A Snapshot of Sources of Coverage Among Medicare Beneficiaries

Most in Traditional Medicare Have Supplemental Coverage that Helps Cover Medicare Cost Sharing but More Than Three Million Don’t

Health care affordability has been a longstanding concern in the U.S., including among older adults, many of whom have relatively low incomes and modest assets to help cover the cost of premiums and medical bills. Medicare offers important financial protection by providing health insurance coverage to 69 million people in the U.S., including adults age 65 or older and younger adults with long-term disabilities. However, Medicare-covered benefits are subject to cost-sharing requirements and exclude some commonly needed services, like dental and vision care. Additionally, traditional Medicare does not include a cap on out-of-pocket costs.

To help with cost sharing for Medicare-covered services and fill the gaps in Medicare benefits, most Medicare beneficiaries supplement traditional Medicare with additional coverage, such as Medigap, for which policyholders pay an average of $2,600 annually in premiums. More than half of people with Medicare are currently enrolled in Medicare Advantage, which offers extra benefits not available in traditional Medicare and caps annual out-of-pocket costs. Medicare beneficiaries may also have employer- or union-sponsored coverage or Medicaid coverage in addition to Medicare. But some people on Medicare lack additional coverage and face the risk of incurring high out-of-pocket costs if they need expensive medical care.

This analysis documents the different sources of coverage among people with Medicare and examines variation in beneficiary characteristics by source of coverage. The analysis draws on data from the Centers for Medicare & Medicaid Services (CMS) March 2025 Medicare Advantage enrollment files and the 2023 Medicare Current Beneficiary Survey (see Methods for details).

Key Facts

- More than half of all people with Medicare Part A and Part B (54% or 34.1 million in 2025) are enrolled in a Medicare Advantage plan, while 46% (28.7 million) are in traditional Medicare.

- Among traditional Medicare beneficiaries, most (87%) had additional coverage that supplements Medicare benefits in 2023, but 3.5 million beneficiaries (13%) lacked additional coverage, leaving them at risk of facing high out-of-pocket costs for medical care.

- Overall, 14.1 million beneficiaries (23% of all Medicare beneficiaries) had employer or union sponsored coverage in 2023, either as a supplement to traditional Medicare or through group Medicare Advantage plans, another 12.2 million (20%) had Medicaid in addition to traditional Medicare or Medicare Advantage, and the same number, 12.2 million (20%) had a Medicare supplemental insurance (Medigap) policy to supplement traditional Medicare.

- The number and share of Medicare beneficiaries with Medicaid (dual eligible individuals) were substantially higher in Medicare Advantage (68%) than traditional Medicare (32% in 2023).

