

How will aggregate and state enrollment trends evolve during 2026?

Medicaid financing changes:

How will federal Medicaid financing changes affect state budgets and provider rates in 2026?

How will state financing challenges affect the development of their FY 2027 budgets?

Will states be able to offset reduced federal funding with state funding or will states adopt policies to restrict Medicaid? What policies will states adopt to reduce state Medicaid spending?

Will states be able to sustain recent increases in provider rates or expansions in services, particularly for long-term care and behavioral health?

Medicaid access changes:

How will broader changes in Medicaid coverage affect access to care?

How will changes in Medicaid 1115 waiver policy affect access to care?

Will changes in financing result in hospital or other provider closures and what will that mean for access to care? Will funding for providers from the rural health transformation fund offset restrictions from other federal and state policies?

How will broader immigration policies affect the long-term care workforce and access to services that are predominantly funded by Medicaid?

As states begin budget debates for state fiscal year (FY) 2027, many states are facing a more tenuous fiscal climate. Slowing revenue growth and heightened spending demands coupled with anticipated federal Medicaid cuts under the 2025 reconciliation law, changes to the Affordable Care Act (ACA) enhanced Marketplace subsidies, and economic changes are contributing to tighter budget conditions and fiscal uncertainty for states. Medicaid is often central to state fiscal decisions as it is simultaneously a significant spending item as well as the largest source of federal revenues for states.

States projected Medicaid enrollment to remain flat for FY 2026 in KFF’s 2025 budget survey of Medicaid officials and total Medicaid spending was expected to increase 7.9%, though there was substantial variation across states. States reported a variety of cost pressures including provider and managed care rate increases, greater enrollee health care needs, and increasing costs for long-term care, pharmacy benefits, and behavioral health services. Some states have already implemented Medicaid spending cuts to address recent budget challenges, and others may follow as they contend with budget gaps and prepare for the implementation of the Medicaid changes in the 2025 reconciliation law.

Now in January 2026, halfway through FY 2026, governors are beginning to release proposed budgets for state legislatures to consider for FY 2027. Most states will be adopting FY 2027 budgets this year and another 16 states enacted biennial budgets last year, though some of these states may adopt a supplemental budget for FY 2027. The state budget cycle in most states runs from July to June, and governors typically release their budget proposals early in the calendar year followed by a convening of the legislature to finalize and enact a budget. While most states have not yet released budget proposals, implementation of the 2025 reconciliation law will put pressure on state Medicaid programs and states such as Colorado and Idaho have already announced Medicaid cuts. Medicaid issues are also likely to intersect with broader health care coverage and affordability debates leading up to the mid-term elections in November 2026. There will be 39 gubernatorial elections (18 incumbent governors running for reelection and 21 incumbent governors who are either term-limited or not seeking reelection) and control of state legislative bodies could also be affected. This brief describes current state fiscal conditions as states begin FY 2027 budget debates and highlights key areas to watch for Medicaid policy changes as states respond to fiscal challenges and the 2025 reconciliation law.

