KFF/theGrio Survey of Black Voters

Overview

The Survey of Black Voters, the first under a new partnership between KFF and theGrio, examines the mood and opinions of Black voters as the 2022 midterm election approaches. For this project, we interviewed 1,000 Black registered voters, allowing for analysis that goes beyond the topline findings and paints a richer picture of the diversity of attitudes within the Black voting population.

The survey explores Black voters’ voting intentions, motivations, and views on key electoral issues for the upcoming midterm. It also examines Black voters’ attitudes toward the Democratic and Republican Parties, views on electoral integrity, and past experiences with voter suppression. In addition to these election-related topics, the survey sheds light on how Black voters feel about timely topics including recent Supreme Court decisions, policies affecting LGBT individuals, and policies aimed at improving health for Black people in the United States.

Read theGrio’s coverage:

Black voters’ mood ahead of midterms tempered by age, economy and racism, TheGrio/KFF Survey finds, published Oct. 18, 2022.

Black voters name inflation, economic issues as biggest concern ahead of midterm elections, published Oct. 18, 2022.

Black voters solidly approve of Biden and Harris, less firm on the president’s reelection in 2024, published Oct. 18, 2022.

Majority of Black voters say Trump should be criminally charged for Jan. 6 insurrection in TheGrio/KFF survey, published Oct. 19, 2022.

As Republicans still scream fraud in 2020 election, Black voters surveyed by theGrio/KFF still believe their votes count, published Oct. 20, 2022.

Black voters surveyed by theGrio/KFF want Biden to address inflation; only 12% named student debt as top economic issue, published Oct. 24, 2022.

Most Black voters tell theGrio/KFF survey they support funding or increased funding for police, published Oct. 25, 2022.

Black voters surveyed by theGrio/KFF think the Supreme Court is politicized and see this as a bad sign for Black people, published Oct. 26, 2022.

Why Black voters don’t want to defund the police, explained, published Oct. 27, 2022.

Young Black voters could be essential in future elections, analysis of theGrio/KFF survey shows, published Oct. 29, 2022.

Black voters say recent Supreme Court decisions are a step backward, hurt Black people: theGrio/KFF survey, published Oct. 30, 2022.

TheGrio/KFF survey shows that Black voters are concerned with voter suppression tactics, published Nov. 1, 2022.

Majority of Black voters support LGBT rights, more divided on the issue of trans student-athletes: theGrio/KFF survey, published Nov. 5, 2022.

Findings

Introduction

The Survey of Black Voters, the first under a new partnership between KFF and theGrio, examines the mood and opinions of an important group of voters as the 2022 midterm election approaches. A group that has historically been a solid voting bloc for Democrats, the views of Black voters are often examined as one monolithic group or even sometimes overlooked in midterm election polling. This survey goes beyond the insights that can be gleaned about Black voters from polls of the general public by collecting data from a large enough sample of Black voters to examine variations within the Black electorate by factors such as age, education, political affiliation, and ideology. The survey explores Black voters’ voting intentions, motivations, and views on key electoral issues for the upcoming midterm. It also examines Black voters’ attitudes toward the Democratic and Republican Parties, views on electoral integrity, and past experiences with voter suppression. In addition to these election-related topics, the survey sheds light on how Black voters feel about timely topics including recent Supreme Court decisions, policies affecting LGBT individuals, and policies aimed at improving health for Black people in the United States.

The survey sample is comprised of 1,000 Black adults who identify as Black or African American (including those who identify as Hispanic and/or multi-racial) and who say they are registered to vote.

Executive Summary

The survey reveals a Black electorate that is greatly concerned about the economy and the rising cost of living, but one that is weighing a variety of economic and non-economic issues in deciding how to vote in November. In addition to inflation and the affordability of health care and housing, voting rights, gun violence, and criminal justice emerge as top issues for Black voters.

About half of Black voters say they are more motivated to vote this year compared to previous elections, with those who are more motivated largely driven by a desire to vote for Democrats or keep Republicans out of office or a general desire for change. While substantial shares across groups express increased motivation this year, the shares are higher among older voters, those who approve of President Joe Biden, and those who lean toward one of the major parties, suggesting that larger shares of younger voters, unaffiliated Black voters, and those who disapprove of the president’s job performance may choose to stay home in November.

Black voters are also concerned about electoral integrity. While a large majority are at least somewhat confident that their own vote will be accurately counted in November, seven in ten are concerned about voter suppression interfering with a fair and accurate election in their state. Half say they have experienced waiting in long lines at their polling place in the past, and one in five have experienced potential voter suppression such as having their registration or identification questioned. Younger Black voters and those who have experienced potential voter suppression in the past are less confident that their vote will be accurately counted this November.

Black voters also express negative views of the Supreme Court. Eight in ten disapprove of the decision to overturn Roe v. Wade (higher than the share of White voters who say the same in other recent surveys), and most say the Court’s recent decisions have been a step backward when it comes to women’s rights, racial equity, climate change, and voting rights. Seven in ten believe the Court’s justices make their decisions mainly based on politics and ideology rather than the law.

The survey also finds that while Black voters continue to solidly identify with the Democratic party, there are some signs of disillusionment with the Democratic establishment. Black voters express a clear preference for the Democratic party over the Republican party when it comes to representing their interests, the parties’ commitment to electoral integrity, and views of racism in the parties. Still, less than a quarter of Black voters say the Democratic party represents their interests very well, and eight in ten say racism is at least a minor problem in the party.

In addition to these topics, the survey also explores more nuances in the attitudes of Black voters. While most Black voters identify as Democrat and hold largely liberal views, they are not a monolith. About one in four Black voters identify as independent, and 11% identify as or lean Republican. These groups express vastly different views from the majority who identify with or lean Democrat, especially on recent Supreme Court decisions, and gender and sexual identity issues. Views on other topics also differ among Black voters by factors such as age, gender, and education, as detailed in this report.

Who Are Black Voters?

Partisan identity: A large majority of Black registered voters either identify as Democrats (61%) or say they lean toward the Democratic Party (13%). About one in ten say they are Republicans (7%) or lean that way (4%). A further 13% of Black voters identify as independents or something else and say they don’t lean toward either the Democratic or Republican Party.

Ideology: About half of Black voters say their views in most political matters are moderate (54%), while 28% say they are liberal and 17% say conservative.

Age: Black voters are older on average than the Black adult population overall. About 1 in 5 (21%) Black voters are under the age of 30, slightly more than a third (36%) are between 30 and 49, a quarter (26%) are 50-64 and 18% are 65 or older.

Gender: Black voters are disproportionately women. A majority of Black voters (57%) are women, compared to about four in ten (42%) men.

Race and ethnicity: Nine in ten Black voters identify as Non-Hispanic Black, while 5% say they are Black and Hispanic or Latino, and a further 5% identify as non-Hispanic Black in addition to at least one other race.

How Do Black Voters View Biden, Harris, and Trump?

Approval of President Joe Biden: About seven in ten (69%) approve of the way Joe Biden is handling his job as president, while 30% disapprove. Biden’s approval rating is 59% among Black voters under age 50 compared to 82% among those ages 50 and older.

Approval of Vice President Kamala Harris: About two-thirds (65%) of Black voters approve of Kamala Harris’s handling of her job as vice president, while 33% disapprove. Harris’s approval rating differs by age as well (56% of those under age 50 approve vs. 77% of those ages 50 and older).

Views of Donald Trump: More than eight in ten (84%) Black voters have unfavorable views of former President Donald Trump, compared to just 15% who view him favorably. Black voters under age 50 are somewhat more likely than their older counterparts to have a favorable view of Trump (21% vs. 7%), though a large majority of both age groups (79% of those ages 18-49 and 91% of those ages 50 and over) view him unfavorably.

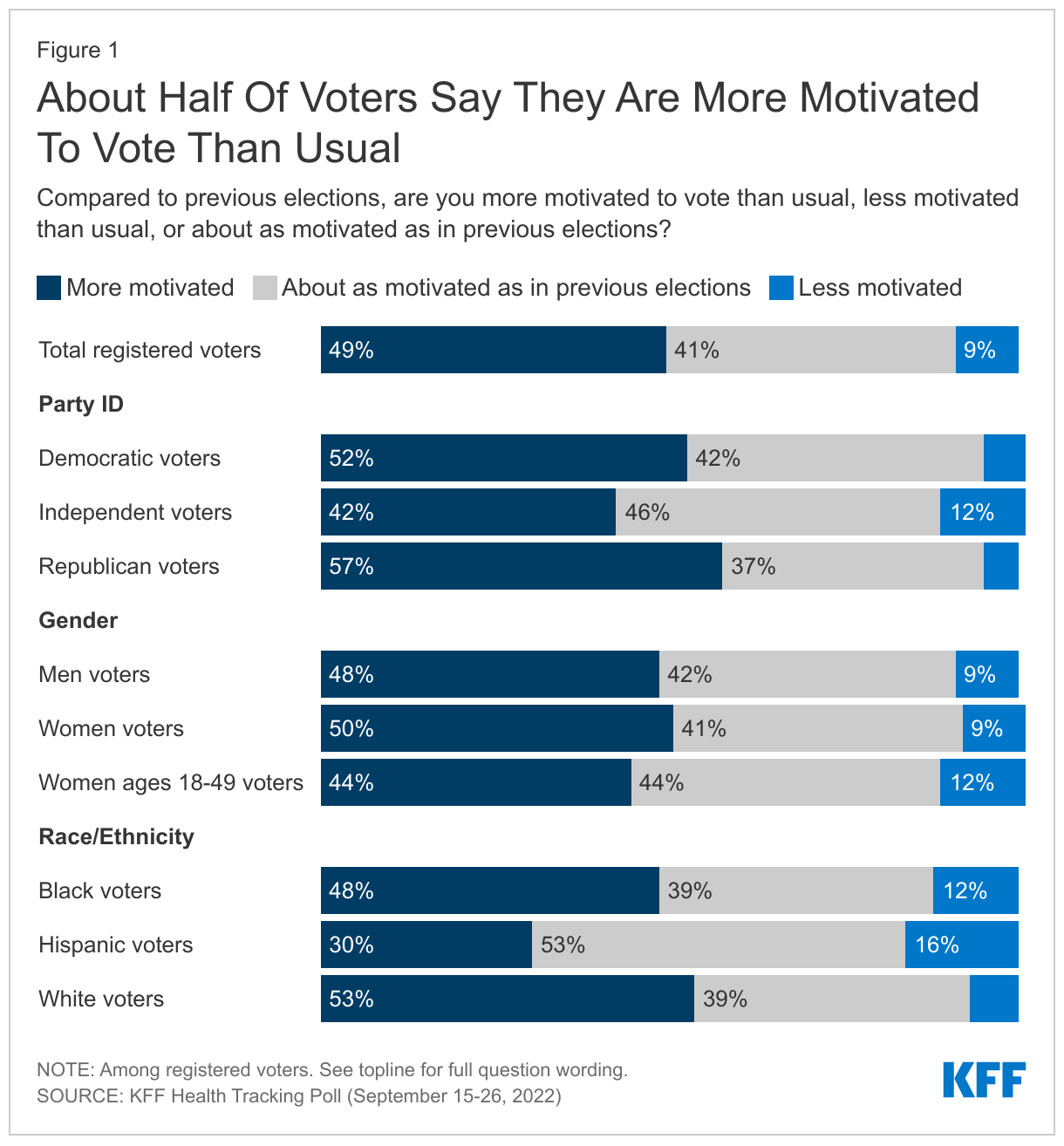

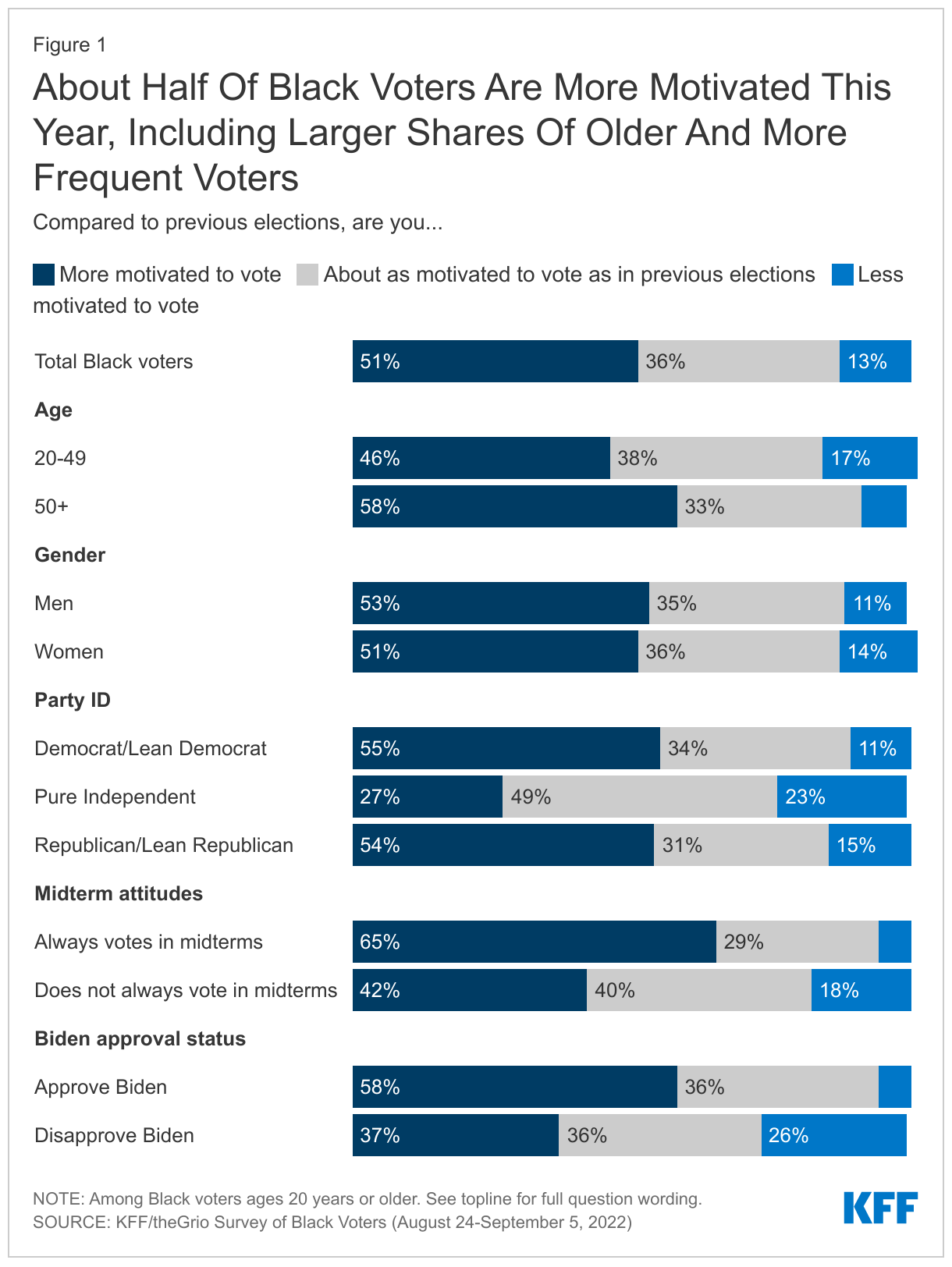

Half Of Black Voters Say They Are More Motivated to Vote This Year

Half (51%) of Black voters say they are more motivated to vote this year compared to previous elections, while 36% say they are about as motivated and 13% say they are less motivated to vote this year. The share of Black voters who say they are more motivated is similar to the share of White voters (53%) who said the same in another KFF survey fielded in September. Substantial shares of Black voters across groups say they are more motivated this year, but motivation is somewhat higher among older vs. younger Black voters (58% vs. 46%), among those who say they always vote in midterms vs. those who vote less often (65% vs. 42%), and among those who approve of Biden’s job performance vs. those who disapprove (58% vs. 37%). About half of both Black men voters and Black women voters say they are more motivated to vote this year, as do similar shares of those who identify as or lean Democrat and those who identify as or lean Republican. A much smaller share (27%) of those who say they are independent and don’t lean toward either party say they are more motivated to vote this year.

