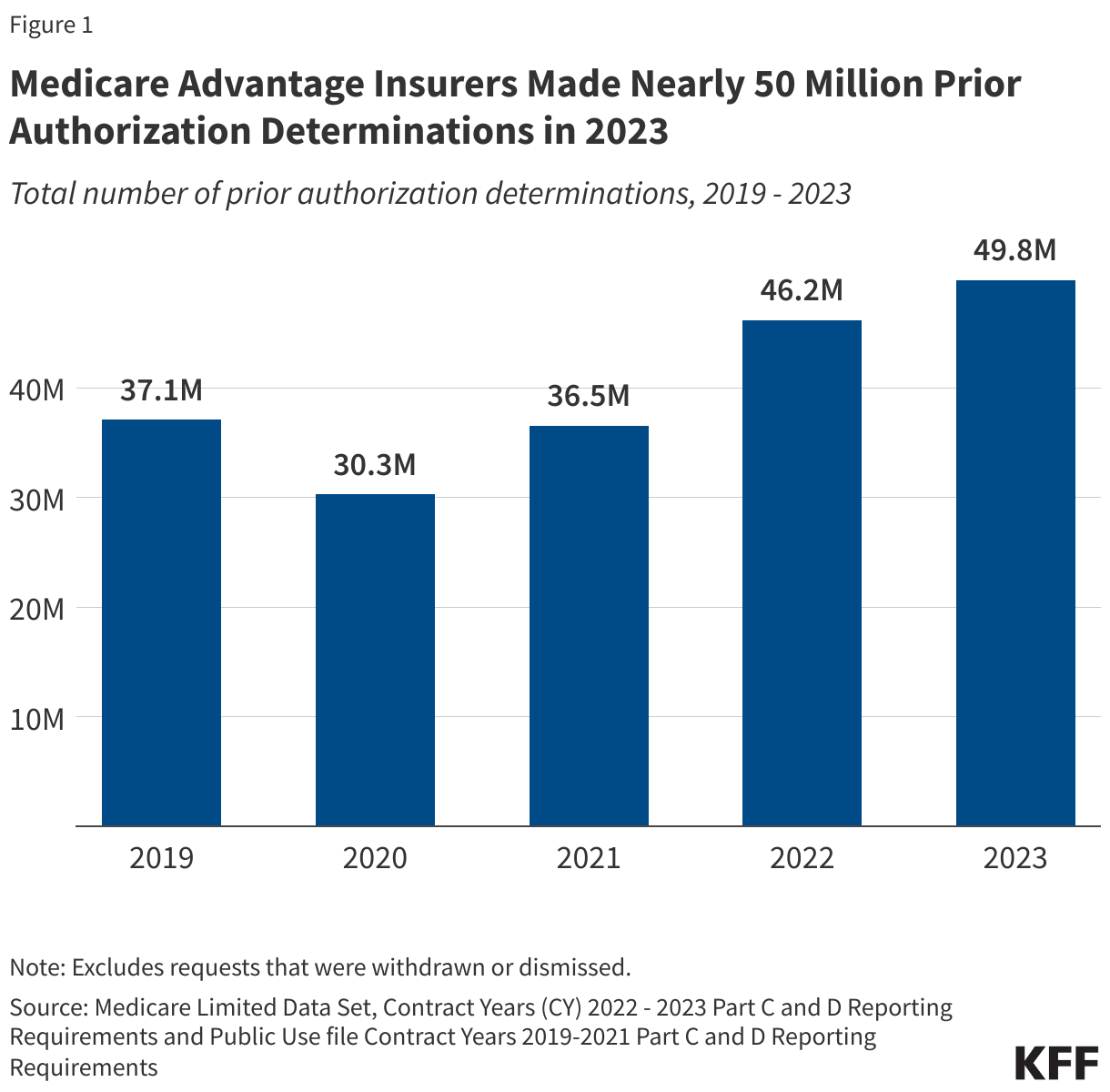

Medicare Advantage Insurers Made Nearly 50 Million Prior Authorization Determinations in 2023

Virtually all enrollees in Medicare Advantage (99%) are required to obtain prior authorization for some services – most commonly, higher cost services, such as inpatient hospital stays, skilled nursing facility stays, and chemotherapy. This contrasts with traditional Medicare, where only a limited set of services, including certain outpatient hospital services, non-emergency ambulance transport, and durable medical equipment, require prior authorization (see Box 1).

Prior authorization requirements are intended to ensure that health care services are medically necessary by requiring approval before a service or other benefit will be covered. Medicare Advantage insurers typically use prior authorization, along with other tools, such as provider networks, to manage utilization and lower costs. This may contribute to their ability to offer extra benefits and reduced cost sharing, typically for no additional premium, while maintaining strong financial performance. At the same time, prior authorization processes and requirements, including the use of artificial intelligence to review requests, may result in administrative hassles for providers, delays for patients in receiving necessary care, and in some instances, denials of medically necessary services, such as post-acute care.

This analysis uses data submitted by Medicare Advantage insurers to the Centers for Medicare and Medicaid Services (CMS) to examine the trends in the number of requests for prior authorization determinations, denials, and appeals for 2019 through 2023, as well as differences across Medicare Advantage insurers. It does not include determinations or denials by type of service or plan because CMS does not collect or report this information, though such data could help inform consumers in choosing among plans. It also presents data from CMS about the use of prior authorization in traditional Medicare, including the number of reviews and denials for 2021 through 2023, and the share appealed and the outcome of the appeal for 2021 and 2022 (the 2023 data do not include this information).

Key Takeaways:

- Medicare Advantage insurers made nearly 50 million prior authorization determinations in 2023, reflecting steady year-over-year increases since 2021 (37 million) and 2022 (46 million) as the number of people enrolled in Medicare Advantage has grown. The determinations represent requests for approval that providers are required to submit before providing a service. Substantially fewer prior authorization reviews for traditional Medicare beneficiaries were submitted to CMS – just under 400,000 in fiscal year 2023 – though the number of people enrolled in Medicare Advantage and traditional Medicare were similar in these years.

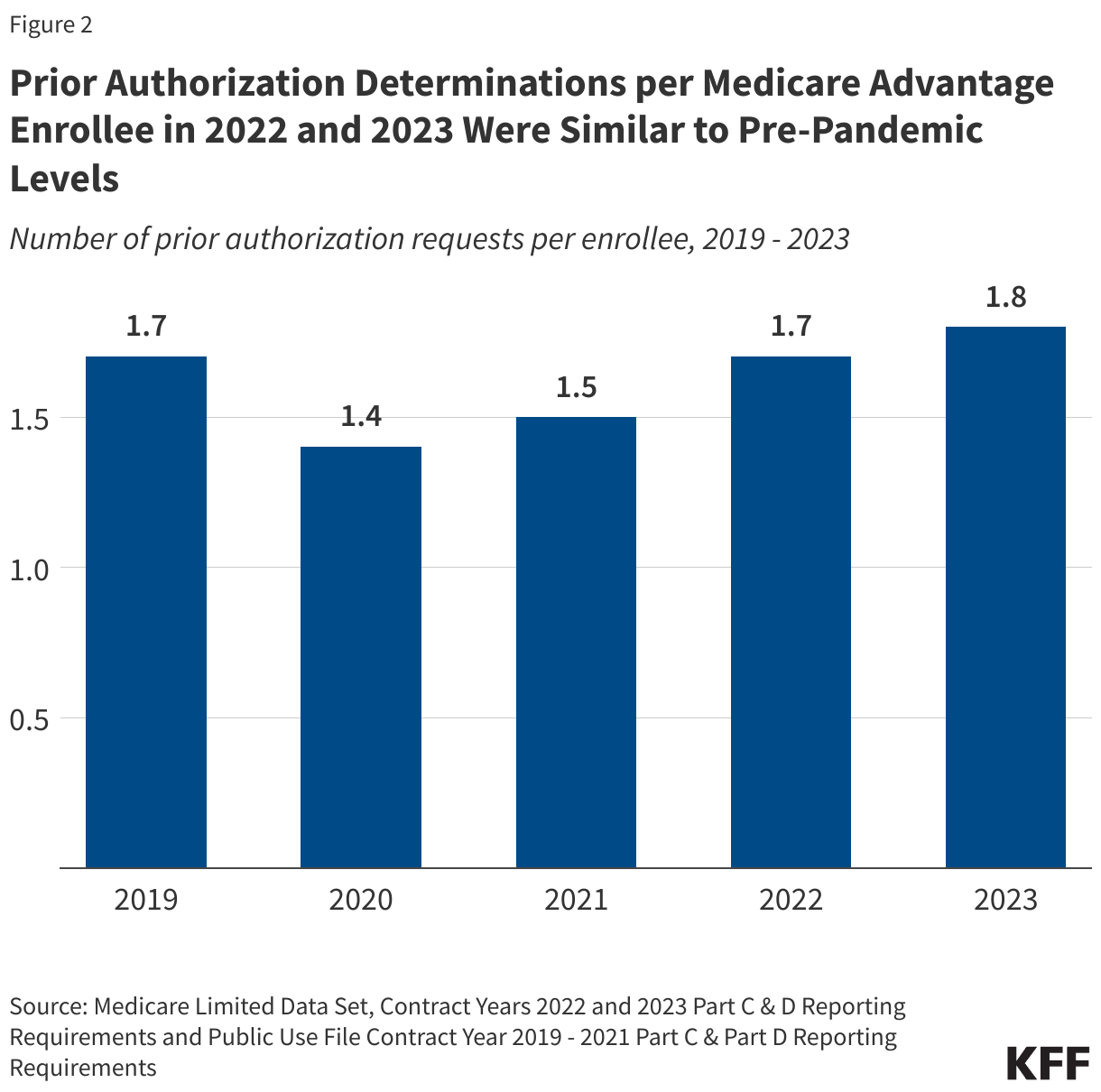

- In 2023, there were nearly 2 prior authorization determinations on average per Medicare Advantage enrollee, similar to the amount in 2019. In contrast, in 2023, about 1 prior authorization review was submitted per 100 traditional Medicare beneficiaries – a rate of about 0.01 per person — which reflects the limited set of services subject to prior authorization in traditional Medicare.

