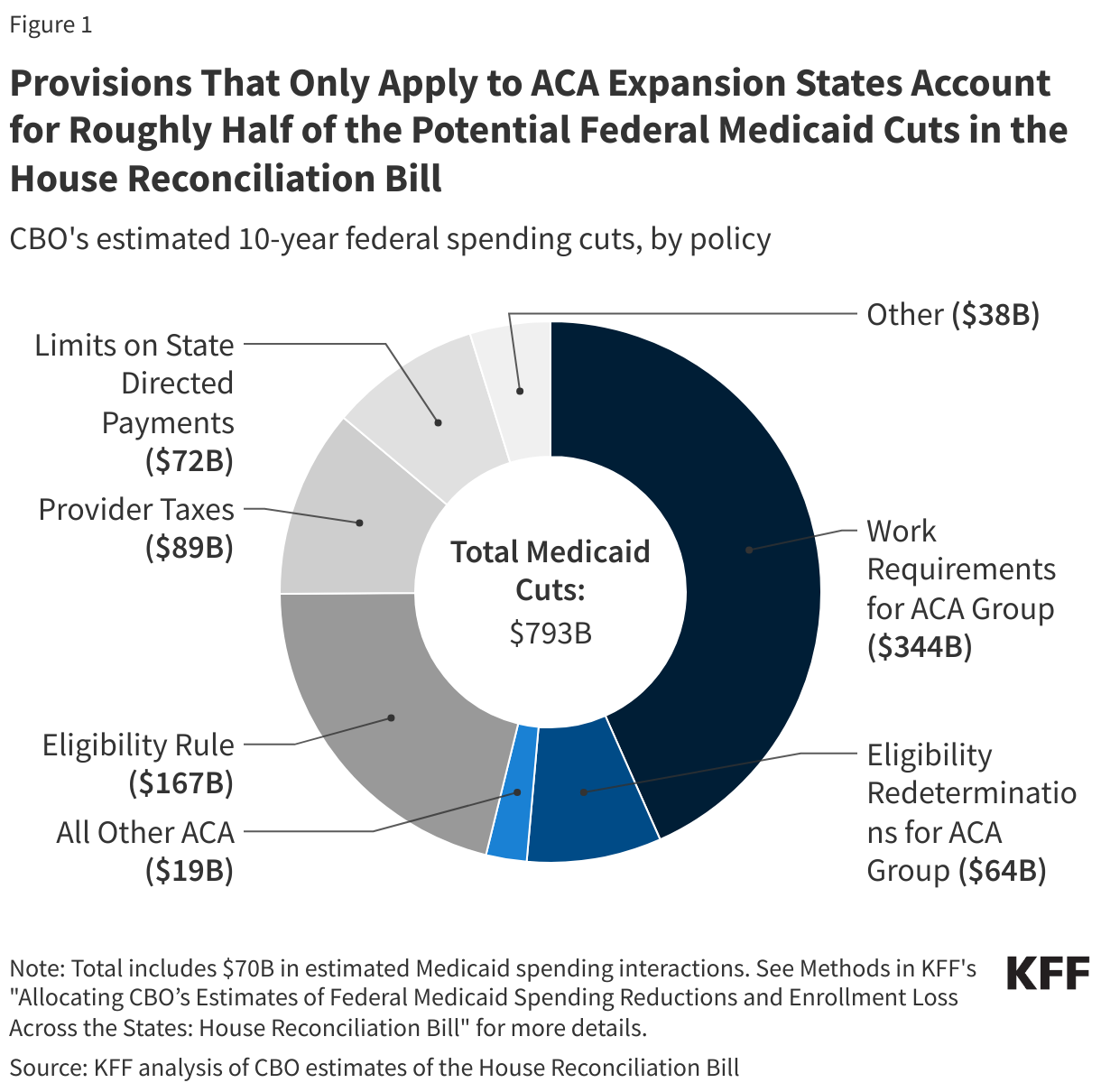

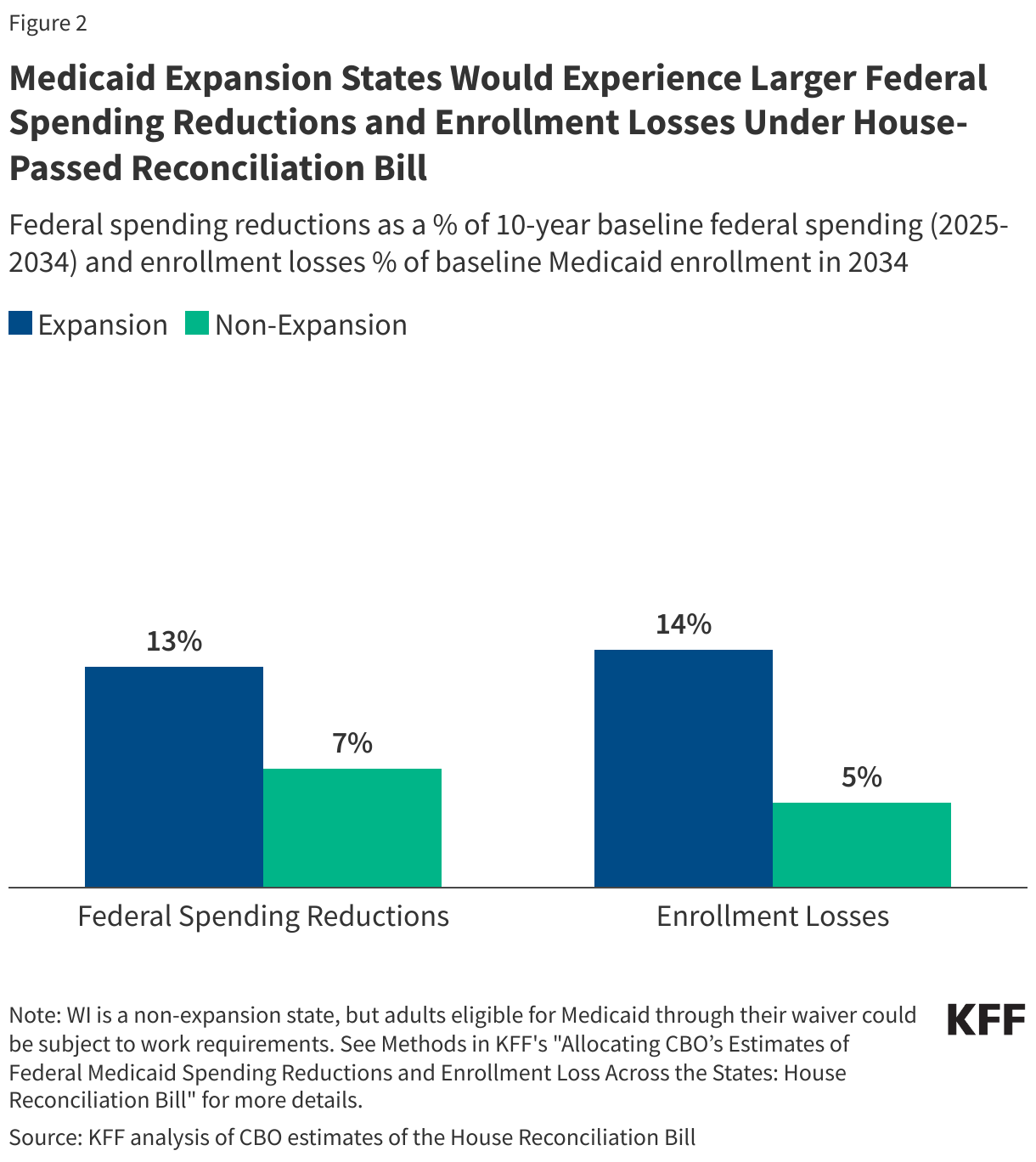

On May 22, the House passed a budget reconciliation bill that includes significant changes to the Medicaid program designed to reduce federal spending and enrollment, and on June 16, the Senate Finance Committee released language that could result in more significant reductions in Medicaid spending and enrollment. The Congressional Budget Office (CBO) estimated that the House bill would reduce federal Medicaid spending by $793 billion and reduce the number of people covered by Medicaid in 2034 by 10.3 million. The two largest sources of spending cuts in CBO’s estimates are establishing work requirements for adults eligible for Medicaid through the Affordable Care Act (ACA) Medicaid expansion (estimated to save $344 billion) and repealing the Biden Administration’s rules simplifying Medicaid enrollment and renewal processes (estimated to save $167 billion). Many of the reductions in coverage will be among Medicaid enrollees ages 50 and older.

The reconciliation bill could also affect access to and quality of care among older Medicaid enrollees because it includes provisions that would limit the ability of states to raise revenues to increase provider payments, limit some supplemental payments for hospitals, and pause implementation of a Biden-era rule on nursing facility staffing (although key elements of that rule were also overturned in court). Beyond the loss of Medicaid coverage, the reduction in federal Medicaid spending could