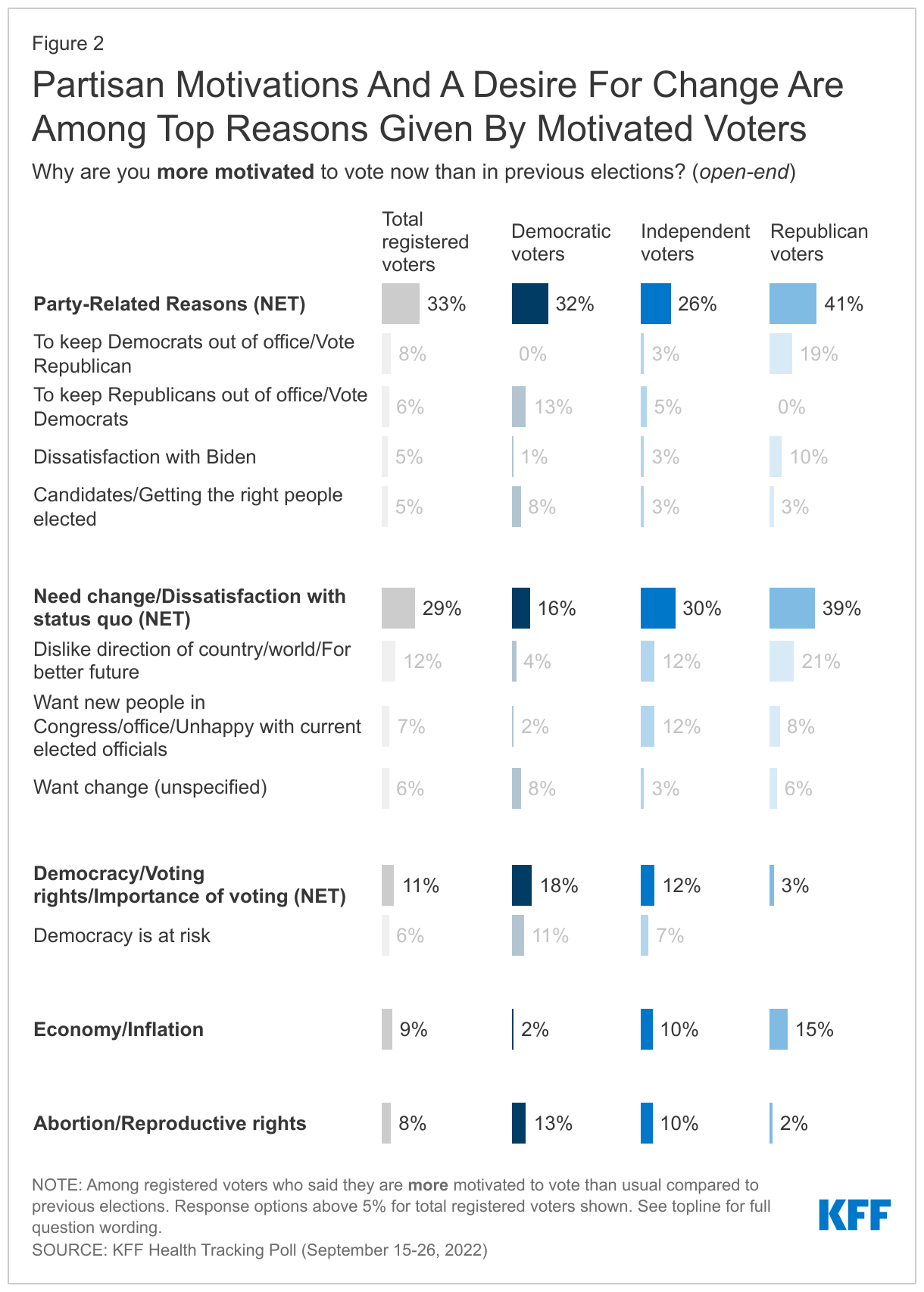

Black voters who are more motivated this year are largely driven by a desire to vote for Democrats or keep Republicans out of office or a general desire for change. Among the 51% of Black voters who say they are more motivated to vote this year compared to previous elections, 28% cite party-related reasons, such as a desire to elect Democrats or to keep Republicans and Trump supporters out of office, and 27% cite a desire for change or dissatisfaction with the status quo. About one in five cite specific issues (21%) or reasons related to democracy, voting rights, and the importance of voting (18%) for their greater motivation. Among the specific issues mentioned, 6% cite abortion rights and 5% cite economic issues as the source of their motivation.

Those who are less motivated largely say that they don’t think their vote will make a difference (22%), that they dislike the candidates (16%), or that they feel all politicians are dishonest (10%).

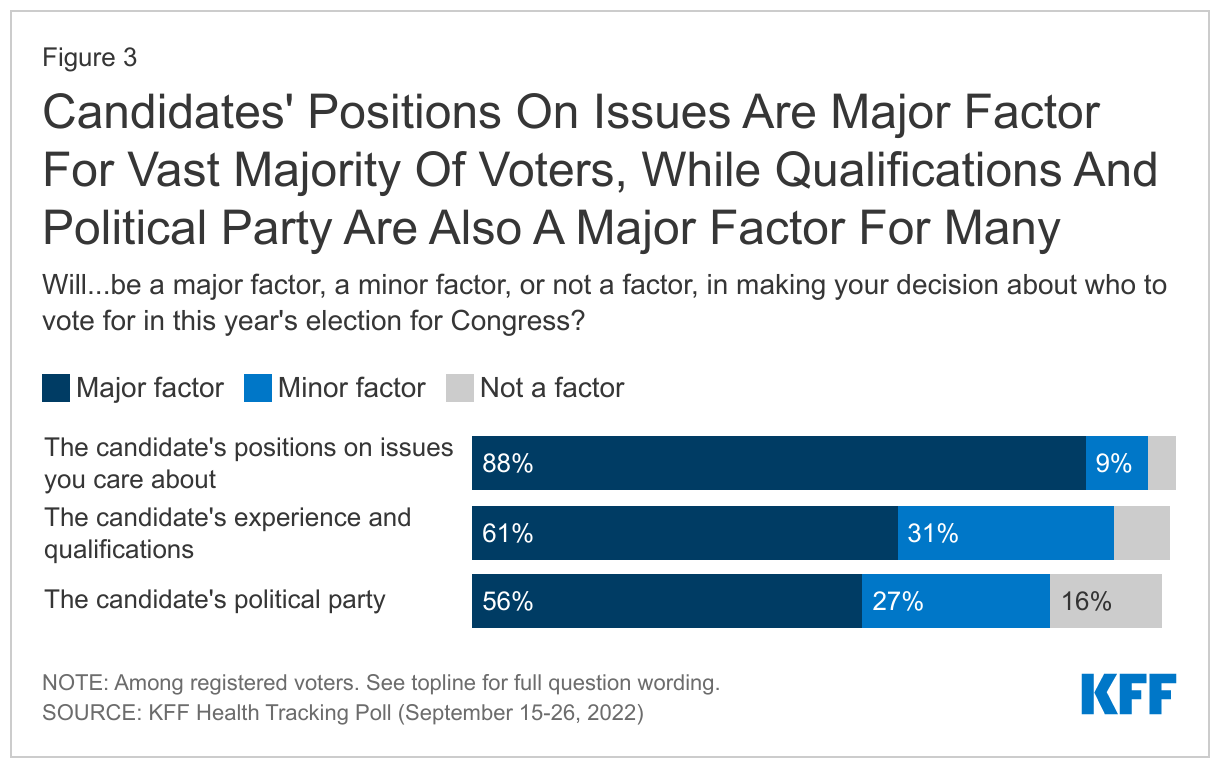

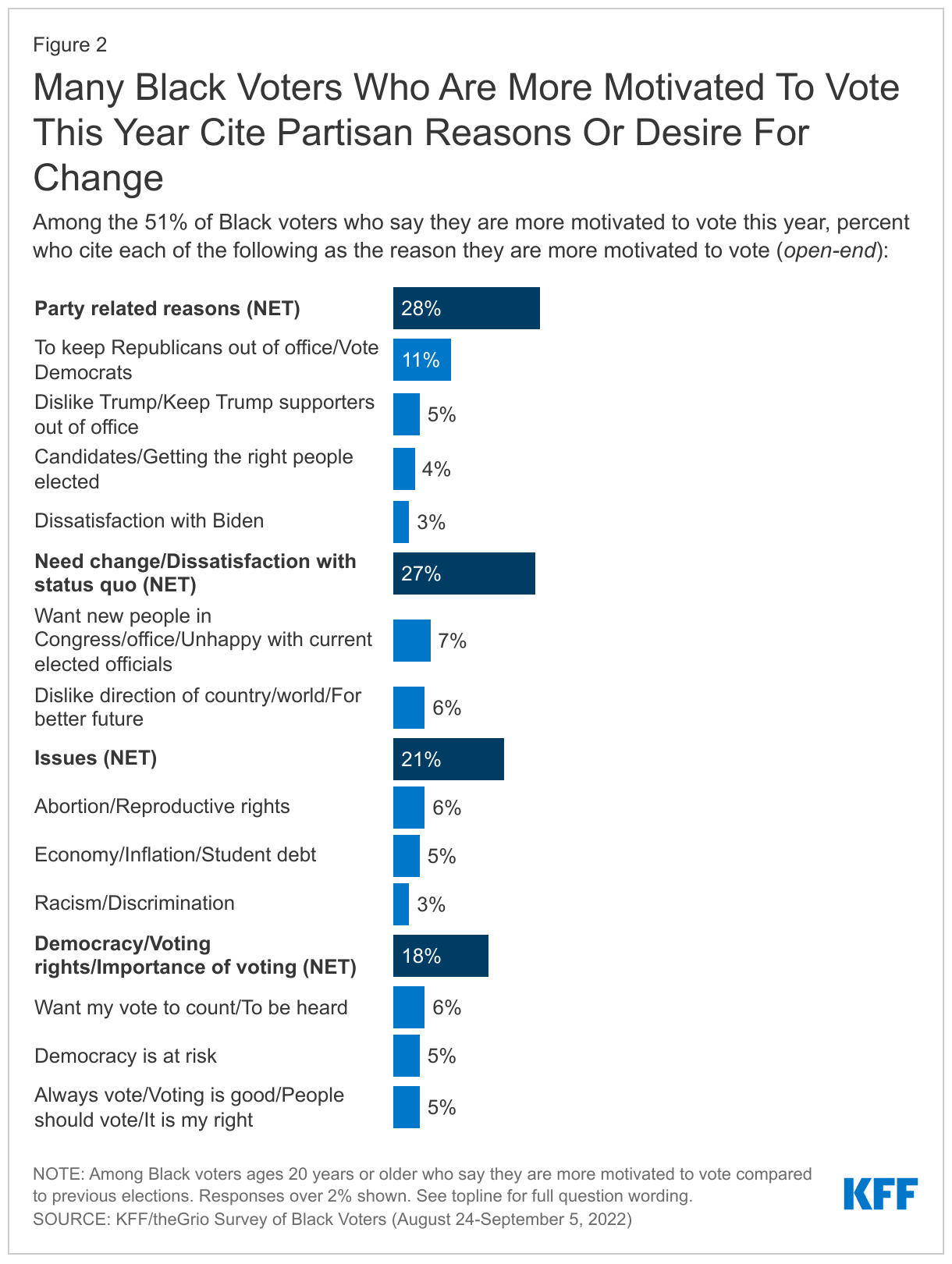

Majorities of Black voters say they consider candidate’s issue positions, character and experience, and political party when deciding how to vote, but fewer say a candidate’s race is a major factor. Large majorities of Black voters say that a candidate’s position on issues (86%) and character and experience (79%) are major factors in making their decision about how to vote for Congress this year, and a smaller majority (55%) say the same about the candidate’s political party. A much smaller share (21%) say a candidate’s race is a major factor in their decision.

Despite reporting they will consider many things beyond the candidate’s party, three-quarters (77%) of Black voters say that if the election were held at the time of the survey, they would be most likely to vote for the Democratic candidate for Congress in their district, while 11% say they would be more likely to vote for a Republican and another 11% for a candidate from another party.

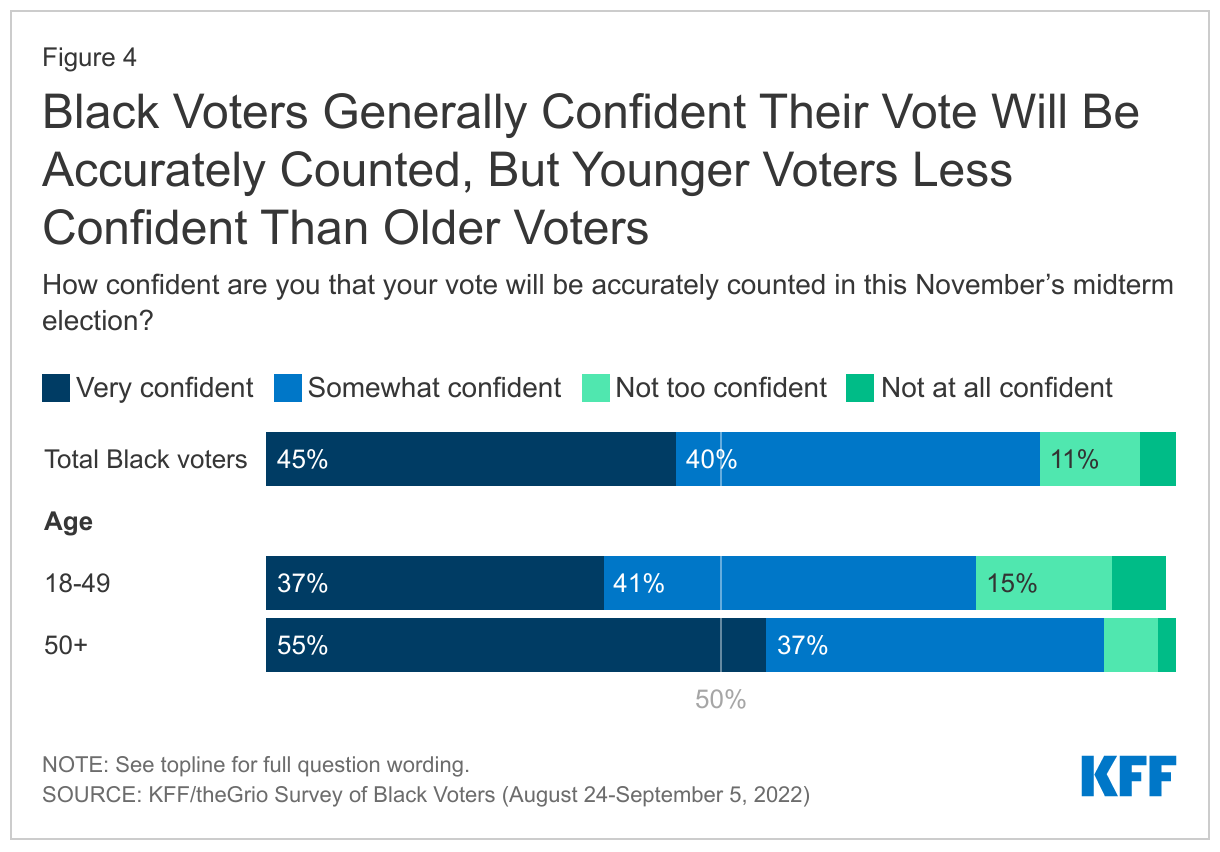

Black Voters Generally Confident Their Vote Will Be Counted, But Concerned About Voter Suppression

Black voters are generally confident that their vote will be accurately counted this November. A large majority (84%) of Black voters say they are at least “somewhat” confident their vote will be accurately counted in this November’s election, including more than four in ten (45%) who say they are very confident. However, younger voters under age 50 are less likely to feel very confident compared to their older counterparts (37% vs. 55%), and about one in five younger Black voters (22%) say they are “not too confident” or “not at all confident” that their vote will be counted accurately.

