The 2025 reconciliation law reduced federal Medicaid spending by an estimated $911 billion from 2025 through 2034, some of which stems from new restrictions on Medicaid state directed payments (SDPs) for hospital and other health care services. While states are generally prohibited from directing how managed care organizations (MCOs) pay for care, states can implement SDPs that require MCOs to increase rates or set minimum rates for specified Medicaid services. In authorizing SDPs, the Centers for Medicare and Medicaid Services (CMS) aimed to help states improve access to care and provider participation. Many states that contract with MCOs use SDPs to make uniform rate increases that function like supplemental payments in fee-for-service (FFS) Medicaid. This issue brief analyzes Medicaid spending by state on SDPs that require prior CMS approval to better understand the use of SDPs before new limits in the reconciliation law take effect. A companion issue brief provides more details about the forthcoming changes.

Using a sample of SDPs estimated to currently be in effect, the analysis includes 305 preprints from 41 states, from SDPs that were publicly available and approved from January 1, 2024 through May 12, 2026. Preprints are application forms which document how states direct Medicaid managed care plans to pay providers using SDPs. Preprints are the only national source of data on SDPs but are limited because there are gaps in data provided by the preprints (see Box 1 and Methods for more details).

KFF’s estimates of spending on SDPs are consistent with CMS’ estimates in the May 2026 proposed rule on SDPs. However, KFF estimates provide state-level data and other information not included in the proposed rule, use the most recently approved preprint for each SDP (instead of providing year-by-year estimates and projections), and include SDPs that were approved between January and May 2026 (which are not included in CMS’ analysis). This analysis finds that:

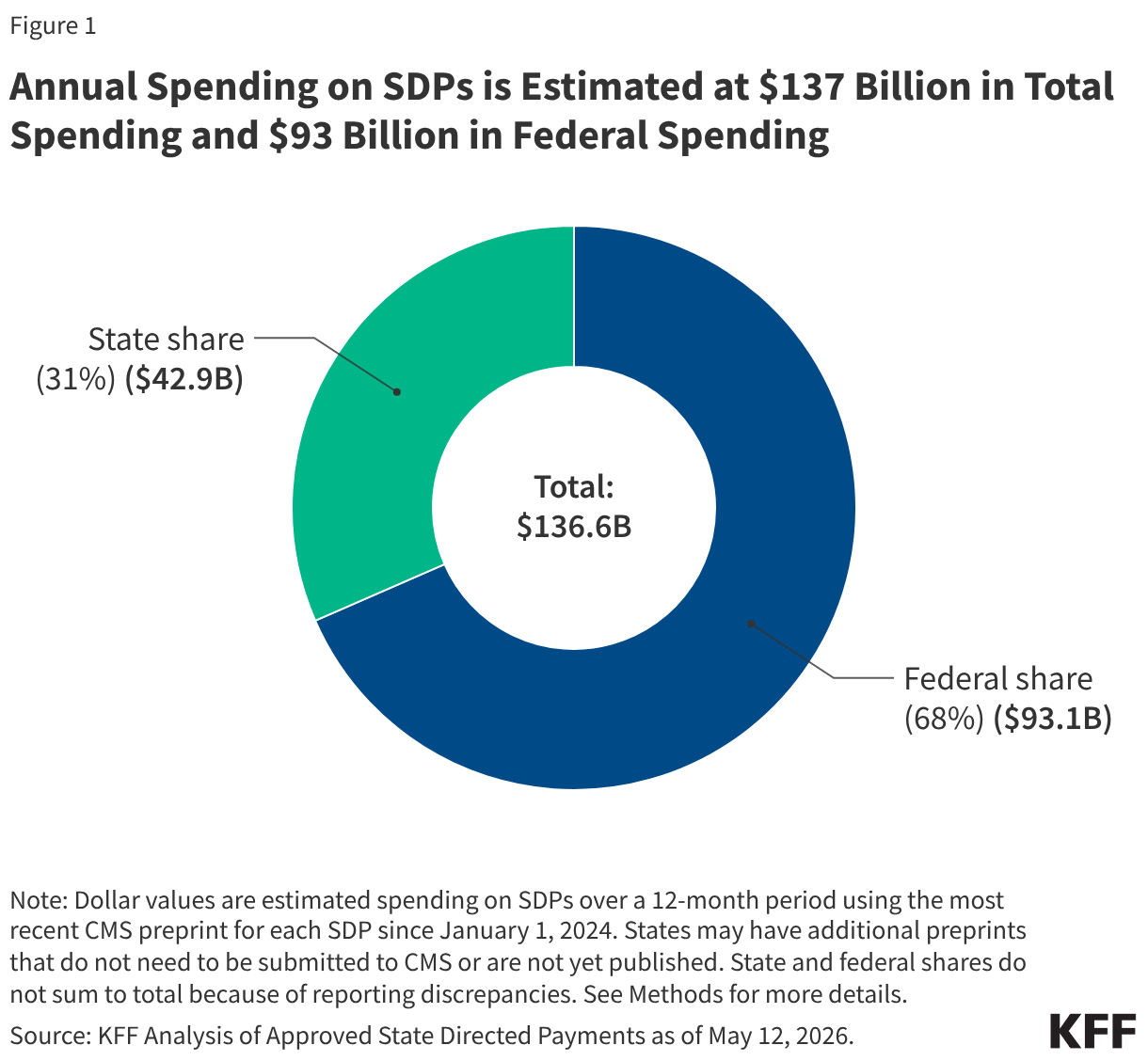

- KFF estimates that annual spending on SDPs is $137 billion in total spending and $93 billion in federal spending.