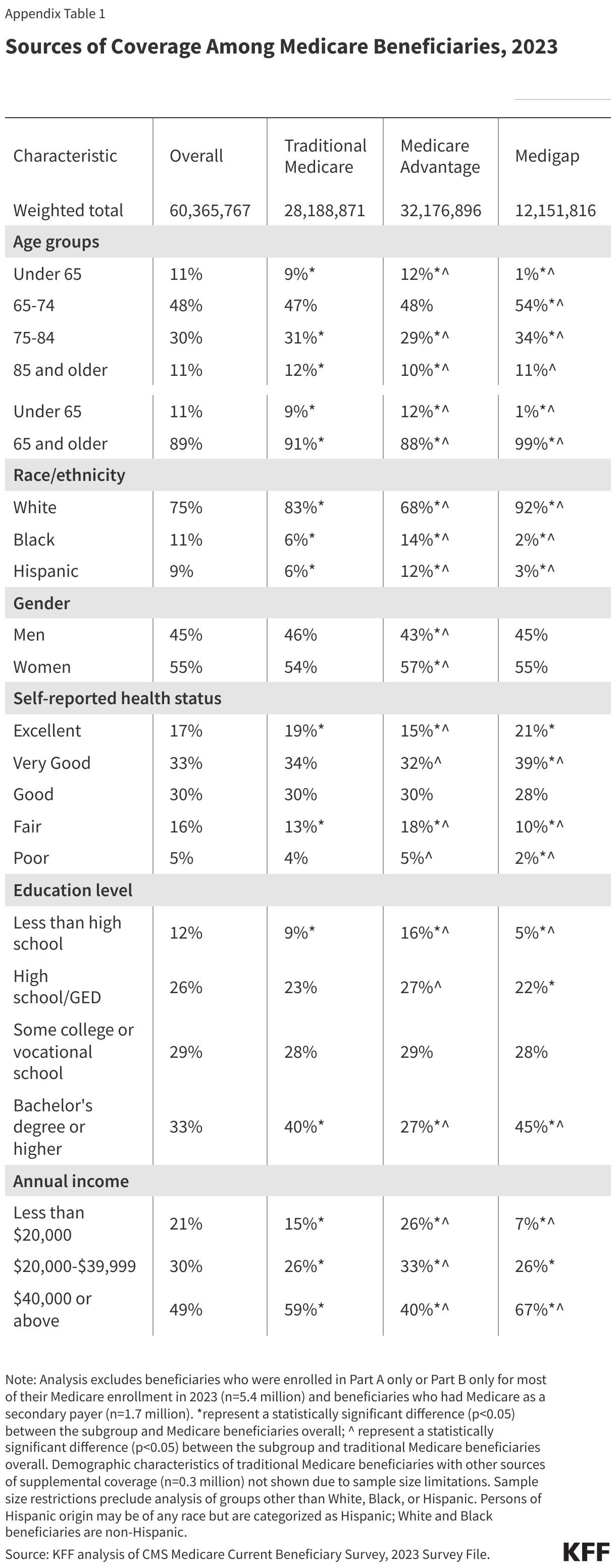

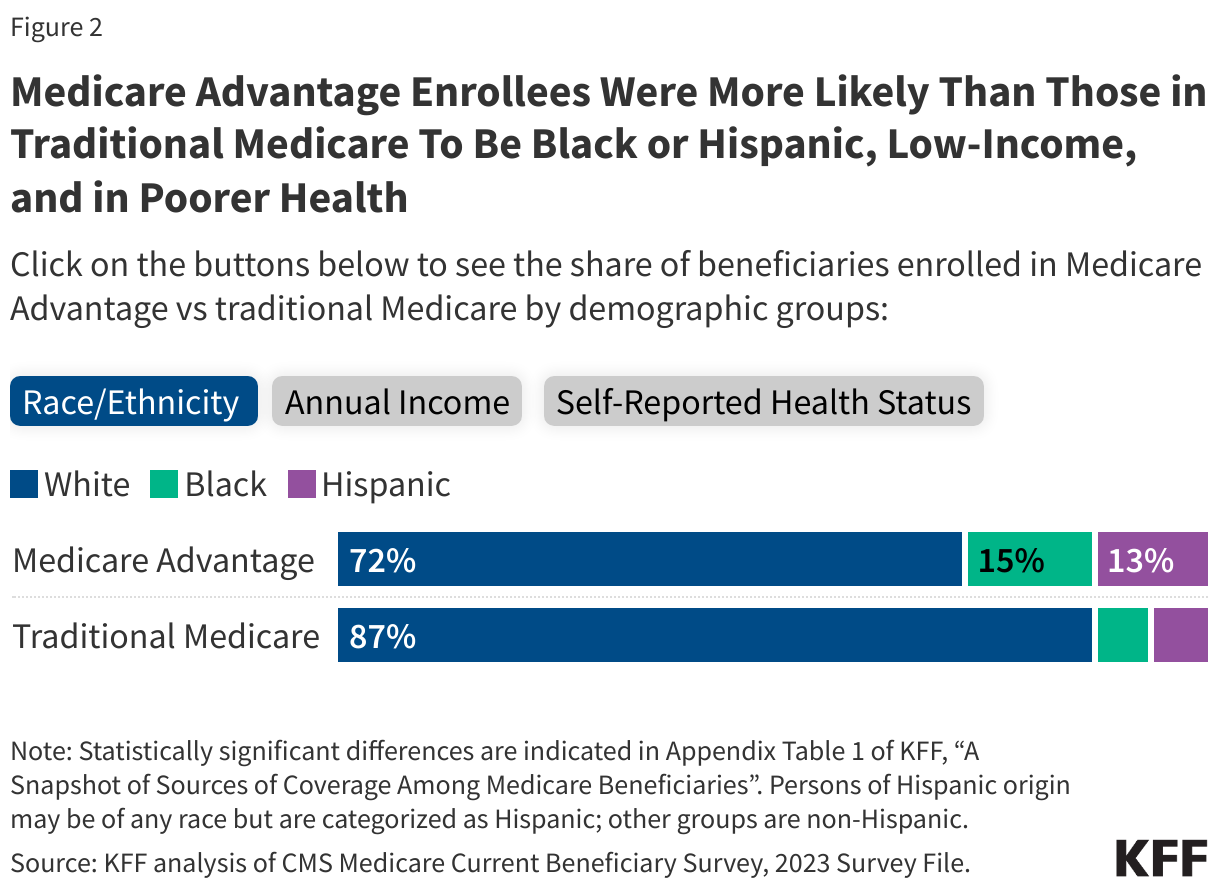

- Compared to traditional Medicare beneficiaries, Medicare Advantage enrollees were more likely to be Black or Hispanic, have incomes below $20,000 per person, and self-report fair or poor health.

