Medicaid Waiver Tracker: Approved and Pending Section 1115 Waivers by State

Tracker

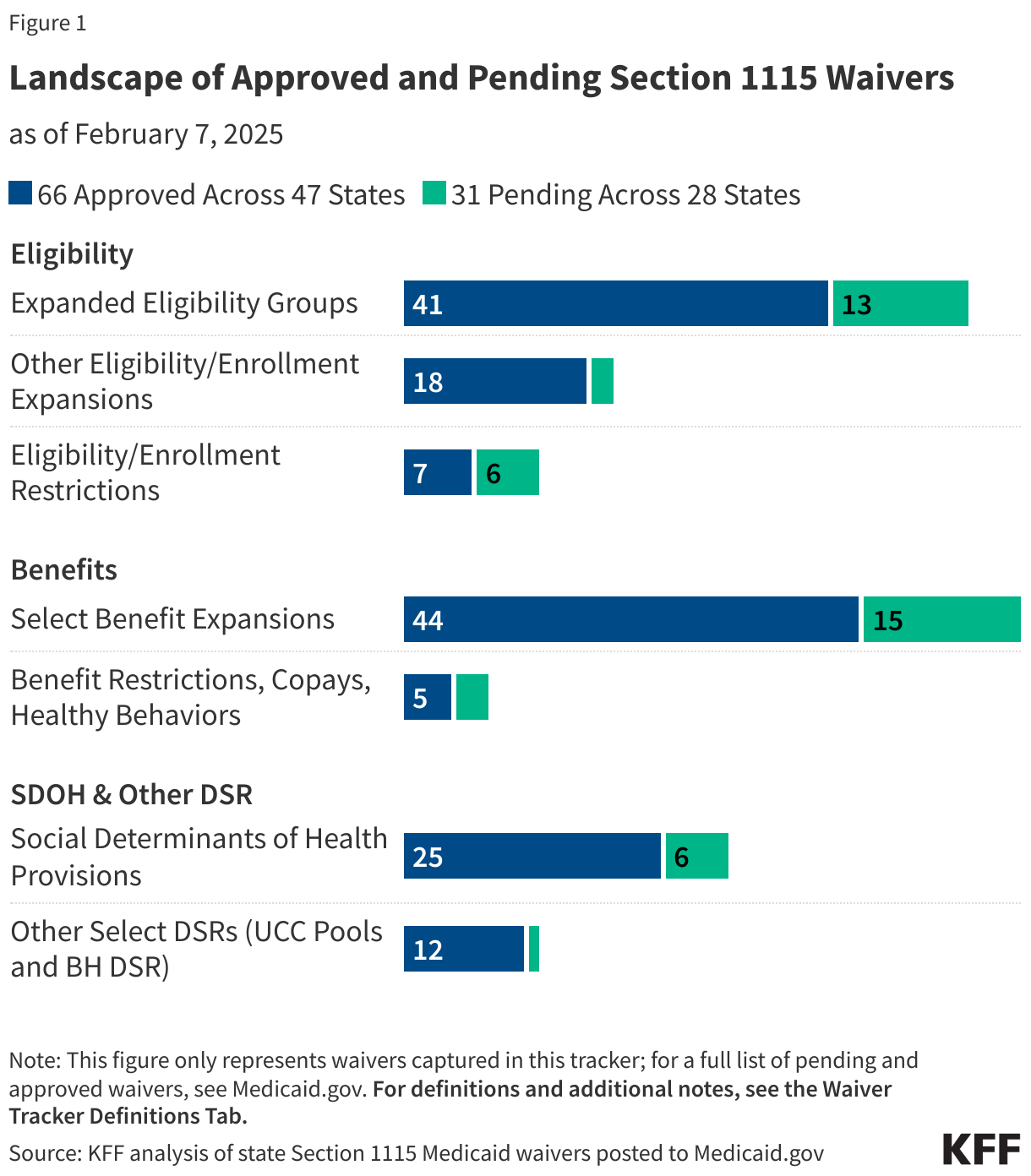

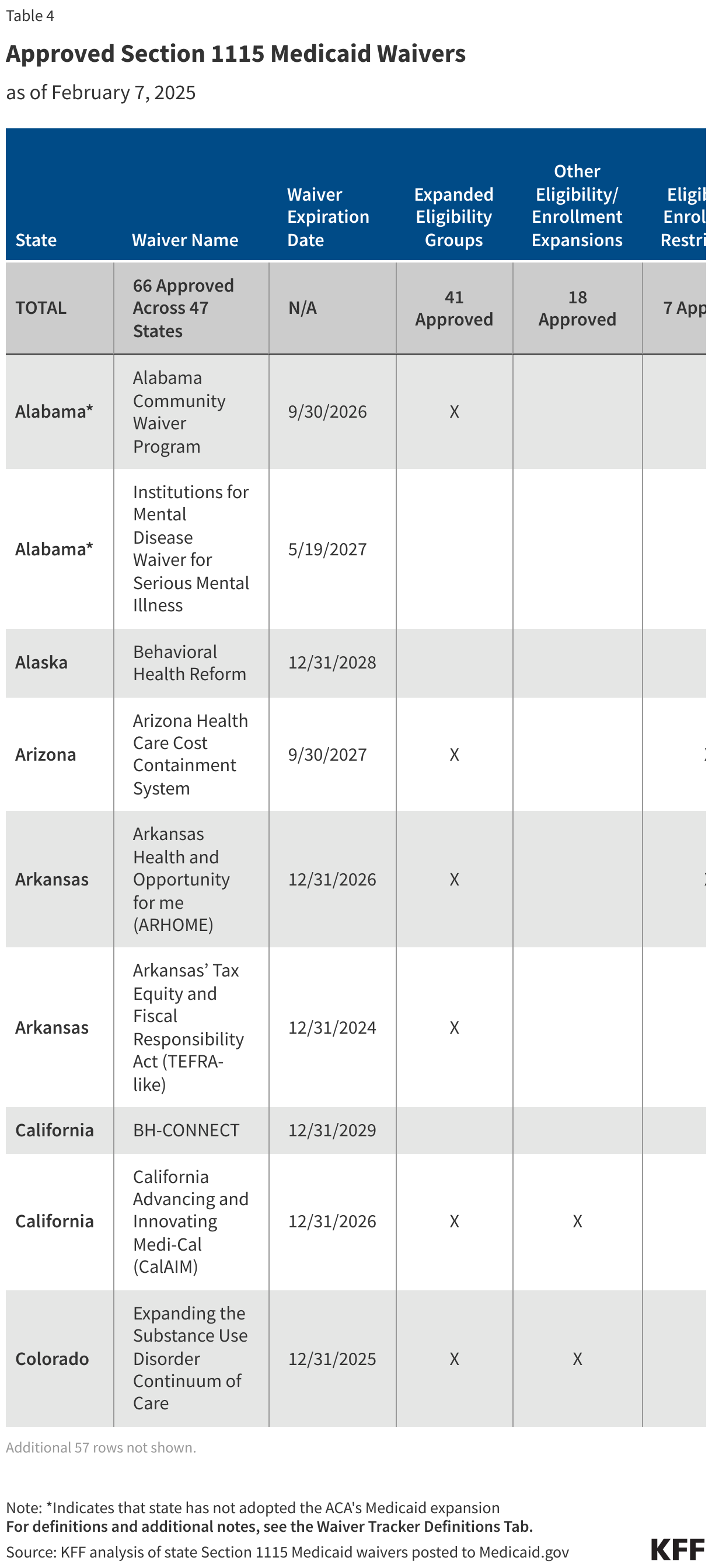

Section 1115 Medicaid demonstration waivers offer states an avenue to test new approaches in Medicaid that differ from what is required by federal statute, if [in the HHS Secretary’s view] the approach is likely to “promote the objectives of the Medicaid program.” They can provide states additional flexibility in how they operate their programs, beyond the considerable flexibility that is available under current law. Waivers generally reflect priorities identified by states as well as changing priorities from one presidential administration to another. Nearly all states have at least one active Section 1115 waiver and some states have multiple 1115 waivers. See the “Key Themes Maps” tab for a discussion of recent waiver trends.