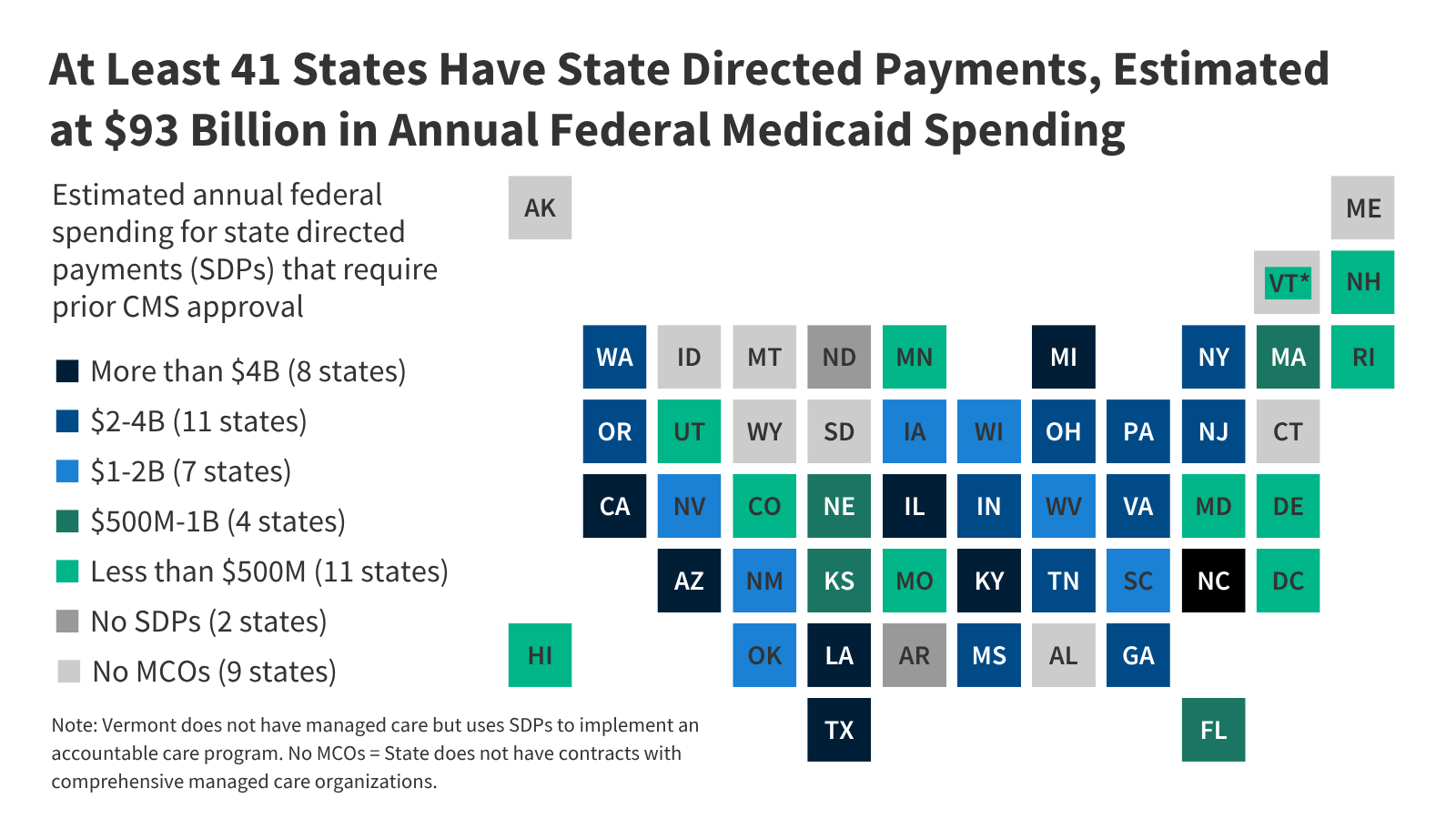

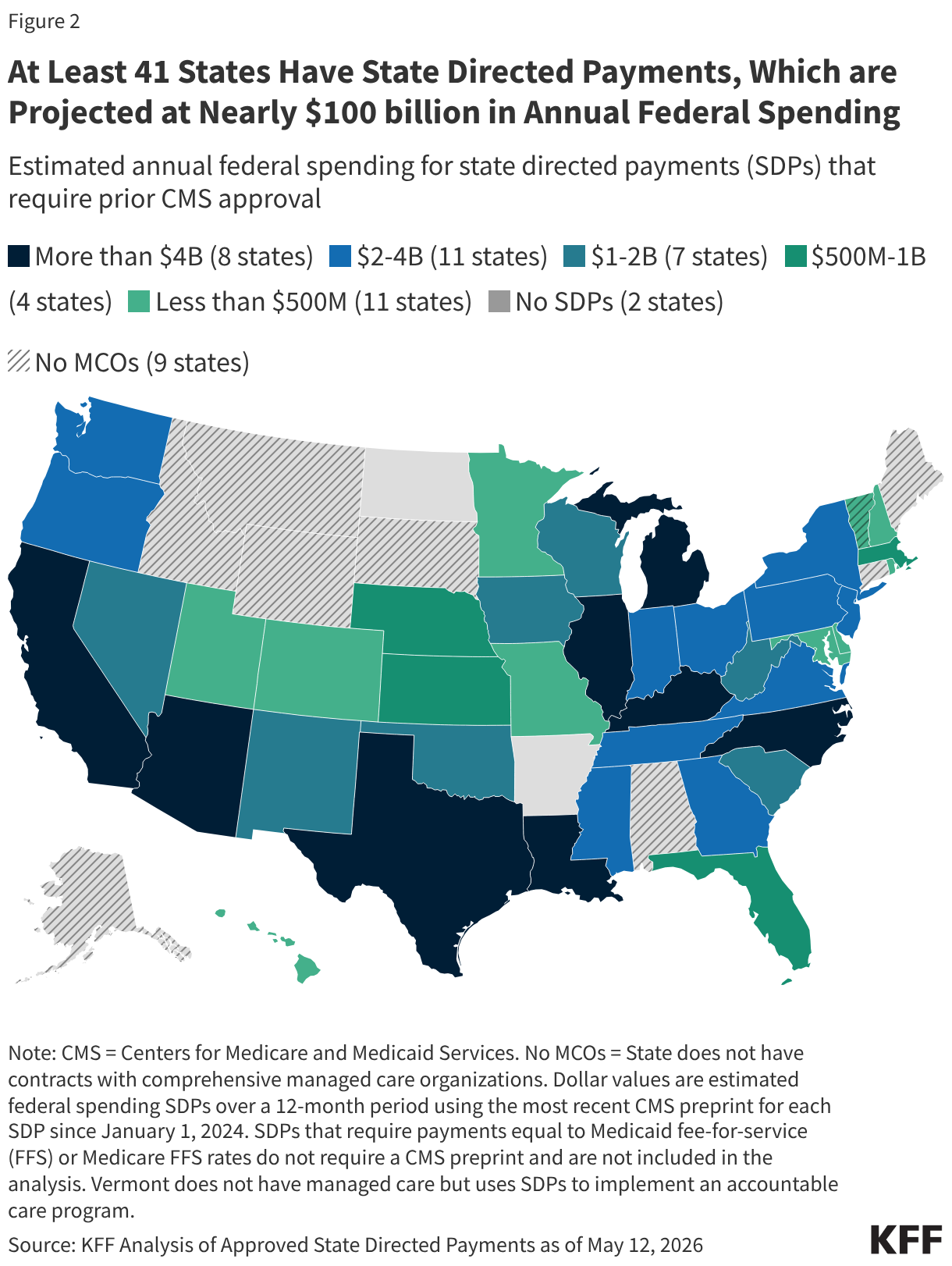

- There are 41 states with SDPs in place (including the District of Columbia, which is hereafter referred to as a state), but the number, structure, and financial impact vary.

