KFF designs, conducts and analyzes original public opinion and survey research on Americans’ attitudes, knowledge, and experiences with the health care system to help amplify the public’s voice in major national debates.

This updated analysis estimates that nationally at least 234,000 deaths from COVID-19 between June 2021 and March 2022 could have been prevented with a primary series of vaccinations. These vaccine-preventable deaths represent 60% of all adult COVID-19 deaths since June 2021, when vaccines first became widely available to adults across the country, and a quarter (24%) of the nearly 1 million COVID-19 deaths since the pandemic began.

While it is clear that vaccine effectiveness increases with booster shots, the analysis does not estimate the potential effect of booster protection here on COVID-19 deaths. If it had, it likely would have found additional deaths among unvaccinated adults, as well as some deaths among vaccinated, could have been prevented.

The analysis can be found on the Peterson-KFF Health System Tracker, an information hub dedicated to monitoring and assessing the performance of the U.S. health system.

Medicare beneficiaries with low incomes and modest assets can qualify for additional financial help with Medicare premiums and cost sharing through both the Medicare Savings Programs and Medicare’s Part D Low-Income Subsidy for prescription drug coverage.

A new analysis and collection of interactive profiles highlight variations across states in the number and characteristics of beneficiaries who receive this additional financial assistance, including race and ethnicity, gender, and age. These findings reflect differences between states such as varying poverty rates among Medicare beneficiaries and higher asset thresholds for the Medicare Savings Program in some states.

Each profile highlights state-level eligibility requirements for the Medicare Savings Programs, which are administered by state Medicaid programs that can choose to adopt more generous income and asset requirements. Eligibility for the Part D Low-Income Subsidy program does not vary by state because it is run by the federal Medicare program.

Key takeaways include:

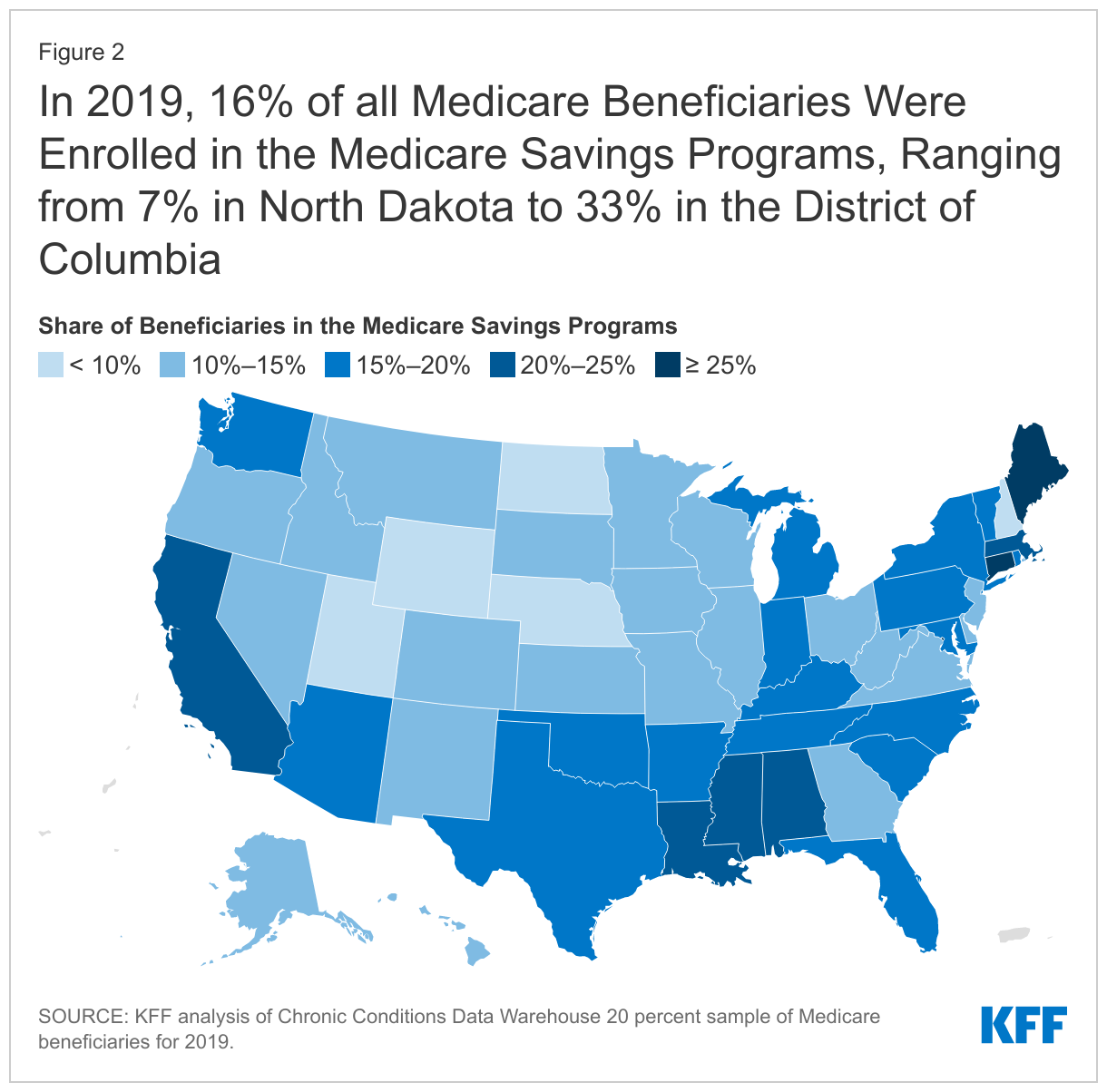

More than 10 million Medicare beneficiaries (16% of beneficiaries) were enrolled in the Medicare Savings Programs. The share of Medicare beneficiaries enrolled in the Medicare Savings Programs varies from a low of 7% in North Dakota to a high of 33% in the District of Columbia.

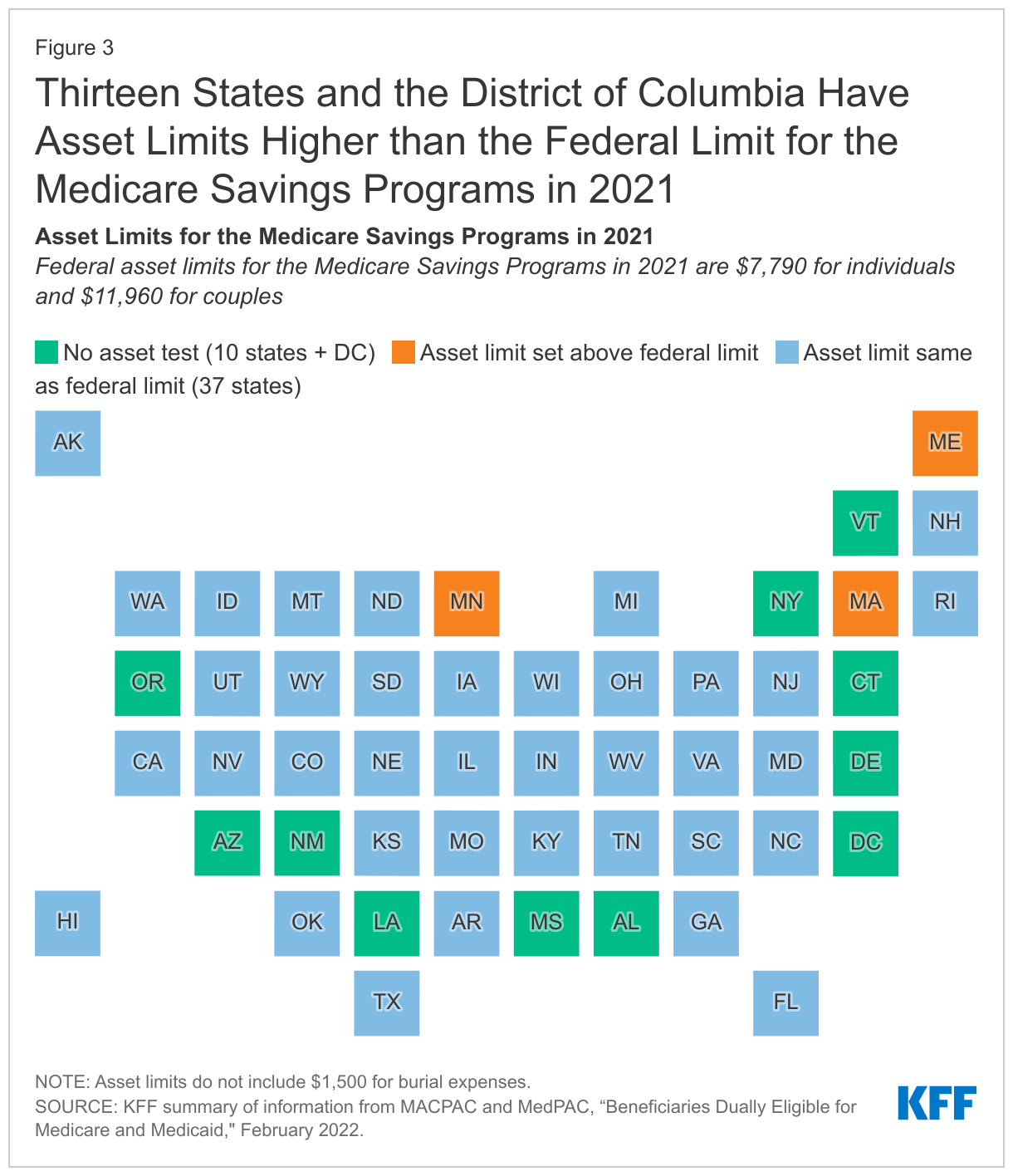

Among the nine states and the District of Columbia that have the highest share of Medicare beneficiaries enrolled in the Medicare Savings Programs, eight either do not have an asset test to qualify or have a higher asset limit than the federal guidelines.

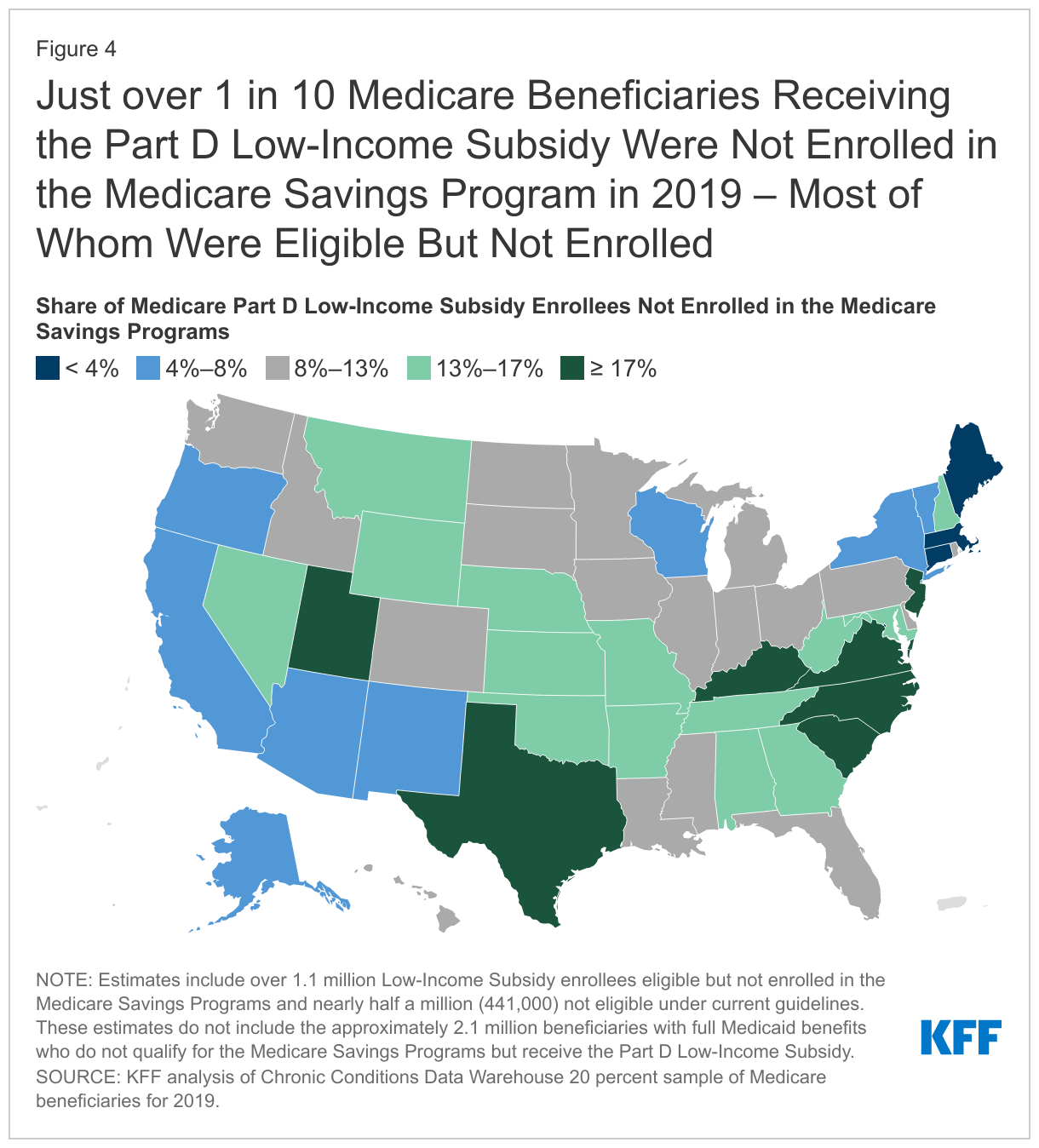

About 14.1 million Medicare beneficiaries were enrolled in the Part D Low-Income Subsidy in 2019, including 1.6 million who didn’t receive full Medicaid benefits and weren’t enrolled in the Medicare Savings Programs. About 1.1 million met the eligibility requirements for the Medicare Savings Programs, but were not enrolled, due in part to the administrative enrollment policies that vary from state to state.

Compared to Medicare beneficiaries overall, the Medicare Savings Programs and Part D Low-Income Subsidy disproportionately serve beneficiaries in communities of color, beneficiaries under 65 with disabilities, and women, who tend to have lower incomes and modest savings.

While Medicare provides health and financial protections to more than 64 million Americans ages 65 and older and younger adults with long-term disabilities, gaps in coverage and high cost-sharing requirements can make health care difficult to afford, particularly for people with modest incomes. Medicare beneficiaries are responsible for Medicare’s premiums, deductibles, and other cost-sharing requirements unless they have private supplemental coverage, a Medicare Advantage plan that covers some of the cost-sharing, or have incomes and assets low enough to qualify for the Medicare Savings Programs (which provide assistance with Medicare Part A and Part B premiums and/or cost sharing) and the Part D Low-Income Subsidy (LIS) (which helps with Medicare Part D drug plan premiums and cost sharing). The Biden Administration has promotedawareness of these programs for low-income beneficiaries in an effort to increase enrollment.

To provide greater insight into the number and characteristics of beneficiaries enrolled in these programs in the U.S. overall and in each state, KFF created profiles of each state showing enrollment of Medicare beneficiaries in the Medicare Savings Programs and the Part D Low-Income Subsidy, and their demographic characteristics including race/ethnicity, age, and gender. (The profiles are now updated with 2020 data.) This data note provides an overview of these programs and highlights findings from the state-level profiles.

Takeaways

In 2019, 10.3 million Medicare beneficiaries, or 16% of all beneficiaries, were enrolled in the Medicare Savings Programs. The share of state Medicare populations enrolled in the Medicare Savings Programs varies from 7% in North Dakota to 33% in the District of Columbia, due in part to differences across states in eligibility criteria for these programs and poverty rates among the Medicare population.

Among the nine states and the District of Columbia that have the highest share of Medicare beneficiaries enrolled in the Medicare Savings Programs, eight either have eliminated the asset test or have asset limits higher than the federal limit (District of Columbia, Connecticut, Maine, Louisiana, Mississippi, Alabama, Massachusetts, New York).

While Medicare beneficiaries enrolled in the Medicare Savings Programs automatically qualify to receive assistance through the Part D Low-Income Subsidy, the opposite is not true, in part because the income threshold to qualify for the Part D Low-Income Subsidy is higher. In 2019, nearly 1.6 million Medicare beneficiaries were enrolled in the Part D Low-Income Subsidy but not receiving premium or cost-sharing assistance through the Medicare Savings Programs, including just over 1.1 million beneficiaries who were eligible but not enrolled and nearly half a million (441,000) who did not meet eligibility criteria.

Compared to Medicare beneficiaries overall, the Medicare Savings Programs and Part D Low-Income Subsidy disproportionately serve beneficiaries in communities of color, beneficiaries under 65 with disabilities, and women, who tend to have lower incomes and modest savings.

Overview of the Medicare Savings Programs and the Part D Low-Income Subsidy

Medicare Savings Programs

Under the Medicare Savings Programs, state Medicaid programs help pay for premium and/or cost-sharing assistance for Medicare beneficiaries who have income and assets below specified levels, up to 135% FPL under federal guidelines ($18,347 for individuals and $24,719 for couples annually in 2022) and limited assets (below $8,400 for individuals and $12,600 for couples in 2022). Beneficiaries may receive help with Medicare’s premiums ($2,041 in 2022 for Part B), deductibles ($1,156 for Part A, $233 for Part B) and other cost-sharing requirements. Most low-income Medicare beneficiaries who qualify for Medicare premium and cost-sharing assistance also qualify for full Medicaid benefits, which can include long-term services and supports and other services such as dental and vision; these beneficiaries are referred to as full-benefit Medicare-Medicaid beneficiaries.

