Assessing PEPFAR’s Economic and Educational Spillover Effects: An Update

This represents an update of an earlier analysis:

Assessing PEPFAR’s Impact: Analysis of Economic and Educational Spillover Effects in PEPFAR Countries

Summary

This analysis updates earlier work that assessed whether PEPFAR, the U.S. global HIV/AIDS program credited with saving 26 million lives, had impacts beyond health (a companion update looks at broader health spillover effects). Specifically, the earlier analysis found that PEPFAR investments were associated with a significant increase in the GDP per capita growth rate and reductions in the shares of girls and boys who were out of school between 2004 and 2018, positive spillover effects that suggest the program has had a greater impact beyond health alone; this was the case even though PEPFAR funding has been relatively flat for more than a decade. The current analysis updates these estimates through 2022 both to capture additional years of data as well as the potential impact of the COVID-19 pandemic, which severely affected the global economy and resulted in widespread school closures. It similarly finds that PEPFAR was associated with continued improvement in these non-health indicators. These findings suggest that more recent changes to the PEPFAR program by the Trump administration, including significantly scaling back funding and services with plans to further do so in the coming years, could not only have negative impacts on the HIV response, but dampen improvements beyond health.

Introduction

PEPFAR, the U.S. global HIV/AIDS program credited with saving 26 million lives, is the largest commitment by any nation to address a single disease. In many countries, PEPFAR funding had accounted for the biggest share of external health investment, often surpassing domestic HIV spending. Numerous studies have documented PEPFAR’s impact on improving HIV outcomes, including reductions in new HIV infections and HIV-related deaths, reversing the epidemic’s impact in sub-Saharan Africa.1 In addition, a growing body of research has also found that PEPFAR investments are associated with improvements in other health areas, such as maternal and child health and outbreak response.2 Research has also examined the relationship between PEPFAR and non-health benefits, such as to the economy and educational sectors. For example, the prior analysis found that PEPFAR was associated with a significant increase in the GDP per capita growth rate and reductions in the shares of girls and boys who were out of school between 2004 and 2018. The reasons for this impact are multifaceted and although PEPFAR is a health program, its investments have led to significant reductions in mortality and greater life expectancy, which are generally associated with economic growth and other benefits. External aid also acts as an economic stimulus in countries.3

The current analysis, done by researchers at KFF and Boston University, updates earlier work to assess whether the spillover effects found between 2004 and 2018 persisted through 2022, to capture additional years of data as well as the potential impact of the COVID-19 pandemic, which severely disrupted the global economy and resulted in widespread school closures. Specifically, the analysis uses a difference-in-difference, quasi-experimental design to analyze the change in the GDP per capita growth rate and the shares of girls and boys of primary school age who were out of school in PEPFAR countries and a comparison group of low- and middle-income countries between 2004 and 2022. Several model specifications were tested. The final model specification controls for numerous baseline variables that could also be expected to influence these outcomes, which helps to make the non-PEPFAR group more comparable to the PEPFAR group. Still, despite the strengths of the difference-in-difference model design, it is possible that there may be other, unobservable ways in which comparison countries differed from PEPFAR countries, which could account for the results (see Methodology for more details).