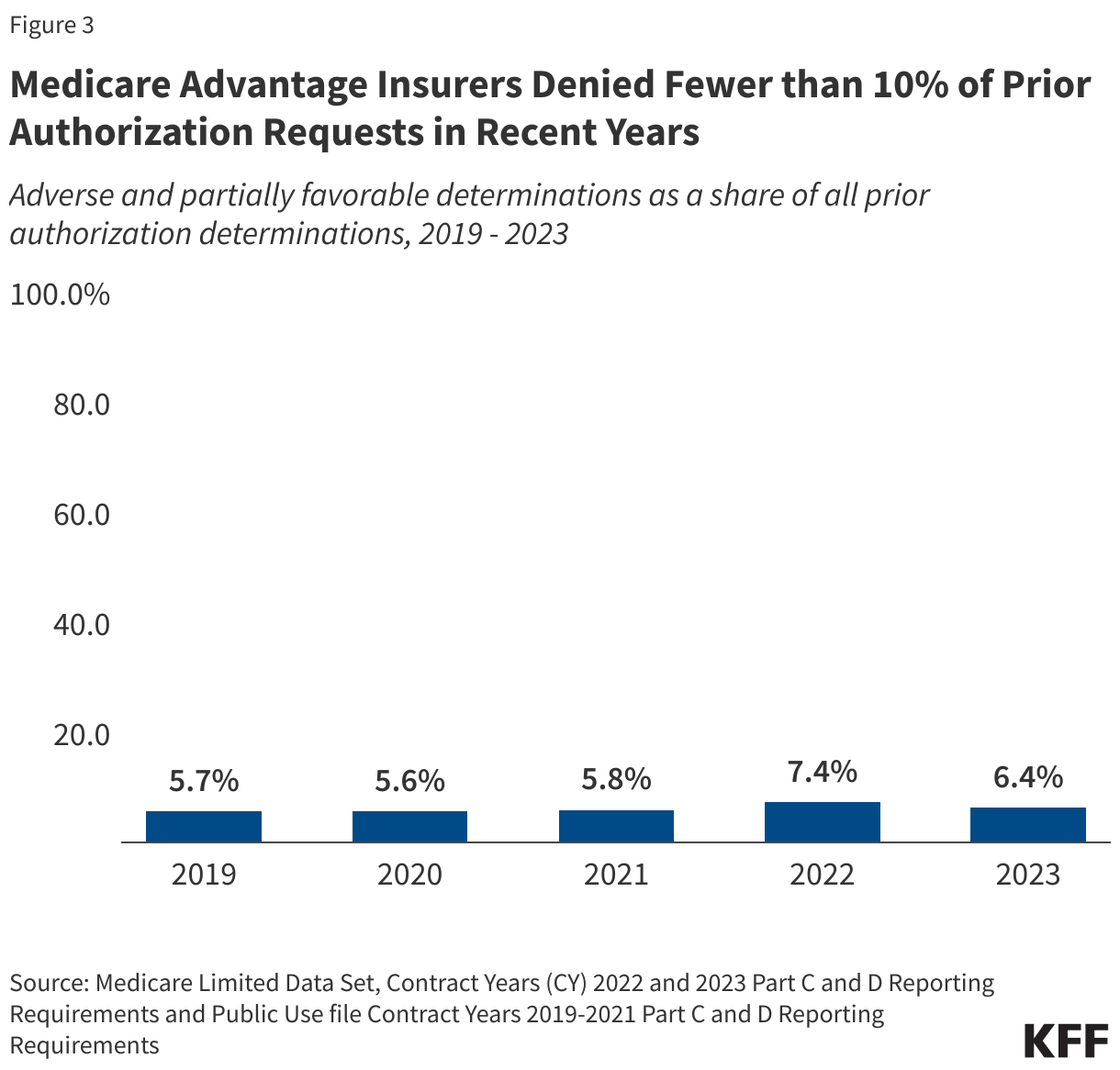

- In 2023, insurers fully or partially denied 3.2 million prior authorization requests, which is a somewhat smaller share (6.4%) of all requests than in 2022 (7.4%). Though there were substantially fewer prior authorization reviews for traditional Medicare beneficiaries, a larger share was denied – 28.8% in 2023. Denial rates varied across the limited set of services subject to prior authorization in traditional Medicare.

- A small share of denied prior authorization requests was appealed in Medicare Advantage (11.7% in 2023). That represents an increase since 2019, when 7.5% of denied prior authorization requests in Medicare Advantage were appealed. A relatively small share of denied prior authorization reviews was appealed in traditional Medicare (6.4% in 2022) as well.

- Though a small share of prior authorization denials were appealed to Medicare Advantage insurers, most appeals (81.7%) were partially or fully overturned in 2023. That compares to less than one-third (29%) of appeals overturned in traditional Medicare in 2022. These requests represent medical care that was ordered by a health care provider and ultimately deemed necessary but was potentially delayed because of the additional step of appealing the initial prior authorization decision. Such delays may have negative effects on a person’s health.

Prior authorization practices have gotten a fair amount of attention in recent years. During the Biden Administration, CMS finalized three rules related to the use of prior authorization in Medicare Advantage. Among other changes, the three rules clarify the criteria that may be used by Medicare Advantage plans to establish prior authorization policies, streamline the prior authorization process for Medicare Advantage and certain other insurers, and require Medicare Advantage plans to evaluate the effect of prior authorization policies on people with certain social risk factors. In December 2024, the outgoing Biden Administration proposed further changes, including clarifying coverage requirements in Medicare Advantage. The Trump Administration will have an opportunity to modify or finalize these proposed changes and may propose additional regulatory changes. Additionally, lawmakers in Congress have held hearings, requested detailed data from the largest Medicare Advantage insurers, and introduced several bills to improve transparency and reform other aspects of prior authorization (see Box 2). Despite bipartisan support encompassing a majority of members in both houses of Congress, legislation on the use of prior authorization has not been enacted.

Use of Prior Authorization in Medicare Advantage

As part of its oversight of Medicare Advantage plans, CMS requires Medicare Advantage insurers to submit data for each Medicare Advantage contract (which usually includes multiple plans) that includes the number of prior authorization determinations made during a year, and whether the request was approved. Insurers are additionally required to indicate the number of initial decisions that were appealed (reconsiderations) and the outcome of that process, including whether the initial decision was affirmed, partially overturned, or fully overturned. These data are useful for assessing overall trends and variations across insurers, but do not contain the information necessary to understand how the use of prior authorization varies by type of service or type of plan.

In 2023, Medicare Advantage insurers made nearly 50 million prior authorization determinations.

After dropping in 2020 amid the initial phase of the COVID-19 pandemic, prior authorization determinations increased steadily between 2021 and 2023 (Figure 1). The decline in 2020 was likely due to both a decline in utilization, as well as the option for insurers to temporarily pause prior authorization requirements during the public health emergency.

The recent increase in the total number of prior authorization determinations since 2020 corresponds to an increase in Medicare Advantage enrollment. Between 2019 and 2023, the number of Medicare Advantage enrollees rose from 22 million people to 31 million people. In 2019, there were approximately 1.7 prior authorization determinations per Medicare Advantage enrollee. That number dropped at the onset of the COVID-19 pandemic to 1.4 in 2020 and 1.5 in 2021, before returning to the pre-pandemic level of 1.7 determinations per enrollee in 2022 and rising slightly to 1.8 in 2023 (Figure 2).

Medicare Advantage insurers denied 3.2 million (6.4%) prior authorization requests in 2023.

Of the 49.8 million prior authorization determinations in 2023, more than 90% (46.6 million) were fully favorable, meaning the requested item or service was approved in full. However, the remaining 3.2 million prior authorization determinations (6.4%) were unfavorable, meaning they were denied in full or in part by Medicare Advantage insurers. This is slightly lower than the 7.4% of requests that were denied in 2022 (which amounted to 3.4 million denials) (Figure 3). Both the share and number of requests denied was higher in 2023 than in 2019. Across all years, most denials (81% in 2023, data not shown) were denied in full, while a minority of denials were determined to be partially favorable, meaning that only part of the request was approved. For example, the insurer may have approved 10 of 14 requested therapy sessions.