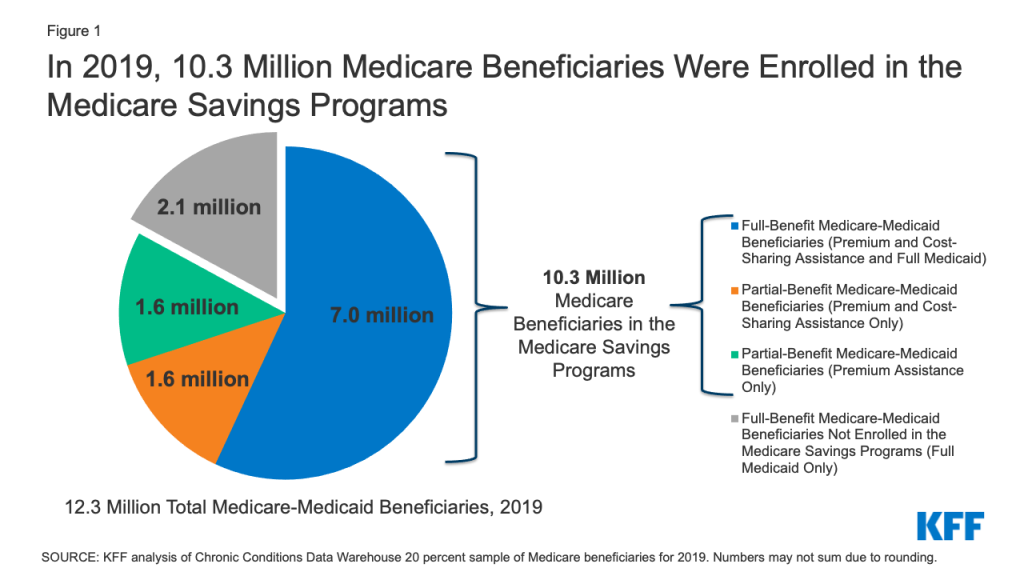

In 2019, 12.3 Medicare beneficiaries were enrolled in both Medicare and Medicaid. Of these beneficiaries, 9.1 million received full Medicaid benefits, including 7 million who also received financial assistance through the Medicare Savings Programs, and 2.1 million with full Medicaid benefits who do notqualify for the Medicare Savings Programs, though some states may choose to pay for Part B premiums for these beneficiaries.

In total, 10.3 million beneficiaries received financial assistance through the Medicare Savings Programs in 2019. This total includes the aforementioned 7 million beneficiaries who also receive full Medicaid benefits and 3.3 million beneficiaries who only receive premium and/or cost sharing assistance (Figure 1).

Figure 1: In 2019, 10.3 Million Medicare Beneficiaries Were Enrolled in the Medicare Savings Programs

Low-income beneficiaries who receive only financial assistance through the Medicare Savings Programs – meaning they qualify for payment of Medicare Part A and/or B premiums and, in some cases, Part A and Part B cost sharing but not full Medicaid benefits – are referred to as partial-benefit Medicare-Medicaid beneficiaries. (See MedPAC MACPAC Data Book: Beneficiaries Dually Eligible for Medicare and Medicaid — February 2022 for a full discussion of the different types of Medicare Savings Programs.)

Of the 3.3 million Medicare beneficiaries who received financial assistance through the Medicare Savings Programs, but not full Medicaid benefits, half (about 1.6 million) received assistance with Part B premium and cost-sharing assistance, while the other half received assistance with Part B premiums but did not qualify for help with Medicare Part A and B deductibles or cost-sharing requirements for covered services, despite having incomes below 135% of poverty.

Part D Low-Income Subsidy

Under the Medicare Part D Low-Income Subsidy (LIS), the federal government subsidizes premiums, deductibles, and cost sharing for the Part D prescription drug benefit, providing varying levels of assistance to beneficiaries at different income and asset levels up to 150% FPL ($20,385 for individuals and $27,465 for couples in 2022) and limited assets (below $14,010 for individuals and $27,950 for couples in 2022). The 150% FPL income threshold for LIS is higher than the 135% FPL threshold for the Medicare Savings Program. Unlike the Medicare Savings Programs, the Part D Low-Income Subsidy is a federal program and not part of the Medicaid program, nor is it administered by the states, so states do not have the option of setting higher income or asset thresholds for the Part D Low-Income Subsidy.

In 2019, 14.1 million (22% of all beneficiaries) were enrolled in the Part D Low-Income Subsidy. The vast majority (97%) of beneficiaries enrolled in the Part D Low-Income Subsidy receive full LIS benefits, while only 3% receive partial LIS benefits.

Both full-benefit and partial-benefit Medicare-Medicaid enrollees automatically receive full Medicare Part D LIS benefits, meaning they pay no Part D premium or deductible and only modest copayments for prescription drugs until they reach the catastrophic threshold, when they face no cost sharing. Beneficiaries who receive partial LIS benefits pay a reduced Part D premium and deductible and 15% coinsurance for drugs until they reach the catastrophic threshold, when they face modest copayments.

Individuals who do not automatically qualify for LIS because they are not enrolled in the Medicare Savings Programs can enroll if they meet income and asset requirements set by the federal government. Depending on their income and assets, they could receive full or partial LIS benefits. However, even if their income and assets meet Medicare Savings Program requirements, individuals who qualify for Part D LIS are not automatically enrolled in Medicare Savings Programs. While states are statutorily required to initiate Medicare Savings Programs applications for beneficiaries who apply for Part D LIS to help facilitate enrollment, CMS has noted that not all states are meeting these standards.

Box 1: Medicare Savings Programs and Part D Low-Income Subsidy Benefit Groups

Full-Benefit Medicare-Medicaid: Full Medicaid benefits; Premium and cost-sharing assistance through the Medicare Savings Programs; Full Low-Income Subsidy

Full-Benefit Medicare-Medicaid Beneficiaries Not Enrolled in the Medicare Savings Programs: Full Medicaid benefits only; Full Low-Income Subsidy

Partial-Benefit Medicare-Medicaid: Premium and cost-sharing assistance through the Medicare Savings Programs; Full Low-Income Subsidy

Partial-Benefit Medicare-Medicaid: Premium Assistance only through the Medicare Savings Programs; Full Low-Income Subsidy

Full Low-Income Subsidy: Part D premium and cost-sharing assistance; May be enrolled in the Medicare Savings Programs depending on income and assets

Partial Low-Income Subsidy: Part D premium and cost-sharing assistance

Findings

In 2019, 10.3 million Medicare beneficiaries, or 16% of all beneficiaries, were enrolled in the Medicare Savings Programs, but the share of state Medicare populations enrolled in the Medicare Savings Programs varies by state, from 7% in North Dakota to 33% in the District of Columbia (Figure 2).

States that have adopted more generous income and asset thresholds – as well as states with higher poverty rates among older adults – tend to have larger shares of beneficiaries enrolled in the Medicare Savings Programs.

The federal government sets minimum income and asset eligibility requirements for the Medicare Savings Programs, but states can expand eligibility to beneficiaries with higher incomes and/or assets. As of 2021:

Four states and the District of Columbia have raised the qualifying federal poverty limits (Connecticut, Indiana, Maine, and Massachusetts) above the federally defined minimum level. For example, for the Qualified Medicare Beneficiary program where the income limit is typically 100% of the federal poverty level ($12,880 for individuals and $17,420 for couples in 2021), Indiana’s income limit is 150% ($19,320 for individuals and $26,130 for couples), while Connecticut’s is 211% ($25,760 for individuals and $34,840 for couples).

These expanded income and asset limits only apply to Medicare premium and cost-sharing assistance through the Medicare Savings Programs. Beneficiaries still are required to meet state-defined eligibility criteria to receive full Medicaid benefits, including nursing home coverage and other long-term services and supports, in their state.

The variation across states in the share of Medicare beneficiaries receiving premium and cost-sharing assistance through the Medicare Savings Programs could be due to a number of reasons. One reason might be the higher asset limits in some states: eight of the nine states and the District of Columbia with the highest share of Medicare beneficiaries enrolled in the Medicare Savings Programs either have eliminated the asset test or have asset limits higher than the federal limit (District of Columbia, Connecticut, Maine, Louisiana, Mississippi, Alabama, Massachusetts, New York). This is not universally true, however; there are a few states with no asset limit or higher asset limits, which have relatively lower shares of enrollment, including Delaware, New Mexico, Oregon, and Minnesota.

Poverty rates among Medicare beneficiaries also vary across states, although the relationship between poverty and Medicare Savings Program enrollment rates is less clear. While some states with high poverty rates (e.g., more than 25% of beneficiaries below 150% of poverty) among the Medicare population have a relatively high share of beneficiaries enrolled in the Medicare Savings Programs, (e.g., more than 20% enrolled: District of Columbia, Louisiana, Mississippi, and Alabama), a handful of states with high poverty rates have a relatively low share of beneficiaries enrolled in the Medicare Savings Programs (e.g., West Virginia: 11%, New Mexico: 14%, Georgia: 14%).

In addition to these factors, variations across states in Medicare Savings Program enrollment may be related to differences in the application process via state Medicaid agencies, which could make it more difficult for beneficiaries in some states to apply, or beneficiaries’ lack of awareness of the Medicare Savings Programs.

In 2019, nearly 1.6 million Medicare beneficiaries (or 11%) received some help through the Part D Low-Income Subsidy, but no premium and/or cost-sharing assistance from the Medicare Savings Programs (Figure 4).

This includes more than 1.1 million people who were not enrolled in the Medicare Savings Programs, even though they were eligible, and another half a million beneficiaries (441,000) who did not qualify for the Medicare Savings Programs because either their incomes and/or assets were too high. These estimates do not include the approximately 2.1 million beneficiaries with full Medicaid benefits who do notqualify for the Medicare Savings Programs but receive the Part D Low-Income Subsidy.

The share of beneficiaries who received assistance through the Part D Low-Income Subsidy Program, but were not enrolled in the Medicare Savings Programs, ranged from 1% in Connecticut to 21% in South Carolina. Variations across states may be due to differences in the administrative complexity of enrolling in the Medicare Savings Programs across states (in contrast to the Low-Income Subsidy where beneficiaries apply through the Social Security Administration), differences in methodologies in how eligibility is determined for the Low-Income Subsidy versus the Medicare Savings Programs in many states, and lack of awareness of the Medicare Savings Programs, which may result in some beneficiaries applying for the Part D Low-Income Subsidy but not the Medicare Savings Programs.

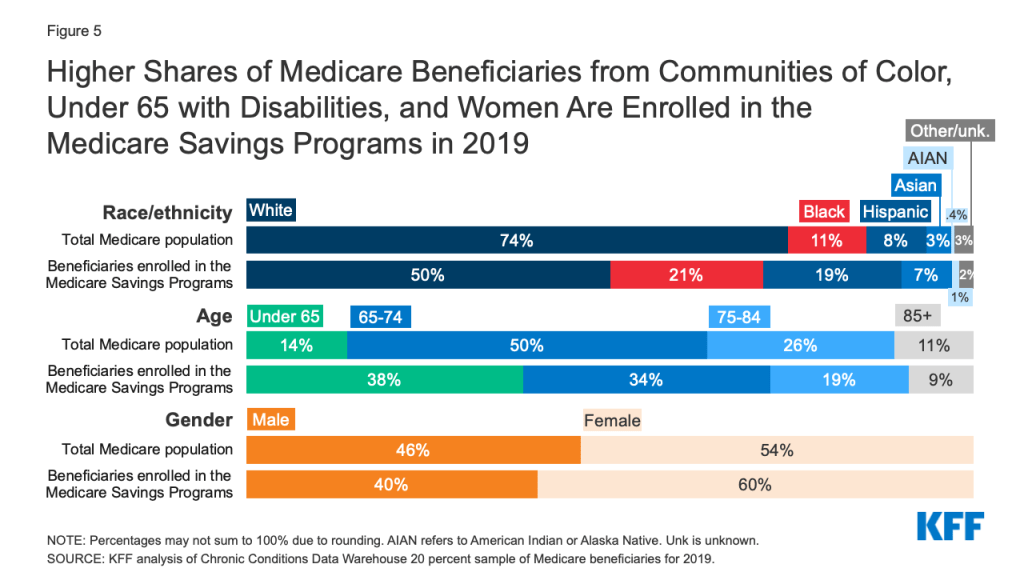

The Medicare Savings Programs and Part D Low-Income Subsidy disproportionately serve beneficiaries in communities of color, beneficiaries under 65 with disabilities, and women, who tend to have lower incomes and modest savings than beneficiaries who are White, 65 or older, or men (Figure 5).

Figure 5: Higher Shares of Medicare Beneficiaries from Communities of Color, Under 65 with Disabilities, and Women Are Enrolled in the Medicare Savings Programs in 2019

Race/ethnicity. One in five (21%) of beneficiaries enrolled in the Medicare Savings Programs are Black, nearly double the share of Black beneficiaries (11%) in the total Medicare population. Similarly, 19% of beneficiaries enrolled in the Medicare Savings Programs are Hispanic, more than double the share of Hispanic beneficiaries (8%) in the total Medicare population.

There are differences in the characteristics of beneficiaries who are enrolled in these programs across states, which may be due to state-level variation in the composition of the Medicare population, as well as variation in the factors mentioned above, such as eligibility thresholds and methods of determining eligibility, poverty rates, and the characteristics of enrollees who have lower incomes. For example, in Alabama, South Carolina, Maryland, and Georgia, Black beneficiaries comprise about a quarter of each state’s Medicare population, but about half of Medicare Savings Program enrollees in the state, ranging from 44% to 50%.

The share of Hispanic beneficiaries enrolled in the Medicare Savings Programs also varies by state. In New Jersey, Colorado, New York, and Nevada, Hispanic beneficiaries comprise one in ten of all Medicare beneficiaries, but about a quarter of Medicare Savings Programs enrollees in the state, ranging from 24% to 27%.

Age. The Medicare Savings Programs also reach a disproportionate share of beneficiaries under age 65 who qualify for Medicare due to long-term disabilities. For example, 38% of Medicare beneficiaries who are under age 65 due to disability are enrolled in the Medicare Savings Programs, nearly three times the share of under age-65 beneficiaries as their share of the total Medicare population (14%).

The share of Medicare beneficiaries who are under age 65 with long-term disabilities enrolled in the Medicare Savings Programs also varies by state, ranging from 23% in California to 59% in New Hampshire.

Gender. Women represent 60% of those beneficiaries enrolled in the Medicare Savings Programs but 54% of the Medicare population overall. There is somewhat less variation across states in enrollment by gender, with the share of women enrolled in these programs varying from 52% in Alaska to 63% in Alabama, Georgia, and Wyoming.

Overall enrollment patterns in the Part D-Low Income Subsidy by race/ethnicity, age, and gender are similar to the Medicare Savings Programs in large part due to the overlap of enrollment in these programs.

Despite the important financial protections the Medicare Savings Programs and Part D Low-Income Subsidy provide to low-income people on Medicare, many low-income beneficiaries are not receiving these benefits. Historically these programs have had lowparticipation, despite some state and federal efforts to increase enrollment. Based on prior KFF work, the share of Medicare beneficiaries with incomes below 150% FPL who are enrolled in the Part D Low-Income Subsidy is estimated to be between 55% and 70%, while 50% to 65% are estimated to be enrolled in the Medicare Savings Programs (lower because beneficiaries with incomes between 135%-150% FPL are not eligible for these programs under federal guidelines) – though not everyone with incomes at or below this level are eligible for either of these programs due to the asset tests.

Additionally, certain groups of low-income beneficiaries are less likely than others to be receiving assistance from the Medicare Savings Programs, which could expose them to higher health care costs. For example, based on our analysis of data from the Medicare Current Beneficiary Survey, in 2019, nearly one in five Black and Hispanic Medicare beneficiaries (19% and 17%, respectively) had incomes below 150% of poverty but were not enrolled in the Medicare Savings Programs, compared to 11% of White beneficiaries.

One reason for relatively low participation rates overall in these programs could be the asset test used to determine eligibility for both the Medicare Savings Programs and the Part D Low-Income Subsidy, requiring beneficiaries to have countable resources, such as money in savings and checking accounts, stocks, and bonds, below a certain limit. This contrasts with eligibility requirements established under the Affordable Care Act that use income, but not assets, to determine eligibility for Medicaid expansion or Marketplace coverage. This means individuals living in states that expanded Medicaid up to 138% FPL would be subject to an asset test when they turn 65 or qualify for Medicare based on having a long-term disability in order to get help from the Medicare Savings Programs with Medicare premiums and cost sharing (unless they live in a state that has eliminated the asset test). This “Medicare cliff” can result in low-income people losing access to valuable financial protections that they qualified for prior to becoming eligible for Medicare.

Discussion

In 2019, 10.3 million Medicare beneficiaries received help through the Medicare Savings Programs. Enrollment in these programs varies by state, due to differences in income and asset eligibility criteria and administrative requirements across states. While 14.1 million beneficiaries received help through the Part D Low-Income Subsidy, nearly 1.6 million of these beneficiaries did not receive premium or cost-sharing help through the Medicare Savings Programs, because either they were ineligible or did not enroll. Both programs disproportionately serve communities of color, adults under 65 with disabilities, and women on Medicare, who tend to have relatively low incomes and modest savings.

