As of this week, federal data from the Centers for Disease Control and Prevention (CDC) show that 78% of the total population in the United States have received at least one dose of a COVID-19 vaccine. While vaccination coverage increased in the first half of 2022, vaccination and booster uptake has leveled off and remains uneven across the country. As the United States navigates another Omicron wave, individuals who have not received any booster dose are at higher risk of infection from the virus, and people who remain unvaccinated continue to be at particularly high risk for infection, severe illness, and death. Over the course of the vaccination rollout, Black and Hispanic people have been less likely than their White counterparts to receive a vaccine, but these disparities have narrowed over time and reversed for Hispanic people. With first booster shot eligibility expanded to all individuals, and vaccinations authorized for people ages 6 months and older, ensuring equity in the uptake of booster shots and vaccinations among children is also important. However, to date, limited data are available to examine racial disparities among booster shot recipients and children. Moreover, some states have reduced the frequency of their reporting of vaccinations by race/ethnicity or stopped reporting these data, further limiting data available to understand vaccination patterns.

This data note presents federal data on COVID-19 vaccinations and booster doses by race/ethnicity and state reported data on COVID-19 vaccinations, COVID-19 vaccinations among children, and booster shot recipients by race/ethnicity, where available.

Federal Data on COVID-19 Vaccinations by Race/Ethnicity

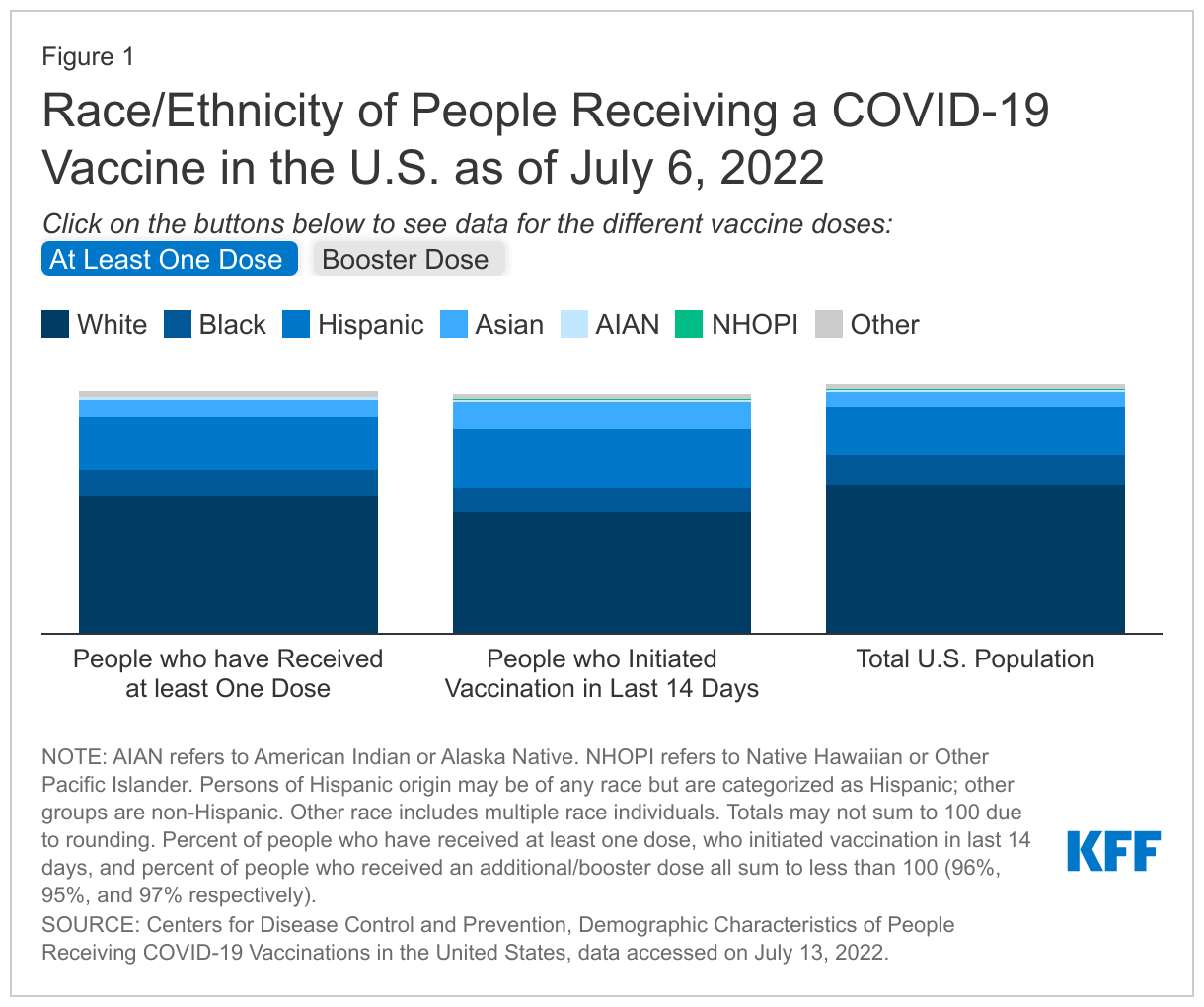

The CDC reports demographic characteristics, including race/ethnicity, of people receiving COVID-19 vaccinations at the national level, including both people who have received one dose and people who have been recently vaccinated (initiated within the last 14 days). CDC reports that as of July 6, 2022, race/ethnicity was known for 75% of people who had received at least one dose of the vaccine. White people make up a smaller share of people who have received at least one dose (55%) and people who have recently received a vaccination (48%) compared to their share of the total population (59%). Black people make up 10% of people who