Global Health Funding Awards by State and Congressional District

This resource provides data on global health funding awards by U.S. state and congressional district in FY 2024. Data were obtained from USAspending.gov, the official source of spending across the U.S. government. While the resource allows users to see how much funding for global health projects was channeled to organizations in the U.S., it only provides information on the prime awardee of funding, not sub-awardee, and should not be used to assess how much funding ultimately went to other countries (other analyses1 show that most funding does go to support health activities in recipient countries). Rather, the analysis can be used to indicate that some funding goes to U.S.-based organizations and companies who in turn work on behalf of the U.S. government on global health.

Some key take-aways are as follows:

- In FY 2024, the U.S. obligated more than $10 billion for global health activities.

- Most of this funding (75% or $7.9 billion) was designated for work primarily to be performed in other countries, whether or not the prime awardee was a U.S. or foreign implementer.

- U.S.-based prime awardees received $4.6 billion (44%) of FY 2024 global health funding (foreign implementers received $5.9 billion or 56%).

- Of the $4.6 billion provided to U.S.-based implementers:

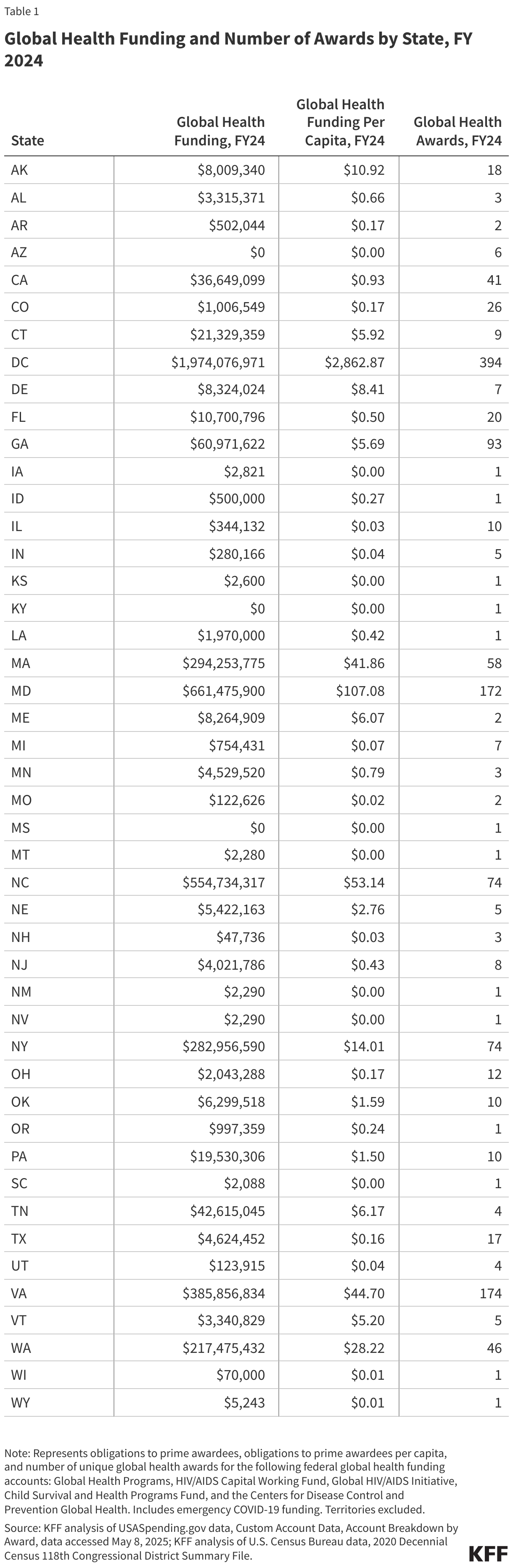

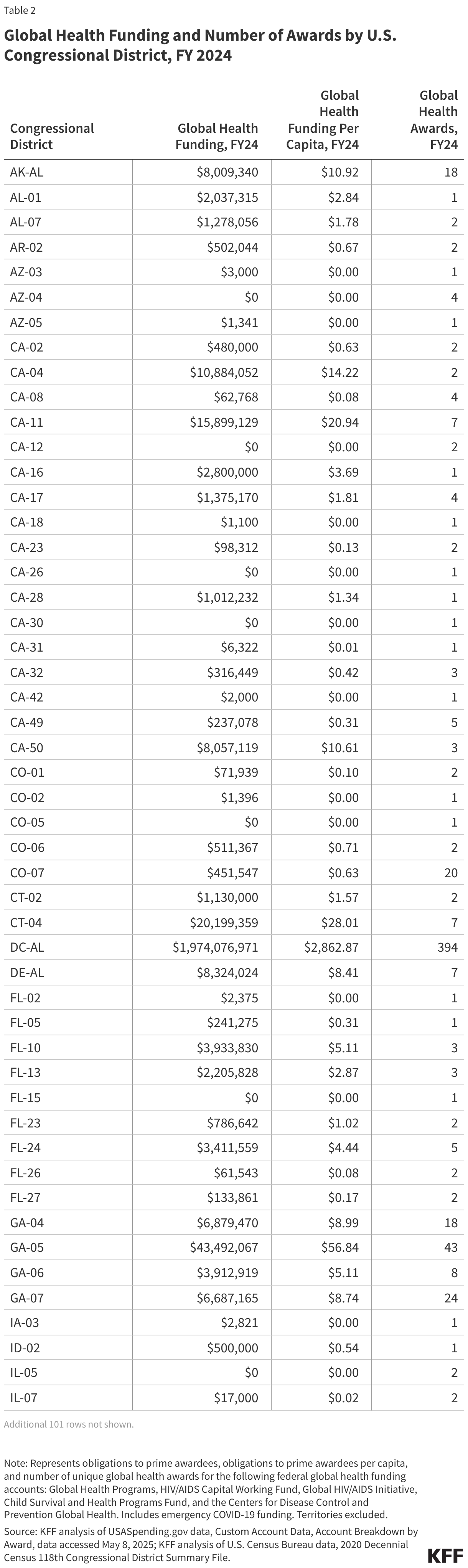

- Funding was provided to organizations in 45 states and the District of Columbia and 151 of 436 congressional districts.2

- The top 10 states accounted for $4.5 billion, or 97%. D.C.-based organizations received the largest amount of funding ($2 billion), primarily because the global health supply chain contractor is based on D.C., followed by Maryland ($661 million), North Carolina ($555 million), Virginia ($386 million), Massachusetts ($294 million), New York ($283 million), Washington ($217 million), Georgia ($61 million), Tennessee ($43 million), and California ($37 million).

- The top 10 congressional districts accounted for $4.2 billion, or 90%. Again, D.C. received the largest amount of funding ($2 billion), followed by NC-04 ($553 million), MD-08 ($384 million), MD-07 ($274 million), WA-07 ($188 million), VA-08 ($188 million), VA-11 ($180 million), NY-13 ($157 million), MA-05 ($142 million), and MA-08 ($141 million).

Detailed data are provided below.

States

Congressional Districts

Methods