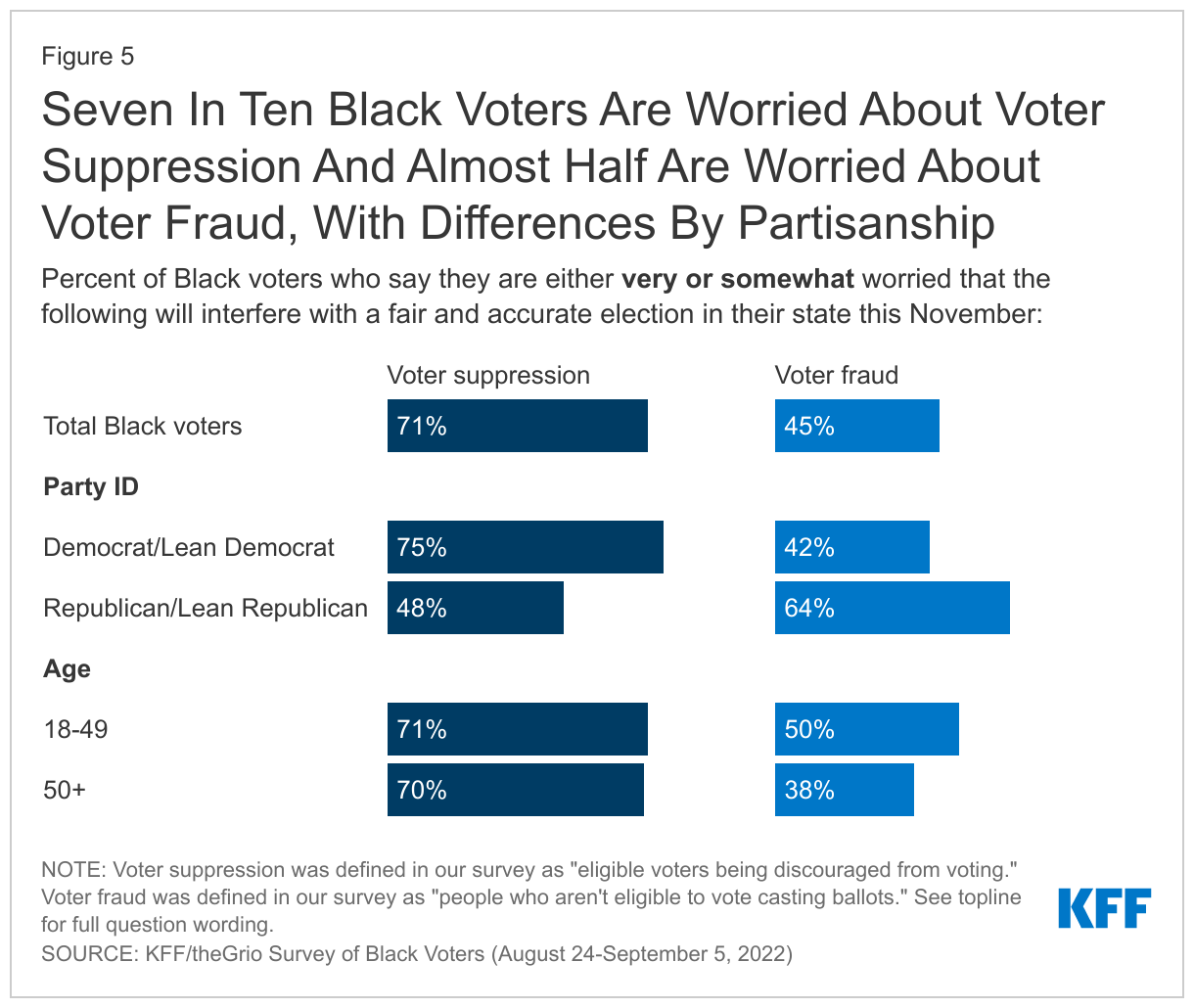

Seven in ten Black voters are worried about voter suppression and almost half are worried about voter fraud interfering with a fair and accurate election in their state this November. Three in four Black voters who are Democrat or lean Democrat say they are worried about voter suppression, compared to about half (48%) of their Republican counterparts. Conversely, Black voters who are Republican or lean toward the party (64%) are more likely than Black Democrats/leaners (42%) to say they are worried about voter fraud. Black voters of all ages are equally likely to express worry about voter suppression, but there is an age gap on concerns about fraud. Half of Black voters under age 50 say they are very or somewhat worried about voter fraud, compared to 38% of voters over 50.

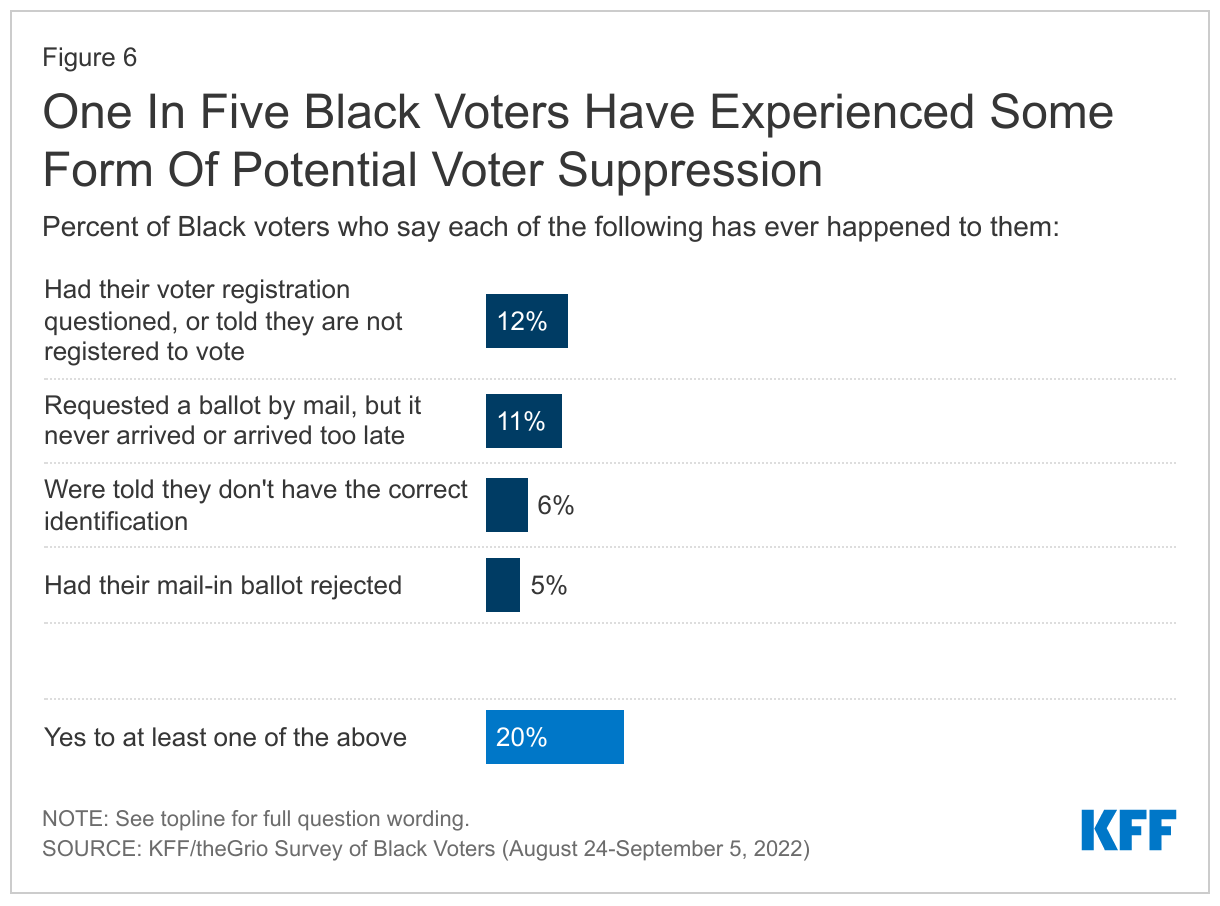

About half of Black voters say they have experienced waiting in long lines at their polling place, while one in five report experiencing acts of potential voter suppression, such as having their voter registration questioned. Nearly half (46%) of Black voters say they have experienced waiting in long lines at their polling place in the past. In addition, small but important shares report experiencing forms of potential voter suppression, including 12% who say they had their voter registration questioned, 11% who say they requested a mail-in ballot but it never arrived or arrived too late, 6% who were told they didn’t have the correct identification, and 5% who say they had their mail-in ballot rejected. Overall, one in five Black voters say they have experienced at least one of these things.

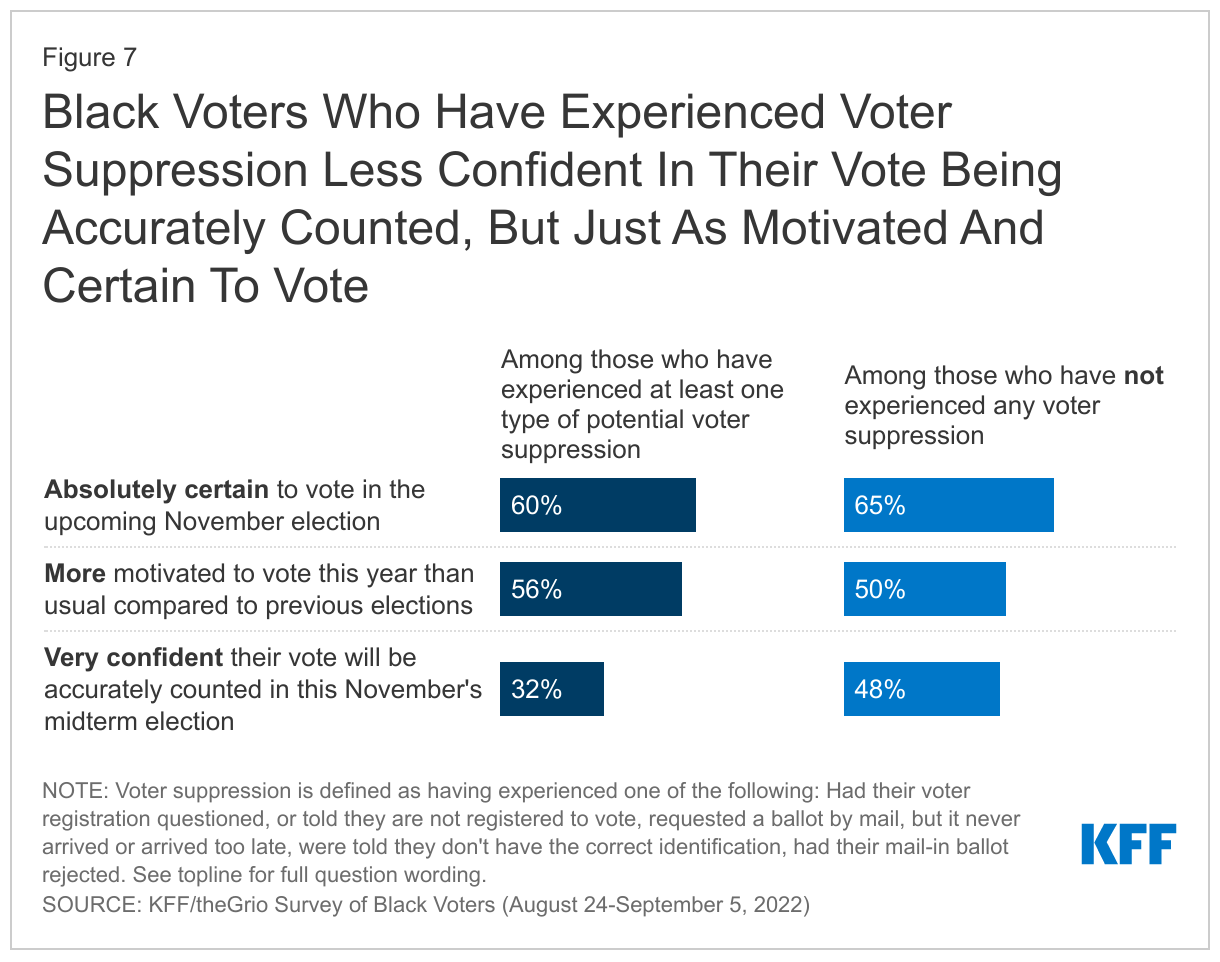

Experiences with potential voter suppression may impact Black voters’ confidence in the electoral process overall, though the survey does not suggest that it will decrease turnout this November. About a third (32%) of Black voters who have experienced potential voter suppression in the past say they are “very confident” their vote will be accurately counted this fall, compared to a larger share of those who have not experienced voter suppression (48%). However, at this point there is no evidence in the survey that these experiences will suppress turnout in November: these two groups are about equally likely to say they are absolutely certain to vote in the upcoming midterm (60% and 65%, respectively) and that they are more motivated to vote this year compared to previous elections (56% and 50%, respectively).

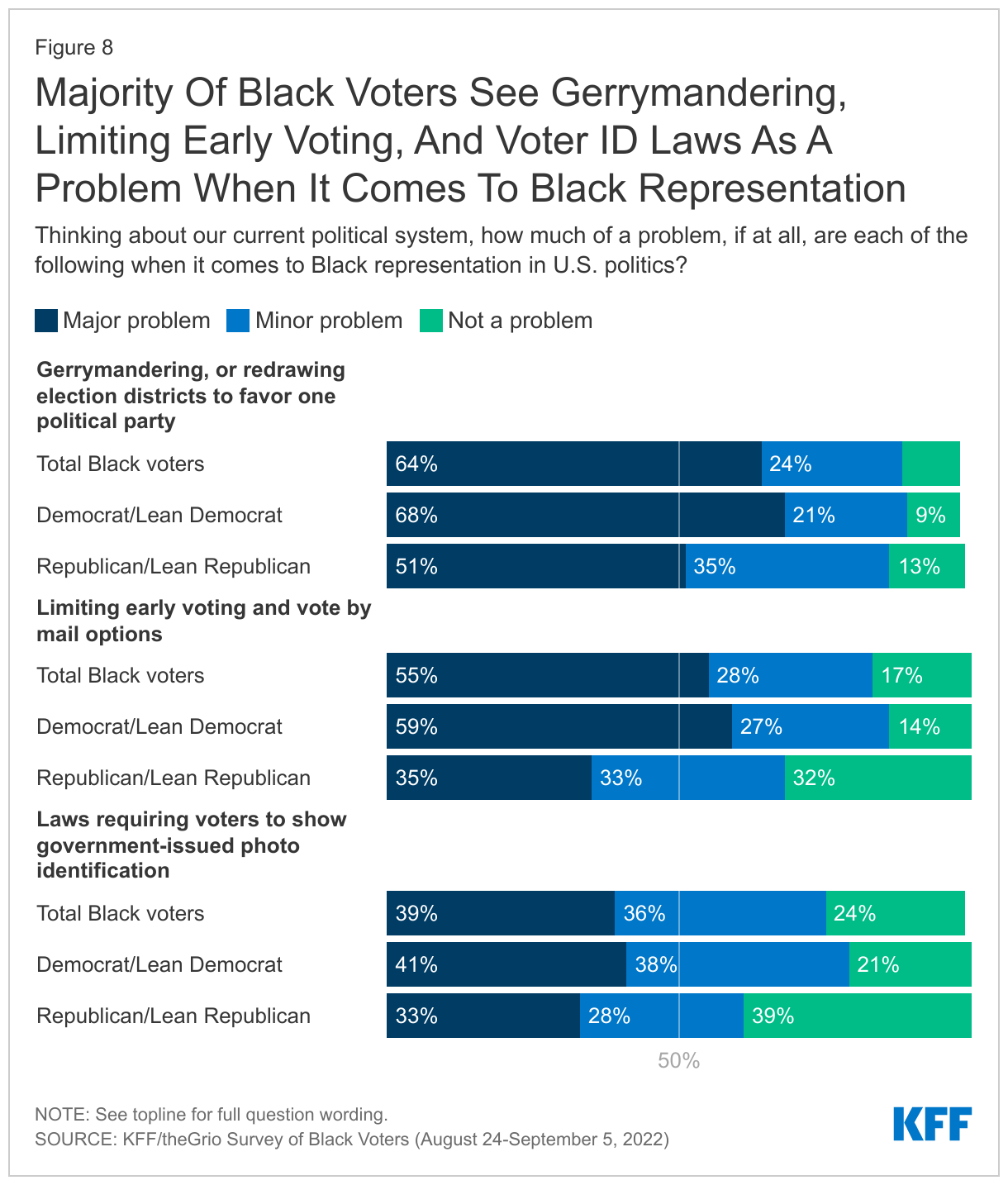

Majorities of Black voters say gerrymandering, limiting early voting, and voter ID laws are problems for Black representation in U.S. politics, with larger shares identifying gerrymandering and limiting early voting as major problems. Majorities of Black voters say these things are at least minor problems for Black representation in U.S. politics, with the largest share identifying gerrymandering as a major problem (64%), followed by limiting early voting (55%) and voter ID laws (39%). On all three issues polled, Black Democrats and those who lean Democratic are more likely to say these are problems than Republicans and those who lean toward the Republican party.

