5 Key Facts About Medicaid Coverage for People With Intellectual and Developmental Disabilities (I/DD)

President Trump signed into law a budget reconciliation package that made major reductions in federal health care spending to offset part of the costs of extending expiring tax cuts. The Congressional Budget Office’s (CBO) latest cost estimate shows that the reconciliation package would reduce federal Medicaid spending over a decade by an estimated $911 billion and increase the number of uninsured people by 10 million, with three quarters of the change stemming from cuts to Medicaid. These reductions could have implications for people with intellectual and developmental disabilities (I/DD) as people with I/DD disproportionately rely on Medicaid.

I/DD include various disabilities such as intellectual disabilities, autism, developmental delays, and learning disabilities. These disabilities are usually present at birth or manifest during childhood and affect the trajectory of the individual’s physical, intellectual, and/or emotional development. Loss of Medicaid coverage or benefits poses unique challenges for people with I/DD, many of whom live on fixed incomes, face barriers to employment and accessing private health coverage, and have high health care needs and spending. People with I/DD are distinct from many other populations who need long-term care as they rely on a broad range of services and supports across the lifespan, while most others who use long-term care often develop care needs later in life. These needs can include assistance with activities of daily living (such as bathing and dressing) and instrumental activities of daily living (such as shopping or cooking), employment-related services, positive behavior supports, and supervision when completing tasks.

According to estimates by the National Council on Disability (NCD), there are at least eight million people in the U.S that have I/DD, though that is likely an underestimate. Other estimates of total number of people in the U.S with I/DD range widely, from eight million to sixteen million people. It is difficult to estimate the exact number because there is no current survey that asks a nationally representative population whether they have an I/DD. The estimated prevalence of I/DD is higher among children than among adults in the U.S., with the NCD noting that about 4% of U.S. children and 2% of U.S. adults have an I/DD (though these rates are much lower than the rate of I/DD in the National Health Interview Survey, which are closer to 14% among U.S. children).