State Fiscal Pressures

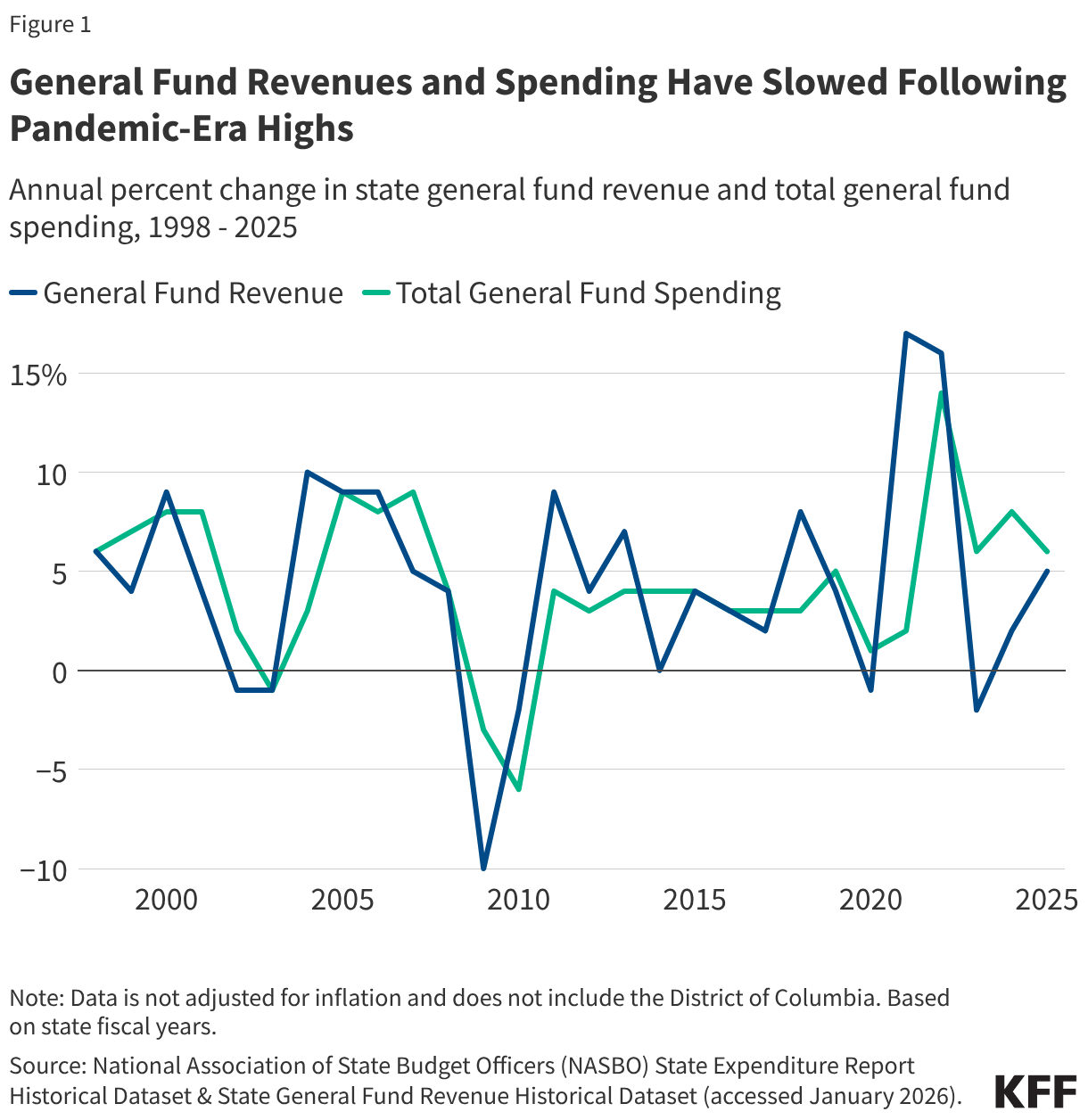

States are facing a more tenuous fiscal climate as they prepare for FY 2027 budget debates. In recent years, tax cuts combined with changes in inflation and consumer consumption patterns has led to slowing state revenue growth following a period of record-breaking revenue and expenditure growth for states after the initial pandemic-induced economic downturn (Figure 1). General fund spending has also slowed, and data show state rainy day fund capacity is also beginning to decline following all-time highs (though funds remain stronger than before the pandemic). States are also contending with increasing spending demands from Medicaid, employee health care, education, housing, and disaster response, though state fiscal conditions vary widely across states. Due to tightening budget conditions, some states have begun implementing more budget management strategies, like spending cuts or other cost containment measures.

Recent federal actions, including the passage of the 2025 reconciliation law, may intensify state budget pressures for FY 2027. States are preparing for significant policy changes and federal funding cuts in the 2025 reconciliation law, including tax code changes as well as Medicaid and SNAP cuts. The new law is expected to reduce federal Medicaid spending by $911 billion (or 14%) over the next decade, though the impact varies by state. States may offset some of the reductions with state funds, though the challenging fiscal climate and the magnitude of federal funding cuts in the new law may make it difficult. For example, states may consider filling in funding gaps created by losses in federal funding for Planned Parenthood or providing state funded coverage for lawfully present immigrants who lose health coverage due to new eligibility restrictions. Some states are also moving to subsidize ACA Marketplace premiums with state funds following the expiration of the enhanced subsidies. The expiration of the enhanced subsidies as well as federal workforcecuts, tariff changes, and shifts in economic conditions contribute to heightened fiscal uncertainty for states. While not expected to offset rural hospitals’ losses under the reconciliation law and funding amounts will vary, states will be receiving additional federal funding through a new rural health fund. Given state budget challenges and fiscal uncertainty, at least 14 states, including Arizona, California, Colorado, Delaware, Maryland, New Mexico, and Rhode Island, have already forecasted budget gaps for FY 2027.

