Children in Immigrant Families: Key Facts on Health Coverage and Care

Introduction

One in four children aged 18 and under living in the U.S. has at least one immigrant parent. Policies undertaken by the Trump administration and Congress aimed at restricting access to health coverage and care for immigrants as well as the significant increase in immigration enforcement activities could have significant implications for the health and well-being of these children, the vast majority of whom are citizens.

This brief provides key data on socioeconomic characteristics and health coverage among children (aged 18 and under) of immigrants based on KFF analysis of 2024 American Community Survey data. It also examines potential implications of recent policies and actions on the health and well-being of children in immigrant families drawing on KFF survey data from Fall 2025.

Children in Immigrant Families

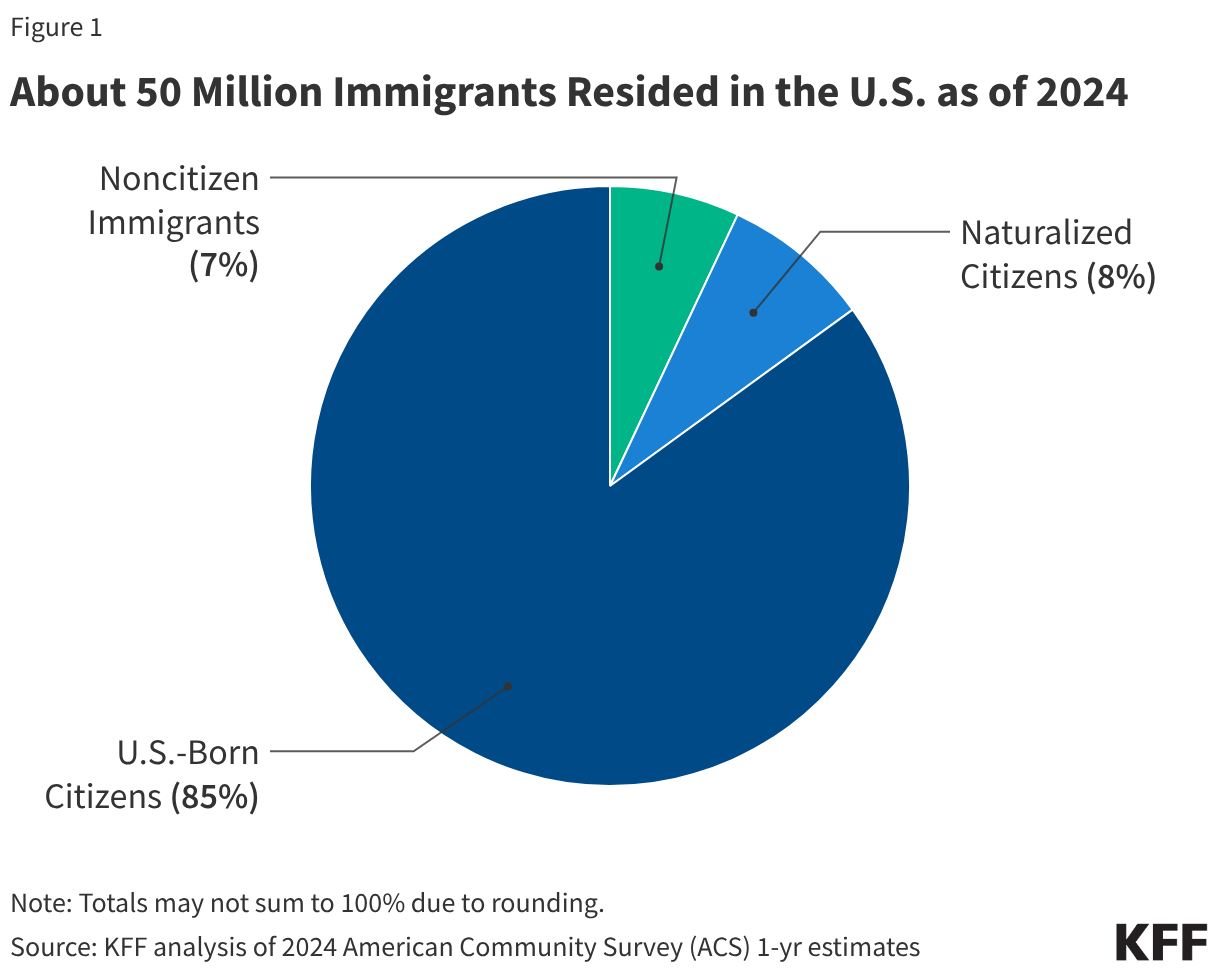

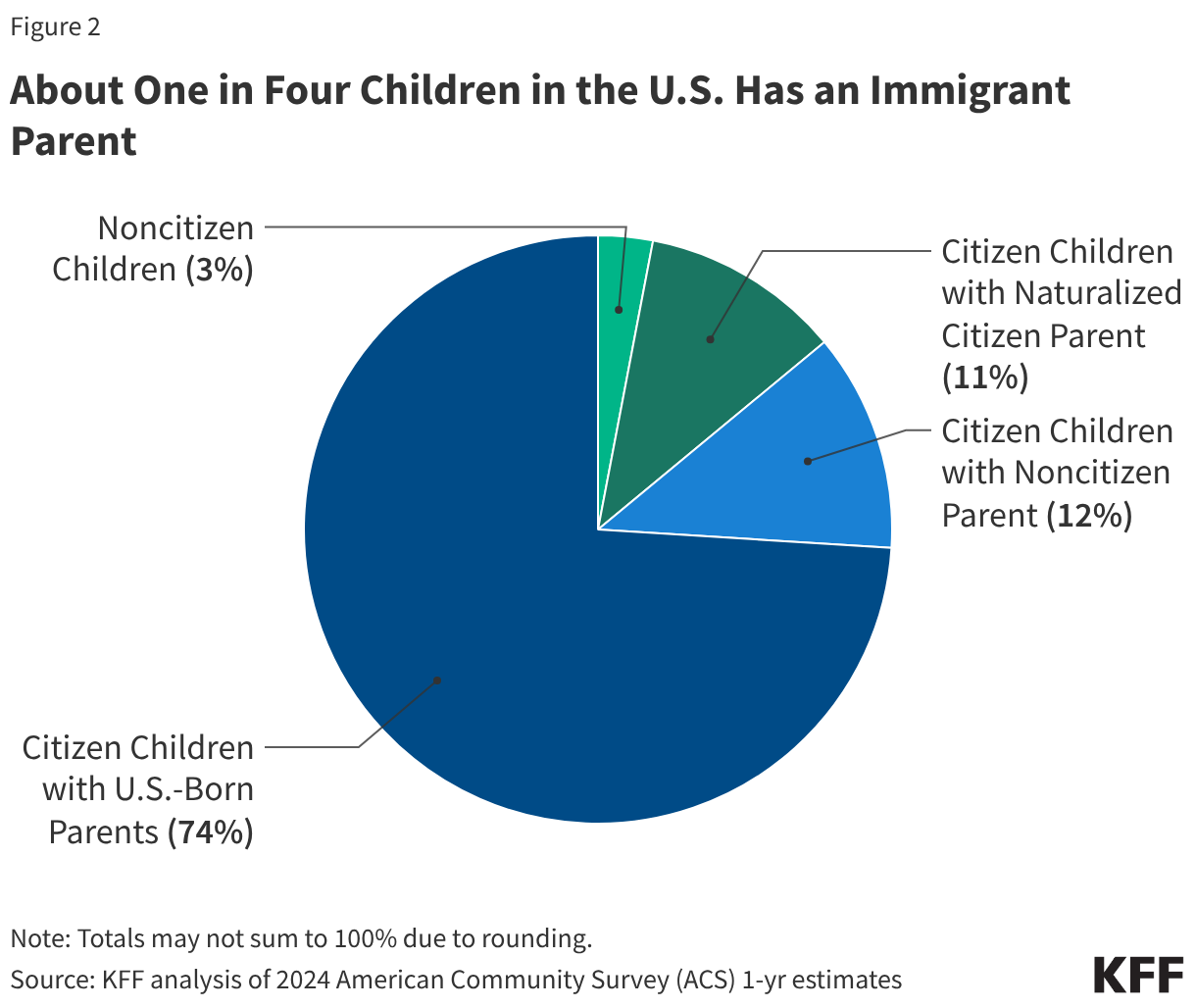

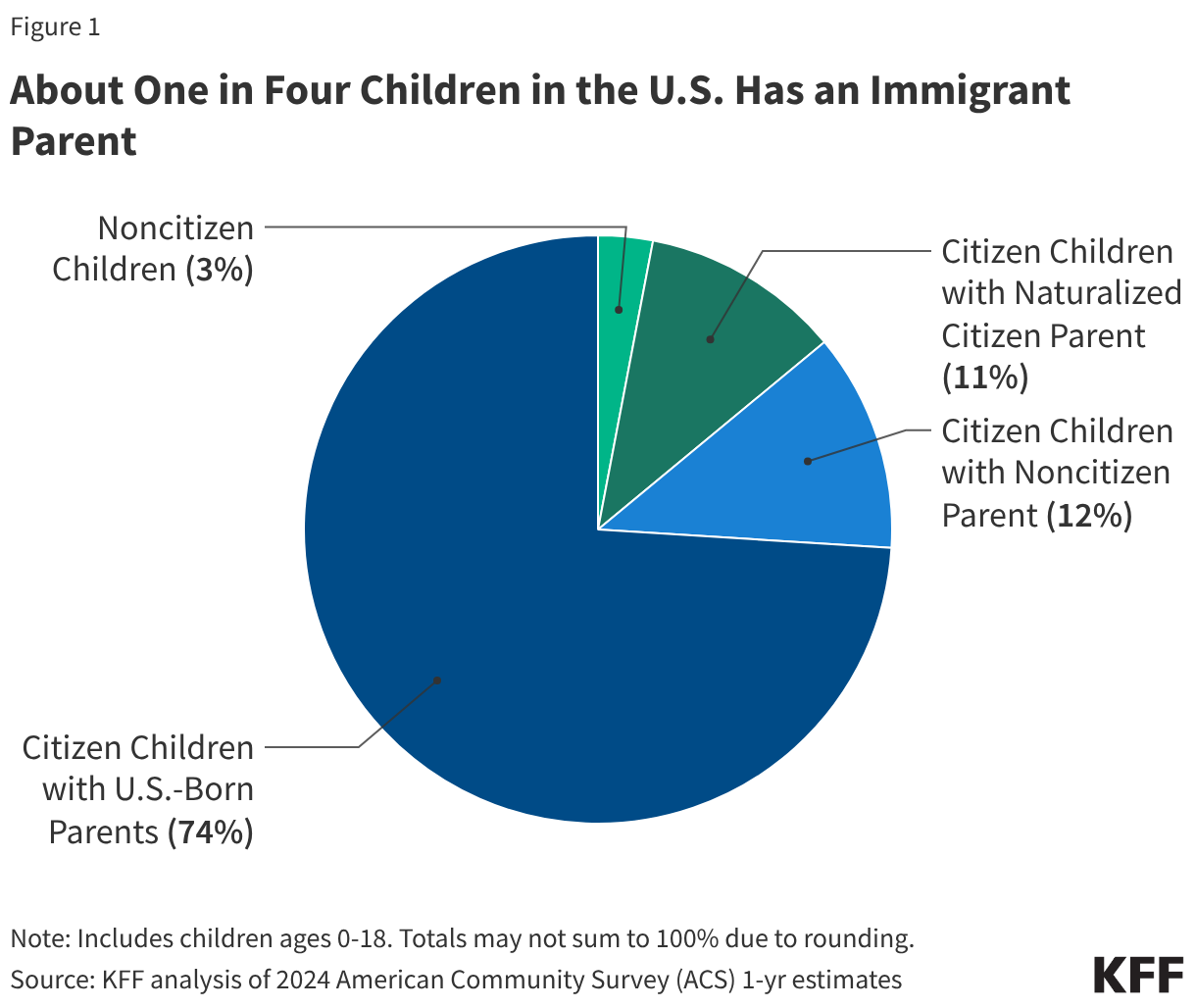

One in four children aged 18 and under in the U.S. has an immigrant parent, and the vast majority of these children are U.S. citizens. As of 2024, close to 20 million, or one in four (26%), children in the U.S. had an immigrant parent (Figure 1). This includes about one in ten (12%) who are citizen children with a noncitizen parent, a similar share (11%) who are citizen children with a naturalized citizen parent, and 3% who are noncitizen children. The share of children with an immigrant parent varies significantly by state, ranging from about 3% in West Virginia to about 45% in California.