Findings

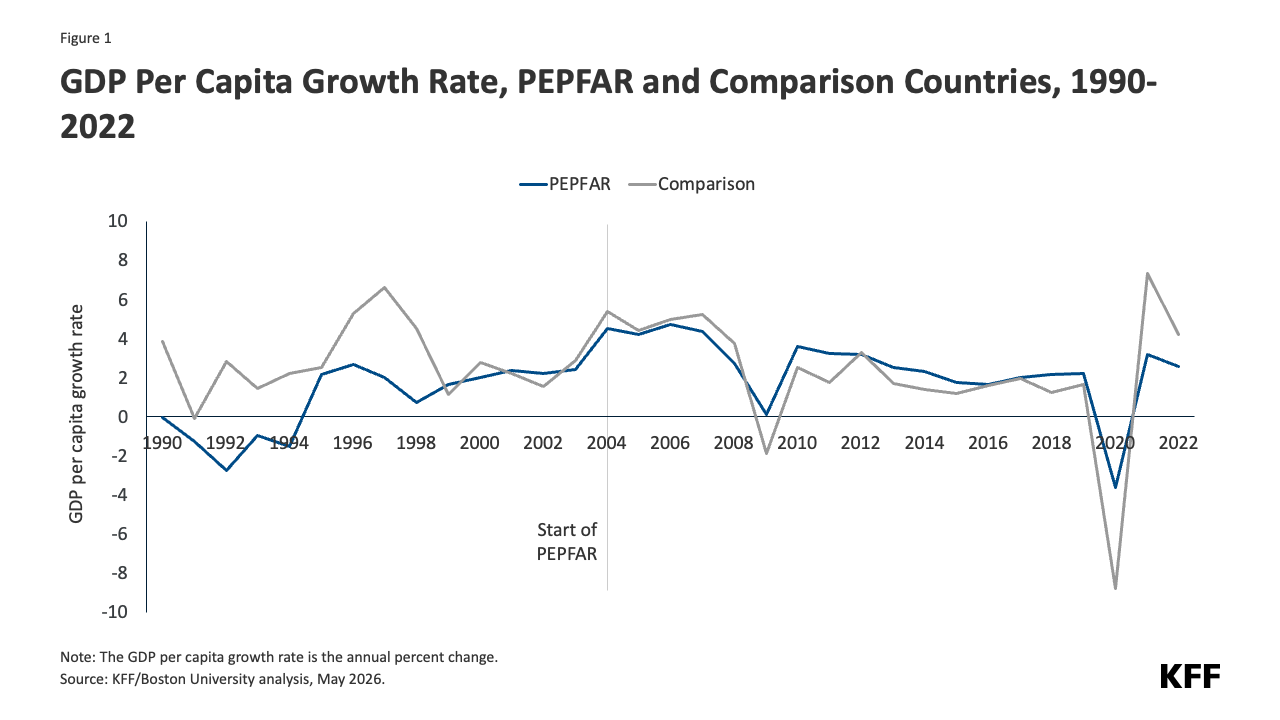

PEPFAR was associated with a significantly higher GDP per capita growth rate during the 2004 to 2022 period.

- Prior to PEPFAR’s initiation, the GDP per capita growth rate was generally higher in comparison countries than PEPFAR countries, although there was some volatility in both.4 The rate in PEPFAR countries accelerated particularly after program’s initiation and until the 2008 global financial crisis, when it dropped in both sets of countries; however, this drop was more pronounced in comparison countries, where it was briefly negative. Similarly, during COVID-19, the GDP per capita growth rate was negative in both PEPFAR and comparison countries, but more so in comparison countries. (see Figure 1).

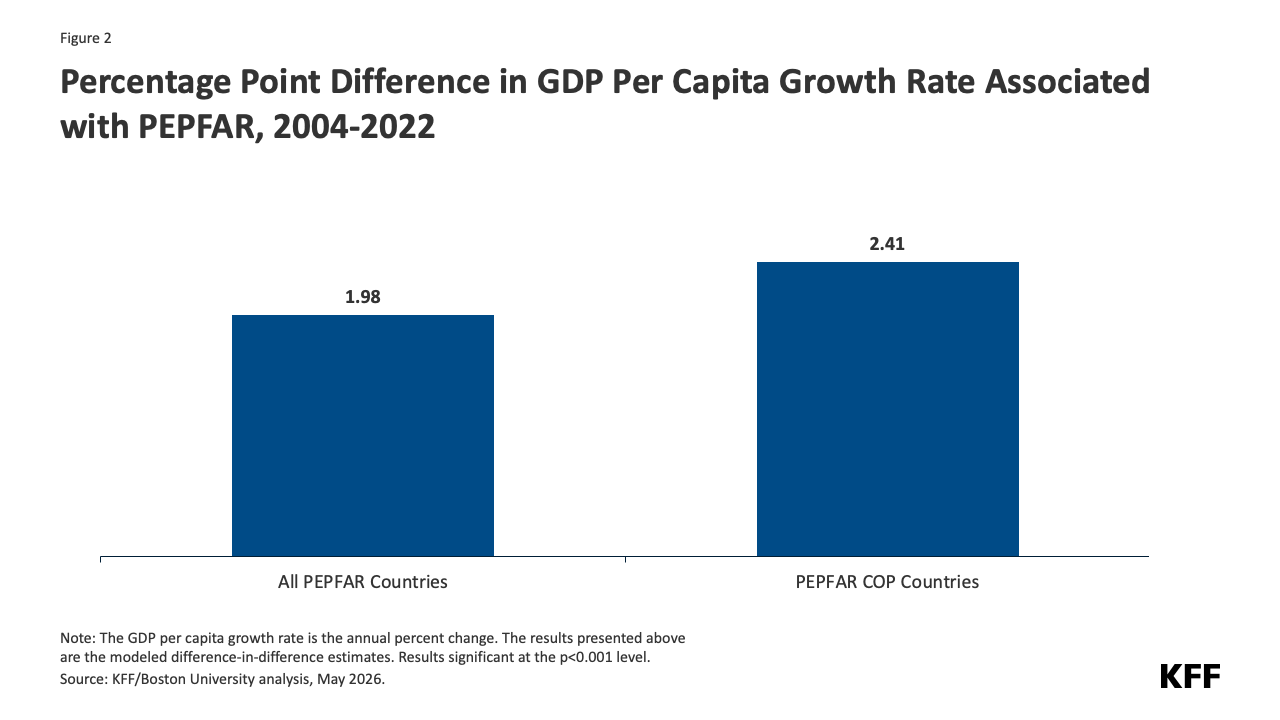

- The difference-in-difference analysis finds that PEPFAR investments were associated with an annual GDP per capita growth rate 1.98 percentage points higher than what would have been expected without the program. While it is possible that the broad economic shocks of 2008 and 2020 affected PEPFAR and comparison countries differently, the model is designed to control for this possibility, supporting the finding that PEPFAR itself was associated with the outcome of interest (see Figure 2 and Tables 5-6).