More than Half of All People with Medicare Are Enrolled in Medicare Advantage

In 2025, Medicare Advantage covered more than half (54%) of Medicare beneficiaries with both Medicare Parts A and B, or 34.1 million out of about 62.8 million people. Of the total number of Medicare Advantage enrollees in 2025, most (62%) are enrolled in individual plans available to all Medicare beneficiaries. One in five (21%) are in Special Needs Plans (SNPs) and 17% are enrolled in employer- or union-sponsored group plans, where employers or unions contract with an insurer and Medicare pays the insurer a fixed amount per enrollee to provide benefits covered by Medicare. (These estimates are based on March 2025 Medicare Advantage plan enrollment data and therefore differ from those discussed below and shown in Figure 1, which are based on the 2023 Medicare Current Beneficiary Survey (MCBS)).

Compared to traditional Medicare beneficiaries, Medicare Advantage enrollees were more likely to be Black or Hispanic, have incomes below $20,000 per person, and self-report fair or poor health, based on KFF analysis of the 2023 MCBS (Figure 2, Appendix Table 1).

Most Medicare Beneficiaries in Traditional Medicare Have Additional Coverage that Supplements Medicare Benefits

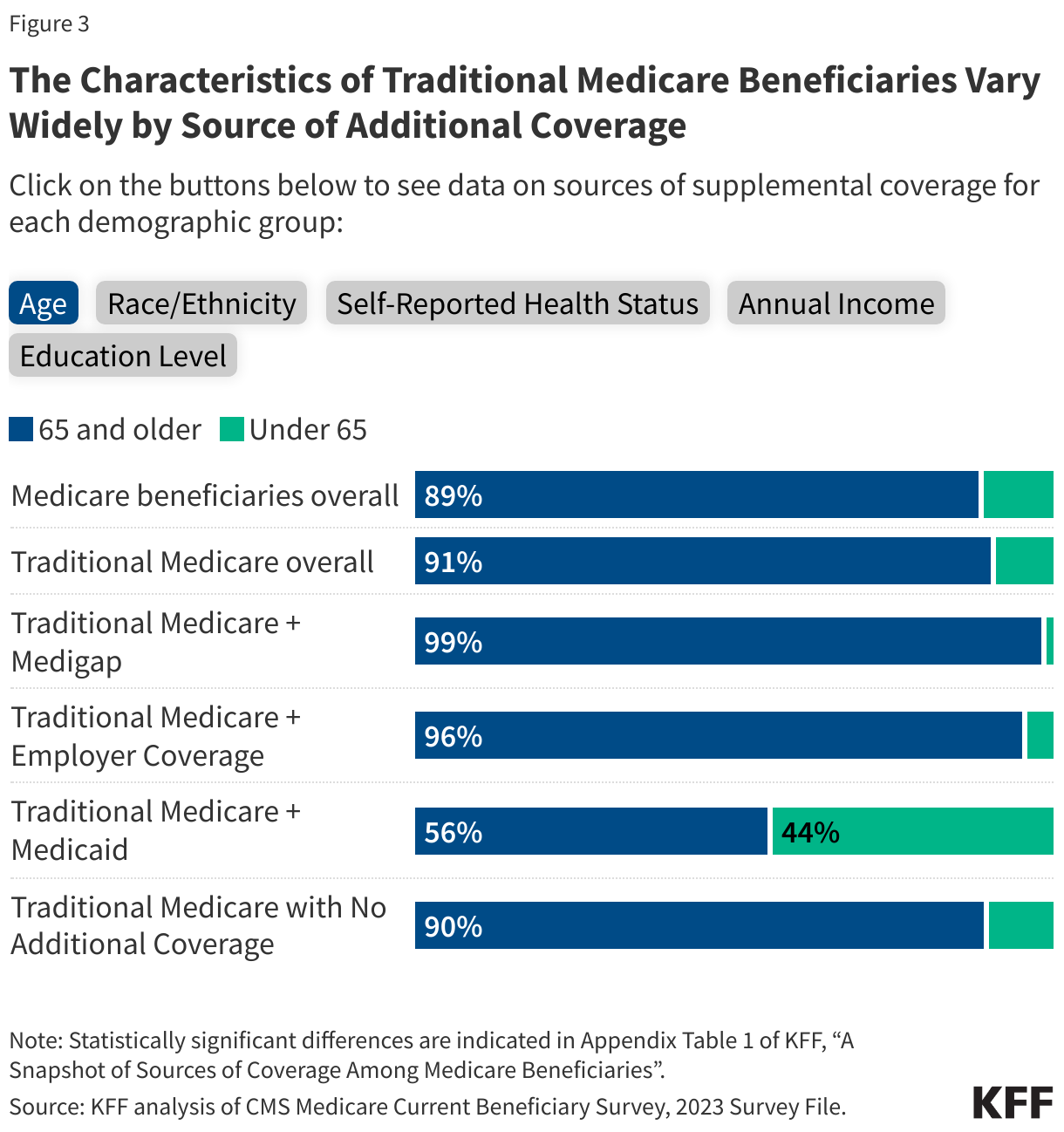

In 2023, most (87%) people in traditional Medicare had some form of additional coverage, either through Medigap (43%), employer coverage (29%), Medicaid (14%), or another source (1%),based on estimates from the MCBS.But 3.5 million Medicare beneficiaries in traditional Medicare (13%) had no additional coverage. A more detailed discussion of these types of coverage and the characteristics of people with each coverage type is below.

Nearly a Quarter of Medicare Beneficiaries Have Employer Coverage, Either through Group Medicare Advantage Plans or in Addition to Traditional Medicare

In total, 14.1 million Medicare beneficiaries – nearly a quarter (23%) of Medicare beneficiaries overall – had some form of employer or union-sponsored health insurance coverage in 2023 in addition to Medicare Part A and Part B. Of this total, 8.2 million beneficiaries had employer coverage in addition to traditional Medicare (29% of beneficiaries in traditional Medicare), while 5.9 million beneficiaries were enrolled in Medicare Advantage employer group plans. Most people with both Medicare Part A and Part B and employer- or union-sponsored coverage are retirees with Medicare as their primary source of health insurance coverage.

Compared to traditional Medicare beneficiaries overall in 2023, beneficiaries with employer or union-sponsored coverage in addition to traditional Medicare were more likely to have higher incomes ($40,000 or greater per person), a bachelor’s degree or higher, self-report excellent or good health, and were less likely to be under age 65 (Figure 3, Appendix Table 1).