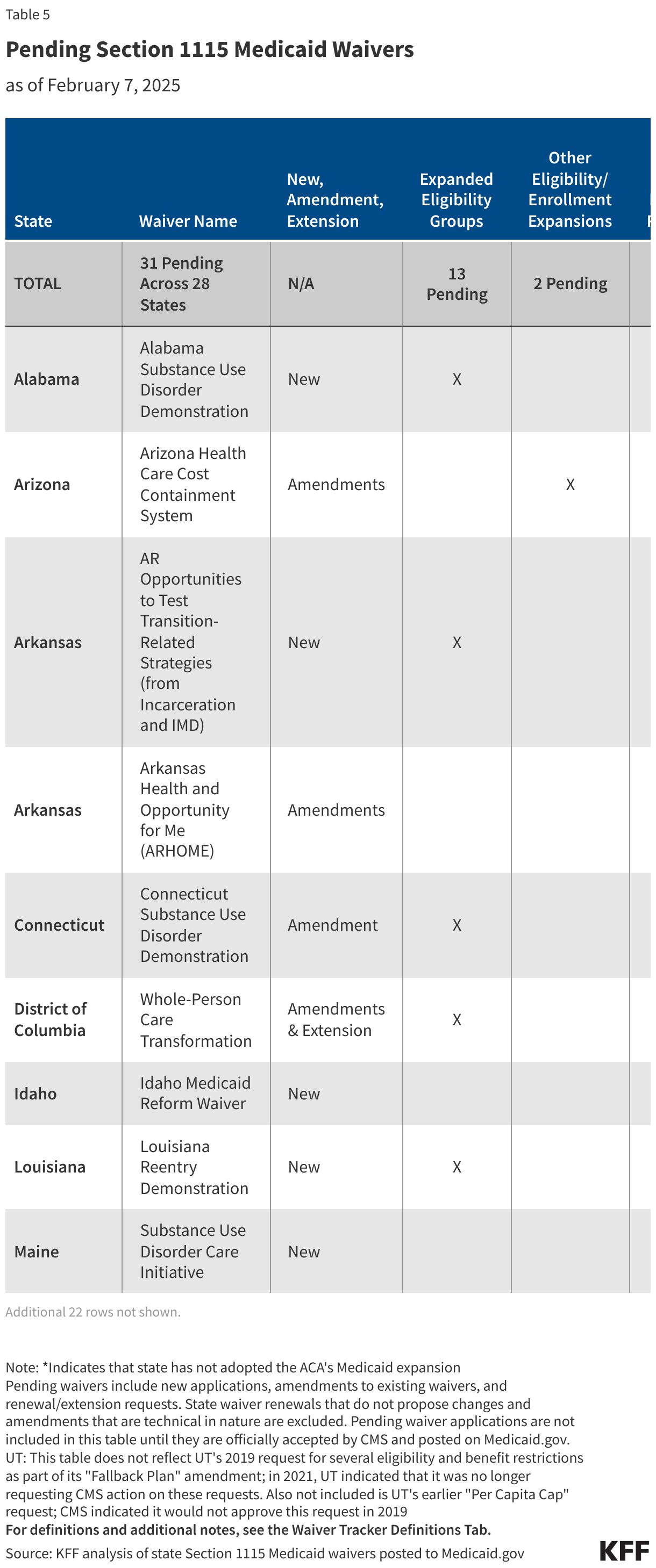

This page tracks approved and pending Section 1115 waiver provisions (including expansions and restrictions) related to eligibility, benefits, and social determinants of health and other delivery system reforms, once such waivers are posted to the state waivers list on Medicaid.gov. For more information on inclusion criteria and on each provision, as well as a list of acronyms, see the Definitions tab.

Detailed Topic Tables

Aggregate State Tables

Waivers with Eligibility Changes

Waivers with Benefit Changes

Waivers with SDOH & Other DSR Changes

All Approved Waivers by Topic

All Pending Waivers by Topic

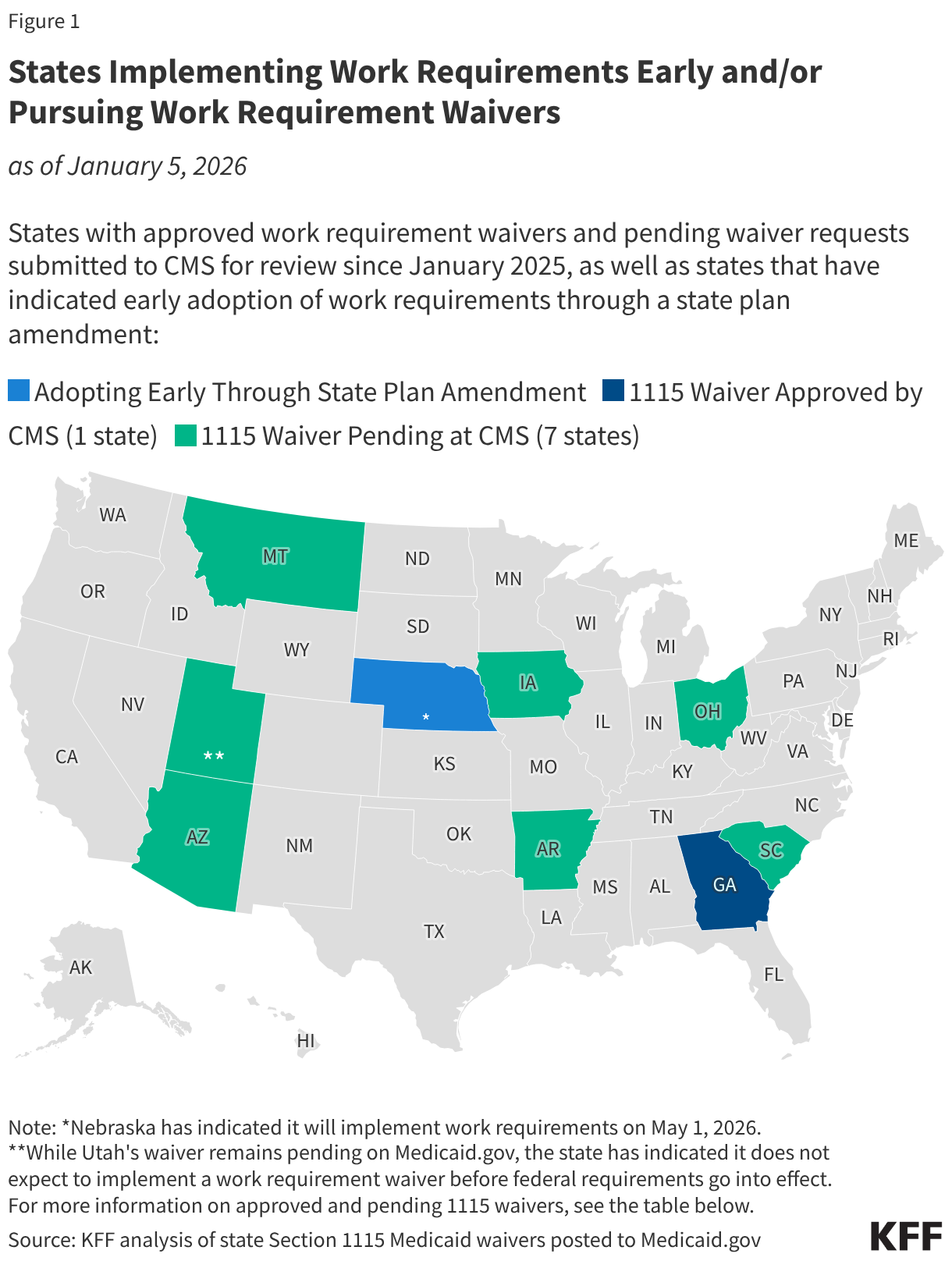

Work Requirements

See KFF's Work Requirements Tracker for additional state and national-level data related to work requirement implementation, including related KFF resources on work requirements.