Economic Concerns Top Of Mind For Black Voters, But Non-Economic Issues Also Seen As Important In Voting Decisions

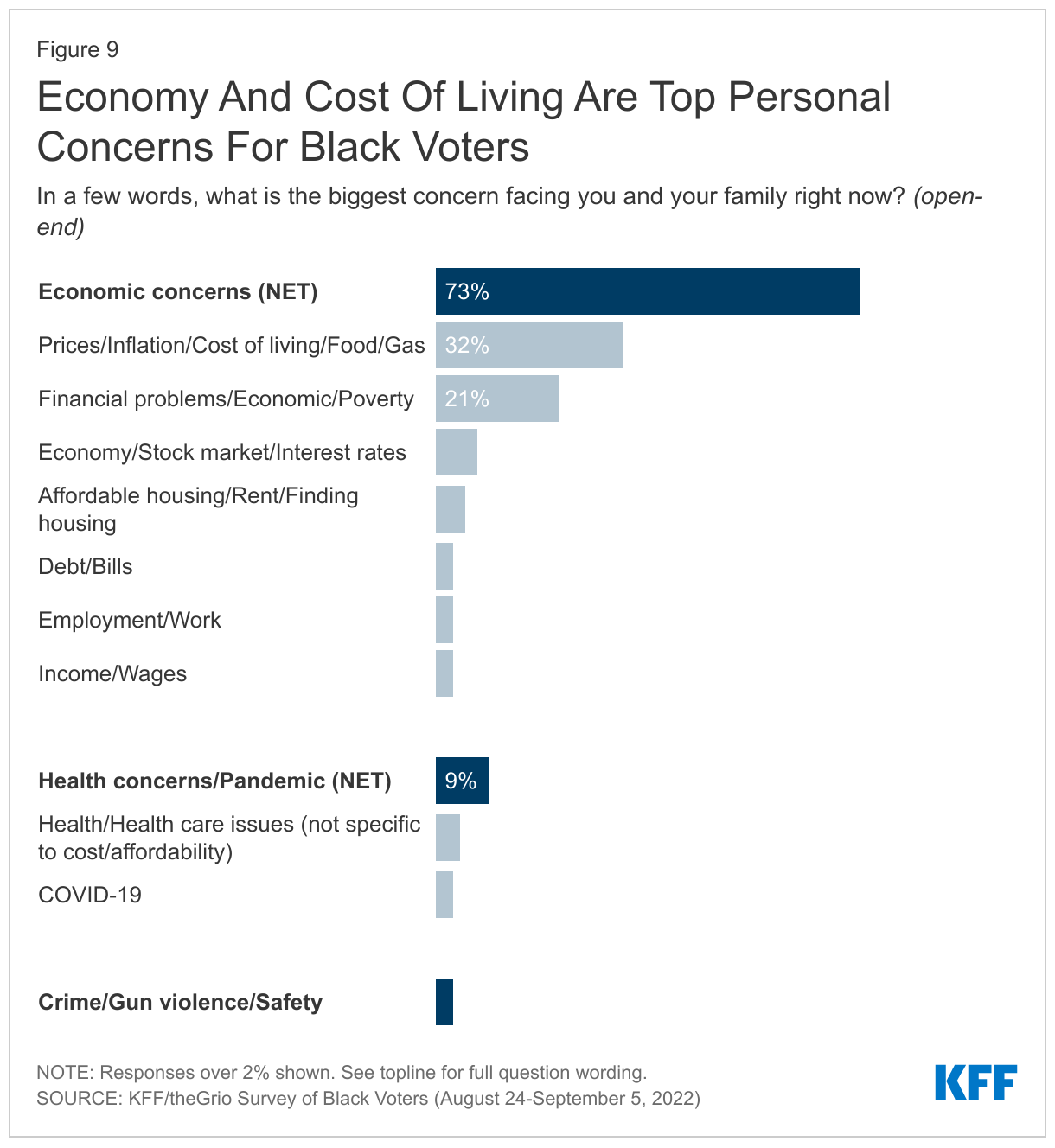

As the election approaches, economic issues loom large for Black voters and their families. When asked to state in their own words the top concern facing them and their families, about three in four (73%) Black voters point to economic concerns, including 32% who mention inflation and the cost of living and 21% who mention financial problems such as loss of income and making ends meet. Voters under age 65 are particularly likely to mention economic concerns (78% vs. 53% of those ages 65 and older), while a larger share of those ages 65 and older mention health concerns (17% vs. 7% of those under age 65). Crime, gun violence, and safety were raised by 3% of Black voters, while 2% named racism and racial disparities.

More broadly, at least six in ten Black voters say it’s a bad time to be a Black man (67%), a Black woman (62%), or a Black child (67%) in the US. Further, around eight in ten (81%) feel the economic system in the U.S. is stacked against people like them and a similar share say the same about the U.S. political system (79%).

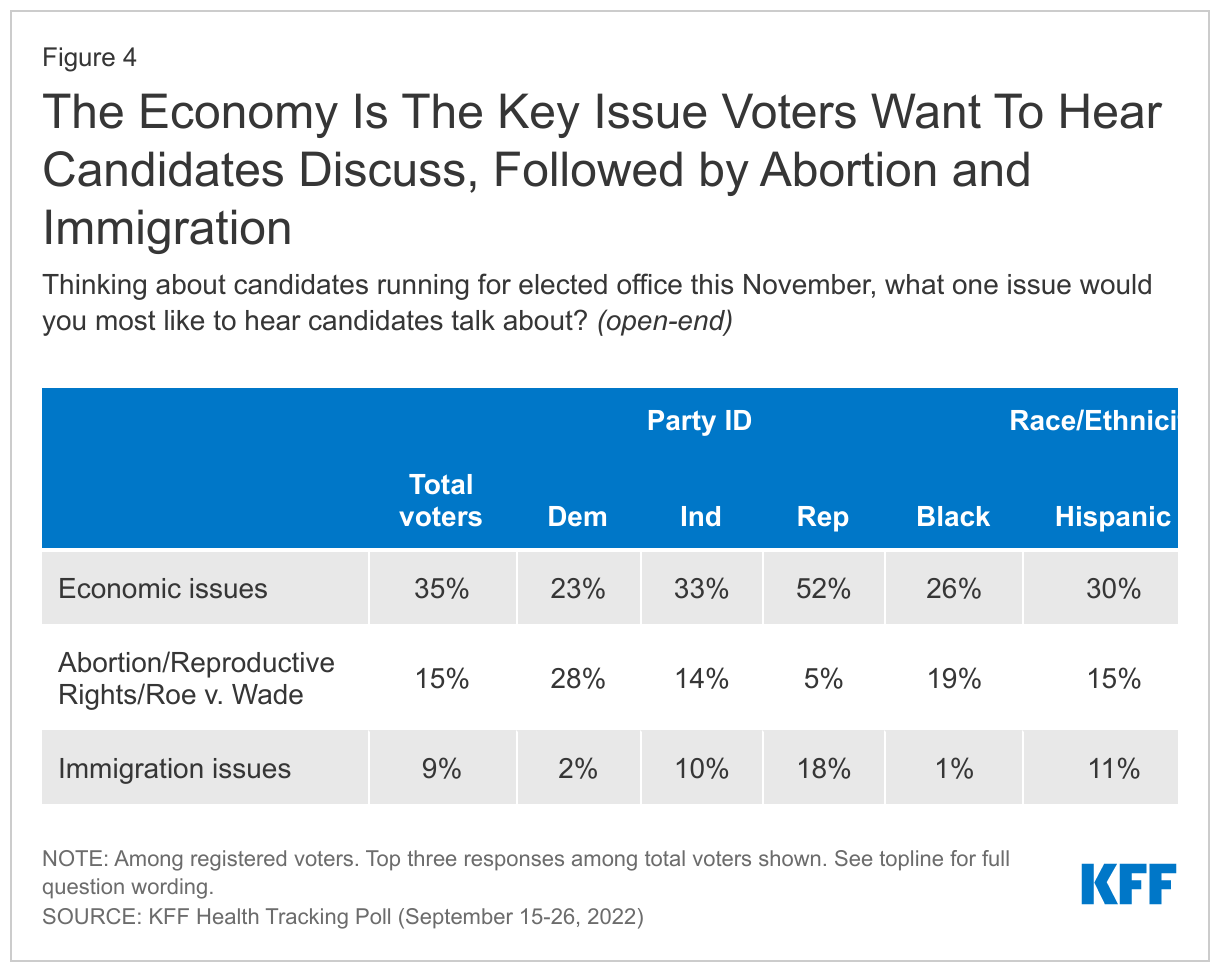

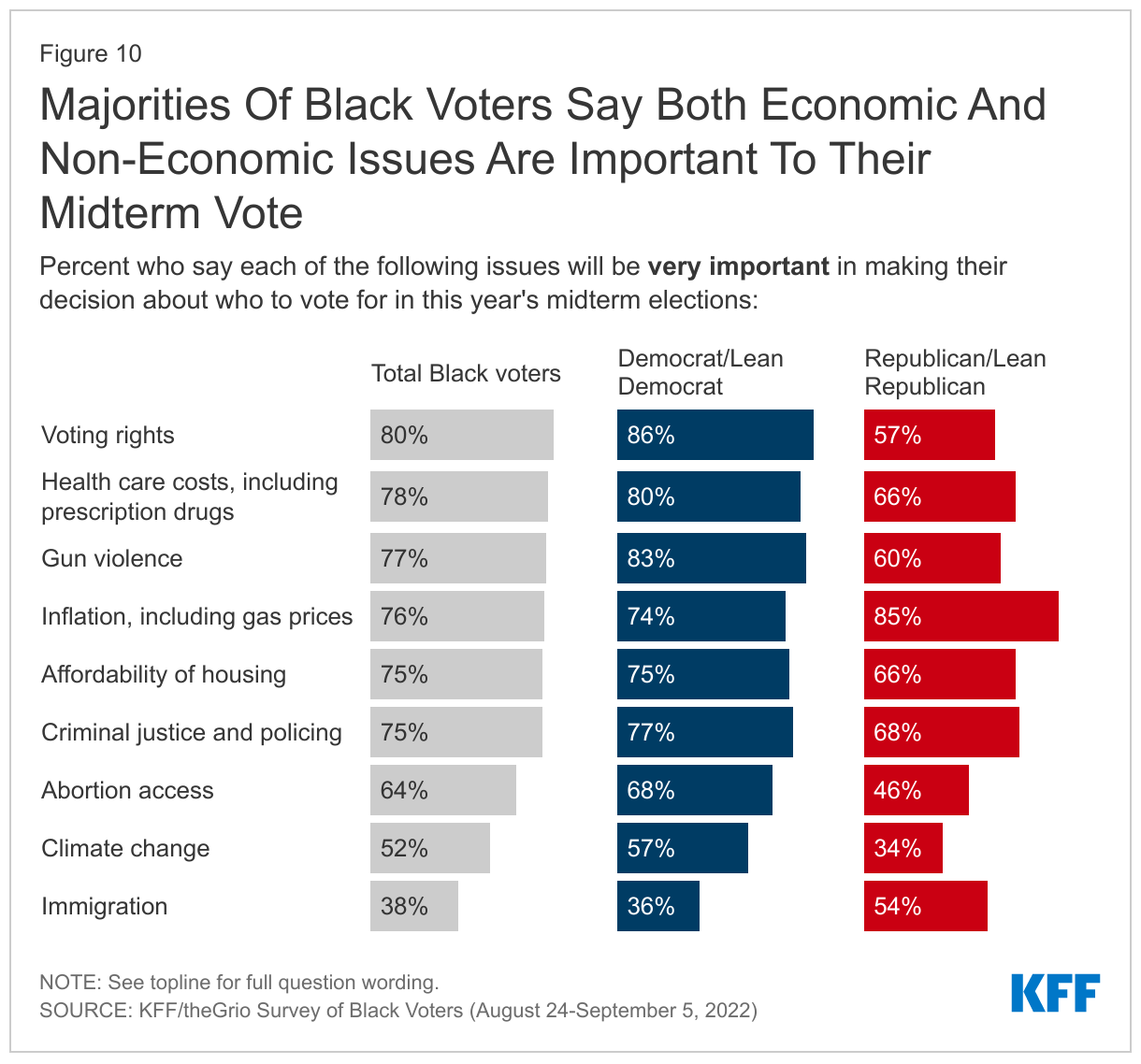

Black voters prioritize a variety of issues as very important to their midterm vote, including economic as well as non-economic issues. Black voters cite an array of issues as very important when considering who to vote for this fall, with no one issue taking the top spot. In a top tier, six issues are clustered together, each with three in four or more Black voters who say the following are very important to their midterm vote: voting rights (80%), health care costs (78%), gun violence (77%), inflation, including gas prices (76%), criminal justice and policing (75%), and the affordability of housing (75%). Ranking somewhat lower is abortion access (64%), followed by climate change (52%), and immigration (38%). Mirroring broader partisan differences in the population as a whole, Black voters who identify as Democrats or lean toward the Democratic party are more likely to cite voting rights, health care costs, gun violence, abortion access, and climate change as important issues in their vote; those who identify or lean Republican are more likely to prioritize inflation and immigration.

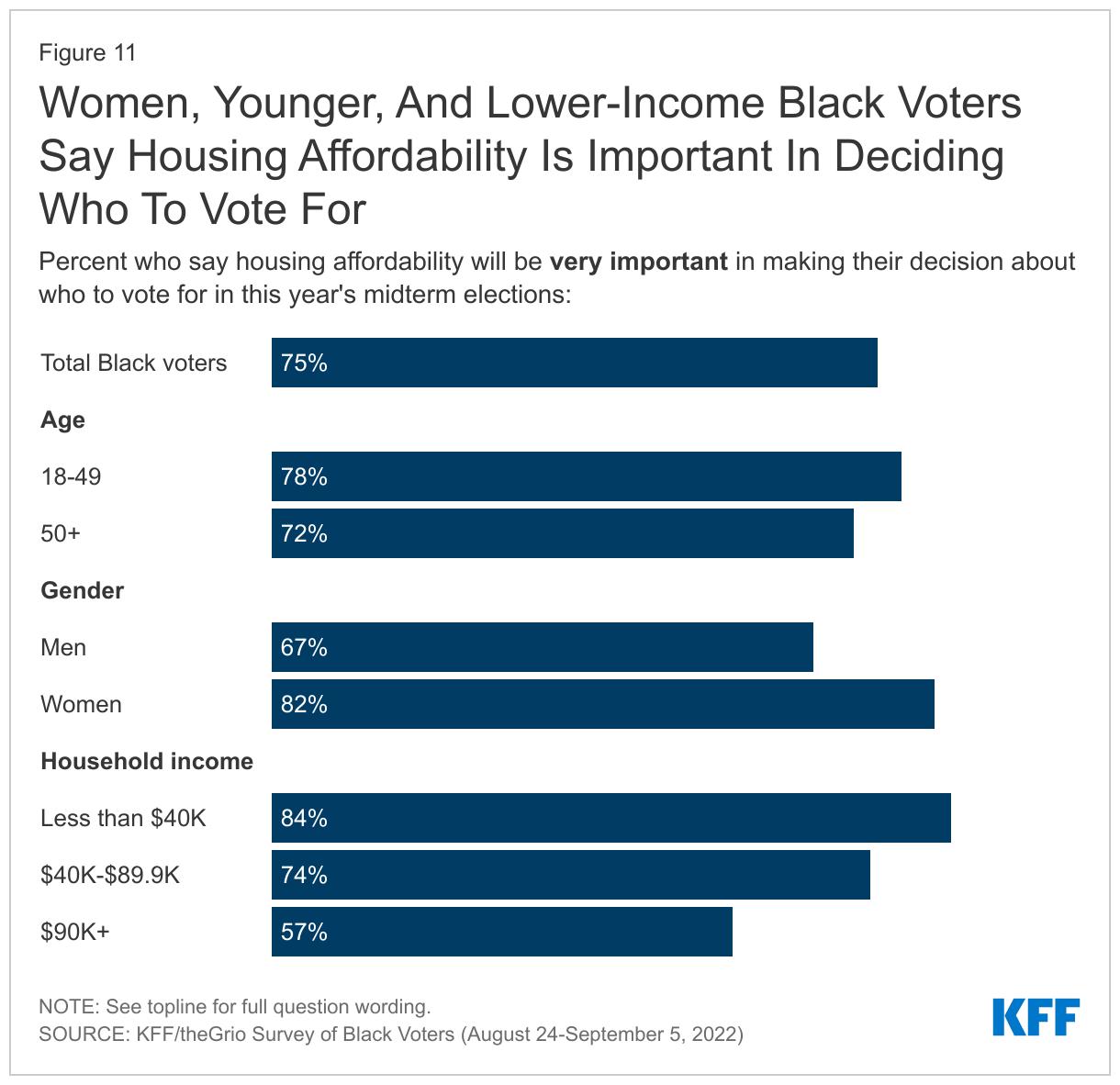

Housing affordability ranks higher as a voting issue for certain groups of Black voters, including women, younger voters, and those with lower incomes. Housing affordability is a top issue for lower-income Black voters, with 84% of voters with incomes under $40,000 saying it is very important to their vote, compared to 57% of those with incomes of $90,000 or more. The cost of housing is also named as an important voting issue by a larger share of younger voters compared to older Black voters (78% of those under age 50 vs. 72% of those 50 and older) and for Black women compared to men (82% vs. 67%).

Gender is an important divide on other issues as well. Beyond housing affordability, Black women voters are more likely than Black men voters to say certain issues are very important to their vote, including health care costs (83% vs. 73%), gun violence (84% vs. 69%), inflation (79% vs. 71%), and abortion access (68% vs. 58%).