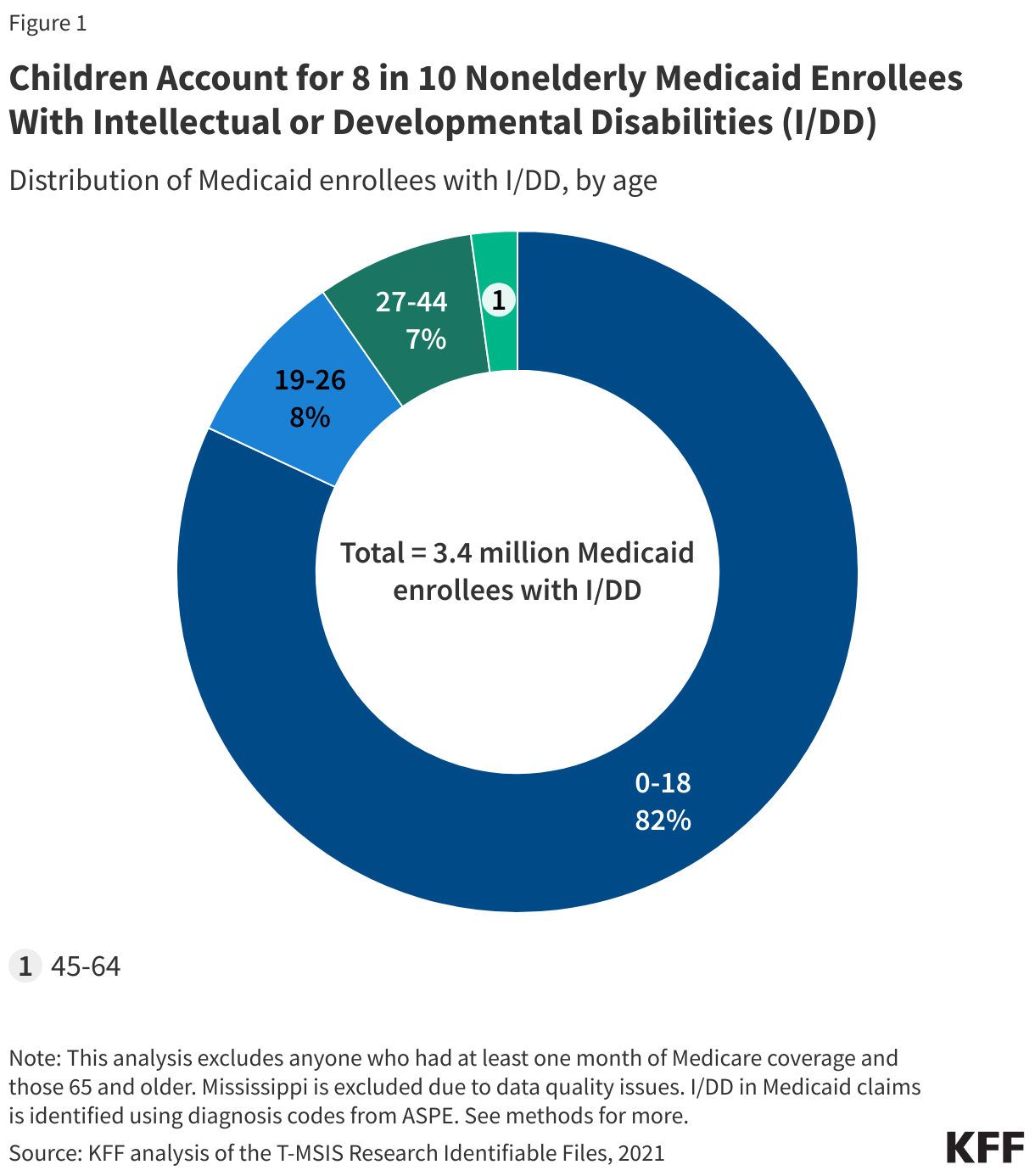

1. Children account for 8 in 10 nonelderly Medicaid enrollees with intellectual or developmental disabilities.

In 2021, there were 3.4 million Medicaid enrollees under age 65 with I/DD, 82% of whom were children under 19 (Figure 1). Medicaid offers additional benefits to children with I/DD beyond what is available to children enrolled in private health insurance and often what is available to adult Medicaid enrollees. This makes Medicaid a key source of coverage for children with I/DD. Under the Early and Periodic Screening, Diagnostic and Treatment (EPSDT), states must provide children with screening for health and developmental problems and with all services needed to diagnose and treat their health conditions, regardless of whether the services are covered for adults or if they are otherwise not covered by the state. States also offer an array of additional optional benefits for people with I/DD through Medicaid waivers, including private duty nursing, specialized therapies, home/vehicle modifications, and more. Those benefits are generally not covered by private insurance.