The 2025 reconciliation law requires states to condition Medicaid eligibility for adults in the ACA Medicaid expansion group on meeting work requirements starting January 1, 2027; however, states have the option to implement requirements sooner through a state plan amendment (SPA) or through an approved 1115 waiver.

State Plan Amendments (SPAs)

States may choose to implement work requirements prior to the required January 1, 2027 implementation date through a state plan amendment. Nebraska is the first state to announce that it will begin enforcing federal work requirements early through a state plan amendment, starting May 1, 2026. Two other states are also planning to implement before January 2027–Montana on July 1, 2026 and Iowa on December 1, 2026. Arkansas has announced that it plans to launch a soft implementation of work requirements on July 1, 2026 but will not disenroll individuals prior to January 1, 2027.

1115 Waivers

Since the start of the second Trump administration, several states have submitted waivers to implement work requirements. However, states are unlikely to be moving forward with proposed 1115 waivers at this time due to the passage of federal work requirements. States that plan to implement federal work requirements early will do so through a state plan amendment. Currently, Georgia is the only state with a Medicaid work requirement waiver in place following litigation over the Biden administration’s attempt to stop it. Georgia’s waiver will expire December 31, 2026; the state is required to come into compliance with the new federal requirements effective January 1, 2027.

Early Implementation and Waiver Status

The map below identifies states that have indicated they will implement work requirements early through a state plan amendment as well as approved (Georgia) and pending work requirement waivers (submitted to CMS since the start of the second Trump administration). The table below the map provides more detailed state waiver information.

Key Themes Maps

Section 1115 waivers generally reflect priorities identified by states as well as changing priorities from one presidential administration to another. Key Biden administration 1115 initiatives included waivers addressing enrollee health-related social needs (HRSN), pre-release coverage for individuals who are incarcerated, and multi-year continuous eligibility for children.

In March 2025, the Trump administration rescinded HRSN guidance issued by the Biden administration. CMS indicates this does not nullify existing HRSN 1115 approvals but going forward they will consider HRSN / SDOH requests on a case-by-case basis. In April 2025, the Trump administration announced it would be phasing out federal funding for “Designated State Health Programs” (DSHP) in waivers. In July 2025, the Trump administration released guidance indicating it will not approve (new) or extend (existing) continuous eligibility waivers for children or adults. CMS also announced in July it would be phasing out initiatives to strengthen the Medicaid workforce for primary care, behavioral health, dental, and home and community based services (not depicted in maps below).

This page tracks pending and approved waivers in key areas of recent state activity and will track Trump administration action in these areas going forward. Hover over individual states to display waiver expiration dates.