There has been some discussion among policymakers of improving financial protections for low-income Medicare beneficiaries, for example, by expanding income eligibility thresholds for both the Medicare Savings Programs and Part D Low-Income Subsidy, aligning eligibility criteria between these two programs, and by raising or eliminating the federal asset test for the Medicare Savings Programs, as some states have done. Such changes could provide stronger financial protections to low-income beneficiaries living just above current eligibility income and asset levels who are now responsible for payment of full Medicare premiums, deductibles, and cost sharing. They would also increase government spending, and do not appear to have strong prospects for passage in the current political environment.

Methods

This analysis uses data from the Chronic Conditions Data Warehouse 20 percent sample of Medicare beneficiaries for 2019. For this analysis, we use an ever-enrolled approach for counting beneficiaries enrolled in the Medicare Savings Program beneficiaries and the Part D Low-Income Subsidy, rather than an average monthly measure, which may explain differences in our estimates compared to other published estimates. This analysis excludes beneficiaries living in Puerto Rico and the territories.

This work was supported in part by AARP Public Policy Institute (PPI). We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Meredith Freed, Juliette Cubanski, and Tricia Neuman are with KFF.Anthony Damico is an independent consultant.

This week marks the fifth annual Black Maternal Health Week, a campaign started by the Black Mamas Matter Alliance that was formally recognized by the Biden administration last year. This week is dedicated to celebrating Black motherhood and raising awareness about the state of Black maternal health in the United States.

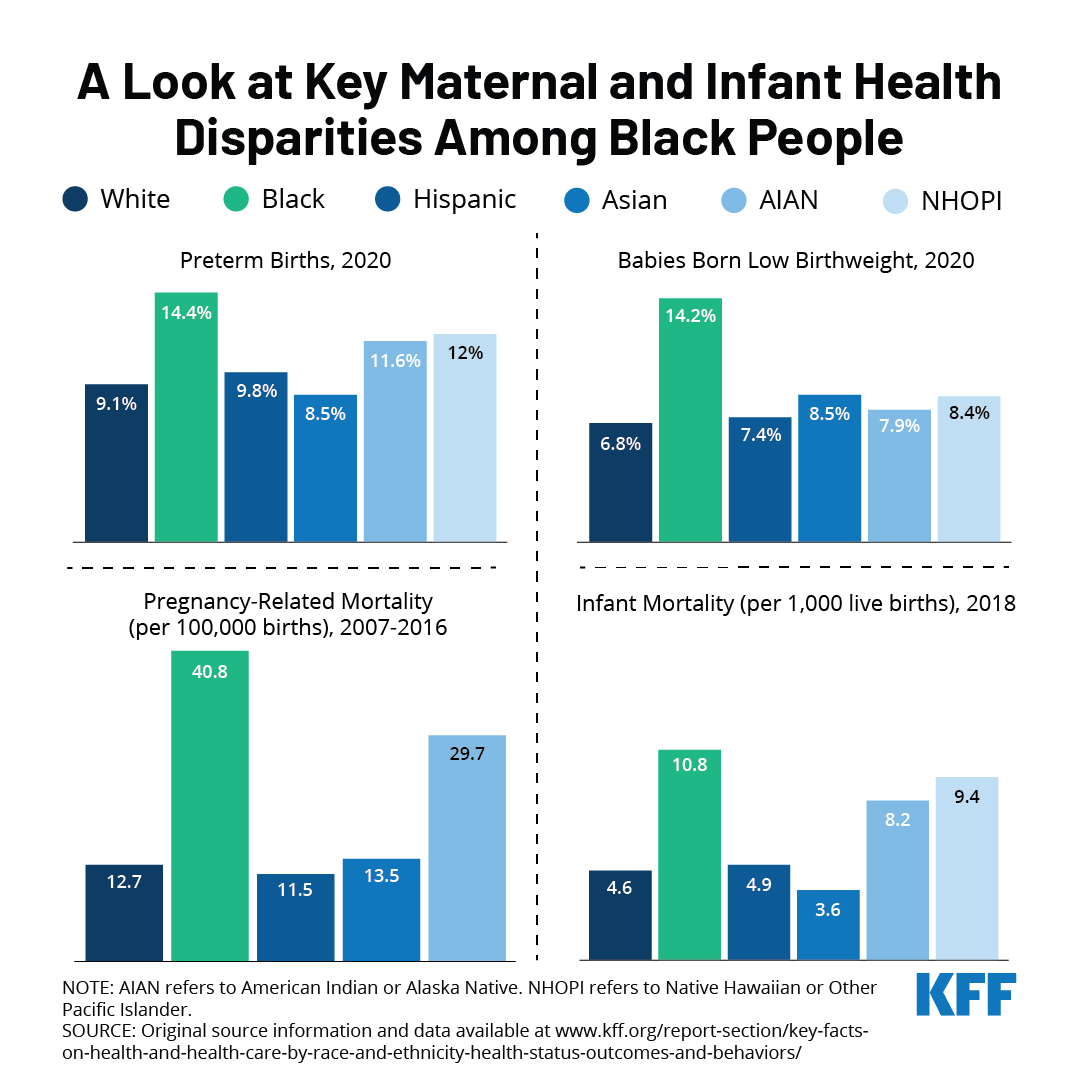

Due to systemic and overt discrimination, Black people are disproportionately affected by high maternal and infant morbidities and mortality. A recent KFF analysis found that Black people fared worse than other racial and ethnic groups in all maternal health indicators measured. They were more likely to have preterm births and have low birthweight babies compared to other racial/ethnic groups. Black infants were twice as likely to die as White infants, and Black people were more likely to die while pregnant or within a year of giving birth compared to all other groups.

These disparities were exacerbated during the pandemic, with Black people experiencing maternal death rates at more than twice the national average, a significant increase from pre-pandemic rates, according to a recent CDC report. The Build Back Better Act (BBBA) includes several provisions to address the social determinants of maternal health, increase funding for the perinatal workforce, improve access to quality maternity care, improve data collection, and mitigate the impacts of the pandemic and climate change on maternal outcomes. The BBBA expands the American Rescue Plan Act’s voluntary postpartum coverage provision by requiring states to expand their Medicaid postpartum coverage from 60 days to 12 months. It also seeks to close the coverage gap by making low-income people in states that have not expanded Medicaid eligible for subsidized coverage in the ACA marketplace. Both provisions facilitate continuity of coverage and care for people at all life stages, including pregnancy and parenthood. However, the fate of the BBBA and its health provisions remains uncertain while the legislation remains stalled.

In addition to legislation, addressing systemic discrimination, implicit bias and racism will be integral to achieving equity in maternal health outcomes.

The Biden Administration recently issued a proposed rule to make it easier for family members of workers offered health insurance at their jobs to qualify for premium tax credits for Marketplace coverage. The proposal aims to address what has been called the “family glitch”. Under the ACA, an individual enrolling in a Marketplace plan is not eligible for a premium tax credit if they are eligible for job-based coverage that is considered affordable and provides minimum value (i.e., covers at least 60% of health expenses on average). Current regulations provide that job-based coverage is considered affordable to a worker and their dependents if the cost of self-only coverage for the worker is less than 9.6 percent of family income, without regard to the cost of adding family members. The proposal would revise that interpretation by assessing the affordability of job-based coverage available for the family members of a worker by comparing the total cost for the whole family (including the worker) to the 9.6 percent threshold. This assessment would measure affordability for members of the family other than the worker. Affordability for the worker himself or herself would continue to be based on the cost of self-only coverage.

The proposed rule explains that the current interpretation leads to cases where family members are considered to have an affordable offer even when they face very high contribution amounts if they want to enroll in that coverage, which the agencies assert is not consistent with the ACA’s purpose of providing access to affordable coverage for everyone. We previously estimated that 5.1 million people are currently caught in this ‘family glitch’.

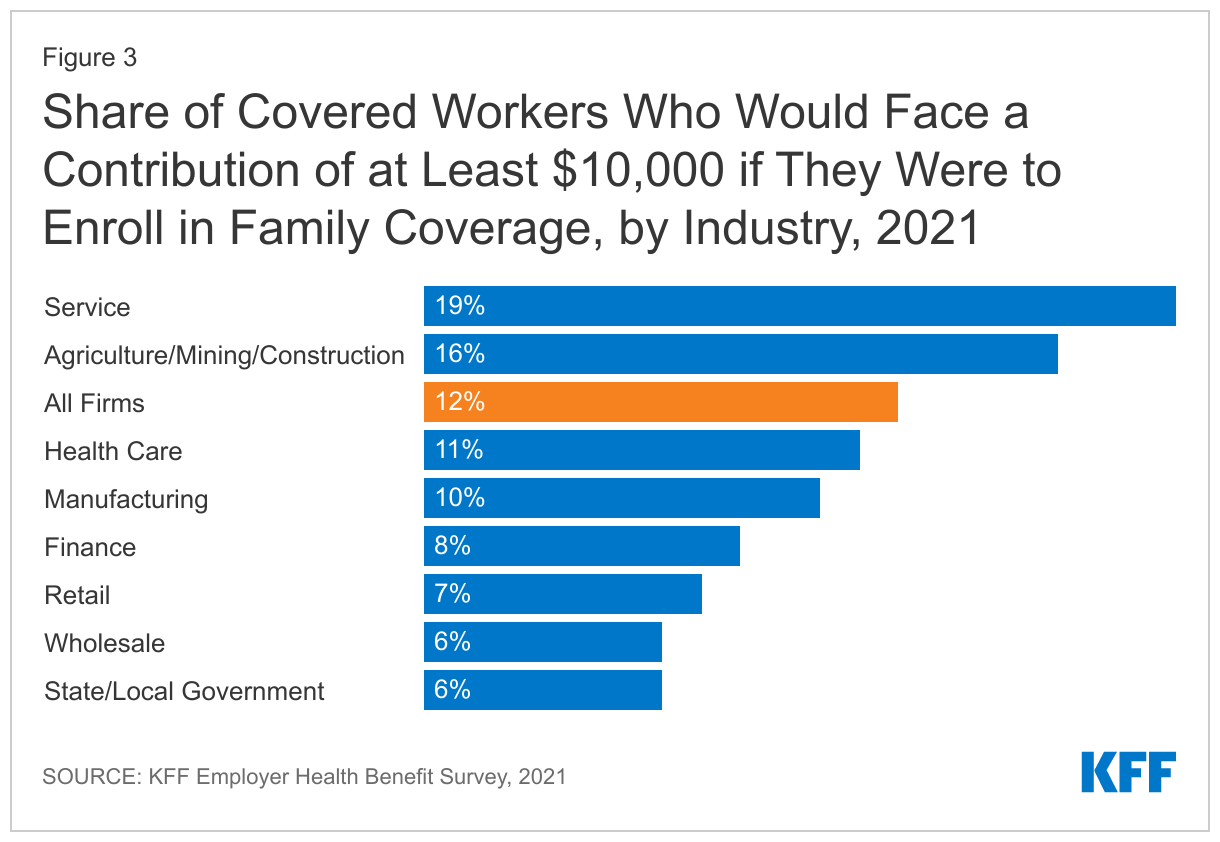

In this analysis, we use the KFF Employer Health Benefits Survey (EHBS) to look at the shares of workers that might pay significant amounts to enroll families and how these shares vary across firms. These are the workers most likely to benefit from a fix to the family glitch.

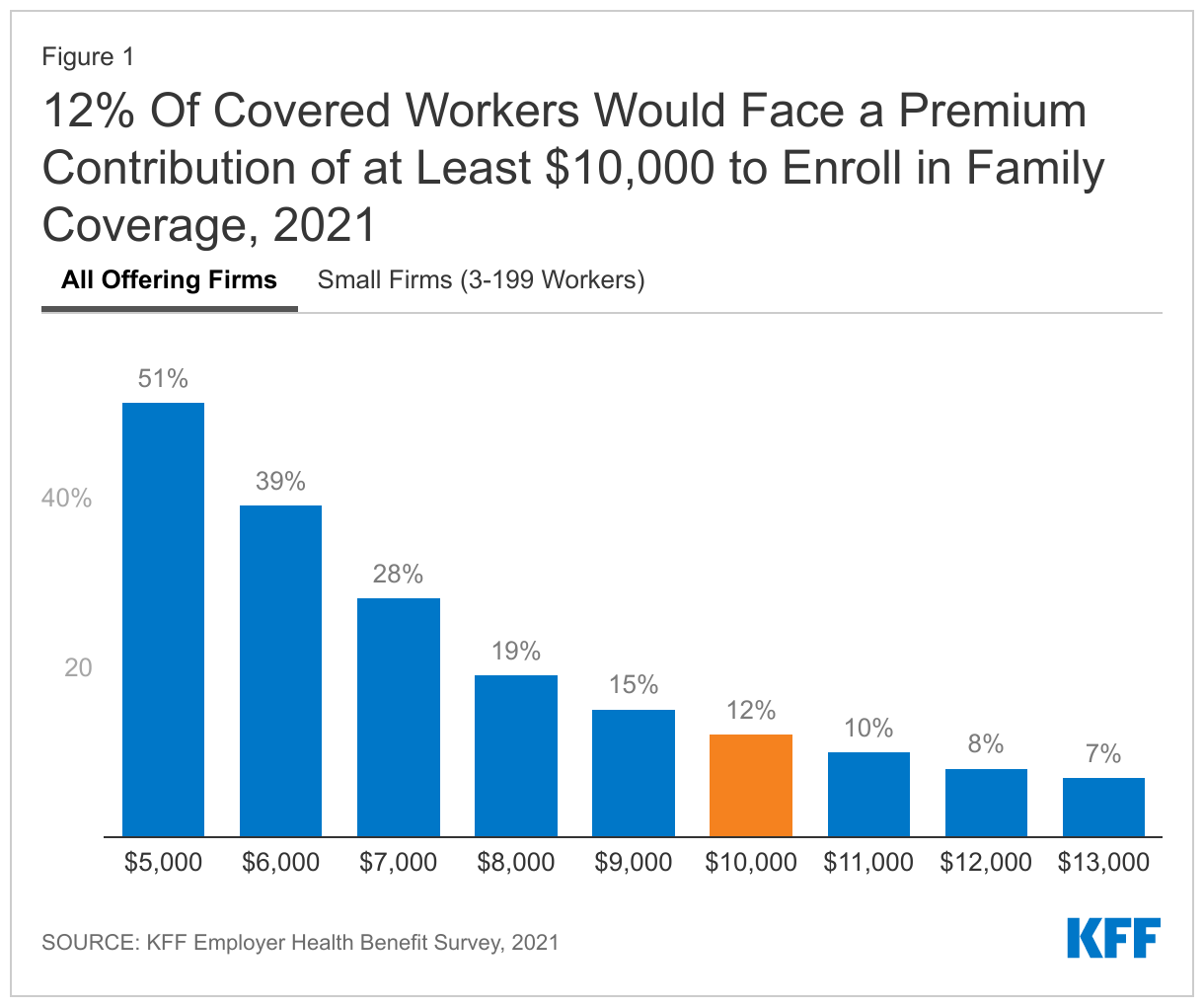

Health insurance is expensive. The average premiums in 2021 were $7,739 for single coverage and $22,221 for a family of four. The average contribution amounts for covered workers were $1,299 for single coverage and $5,969 for a family of four. Importantly, there was considerable variation around these averages: for example, ten percent of covered workers were enrolled in a plan with a premium of more than $29,000 for family coverage; and 12% of covered workers were enrolled in a plan with a contribution of at least $10,000 for family coverage. It is the family members of workers in firms with high contributions that are most likely to benefit from the proposed rule change.

Before looking at some of the characteristics of these firms and workers, we should be clear about what these percentages mean. When we say that 12% of covered workers are in a plan that has a worker contribution of at least $10,000, we are not saying that 12% of covered workers actually enroll in family coverage and pay those amounts. Instead, we are saying that 12% of covered workers work at firms where the contribution for a family of four for their largest health plan (or sometimes an average of several plans) is at least $10,000. Surveys do not collect information about all of the health plans each employer may offer, nor are they able to account for potential adjustments that might affect individual workers or families (smoking surcharges, discounts for filling out a health risk assessment, surcharge if spouse is offered coverage at another job). So, while these surveys cannot give precise results on actual costs, they give a pretty good picture of the magnitude of the costs workers face to enroll in the plans that most workers choose.