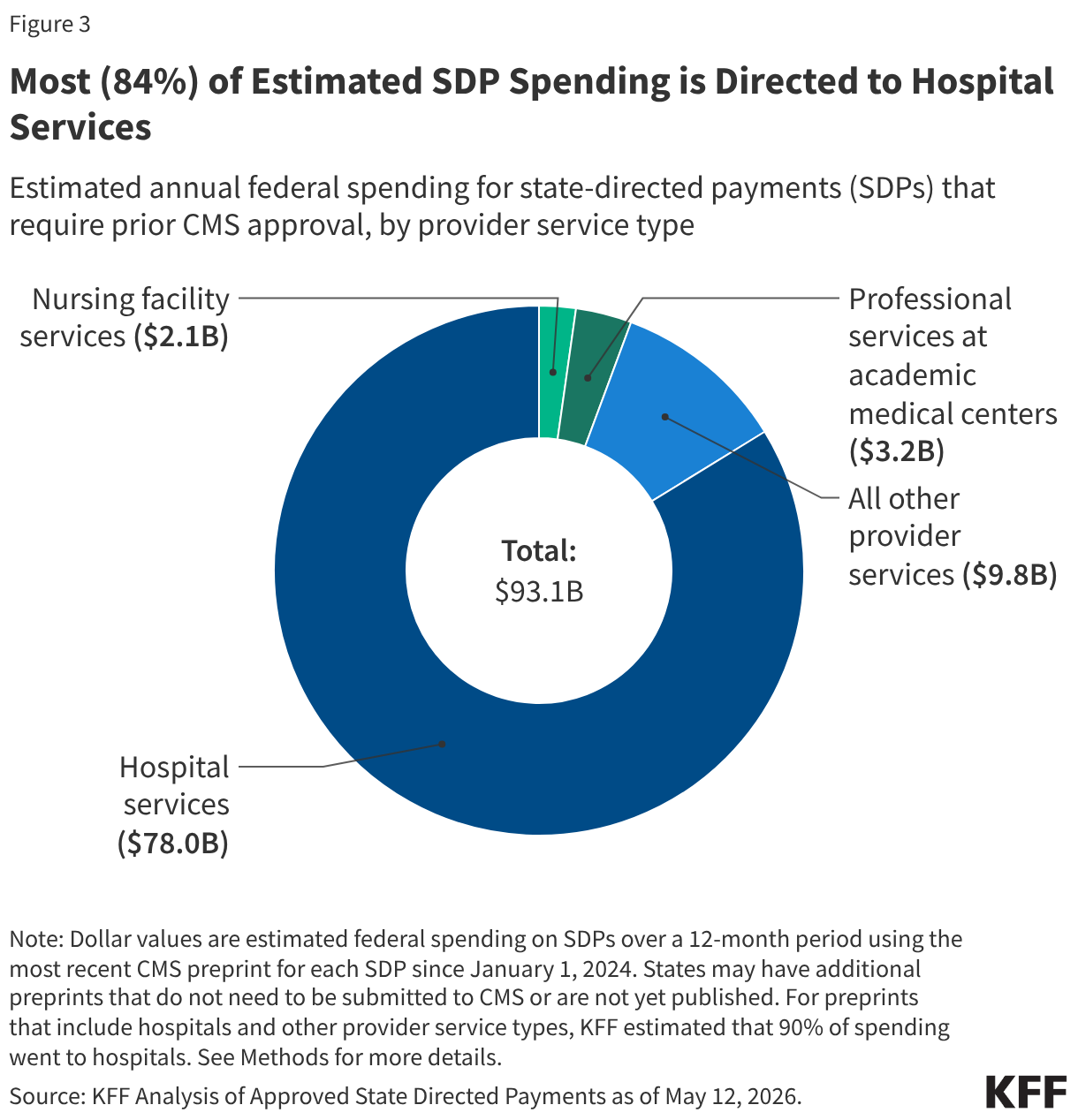

- Most (84%) of estimated SDP spending is for hospital services.