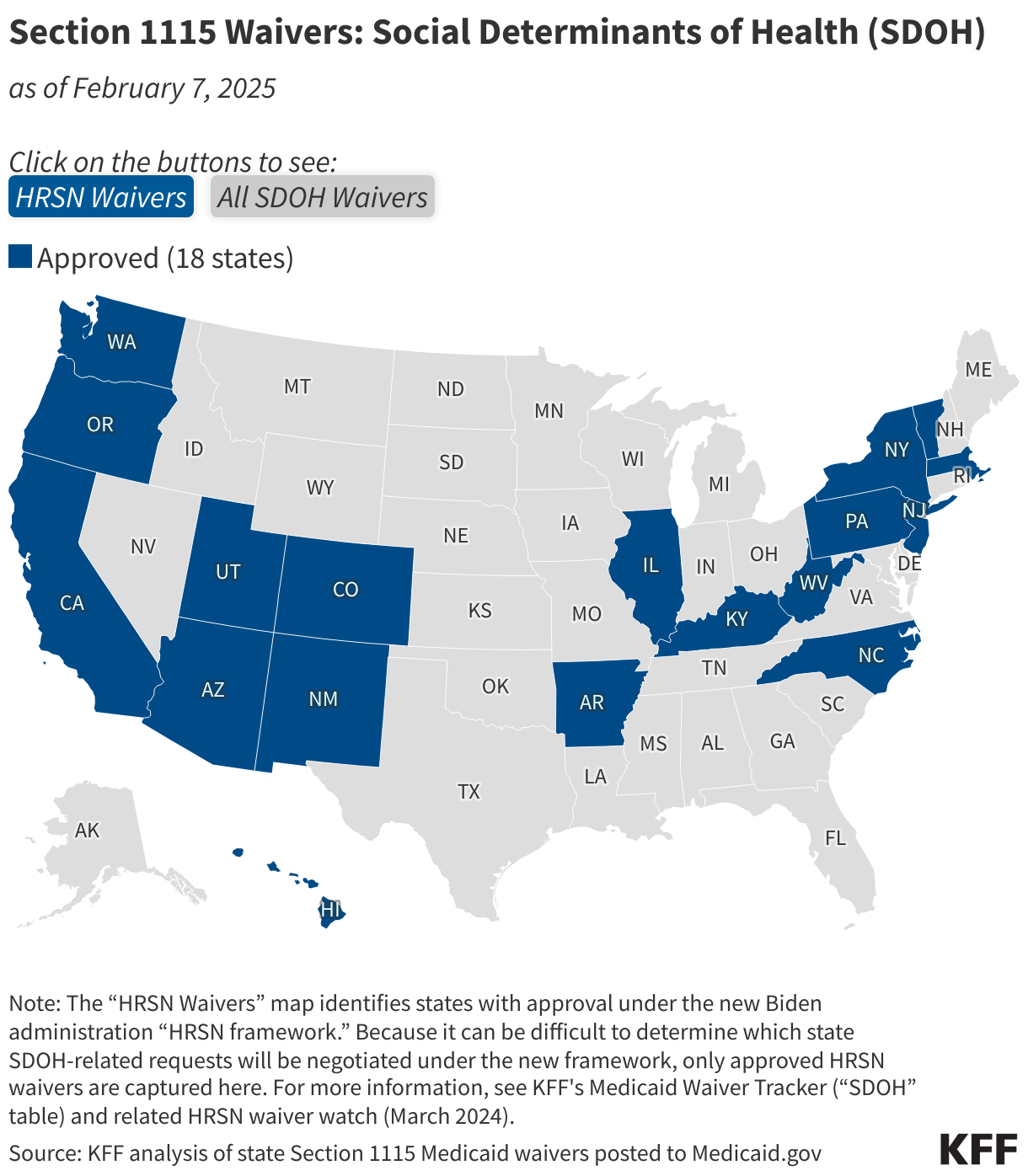

Social Determinants of Health

Social determinants of health (SDOH) are the conditions in which people are born, grow, live, work and age. SDOH include but are not limited to housing, food, education, employment, healthy behaviors, transportation, and personal safety. In 2022, CMS (under the Biden administration) announced a demonstration waiver opportunity to expand the tools available to states to address enrollee “health-related social needs” (or “HRSN”) including housing instability, homelessness, and nutrition insecurity, building on CMS’s 2021 guidance. In 2023, CMS issued a detailed Medicaid and CHIP HRSN Framework accompanied by an Informational Bulletin, which were updated in 2024.

In March 2025, the Trump administration rescinded the Biden administration HRSN guidance. CMS indicates this does not nullify existing HRSN approvals but going forward they will consider HRSN / SDOH requests on a case-by-case basis.

The “HRSN Waivers” map below identifies states with approval under the Biden administration HRSN framework. The “All SDOH Waivers” map identifies SDOH-related 1115 waivers more broadly, including those that pre-date or were approved outside of the HRSN framework. For more detailed waiver information, refer to KFF’s Medicaid Waiver Tracker (“SDOH” table) and HRSN waiver watch (March 2024).