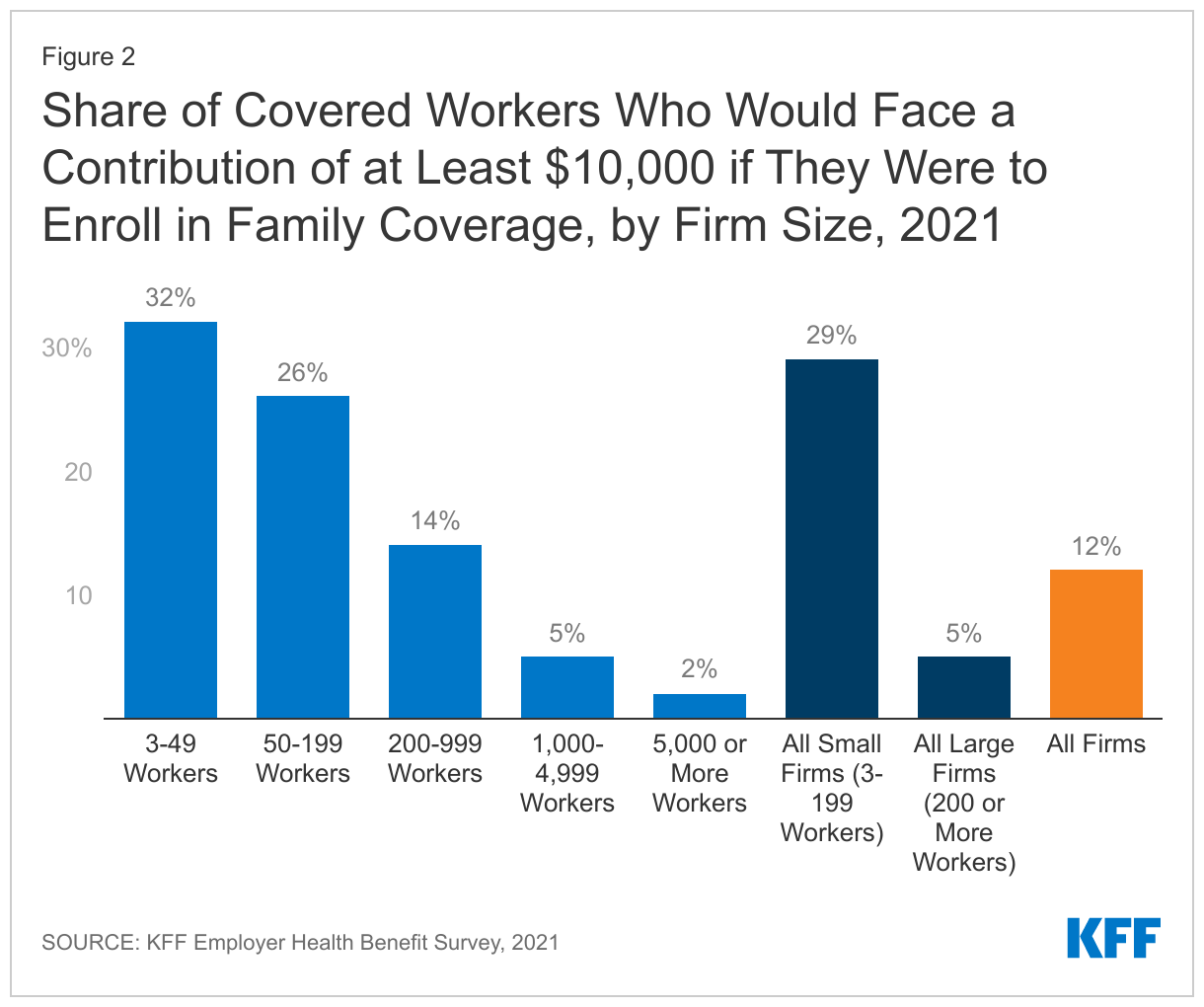

Workers in small firms face higher contributions for family coverage. Workers in small firms (3-199 workers) on average face higher contributions to enroll in family coverage and are more likely to face very high contribution amounts. The average contribution for a family of four in 2021 was $7,710 for workers in small firms, compared to $5,269 for workers in larger firms. Twenty-nine percent of covered workers in small firms faced a contribution of at least $10,000 for family coverage, compared to only 5% of covered workers in larger firms.

One reason family contributions may be higher in smaller firms is that some small employers only make a contribution toward the cost of self-only coverage, leaving the worker to pay the entire difference between the premium for self-only coverage and the premium for family coverage. Even in firms selecting less comprehensive coverage, this difference can be many thousands of dollars. We estimate that 19% of small firms offering health benefits make little or no additional contribution towards the cost of family coverage. These firms employ about 17% percent of the covered workers enrolled at small firms (3-199 workers).

Workers in the service industry are more likely to face high contributions for family coverage. Contributions for family coverage vary significantly by industry. Covered workers in certain industries are more likely to face high contributions for family coverage while covered workers in other industries (wholesale, transportation, communications, utilities, state and local government) are less likely.

The proposed rule addresses the eligibility for premium tax credits in situations where workers face unaffordable contribution amounts to enroll their family members in job-based coverage. Data from the KFF Employer Health Benefits Survey demonstrates that some workers face very high contribution amounts for family coverage, with 12% facing a contribution of at least $10,000 for a family of four. Workers with coverage through small firms are particularly at risk of high contributions for family coverage, and would therefore benefit from the family glitch fix.

Methods

The annual KFF Employer Health Benefits Survey (EHBS) for 2021 was conducted between January and July of 2021, and included almost 1,700 randomly selected, non-federal public and private firms with three or more employees. The full EHBS, including a detailed methodology section, is available at ehbs.kff.org. EHBS collects information from employers about how much employers and employees contribute in their largest health plans.

Ending COVID-19 Emergency Declarations Will Bring an End to Flexibilities that Aided Patients, Providers, Insurers, and Public Programs in Responding to the Pandemic

When the federal government ends COVID-19 emergency declarations that were declared in the early days of the pandemic, it will bring to a close several changes that were enacted temporarily to enable the U.S. health care system to better deal with the crisis.

A new KFF resource details a number of those flexibilities and lays out what it will mean for people, providers and federal health programs when they go away. One of the key declarations, the COVID-19 Public Health Emergency, is slated to expire on April 16, though it is expected to be renewed by the Biden administration. The end of the emergency declarations also will bring about a ramping down of heightened federal spending related to the pandemic, which was always intended to be temporary.

The changes will eliminate a pathway through Medicaid to free COVID-19 testing, treatment and vaccines for people without health insurance and could trigger higher out-of-pocket costs for tests for people with private insurance. Millions of people could lose Medicaid coverage when the continuous enrollment requirement ends and the federal government shuts off pandemic-related enhanced federal Medicaid funding.

Most Medicare beneficiaries would lose access to coverage of nearly all telehealth services within a few months, with some exceptions, and hospitals would no longer receive a special pandemic-related 20 percent increase in Medicare payments for treatment of patients diagnosed with COVID-19. In addition, any COVID tests, vaccines, or therapeutics that were granted emergency authorization for use but have not been approved by the FDA could no longer be used.The new KFF resource addresses flexibilities adopted during the COVID-19 pandemic and implications of their drawing to a close in the following areas:

Coverage, costs, and payment for COVID-19 testing, treatments, and vaccines

Medicaid coverage and federal match rates

Telehealth

Other Medicaid and CHIP flexibilities

Other Medicare payment and coverage flexibilities

Other private insurance coverage flexibilities

Access to medical countermeasures (vaccines, tests, and treatments) through FDA emergency use authorization (EUA)

Liability immunity to administer medical countermeasures

For more COVID-19-related analyses and data, visit kff.org.

Earlier this week, the Biden Administration announced the final Medicare Advantage rates for 2023, which are projected to result in an average increase in Medicare Advantage plan revenue of 8.5% compared to 2022 – the highest average expected increase in recent years.

Payments to Medicare Advantage plans as a share of total Medicare spending on Part A and Part B services have increased from 26% in 2010 to 45% in 2020, and are expected to rise to 54% in 2030, accounting for more than half of Medicare Part A and B spending by 2024.

The higher spending also contributes to Medicare’s solvency and affordability challenges, including the projected depletion of the Hospital Insurance Trust Fund in 2026, and rising Part B premiums for all Medicare beneficiaries, including those in traditional Medicare.

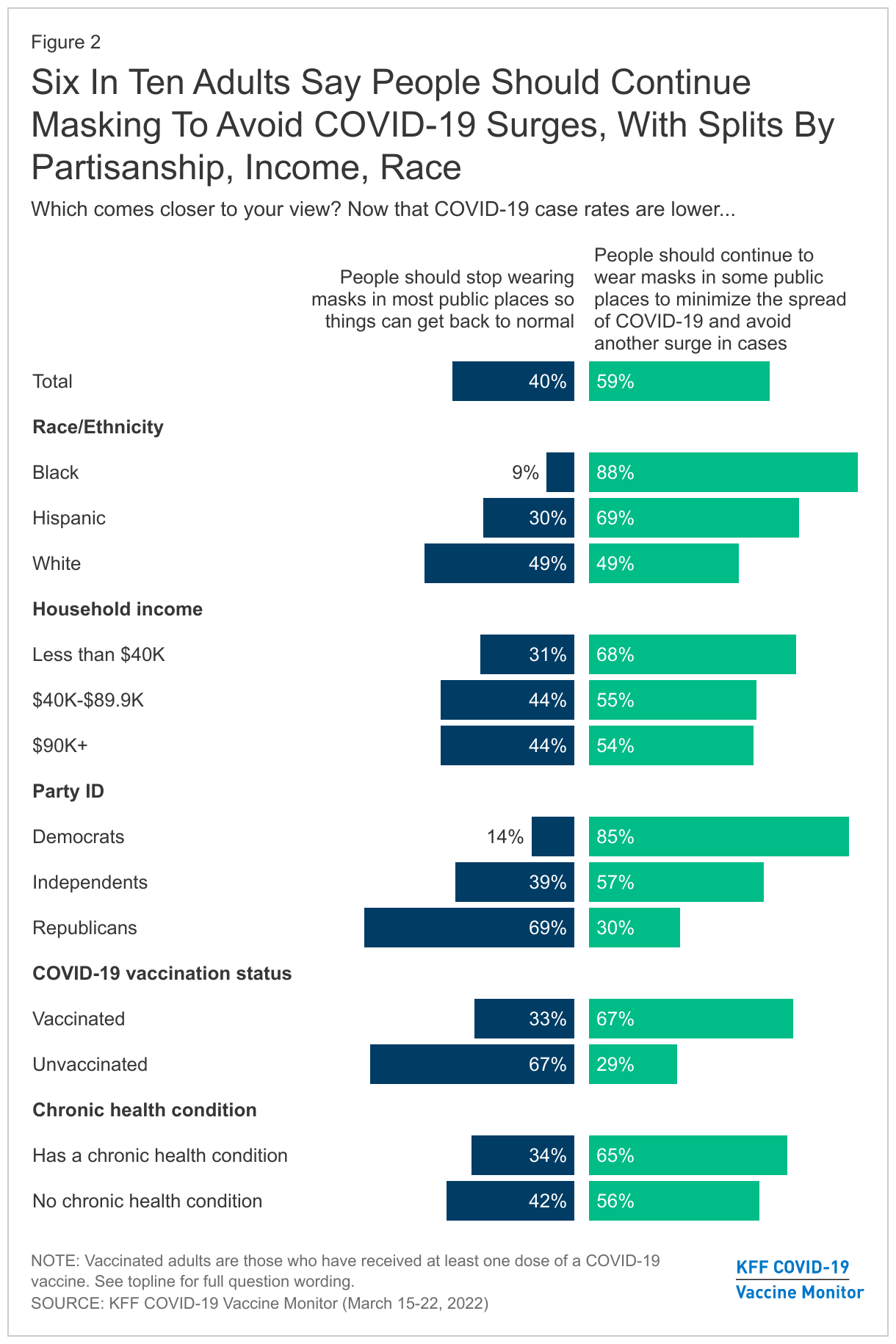

People of Color, Lower Income Adults, and Those With Chronic Conditions Are More Vigilant About COVID-19 Precautions Like Masking, and Want Others to Continue Them as Well

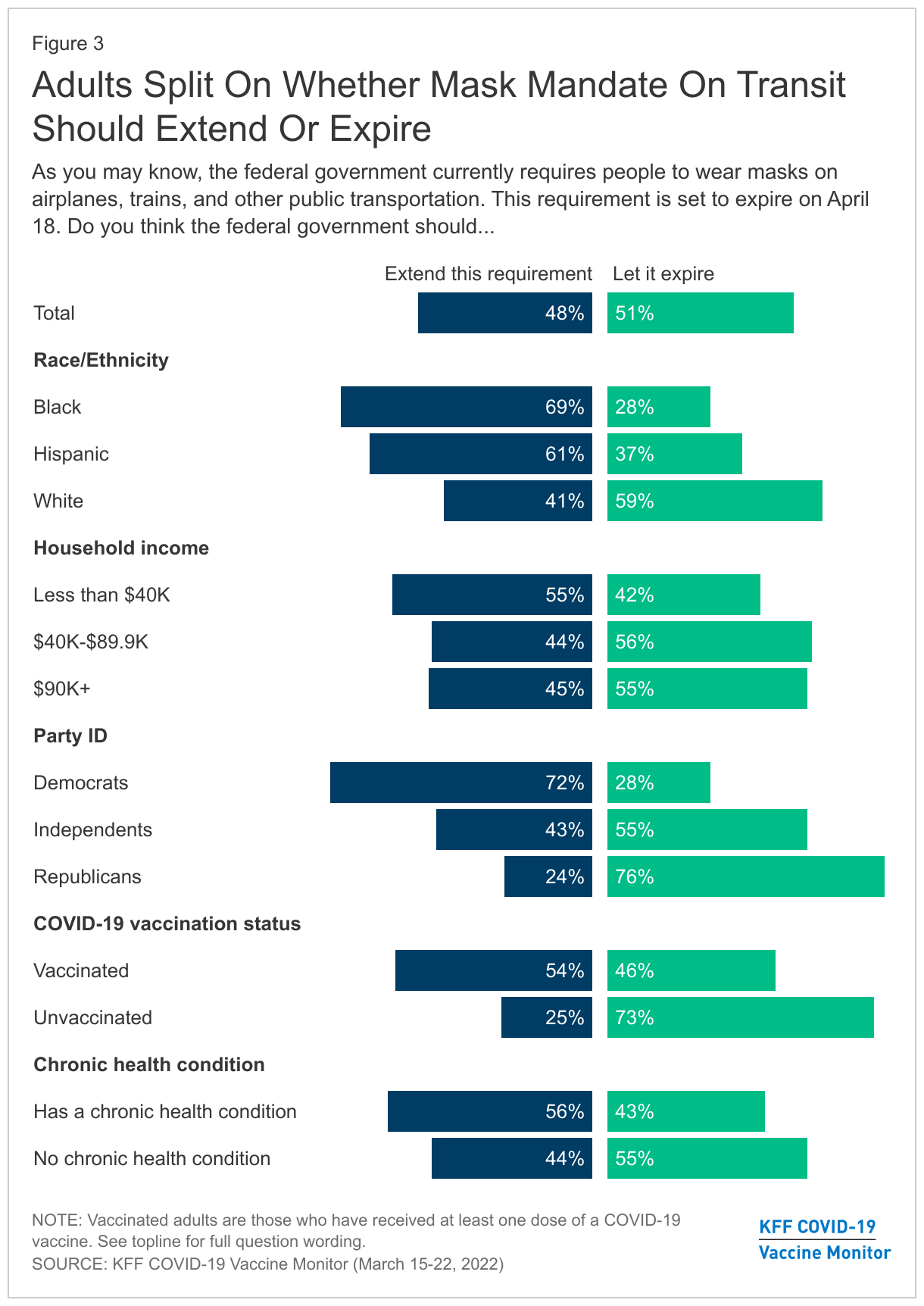

The Public Is Divided About Public Transportation Mask Requirement, With Half Wanting the Mandate Extended and the Other Half Wanting to Let it Expire