Separately, in 2023, an estimated 5.8 million Medicare beneficiaries had Part A only, a group that primarily includes people who were active workers (either themselves or their spouses) and had primary coverage from an employer plan and Medicare as a secondary payer. People with Part A only cannot enroll in a Medicare Advantage plan, so people with coverage through Medicare Advantage employer group plans are likely to be retired.

Four in 10 People in Traditional Medicare Have a Medigap Supplemental Policy

Medicare supplement insurance, also known as Medigap, covered 2 in 10 (20%) Medicare beneficiaries overall, or 43% of those in traditional Medicare (12.2 million beneficiaries) in 2023. Medigap policies, sold by private insurance companies, fully or partially cover Medicare Part A and Part B cost-sharing requirements, including deductibles, copayments, and coinsurance. Medigap limits the financial exposure of Medicare beneficiaries and provides protection against catastrophic medical expenses. However, Medigap premiums can be costly and can rise with age, among other factors, depending on the state in which they are regulated.

Compared to all traditional Medicare beneficiaries in 2023, beneficiaries with Medigap were more likely to be White, have higher annual incomes (above $20,000 per person), self-report excellent, very good, or good health, and have a bachelor’s degree or higher (Figure 3, Appendix Table 1).

In contrast, a smaller share of traditional Medicare beneficiaries under age 65 have a Medigap policy than traditional Medicare beneficiaries ages 65 and older (1% versus 9%). Federal law provides a 6-month guarantee issue protection for adults ages 65 and older when they first enroll in Medicare Part B if they want to purchase a supplemental Medigap policy, but these protections do not extend to adults under the age of 65 with disabilities, and most states do not require insurers to issue Medigap policies to beneficiaries under age 65.

One in Five People with Medicare Also Have Coverage from Medicaid, with More Covered Under Medicare Advantage than Traditional Medicare

Medicaid, the federal-state program that provides health and long-term services and supports coverage to low-income people, was a source of supplemental coverage for 12.2 million Medicare beneficiaries with low incomes and modest assets in 2023, or 20% of all Medicare beneficiaries. A larger number and share of Medicare beneficiaries with Medicaid (known as dual-eligible individuals) were enrolled in a Medicare Advantage plan (8.3 million, or 68% of all dual-eligible individuals) than in traditional Medicare (4.0 million, or 32%) (Appendix Table 1). For these beneficiaries, Medicaid typically pays the Medicare Part B premium and may also pay a portion of Medicare deductibles and other cost-sharing requirements. Most dual-eligible individuals are also eligible for full Medicaid benefits, including long-term services and supports.