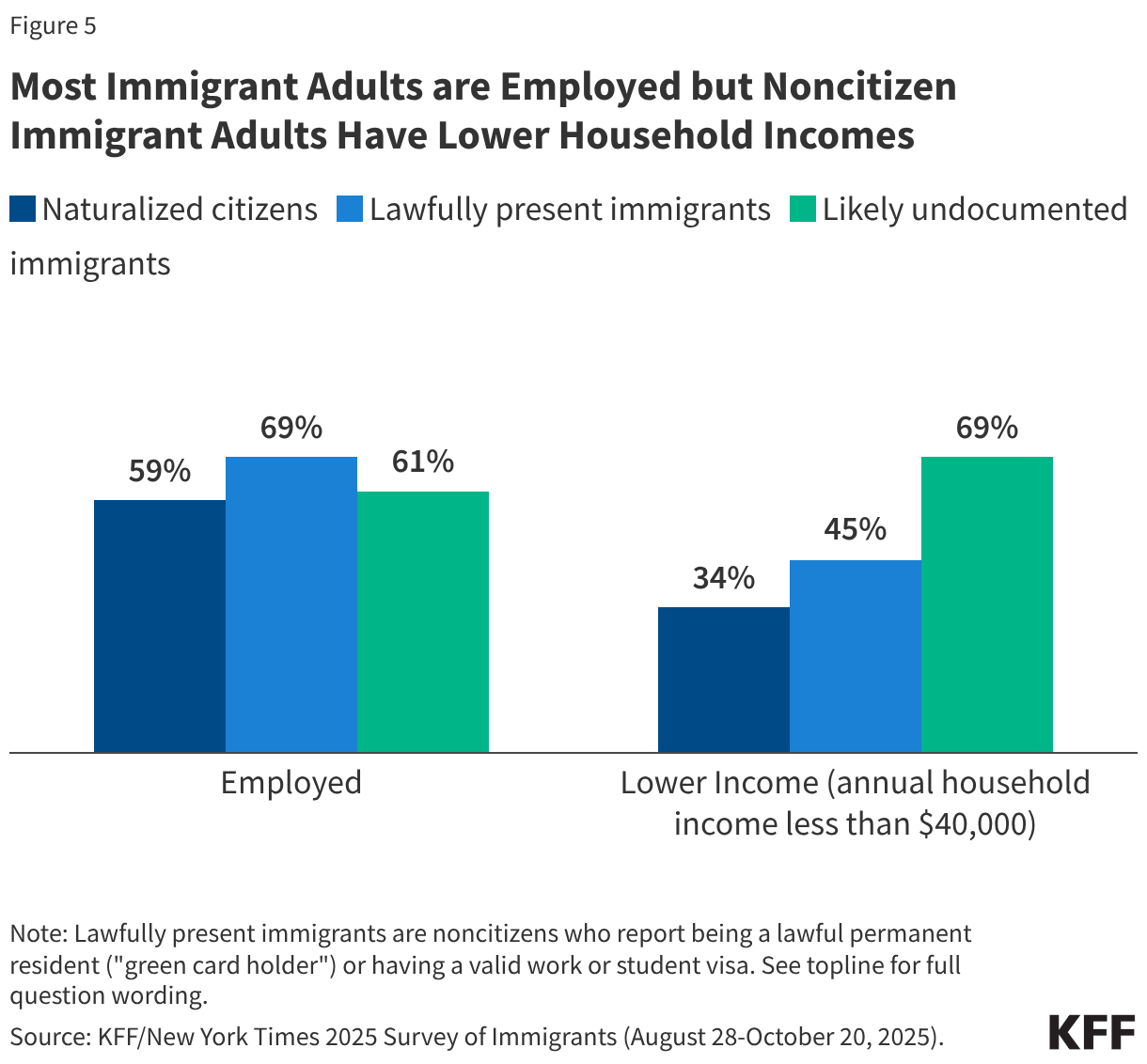

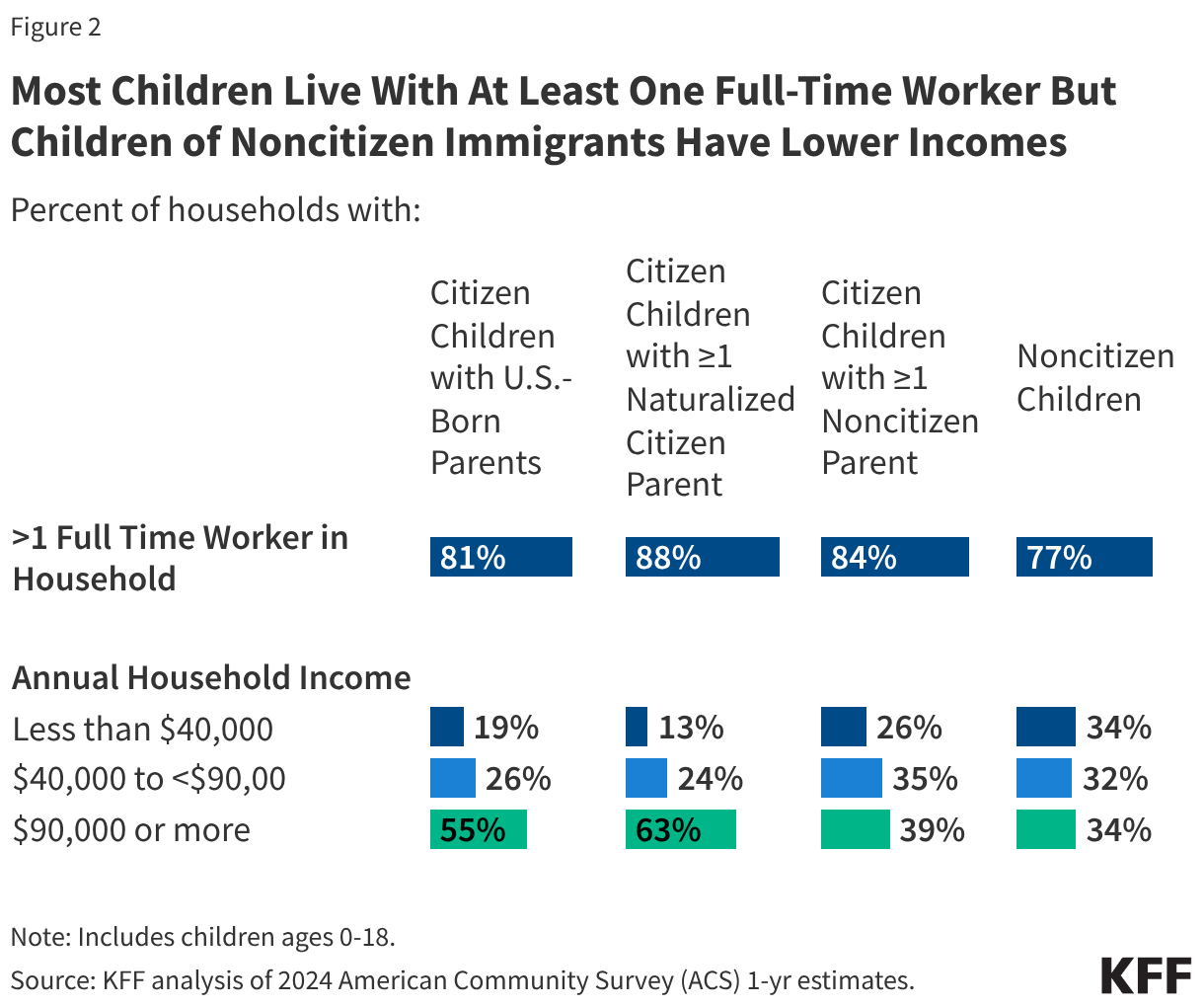

Most children of immigrants live in households with a full-time worker regardless of parental citizenship status; however, children with a noncitizen parent are more likely than children with citizen parents to live in lower income households. More than eight in ten citizen children live in a household with a full-time worker across parental citizenship statuses, and over three in four (77%) noncitizen children live in a household with a full-time worker (Figure 2). However, noncitizen children (34%) and citizen children with a noncitizen parent (26%) are more likely than those with U.S.-born parents (19%) and naturalized citizen parents (13%) to live in lower income households with annual incomes of less than $40,000. Lower household income among children of noncitizen immigrants reflects noncitizen immigrants’ disproportionate employment in lower-wage jobs in industries such as construction, agriculture, and service, which are less likely to provide employer-sponsored insurance.