spur states to make additional spending reductions by reducing covered benefits or cutting workforce payment rates that can affect care for adults ages 50 and older. This issue brief examines Medicaid coverage for the 22 million Medicaid enrollees who are ages 50 and older and implications of the provisions in the House reconciliation bill for these enrollees.

1. The 22 million adults ages 50 and older comprise 23% of Medicaid enrollees and 42% of Medicaid spending.

Adults ages 50 and older comprise 23% of Medicaid enrollment and 42% of federal and state Medicaid spending (Figure 1). The higher spending relative to enrollment is consistent with the greater health and functional needs of people as they age. Nearly half of Medicaid enrollees ages 50 and older rely on Medicaid alone for their coverage, while just over half (known as dual-eligible individuals) have Medicare as their primary source of health coverage because they are either age-eligible for Medicare (65+) or qualify due to having a long-term disability (data not shown). For dual-eligible individuals, Medicaid wraps around Medicare, paying Medicare premiums and, in most cases, cost sharing, and often pays for supplemental benefits that are not covered by Medicare, most notably, long-term care.

Even with Medicaid as the secondary payer, Medicaid spending is high for dual-eligible individuals. Dual-eligible individuals ages 50 and older account for 12% of all Medicaid enrollees but 25% of spending. Enrollees ages 50 and older with only Medicaid coverage account for 10% of Medicaid enrollment and 17% of Medicaid spending.

Relatively higher Medicaid spending among dual-eligible individuals reflects their higher rates of long-term care use. Among Medicaid enrollees who use long-term care, 63% are also enrolled in Medicare, compared to only 8% among Medicaid enrollees who don’t use long-term care. On average, Medicaid per person spending for enrollees using long term care was 8-times greater than average Medicaid spending for enrollees who did not use any long term care.

2. Over 90% of older adults with Medicaid enroll through pathways that would be affected by reconciliation provisions making it harder to enroll in and maintain Medicaid.

Among Medicaid enrollees ages 50 and older, 92% are eligible for Medicaid either through the ACA expansion pathway (27%) or through pathways that are specifically for older adults and people with disabilities (65%), both of which are disproportionately affected by the House and Senate versions of the reconciliation bill (Figure 2). In the House-passed reconciliation bill, about half of the federal spending reductions, accounting for $427 billion over 10 years, stem from provisions that only apply to states that have adopted the ACA Medicaid expansion. The biggest reductions in enrollment for expansion enrollees stem from work requirements and a new requirement for states to redetermine eligibility for expansion enrollees at least twice per year. Those changes are likely to reduce Medicaid enrollment among adults ages 50-64.