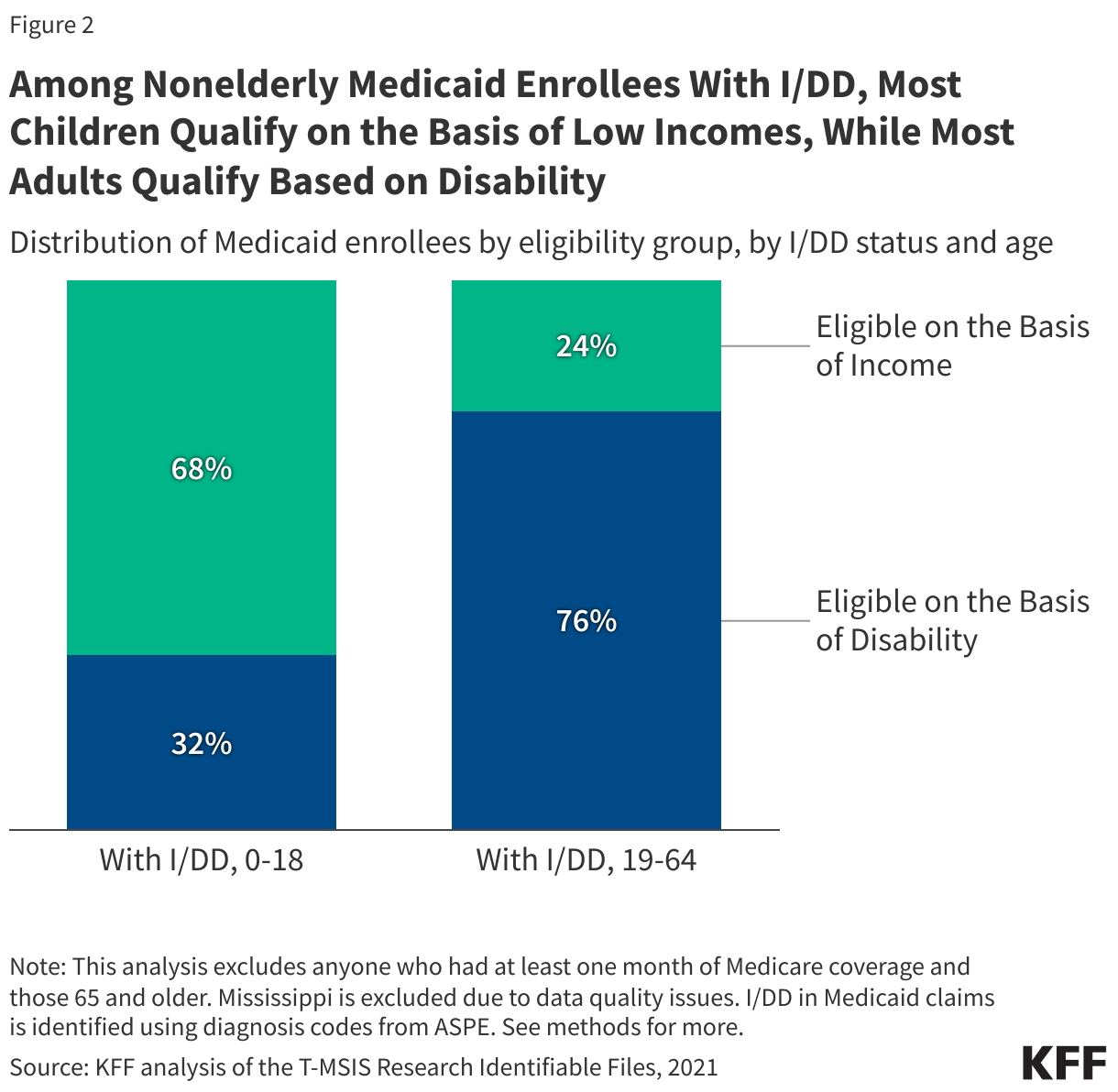

2. Among nonelderly Medicaid enrollees with I/DD, most children qualify on the basis of low incomes, while most adults qualify based on disability.

Over two-thirds (68%) of children with I/DD qualify for Medicaid on the basis of low income alone, compared with fewer than one in four nonelderly adults with I/DD (24%). The remaining 32% of children and 76% of nonelderly adults with I/DD qualify on the basis of disability. Qualifying on the basis of disability requires demonstration of limited income, limited savings, and meeting disability requirements. Beyond requiring additional information from applicants, KFF’s survey of states on their eligibility practices has shown that qualifying on the basis of disability tends to have more cumbersome application and renewal processes. Both children and nonelderly adults with I/DD are more likely to qualify for Medicaid through a disability-related pathway than are children and nonelderly adults without I/DD (among whom only 9% qualify for Medicaid on the basis of disability, data not shown).

Child eligibility remains the highest for all income-based eligibility pathways, with a median eligibility level of 255% FPL, or $67,957 for a family of three. This is a key reason why most children with I/DD are eligible on the basis of income while most adults under age 65 are not. In general, children with disabilities are eligible for all of the pathways available to nonelderly adults with disabilities, though eligibility criteria may differ between children and nonelderly adults and be less restrictive for children. The ACA expansion pathway was created to provide coverage to low-income adults under age 65 without requiring another eligibility factor like disability. This pathway has helped some nonelderly adults with I/DD maintain access to services which are only covered through Medicaid programs, such as long-term care. However, some provisions in the reconciliation package target those enrolled through the ACA expansion, putting this coverage at risk.

Many state Medicaid agencies set their age cut-offs for child pathways between 19 and 21, but children with special health care needs, including I/DD, often need the care that the Medicaid program provides throughout their lifetime. As people transition out of child Medicaid eligibility, they often encounter barriers to maintaining coverage because of the lower adult income eligibility levels. Among those who continue to qualify for Medicaid, they may lose access to benefits that are particularly critical for children with I/DD and only available through the EPSDT benefit (which is only available for people under age 21 in all states). Families of children with special health care needs who are aging out of child benefits report that there is frequently a lack of clear information available to them and that they are often unprepared for the transition.