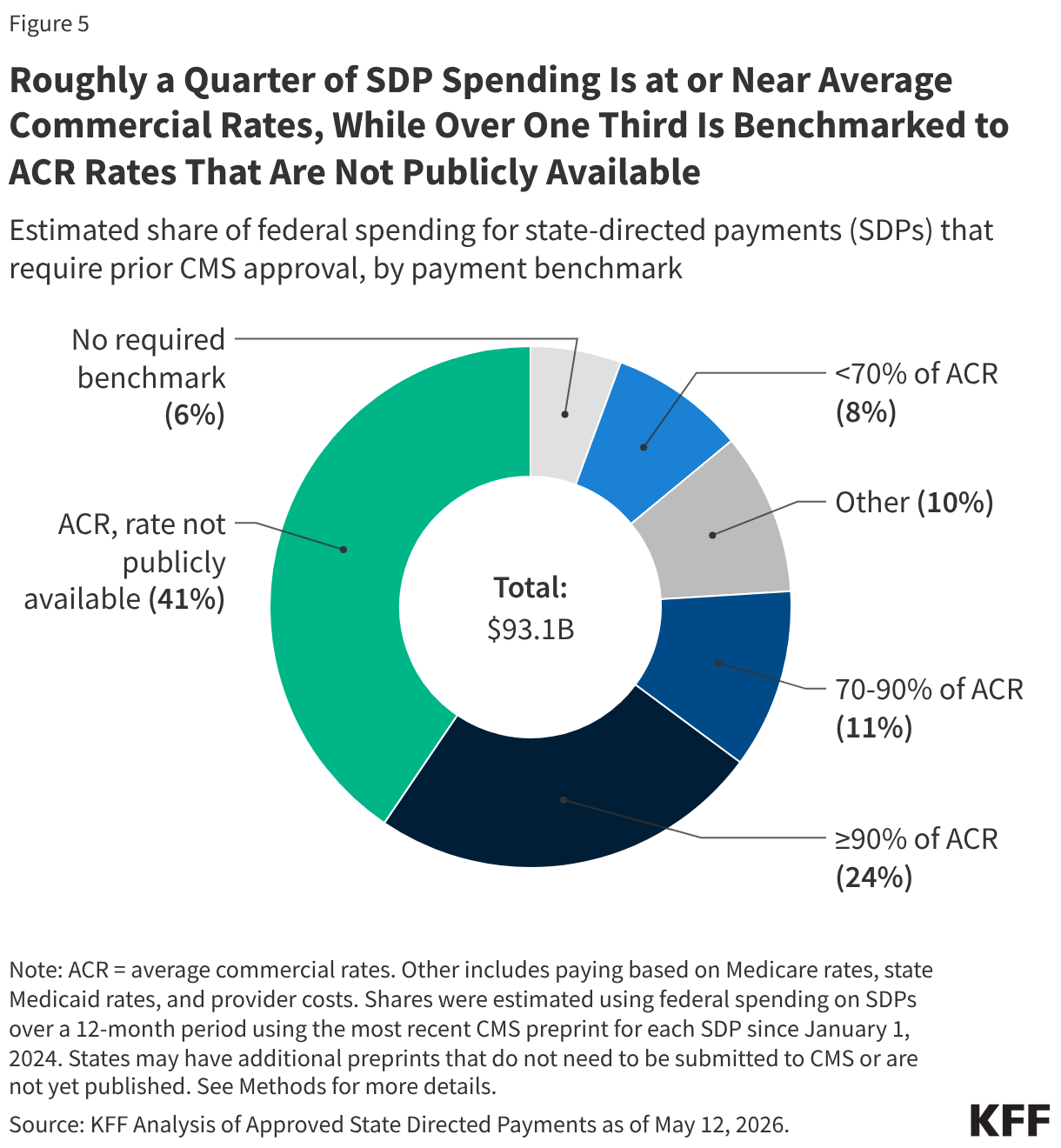

- Most (84%) of estimated SDP spending is from SDPs that use commercial (private) payment rates as a basis for MCO payments, but data on specific payment levels are often not publicly available.

Much remains unknown about how forthcoming policy changes for SDPs will affect states, providers, and Medicaid enrollees, but data about existing SDPs highlights states and services for which changes could be most substantial.

Box 1. Gaps in Data Available to Analyze State Directed Payments (SDPs)

There are major gaps in the data available to analyze state directed payments (SDPs), which come from “preprints” (documents states submit to CMS outlining how SDPs will work and projecting future spending.) Regulations governing SDPs specify which types of payments require prior approval from CMS and which do not, and the information available through the preprints. Missing information stems from the following lack of certain information and exceptions to reporting requirements governing preprints (see Methods for how KFF handled missing information in the estimates).

- When states require MCOs to use the state’s FFS payment rates or Medicare FFS payment rates as a basis for payment, they do not have to obtain prior approval from CMS or submit a preprint file to obtain that approval. (Preprints are required if payment rates use a Medicaid or Medicare benchmark but not the exact FFS payment rates.) It is unknown how many states have SDPs that equal FFS Medicaid or Medicare rates. Since the exemption for Medicare rates was only established in a 2024 rule (see Appendix Figure), some SDPs that use Medicare rates still show up in publicly available preprints.

- Preprints include states’ projected estimates of what they will spend in the future as approved by CMS, but there is no source of information about what states spent. CMS issued guidance in March 2026 specifying that states must start reporting paid amounts in the Transformed Medicaid Statistical Information System (T-MSIS) by September 2026. It is unclear how comprehensive those data will be—most states currently do not report other types of supplemental payments in T-MSIS.

- For preprints that span multiple types of services, states are not required to specify the projected spending by type of service.

- States may provide some information in an addendum to the preprint rather than in the publicly available preprint form, and CMS has not published many preprint addendums, resulting in additional missing information. Some of the information that is most frequently placed in addendums relates to states’ specific payment rates and the details around how the state share of SDP spending is financed. For example, among 139 preprints in this analysis that included payments for hospital services (estimated at $80.3 billion in federal spending), the specific payment rate was missing or incomplete for 38 preprints (estimated at $41.4 billion in federal spending).

How much spending currently flows through SDPs?

Using a sample of preprints estimated to be currently in effect, KFF estimates that Medicaid is spending about $137 billion per year through SDPs. Based on states’ projected spending in the preprints, the federal government pays an estimated 68% ($93 billion) of the total, and the remainder is paid through the state share of SDP financing. The federal and state shares of financing are determined using the standard formulas for Medicaid financing and reflect the state’s federal matching assistance percentage, along with adjustments for some services and eligibility groups for which the federal government pays a higher rate. The state share of financing may come from a variety of sources including state general fund revenues, provider taxes, and intergovernmental transfers.

Financing for SDPs is often complex, and providers may pay for part of the state share of spending through provider taxes and intergovernmental transfers. States may finance the state share of Medicaid spending through provider taxes and intergovernmental transfers (such as transfers from public hospitals), which means those payments are not new revenues for the providers receiving them. In the proposed rule on SDPs, CMS reports that among current SDPs with payment rates above Medicare rates:

- 40% are financed wholly or in part by intergovernmental transfers,

- 27% are financed wholly or in part by provider taxes, and

- 14% are financed wholly or in part by both intergovernmental transfers and provider taxes.