The second largest source of spending cuts in the reconciliation bill ($167 billion) stem from delaying implementation of two rules that streamline Medicaid enrollment and renewal processes until 2035. The delayed rules were expected to disproportionately increase enrollment among Medicaid enrollees eligible because they were ages 65 and older or because of a disability, who account for 65% of all older Medicaid enrollees. The first rule helps eligible Medicare beneficiaries more easily access Medicaid coverage of Medicare premiums and cost sharing while the second rule streamlines application and enrollment processes in Medicaid, including requiring states to renew eligibility only every 12 months for older adults and people with disabilities. CBO estimates that eliminating those rules would reduce the number of Medicaid enrollees by 2.3 million in 2034, 1.3 million of whom also have Medicare (dual-eligible individuals).

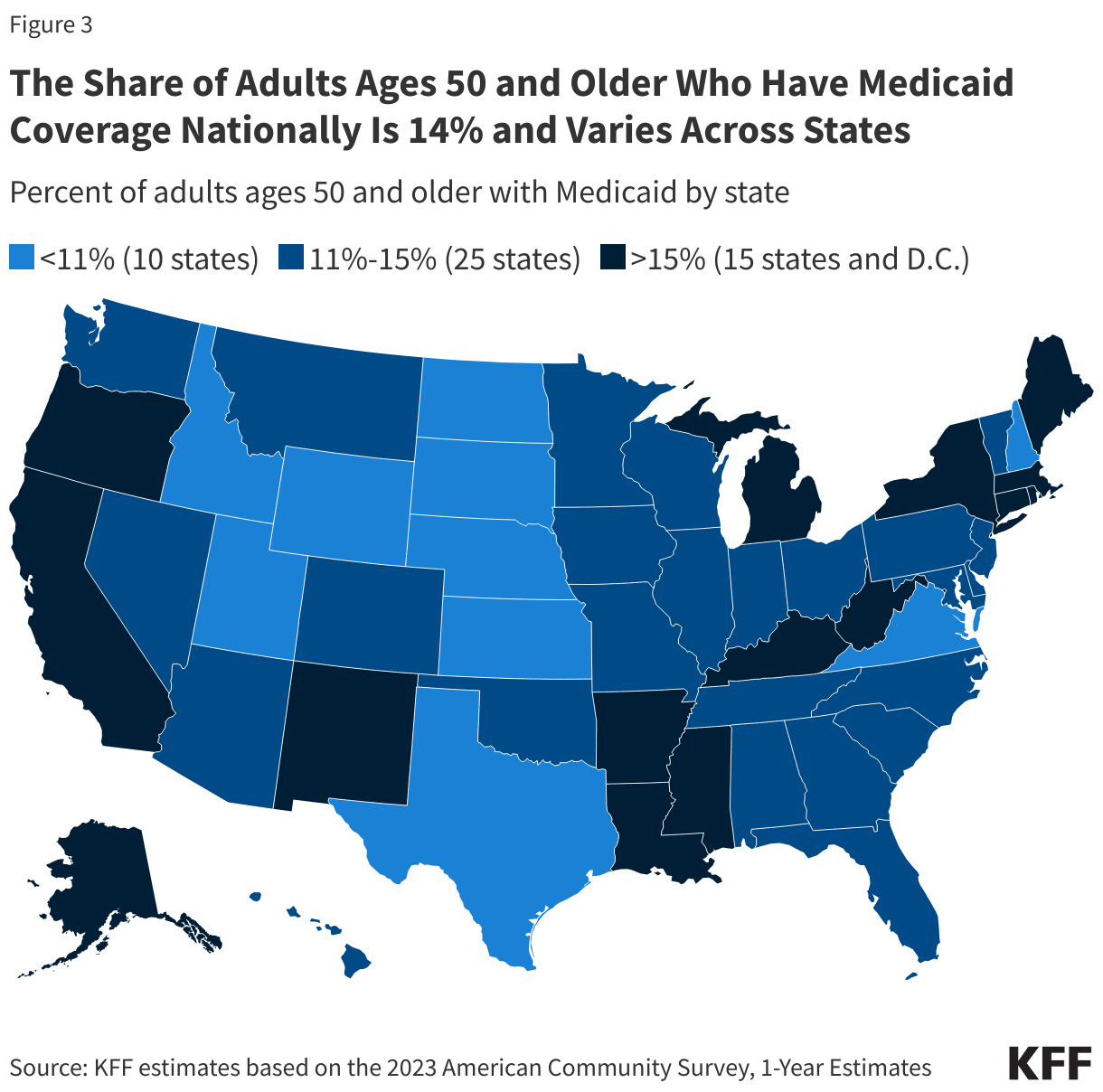

3. The share of adults ages 50 and older who have Medicaid coverage nationally is 14% and varies across states.

Nationally, 14% of adults ages 50 and older have Medicaid, with more than 20% of people 50 and older having Medicaid in four states and the District of Columbia (Louisiana, New Mexico, California and New York, Figure 3). Medicaid enrollees include those for whom Medicaid is their only source of health insurance and those who have Medicaid in addition to another source of coverage, including Medicare. The percentage of adults ages 50 and older covered by Medicaid tends to be higher in the 41 states that expanded Medicaid under the ACA (15%), than in states that did not expand Medicaid under the ACA (12%). Additionally, rates of Medicaid coverage among those ages 50 and older are higher in states with lower average incomes and lower rates of health insurance offered through employers.