Methods: Data represent obligations and number of unique awards (federal contracts, grants, or loans) to U.S.-based organizations listed as the “prime” implementer of the award for the 2024 fiscal year for the following federal accounts: Global HIV/AIDS Initiative (019-1030), Global Health Programs (019-1031), Child Survival and Health Programs Fund (072-1095), HIV/AIDS Working Capital Fund (072-1033), and Global Health, Centers for Disease Control and Prevention (075-0955). Several additional federal accounts that may contain funding for global health activities, such as the Economic Support Fund (ESF) account, were not included because these accounts support numerous development activities and global health funding amounts could not be disaggregated. Prime awardees based in U.S. territories were excluded from the analysis. Recipients identified as “Foreign Awardees” were not included in the U.S.-based implementers analyses. While many prime awardees make sub-agreements with other entities to perform a portion of the original award, data on sub-awardees were not available. Where aggregate amounts by state or congressional district were negative (representing de-obligations or cancelled funds), these amounts were converted to zero to signify that the state/congressional district received overall no additional global health funding obligations in FY2024.

Sources: Award and obligation data were obtained from USASpending.gov’s Custom Account Data query page using the “Account Breakdown by Award” file for fiscal year 2024 for the following federal accounts: Global HIV/AIDS Initiative (019-1030), Global Health Programs (019-1031), Child Survival and Health Programs Fund (072-1095), HIV/AIDS Working Capital Fund (072-1033), and Global Health, Centers for Disease Control and Prevention (075-0955). Data were obtained on May 8, 2025. Population data were obtained from the U.S. Census Bureau’s 2020 Decennial Census 118th Congressional District Summary File. Data were obtained on June 12, 2025.

- See: Center for Global Development, “No, 90 Percent of Aid Is Not Skimmed Off Before Reaching Target Communities,” https://www.cgdev.org/blog/no-90-percent-aid-not-skimmed-reaching-target-communities; WLRN Public Radio and Television, “PolitiFact FL: Does as little as 10% of USAID go to help people in need? What that claim gets wrong,” https://www.wlrn.org/government-politics/2025-02-07/politifact-florida-usaid; PEPFAR, “PEPFAR 2022 Country and Regional Operational Plan (COP/ROP) Guidance for all PEPFAR-Supported Countries”, https://modern.kff.org/wp-content/uploads/2022/02/PEPFAR-2022-COP-ROP-Guidance-Final.pdf#page=97; Washington Post, “Vance, Rubio peddle fiction that 88 percent of foreign aid doesn’t go overseas,” https://www.washingtonpost.com/politics/2025/06/11/usaid-vance-rubio-fact-checker/. ↩︎

- Excludes congressional districts in U.S. territories; includes D.C.’s congressional district. ↩︎