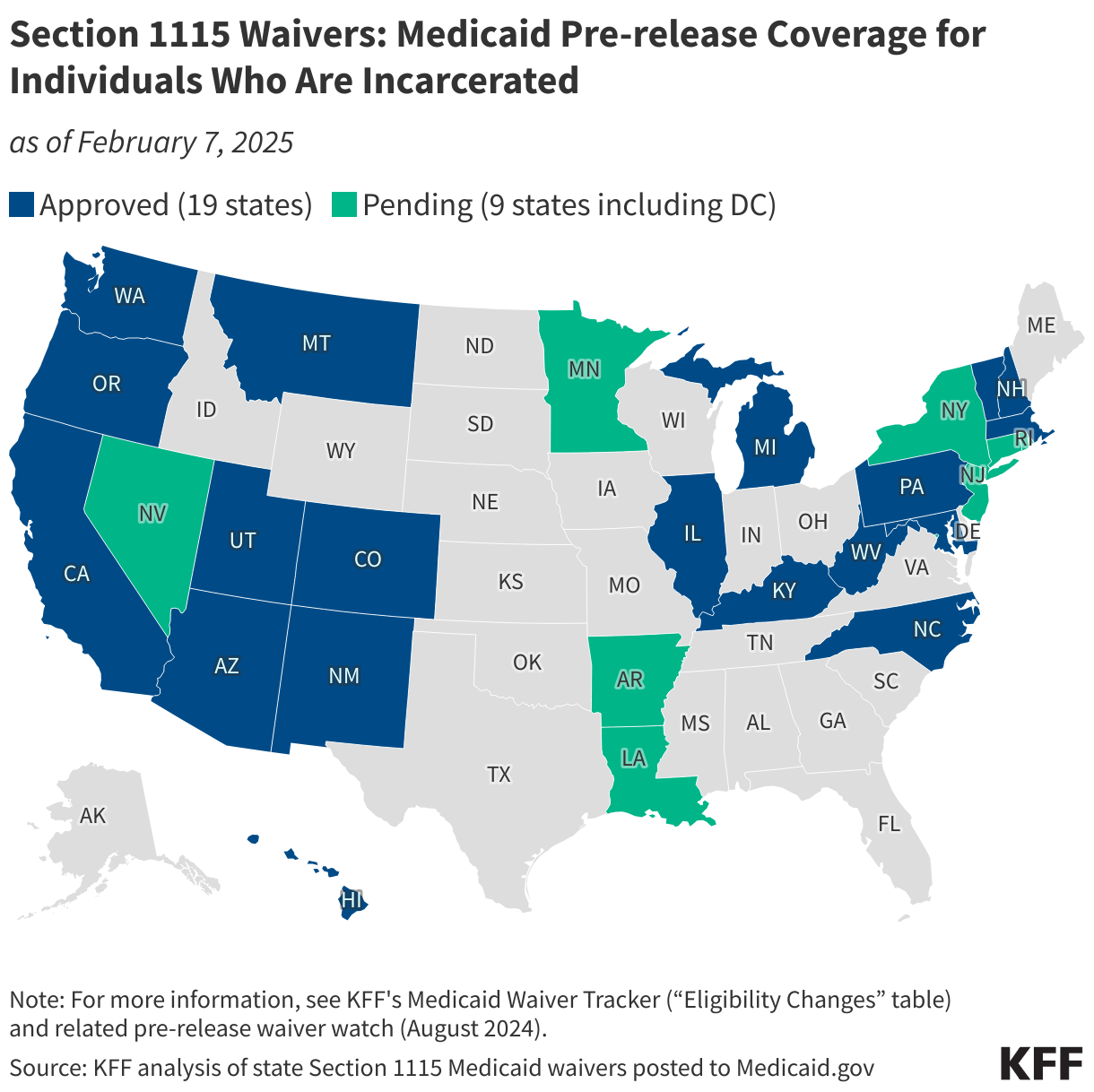

Medicaid Pre-release Coverage for Individuals Who Are Incarcerated

In April 2023, the Biden administration released guidance encouraging states to apply for a new Section 1115 demonstration opportunity to test transition-related strategies to support community reentry for people who are incarcerated. This demonstration allows states a partial waiver of the inmate exclusion policy, which prohibits Medicaid from paying for services provided during incarceration (except for inpatient services). Reentry services aim to improve care transitions and increase continuity of health coverage, reduce disruptions in care, improve health outcomes, and reduce recidivism rates. The Biden administration approved 19 state waivers to facilitate reentry for individuals who are incarcerated. The map below identifies states with approved and pending waivers to provide pre-release services to Medicaid-eligible individuals who are incarcerated. Medicaid pre-release waivers have been pursued by both Republican and Democratic governors. For more information, refer to KFF’s Medicaid Waiver Tracker (“Eligibility Changes” table) and related pre-release waiver watch (August 2024).