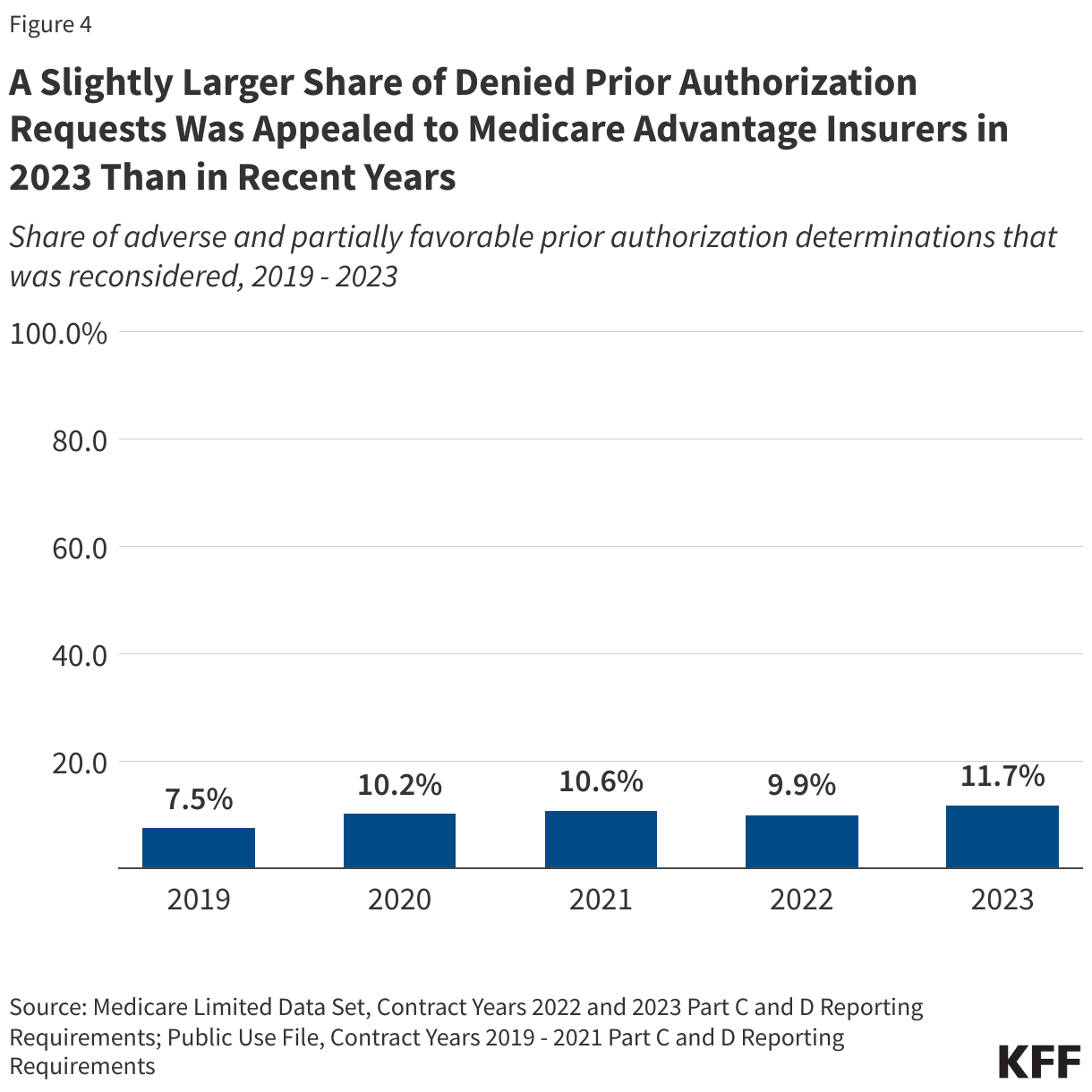

Just 11.7% of denied prior authorization requests were appealed to Medicare Advantage insurers in 2023.

The majority of the 3.2 million denied prior authorization requests were not appealed, similar to previous years. In 2019, just 7.5% of all denials were appealed. That share increased somewhat in 2020 to 10.2% and was relatively stable in 2021 (10.6%) and 2022 (9.9%) (Figure 4). These include appeals of determinations that were both fully and partially denied.

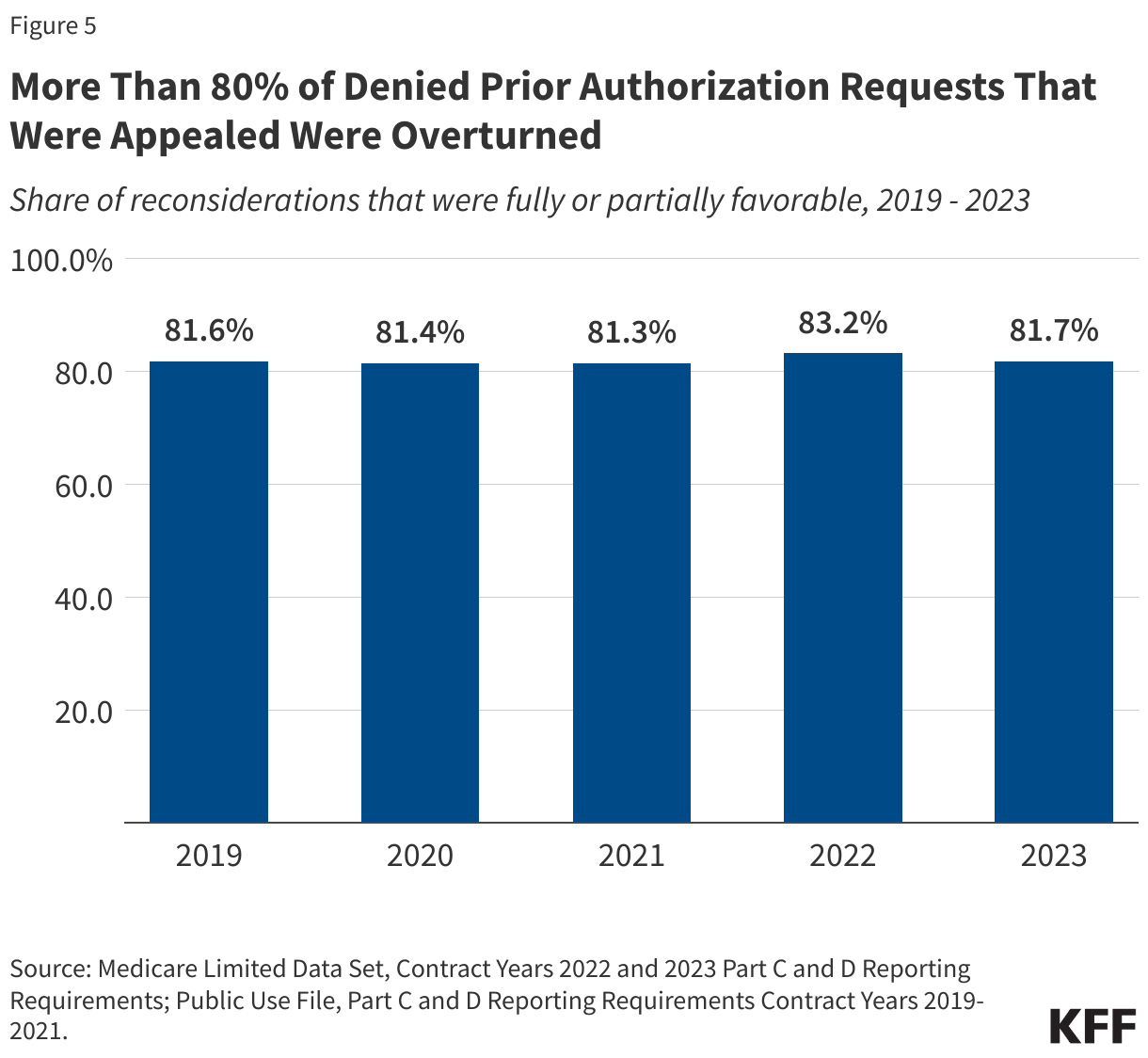

The vast majority of denied prior authorization requests that were appealed were subsequently overturned by Medicare Advantage insurers.

From 2019 through 2023, more than eight in ten (81.7%) denied prior authorization requests that were appealed were overturned (Figure 5). This raises questions about whether the initial request should have been approved, although it could also indicate that the initial request was missing the required documentation to justify the service. In either case, patients potentially faced delays in obtaining services that were ultimately approved because of the prior authorization process.

Variation in Use of Prior Authorization Across Medicare Advantage Insurers in 2023

In 2023, the volume of prior authorization determinations varied across Medicare Advantage insurers, as did the share of requests that were denied, the share of denials that were appealed, and the share of decisions that were overturned upon appeal, meaning people may have different experiences depending on the Medicare Advantage plan in which they enroll.

Across most insurers, a higher number of prior authorization determinations per enrollee was correlated with a smaller share of requests being denied and vice versa. For example, prior authorization determinations for UnitedHealthcare and Humana, the two largest Medicare Advantage insurers, were among the highest (Humana, 3.1 determinations per enrollee) and lowest (UnitedHealthcare, 1.0 determinations per enrollee) observed, and correspondingly, denial rates were below average (Humana, 3.5%) and above average (UnitedHealthcare, 9.1%) for these insurers.

While all Medicare Advantage insurers require prior authorization for at least some services, there is variation across insurers and plans in the specific services that are subject to these requirements. In addition, some insurers waive prior authorization requirements for certain providers, for example, as part of risk-based contracts or through “gold carding” programs that exempt providers with a history of complying with the insurer’s prior authorization policies.