- These estimated effects were even larger in PEPFAR “COP” countries, those that engaged in more intensive planning and programming.5 In COP countries, PEPFAR was associated with an annual GDP per capita growth rate 2.41 percentage points higher (see Tables 5-6).

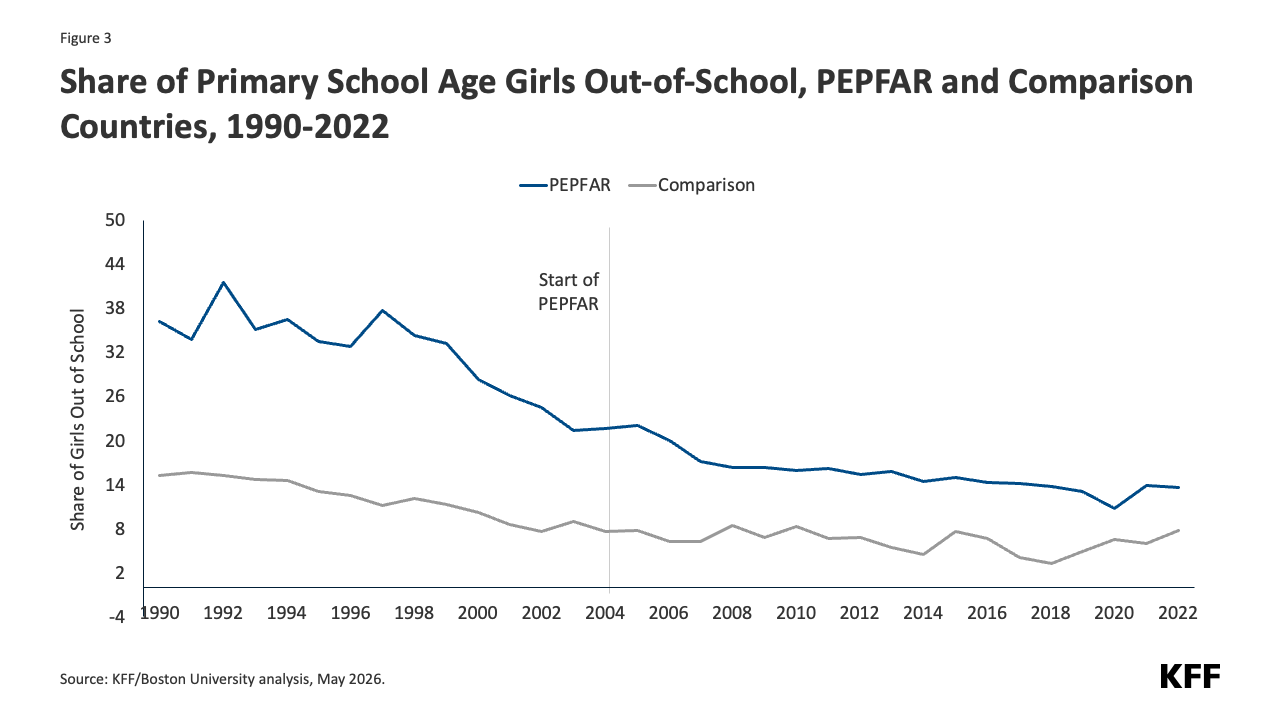

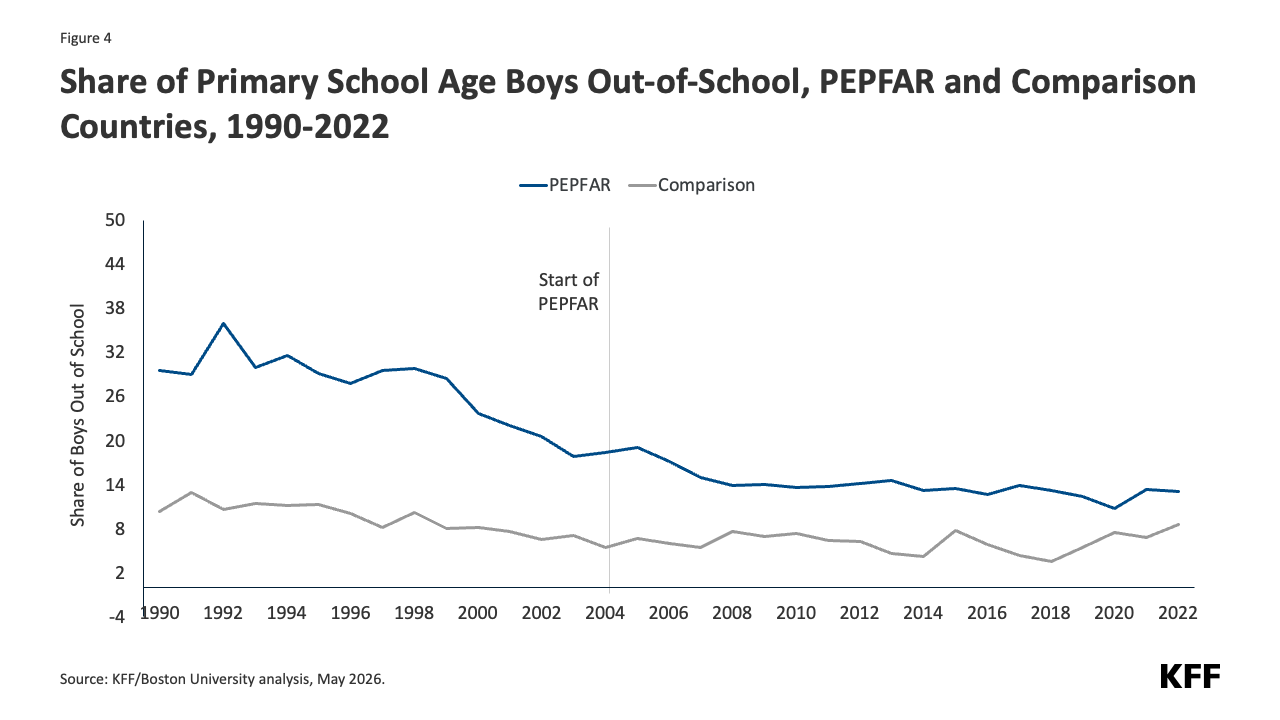

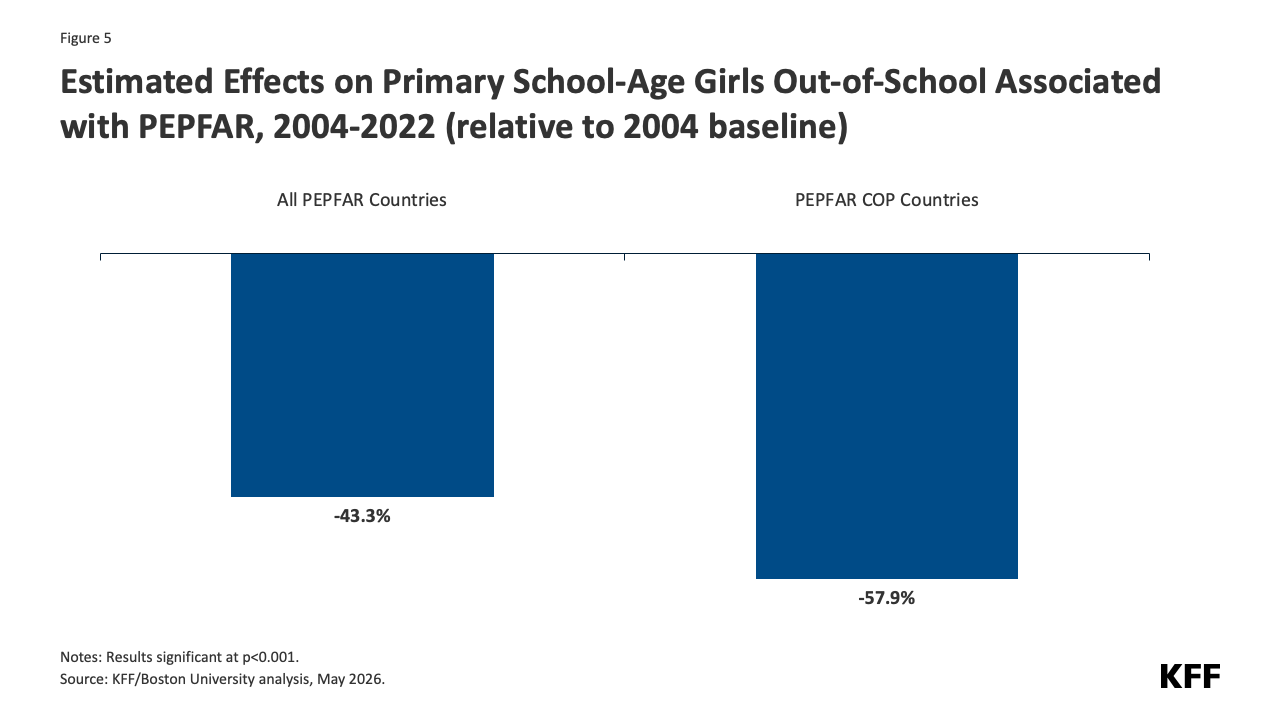

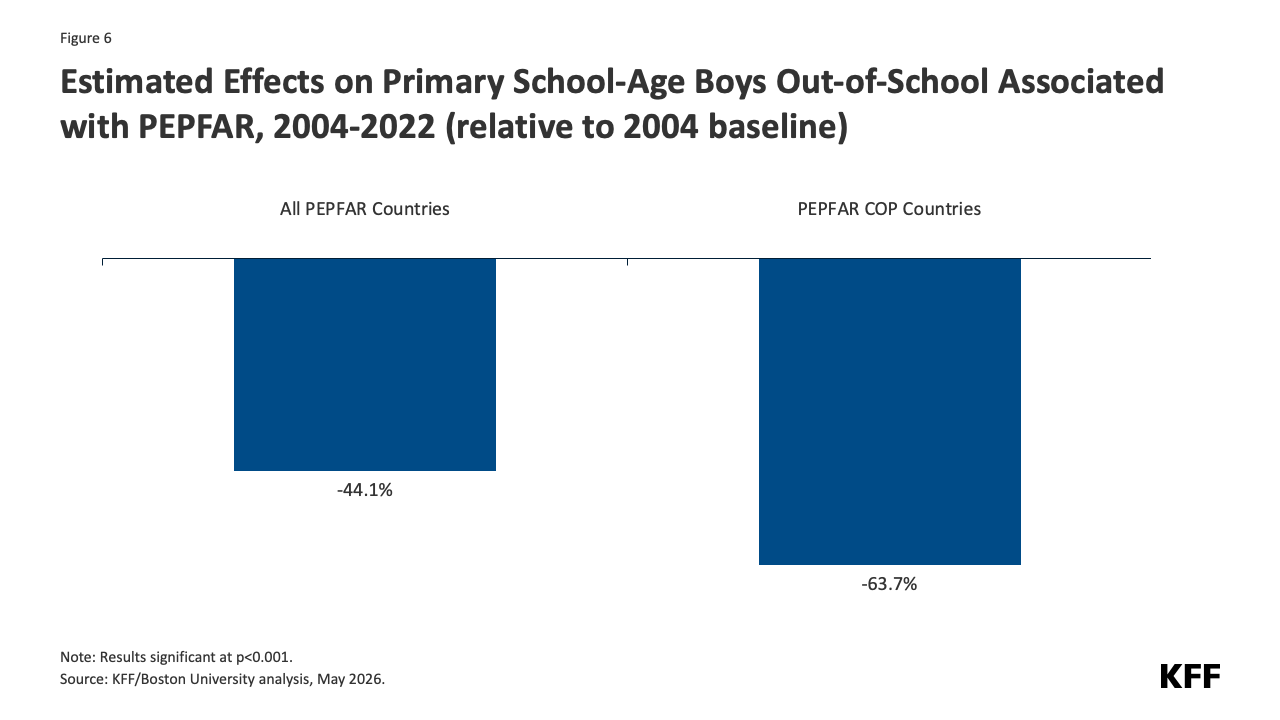

PEPFAR was also associated with significant declines in the shares of girls and boys of primary school age who were out-of-school over the period.

- Before PEPFAR, the shares of girls and boys who were out-of-school were higher in PEPFAR than in comparison countries. While they had begun to drop in PEPFAR countries, the drop accelerated after the introduction of the program, moving closer to comparison countries. There was a slight uptick in both sets of countries during COVID-19, a period marked by widespread school closures. (see Figures 3-4).

- The analysis finds that the share of primary school-age girls who were out of school was 9.37 percentage points lower than would have been expected without PEPFAR (a 43.3% decline relative to the 2004 baseline). The percentage point decline for boys was 8.14 (a 44.1% decline (see Figures 5-6 and Tables 5-6).

- The estimated effects were larger in COP countries (57.9% for girls and 63.7% for boys relative to the baseline) (see Tables 5-6).

Finally, PEPFAR investments were associated with incremental improvements in most outcomes in each successive phase of the program.

- In each successive phase of the program, corresponding to its different authorization periods, PEPFAR investments continued to be associated with improvements in most outcomes; the only exception was the GDP per capita growth rate in the most recent period. The greatest incremental improvements were in the first five years of the program, which also marked a significant influx of new funding; PEPFAR funding plateaued after that which may explain the smaller incremental gains in later years (see Table 7).