4. More than 8 in 10 older adults on Medicaid are working or face barriers to work.

The CBO estimates that Medicaid work requirements in the House reconciliation bill, which would apply to adults ages 19-64, would reduce the number of people with Medicaid by 5.2 million. Medicaid enrollees ages 50 and older typically have lower rates of employment and increased barriers to work compared to all Medicaid enrollees ages 19-64. Among adults ages 50 to 64 with Medicaid who do not receive benefits from the Social Security disability programs, Supplemental Security Income (SSI) and Social Security Disability Insurance (SSDI), and who are not also covered by Medicare, 37% reported working full-time and 15% were working part-time. Others reported not working due to caregiving responsibilities (9%), illness or disability (20%), or school attendance (1%, Figure 4). The remaining 17% of Medicaid adults ages 50-64 reported that they are retired, unable to find work, or are not working for another reason. A 2022 CBO report found that Medicaid work requirements were unlikely to increase employment rates but would be likely to result in loss of Medicaid.

Even though both reconciliation bills provide exemptions for people based on caregiving responsibilities and illness or disability, those people still must comply with reporting requirements, increasing the risk of losing Medicaid. The provisions in the bills apply to individuals in the ACA Medicaid expansion group, so it would not include individuals who have Medicare or SSI; however, many who are enrolled in the expansion group may have a disability, despite not receiving SSI or SSDI benefits. In Arkansas, which implemented work requirements from June 2018-March 2019, about 70% of the population that had to actively report work hours lost coverage primarily due to failure to regularly report work status or document eligibility for an exemption.