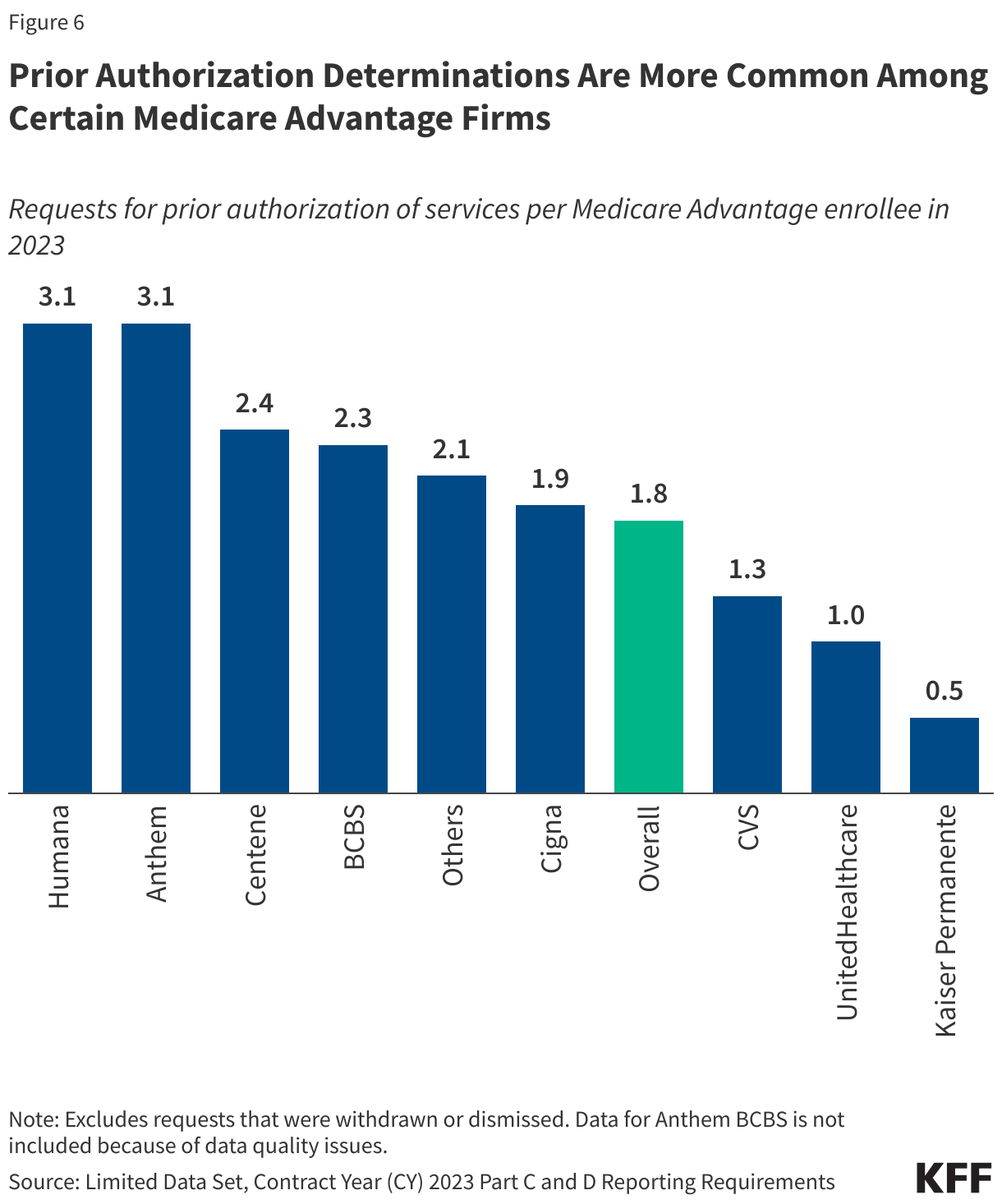

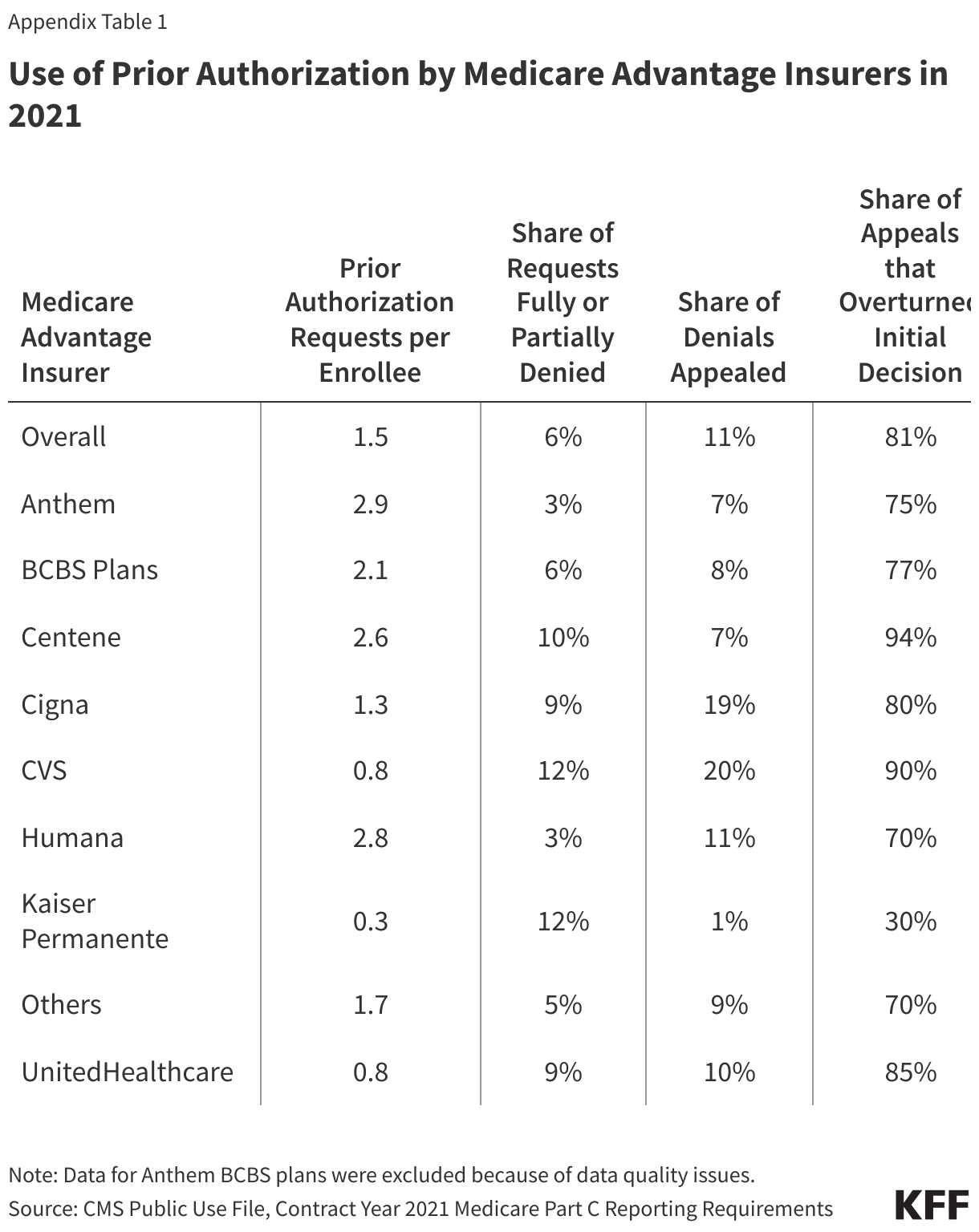

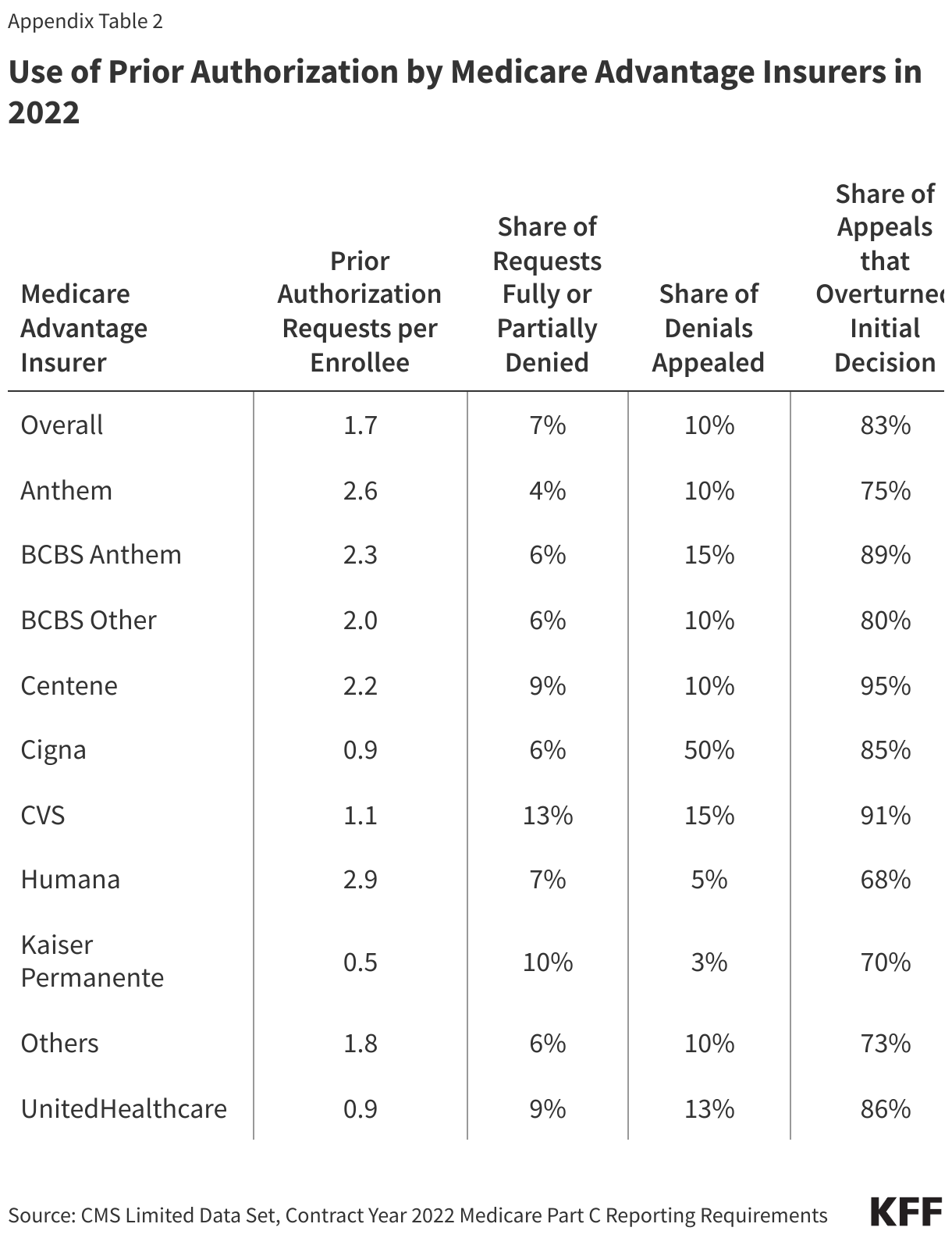

Prior authorization determinations were most common among Humana and Anthem plans.

The number of prior authorization determinations per enrollee ranged from a low of 0.5 determinations per enrollee in Kaiser Permanente plans to a high of 3.1 determinations per enrollee in Humana and Anthem plans (Figure 6). Kaiser Permanente is atypical among insurers in that it generally operates its own hospitals and contracts with an affiliated medical group. Looking across insurers that are more similar, the low end of the range was 1.0 determinations per enrollee in UnitedHealthcare plans. Differences across Medicare Advantage insurers in the number of prior authorization determinations per enrollee likely reflect some combination of differences in the services subject to prior authorization requirements, the frequency with which contracted providers are exempted from those requirements (which may be related to the extent to which providers are affiliated with the insurer), how onerous the prior authorization process is for a particular insurer relative to others, and differences in enrollees’ health conditions and the health care services they use.