Taken together, these findings provide continued evidence of PEPFAR’s knock-on effects beyond health alone. This is supported by numerous other studies that have found that health investments generally are correlated with educational attainment and economic growth, including, for example, by enabling children to stay in school longer and by supporting adults to join and/or remain in the labor force.These findings also suggestthat more recent changes made to the PEPFAR program by the Trump administration, including significantly scaling back funding and services with plans to further do so in the coming years, could not only have negative impacts on the HIV response, they could also dampen economic and educational gains beyond health.

Jen Kates is with KFF. William Crown, Deborah Stenoien, and Allyala Nandakumar are with Boston University.

Methods & Tables

A difference-in-difference, quasi-experimental design was used to estimate a “treatment effect” (PEPFAR), based on comparison to a control group (the counterfactual). The difference-in-difference design compares the before and after change in outcomes for the treatment group to the before and after change in outcomes for the comparison group. The outcomes of interest, their definitions and sources are listed in Table 1. Baseline variables are listed in Table 2. The panel data set of 157 low- and middle- income countries used in the prior analysis, covering 1990 to 2018, was updated to include data through 2022. COVID-related funding was not included. All values were adjusted to constant 2022 dollars.

The PEPFAR group included 90 countries that had received PEPFAR support over the period. The comparison group included 67 low- and middle- income countries that had not received any PEPFAR support or had received minimal PEPFAR support (<$1M over the period or <$.05 per capita) between 2004 and 2022. Data on PEPFAR spending by country were obtained from the U.S. government’s https://foreignassistance.gov/ database and represent U.S. fiscal year disbursements. Data for other indicators were obtained from the World Bank’s World Development Indicator database (WDI) (https://datatopics.worldbank.org/world-development-indicators/, unless otherwise noted. Several different model specifications were explored. Each specification controlled for numerous baseline variables, compared to an unadjusted model, variables which may be expected to influence the outcomes of interest and which help make the comparison group more comparable to the PEPFAR group.

Table 3 provides the model specifications used in the updated analysis. Each model specification produced similar, statistically significant results. All models were also run with and without China and India, the two most populous countries in the world, to assess whether they were influencing the results. In both cases, PEPFAR’s impact was still significant and results were similar. The final reported results are from model specification 3. The pre-intervention period for this model started in 2002. All results were significant at the p<0.001 level. Table 4 provides the mean values for baseline outcomes and Tables 5-6 provide model results. The Table 5 difference-in-difference estimates should be interpreted as the unit change (e.g., percentage point change in the GDP per capita growth rate) in the outcome associated with PEPFAR. The Table 6 estimates should be interpreted as the percent change in the outcome, relative to the baseline, associated with PEPFAR.

Despite the strengths of the difference-in-difference design, there are limitations to this approach. While the models adjusted for numerous baseline factors that could be correlated with the outcomes of interest, there may be other, unobservable factors not captured. Similarly, while baseline factors are also intended to adjust for selection bias, and make the PEPFAR and comparison groups more similar, there may be other ways in which comparison countries differed from PEPFAR countries (and factors which influenced which countries received PEPFAR support), which could bias the estimates. A recent published research article, based on the earlier 2004-2018 period, tested multiple model specifications and conducted sensitivity analyses. The results were similar across all models, adding to the confidence of the analytic approach used here. At the same time, there were some tests that indicated that the parallel trends assumption was not supported in all cases, warranting further analysis.6 Another recent analysis, under review for publication, conducted additional robustness tests and found consistent results.7

| Table 1: Outcome Variables | |

| Variable | Data Source |

| 1. GDP per capita growth (annual %) | Annual percentage growth rate of GDP per capita based on constant local currency. GDP per capita is gross domestic product divided by midyear population. |

| 2. Children out of school, female (% of female primary school age) | Percentage of female primary-school-age children who are not enrolled in primary or secondary school. |

| 3. Children out of school, male (% of male primary school age) | Percentage of male primary-school-age children who are not enrolled in primary or secondary school. |

| Source: World Bank, WDI, https://datatopics.worldbank.org/world-development-indicators/ | |

| Table 2: Baseline Variables | |

| Variable | Data Source |

| 1. Gross Domestic Product (GDP) per capita (current USD) | World Bank Development Indicators |

| 2. Recipient of U.S. HIV funding prior to 2004 (dummy variable) | https://foreignassistance.gov/ |

| 3. Total population | United Nations, Department of Economic and Social Affairs, Population Division |

| 4. Life expectancy at birth (years) | World Bank Development Indicators |

| 5. Total fertility rate (births per woman) | World Bank Development Indicators |

| 6. Percent urban population (of total population) | World Bank Development Indicators |

| 7. School enrollment, secondary (% gross) | World Bank Development Indicators |