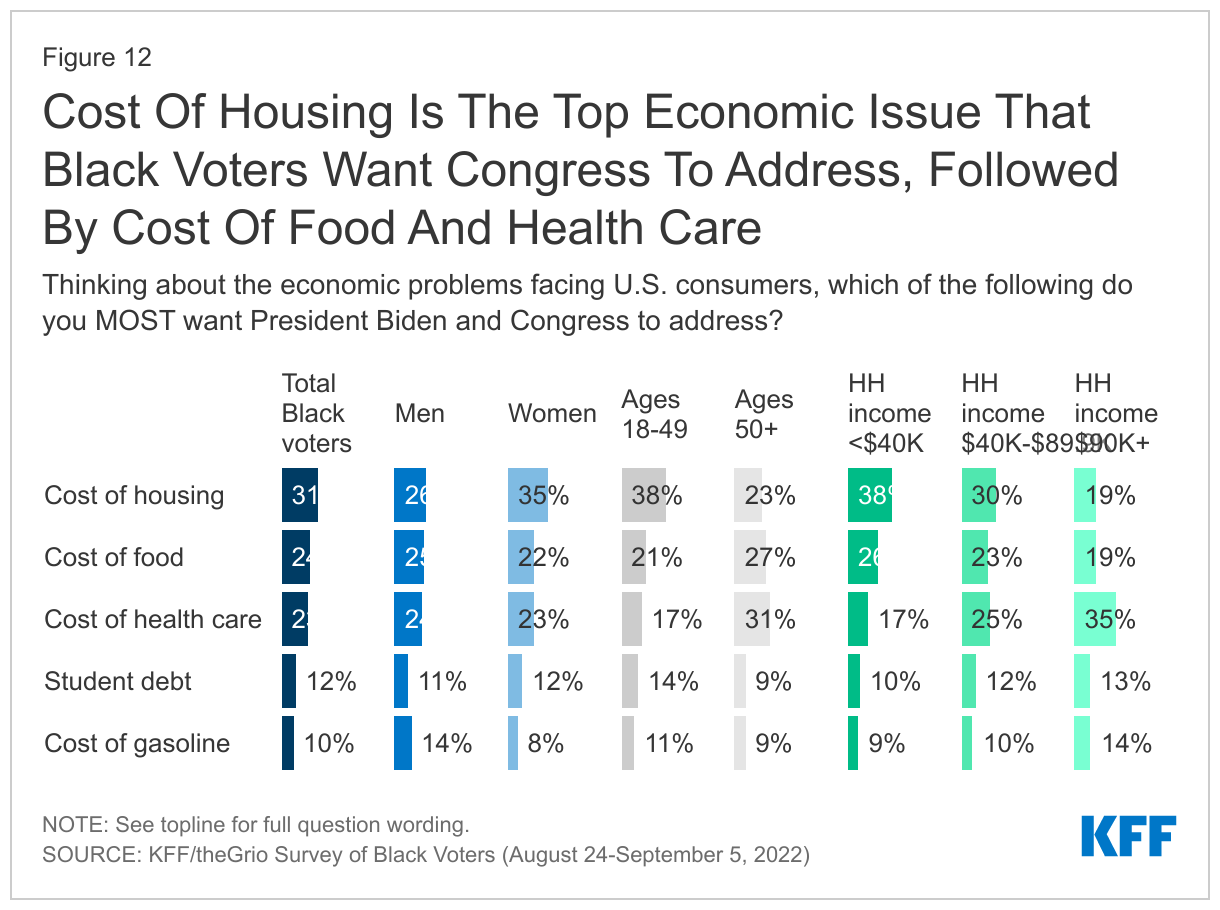

When asked about economic issues they would most like Biden and Congress to address, Black voters focus on basics like food and housing as well as the cost of health care. Of the issues polled, the cost of housing is a top concern for Black voters, with about three in ten (31%) saying it is the economic issue facing U.S. consumers they most want the President and Congress to address, including higher shares of women, younger voters, and those with lower incomes. About a quarter cite other necessities like the cost of food and health care, respectively.

In a sharp turnaround from early this summer, when gas prices were at their peak and the cost of gasoline took the top spot in a KFF poll of all adults, the cost of gas now ranks lower as a priority among Black voters.1 One in ten Black voters now cite the cost of gasoline as the economic problem they most want the President and Congress to address, while a similar share (12%) cites student debt.2

Black Voters Express Negative Views Of The Supreme Court

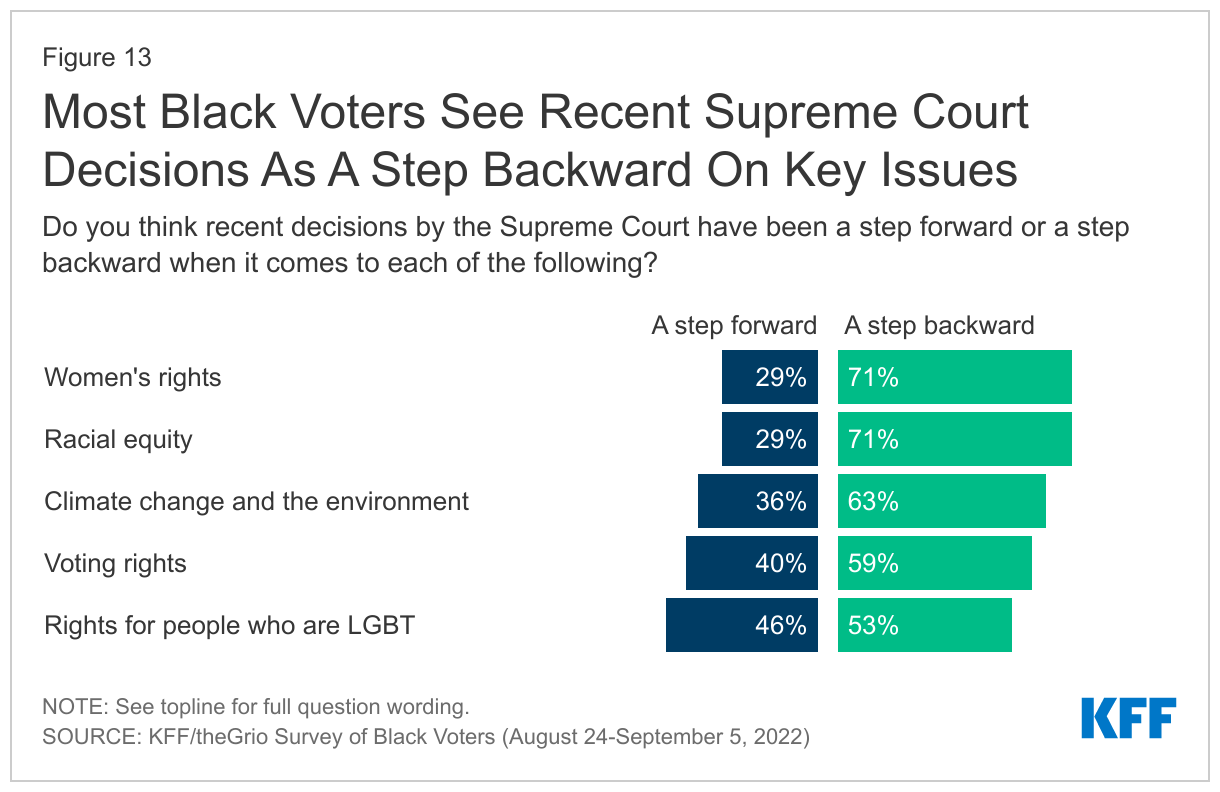

Most Black voters say recent Supreme Court decisions are a step backward when it comes to women’s rights, racial equality, climate change, and voting rights. About seven in ten Black voters say recent Supreme Court decisions have been a step backward on women’s rights (71%) and racial equity (71%), while about six in ten say the same about climate change (63%) and voting rights (59%). Black voters are more divided on the impact of recent Court decisions on LGBT rights, about half (53%) see the decisions as a step backward and nearly as many (46%) seeing a step forward.

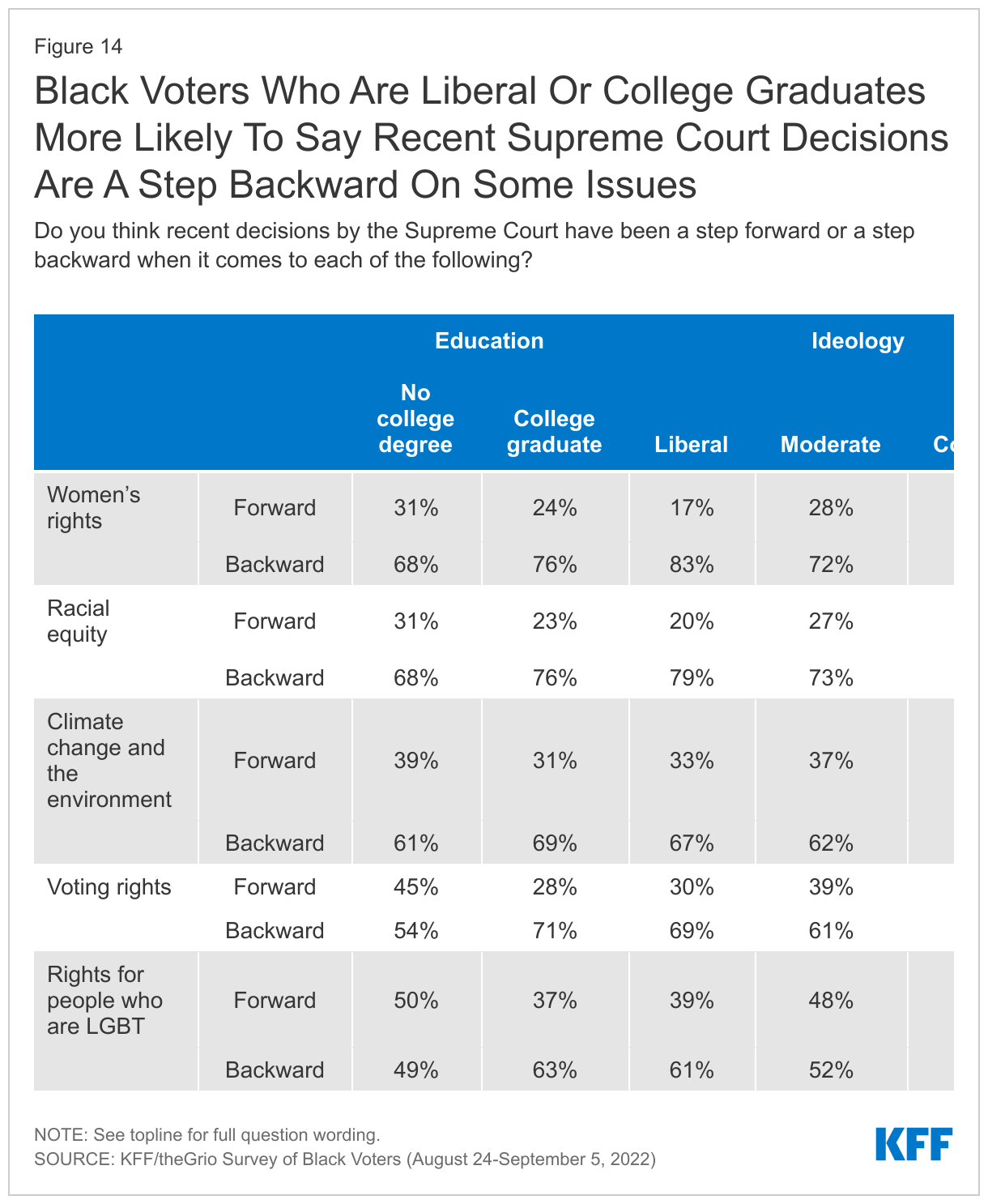

Black voters who identify as Evangelical Christians, conservatives, and those who are Republican or lean toward the Republican party are more likely to say the recent decisions are a step forward on most of the issues asked. And Black voters who are college graduates are more likely than non-graduates to see recent decisions as a step backward on each of the topics polled.

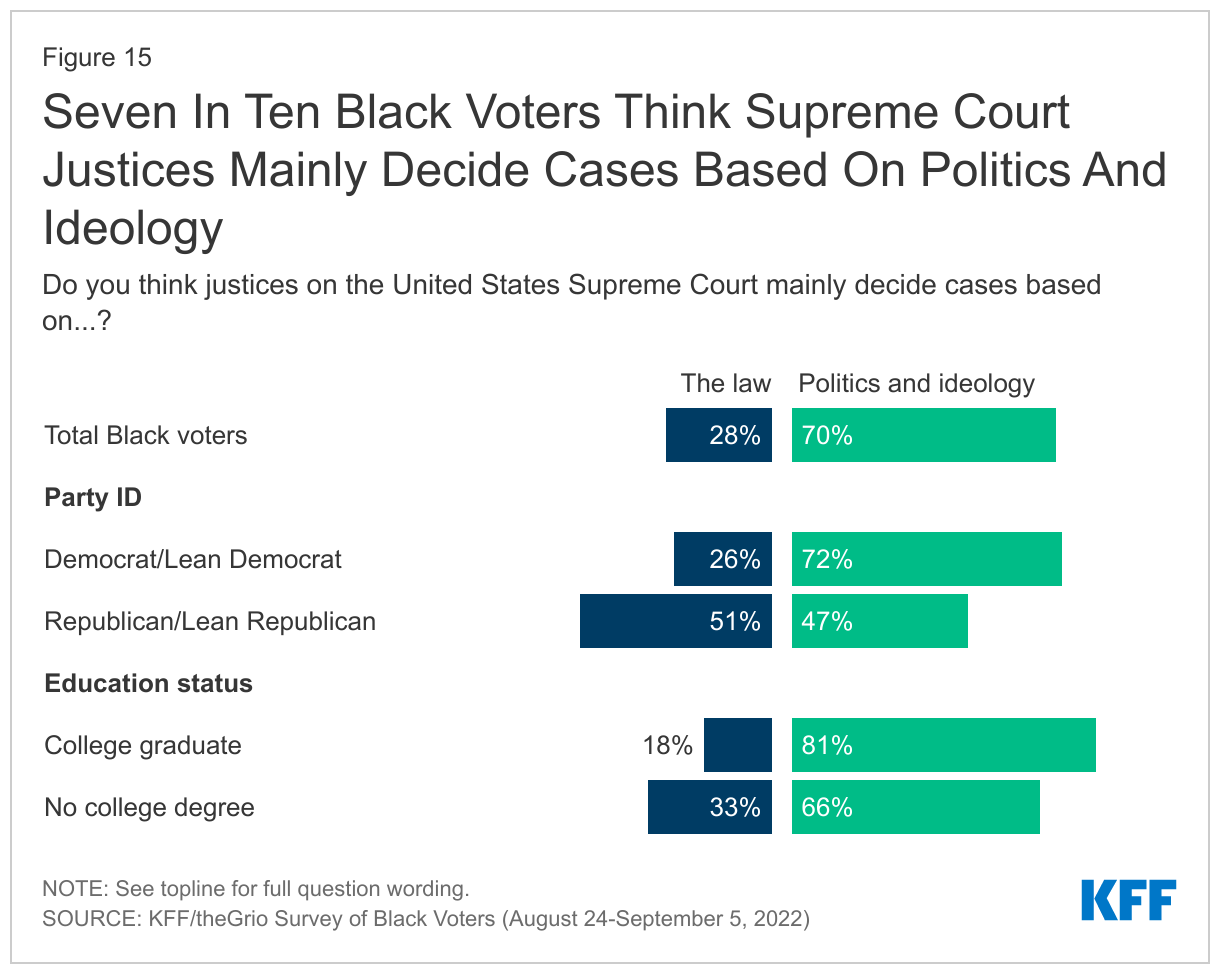

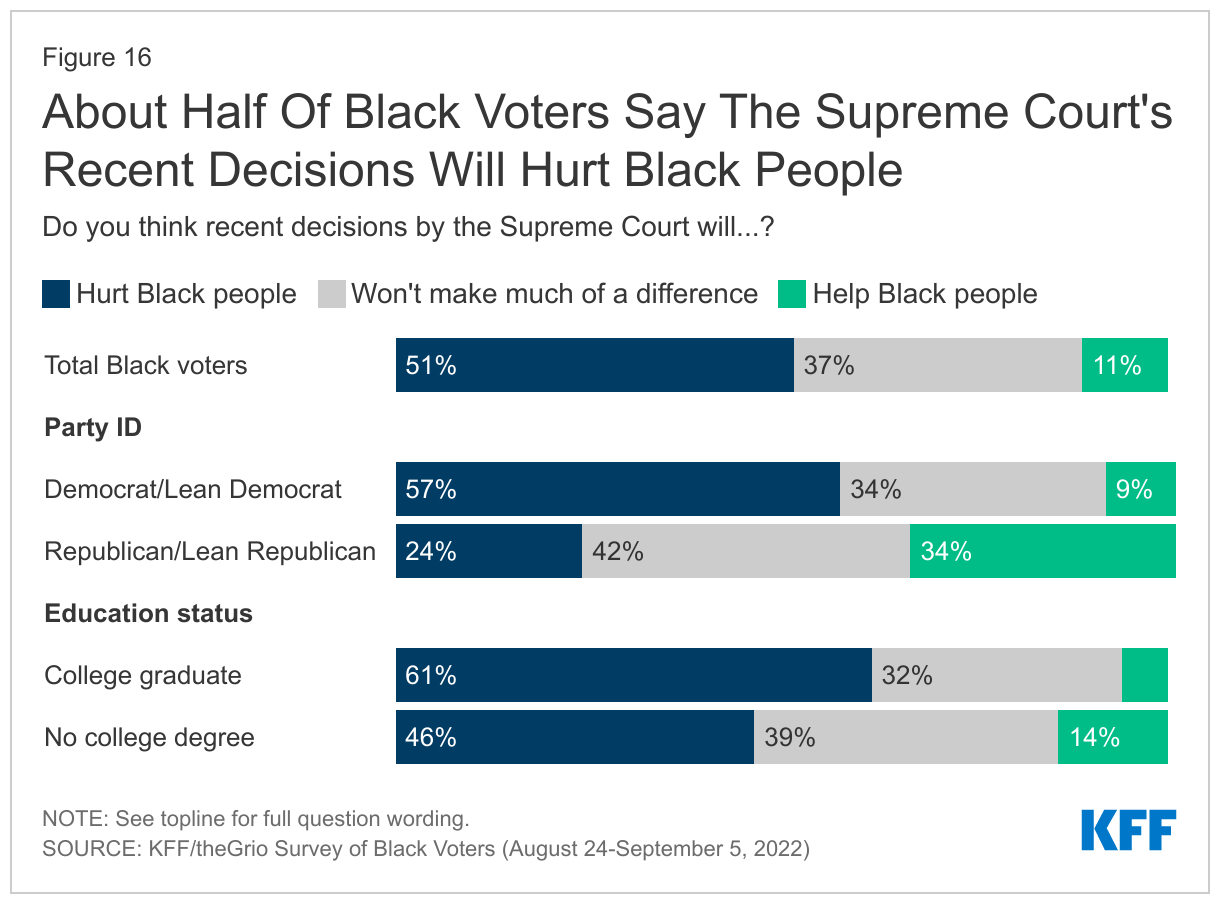

A large majority of Black voters believe that Supreme Court justices decide cases based on politics and ideology rather than the law, and about half of Black voters say recent Court decisions will directly hurt Black people. Seven in ten Black voters believe Supreme Court justices decide cases mainly based on politics and ideology rather than the law. The majority of Black Democrats and those who lean Democrat (72%) think decisions are based on politics and ideology, but Republicans and Republican leaners are more split: 51% say decisions are made on the law, while 47% say they are made on politics and ideology.