Combined, 81% of those SDPs are financed wholly or in part by intergovernmental transfers and provider taxes. In such cases, it is difficult to determine the amount of new revenues for health care providers. For that reason, KFF’s analysis focuses on changes in federal spending rather than changes in total spending.

How many states have publicly available SDPs?

Nearly all states with comprehensive managed care in Medicaid are estimated to use state directed payments, but the number, structure, and financial impact of these payments vary. Of the 42 states that contract with MCOs, all but two states (Arkansas and North Dakota) have approved SDPs that are estimated to still be in effect. (Arkansas has two approved SDPs for the 2022 rating period, but none have been approved since.)

Vermont does not contract with comprehensive, risk-based MCOs but does have an SDP to implement an accountable care organization program that is transitioning providers to value-based payments through Medicaid. Under the accountable care model, provider groups contract with state Medicaid agencies to assume accountability for the costs and quality of care. The Accountable Care Organization distributes payments to contracted providers in the way comprehensive MCOs pay contracted providers. In essence, the SDP functions similarly but is directing payments through an accountable care organization instead of through an MCO.

The number of SDPs and dollars spent through SDPs varies by state:

- New Jersey and Ohio have the largest number of SDPs (28 and 20 respectively), while two states (Minnesota and West Virginia) and DC have one SDP each (data not shown).

- California has the highest projected federal SDP spending ($10.6 billion), followed by Texas ($6.3 billion), North Carolina ($5.2 billion), and Illinois ($5.1 billion).

Vermont has the lowest projected federal SDP spending ($12.4 million), followed by Maryland ($52.6 million), Missouri ($145 million), and Minnesota ($161 million). Although this analysis focuses on trends in federal spending, patterns are similar when looking at total spending (Appendix Table 1). All 10 states with the highest federal spending also are in the top 10 states for total spending. Many—but not all—of these SDPs could be affected by the new requirements for SDPs in the 2025 reconciliation law.

How are SDPs used across provider types?

An estimated 84% of federal dollars spent through SDPs that require CMS approval pay for hospital services (Figure 3). Of $93 billion in annual projected federal SDP spending, an estimated $78.0 billion (84%) is directed to hospital services. (The share of total spending that pays for hospital services is the same as the share of federal spending.) Professional services at academic medical centers ($3.2 billion) and nursing facility services ($2.1 billion) comprise the next largest shares of federal SDP spending. Although most spending is from SDPs exclusively targeting hospital services, many SDPs include spending for multiple service types and do not specify how much of the total spending is for each service, which creates uncertainty in the estimates (see Methods).

The largest number of SDPs also pay for hospital services, although 64 SDPs are directed to multiple service types, including hospitals. Specifically, of the 305 preprints included in this analysis, 107 were exclusively for hospital services. The next most frequent services were behavioral health services (20 SDPs), professional services at academic medical centers (18), and nursing facility services (17) (data not shown). The remaining preprints were directed exclusively to other services, or to combinations of services.

What types of payment rates do existing SDPs require of MCOs?