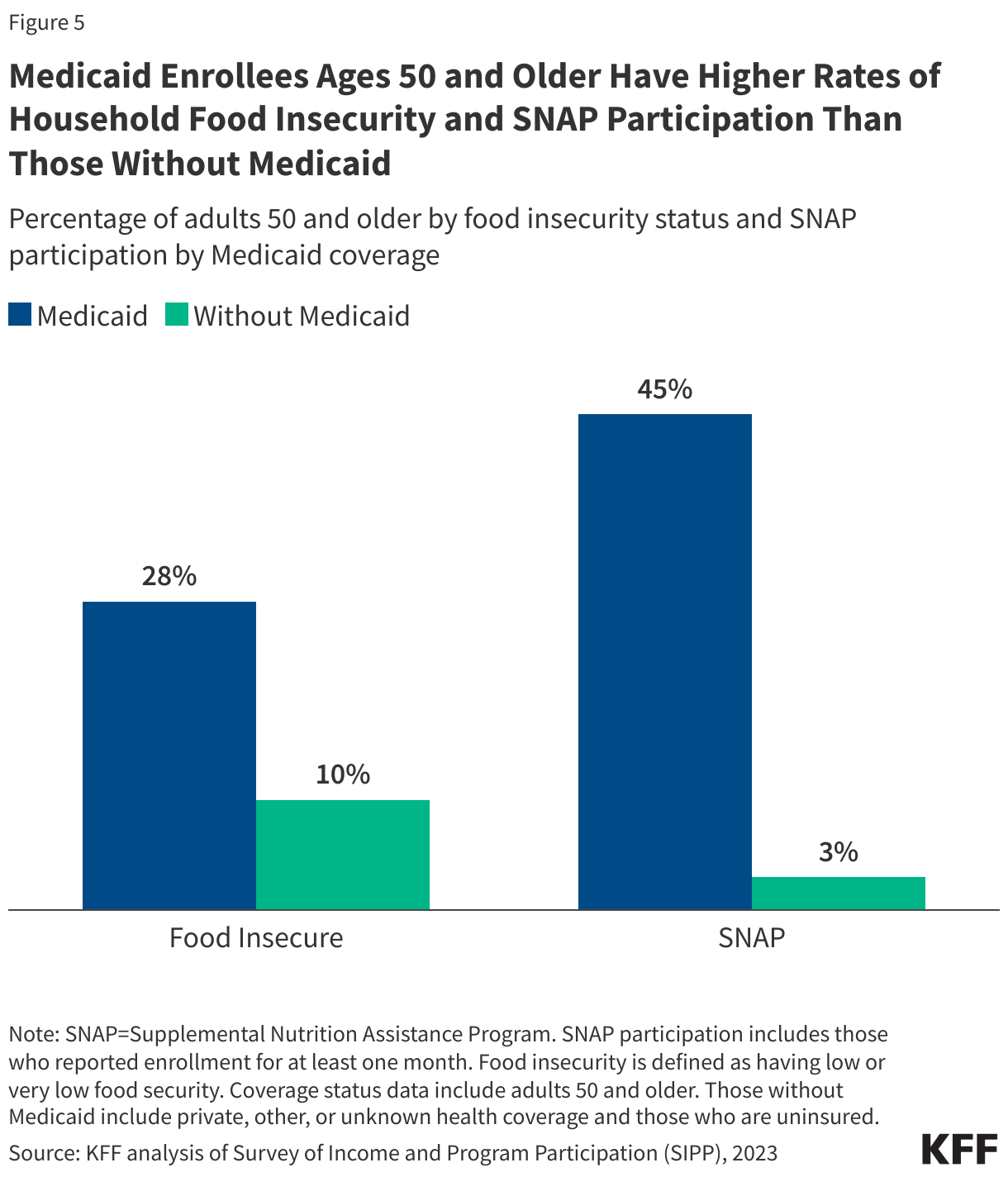

5. Provisions in the House and Senate reconciliation bills could result in loss of coverage and SNAP benefits for Medicaid enrollees ages 50 and older who already report higher rates of household food insecurity compared to those without Medicaid.

The House and Senate reconciliation bills would create work requirements for the Supplemental Nutrition Assistance Program (SNAP), which could exacerbate financial challenges for older Medicaid enrollees. Medicaid enrollees ages 50 and older are over two and a half times more likely to experience household food insecurity than those not enrolled in Medicaid. Among Medicaid enrolled adults ages 50 and older, 28% live in households with food insecurity compared to 10% of those not enrolled in Medicaid (Figure 5). Among Medicaid enrollees 50 or older, nearly half (45%) were enrolled in SNAP for at least one month compared to 3% of their counterparts who were not enrolled in Medicaid. This pattern primarily reflects the significant overlap in eligibility requirements for Medicaid and SNAP, though this may vary by state and coverage population. Beyond the direct reductions proposed to SNAP, loss of Medicaid coverage may increase barriers to enrolling in SNAP as many states use Medicaid enrollment to determine eligibility for other public benefit programs, including SNAP.

This work was supported in part by The John A. Hartford Foundation and Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.