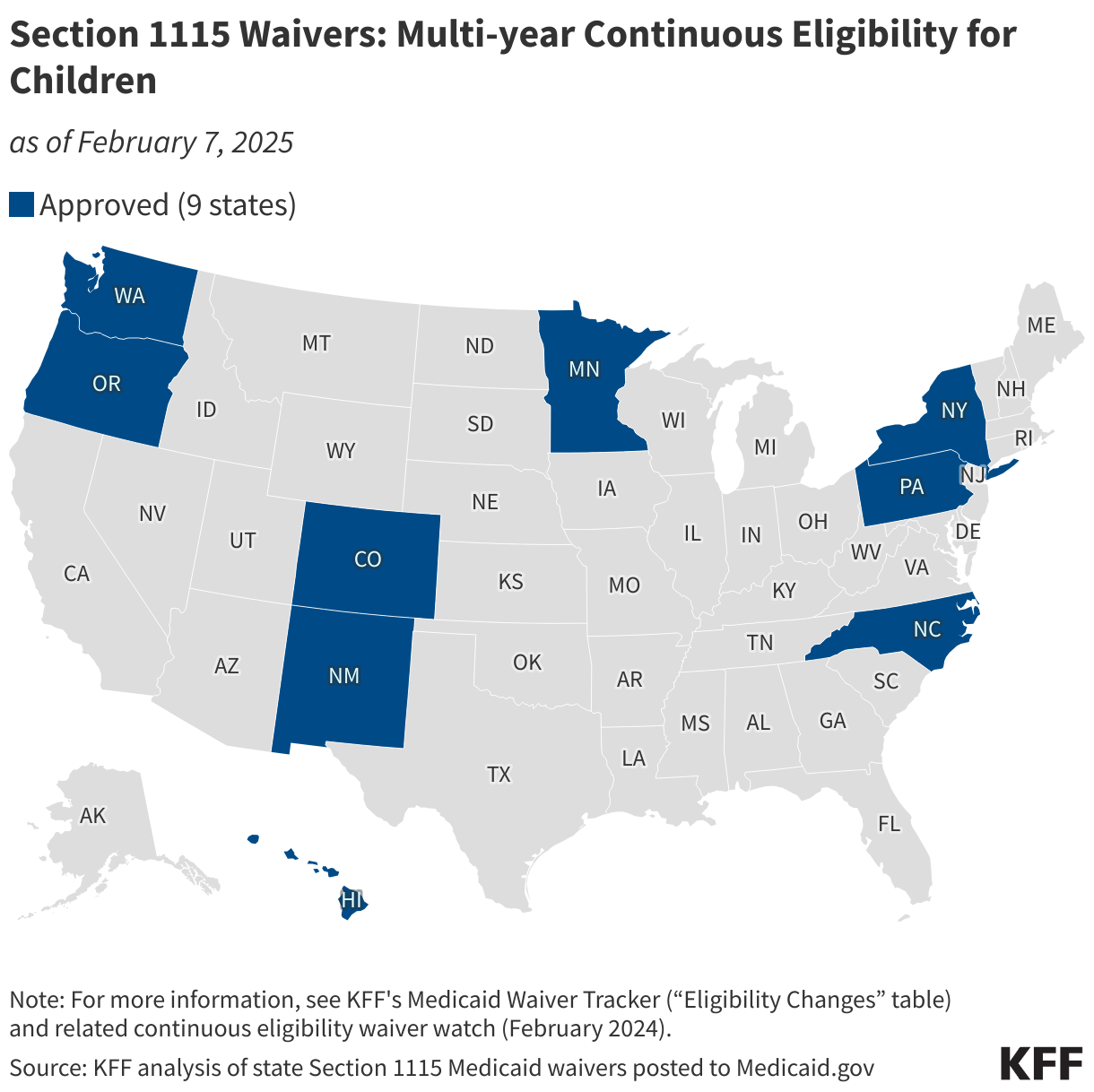

Multi-year Continuous Eligibility for Children

The Consolidated Appropriations Act, 2023 required all states to implement 12-month continuous eligibility for children beginning on January 1, 2024. The Biden administration approved 9 waivers that allow states to provide multi-year continuous eligibility for children (e.g., from birth to age six). Continuous eligibility has been shown to reduce Medicaid disenrollment and “churn” rates (rates of individuals temporarily losing Medicaid coverage and then re-enrolling within a short period of time).

In July 2025, the Trump administration released guidance indicating it will not approve (new) or extend (existing) continuous eligibility waivers for children or adults. The map below displays states with waiver approval to provide multi-year continuous eligibility for children. For more information, refer to KFF’s Medicaid Waiver Tracker (“Eligibility Changes” table) and related continuous eligibility waiver watch (February 2024).

Definitions

Related Resources

Recent Developments

- A Look at 1115 Waiver Evaluations for Medicaid Payments to Institutions of Mental Disease (IMD) for Substance Use Disorder, July 2026

- A Closer Look at Nebraska, the First State Planning to Implement a Medicaid Work Requirement, January 2026

- Section 1115 Waiver Watch: Early Signs Point to New Directions Under Trump Administration, May 2025

- 5 Key Facts About Medicaid Work Requirements, February 2025

- Medicaid 1115 Waiver Watch: Round-up of Key Themes at the End of the Biden Administration, January 2025

- Medicaid Section 1115 Waivers: The Basics, January 2025

- Section 1115 Waiver Watch: A Look at the Use of Contingency Management to Address Stimulant Use Disorder, January 2025

- Medicaid Work Requirements: Current Waiver and Legislative Activity, November 2024

- Section 1115 Waiver Watch: Medicaid Services for Traditional American Indian and Alaska Native Health Care Practices, November 2024

- Medicaid Waiver Priorities Under the Trump and Biden-Harris Administrations, September 2024

- Section 1115 Waiver Watch: Medicaid Pre-Release Services for People Who Are Incarcerated, August 2024