recently received a vaccination, which is the same as their share of people who have received at least one dose (10%), and smaller than their share of the total population (12%), Hispanic people make up a larger share of vaccinated people (21%) and people who recently received a vaccination (23%) compared to their share of the total population (19%). The overall share of vaccinated people who are Asian is similar to their share of total population (7% and 6%, respectively), while they make up a larger share of people who recently got vaccinated (11%) (Figure 1).

For children, CDC reports that as of July 6, 2022, 37% of children ages 5-11 and 70% of children ages 12-17 have received at least one COVID-19 vaccine dose. However, CDC does not currently report race/ethnicity of vaccinated children. Children ages 6 months to 5 years old became eligible for vaccination on June 18, 2022, but CDC had not yet begun reporting vaccination data for this group as of the time of this update.

The CDC also reports the race/ethnicity of people who have received an additional/booster vaccine dose at the federal level. Race/ethnicity data was available for 89% of people who have received their first booster dose as of July 6, 2022. Among this group, 61% of booster recipients were White, 8% were Black, 8% were Asian, 15% were Hispanic, and AIAN and NHOPI people made up less than 1% of recipients (0.7% and 0.3%, respectively). The shares of booster dose recipients who are Black (8%) and Hispanic (15%) are smaller than their shares of fully vaccinated people ages 5 and older (10% and 20%, respectively). However, Black, and Hispanic people made up larger shares of people receiving a booster dose in the past 14 days (11% and 23%, respectively). Overall, Asian (62%) and White (56%) people had the highest shares of eligible people who had received a booster dose as of July 6, 2022, while less than half of NHOPI (49%), AIAN (47%), Black (44%) and Hispanic (41%) people had received a booster shot.

While these data provide helpful insights at the national level, significant gaps in data remain to help understand who is and is not getting vaccinated. To date, CDC is not publicly reporting state-level data on the racial/ethnic composition of people vaccinated or receiving booster doses. Moreover, CDC is not reporting racial and ethnic data for vaccinations among children.