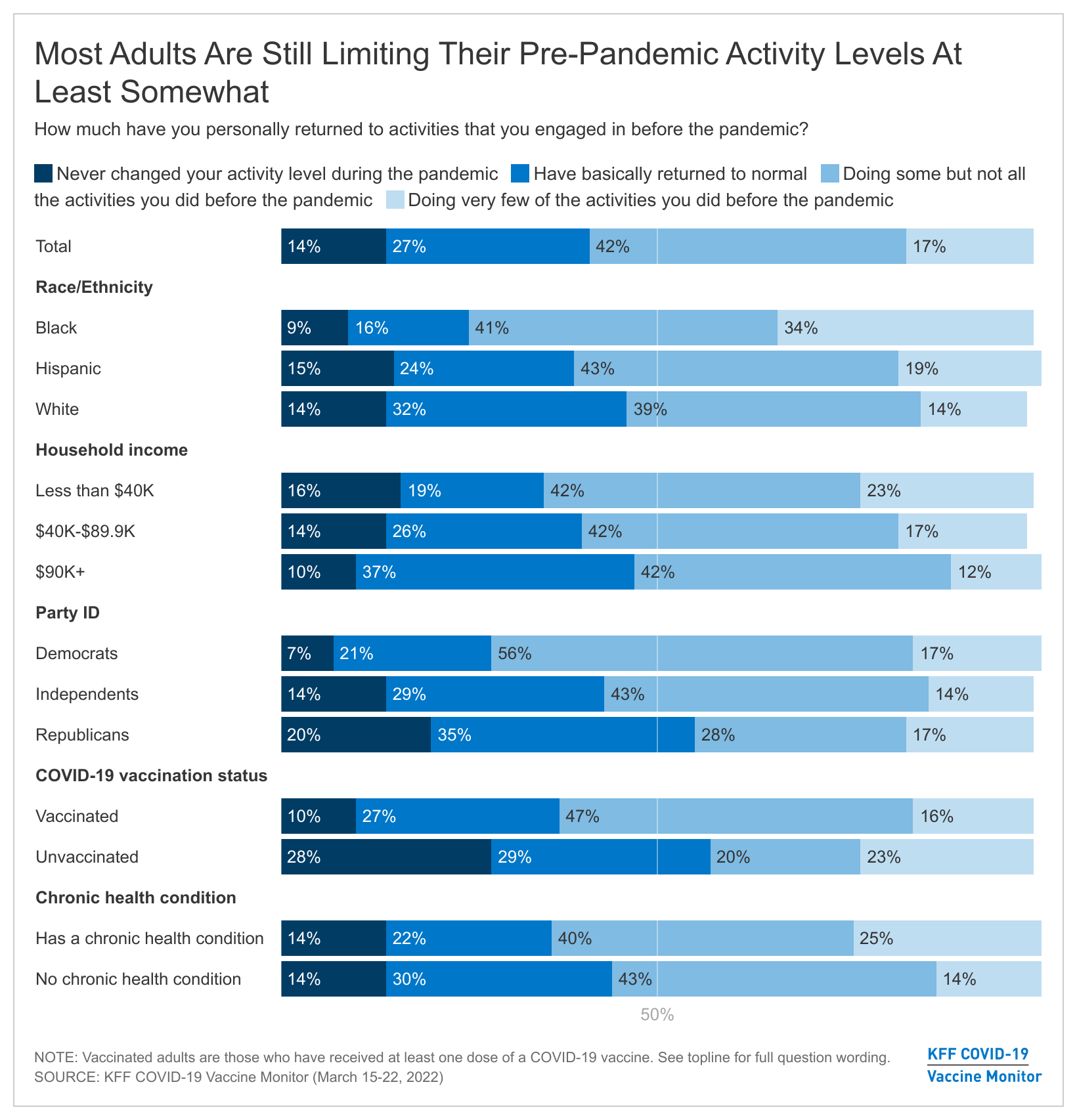

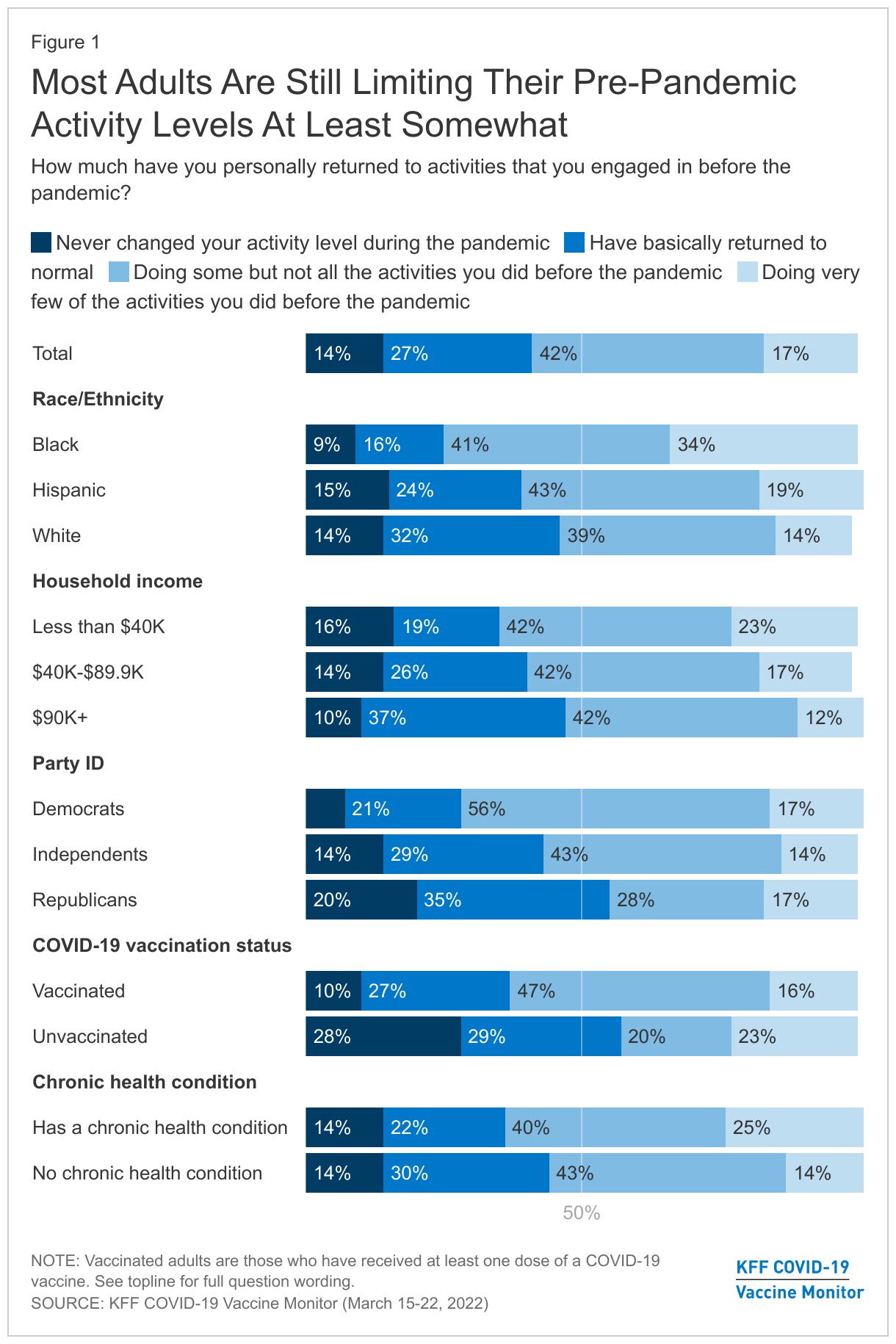

Conventional wisdom may be that Americans are ready to put COVID-19 in the rearview mirror and cast precautions aside, but the latest KFF COVID-19 Vaccine Monitor report finds that most adults have not yet resumed all of their normal pre-pandemic activities and most continue to mask regularly in public places.

Six in ten adults (59%) say they have not fully returned to their normal pre-pandemic activities, including 42% who say they have returned to doing only some of these activities and 17% who say they are doing very few of the activities they did before the pandemic. A smaller share of adults say they have basically returned to normal (27%) or never changed their routine at all (14%). Majorities of unvaccinated adults (57%) and Republicans (55%), and nearly half of White adults (47%) report they never changed activity levels or have basically returned to normal.

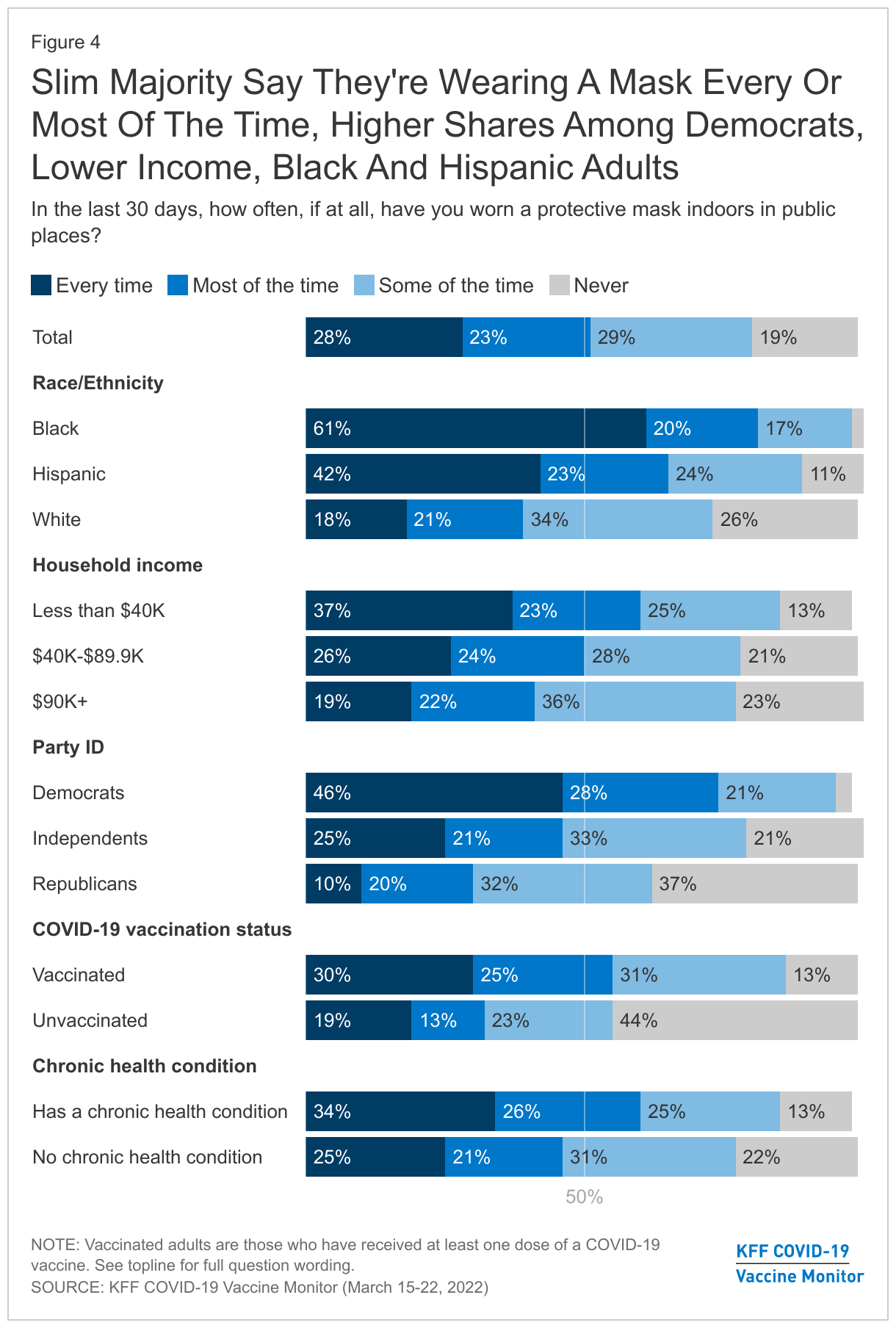

Around half of adults (51%) say that in the past 30 days they wore a mask every time or most of the time when indoors in public places, including 28% who say they wore one every time. This was higher among Black adults, with 61% of Black adults masking every time and 20% masking most of the time. By contrast, 18% of White adults reported using a mask every time.

About six in ten (59%) adults think people should continue to wear masks in public places to minimize the spread of COVID-19. The survey, which was conducted prior to the FDA approval of a fourth booster dose for certain groups, shows 40% of adults think people should stop wearing masks in public places “so things can get back to normal.”

Black and Hispanic adults, those with a chronic condition, and those with lower incomes are more likely to want people to keep masking. Larger shares of Black adults (88%) and Hispanic adults (69%) say people should continue to wear a mask in public places, versus White adults (49%). This finding may be reflective of larger shares of Black and Hispanic adults working in service industries compared to White adults, increasing their risk of exposure to COVID-19.

Similar to past reports, views of masking are largely divided across political parties and by vaccination status. Eighty-five percent of Democrats say people should continue masking in public places as do 67% of vaccinated adults. On the other hand, nearly seven in ten Republicans (69%) and unvaccinated adults (67%) say people should stop masking to so things can get back to normal.

With the federal public transportation masking requirement set to expire April 18, adults are split on whether the requirement should expire (51%) or be extended (48%) but views are largely partisan. A majority of Democrats (72%) and vaccinated adults (54%) say they support extending the public transit masking requirement compared to around three quarters of Republicans (76%) and unvaccinated adults (73%) who support the April 18th expiration.