- Section 1115 Medicaid Waiver Watch: A Closer Look at Recent Approvals to Address Health-Related Social Needs (HRSN), March 2024

- Section 1115 Waiver Watch: Continuous Eligibility Waivers, February 2024

- Medicaid Authorities and Options to Address Social Determinants of Health (SDOH), January 2024

General/Overview Resource

- Medicaid 1115 Waiver Watch: Round-up of Key Themes at the End of the Biden Administration, January 2025

- Medicaid Section 1115 Waivers: The Basics, January 2025

- Medicaid Waiver Priorities Under the Trump and Biden-Harris Administrations, September 2024

- Recent Developments and Key Issues to Watch with Medicaid Section 1115 Waivers, September 2022

- What to Watch in Medicaid Section 1115 Waivers One Year Into the Biden Administration, January 2022

- 5 Targeted Actions a Biden Administration Could Use to Expand Medicaid Coverage, December 2020

- Key Questions About Medicaid Home and Community-Based Services Waiver Waiting Lists, April 2019

- The Landscape of Medicaid Demonstration Waivers Ahead of the 2020 Election, October 2020

- Explaining Stewart v. Azar: Implications of the Court’s Decision on Kentucky’s Medicaid Waiver, July 2018

- Web Briefing for Journalists: A Closer Look at the Evolving Landscape of Medicaid Waivers (recording and slides), February 2018

- How Medicaid Section 1115 Waivers Are Evolving: Early Insights About What to Watch, October 2017

- Current Flexibility in Medicaid: An Overview of Federal Standards and State Options, January 2017

- The New Review and Approval Process Rule for Section 1115 Medicaid and CHIP Demonstration Waivers, March 2012

Eligibility and Enrollment Expansions

- Section 1115 Waiver Watch: Medicaid Pre-Release Services for People Who Are Incarcerated, April 2024

- Medicaid Postpartum Coverage Extension Tracker, March 2024

- Section 1115 Waiver Watch: Continuous Eligibility Waivers, February 2024

- Section 1115 Waiver Watch: How California Will Expand Medicaid Pre-Release Services for Incarcerated Populations, February 2023

- State Policies Connecting Justice-Involved Populations to Medicaid Coverage and Care, December 2021

- Expanding Postpartum Medicaid Coverage, March 2021

- Key Issues to Watch for Justice-Involved Populations: COVID-19, Vaccines, & Medicaid, February 2021