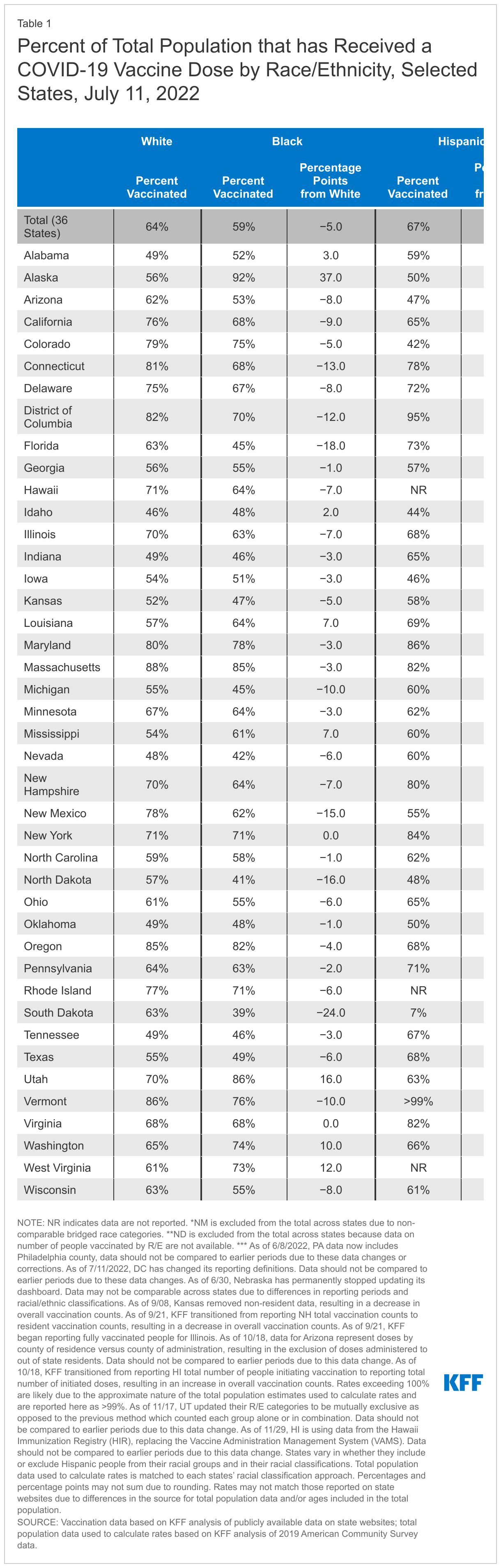

State Data on COVID-19 Vaccinations by Race/Ethnicity

To provide greater insight into who is receiving the vaccine and racial/ethnic disparities in vaccinations, KFF is collecting and analyzing state-reported data on COVID-19 vaccinations by race/ethnicity, as well as data on race/ethnicity of vaccinations among children and booster dose recipients where available.

Percent Who Have Received At least One Dose

As of July 11, 2022, 41 states and Washington D.C. were reporting vaccination data by race/ethnicity, including 39 that reported race/ethnicity of people who received at least one dose of the vaccine.1 Table 1 shows the percent of the total population who have been vaccinated by race/ethnicity in each of these 42 states and the total across 36 of these states. (Idaho, Minnesota, New Mexico, North Dakota, and Oregon are excluded from the total due to differences in their reporting of data.) It also shows the percentage point difference between vaccination rates for White people and the rates for Black, Hispanic, and Asian people. These data will differ from survey estimates of vaccination rates that are limited to adults. More than two years into the pandemic, some states have either reduced or stopped reporting their vaccination data. For example, since our last data update, Arizona, Florida, Kansas, and Michigan have all reduced the frequency of their vaccination data updates, while Kentucky, Missouri, Nebraska, and South Carolina stopped reporting vaccination data by race/ethnicity.