| 8. World Bank country income classification | World Bank |

| 9. HIV prevalence (% of population ages 15-49) | World Bank Development Indicators To address missing values in some cases, additional data were obtained from the Global Burden of Disease Collaborative Network |

| 10. Per capita donor spending on health (non-PEPFAR) (constant $) | OECD Creditor Reporting System database |

| 11. Per capita domestic health spending, government and private, PPP (current $) | World Bank Development Indicators |

| Table 3: Model Specifications |

| 1. Unadjusted model |

| 2. Includes baseline variables 1-9 |

| 3. Includes baseline variables 1-11 |

| Table 4: Baseline Mean Outcome Values, 2004 | ||

| Outcome | All PEPFAR Countries | PEPFAR COP Countries |

| GDP per capita growth rate (% change) | 4.5 | 4.1 |

| Primary School-Age Girls Out of School (%) | 21.7 | 21.3 |

| Primary School-Age Boys Out of School (%) | 18.5 | 19.2 |

| Table 5: Difference-in-Difference Estimates Associated with PEPFAR, 2004-2022 (standard errors in parentheses) | ||

| Outcome | All PEPFAR Countries | P Countries |

| GDP per capita growth rate (% change) | 1.977 | 2.410 |

| (0.449) | (0.653) | |

| Primary School-Age Girls Out of School (%) | -9.374 | -12.31 |

| (1.077) | (1.223) | |

| Primary School-Age Boys Out of School (%) | -8.140 | -12.19 |

| (0.961) | (1.089) | |

| All results significant at p < 0.001 | ||

| Table 6: Estimated Percent Change Associated with PEPFAR, 2004-2022 (Relative to 2004 Baseline) | ||

| Outcome | All PEPFAR Countries | PEPFAR COP Countries |

| GDP per capita growth rate (% change) | 43.5% | 59.2% |

| Primary School-Age Girls Out of School (%) | -43.3% | -57.9% |

| Primary School-Age Boys Out of School (%) | -44.1% | -63.7% |

| All results significant at p < 0.001 | ||

| Table 7: Estimated Incremental Percent Change Associated with PEPFAR by Time Period (Relative to 2004 Baseline) | ||||

| Outcome | 2004-2008 | 2009-2013 | 2014-2018 | 2019-2022 |

| GDP per capita growth rate (% change) | 19.3% | 21.6% | 4.7% | -2.1% |

| Primary School-Age Girls Out of School (%) | -30.9% | -7.0% | -4.5% | -0.9% |

| Primary School-Age Boys Out of School (%) | -30.7% | -8.2% | -4.3% | -1.0% |

Endnotes

- Eran Bendavid E, Bhattacharya J. The President’s Emergency Plan for AIDS Relief in Africa: An Evaluation of Outcomes. Ann Intern Med. 2009;150:688-695. Available at: https://www.acpjournals.org/doi/10.7326/0003-4819-150-10-200905190-00117?url_ver=Z39.88-2003&rfr_id=ori%3Arid%3Acrossref.org&rfr_dat=cr_pub%3Dpubmed&; Bendavid E, Holmes CB, Bhattacharya J, Miller G. HIV Development Assistance and Adult Mortality in Africa. JAMA. 2012;307(19):2060–2067. Available at: https://jamanetwork.com/journals/jama/fullarticle/1157487; IOM (Institute of Medicine). 2013. Evaluation of PEPFAR. Washington, DC: The National Academies Press. Available at: https://www.ncbi.nlm.nih.gov/books/NBK207013/; Wagner Z, Barofsky J, Sood N. PEPFAR Funding Associated With An Increase In Employment Among Males in Ten Sub-Saharan African Countries. Health Aff (Millwood). 2015;34(6):946-953. Available at: https://www.ncbi.nlm.nih.gov/pmc/articles/PMC4782769/; and Daschle T, Frist B. Building Prosperity, Stability, and Security Through Strategic Health Diplomacy: A Study of 15 Years of PEPFAR. Bipartisan Policy Center, Washington DC, 2018. Available at: https://bipartisanpolicy.org/download/?file=/wp-content/uploads/2019/03/Building-Prosperity-Stability-and-Security-Through-Strategic-Health-Diplomacy-A-Study-of-15-Years-of-PEPFAR.pdf; Chun HM, Dirlikov E, Cox MH, et al. Vital Signs: Progress Toward Eliminating HIV as a Global Public Health Threat Through Scale-Up of Antiretroviral Therapy and Health System Strengthening Supported by the U.S. President’s Emergency Plan for AIDS Relief — Worldwide, 2004–2022. MMWR Morb Mortal Wkly Rep 2023;72:317–324. Available at: https://www.cdc.gov/mmwr/volumes/72/wr/mm7212e1.htm?s_cid=mm7212e1_w#suggestedcitation; Gaumer G, Luan Y, Hariharan D, Crown W, Kates J, Jordan M, et al. “Assessing the impact of the president’s emergency plan for AIDS relief on all-cause mortality”. PLOS Glob Public Health 2024; 4(1): e0002467. Available at: https://pmc.ncbi.nlm.nih.gov/articles/PMC10796053/. ↩︎