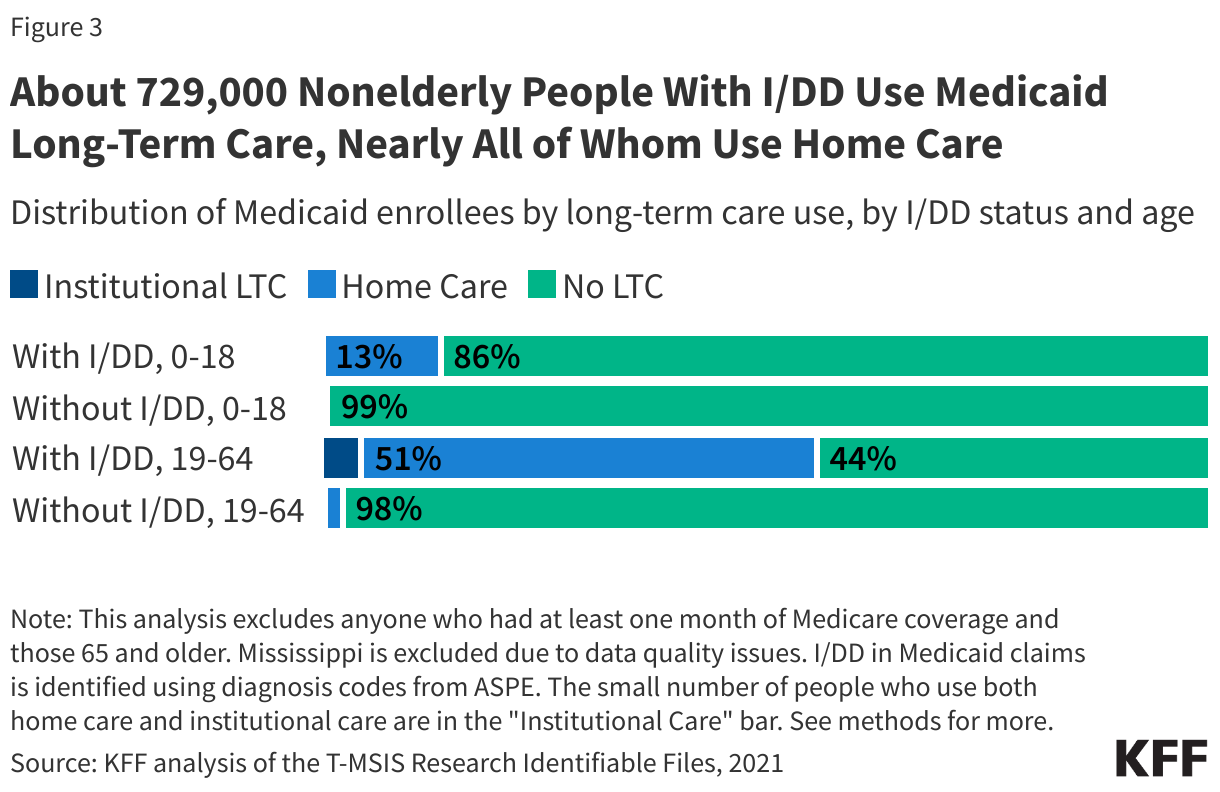

3. About 729,000 nonelderly people with I/DD use Medicaid long-term care, nearly all (700,000) of whom use home care.

Over one in ten child enrollees with I/DD and over half of nonelderly adult enrollees with I/DD use long-term care, nearly all of which is home care. Medicaid is the primary payer for long-term care in the U.S, and most people who use Medicaid long-term care use home care. Medicaid home care can be offered through either the Medicaid state plan or as part of a specialized waiver. Nearly all states (48) provide Medicaid home care through waivers that offer benefits specifically targeted to people with I/DD. These waivers may provide a range of services including supported employment; equipment, technology, and modifications; home-based services; day services; non-medical transportation; round-the-clock-services; personal care services; and home-delivered meals. Some home care waivers for children are age-limited and end after they turn 21 (or younger). While some waivers define transition of care services and transition plans, many do not. Some states may offer similar waivers for adults, though benefits may differ and enrollment may not be guaranteed due to limited availability of waiver slots. In Medicaid home care, many people “self-direct” their services, allowing them to provide payments to family caregivers in some cases. Beyond paying for their caregiving, Medicaid supports family caregivers with services such as training, support groups, and respite care (which is paid care that allows family caregivers to take a break from their normal responsibilities).