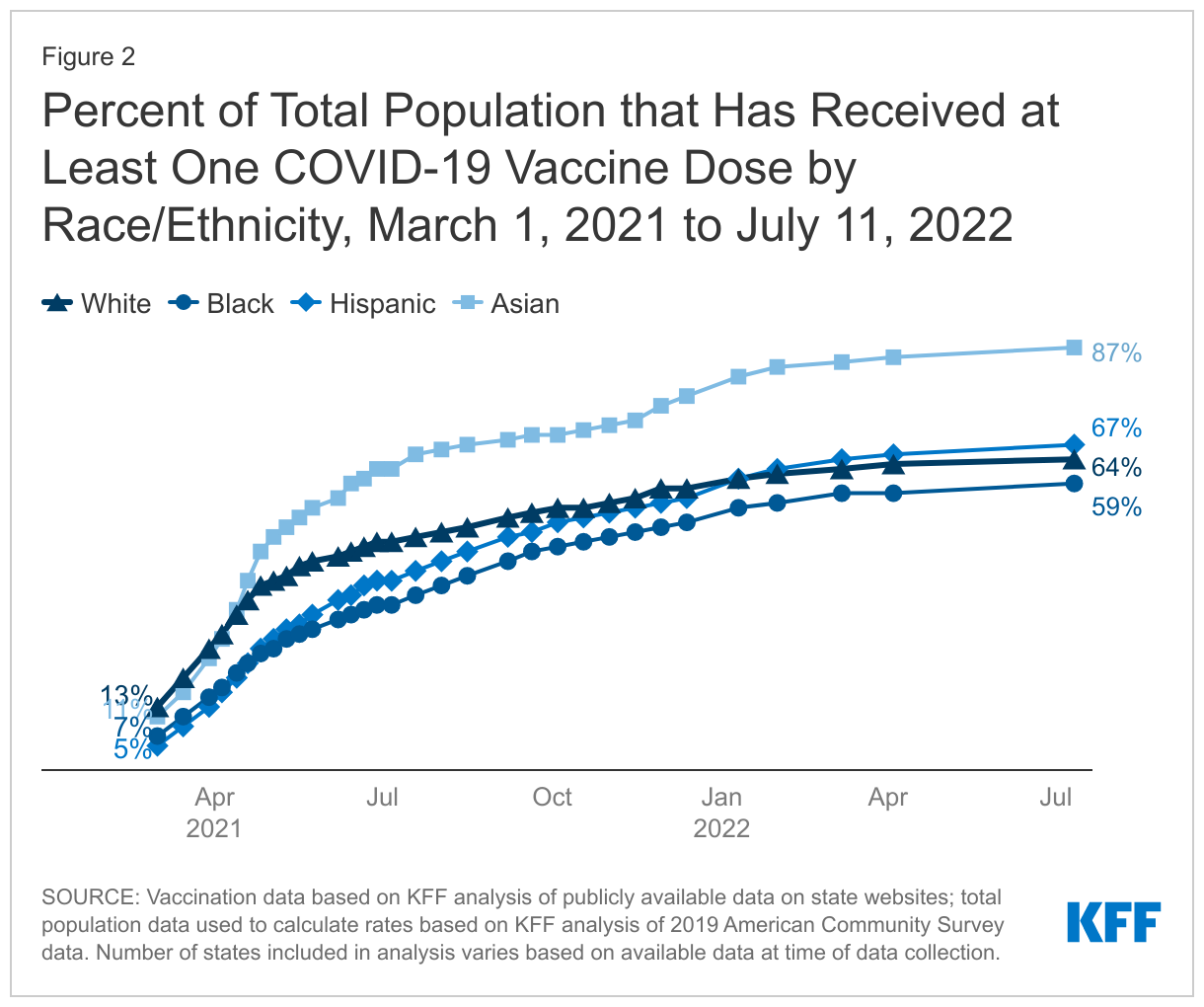

Across the 36 states for which a total vaccination rate could be calculated by race/ethnicity as of July 11, 2022, 87% of Asian, 67% of Hispanic, and 64%of White people had received at least one COVID-19 vaccine dose, higher than the rate for Black people (59%). Hispanic people had a similar or higher vaccination rate than White people in 22 states. White people had a higher rate than Black people in most reporting states, except for Alabama, Mississippi, Louisiana, Alaska, West Virginia, Utah, Idaho, and Washington. The size of these differences varied widely across states, and they have been narrowing over time. The overall vaccination rate across states for Asian people was higher compared to White people (87% vs. 64%), which was reflected across all reporting states except for North Dakota, South Dakota, and Colorado.

Vaccination rates across racial and ethnic groups experienced a small two percentage-point increase between our last data update on April 4 and July 11, 2022. Over the course of the vaccination rollout, differences between vaccination rates for Black, Hispanic, and White people have narrowed, and the disparity for Hispanic people has reversed. Between late April 2021, when most adults became eligible for vaccines across states, and July 11, 2022, the gap in vaccination rates between White and Black people fell from 14 percentage points (38% vs. 24%) to 5 percentage points (64% vs. 59%) while the 13% percentage point difference (38% vs. 25%) between White and Hispanic vaccination rates was eliminated, with Hispanic people having a slightly higher rate than White people since early 2022.