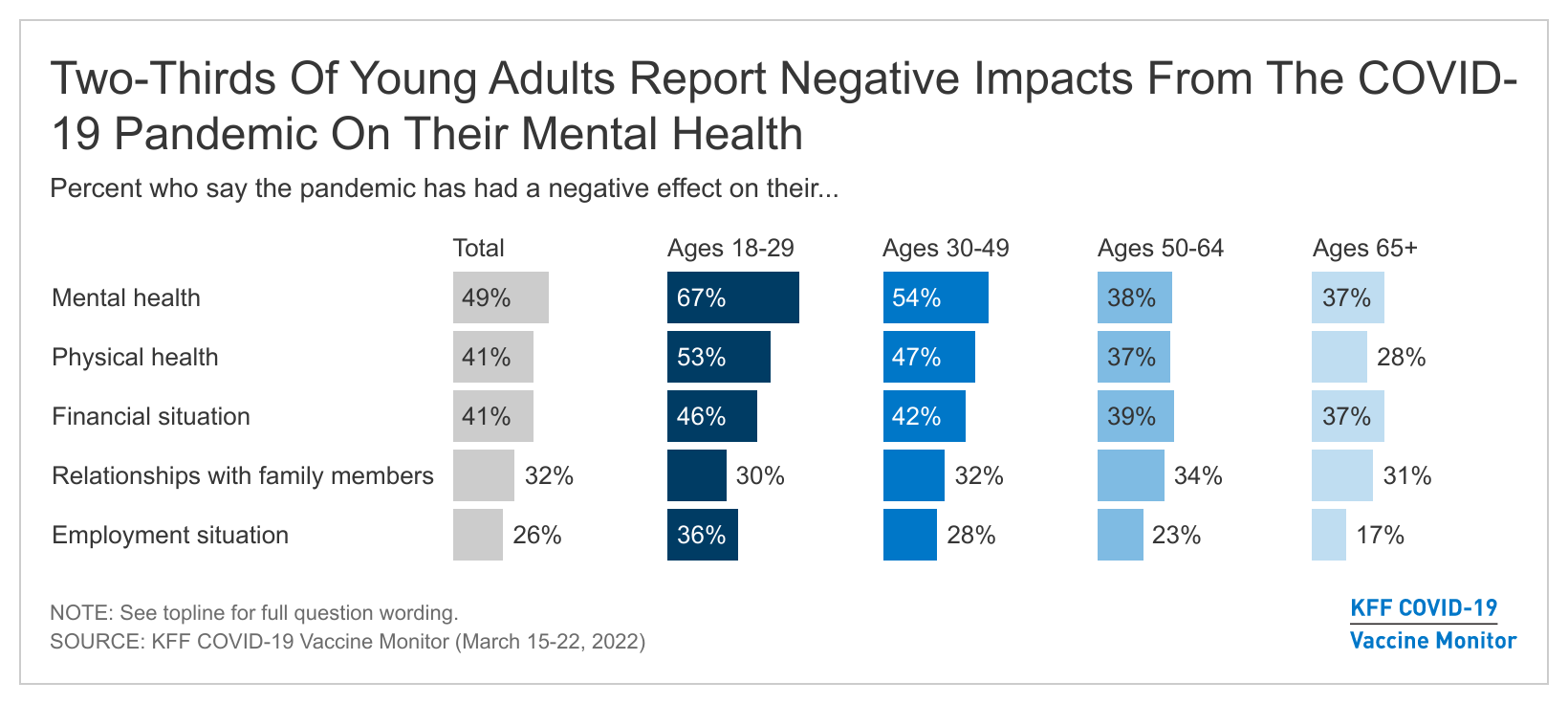

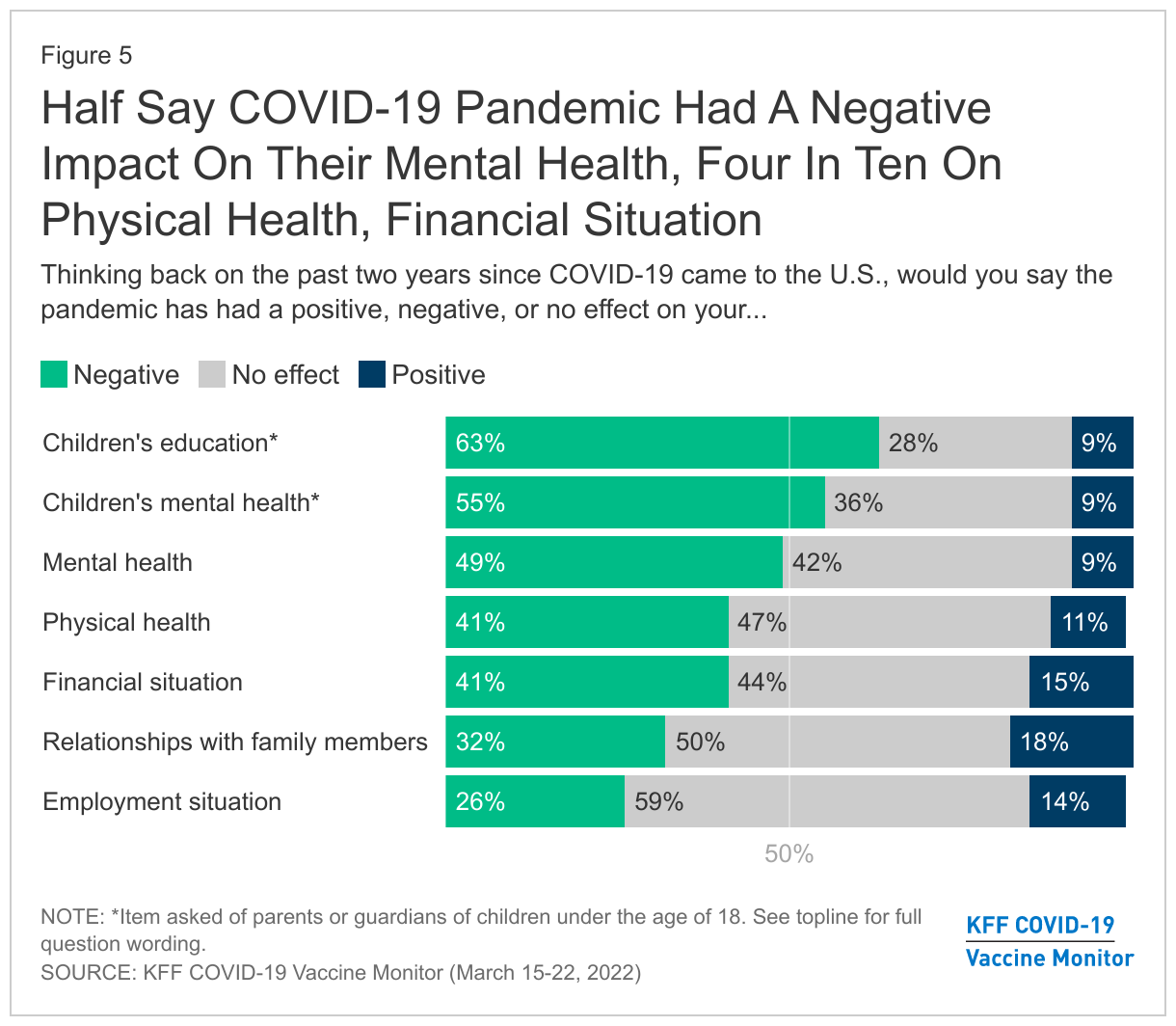

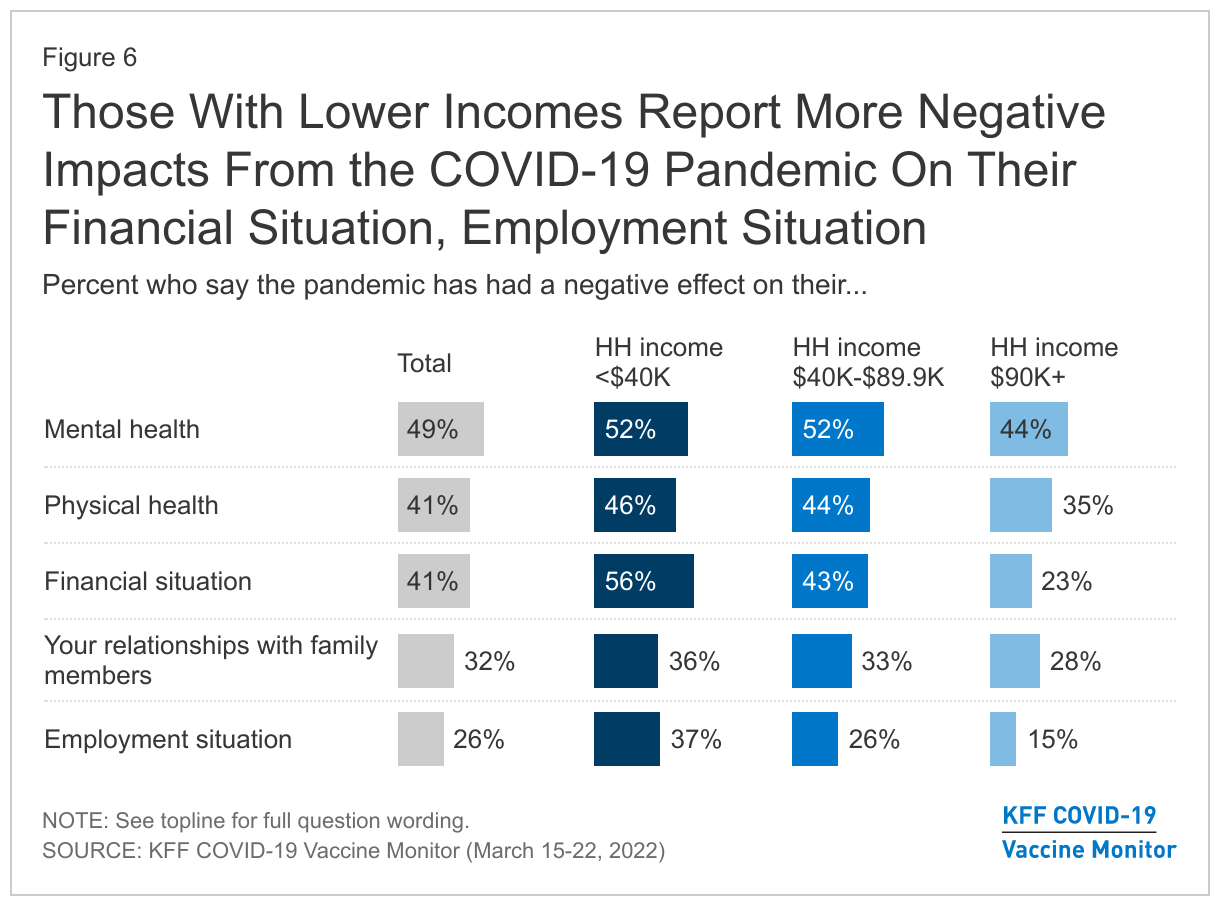

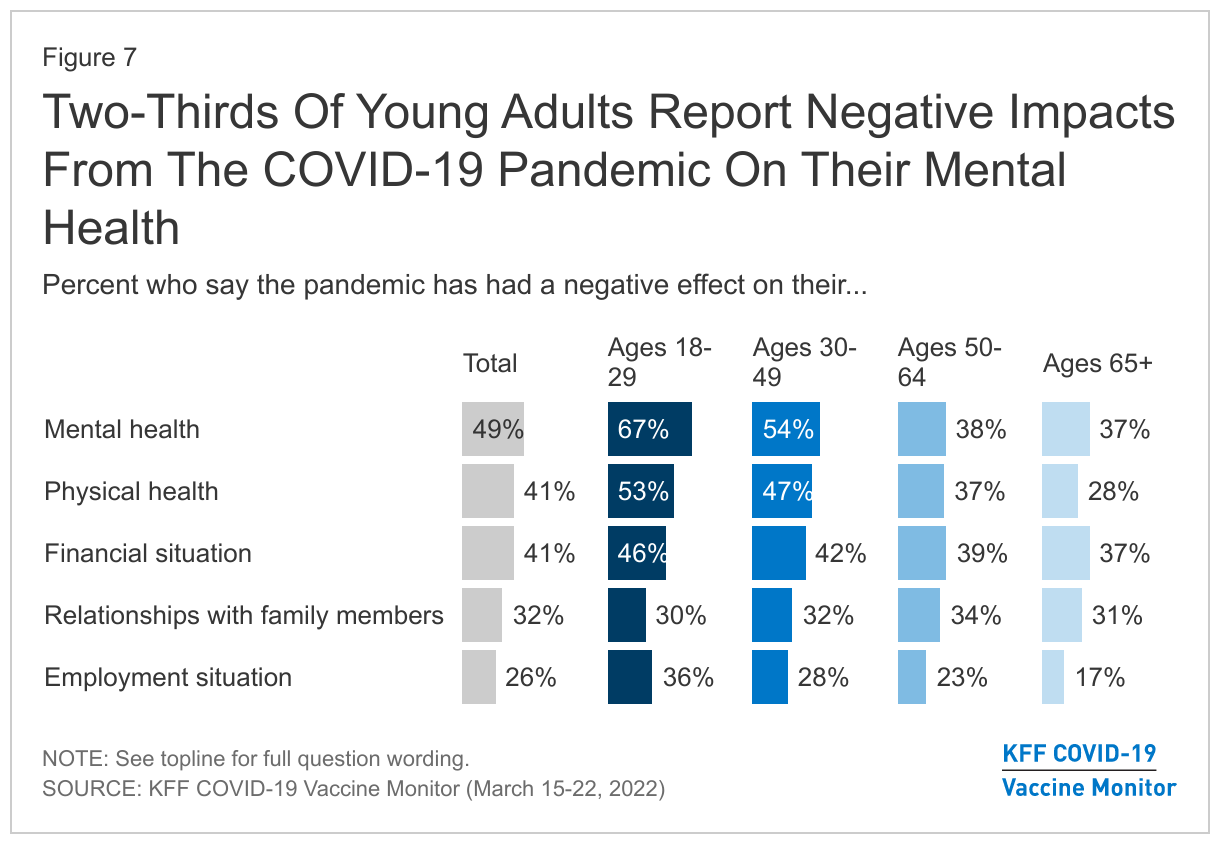

The latest KFF COVID-19 Vaccine Monitor also finds that two-thirds of parents (63%) say the pandemic has negatively affected their child’s education and over half (55%) say the pandemic had a negative impact on their child’s mental health. Overall, about half of all adults (49%) say the pandemic has had a negative effect on their mental health but younger adults are more likely to report difficulties with their mental and physical health compared to other age groups. Two-thirds (67%) of young adults (ages 18–29) say the pandemic has negatively impacted their mental health and 53% of this group reports a negative impact on their physical health.

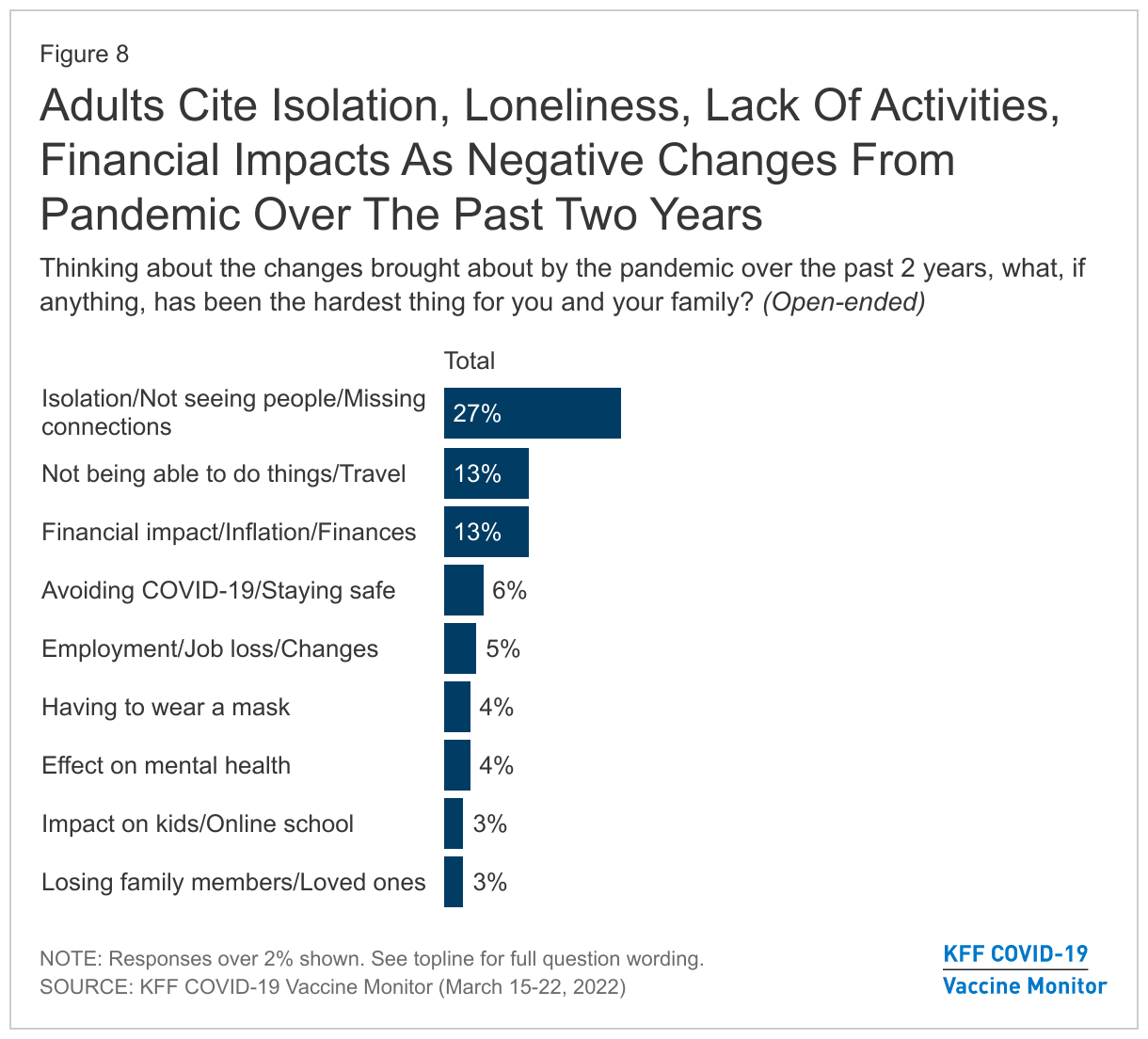

When asked to name in their own words the hardest part of the pandemic over the past two years, people most often cited the lack of human interactions with about one in four (27%) adults saying the hardest part of the pandemic was isolating and not seeing people.

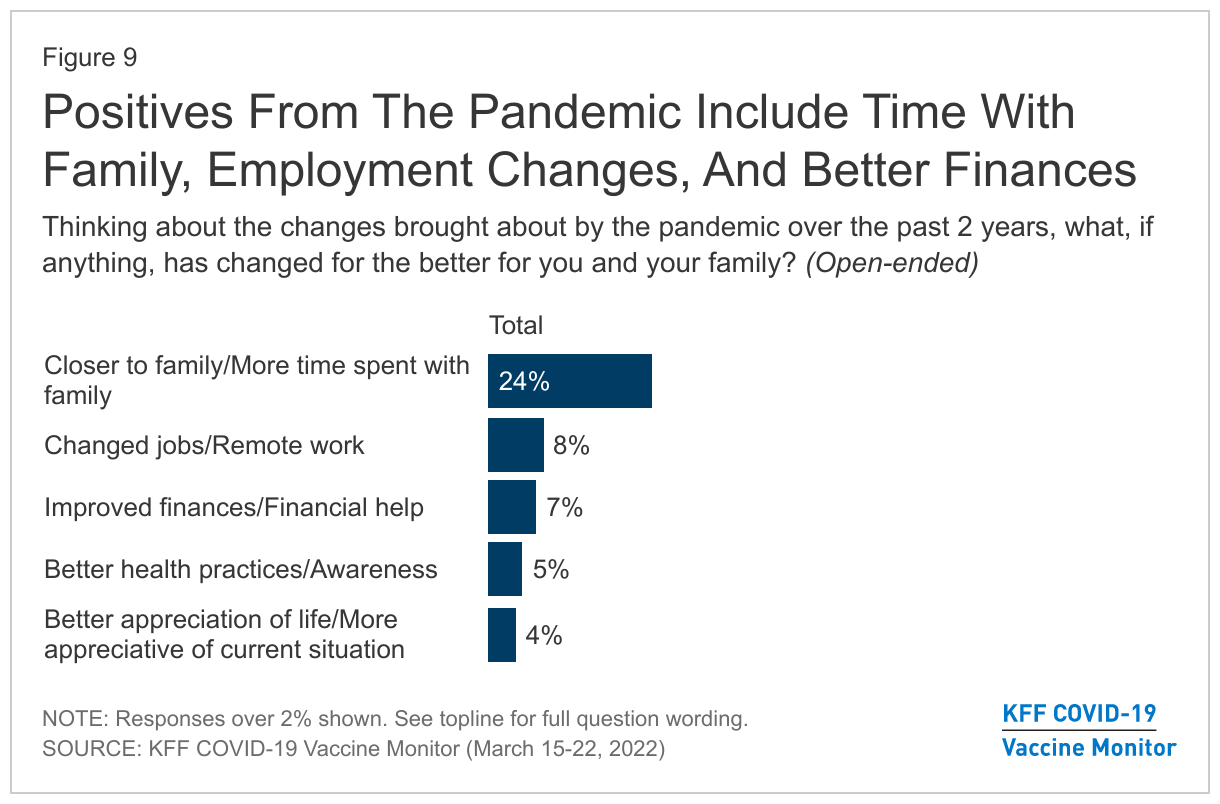

On the flip side, when asked about the positives of the pandemic, 24% of adults say changes brought about by the pandemic have made them closer to their families.

Designed and analyzed by public opinion researchers at KFF, the KFF COVID-19 Vaccine Monitor was conducted from March 15-22 among a nationally representative probability-based sample of 1,243 adults. Interviews were conducted in English and Spanish online (974) and by telephone (269). The margin of sampling error is plus or minus 4 percentage points for the full sample. For results based on subgroups, the margin of sampling error may be higher.

The KFF COVID-19 Vaccine Monitor is an ongoing research project tracking the public’s attitudes and experiences with COVID-19 vaccinations. Using a combination of surveys and qualitative research, this project tracks the dynamic nature of public opinion as vaccine development and distribution unfold, including vaccine confidence and acceptance, information needs, trusted messengers and messages, as well as the public’s experiences with vaccination.

The KFF COVID-19 Vaccine Monitor is an ongoing research project tracking the public’s attitudes and experiences with COVID-19 vaccinations. Using a combination of surveys and qualitative research, this project tracks the dynamic nature of public opinion as vaccine development and distribution unfold, including vaccine confidence and acceptance, information needs, trusted messengers and messages, as well as the public’s experiences with vaccination.

Key Findings:

With pandemic-related restrictions being lifted in many states as well as local areas and remaining mask mandates set to expire soon, most of the public (59%) say they have personally returned to doing some of their pre-pandemic activities, but not all, or say they are still doing very few of the activities they were doing before the pandemic. Two years into the pandemic, about a quarter of adults say they have basically returned to normal while one in seven say they never changed their activity level during the pandemic.

With people returning to some pre-pandemic activities, majorities still report wearing masks in public indoor areas. Eight in ten adults say they’ve worn a mask in public indoors at least some of the time in the last 30 days. Similarly, most say people should continue to wear masks in some public places to minimize the spread of COVID-19 and avoid another surge in cases (59%) while four in ten say people should stop wearing masks in public so things can get back to normal. Views of the federal mask mandate on airplanes and public transit are divided, with half of the public wanting the mandate extended and half wanting it to expire.

Larger shares of Democrats and vaccinated adults report they’ve been wearing masks and want others to continue doing so, while most Republicans and unvaccinated adults are eager to return to normal and lift mask mandates. Further, compared to their counterparts, Black adults, Hispanic adults, and those with lower incomes are less likely to say they’ve returned to normal, more likely to say they’re wearing masks frequently, and much more likely to say people should continue to wear masks to minimize the spread of the virus and prevent another surge. With Black and Hispanic adults and those with lower-incomes more likely to work in jobs that are highly impacted by COVID-19, the survey finds that they’re more likely to show concerns over reopening and unmasking measures.