Very few Medicaid enrollees with I/DD use long-term care in institutional settings such as nursing facilities or intermediate care facilities. Nursing facility care is a required Medicaid benefit, in contrast with home care, which is provided at state option. Care at intermediate care facilities (a type of institutional care that is often targeted towards people with I/DD) is also optional for states to provide, but all states offer it. Most people with I/DD using institutional long-term care are in intermediate care facilities (data not shown).

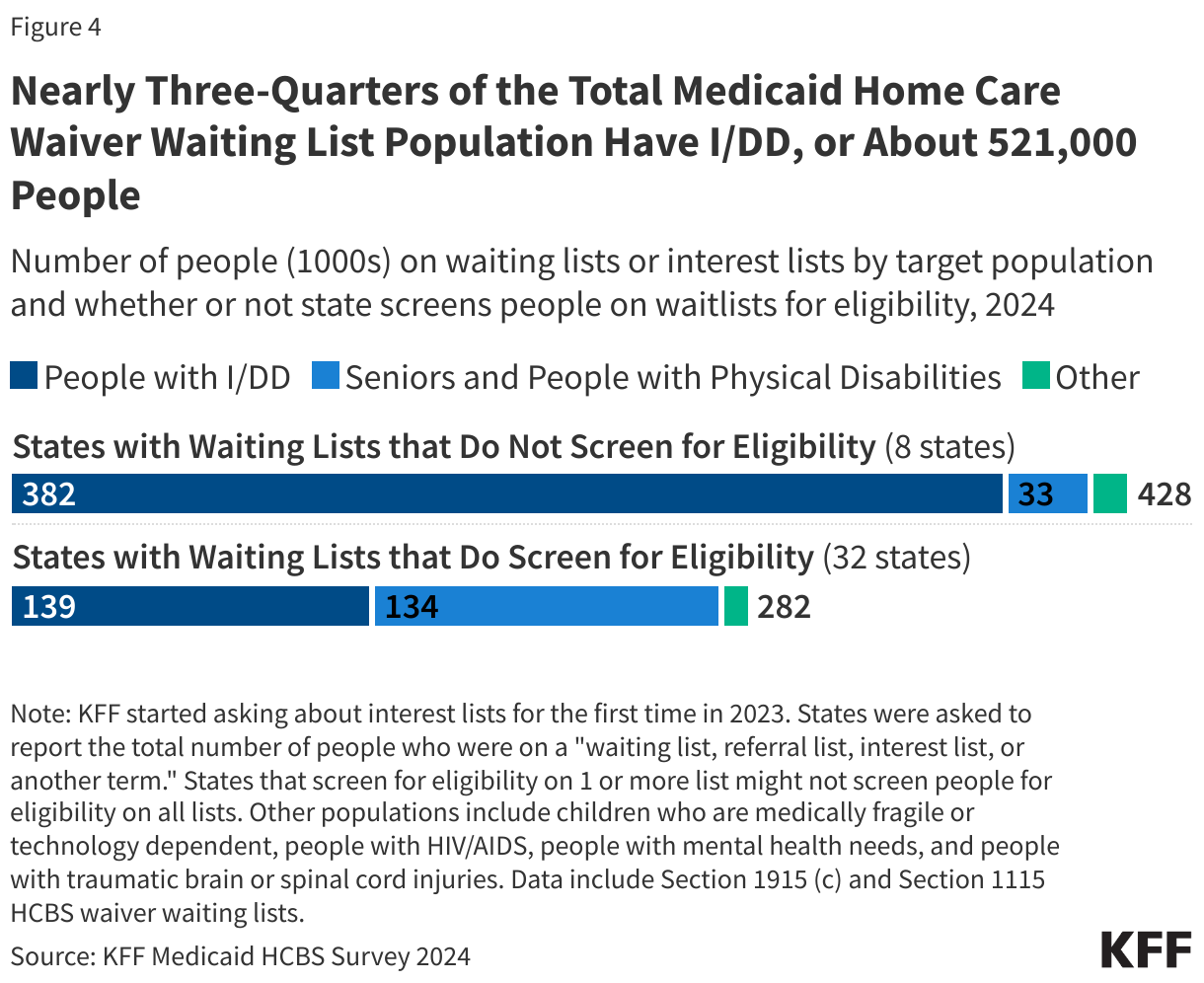

4. Nearly three-quarters of the total Medicaid home care waiver waiting list population have I/DD, or about 521,000 people.