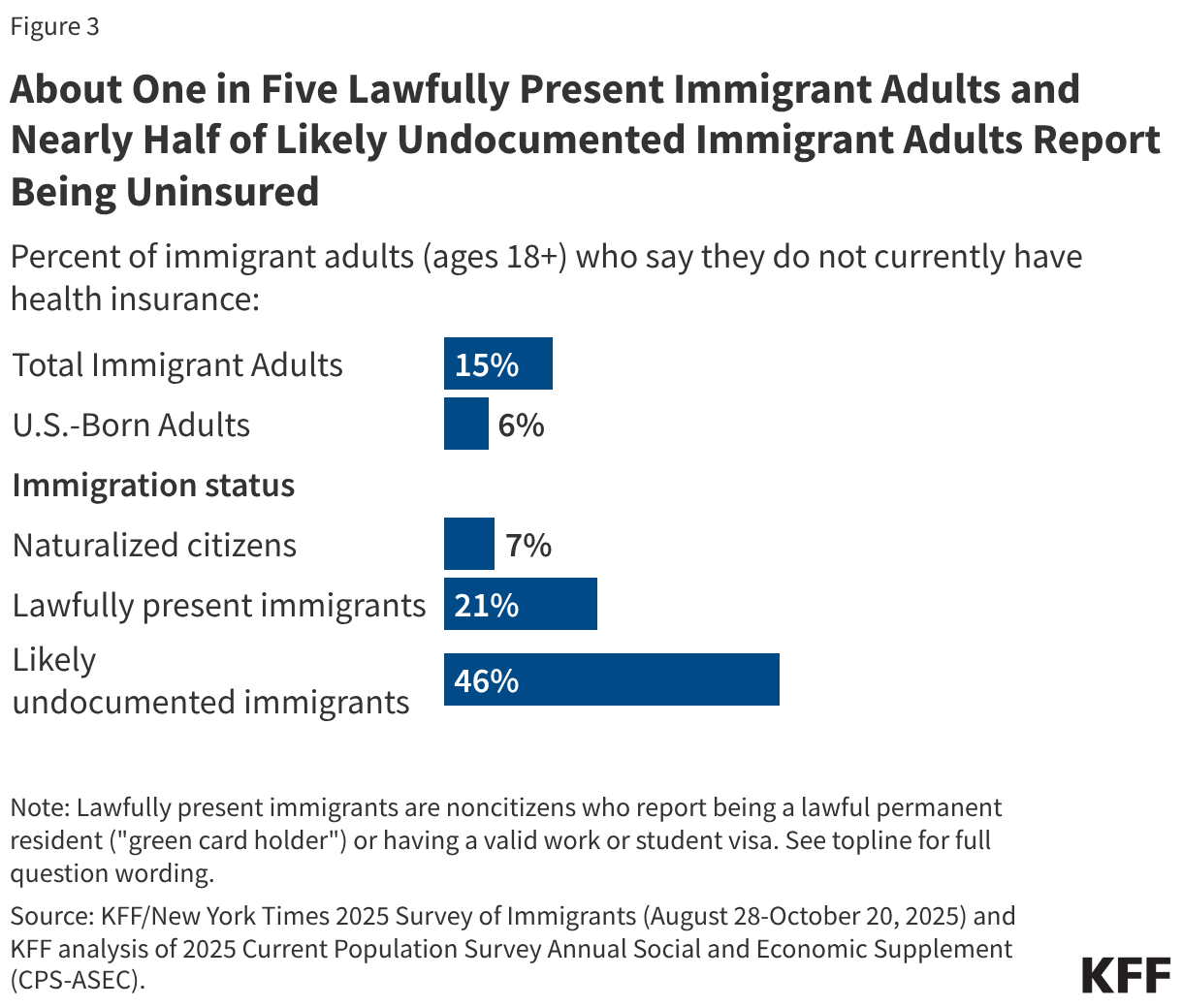

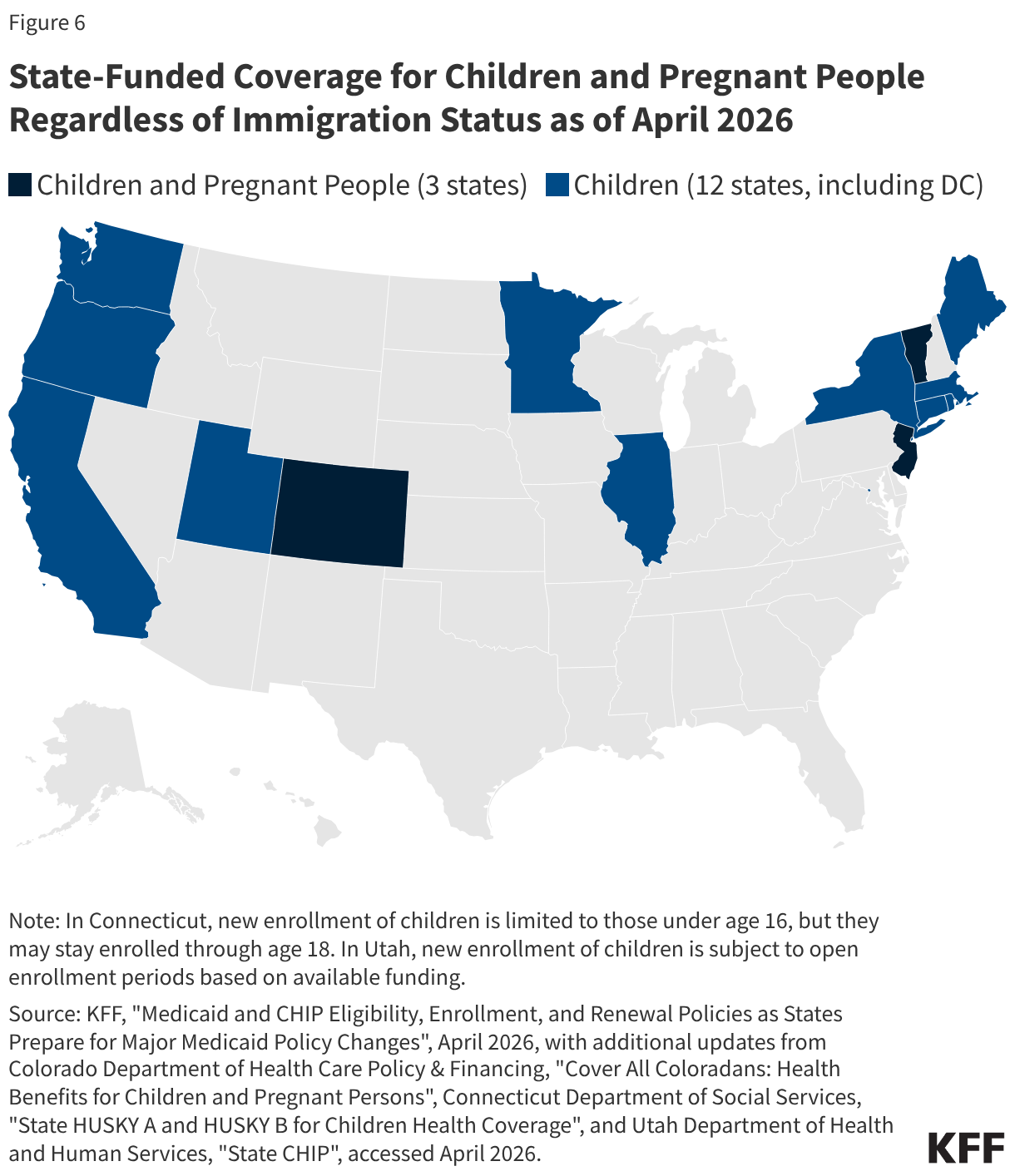

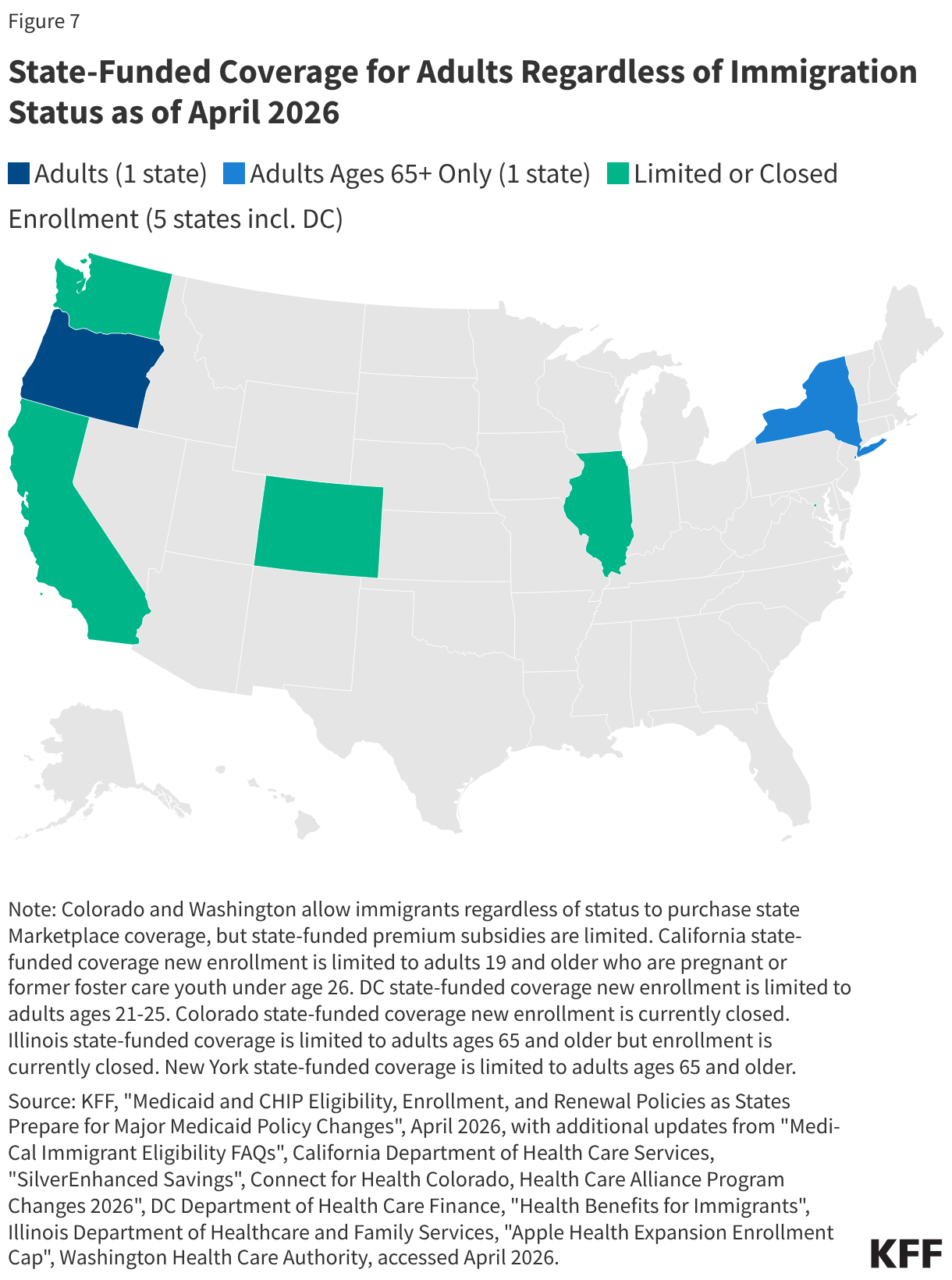

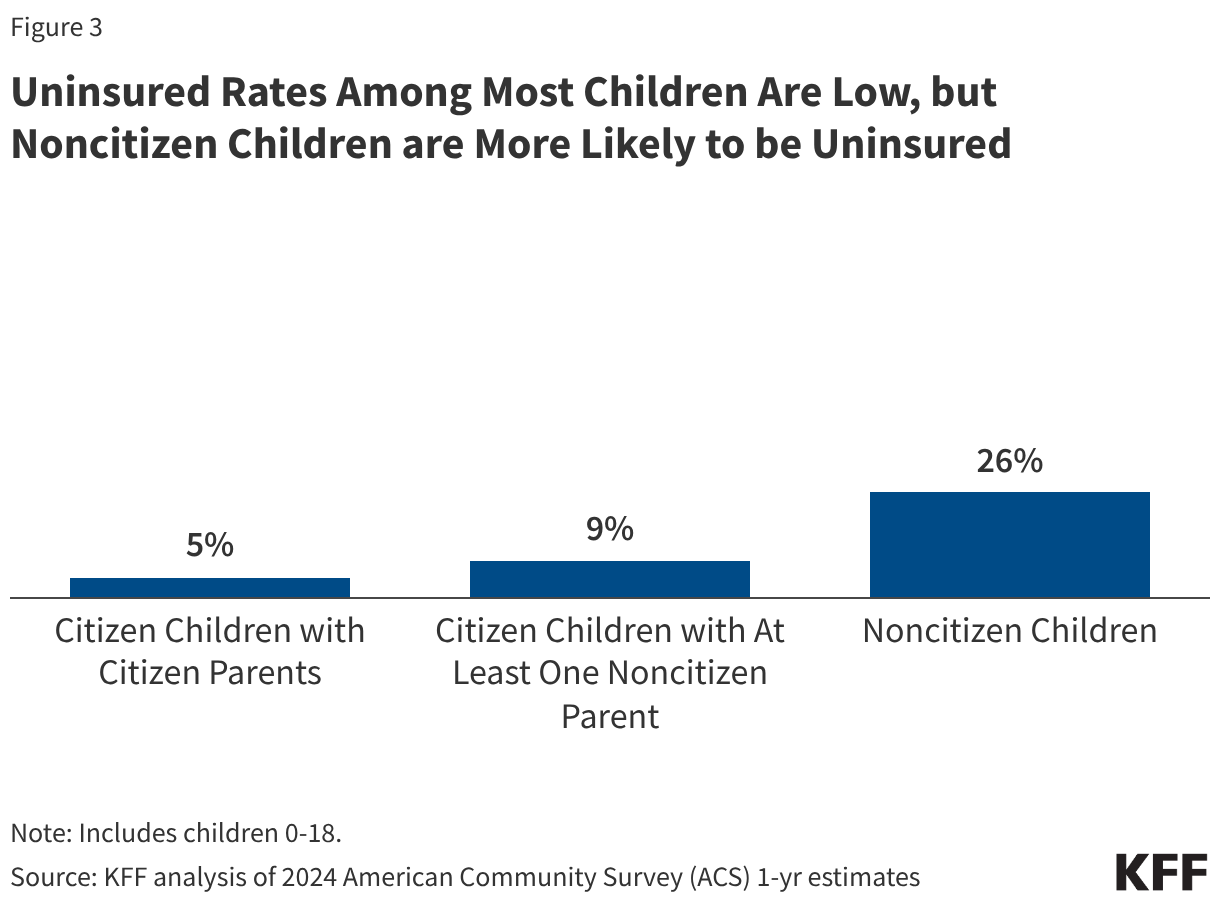

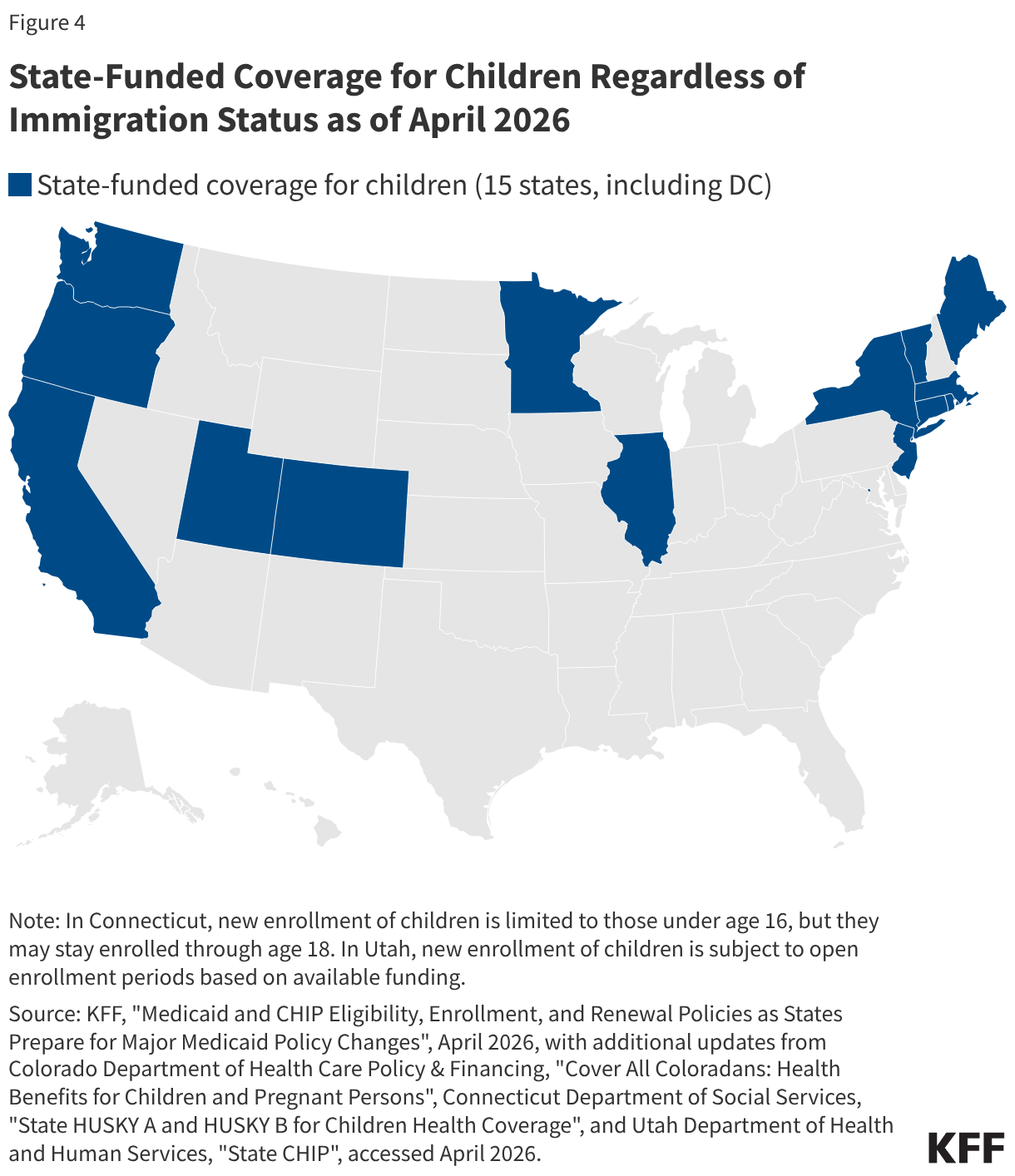

Uninsured rates among children remain relatively low, but those with a noncitizen parent or who are noncitizens are more likely to be uninsured than those with citizen parents. As of 2024, the uninsured rate was 9% among citizen children with noncitizen parent(s) and 26% among the small share of children who are noncitizens compared to 5% of citizen children with citizen parents (Figure 3). Medicaid and the Children’s Health Insurance Program (CHIP) offer broad coverage to lower-income children. However, lawfully present immigrant children may face eligibility restrictions on coverage, including a five-year waiting period, and the small number of children who are undocumented are ineligible for Medicaid, CHIP, and other federally funded coverage options. Moreover, parents may be reluctant to enroll citizen or lawfully present children in coverage even if they are eligible due to immigration-related fears or have difficulty enrolling their children due to confusion about eligibility rules or language barriers. States have an option to expand Medicaid or CHIP coverage for lawfully residing children without a five-year waiting period, which was taken up by 38 states, including DC, as of April 2026. Additionally, as of April 2026, 15 states, including DC, provide comprehensive fully state-funded coverage for lower income children regardless of immigration status with one state (Colorado) planning to scale back coverage due to budget pressures (Figure 4).