Vaccinations Among Children

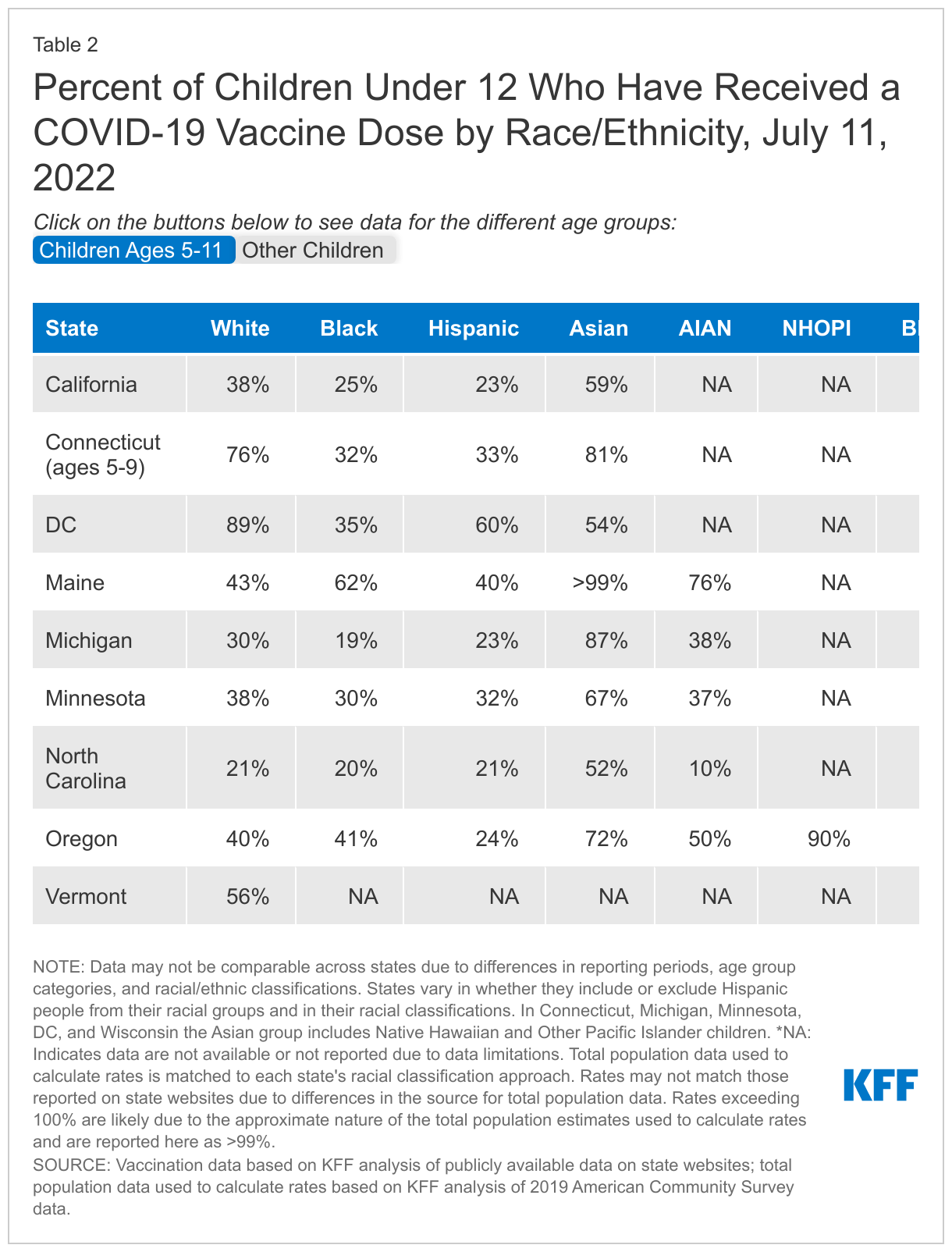

As of the week of July 11th, ten states (California, Connecticut, Kansas, Maine, Michigan, Minnesota, North Carolina, Oregon, Vermont, and Wisconsin) and Washington D.C. reported COVID-19 vaccination data by race/ethnicity for children (Table 2). While these states report race/ethnicity of vaccinated children, they vary in their racial/ethnic categorizations and age groups, making it challenging to compare vaccination data across states. Seven states (California, Maine, Michigan, Minnesota, North Carolina, Oregon and Vermont) and Washington D.C. reported race/ethnicity data separately for children ages 5-11. As of June 18th, children between ages six months and 5 years old were the most recent group to become eligible for the vaccine. As of this update, five states have begun reporting data for this age group by race/ ethnicity, but they were excluded from the analysis due to limited data.