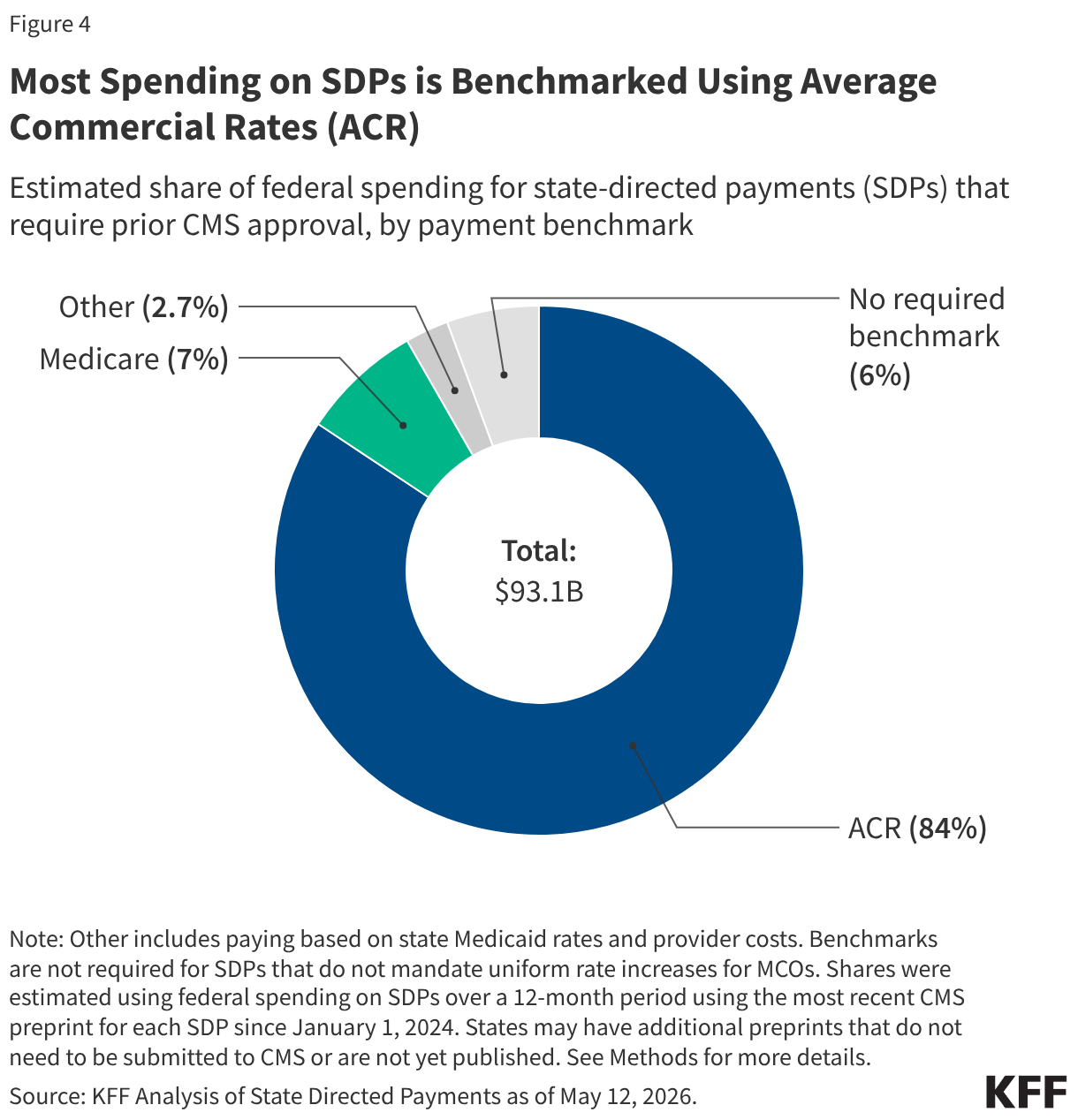

Most spending (84%) comes from SDPs that use average commercial rates as a benchmark, which likely reflects the federal requirements that determine which SDPs require a preprint. The share of spending for SDPs that use average commercial rates is high relative to the share of preprints that use average commercial rates: Nearly two-thirds (65%) of preprints are benchmarked to average commercial rates. The dominance of average commercial rates in the publicly available preprint data likely reflects the fact that when benchmarks equal FFS Medicare or Medicaid rates, no preprint is required. Only a small share of spending is from SDPs that do not require a benchmark.

Roughly a quarter of SDP spending ($23 billion) is paid at or above 90% of average commercial rates, while over one third ($38 billion) is benchmarked to ACR rates that are not publicly available. An additional $10 billion is paid at 70%–90% of average commercial rates. Among the SDPs that do not use ACR as a benchmark, missing payment rates are somewhat less common. Among SDPs that use Medicare rates as a benchmark, just over half result in total payment rates greater than what Medicare pays. (Other SDPs that use Medicare rates as a benchmark may pay at or below Medicare.)

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

Patrick Drake, an independent consultant, contributed to the analysis of SDP data.

KFF appreciates the contributions of external reviewers who provided comments on earlier versions of this analysis.

Methods

Data source: This analysis uses data available from the list of approved state directed payment preprints published by the Centers for Medicare and Medicaid Services (CMS) as of May 12, 2026. The approved state directed payment (SDP) preprints are PDF versions of forms that are completed by states and approved by CMS. States are required to seek approval using such a preprint for any SDP that requires managed care organizations (MCOs) to pay for services at any rate other than fee-for-service (FFS) Medicare or Medicaid rates. The approved preprints are often posted online 6–12 months after their start date, although some approved preprints are posted online much later.

KFF developed a Python script to download the available PDFs, extract relevant data from them, and standardize certain fields. Each preprint was turned into one row in a spreadsheet. Data from tables within the preprint were extracted and converted into separate tables in KFF’s data file with each row in the preprint table converted into a row in the spreadsheet table.

SDP preprint inclusion criteria: KFF included all SDPs in the analysis with a rating period start date of January 1, 2024 onwards for the 50 states and Washington DC (hereafter referred to as a state). Puerto Rico was the only territory that had published SDPs, which were excluded. In each case, KFF only kept the most recent preprint for any given SDP. For example, if an SDP had an initial approval in 2024 and then renewals in 2025 and 2026, KFF would only include the 2026 renewal in the final dataset. Out of the 305 preprints included in this analysis, 24 (totaling $8.8 billion in federal spending) ended in calendar year 2024.

A small number of SDP preprints were excluded due to file formatting or data validity issues. Specifically:

- Data from five preprints excluded from this sample were encoded differently, so the data could not programmatically be extracted into the dataset, and were therefore excluded from the analysis (two from New Hampshire, one from Ohio, and two from Florida, totaling $89 million in federal spending for one year).

- Data from preprints that had obvious data quality issues were excluded from this sample. For instance, two were from Illinois (which projected total annual spending of more than $100 billion) while one from Minnesota did not report spending data in the preprint.