The pandemic has taken a heavy toll on adults and children over the last two years with many reporting difficulties balancing their child’s education and their work, household finances, and mental or physical health. Six in ten parents say the pandemic has negatively affected their children’s schooling and over half saying the same about their children’s mental health. In addition, half of adults overall say their own personal mental health has been negatively affected, and four in ten say the same about their physical health and their financial situation. Those with lower incomes are more likely to report a negative impact on their finances, while young adults are more likely than older adults to say the pandemic had a negative impact on their mental and physical health as well as their employment situation.

Asked to say in their own words what has been the biggest challenge and/or any positive change brought about by the pandemic over the past two years, the top responses on both the negative and positive side related to human interactions and relationships or lack thereof. On the negative side, 27% say the hardest thing has been isolation and not seeing people. When asked if anything has changed for the better because of the pandemic, 24% say they’re closer to their family or spent more time with their families.

How Ready Is The Public To Return To “Normal” And Who Is More Hesitant About Lifting Mask Restrictions?

The latest analysis from a KFF COVID-19 Vaccine Monitor survey1 finds that as the omicron surge recedes, a majority of adults say they are limiting their activity levels from pre-pandemic at least somewhat in order to protect themselves from COVID, with 42% who are doing some but not all the activities they did before the pandemic and 17% who are doing very few of the activities they did before COVID-19. Around four in ten adults say they have basically returned to normal in terms of activities that they engaged in before the pandemic (27%) or that they never changed their activity level to begin with (14%).

Unvaccinated adults (57%), Republicans (55%), and White adults (47%) are the groups most likely to say they never changed activity levels or have basically returned to normal. Nearly half of those with household incomes of $90,000 or more say the same. Black adults (34%), those with a chronic condition that puts them at higher risk for COVID-19 (25%), and those living in households with incomes less than $40,000 (23%) are the most likely to say they are doing very few of the activities they did before the pandemic.

About six in ten adults (59%) say that now that COVID-19 case rates are lower, people should continue to wear masks in some public places to minimize the spread and avoid another surge in cases, while four in ten say that people should stop wearing masks in most public places so things can go back to normal. There are significant divides not only by partisanship, and vaccination status, but also by race, ethnicity, and income.

Eight-five percent of Democrats say that people should continue to wear masks, as do 57% of independents and 67% of vaccinated adults. Around seven in ten Republicans (69%) say that people should stop wearing masks so that things can return to normal, as do 67% of unvaccinated adults.

While White adults are split (49% say people should stop wearing masks, 49% say they should continue to wear them in some public places), large majorities of Black adults (88%) and Hispanic adults (69%) say that people should continue to wear masks in some public places to minimize the spread of COVID-19. Around two-thirds of those with a household income of less than $40,000 a year (68%) say the same, compared to 55% of those with an income between $40,000-$89,900 and 54% of those with an income of $90,000 or more. This finding that people of color are more likely to support continued mask wearing may reflect larger shares of Black and Hispanic adults being employed in service industries compared to White adults, putting them at an increased risk of exposure to COVID-19.

This finding is consistent with previous Vaccine Monitor surveys, which found Black and Hispanic adults were more likely to be worried that they personally will contract COVID-19, as well as be worried that someone in their family or their child will get sick. Black and Hispanic adults, as well as those with lower incomes were also more likely to say they don’t get paid time off if they get COVID-19.

On the more specific question of mandating masks on public transportation, the public is more evenly divided. The federal government currently requires people to wear masks on airplanes, trains, and other public transportation. With this requirement set to expire on April 18, adults are split on whether the federal government should let the requirement expire (51%) or extend the requirement (48%).

Majorities of Democrats (72%) and vaccinated adults (54%) support extending the masking requirement on transportation. By contrast, three-quarters of Republicans (76%) and unvaccinated adults (73%), and over half of independents (55%) would prefer to let the requirement expire on April 18.

However, preferences for this federal mandate extend beyond partisanship and vaccination status, with lower income adults and people of color voicing support for keeping the requirement after April 18. At least six in ten of Black (69%) and Hispanic adults (61%) say the federal government should extend the requirement, compared to 41% of White adults. Over half of adults with lower incomes (55%) want to extend the masking requirement, compared to 44% of those with a household income of between $40,000-$89,900, and 45% of those with an income of $90,000 or more. Similar to views of general masking, this divide by racial and ethnic groups as well as income groups may reflect those most likely to be working in areas where they would be exposed to COVID-19 without mask mandates.

Those with chronic conditions are also more likely to support extending the federal mask mandate on transportation (56%), while more than half (55%) of those without chronic conditions want to let the mandate expire.

current MASK USAGE

Most adults report continuing to wear a mask at least sometimes in public places. Around half of adults (51%) say that in the past 30 days they wore a mask every time or most of the time when indoors in public places, including 28% who say they wore one every time. Another 29% say they wore a mask some of the time, and 19% say they never wore a mask indoors in public places.

In line with attitudes about mask requirements on transportation, Democrats are more likely to say they always or mostly wore a mask indoors in the past 30 days (75%), compared to independents (46%) and Republicans (30%).

Two-thirds of unvaccinated adults say they have been wearing a mask some of the time or never have worn a mask indoors in the past 30 days (67%), while one-third (32%) report wearing one every or most of the time. A majority of vaccinated adults say they wore a mask every or most of the time (56%).

Showing differences by race and ethnicity, twice the share of Black adults compared to White adults report wearing a mask always or most of the time in the past 30 days (80% vs. 39%). Around two-thirds of Hispanic adults say the same (65%).

The Pandemic’s Toll On Families Two Years In

IMPACTs ON MENTAL, PHYSICAL, and FINANCIAL HEALTH

The survey finds the pandemic has taken a heavy toll on adults and children over the last two years. Whether it comes to their education, work, finances, mental or physical health, many – regardless of race, ethnicity and income – report feeling the negative effects of the pandemic.

The most common negative effects of the pandemic, as reported by parents, are about their children’s education and mental health. Almost two-thirds of parents say that the pandemic has negatively affected their children’s education (63%), with 28% saying it had no effect, and 9% who report it had a positive effect. Moreover, over half (55%) of parents say the pandemic has had a negative impact on their children’s mental health, compared to 36% who say it made no difference, and 9% saying it had a positive effect.

Among all adults, half say the pandemic has had a negative effect on their personal mental health (49%), and 41% say it has had a negative impact on their physical health. Few say it has had a positive effect on either their physical (11%) or mental health (9%).

About four in ten adults say the pandemic had a negative impact on their financial situation (41%) while a similar share report it had no impact (44%), with 15% who say it had a positive impact. One-quarter of adults say the pandemic has had a negative impact on their employment situation (26%), with 59% who report it has not had an impact.

Results are more mixed when it comes to the pandemic’s effect on family relationships. Around a third say the pandemic has had a negative impact on their relationships with family members (32%) while 18% say it has had a positive impact. Half say it has not had any impact one way or another.

Adults in households with lower incomes report being harder hit by the pandemic, especially when it comes to financial and employment impacts. Adults with a household income of less than $40,000 a year are more likely to say the pandemic has had a negative impact on their financial situation (56%), compared to 43% of those with an income of between $40,000 and $90,000 and 23% of those with a household income of $90,000 or more a year.

In addition, the share of those with lower incomes who say the pandemic had a negative impact on their employment situation (37%) is more than twice the share of those with annual incomes greater than $90,000 (15%).

Younger people also report disproportionate effects from the COVID-19 pandemic, especially when it comes to their mental and physical health. Two-thirds of young adults aged 18-29 (67%) report that the pandemic has had a negative impact on their mental health, compared to just over half of 30-49 year-olds (54%), and under four in ten 50-64 year-olds (38%) and those over the age of 65 (37%).

Young adults are also more likely to report difficulties with their physical health due to the pandemic, with 53% of those under 30 reporting a negative impact, 47% of those 30-49, 37% of those 50-64, and 28% of those over the age of 65. In addition, larger shares of young adults report negative effects on their employment situation (36%) compared to older adults, including those ages 50-64 (23%) and those 65 and older (17%).

PANDEMIC IMPACTS: IN THEIR OWN WORDS

In their own words, when asked about the biggest challenge and/or positive change brought about by the pandemic over the past two years, the top responses regarding both negative and positive effects were related to human interactions and relationships, or the lack thereof.

When asked about changes that have been brought about by the pandemic over the past two years, 27% say the hardest thing has been isolation and not seeing people. Another 13% say they have struggled with not being able to do things or travel, and 13% cite the financial impact, including inflation.

Some say the hardest part has been avoiding COVID-19 and staying safe (6%), employment changes and job loss (5%), having to wear a mask (4%), the effect on mental health (4%), the impact on kids and online schooling (3%), and losing family members and loved ones (3%).

In their own words: Thinking about the changes brought about by the pandemic over the past two years, what, if anything, has been the hardest thing for you and your family?“

Being evicted and still not recovered financially.” – 43 year old, male, White, Democrat, South Carolina

“Not allowed to be with my wife when she was hospitalized with stage 4 cancer.” – 65 year old, male, White, Republican, Arkansas

“Finances, health, loss of family members, being hospitalized, lasting effects. My family's going through things because of the whole COVID thing. Their finances are going down and they're struggling; I had to leave my apartment - everything was chaotic.” – 31 year old, female, White, Independent, Tennessee

“Concern over preexisting conditions.” – 24 year old, female, Asian, Democrat, Illinois

“Deal with all mandates and restrictions.” – 30 year old, male, Hispanic, independent, Indiana

“Just the online schooling, I had to quit work to stay at home.” – 31 year old, female, White, Democrat, Ohio

“Division over what's real or not and what we should follow.” – 25 year old, male, Hispanic, Republican, Florida

“Having to wear masks everywhere, it’s terrible.” – 24 year old, male, White, Independent, Michigan

“Inability to visit elderly parents.” – 63 year old, male, White, Independent, Florida

“Getting clear information about it and how best to manage through the maze of many, many authorities giving advice about Covid.” – 90 year old, female, Black, Democrat, New York

“Mask mandates and business closures, especially as a truck driver.” – 58 year old, male, White, independent, South Dakota

“Medical debt, inability to work from disabilities exacerbated or initiated by covid.” – 31 year old, other, White, independent, Oregon

“Loss of non-family social relationships.” – 22 year old, female, White, Democrat, New York

“Mental health got a lot worse due to distancing people from each other.” – 38 year old, male, White, independent, Illinois

“The grief of people dying.” – 39 year old, female, White, independent, Texas

When asked if anything has changed for the better in the last two years, 24% say they are closer to their family or have spent more time with their families. Some (8%) also say that job changes or remote work were a positive change, 7% cited improvements in their financial situation, 5% said they had better health practices or awareness, and 4% cited a general appreciation of life or their current situation. A third of respondents said nothing changed for the better.

In their own words: Thinking about the changes brought about by the pandemic over the past two years, what, if anything, has changed for the better for you and your family?“

Being able to use telehealth communications for doctors and by doing a lot of things by phone and email now, very convenient for families.” – 25 year old, female, White, independent, Kentucky

“Closer bonding with family and more stability with work life.” – 30 year old, male, Asian, independent, Texas

“Eating more prepared meals from home and saving money.” – 66 year old, female, White, Republican, Illinois

“Better handwashing and wearing a mask has helped with overall health.” – 66 year old, male, White, Democrat, California

“Gives me a good excuse to get out of dinner with in-laws.” – 37 year old, other, Hispanic, independent, Pennsylvania

“It helped cherish the moments you have with each other and to be less wasteful. Realize that habits/behaviors can change all the time; make the best changes.” – 39 year old, female, Black, Democrat, Tennessee

“The stimulus checks helped keep me out of debt.” – 52 year old, female, White, independent, Colorado

“More remote opportunities in education and employment.” – 21 year old, male, White, Democrat, Maryland

Methodology

This KFF Health Tracking Poll/COVID-19 Vaccine Monitor was designed and analyzed by public opinion researchers at the Kaiser Family Foundation (KFF). The survey was conducted March 15-22, 2022 online and by telephone among a nationally representative sample of 1,243 U.S. adults, conducted in English (1,188) and in Spanish (55). The sample includes 1,004 adults reached through the SSRS Opinion Panel either online or over the phone (n=39 in Spanish). The SSRS Opinion Panel is a nationally representative probability-based panel where panel members are recruited randomly in one of two ways: (a) Through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS) provided by Marketing Systems Groups (MSG) through the U.S. Postal Service’s Computerized Delivery Sequence (CDS); (b) from a dual-frame random digit dial (RDD) sample provided by MSG. For the online panel component, invitations were sent to panel members by email followed by up to three reminder emails. 974 panel members completed the survey online and panel members who do not use the internet were reached by phone (30).

Another 239 (n=16 in Spanish) interviews were conducted from a random digit dial telephone sample of prepaid cell phone numbers obtained through MSG. Phone numbers used for the prepaid cell phone component were randomly generated from a cell phone sampling frame with disproportionate stratification aimed at reaching Hispanic and non-Hispanic Black respondents. Stratification was based on incidence of the race/ethnicity groups within each frame.

The combined cell phone and panel samples were weighted to match the sample’s demographics to the national U.S. adult population using data from the Census Bureau’s 2021 Current Population Survey (CPS). Weighting parameters included sex, age, education, race/ethnicity, region, and education. The sample was also weighted to match patterns of civic engagement from the September 2017 Volunteering and Civic Life Supplement data from the CPS. The sample was also weighted to match frequency of internet use from the National Public Opinion Reference Survey (NPORS) for Pew Research Center. The weights take into account differences in the probability of selection for each sample type (prepaid cell phone and panel). This includes adjustment for the sample design and geographic stratification of the cell phone sample, within household probability of selection, and the design of the panel-recruitment procedure.

The margin of sampling error including the design effect for the full sample is plus or minus 4 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. For results based on other subgroups, the margin of sampling error may be higher. Sample sizes and margins of sampling error for other subgroups are available by request. Sampling error is only one of many potential sources of error and there may be other unmeasured error in this or any other public opinion poll. Kaiser Family Foundation public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

This work was supported in part by grants from the Chan Zuckerberg Initiative DAF (an advised fund of Silicon Valley Community Foundation), the Ford Foundation, and the Molina Family Foundation. We value our funders. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Group

N (unweighted)

M.O.S.E.

Total

1,243

± 4 percentage points

COVID-19 vaccination status

Have gotten at least one dose of the COVID-19 vaccine

981

± 4 percentage points

Have not gotten the COVID-19 vaccine

259

± 7 percentage points

Race/Ethnicity

White, non-Hispanic

748

± 5 percentage points

Black, non-Hispanic

188

± 10 percentage points

Hispanic

213

± 9 percentage points

Party identification

Democrat

396

± 6 percentage points

Republican

321

± 7 percentage points

Independent

310

± 8 percentage points

Registered voters

Total voters

1,036

± 4 percentage points

Democratic voters

351

± 7 percentage points

Republican voters

293

± 7 percentage points

Independent voters

253

± 9 percentage points

Endnotes

The latest data from the KFF COVID-19 Vaccine Monitor includes interviews conducted over the phone and online using a probability-based sample. ↩︎

The disproportionate impact of the COVID-19 pandemic on nursing facility residents and staff has brought increased attention to long-standing workforce issues that can affect care quality and safety, such as staffing shortages and high turnover rates. These issues have existed for decades and have been associated with adverseoutcomes, including increased mortality rates, hospitalization rates, and emergency department visits. In a recent KFF poll, a majority (70%) of adults said that this country’s nursing facilities and other long-term facilities are doing a “bad job” of maintaining adequate staffing levels.

Since the onset of the pandemic, more than 200,000 COVID-19 deaths have occurred among long-term care residents and staff, with most of these deaths (150,000 COVID-19 deaths) occurring among residents and staff in nursing facilities that are certified to receive Medicare and/or Medicaid payments. In response to these issues, the Biden Administration recently announced a set of nursing facility reforms, which were highlighted in the State of the Union address.

This analysis presents the most recent national and state-level data on nursing facility-reported staff shortages and describes the Biden Administration’s new policy initiatives to address staffing and other quality issues in nursing facilities. National staff shortage trend data spans from May 2020, the first month when nursing facilities were required to report COVID-19 facility data to the CDC, through March 20, 2022, the most recent week of data available. See the Methods box below for more details.