The data from these states have mixed findings regarding vaccinations by race/ethnicity among children. Black children had lower vaccination rates than White children in most but not all reporting states. Asian children had the highest vaccination rate in most reporting states. Rates for Hispanic children were lower than rates for White children in most states among those in the age 5-11 age group. However, among children 12 and older or children overall (in states that do not include separate age breaks among children), their rates were mostly higher or similar to the rates for White children. Overall, it remains challenging to draw strong conclusions about racial equity in COVID-19 vaccinations among children due to the dearth of comprehensive data, inconsistency in reporting, and the lack of disaggregated data for smaller racial/ethnic groups, particularly NHOPI children.

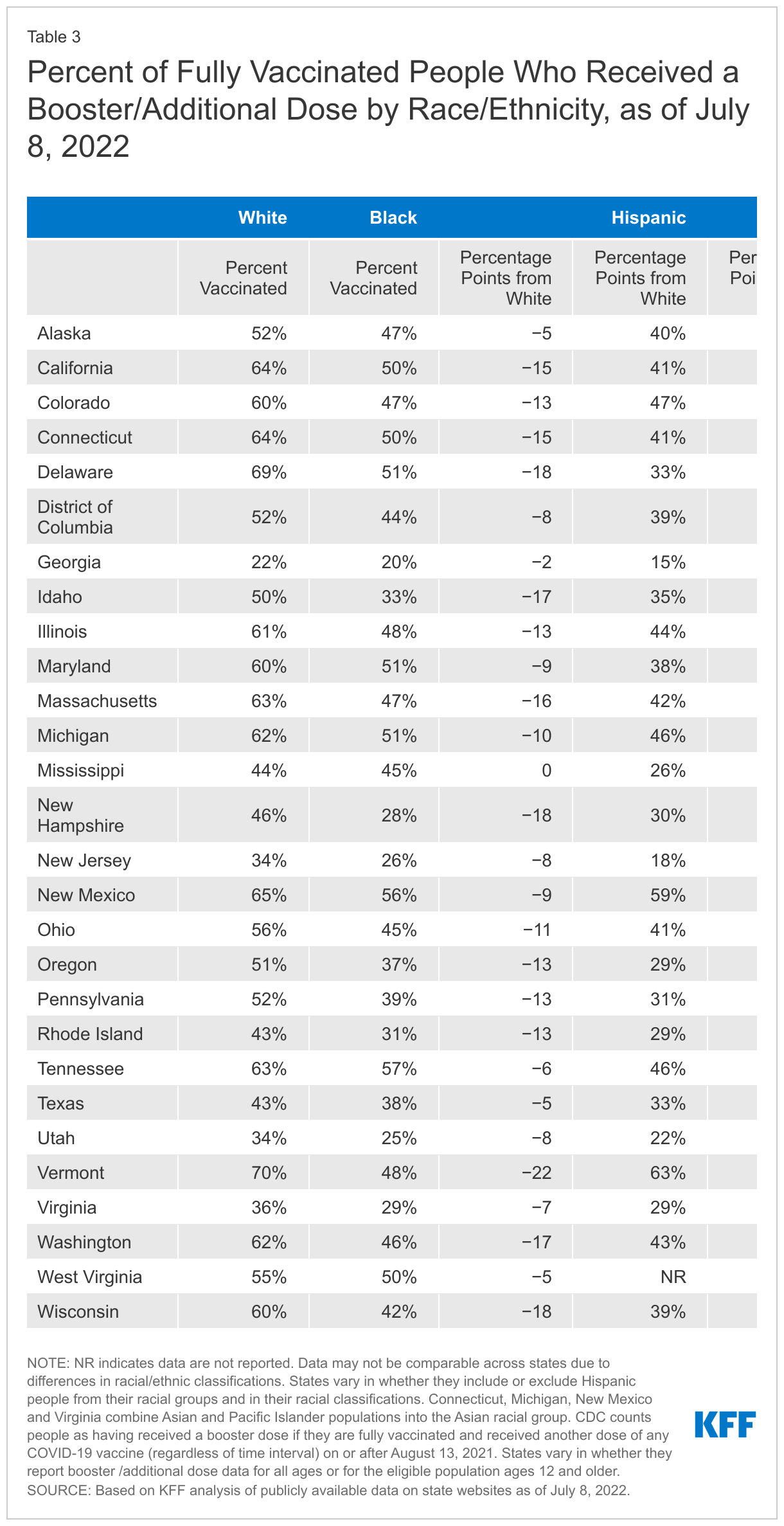

Booster Dose Recipients

As of July 8, 2022, 27 states and Washington DC were reporting vaccination booster data by race/ethnicity, a small increase from the 25 states reporting these data as of April 1, 2022. Among these states, the share of Black and Hispanic people who had received a booster shot was lower compared to White people. Findings for Asian people were more mixed, with rates similar or higher than White people in about half the states, but lower in the others (Table 3). However, like the data for children, it is difficult to make strong conclusions about disparities in booster shots due to the lack of data and inconsistency across data where it is available.

Discussion

Data point to significantly increased risks of COVID-19 illness and death for people who remain unvaccinated. White people account for the largest share of people who remain unvaccinated. Black and Hispanic people have been less likely than their White counterparts to have received a vaccine over the course of the vaccination rollout, but these disparities have narrowed over time and reversed for Hispanic people.

The increasing equity in vaccination rates likely reflects a combination of efforts focused on increasing vaccination rates among people of color through outreach and education and reducing access and logistical barriers to vaccination. It may also reflect increased interest in getting the vaccine in response to variants and increases in vaccinations among younger adults and adolescents who include higher shares of people of color compared to other adults.

Despite this progress, the ongoing disparities in rates highlight the importance of continued efforts to increase vaccination rates and to address gaps in vaccination both geographically and across racial/ethnic groups. Moreover, it will be important to prevent disparities in the uptake of booster shots, and among children, among whom vaccination rates are lagging overall. At the same time, ensuring equity in access to treatments will be important, particularly as other analysis suggests potential disparities in access to oral antiviral pills.