- “The Future of Investment In PEPFAR: Understanding PEPFAR’s Multiple Economic, Health, And Diplomatic Impacts”, Health Affairs Blog, April 17, 2017. Available at: https://www.healthaffairs.org/content/forefront/future-investment-pepfar-understanding-pepfar-s-multiple-economic-health-and-diplomatic; Crown W, Hariharan D, Kates J, Gaumer G, Jordan M, Hurley C, et al. “Analysis of economic and educational spillover effects in PEPFAR countries.” PLoS ONE 2023; 18(12): e0289909. Available at: https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0289909; ; Gaumer G, Crown WH, Kates J, et al. “Analysis of maternal and child health spillover effects in PEPFAR countries.” BMJ Open 2023;13: e070221. Available at: https://bmjopen.bmj.com/content/13/12/e070221.long. ↩︎

- “The Future of Investment In PEPFAR: Understanding PEPFAR’s Multiple Economic, Health, And Diplomatic Impacts”, Health Affairs Blog, April 17, 2017. Available at: https://www.healthaffairs.org/content/forefront/future-investment-pepfar-understanding-pepfar-s-multiple-economic-health-and-diplomatic; Crown W, Hariharan D, Kates J, Gaumer G, Jordan M, Hurley C, et al. “Analysis of economic and educational spillover effects in PEPFAR countries.” PLoS ONE 2023; 18(12): e0289909. Available at: https://journals.plos.org/plosone/article?id=10.1371/journal.pone.0289909; ; Gaumer G, Crown WH, Kates J, et al. “Analysis of maternal and child health spillover effects in PEPFAR countries.” BMJ Open 2023;13: e070221. Available at: https://bmjopen.bmj.com/content/13/12/e070221.long.

[iii] Vogl T, Education and health in developing economies, Working Papers 1453, Princeton University, Woodrow Wilson School of Public and International Affairs, 2012; Wagner Z, Barofsky J, Sood N, “PEPFAR funding associated with an increase in employment among males in ten sub-Saharan African countries,” Health Affairs, 2015 Jun, 34(6): 946-953. Available at: https://pmc.ncbi.nlm.nih.gov/articles/PMC4782769/; Piabuo S, Tieguhong J, “Health expenditure and economic growth – a review of the literature and an analysis between the economic community for central African states (CEMAC) and selected African countries,” Health Econ Rev, 2017 Dec, 7(23); Bloom D, Kuhn M, Prettner K, Health and economic growth, 2018, IZA DP No. 11939, available at: https://www.iza.org/publications/dp/11939/health-and-economic-growth; Collin M, Weil D, The effect of increasing human capital investment on economic growth and poverty: a simulation exercise, World Bank, WPS8590, 2018, available at: https://openknowledge.worldbank.org/handle/10986/30463. Remes J, Wilson M, Ramdorai A, How investing in health has a significant economic payoff for developing economies, Brookings, July 2020, available at: https://www.brookings.edu/blog/future-development/2020/07/21/how-investing-in-health-has-a-significant-economic-payoff-for-developing-economies/; Bloom D, Khoury A, Kufenko V, Prettner K, “Spurring economic growth through human development: research results and guidance for policymakers,” Population and Development Review, 2021 Jun, 47(2): 377-409; World Bank, Human Capital Project, available at: https://www.worldbank.org/en/publication/human-capital. ↩︎ - This volatility appears to have been influenced by a subset of outlier countries; after removing these countries from the analysis, the results remain significant. ↩︎

- Historically, a subset of countries receiving PEPFAR support had been required to prepare annual Country Operational Plans (COPs) which documented annual funding levels linked to results and served as budget and tracking tools. These were prepared by country teams who worked intensively to develop these plans in concert with headquarters at the State Department. ↩︎

- Crown W, Hariharan D, Kates J, Gaumer G, Jordan M, Hurley C, Luan Y, Nandakumar A. (2023) “Analysis of economic and educational spillover effects in PEPFAR countries”. PLOS ONE 18(12): e0289909. https://doi.org/10.1371/journal.pone.0289909. ↩︎

- Crown W, Stenoien D, Reid MJA, Kumar S, Kates J, Jordan M, Nandakumar A. “The Economic Impact of Lives Saved in PEPFAR Countries”, under review, BMJ Global Health. https://doi.org/10.12688/verixiv.2057.1 ↩︎