- Michigan’s Medicaid Section 1115 Waiver to Address Effects of Lead Exposure in Flint, March 2016

Eligibility and Enrollment Restrictions

Work Requirements:

- 5 Key Facts About Medicaid Work Requirements, February 2025

- Understanding the Intersection of Medicaid and Work: An Update, February 2025

- Medicaid Work Requirements: Current Waiver and Legislative Activity, November 2024

- Medicaid Work Requirements are Back on the Agenda, April 2023

- An Overview of Medicaid Work Requirements: What Happened Under the Trump and Biden Administrations?, May 2022

- Work Among Medicaid Adults: Implications of Economic Downturn and Work Requirements, February 2021

- Medicaid Work Requirements at the U.S. Supreme Court, February 2021

- Supporting Work without the Requirement: State and Managed Care Initiatives, December 2019

- The Relationship Between Work and Health: Findings from a Literature Review, August 2018

- What Do Different Data Sources Tell Us About Medicaid and Work?, July 2018

- Implications of a Medicaid Work Requirement: National Estimates of Potential Coverage Losses, June 2018

- Medicaid Enrollees and Work Requirements: Lessons From the TANF Experience, August 2017

- Don’t Expect Medicaid Work Requirements to Make a Big Difference [column], April 2017

Other:

- Understanding the Impact of Medicaid Premiums & Cost-Sharing: Updated Evidence from the Literature and Section 1115 Waivers, September 2021

- Key State Policy Choices About Medical Frailty Determinations for Medicaid Expansion Adults, June 2019

- “Partial Medicaid Expansion” with ACA Enhanced Matching Funds: Implications for Financing and Coverage, February 2019

- Implications of Emerging Waivers on Streamlined Medicaid Enrollment and Renewal Processes, February 2018

- Medicaid Retroactive Coverage Waivers: Implications for Beneficiaries, Providers, and States, November 2017

- The Effects of Premiums and Cost Sharing on Low-Income Populations: Updated Review of Research Findings, June 2017

Benefit Expansions

- A Look at 1115 Waiver Evaluations for Medicaid Payments to Institutions of Mental Disease (IMD) for Substance Use Disorder, July 2026

- Section 1115 Waiver Watch: A Look at the Use of Contingency Management to Address Stimulant Use Disorder, January 2025

- Medicaid Coverage of Behavioral Health Services in 2022: Findings from a Survey of State Medicaid Programs, March 2023

- State Policies Expanding Access to Behavioral Health Care in Medicaid, December 2021

- State Options for Medicaid Coverage of Inpatient Behavioral Health Services, November 2019

- Key Themes in Medicaid Section 1115 Behavioral Health Waivers, November 2017

Benefit Restrictions, Copays, and Healthy Behaviors

- Understanding the Impact of Medicaid Premiums & Cost-Sharing: Updated Evidence from the Literature and Section 1115 Waivers, September 2021

- The Effects of Premiums and Cost Sharing on Low-Income Populations: Updated Review of Research Findings, June 2017

- Medicaid Non-Emergency Medical Transportation: Overview and Key Issues in Medicaid Expansion Waivers, February 2016

Social Determinants of Health

- Section 1115 Waiver Watch: Early Signs Point to New Directions Under Trump Administration, May 2025

- Medicaid 1115 Waiver Watch: Round-up of Key Themes at the End of the Biden Administration, January 2025

- Section 1115 Waiver Watch: Medicaid Services for Traditional American Indian and Alaska Native Health Care Practices, November 2024

- Section 1115 Waiver Watch: Medicaid Pre-Release Services for People Who Are Incarcerated, April 2024

- Section 1115 Medicaid Waiver Watch: A Closer Look at Recent Approvals to Address Health-Related Social Needs (HRSN), March 2024

- Medicaid Authorities and Options to Address Social Determinants of Health (SDOH), January 2024

- Medicaid and Racial Health Equity, June 2023

- A Look at Recent Medicaid Guidance to Address Social Determinants of Health and Health-Related Social Needs, February 2023

- State Policies for Expanding Medicaid Coverage of Community Health Worker (CHW) Services, January 2023

- California Efforts to Address Behavioral Health and SDOH: A Look at Whole Person Care Pilots, March 2022

- A First Look at North Carolina’s Section 1115 Medicaid Waiver’s Healthy Opportunities Pilots, March 2019

- Beyond Health Care: The Role of Social Determinants in Promoting Health and Health Equity, May 2018

Delivery System Reform

- Mapping Medicaid Delivery System and Payment Reform, March 2023

- Tennessee & Other Medicaid 1115 Waiver Activity: Implications for the Biden Administration, January 2021

- Implications of CMS’s New “Healthy Adult Opportunity” Demonstrations for Medicaid, February 2020

- Why it Matters: Tennessee’s Medicaid Block Grant Waiver Proposal, December 2019

- From Ballot Initiative to Waivers: What is the Status of Medicaid Expansion in Utah?, November 2019

- “Partial Medicaid Expansion” with ACA Enhanced Matching Funds: Implications for Financing and Coverage, February 2019

- Key Themes From Delivery System Reform Incentive Payment (DSRIP) Waivers in 4 States, April 2015

- An Overview of Delivery System Reform Incentive Payment (DSRIP) Waivers, September 2014