A state’s ability to cap the number of people enrolled in home care waivers can result in waiting lists when the number of people seeking services exceeds the number of waiver slots available. Waiting lists provide an indication of people who may need services they are not receiving, but they are an incomplete measure of unmet need because they don’t include people with unmet needs in states that do not cover the applicable services (and therefore, have no waiting list) or people who are in the waiver but not receiving services because there are too few providers available. Waiting lists reflect the populations a state chooses to serve, the services it decides to provide, the resources it commits, and the availability of workers to provide services. People with I/DD comprise almost three-quarters (73%) of the total home care waiver waiting list population, and reflect a higher share of people in states that do not screen for waiver eligibility before placing someone on a waiting list (89% in in the eight states that do not screen for eligibility and 49% in the 32 states that do screen for eligibility).

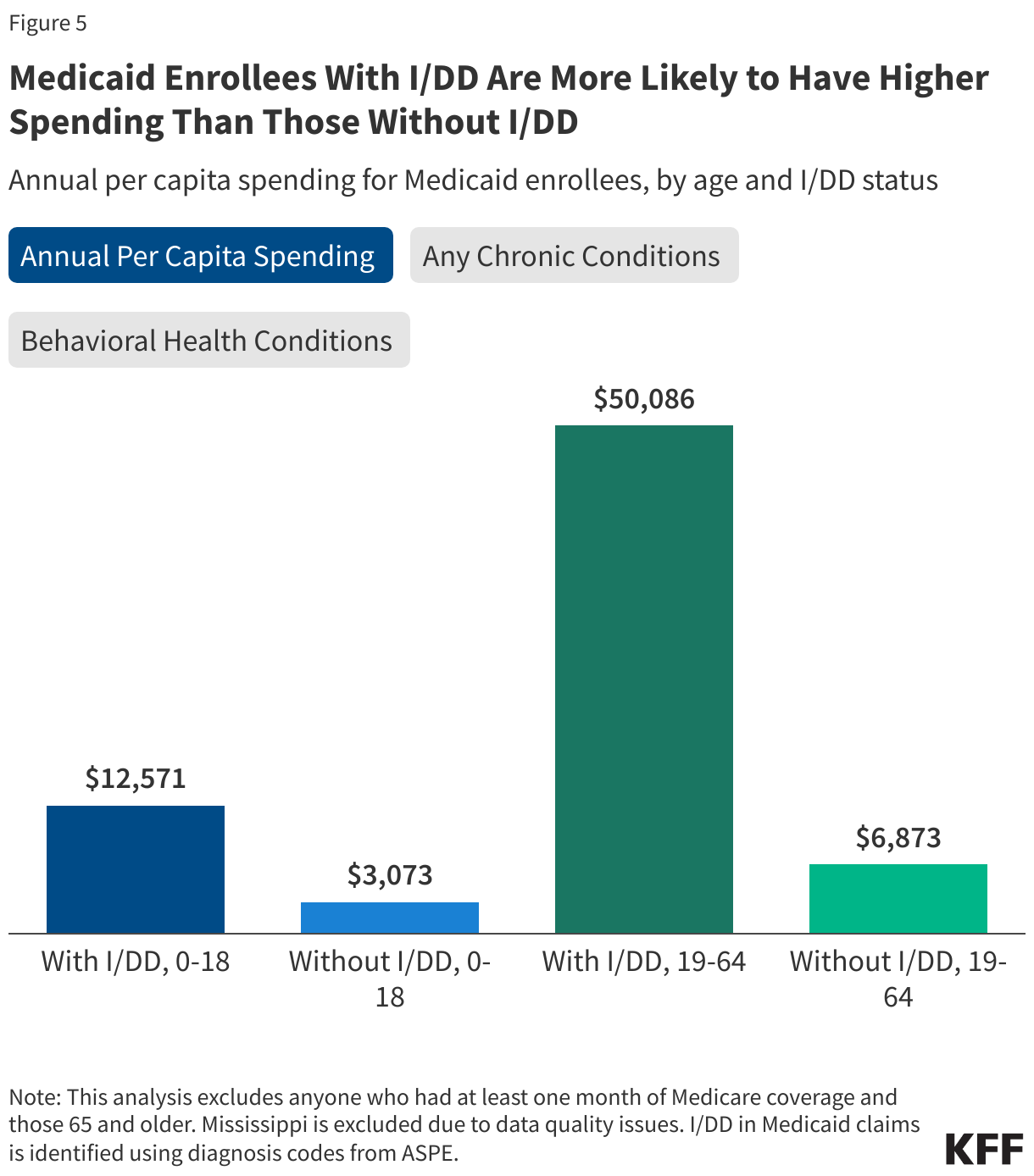

5. Medicaid enrollees with I/DD incur higher Medicaid costs and have higher rates of chronic conditions than those without I/DD.