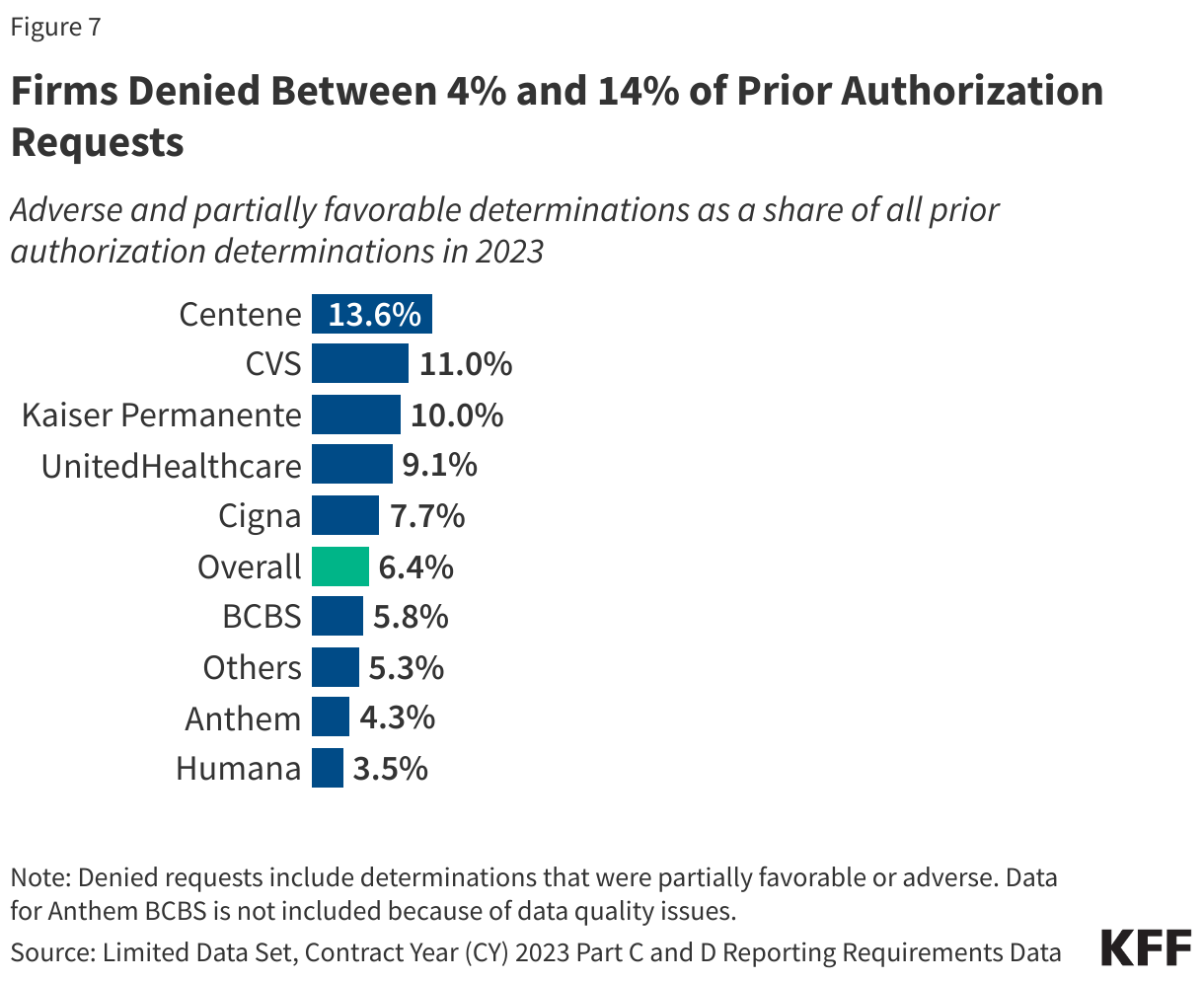

Centene denied the highest share or prior authorization requests while Humana denied the fewest.

The denial rate ranged from 3.5% of prior authorization requests for Humana plans to 13.6% of prior authorization requests for Centene plans (Figure 7). The overall denial rate includes requests that were both fully and partially denied (adverse and partially favorable determinations, respectively).

Most insurers that had more prior authorization determinations per enrollee than average denied a smaller share of requests than average and vice versa. Centene was an exception with both a relatively high number of prior authorization determinations (2.4 per enrollee) and the highest denial rate (13.6%).

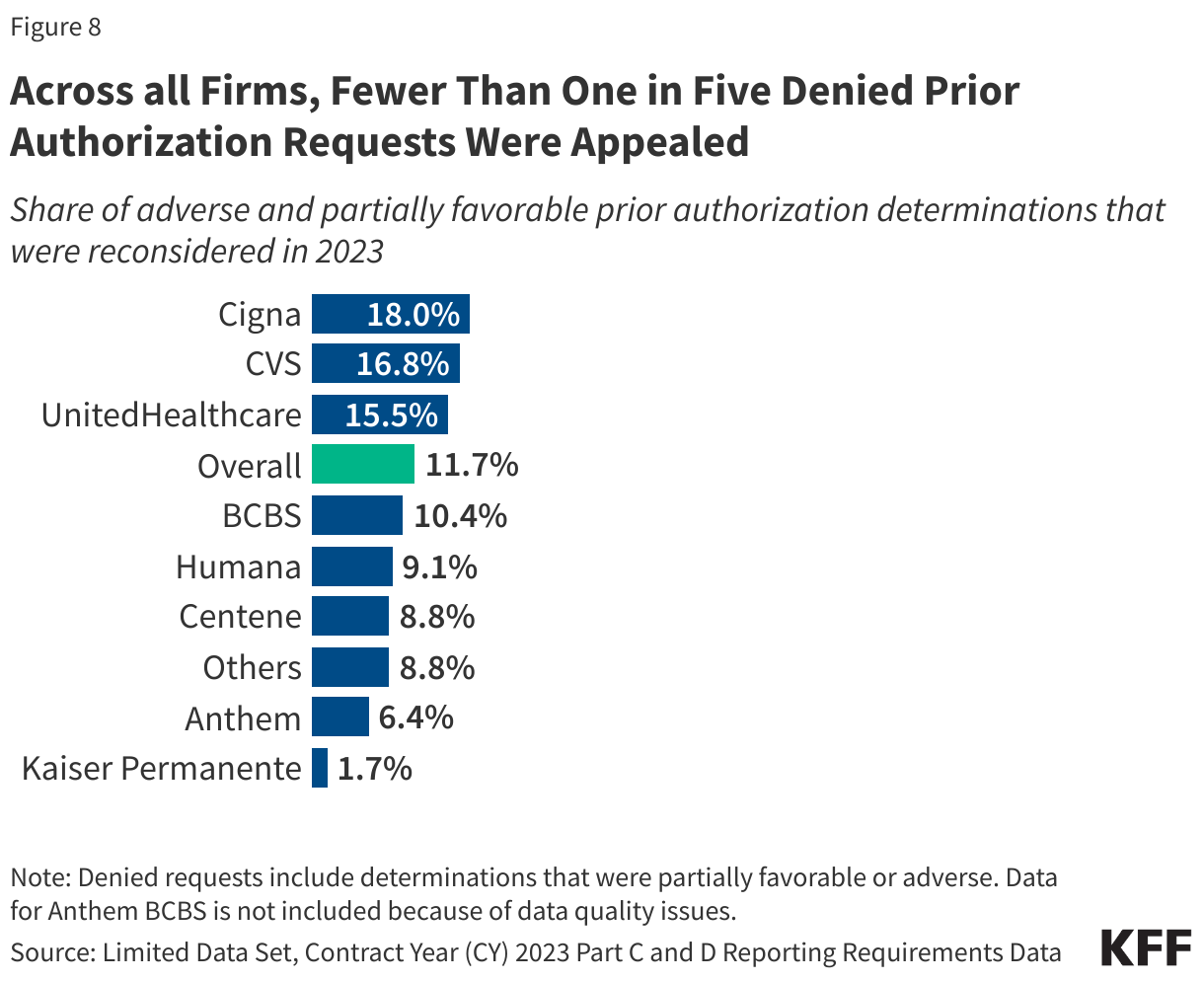

Across all insurers, a small share of denials was appealed.

Fewer than one in five denied prior authorization requests were appealed across all firms. The shares ranged from 1.7% for Kaiser Permanente to 18.0% for Cigna (Figure 8).