State Medicaid Changes

In response to mounting state budget pressures and the passage of the 2025 reconciliation law, FY 2027 state budget debates may include efforts to reduce Medicaid spending. Even though many provisions of the reconciliation law do not take effect immediately, a few states have already implemented Medicaid spending cuts for FY 2026 and, heading into the FY 2027 budget cycle, states may continue to propose Medicaid policy changes in key areas (Figure 2). This brief includes Medicaid changes from recently announced governors’ budget proposals, though most states have not yet released detailed budget proposals yet. The state budget landscape will likely continue to evolve as revenue forecasts and spending demands become clearer and as more states release their budgets. Given the timing and disparate impact of the reconciliation law across states as well as variation in state fiscal conditions, FY 2027 Medicaid policy changes will vary by state and some Medicaid cuts may not begin until FY 2028 or later.

Figure 2

Provider Rates

States have substantial flexibility to establish Medicaid provider reimbursement methodologies and amounts, especially within a fee-for-service (FFS) delivery system where a state Medicaid agency pays providers or groups of providers directly. Historically, during times of weak state revenue collections, states have typically turned to provider rate restrictions to contain costs. KFF’s 2025 Medicaid budget survey found that adopted FY 2026 budgets included more rate increases than cuts, but there was a notable uptick in states reporting provider rate restrictions compared to previous years. Some notable restrictions in FY 2026 included 4% across the board reductions for all provider types and services in Idaho, and a reversal of 1.6% across the board provider rate increases to address budget shortfalls in Colorado.

State budget pressures and the 2025 reconciliation law may result in additional rate cuts in FY 2027 budgets. While the 2025 reconciliation law did not directly make changes to how states set provider rates, the law imposes new limits on managed care state-directed payments for inpatient hospital and nursing facility services and new restrictions on states’ ability to generate Medicaid provider tax revenue. Some provider tax provisions in the new law have already been implemented, and some states may be anticipating the effect of future provider tax limits that will be phased on over time, which could exacerbate state budget challenges and result in reimbursement rate cuts. Some early FY 2027 governors’ budget proposals include provider rate restrictions: Colorado proposed reducing Medicaid provider rates to 85% of Medicare rates, along with rate reductions for certain home health, dental, behavioral health, and other services, and Idaho proposed extending their 4% provider rate reductions. Texas has also proposed reimbursement rate reductions for FY 2027 for substance use treatment facilities and durable medical equipment. North Carolina has not yet passed their biennial budget for FY 2026 and FY 2027; while this stalemate resulted in rate cuts that were eventually restored in FY 2026, the legislature may consider additional cuts as they finalize their budget.

Benefits

State Medicaid programs must cover a comprehensive set of “mandatory” benefits, including items and services typically excluded from traditional insurance, but may also cover a broad range of optional benefits. For example, all states cover prescription drugs as an optional benefit, and most states cover other optional services such as physical therapy, eyeglasses, and adult dental care. KFF’s 2025 Medicaid budget survey found that benefit expansions continued to far outweighed benefit restrictions and limitations in FY 2026 (consistent with prior survey years), particularly for behavioral health. However, some states had plans to restrict coverage of GLP-1s for obesity treatment, including California, New Hampshire, Pennsylvania, and South Carolina, which all eliminated coverage of GLP-1s for obesity treatment in January 2026, likely reflecting recent state budget challenges and fiscal uncertainty.

As states enter FY 2027 budget debates, it may be challenging to sustain recent benefit expansions and states may face increased pressure to cut or limit optional benefits. While the 2025 reconciliation law does not directly change Medicaid benefits, states may have to cut or limit optional benefits to offset federal funding cuts in the new law or respond to existing budget challenges. Colorado’s recently released governor’s budget proposal for FY 2027 includes capping dental benefits, and Rhode Island’s Medicaid program FY 2027 budget proposal considers ending GLP-1 coverage. Idaho governor’s budget proposal includes suggested cuts to dental, pharmacy, and various medical service benefits.

Home Care

Medicaid pays for almost 70% of all home care spending in the U.S., and most Medicaid home care is provided through optional services, giving states flexibility to manage costs. Most states use various mechanisms to limit home care spending under waiver programs, including caps on enrollment, total spending, and per-participant costs, as well as restrictions on specific services like personal care. Nearly a third of states reported planning to adopt new strategies in FY 2026 to contain home care costs, according to data from KFF’s 2025 survey of officials administering Medicaid home care programs.

State budget challenges and federal funding cuts in the 2025 reconciliation law could result in additional pressure to reduce optional home care services in FY 2027 budgets. The 2025 reconciliation law does not directly change home care benefits, but significant Medicaid spending on home care and the availability of mechanisms for limiting such spending could spur states to make home care cuts. When faced with fiscal pressures in the past, all states reduced spending on home care by either serving fewer people (40 states) and/or by cutting benefits or payment rates for long-term care providers (47 states). Recently released governors’ budget proposals from Colorado and Idaho include suggested cuts to home care services, although specifics of these proposals are not available and may evolve during the legislative process.

Eligibility and Work Requirements