Potential Implications of Recent Policies

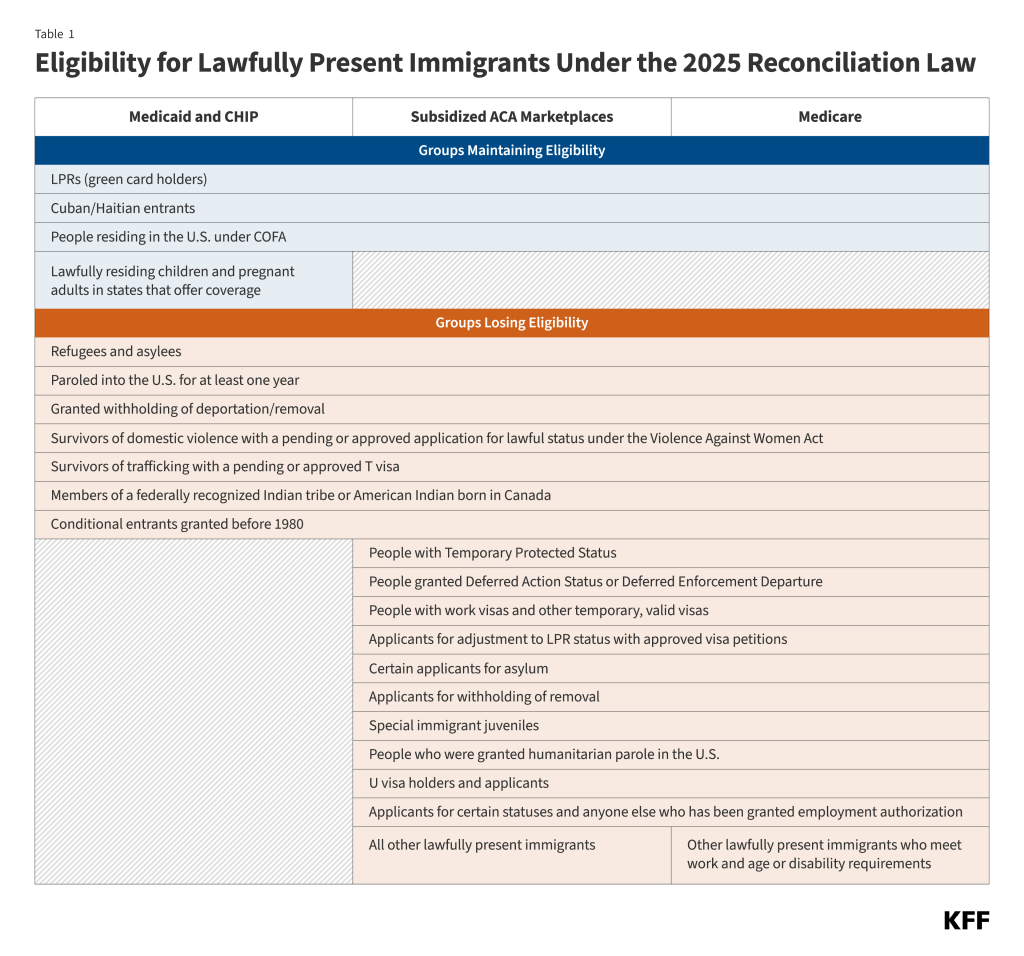

Since taking office, the Trump administration has taken a range of actions focused on increasing immigration enforcement, restricting immigration, and limiting immigrants’ access to health care and other services. These actions include an Executive Order (EO) issued in January 2025 to end birthright citizenship, a right guaranteed under the 14th amendment of the U.S. Constitution, for the children of some noncitizen parents, including those who may be undocumented as well as lawfully present individuals on non-immigrant visas (for example, certain work visas). Implementation of the EO is blocked as of April 2026 under court order, with the Supreme Court expected to rule on it in June or July 2026. Ending birthright citizenship for the children of some immigrants would have broad implications, including limiting their access to health coverage. Moreover, the 2025 reconciliation law will further restrict lawfully present immigrants’ access to health coverage, which is expected to increase the number of uninsured. The combination of growing immigration-related fears among immigrant families, increased restrictions on coverage for lawfully present immigrants, and growing financial pressures will likely negatively impact health and health care for children in immigrant families, including U.S. citizens, and could have longer-term impacts on the U.S. workforce.