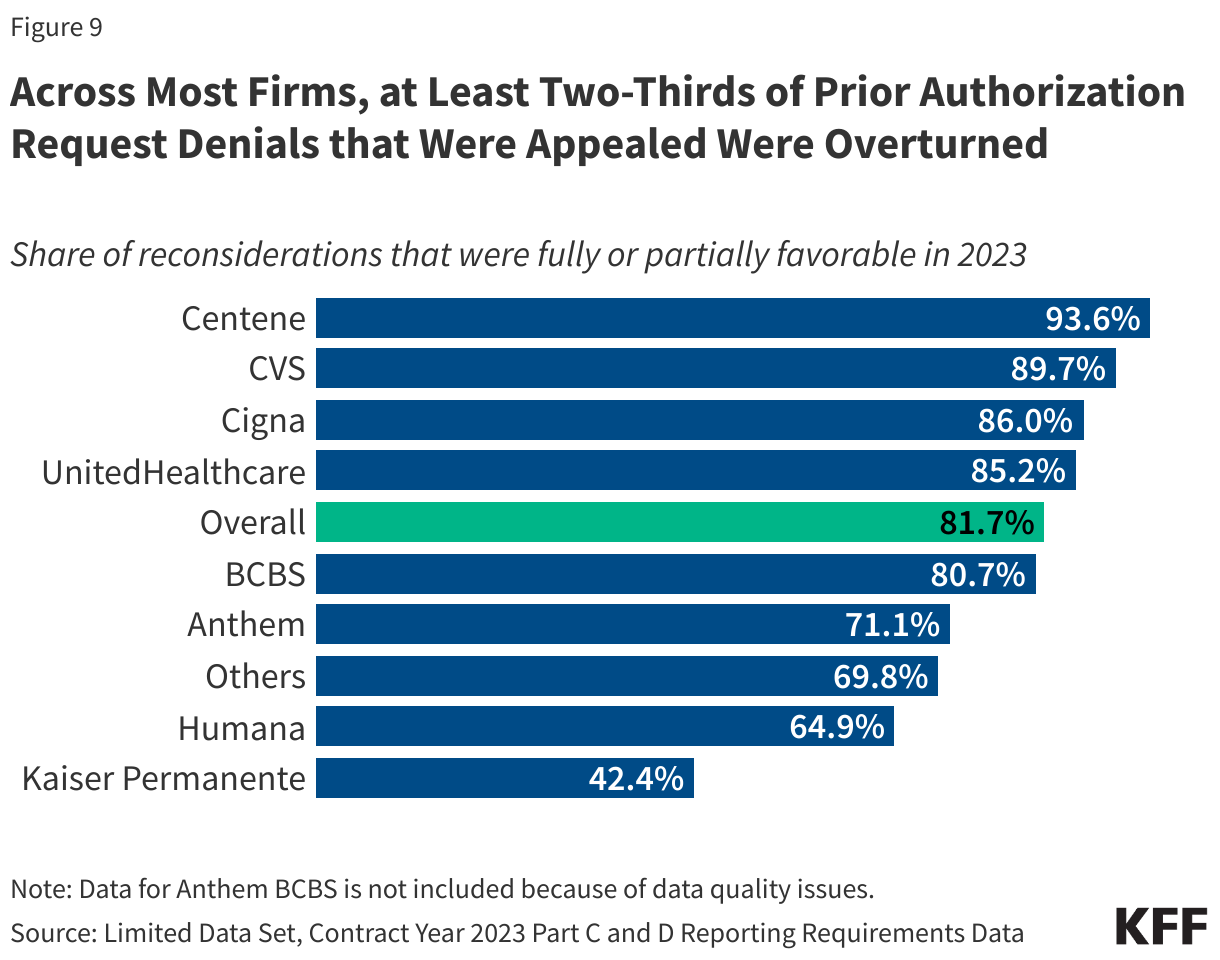

Across most firms, at least two-thirds of appeals were successful.

Even though most denials were not appealed, when they were, most of the initial decisions were partially or fully overturned. The share of appeals that resulted in favorable decisions was lowest for Kaiser Permanente (42.4%) and highest for Centene (93.6%), which also had the highest share of requests initially denied (Figure 9).

The Use of Prior Authorization in Traditional Medicare

The use of prior authorization is relatively new to traditional Medicare and only used for a limited set of services, including certain outpatient hospital services, non-emergency ambulance transport, and durable medical equipment (see Box 1). The prior authorization process does not change any documentation requirements that are not already necessary for receiving Medicare payment – they are just required earlier in the process. CMS has recently published two reports presenting data on the use of prior authorization in traditional Medicare for fiscal years 2021, 2022, and 2023. These reports include information on the number of reviews completed and the number and share of reviews that were affirmed. For 2021 and 2022 only, the data also include information on appeals and the outcome of the appeal.

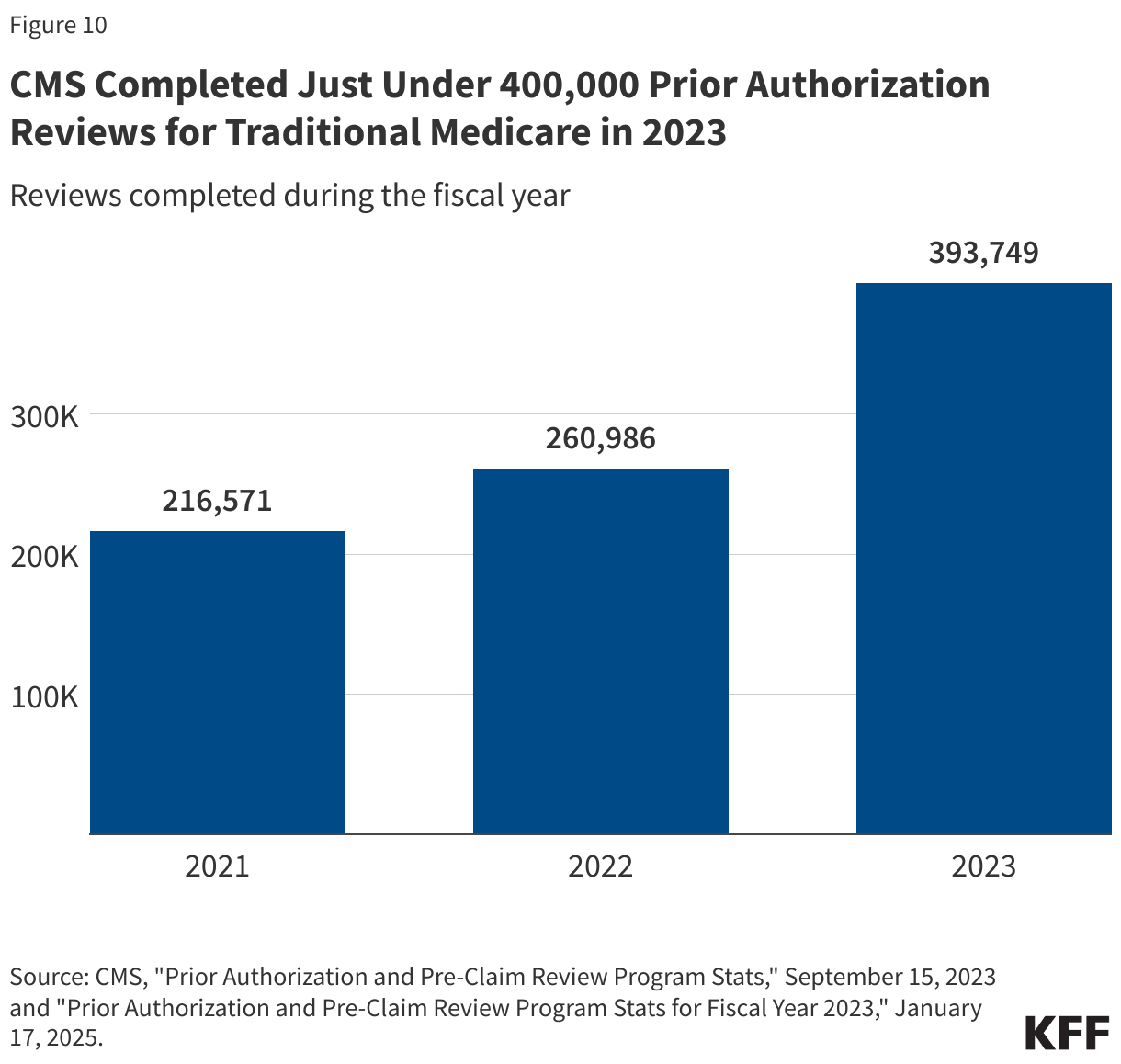

Just under 400,000 prior authorization reviews were completed by CMS for traditional Medicare in 2023.

Across the three categories of services that required prior authorization for certain services, there were 216,571 reviews completed in 2021, 260,986 reviews completed in 2022, and 393,749 reviews completed in 2023 (Figure 10). This translates to about 1 prior authorization review per 100 traditional Medicare beneficiaries in 2023 – a rate of about 0.01 per person.

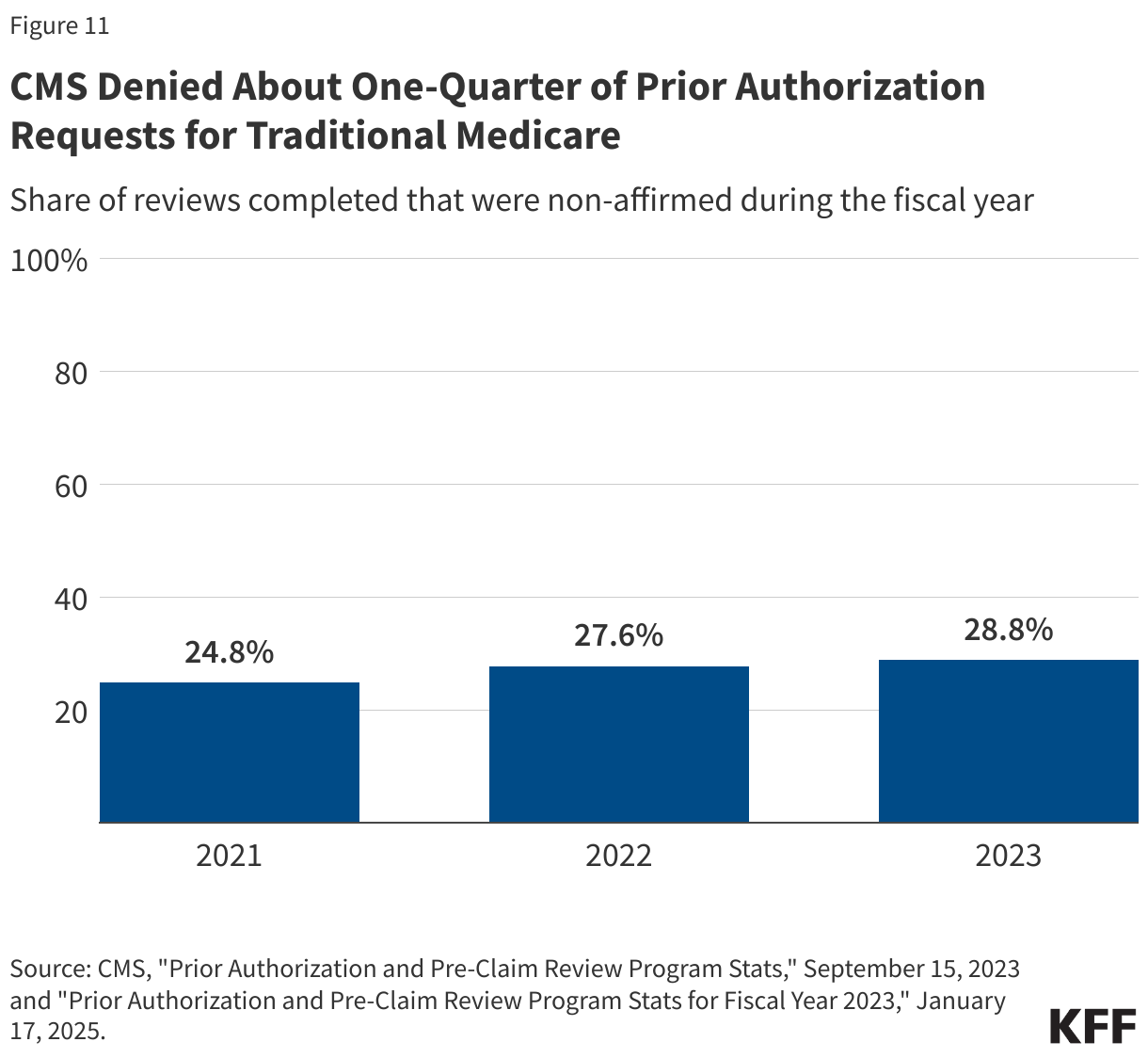

About one-quarter of prior authorization reviews in traditional Medicare denied coverage of the service.