When asked more directly about the impact of recent Court decisions on Black people, 51% of Black voters say recent decisions will hurt Black people, 11% say they will help, and 37% say they won’t make much of a difference.

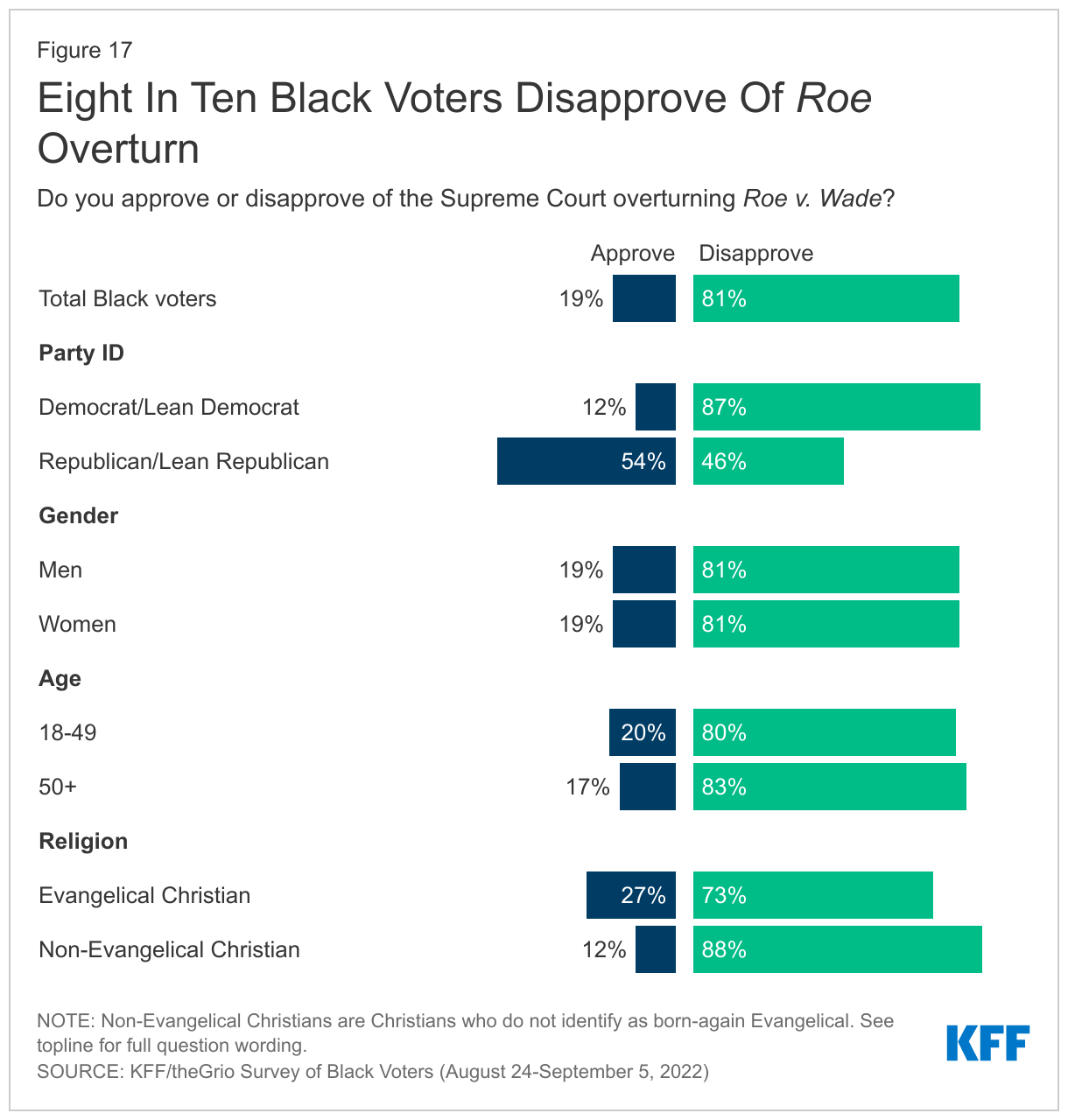

Eight in ten Black voters disapprove of the Supreme Court’s decision to overturn Roe v. Wade (81%). This share is similar across gender, age, education, and income groups. Black voters who identify as Republicans or lean toward the party are the only group that is more split on the decision, with about half (54%) approving and the other half disapproving (46%). About a quarter (27%) of Black voters who identify as Evangelical Christians approve of the overturn of Roe, far fewer compared to White Evangelicals (72%) as measured in a KFF survey of all adults in September. The same survey also found that Black voters are more likely to disapprove of the Roe overturn than are Hispanic voters (67%) and White voters (57%).

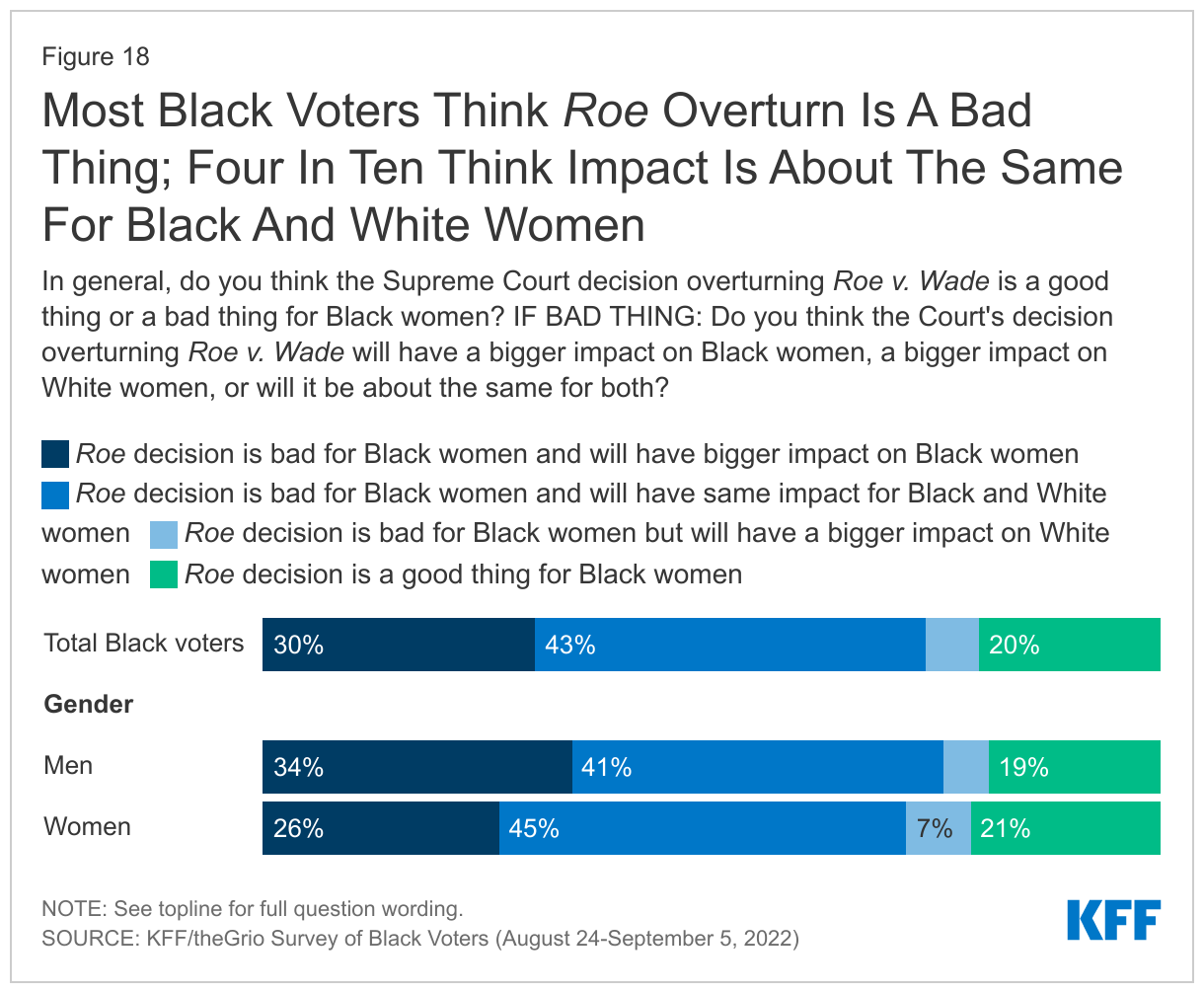

Most Black voters see the Court’s overturn as a bad thing for Black women, but a smaller share believes the Roe overturn will have a disproportionate impact on Black women compared to White women. Nearly eight in ten (79%) of Black voters say the decision to overturn Roe is a bad thing for Black women. However, most don’t see the decision disproportionately impacting Black women: 30% say the decision will have a bigger negative impact on Black women compared to White women, while 43% say the negative impact will be about the same for both groups. Black men are slightly more likely than Black women to say the decision will have a bigger negative impact on Black women than White women (34% vs. 26%), while almost half (45%) of Black women say the negative impact will be the same for both Black and White women.

Six In Ten Black Voters Say Congress Should Prioritize Policies To Improve Health Care For Black People

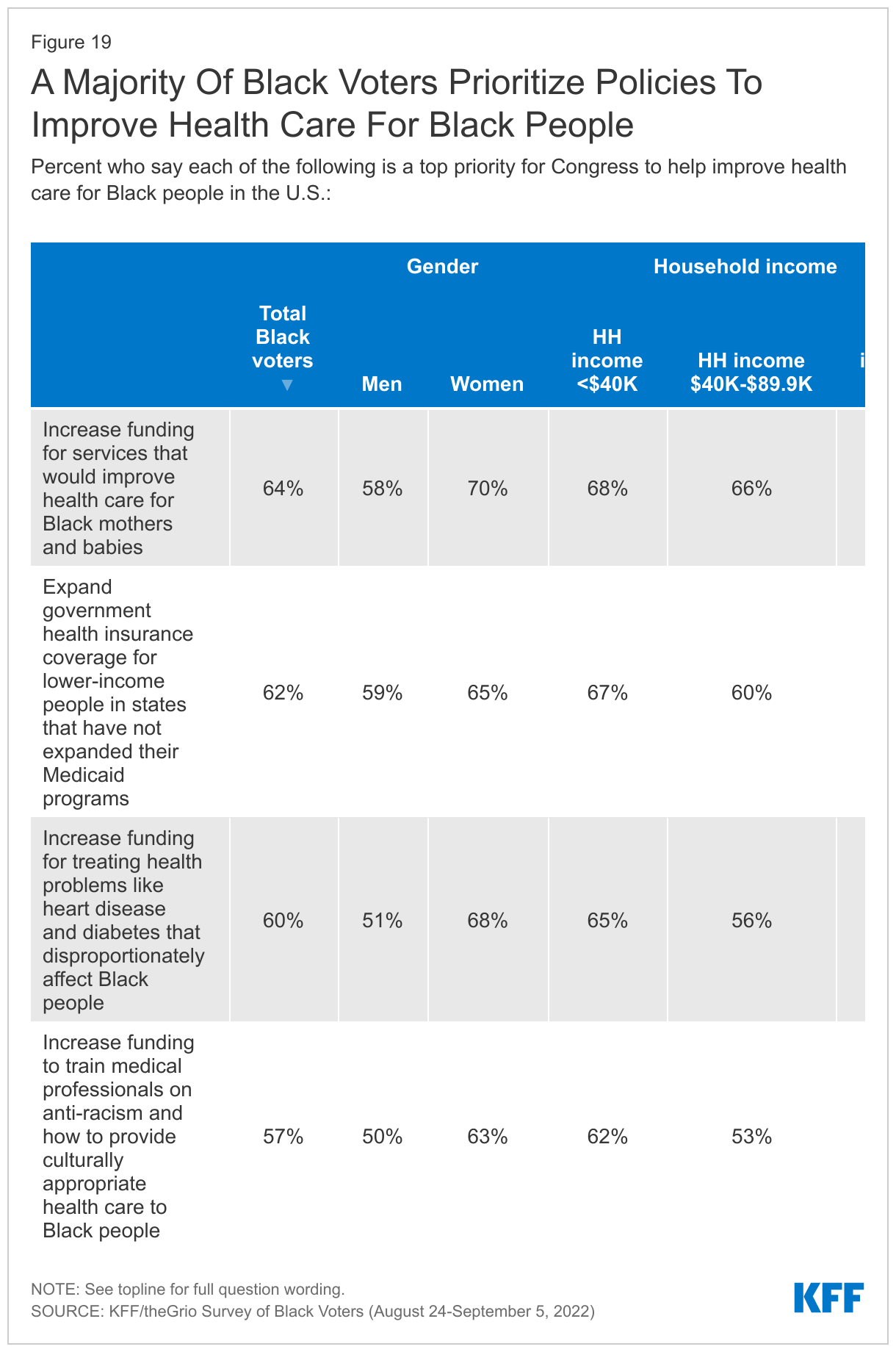

When asked about various things Congress could do to help improve health care for Black people in the US, Black voters prioritize many potential policies, with about six in ten saying each option polled should be a top priority. Nearly two-thirds (64%) of Black voters say increasing funding for services that would improve health care for Black mothers and babies is a top priority. About six in ten prioritize expanding government health insurance for lower-income people in states that have not expanded their Medicaid programs (62%) as well as increasing funding for treating health problems like heart disease and diabetes that disproportionately affect Black people (60%). A similar share (57%) also say it should be a top priority for Congress to increase funding to train medical professionals on anti-racism and how to provide culturally appropriate health care to Black people.

On many of these issues, Black women voters and those with lower incomes are particularly likely to see each of these as top priorities for Congress. Larger shares of Black women than Black men voters say increasing funding for services that would improve health care for Black mothers and babies (70% vs. 58%), increasing funding for health problems that disproportionately affect Black people (68% vs. 51%), and training medical professionals on anti-racism and culturally appropriate care (63% vs. 50%) should be top priorities for Congress.

Black voters with household incomes of less than $40,000 a year are more likely than those with incomes of $90,000 or more to say Congress should prioritize increasing funding for services to improve health care for Black mothers and babies (68% vs. 52%). There is a similar gap in the share of lower-income and higher-income Black voters who say it should be a top priority for Congress to expand government health insurance coverage for lower-income people in states that have not expanded their Medicaid programs (67% vs. 54%).