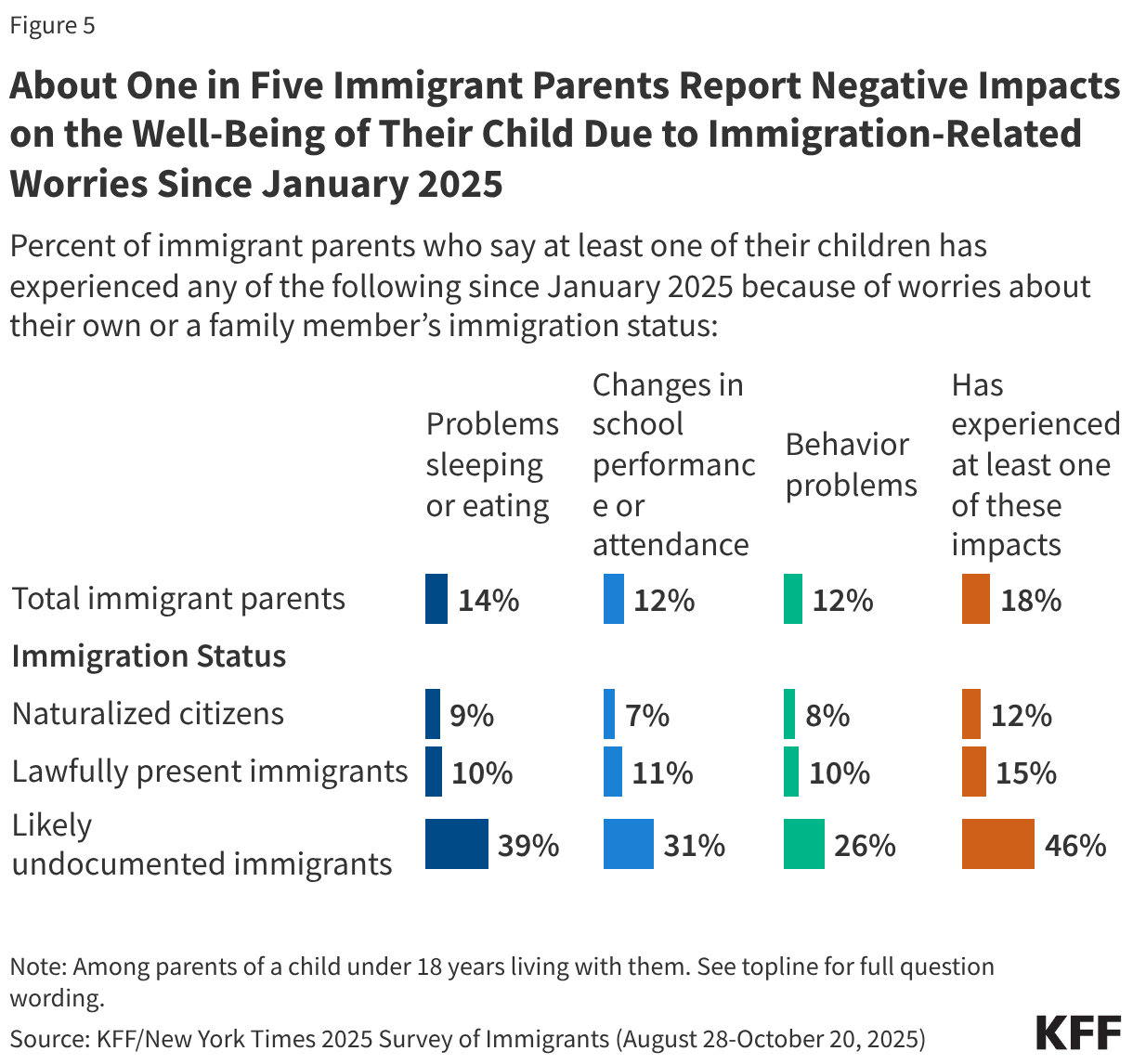

Increased immigration-related worries will likely have long-term negative impacts on children’s physical and mental health. The American Academy of Pediatrics has identified fear of parental deportation and separation as a toxic stress, which can adversely affect a child’s development, leading to lifelong negative effects on physical, mental, and behavioral health. KFF survey data from Fall 2025 show that over one in four (27%) immigrant parents say their children have expressed worries about something bad happening to someone in their family due to immigration status, with this share rising to six in ten of likely undocumented parents. These worries have negative impacts on children’s health and well-being. About one in five (18%) immigrant parents say a child has experienced problems sleeping or eating (14%), changes in school performance or attendance (12%), or behavior problems (12%) due to worries about a family member’s immigration status (Figure 5). This share rises to nearly half among parents who are likely undocumented.

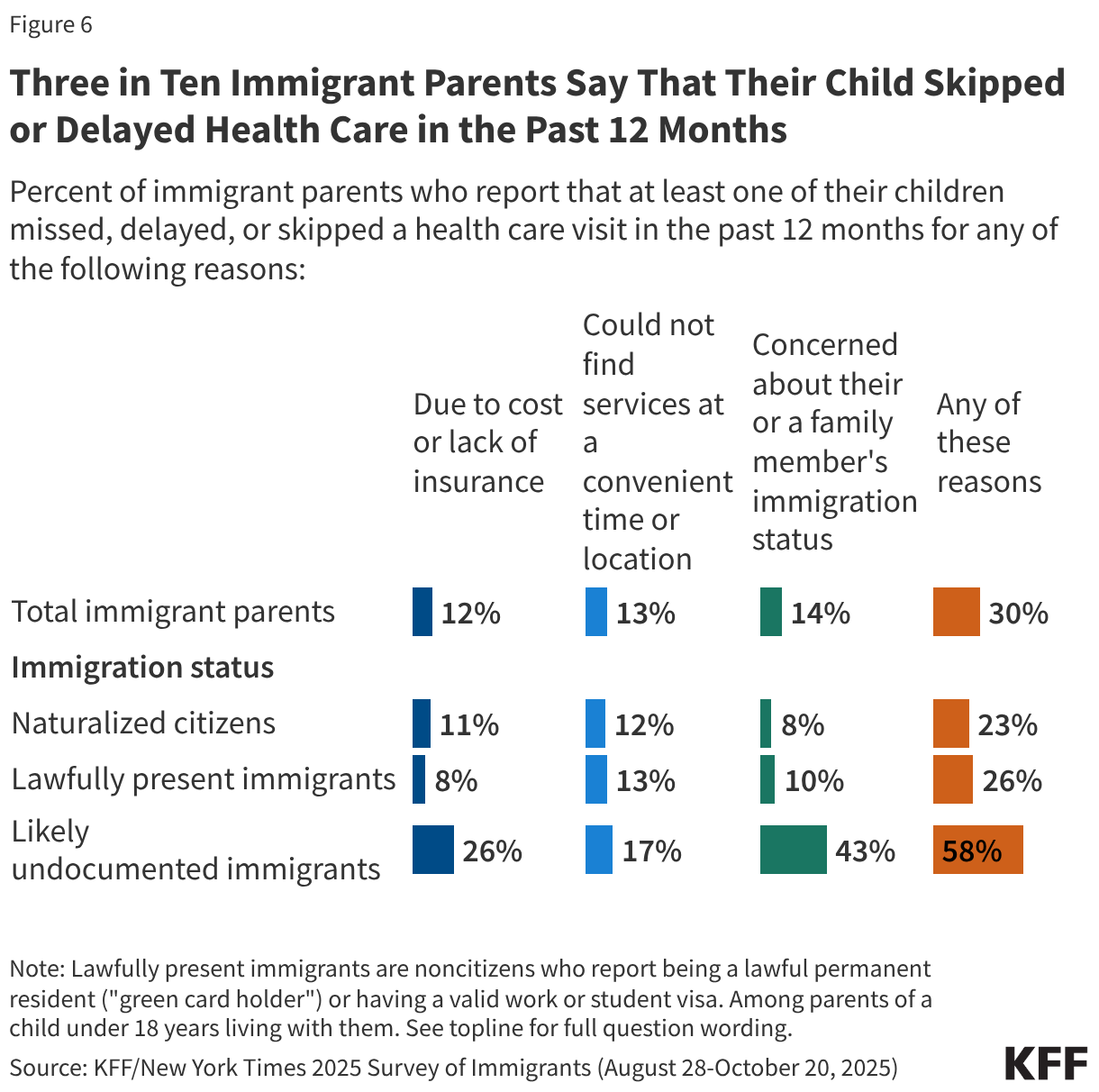

Children in immigrant families may face greater barriers to accessing health care due to increased restrictions on health coverage and immigration-related fears. The Trump administration and Congress have enacted a number of policy changes aimed at reducing access to health coverage and care for immigrants including but not limited to new restrictions on eligibility for health coverage for lawfully present immigrants under 2025 reconciliation law, proposed changes to public charge rules, sharing of noncitizen Medicaid enrollee data with immigration enforcement officials, as well as restrictions on access to community health centers and other social services. These changes are likely to result in coverage losses for immigrants, including among citizen children in immigrant families. Coverage losses among immigrant parents may lead to losses among their children as research shows that parental coverage impacts children’s access to health coverage and care. Moreover, growing immigration-related fears have made families more reluctant to access programs and services even if they are eligible. KFF survey data from Fall 2025 show that about one in ten (11%) immigrants say they stopped participating in government programs that help pay for food, housing, or health care since January 2025 due to immigration-related fears. Further, one in seven (14%) immigrant parents, rising to over four in ten (43%) of likely undocumented immigrant parents, say that their child missed, skipped, or delayed health care in the past 12 months due to immigration-related concerns (Figure 6).

Beyond impacts on the health and well-being of immigrant families, the current environment may negatively impact the U.S. workforce given the significant role immigrants and their adult children play, especially in health care. Adult children of immigrants have higher educational attainment and incomes than their parents as well as the adult children of U.S.-born parent(s) and play an outsized role in the U.S. health care workforce. Based on KFF analysis of 2024 federal survey data, adult children of immigrants ages 18 and older make up about 7%, or over 1.4 million, of the total health care workforce, including 11% of physicians, surgeons, and other practitioners. Moreover, immigrants and their adult children contribute billions of dollars in federal, state, and local taxes each year and help to create jobs for U.S.-born people. Research further shows that adult children of immigrants contribute more in taxes on average than their parents or the rest of the U.S.-born population and that their fiscal contributions exceed their costs associated with health care, education, and other social services. As such, restrictions in immigration could have long-term implications for the U.S. workforce and economy.