CMS approved (or affirmed) coverage in the majority of prior authorization reviews it completed. CMS reported that 24.8% of requests were denied (or non-affirmed) in 2021, 27.6% of requests were denied in 2022, and 28.8% of requests were denied in 2023 (Figure 11). This reflects 53,680 denied requests in 2021, 72,029 denied requests in 2022, and 113,448 denied request in 2023.

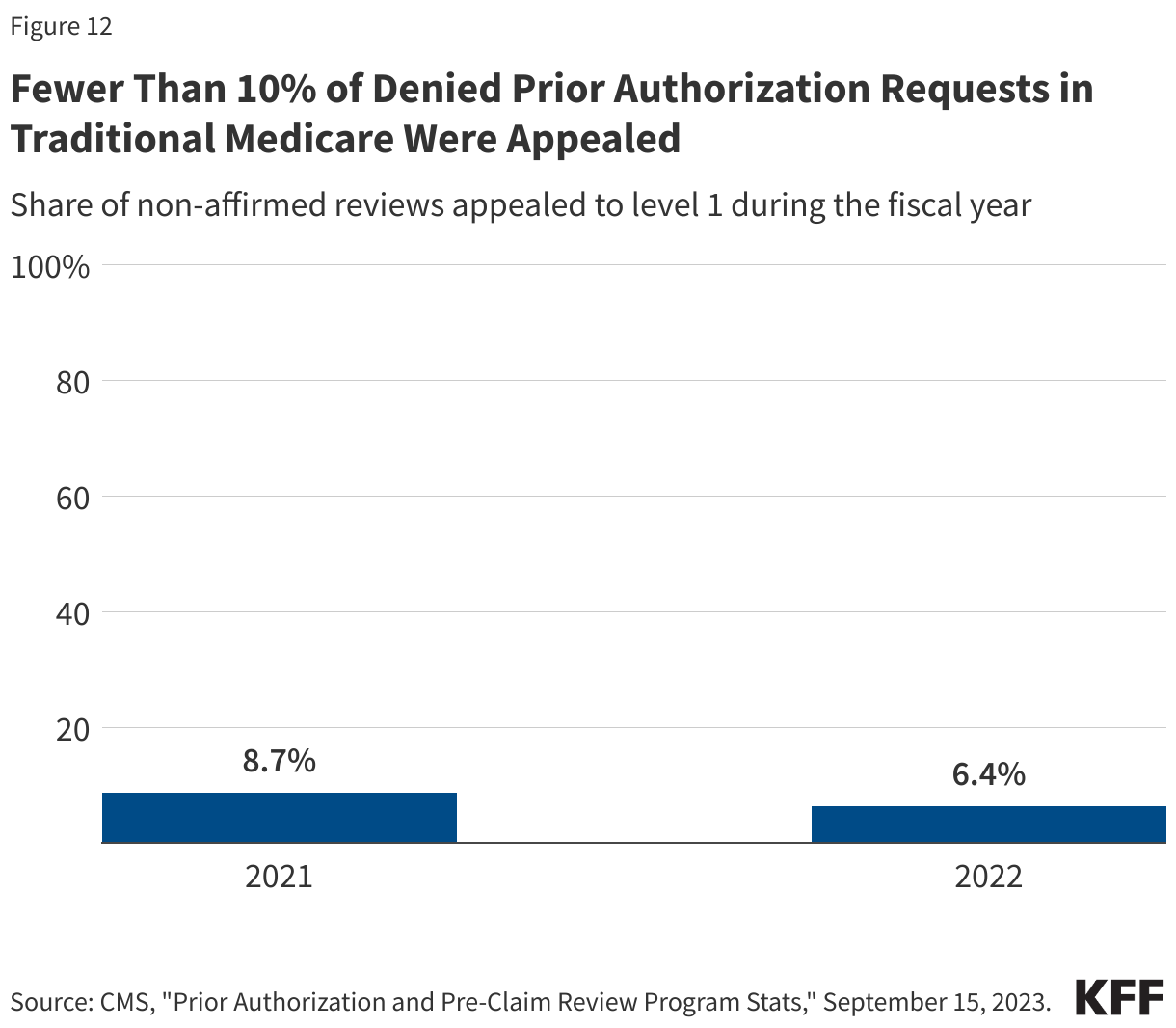

A small share of denied prior authorization requests in traditional Medicare was appealed to CMS.

In both 2021 and 2022, fewer than 5,000 denied prior authorization requests were appealed to the first level. As a share of all denied requests that translates into 8.7% appealed in 2021 and 6.4% appealed in 2022 (Figure 12). Appeals data are presented differently across the two CMS reports. Specifically, the 2023 report includes a separate claims and appeals section for each category of service, which appears to include a broader universe of reviews by Medicare Administrative Contractors, including those for payment of services rendered, than what is presented in the report for 2021 and 2022. Given the differences in the data reported, we present total appeals for 2021 and 2022 only.

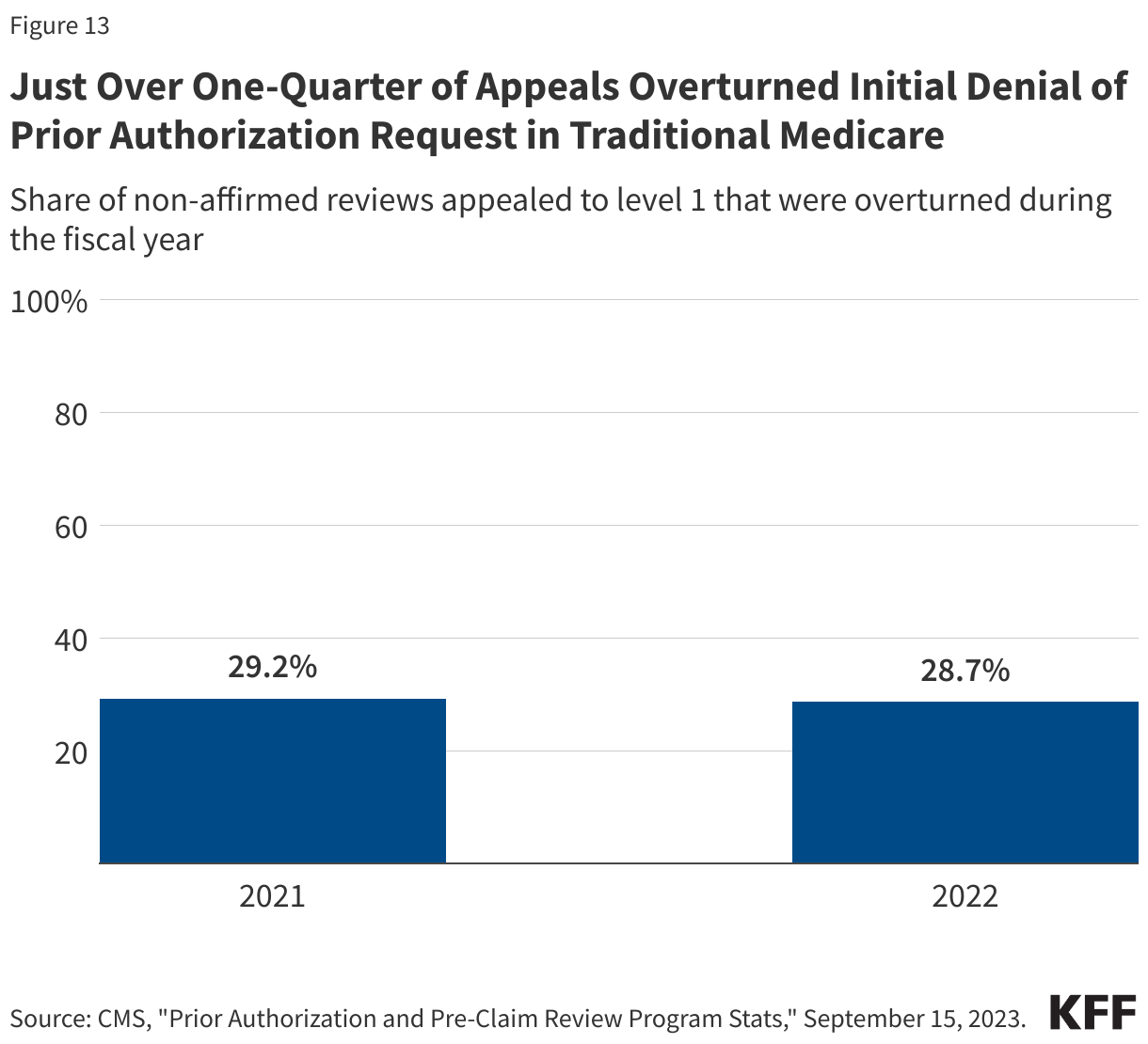

Just over one-quarter of appeals to CMS overturned the denied prior authorization request in traditional Medicare.

In 2021, 1,365 prior authorization denials were overturned upon appeal. In 2022, 1,323 prior authorization denials were overturned upon appeal. That represents 28.7% of all first level appeals in 2022 (Figure 13).