Views On Gender And Sexual Identity Issues

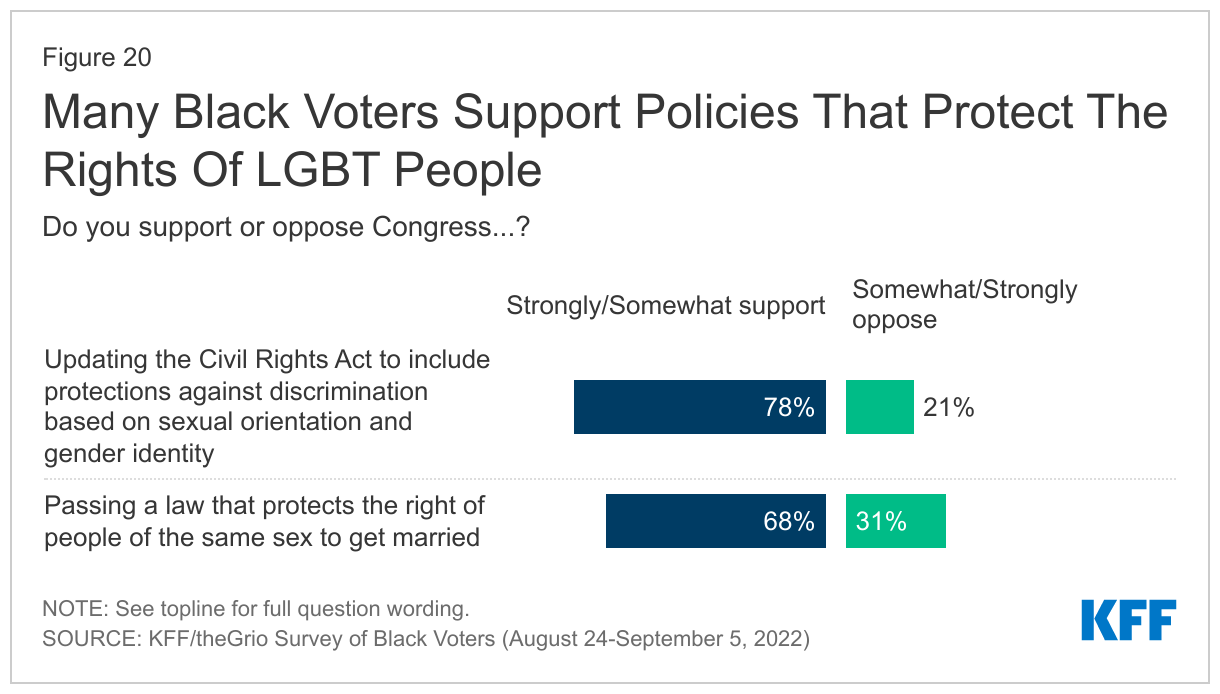

In general, Black voters are supportive of policies that protect the rights of LGBT individuals, with more support among younger voters, those who identify as liberal, and those who themselves identify as LGBT. A large majority (78%) of Black voters support Congress updating the Civil Rights Act to include protections against discrimination based on sexual orientation and gender identity, including large majorities across age groups, and 93% of Black voters who identify as LGBT. Nine in ten liberal Black voters support updating the Civil Rights Act in this way (89%), but a majority (58%) of those who identify as conservatives do as well.

Same sex marriage also garners solid support among Black voters, with more than two in three (68%) saying they support Congress passing a law to protect same sex marriage (including 44% who say they strongly support this measure). About nine in ten (93%) Black voters who identify as LGBT support protecting same sex marriage. Support differs by age among all Black voters, with nearly eight in ten (78%) Black voters ages 18-29 saying they support this compared to a narrower majority (55%) of those ages 65 and older. On this topic, about eight in ten (83%) liberal Black voters are in support, but conservative Black voters are split: 49% support it, while 51% oppose.

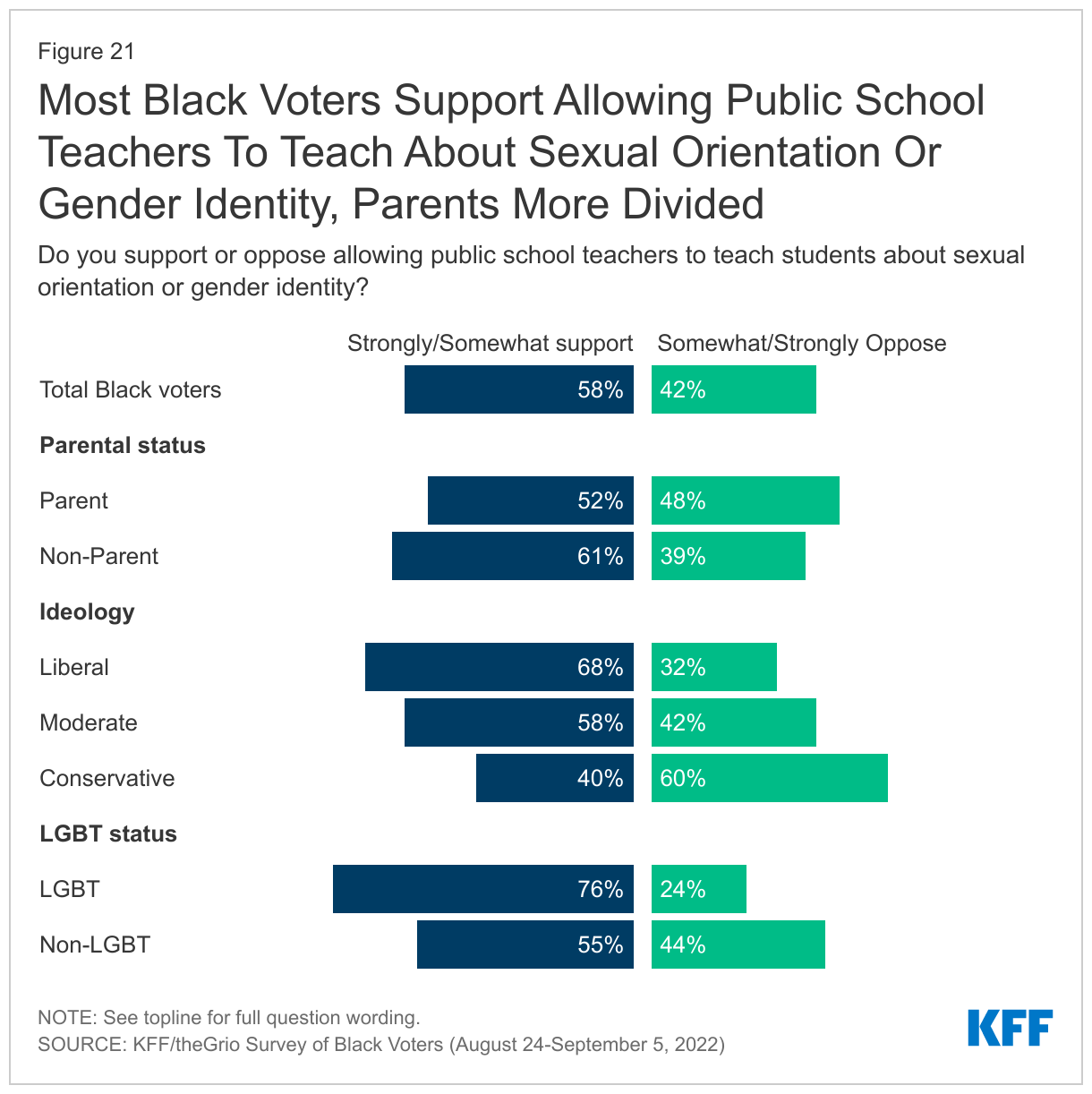

Most Black voters support allowing public schools to teach students about sexual orientation and gender identity, but those who are parents are more divided. Nearly six in ten (58%) Black voters support allowing public school teachers to teach students about sexual orientation and gender identity. However, while a clear majority (61%) of Black voters who are not parents support this, Black voters who are parents of children under 18 are more divided (52% support and 48% oppose).

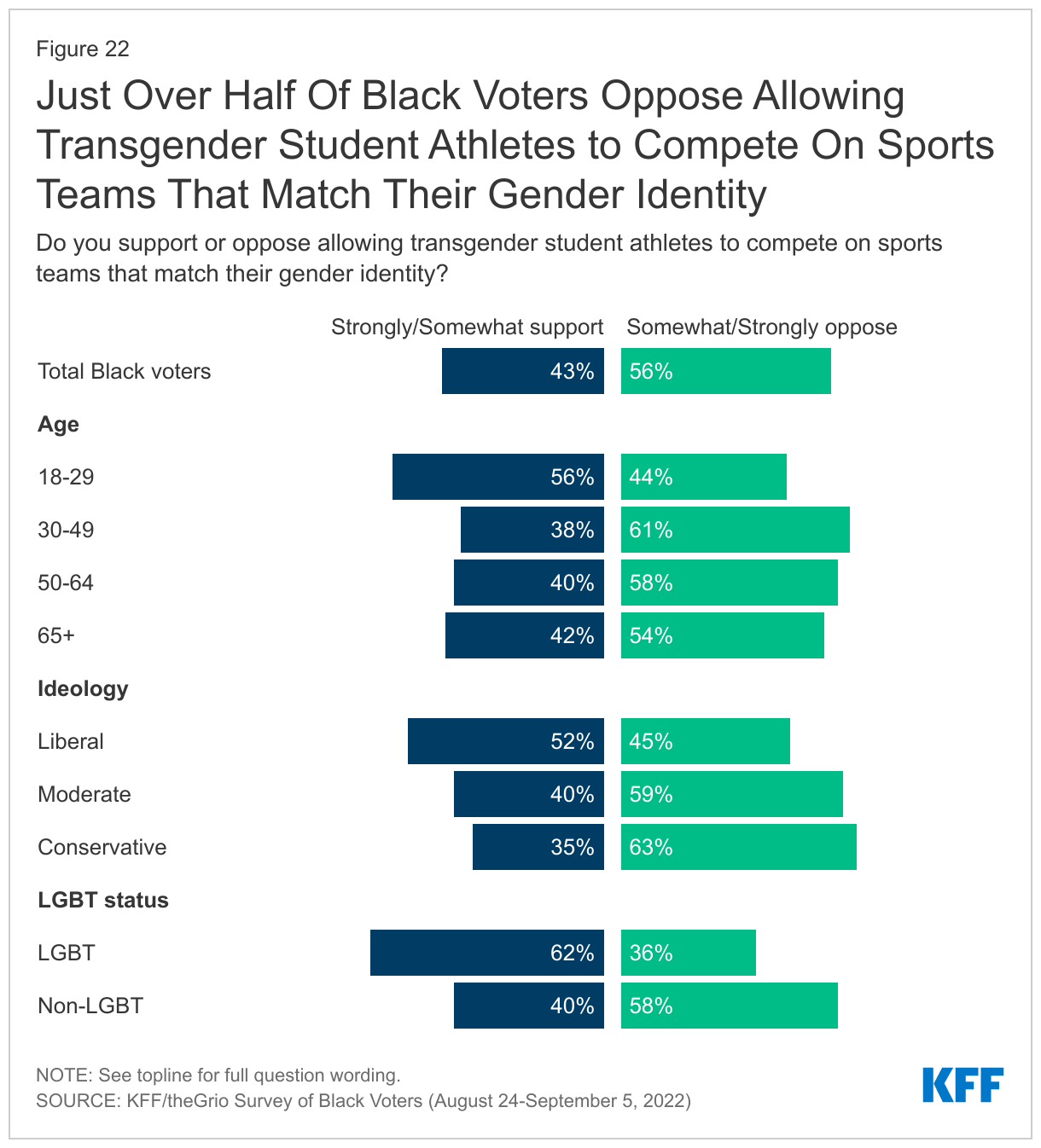

More Black voters oppose rather than support allowing transgender student athletes to compete on sports teams that match their gender identity, though majorities of younger Black voters and those who identify as LGBT are in support. Fewer than half of Black voters (43%) support allowing transgender student athletes to compete on sports teams that match their gender identity, while 56% oppose. However, a majority (56%) of young Black voters aged 18-29 are in support, as are six in ten Black voters who identify as LGBT (62%) and about half (52%) of liberal Black voters.

Black Voters And The Democratic And Republican Parties

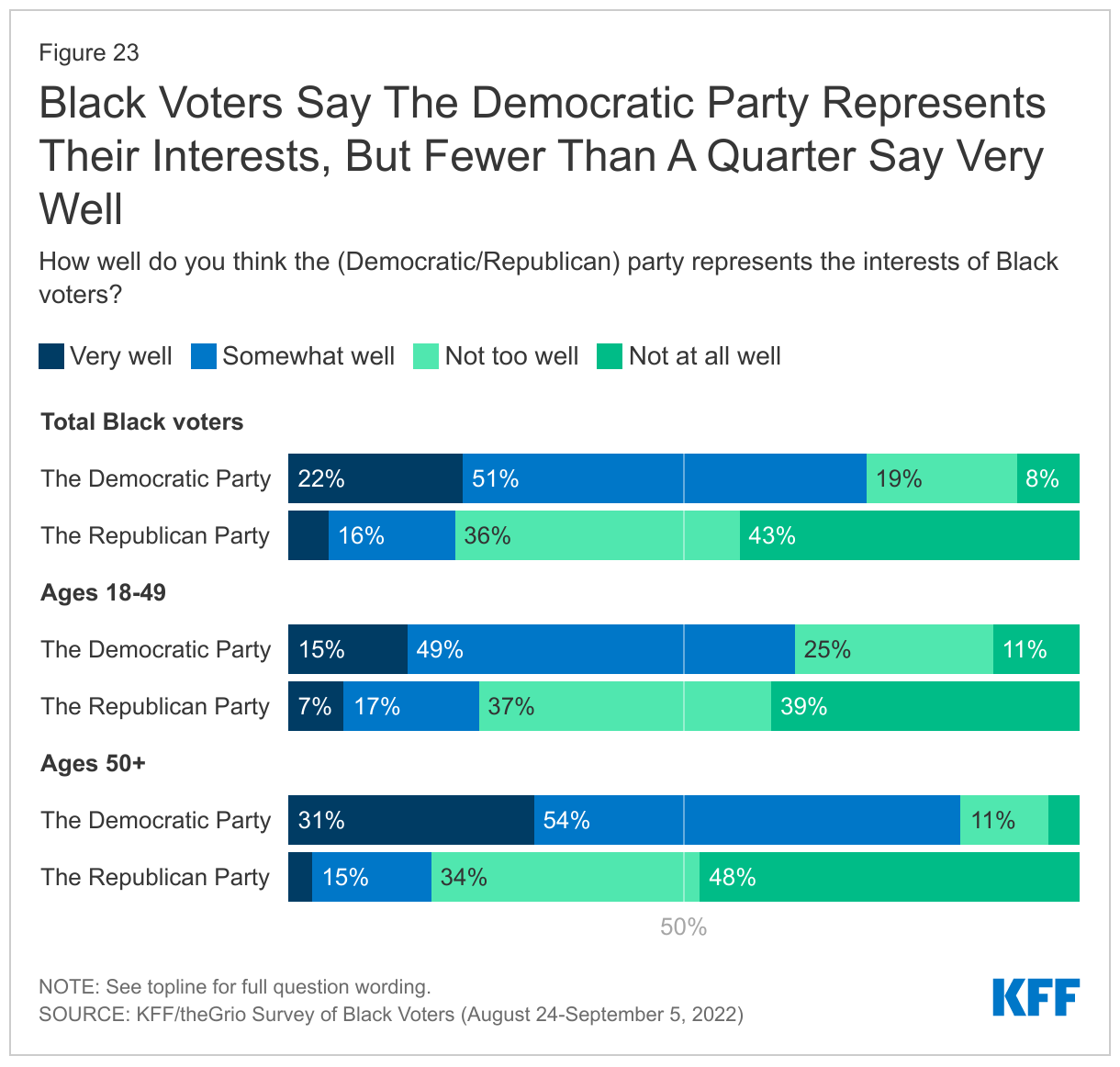

A much larger share of Black voters say the Democratic party does a good job of representing Black voters than say the same about the Republican party, but less than a quarter say the Democratic party represents the interests of Black voters very well. About three in four (73%) Black voters say the Democratic party represents the interests of Black voters “very” or “somewhat” well, which is more than three times the share who say the same about the Republican party (21%). However, this comparison masks a lackluster response about the Democrats: just 22% of Black voters say the Democratic Party represents Black voter interests “very” well. This is only slightly higher – 27% – if the sample is limited to Black voters who identify as Democrats or lean that way. And, in a sign that the Democratic party may have a tenuous hold on younger Black voters, there is large gap between Black voters under age 50 (64%) and those ages 50 and older (85%) who say the Democrats represent Black voters’ interests at least somewhat well.