KFF also reviewed all preprints with end dates prior to July 1, 2025, and excluded preprints for the following reasons.

- The preprint was likely funded from COVID-19 relief dollars (including the increased federal funding for home care from the American Rescue Plan Act) and so unlikely to still be in place.

- The preprint was likely combined into a different preprint when renewed or was otherwise renamed when renewed.

- The preprint ended in 2024, and online research suggests that the payment was discontinued.

See Methods Table 1 for a list of the inclusion criteria, the counts of preprints after each criterion was applied, and the federal spending for preprints that were retained at each stage.

Calculating total spending on SDPs: This analysis used the states’ projected total, federal, and state spending from the preprint. Most preprints are for a one-year period but some are for longer or shorter periods. In such cases, KFF adjusted the data to be a one-year equivalent. When preprints were for periods shorter than 12 months, dollars were scaled up (e.g., if the preprint was for 6 months, the spending was multiplied by two) and for preprints that were for periods longer than 12 months, spending was scaled down (e.g., retaining two-thirds of spending if the preprint extended for 18 months).

KFF also manually reviewed the federal spending numbers because some states reported them as percentages and others reported them as dollar amounts. Manual review ensured the Python script had adequately handled the different reporting structures.

In most cases, the state and federal shares equaled the total share, but in 8 states, this was not always the case (see Appendix Table 1).

Calculating SDP spending by service type: For preprints that made payments for multiple service types (which accounted for $32.6 billion in federal spending), spending was apportioned across service types.

- For SDPs directed to hospital and non-hospital services, 90% of spending was allocated to hospital services. Remaining dollars were apportioned equally among any other service types.

- For SDPs directed to both inpatient and outpatient hospital services, 68% of hospital spending was allocated to inpatient services and 32% was allocated to outpatient services. This assumption does not affect the estimates of spending by service type but is relevant for calculating the amount of spending by benchmark rate.

- For SDPs that did not direct any spending to hospital services, spending was allocated equally among named services.

Apportioning spending across service types is difficult and KFF used a variety of sources to approach developing the most realistic assumptions feasible. KFF analyzed data on Medicaid spending including CMS-64 spending by service type, data on Medicaid spending by service type from the National Health Expenditures, the Congressional Budget Office Medicaid baseline, and existing studies on hospital payment policies such as those from the Medicaid and CHIP Payment and Access Commission (MACPAC). All of those data points suggest that the vast majority of SDP spending pays for hospital services, and $53.1 out of the $60.5 billion in federal spending from preprints directed to a single provider type went to hospital services. KFF also strove to use an assumption that resulted in estimates of hospital SDP spending that are similar to what could be expected on the basis of other data and research as described above.

When identifying the service types in the preprints, the Python script attempted to align service types between preprint Table 2 (which specifies payment rates for sets of providers) and preprint question 20 (a checklist of services included in the SDP). In many cases, this alignment involved some uncertainty, requiring manual review and classification of service types.

Identifying benchmarks for MCO payments: The most common type of SDPs requires MCOs to make payments that are on top of the regular base payment rate (as opposed to limiting or replacing the negotiated rate). In such cases, payments are measured using a “benchmark” or standardized rate to compare the MCO rates to other payment rates such as those of Medicaid FFS, Medicare FFS, or the average among commercial payers (“average commercial rates”). Among the 305 preprints in this sample (accounting for $93.1 billion in federal spending), 264 preprints are required to report a benchmark (accounting for $87.9 billion in federal spending). KFF used the Python script to identify the applicable benchmark type from the preprint, but also manually reviewed the data since states sometimes used inconsistent terminology to report the same benchmarks.

Identifying payment levels: To identify how current payment rates align with the new limits on SDPs in the reconciliation law, KFF first needed to identify payment levels in the preprints. The level is specified as a percentage of the benchmark (e.g., 90% of average commercial rates or 140% of Medicare rates). Both types of payments were pulled from Table 2 when available. Payment rates for inpatient and outpatient hospital services were tracked separately with each row in Table 2 when applicable.

Methods Table 1

| | | |

|---|

| Analysis Step | Count of Preprints | Federal Spending Among Preprints (billion $) | Analysis Step |

| Preprints listed on CMS’s website as of May 12, 2026 | 1,038 | | |

| All preprints pulled from CMS website | 987 | 246.4 | Some links are broken or duplicates |

| Preprints in time period and states | 570 |

166.1

| Includes the most recent preprint for each state directed payment (SDP) from January 2024 onwards for the 50 states and DC |

| Most recent SDP submission or renewal | 358 | 99.6 | |

| Preprints without data quality issues | 352 | 99.6 | KFF dropped preprints that were missing information about the start date, end date, spending amounts, etc. |

| Preprints manually reviewed and dropped | 305 | 93.1 | KFF dropped preprints from older years that were subsumed into newer preprints and those that were temporary policies started during the COVID-19 pandemic |

Appendix Table: States’ Number of and Spending on SDPs