1. What do the data show about nursing facility staffing?

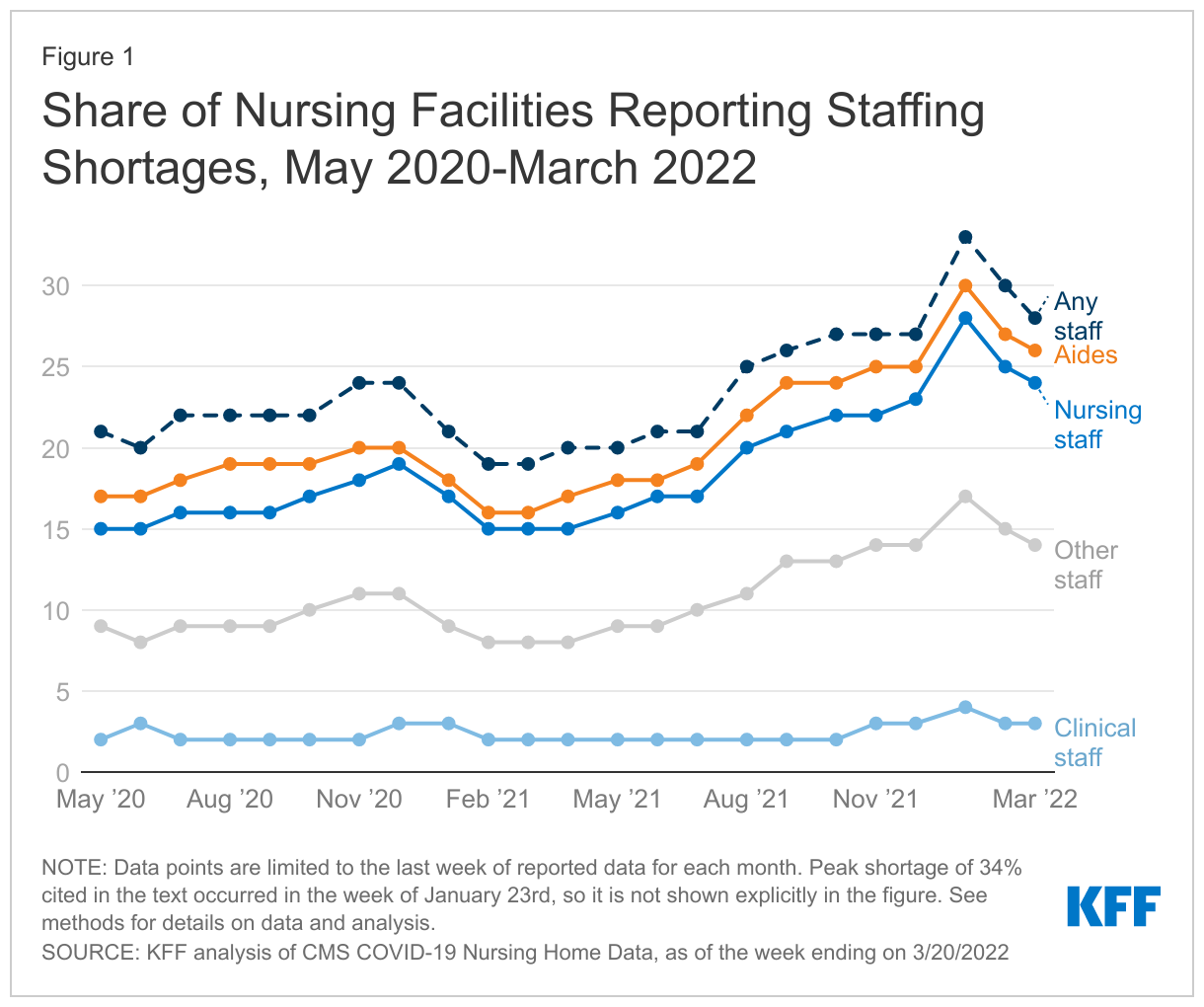

As of the week ending March 20, 2022, the most recent data available, 28% of nursing facilities reported at least one staffing shortage (approximately 3,900 out of 14,000 facilities) (Figure 1). The current rate represents a slight drop since the week ending January 23, 2022, when the share of nursing facilities reporting a staff shortage peaked at 34%. This slight decline between January and March may be partly due to the decline in cases related to the Omicron variant as well as other potential factors, including anecdotalaccounts of nursing facilities offering higher wages to attract workers. The current rate, 28%, is higher than the rate reported in May 2020, when 21% of nursing facilities reported at least one type of staff shortage.

The current level of staff shortages coincides with a period when health care providers, including nursing facilities, grappled with the impact of the Omicron variant, a highly transmissible variant that broke case and hospitalization records. This variant primarily affected residents and staff who were not vaccinated or boosted, though vaccinated older adults and those with other health conditions still faced a high risk of infection and mortality.

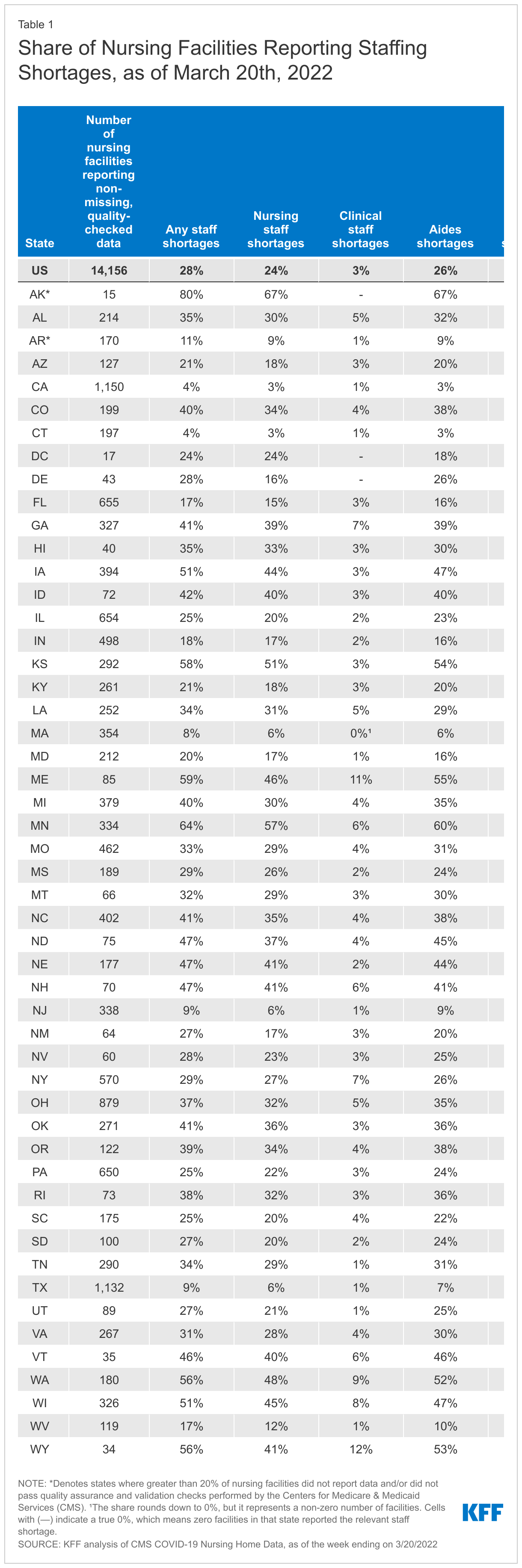

Nursing facilities were most likely to report a shortage of aides and least likely to report a shortage of clinical staff as of March 20, 2022. (Figure 1). Among the approximately 14,000 nursing facilities reporting complete and reliable data for the week ending March 20th, 26% reported aide shortages while just 3% reported clinical staff shortages. Staff shortages were nearly as high for nursing staff as they were for aides, with 24% of facilities reporting nursing staff shortages. In the same time period, 14% reported other staff shortages. These patterns have held steady since nursing facilities began reporting this data in May 2020. For purposes of reporting staff shortages, the Centers for Medicare & Medicaid Services (CMS) defines aides to include certified nursing assistants (CNAs), nurse aides, and medication aides or technicians. Aides typically oversee overall care needs, including assistance with personal care needs and ensuring that each resident’s plan of care is being followed. Clinical staff primarily oversee medical needs and include physicians, physician assistants, and advanced practice nurses. Nursing staff include registered nurses, licensed practical nurses, and vocational nurses.

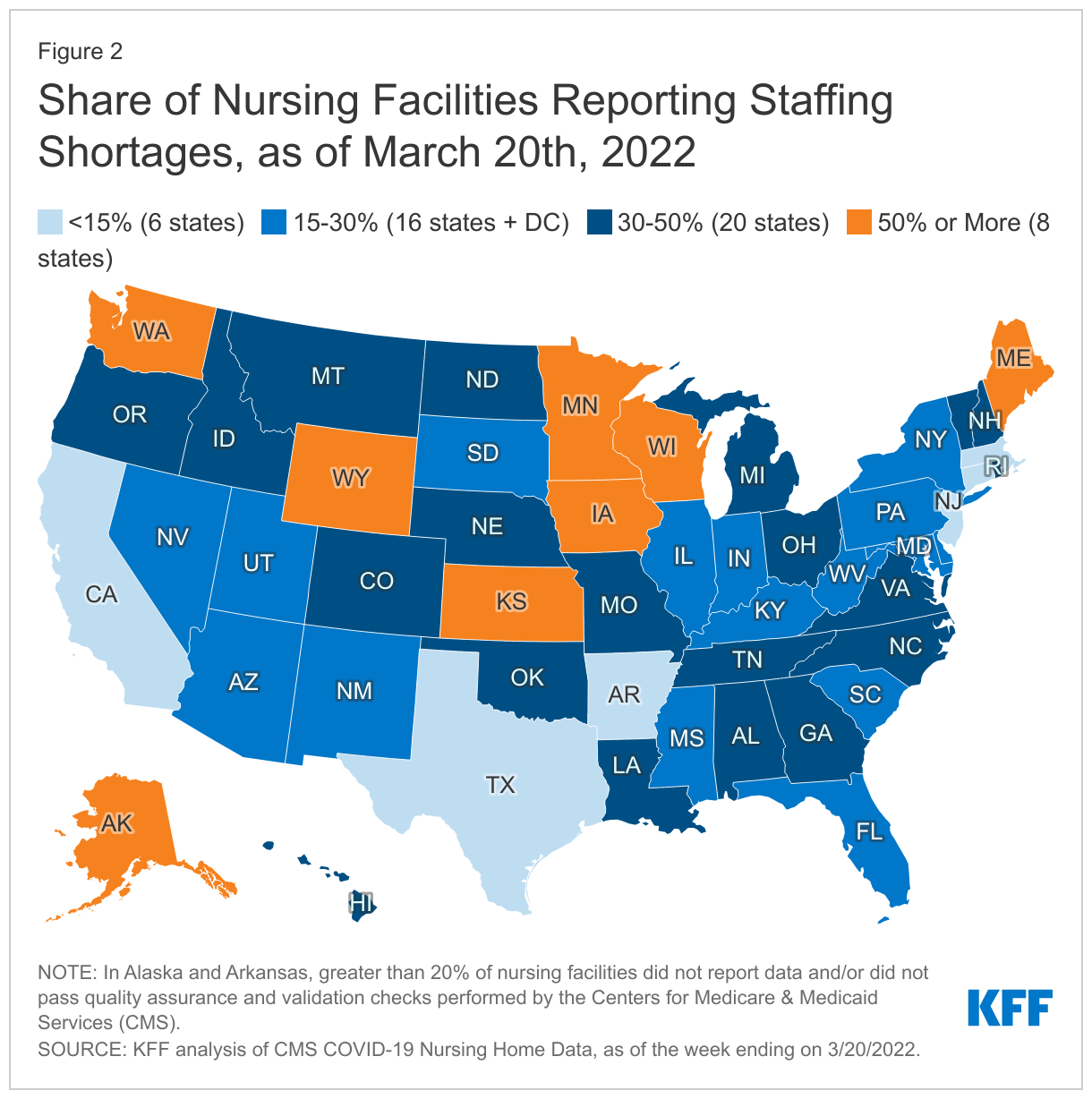

The share of nursing facilities reporting staffing shortages varies widely by state (Figure 2 and Table 1). As of the week ending March 20, 2022, the share of nursing facilities reporting staff shortages ranged from 4% of nursing facilities in Connecticut and California to 80% in Alaska (Figure 2, Table 1). Of note, less than 80% of nursing facilities in Alaska reported data and passed quality-checks performed by CMS.

In eight states, at least half of nursing facilities reported one or more staff shortage as of March 20, 2022. The five states with the highest shares of nursing facilities reporting any staffing shortages include Alaska (80%), Minnesota (64%), Maine (59%), Kansas (58%), and Wyoming (56%). Conversely, the five states with the lowest share of nursing facilities reporting staff shortages include California (4%), Connecticut (4%), Massachusetts (8%), Texas (9%), and New Jersey (9%) (Table 1). State variation in staffing shortages at the facility-level may be attributable to variation in local economies and labor markets, and could also be due to differences in the way in which nursing facilities define staff shortages.

2. What new policies did the Biden Administration announce?

The Biden Administration’s new initiatives are focused on improving care quality, nursing facility oversight, data transparency, career pathways, and pandemic and emergency preparedness. Key policy proposals include establishing minimum staffing levels for Medicare and Medicaid-certified nursing facilities, strengthening oversight of poor-performing nursing facilities, supporting state efforts to tie Medicaid reimbursement rates to increases in staff compensation, and launching a national nursing career pathways campaign to recruit, train, and retain long-term care staff, among others. While some of the new policies can be adopted by the Administration, others would require Congressional action.

The Biden Administration plans to propose new regulations that would establish a minimum nursing facility staffing requirement within the next year. The fact sheet announcing this new proposal highlights adequate staffing levels as the “measure most closely linked to the quality of care residents receive.” The fact sheet cites a study of Connecticut nursing facilities, which found that an increase in registered nurse staffing of 20 minutes per resident day was associated with 22 percent fewer confirmed COVID-19 cases and 26 percent fewer COVID-19 deaths. Before proposing new regulations, CMS will conduct a new study to “determine the level and type of staffing needed to ensure safe and quality care.” Policymakers and other stakeholders have debated issues about care quality and staffing levels ever since federal requirements for nursing facilities to receive Medicare and Medicaid funds were established. The 1987 Nursing Home Reform Act adopted the current federal requirement that facilities provide 24-hour licensed nursing services “sufficient to meet resident needs,” including registered nurse services at least eight consecutive hours per day. However, there are no other federal requirements for minimum staffing hours per resident day, and staffing levels and their impact on care quality remain a topic of recurring concern among government regulators and other stakeholders. While these proposed Biden reforms could take place administratively, some policy changes can be done via legislation. Provisions in the Build Back Better Act (BBBA) passed by the U.S. House of Representatives would have required HHS to conduct regular studies and report to Congress on the appropriateness of establishing minimum staffing ratios in nursing homes and to specify any appropriate minimum ratios for nurses and aides in regulations. However, whether the BBBA advances in the Senate remains uncertain.

3. What issues are important to watch?

Looking ahead, open questions remain about how and when the new Biden policy proposals will be implemented. The specific details about what minimum staff levels will be proposed are not yet known, and as noted above, CMS intends to conduct a study to inform the new proposed regulations. While the Administration plans to issue proposed rules within a year, it is not yet known when the new rules would be finalized or take effect. Enforcement of the new rules will likely be through the existing state inspection process, with facilities potentially subject to penalties such as fines or loss of Medicare or Medicaid funding. Another open question is how stakeholder reaction will affect the new rules. The proposal faces stiff opposition from the nursing home industry, which argues that facilities will be unable to meet new staffing and oversight requirements without additional federal funding. Proponents of the new rules contend that minimum staffing requirements are an important protection for nursing home residents. Others argue that the Biden proposal does not go far enough and should also address issues around Medicaid reimbursement rates and worker compensation. It is not clear whether Congress will authorize additional federal funding beyond the pandemic relief funds already provided for nursing facilities.

Another open question is how the pandemic and CMS’s health care provider vaccination mandate will affect nursing facility staffing shortages. When issuing the mandate, CMS acknowledged that some staff may leave their jobs because they do not want to receive the vaccine, but cited examples of vaccine mandates adopted by health systems in Texas and Detroit and a long-term care parent corporation with 250 facilities as well as the New York state health care worker mandate, all of which resulted in high rates of compliance and few employee resignations. Staff vaccination rates currently vary by state, likely reflecting a mix of federal mandate deadlines not yet passing, varying state and/or local mandates, and different degrees of vaccine hesitancy among staff. Data also show that the number of workers in nursing care and elder care facilities has continued to decline even while other health settings have returned to nearly pre-pandemic levels, raising questions about the long-term effects of the pandemic on the workforce. Forthcoming KFF analyses will analyze the impact of the mandate when data is available, as well as evaluate state minimum staffing requirement changes post-COVID. It will be important to watch whether and how lessons from the pandemic are integrated into new policies to improve nursing facility care quality and protect residents and staff.

Methods

This analysis uses federal data on staffing reported weekly by facilities to the CDC’s National Healthcare Safety Network (NHSN) and reflects data from mid-May 2020 through March 20, 2022. These data are updated regularly to reflect revised data from previous weeks, so future versions of this dataset reflecting the same time period may output different values.

Each week, approximately 15,200 nursing facilities submit data through NHSN, including whether they are experiencing a shortage in nursing staff (including registered nurses, licensed practical nurses, and vocational nurses), clinical staff (including physicians, physician assistants, and advanced practice nurses), aides (including certified nursing assistants, nurse aides, medication aides, and medication technicians), or other staff (including administrative, custodial, and other environmental service staff). These measures are asked and reported as binary measures (yes/no) and reflect staffing shortages as of the week of data reporting; therefore, we are unable to determine the magnitude of staffing shortages among nursing facilities that report “yes” to one or more staff positions. Additionally, these measures differ from other measures of staffing sufficiency, including the minimum staffing levels required by the federal government and states.

CMS performs data quality checks to identify facilities that may have entered incorrect data before publishing this data for public download. Facilities that have submitted erroneous data will have an “N” displayed in the column titled “Passed Quality Assurance Check”. Our final sample of nursing facilities in this analysis excludes facilities that CMS flagged in their data quality check, as well as facilities that are missing shortage measures. With these exclusions, each week of data in Figure 1 represents anywhere from 14,100 to 15,100 facilities. Each week of data represents a slightly different set of facilities due to weekly variation in nursing facility reporting. The most recent week of data, as of March 20, 2022, includes 14,156 nursing facilities. The federal data includes only data on Medicare or Medicaid certified nursing facilities. This analysis therefore does not reflect other long-term care settings, such as assisted living facilities, residential care facilities, group homes, or intermediate care facilities.