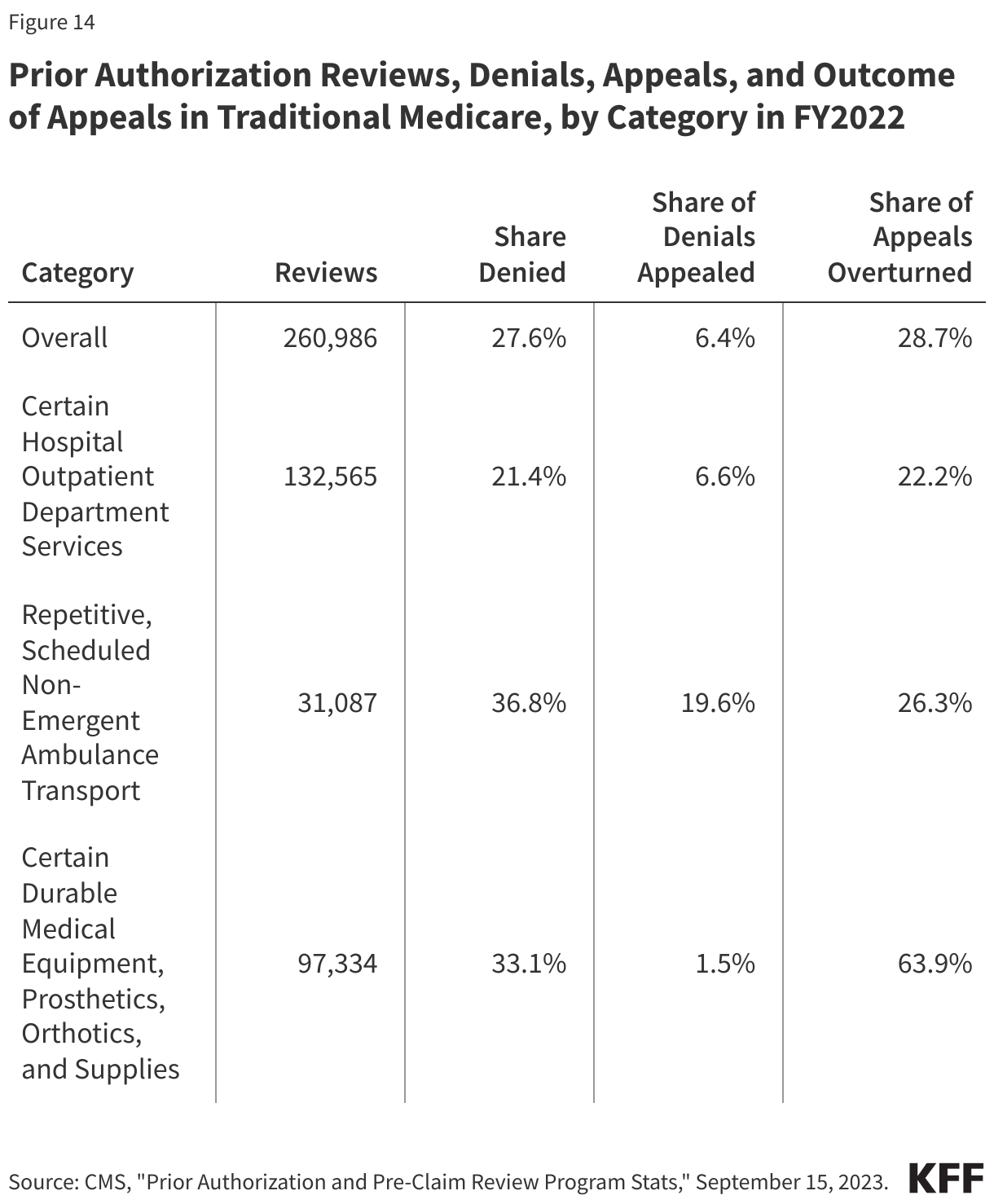

The share of prior authorization reviews that were denied, appealed, and overturned varied across service type in traditional Medicare.

In 2022, the largest number of prior authorization reviews in traditional Medicare were for certain hospital outpatient department services (132,565), followed by reviews for certain durable medical equipment, prosthetics, orthotics and supplies (97,334), which are both applied nationwide. Repetitive, scheduled non-emergent ambulance transport had the fewest number of requests (31,087), which in part may reflect that it became a nationwide program after expanding to additional jurisdictions in 2022, as well as the ability to approve multiple ambulance rides through a single request (Figure 14).

Across the three service categories, denials were most common for repetitive, scheduled non-emergent ambulance transport (36.8%), followed by certain durable medical equipment, prosthetics, orthotics and supplies (33.1%), and least common for certain hospital outpatient department services (21.4%). Denied requests for the ambulance transport services were also most often appealed (19.6%); just 6.6% of denials for certain hospital outpatient services and 1.5% of certain durable medical equipment, prosthetics, orthotics and supplies requests were denied (Figure 14).

The share of appeals that resulted in overturning the initial decision also varied widely. Nearly two-thirds (63.9%) of appeals for durable medical equipment, prosthetics, orthotics and other supplies were successful. That compares to 26.3% of appeals for the ambulance transport services and 22.2% of appeals for certain hospital outpatient services (Figure 14).

Box 1. Prior Authorization Requirements in Traditional Medicare

In 2015, CMS issued a final rule that established a prior authorization process for certain Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (DMEPOS) items, with the goal of reducing the use of items that had been frequently subject to unnecessary utilization. Initial implementation began March 20, 2017, and items have been added and subtracted to the list over the following years through subsequent rulemaking. As of December 18, 2024, the DMEPOS items prior authorizations list includes over 60 items, including for pressure reducing support surfaces, power mobility devices, and lower limb prosthetics.

In a 2019 final rule (effective July 1, 2020), CMS established national prior authorization requirements for a set of hospital outpatient department services which had experienced significant increases in utilization and that are likely to be cosmetic procedures and not covered by Medicare, but may be combined with other therapeutic services, including blepharoplasty, botulinum toxin injections, panniculectomy, rhinoplasty, and vein ablation. In further rulemaking (effective July 1, 2021), CMS added implanted spinal neurostimulators and cervical fusion with disc removal to the list of services requiring prior authorization, and another rule (effective July 1, 2023) added facet joint interventions.

The CMS Repetitive, Scheduled Non-Emergent Ambulance Transport (RSNAT) Prior Authorization Model uses the authority provided through the Center for Medicare and Medicaid Innovation (CMMI, or Innovation Center) to test whether prior authorization for non-emergent ambulances for certain medical appointments would save money for Medicare while maintaining access and quality of care. The model was first implemented in select states in December 2014 and was ultimately expanded nationwide in September 2020 as it met the model requirements, saving Medicare about $650 million over four years.

Box 2. Recent Administrative Actions and Proposed Legislation on Prior Authorization

The Biden Administration finalized three rules related to prior authorization.

The first rule (effective date: June 5, 2023) clarifies the criteria that may be used by Medicare Advantage plans in establishing prior authorization policies and the duration for which a prior authorization is valid. Specifically, the rule states that prior authorization may only be used to confirm a diagnosis and/or ensure that the requested service is medically necessary and that private insurers must follow the same criteria used by traditional Medicare. That is, Medicare Advantage prior authorization requirements cannot result in coverage that is more restrictive than traditional Medicare. The rule also describes how private insurers may consider additional information when traditional Medicare does not have fully established coverage criteria. The rules apply to coverage beginning with plan year 2024.

The second rule (effective date: April 8, 2024) is intended to improve the use of electronic prior authorization processes, as well as the timeliness and transparency of decisions, and applies to Medicare Advantage and certain other insurers. Specifically, it shortens the standard time frame for insurers to respond to prior authorization requests from 14 to 7 calendar days starting in January 2026 and standardizes the electronic exchange of information by specifying the prior authorization information that must be included in application programming interfaces starting in January 2027. A bipartisan bill has also been introduced to codify pieces of this rule.

The third rule (effective date: June 3, 2024) will require Medicare Advantage plans to evaluate the effect of prior authorization policies on people with certain social risk factors (“health equity analysis”) starting with plan year 2025.

In December 2024, CMS issued a proposed rule that contained several provisions related to prior authorization. These include defining the term “internal coverage criteria,” revising the requirements of the health equity analysis to include metrics reported at the service level, and several other changes to further clarify coverage requirements.

Additionally, lawmakers in Congress have introduced several bills aimed at improving the timeliness of the prior authorization process, increasing transparency, clarifying the criteria that may be used in prior authorization decisions, and exempting some providers from prior authorization requirements in the Medicare Advantage program. Other lawmakers have proposed banning the use of prior authorization altogether.

Methods

The analysis of Medicare Advantage uses organization determinations and reconsiderations – Part C data from the Centers for Medicare and Medicaid Services (CMS) Part C and D reporting requirements public use file for contract years 2019 – 2021 and the limited data set for contract years 2022 and 2023. Medicare Advantage insurers submit the required data at the contract level to CMS and CMS performs a data validation check.

Data for Medicare Advantage contracts is aggregated to the parent company level. Insurers with less than 2% of total Medicare Advantage enrollment are combined into “others”. BCBS stands for Blue Cross Blue Shield. BCBS plans that are offered by Anthem (Elevance) are grouped together and those offered by all other parent companies are grouped together (BCBS Other). BCBS Anthem contracts are excluded for 2021 and 2023 because they did not pass the data validation checks.

This analysis reflects data on service determinations and does not include claims determinations (for payment for services already provided). We also do not include withdrawn or dismissed determination requests in this analysis.

The enrollment data are from the CMS Medicare Advantage enrollment file for March of each year at the contract-plan-county level. We then sum up to the contract level to merge with the determination and reconsideration data. Contract-plan-county combinations are not included if there are fewer than 11 enrollees.

The traditional Medicare analysis uses data included “Prior Authorization and Pre-Claim Review Program Stats,” published by CMS on September 15, 2023, which reflects prior authorization reviews completed in fiscal years 2021 and 2022, and “Prior Authorization and Pre-Claim Review Program Stats for Fiscal Year 2023,” published on January 17, 2025. The total number of traditional Medicare beneficiaries is from the Medicare Monthly Enrollment Dashboard for 2021 through 2023. While CMS published data on the use of prior authorization in traditional Medicare for FY2023, the information for appeals of are not comparable to FY2021 and FY2022 data and are therefore not included in this analysis.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.