Compared to traditional Medicare beneficiaries overall in 2023, dual-eligible individuals were more likely to have low incomes and relatively low education levels, self-report fair or poor health, identify as Black or Hispanic, and be under the age of 65 (Figure 3, Appendix Table 1).

3.5 Million Traditional Medicare Beneficiaries Lack Supplemental Coverage

In 2023, 3.5 million Medicare beneficiaries – 6% overall –and 13% of beneficiaries in traditional Medicare – had no supplemental health insurance coverage. Traditional Medicare beneficiaries with no additional coverage are fully exposed to Medicare’s cost-sharing requirements, which would mean paying a $1,736 deductible for a hospital stay in 2026, daily copayments for extended hospital and skilled nursing facility stays, and a $283 deductible plus 20% coinsurance for physician visits and other outpatient services. (These costs are in addition to the standard Part B premium amount of $203 per month in 2026). Beneficiaries in traditional Medicare without additional coverage also face the risk of high annual out-of-pocket costs because there is no cap on out-of-pocket spending for Part A and B services in traditional Medicare, unlike in Medicare Advantage plans.

Beneficiaries in traditional Medicare without any form of additional coverage were more likely to have modest incomes (between $20,000 and $40,000 per person) compared to all traditional Medicare beneficiaries in 2023 (Figure 3, Appendix Table 1). Medicare beneficiaries with modest incomes have limited ability to afford Medigap premiums and are unlikely to qualify for Medicaid because their income and assets are not low enough to meet eligibility guidelines.

The number and share of traditional Medicare beneficiaries without any form of supplemental coverage has steadily declined in recent years. Between 2018 and 2023, the number of traditional Medicare beneficiaries without supplemental coverage declined from 5.6 million beneficiaries (10% of the total Medicare population, or 17% of those in traditional Medicare) to 3.5 million (6% of the total Medicare population, or 13% of those in traditional Medicare). This decline likely reflects the increase in Medicare Advantage enrollment over time, which has increased from 20 million in 2018 to 34 million in 2025.

Methods

For information on Medicare Advantage enrollment in 2025, this analysis draws on data from the Centers for Medicare & Medicaid Services (CMS) Medicare Advantage Enrollment files for March 2025 (See Methods of KFF, “Medicare Advantage in 2025: Enrollment Update and Key Trends” for more details). For information on sources of supplemental coverage within traditional Medicare and Medicare Advantage, this analysis draws on data from the CMS Medicare Current Beneficiary Survey (MCBS) 2023 Survey file data (the most recent year available), a nationally representative survey of Medicare beneficiaries.

Sources of coverage are determined based on the source of coverage held for the most months of Medicare enrollment in 2023. The analysis includes 60.4 million people with both Part A and B Medicare coverage in 2023 (weighted), including beneficiaries living in the community and in facilities. It excludes beneficiaries who were enrolled in Part A only (typically active workers or their spouses with employer or union sponsored coverage) or Part B only for most of their Medicare enrollment in 2023 (weighted n=5.4 million) and beneficiaries who had Medicare as a secondary payer (weighted n=1.7 million). (Because this analysis reflects coverage held for most months, it shows fewer Medicare beneficiaries with Part A-only or Part B-only coverage than the CMS Medicare enrollment dashboard, which reports 5.8 million with Part A only in 2023). The analysis also focuses only on coverage for Part A and Part B benefits, not Part D. This analysis of the MCBS accounted for the complex sampling design of the survey.

In this brief, the number and share of beneficiaries enrolled with both Medicare and Medicaid coverage (dual-eligible individuals) do not align with other KFF estimates due to differences in data sources and methods used. In other KFF publications, the number of dual-eligible individuals is estimated using a 100% CCW sample and include dual-eligible individuals with at least one month of enrollment in Medicare Part A or Part B, rather than those with coverage for most months of the year. The analysis in this brief is based on the MCBS because this data source provides a wider array of demographic and health status indicators than the CCW.

All reported differences in the text are statistically significant; results from all statistical tests are reported with p<0.05 considered statistically significant. Because estimates reported in the text and figures are rounded to the nearest whole number, some estimates may not sum to overall totals due to rounding.

Appendix