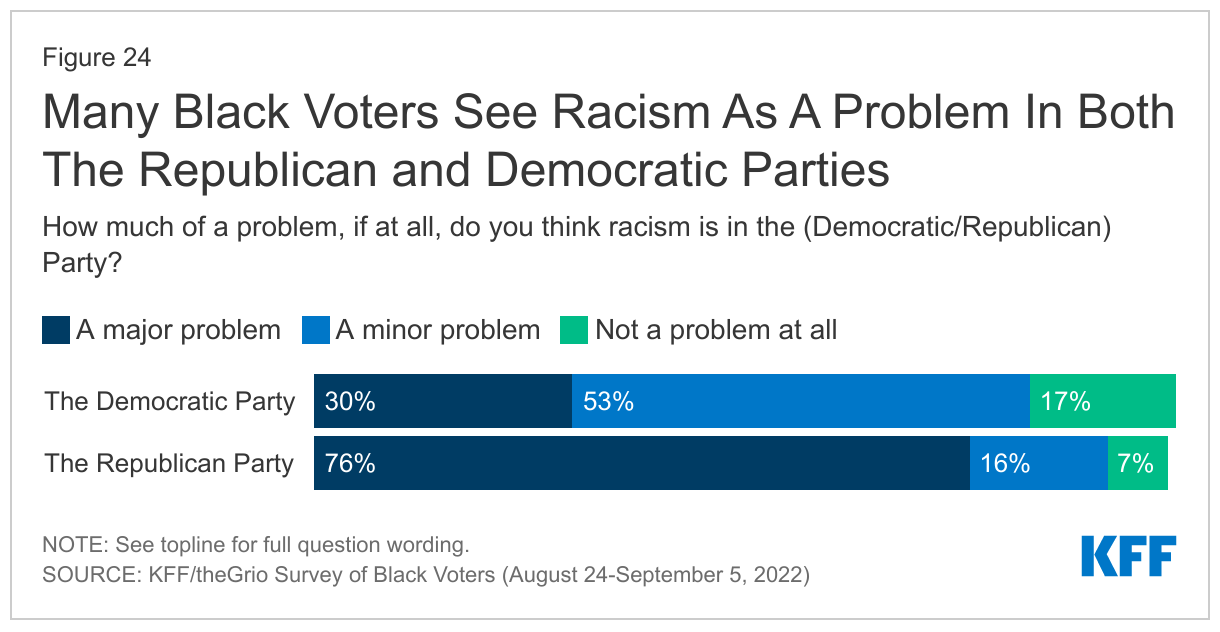

A large majority of Black voters see racism as a major problem in the Republican Party, and most believe racism is at least a minor problem in the Democratic Party as well. Black voters draw a distinction between the two major parties when it comes to racism, with about three in four saying racism is a major problem in the Republican party (76%), compared to three in ten who say the same of the Democratic party. However, about half (53%) see racism as a minor problem in the Democratic Party, and fewer than one in five (17%) say racism is not a problem at all in the Democratic party.

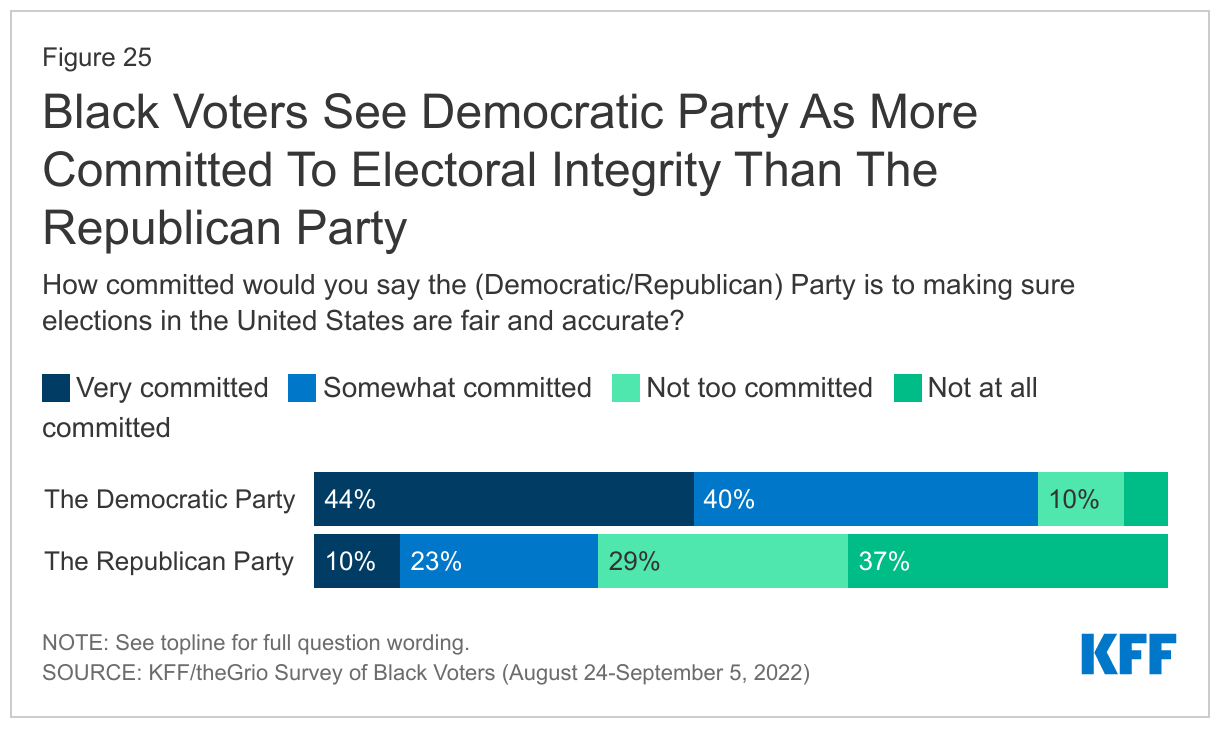

The Democratic party has a clear advantage among Black voters on the perception of electoral integrity. A large majority (85%) of Black voters say the Democrats are very or somewhat committed to making sure US elections are fair and accurate, compared to about one third (34%) who say the same about the Republican party.

Most Black voters are aware that they are a key voting bloc for the Democrats. About eight in ten (83%) say that Black voters are important for the Democratic party to win elections, including half (50%) who say they are “absolutely essential” to the party’s electoral success, and a third (33%) who say they are “very important.”

Joe Biden and Kamala Harris in 2024 and Beyond

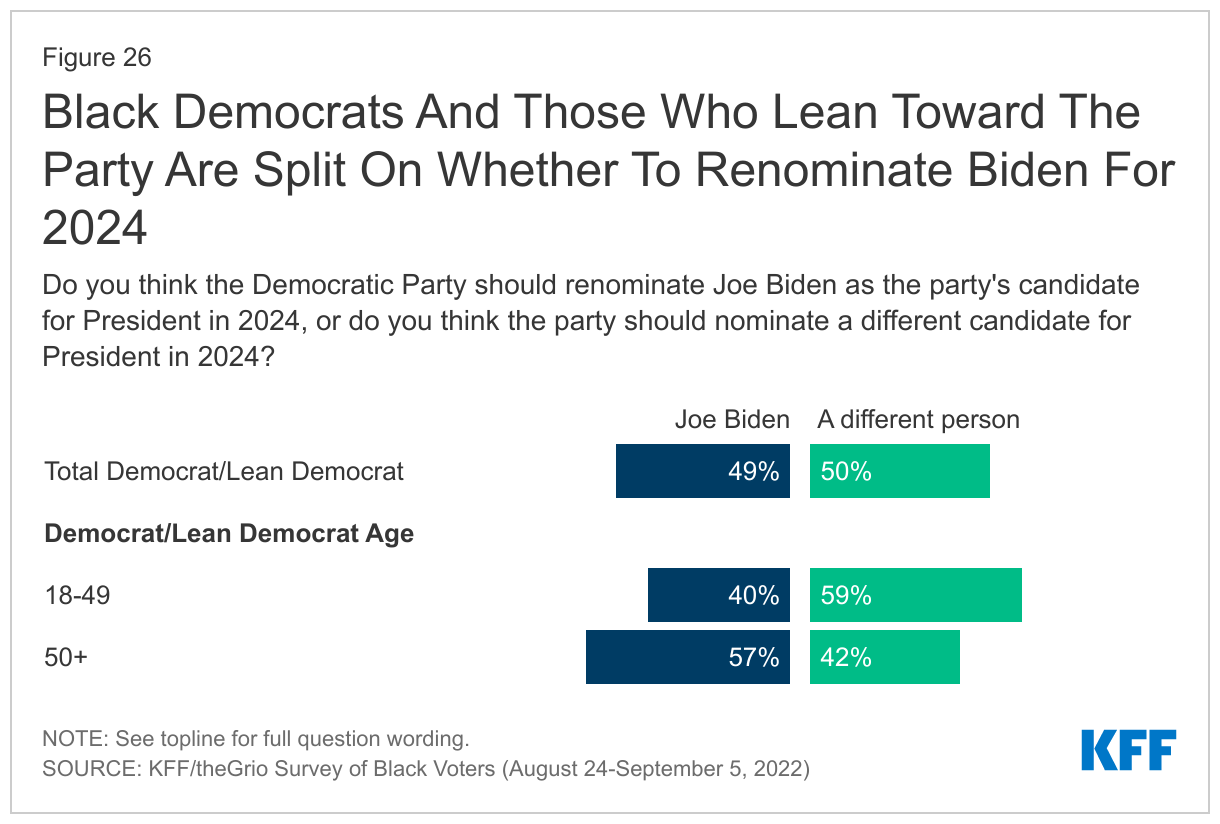

Black Democratic voters and those who lean toward the party are split on whether the Democratic Party should renominate Joe Biden for 2024. Among Black voters who identify as Democrats or lean that way, about half (49%) say the party should renominate Biden for President in 2024, while the other half (50%) say the party should nominate someone else. There is an age divide on Joe Biden’s future in office, with Black Democrats and Democratic leaners under 50 more likely to say they want someone else in 2024 than those older 50. About six in ten (59%) younger Black Democrats and leaners say they want someone else, while four in ten want Biden to be renominated. Among Black Democrats and leaners 50 and older, nearly six in ten (57%) say they want Biden to be renominated, and 42% say they want the Democratic Party to nominate someone else for President. Black voters who voted for Biden for president in 2020 are also divided on his future prospects (48% say renominate Biden and 51% say someone else).

Black Democratic voters who disapprove of Biden’s job performance are much more likely to say they want a different candidate in 2024. Among Black Democrats and Democratic leaning voters who disapprove of Biden’s job performance, nine in ten (91%) want a different Democratic nominee in 2024. It is notable that even among Black Democrats and leaners who approve of his job performance, about four in ten (41%) want the party to nominate someone else in 2024.

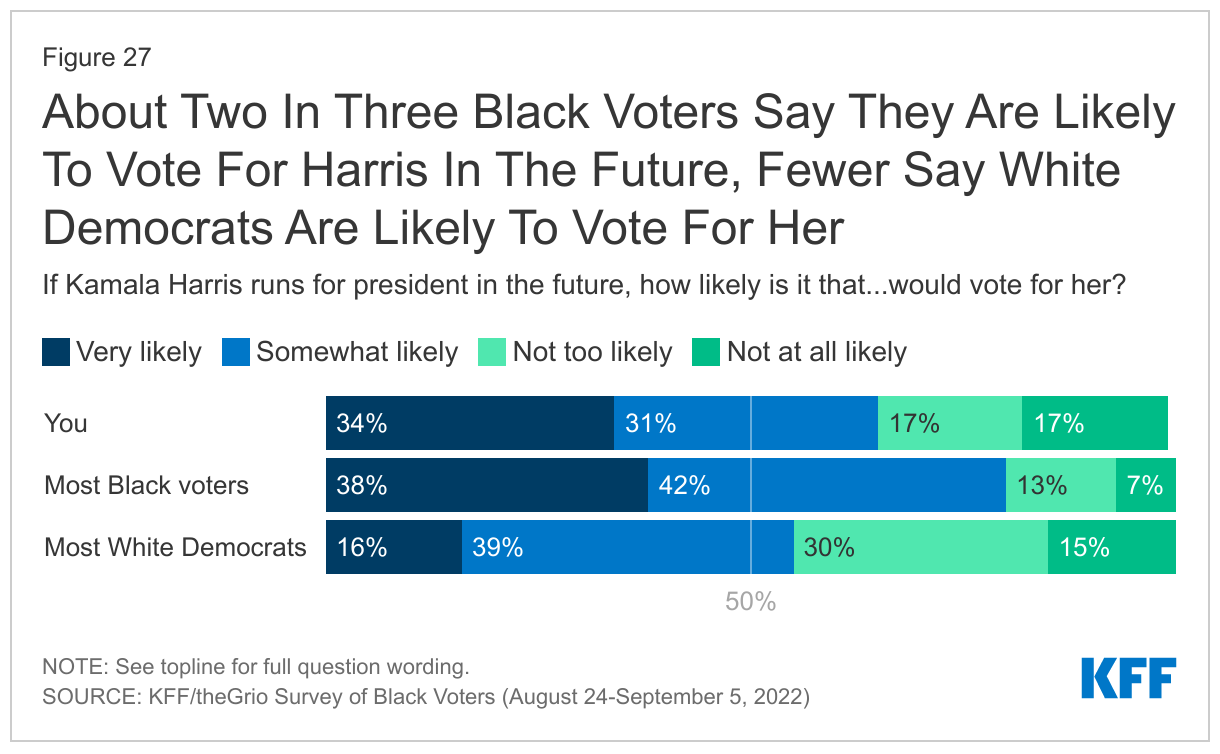

Most Black voters support a future Presidential bid by Kamala Harris, but her support is weakest among young voters. About two-thirds of Black voters say they would be very or somewhat likely to vote for Kamala Harris if she runs for president in the future, with about a third saying they would be “very likely.” Though most say they would be at least somewhat likely vote for her in the future, support for a future Harris presidential run is lower among Black voters under age 50 (57%) than among voters 50 and older (76%). Harris also gets higher support from women (69% vs. 60% of men), particularly women ages 50 and over (78%).

Majorities of Black voters say most Black voters would vote for Harris in the future, but fewer say they think White Democrats would. Eight in ten Black voters say they think most Black voters are at least somewhat likely to vote for Harris in the future. A much smaller share, though still a majority (55%) of Black voters say that White Democrats would be somewhat or very likely to vote for Harris, with 16% who say White Democrats would be “very likely”.

Methodology

The KFF/theGrio Survey of Black Voters was conducted August 24-September 5, 2022, online and by telephone among a nationally representative sample of 1,000 U.S. adults in English who identify as Black or African American and are registered to vote. The sample includes 800 Black adults registered to vote reached online through the SSRS Opinion Panel. An additional 100 respondents were reached online through the Ipsos KnowledgePanel. To reach Black voters who do not use the Internet, another 100 interviews were conducted by calling back respondents who previously participated in an SSRS Omnibus poll and identified as Black and said they did not use the Internet. Sampling, data collection, weighting, and tabulation were managed by SSRS in close collaboration with KFF researchers. Teams from KFF and theGrio worked together to develop the questionnaire and analyze the data, and KFF financed the survey. Each organization is solely responsible for its content.

The SSRS Opinion Panel is a nationally representative probability-based panel where panel members are recruited randomly in one of two ways: (a) through invitations mailed to respondents randomly sampled from an Address-Based Sample (ABS) provided by Marketing Systems Groups (MSG) through the U.S. Postal Service’s Computerized Delivery Sequence (CDS); (b) from a dual-frame random digit dial (RDD) sample provided by MSG. The SSRS Omnibus survey is a nationally representative bilingual telephone survey designed to meet standards of quality associated with custom research studies. Sample for the SSRS Omnibus was obtained through Marketing System Groups (MSG). The Ipsos KnowledgePanel is a nationally representative probability-based panel where members are recruited randomly using ABS based on a stratified sample from the CDS. For the online panel components, invitations were first sent by email to panel members who previously identified as Black or African American, followed by up to three reminder emails. Respondents in the phone samples received a $10 incentive.

Both phone and web samples were asked to confirm their race and voter registration status in order to be eligible. Respondents were considered eligible if they identified as Black or African American even if they also identified as Hispanic or another race group.

The combined cell phone and panel samples were weighted to match the sample’s demographics to the national U.S. population of Black or African American adults (including Hispanic Black and multi-racial Black adults) who are registered to vote using data from the Census Bureau’s 2020 Current Population Survey (CPS) Voting and Registration supplement. Weighting parameters included sex, age, education, race/ethnicity, region, and education. The weights take into account differences in the probability of selection for each sample type (callback sample and panels). This includes adjustment for the sample design, within household probability of selection, and the design of the panel-recruitment procedure.

The online questionnaire included two questions designed to establish that respondents were paying attention. Surveys with a length less than one quarter of the mean length by mode were flagged and reviewed. Cases that failed two quality control questions (i.e. trap questions) were also flagged and reviewed. One case was removed due to a short survey length and failure of the two quality control questions.

The margin of sampling error including the design effect for the full sample is plus or minus 4 percentage points. Numbers of respondents and margins of sampling error for key subgroups are shown in the table below. Sample sizes and margins of sampling error for other subgroups may be higher and are available by request. Sampling error is only one of many potential sources of error and there may be other unmeasured error in this or any other public opinion poll. KFF public opinion and survey research is a charter member of the Transparency Initiative of the American Association for Public Opinion Research.

| Group | N (unweighted) | M.O.S.E. |

| Total Black voters | 1,000 | ± 4 percentage points |

| Age | ||

| 18-49 | 567 | ± 5 percentage points |

| 50+ | 433 | ± 6 percentage points |

| Party identification | ||

| Democrats/Democratic-leaning independents | 758 | ± 4 percentage points |

| Republicans/Republican-leaning independents | 103 | ± 11 percentage points |