While the data provide useful insights, they remain subject to gaps, limitations, and inconsistencies that limit the ability to get a complete picture of who is and who is not getting vaccinated. As noted, at the federal level, race/ethnicity remains unknown for about a quarter of vaccinations. Moreover, CDC does not report state level vaccination data, including booster doses, by race/ethnicity nor racial/ethnic data for vaccinations among children.

At the state level, the completeness of race/ethnicity data has improved in most states over time. However, some states still have relatively high shares of vaccinations among people classified with “unknown” race/ethnicity. Further, seven states do not report vaccination data by race/ethnicity, and some states have recently halted or reduced the frequency of their reporting of these data. Inconsistences in racial/ethnic classifications across states, as well as separate reporting of data for federally administered vaccinations, including those provided through the Indian Health Service and federal long-term care partnership program, limit the ability to interpret the data. Only a handful of states report data in a way that allows for analysis of vaccination rates by race/ethnicity among children. Similarly, state data are available on race/ethnicity of COVID-19 booster shot recipients in only half of the states.

In addition, ongoing changes and updates to the data may make it challenging to interpret the data and trend it over time. For example, some states have reported declines in cumulative vaccinations for some racial/ethnic groups over time. These declines reflect a variety of factors, including changes in state reporting methods and recoding of individuals’ racial/ethnic classifications over time. For example, several states have indicated that an individual’s self-reported race/ethnicity may change if they record a different classification when receiving a subsequent COVID-19 vaccine dose or another vaccination, such as the flu shot.

Overall, comprehensive standardized data are vital to monitor and ensure equitable access to and uptake of the vaccine. For example, without improvements in data reporting, it will not be possible to identify disparities in vaccination uptake among children.

Complete data on the distribution of vaccinations by race/ethnicity as well as the percent of the total population that have received at least one COVID-19 vaccine dose are available and downloadable through our State Health Facts Online tables. Moving forward, KFF will update these data on a periodic basis.