Medicaid spending for people with I/DD is disproportionately high. Among Medicaid enrollees under 19, Medicaid spends, on average, about four times more annually on those with I/DD when compared to those without I/DD ($12,571 vs $3,073). Similarly, among Medicaid enrollees 19-64 years old, those with I/DD have spending seven times higher than those without I/DD ($50,086 vs. $6,873). With an unprecedented reduction in federal Medicaid spending, states will face pressure to reduce Medicaid costs and may look at approaches to reduce spending among high-cost populations, such as those with I/DD. States may also face pressure to restrict eligibility criteria for optional eligibility groups or reduce coverage of optional benefits such as home care, both of which could disproportionately affect people with I/DD.

The higher spending among those with I/DD reflects both greater use of long-term care and overall, more health care use on account of other chronic conditions. Medicaid enrollees under 12 with I/DD are nearly twice as likely to have another chronic condition as those without I/DD (19% vs. 11%) (Figure 5). Similarly, those ages 12-18 with I/DD are also more likely to have chronic conditions than those without I/DD (51% vs. 29%). This group is also over twice as likely to be diagnosed with a behavioral health condition, such as those related to mental health and substance use disorders (37% vs 17%).Enrollees ages 19-64 with I/DD are also more likely to have a chronic condition as those without I/DD (67% vs. 42%); twice as likely to be diagnosed with a behavioral health condition (46% vs. 23%); and twelve times as likely to be diagnosed with a physical health condition (24% vs 2%) (data not shown).

Methods

Data Sources: This analysis uses two different data sources:

- Figure 1-3, 5: These figures use 2021 T-MSIS Research Identifiable Files including the inpatient (IP), long-term care (LT), and other services (OT) claims files merged with the demographic-eligibility (DE) files from the Chronic Condition Warehouse (CCW).

- Figure 4: This figure uses data from KFF’s 2024 HCBS Survey. See KFF’s brief on waiting lists for more information on these data.

Identifying I/DD in Medicaid Claims Data: I/DD diagnoses were identified using a list of ICD-9 and ICD-10 diagnosis codes provided by the Assistant Secretary for Planning and Evaluation (ASPE). This list of codes categorizes I/DD conditions under six groups: intellectual disabilities, developmental delays/disabilities, learning disabilities, autism spectrum disorders, cerebral palsy, and spina bifida. A complete list of diagnosis codes and categorizations that were used for this analysis are available upon request. For more information on the ASPE methods, please reference their report.

Enrollee Inclusion Criteria in Medicaid Claims Data: All T-MSIS figures exclude enrollees 65 and older and those who had at least one month of Medicare coverage. These enrollees were excluded from these calculations since they may not have had sufficient claims in T-MSIS to accurately identify chronic conditions such as I/DD.

Identifying Medicaid Long-Term Care Use (Figure 3): KFF categorized claims using the type-of-service code from the first line claim, which was applied to the header claim in a merged dataset. KFF included all people with at least one month of Medicaid enrollment who were using the following types of long-term care: institutional care (care provided in a nursing facility or intermediate care facility) and home care (home health, personal care, 1915(c) waiver, 1115 waiver, and “other” home care).The small number of people using both types of long-term care were included in “institutional care”. For more information, see KFF’s brief on the number of people using Medicaid long-term care.

Defining Chronic Conditions in Medicaid Claims Data (Figure 5): This analysis used the CCW algorithm for identifying chronic conditions (updated in 2020), excluding its definition for mental illness, which was pulled from a different source. This analysis also included in its definition of chronic conditions substance use disorder, mental illness, obesity, HIV, and hepatitis C. For enrollees ages 0-11, behavioral health conditions (specifically, substance use disorder and mental illness) are not included as these codes have not been validated for children by the algorithm used to create the diagnosis flags.