A View of Medicaid Today and a Look Ahead: Balancing Access, Budgets and Upcoming Changes

Results from an Annual Medicaid Budget Survey for State Fiscal Years 2025 and 2026

Overview

This annual Medicaid budget survey report highlights certain policies in place in state Medicaid programs in state fiscal year (FY) 2025 and policy changes implemented or planned for FY 2026. The findings are drawn from the 25th annual budget survey of Medicaid officials conducted by KFF and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD).

Reports published since 2016 are available here. Older reports have been archived here.

NEWS RELEASE

- A news release announcing the publication of the 2025 Medicaid Budget Survey is available.

EXECUTIVE SUMMARY

- The Executive Summary provides an overview of the 2025 survey results and is available under the Executive Summary section.

FULL REPORT

- The complete 2025 Medicaid Budget Survey Report contains 6 separate sections. Users can view each section separately or download a full Report PDF from the right side of the page.

ENROLLMENT & SPENDING BRIEF

- This companion issue brief provides an overview of Medicaid enrollment and spending growth with a focus on FY 2025 and FY 2026.

ADDITIONAL BRIEFS

Executive Summary

Following years of significant changes in Medicaid spending, enrollment, and policy during the COVID-19 pandemic and the subsequent Medicaid unwinding period, state Medicaid programs returned to more routine operations in state fiscal year (FY) 2025 and were focused on an array of other priorities, including improving access to care or addressing social determinants of health. However, heading into FY 2026, states were facing a more tenuous fiscal climate and beginning to prepare for another major set of changes to the Medicaid program. The 2025 federal budget reconciliation law (H.R.1) includes substantial Medicaid policy changes and reductions in federal funding, though the impacts vary by state. While many of the provisions do not take effect until FY 2027 or later, states are anticipating the upcoming changes, assessing budgetary and programmatic impacts, and preparing for the implementation of multiple and complex policy changes. Serving over one in five people living in the United States and accounting for nearly one-fifth of health care spending (and over half of long-term care spending), Medicaid represents a large share of state budgets and is a key part of the overall health care system.

This report highlights certain policies in place in state Medicaid programs in FY 2025 and policy changes implemented or planned for FY 2026, which began on July 1, 2025 for most states.1 The findings are drawn from the 25th annual budget survey of Medicaid officials in all 50 states and the District of Columbia conducted by KFF and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD). The survey was sent to states in June 2025 and 48 states responded by October 2025, although response rates for specific questions varied.2 The District of Columbia is counted as a state for the purposes of this report, and due to differences in the financing structure of their programs, the U.S. territories were not included in this analysis.

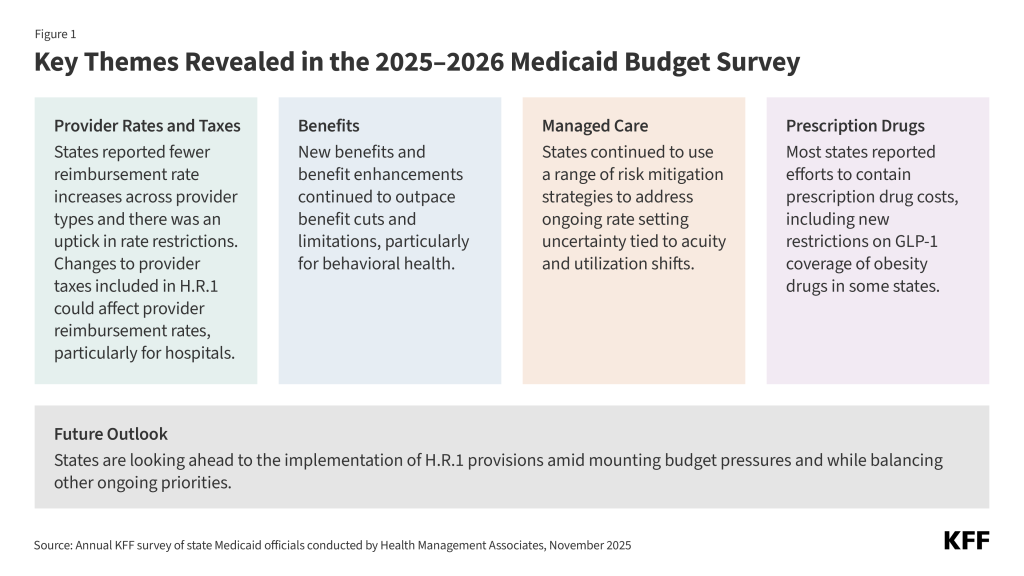

Key Take-Aways

- Provider Rates and Taxes. At the time of the survey, responding states had implemented or were planning more fee-for-service (FFS) rate increases than rate restrictions in both FY 2025 and FY 2026; however, across many individual provider types, notably fewer states reported rate increases in FY 2025, or planned for FY 2026, compared with recent years. States continue to target rate increases for nursing facilities and home and community-based services (HCBS) providers more often than for other provider types. There was a notable uptick in states reporting provider rate restrictions in FY 2025 (6 states) and FY 2026 (6 states), compared with the number of states reporting provider rate decreases for FY 2024 (1 state) and FY 2023 (2 states). Trends in provider reimbursement rates typically reflect state fiscal conditions. All states except Alaska continue to rely on provider taxes to fund a portion of the non-federal share of Medicaid, and taxes on hospitals (47 states) and nursing facilities (45 states) are most common. States report that provider tax revenue is most often used to increase FFS or managed care organization (MCO) payment rates or fund supplemental payments to providers. H.R.1 imposes significant new restrictions on states’ ability to generate Medicaid provider tax revenue, including prohibiting all states from establishing new provider taxes or from increasing existing taxes and reducing existing provider taxes for states that have adopted the Affordable Care Act (ACA) Medicaid expansion.

- Benefits. The number of states reporting new benefits and benefit enhancements continues to greatly outpace the number of states reporting benefit cuts and limitations; however, state Medicaid agencies could face increasing pressure to cut or limit optional benefits to reduce Medicaid costs as states face a more tenuous fiscal climate and start to prepare for the impact of H.R.1. Consistent with trends in recent years, many states reported expanding services across the behavioral health care continuum, particularly community-based behavioral health services.

- Managed Care. States and plans faced heightened rate setting uncertainty when the Medicaid continuous enrollment provision expired on March 31, 2023, resulting in acuity and utilization shifts within the remaining population that were difficult to predict. While states have continued to use a range of risk mitigation strategies to address this uncertainty, half of responding MCO states reported seeking Centers for Medicare and Medicaid Services (CMS) approval for a capitation rate amendment to address unanticipated shifts in acuity and/or utilization for a rating period beginning in FY 2025. Most states reported that the changes were applied retrospectively. Beyond rate setting, this year’s survey also asked states about requirements related to MCO use of artificial intelligence (AI) to automate parts of the prior authorization process. As of July 1, 2025, less than one-quarter of responding MCO states reported requiring MCOs to disclose the use of AI in prior authorization processes. Several states reported implementing new or expanded oversight activities or adopting other safeguards in FY 2025 or 2026 to support appropriate use of AI in MCO prior authorization processes.

- Prescription Drugs. Sixteen state Medicaid programs reported covering GLP-1s (glucagon-like peptide-1s) for obesity treatment as of October 1, 2025, and some states reported plans to restrict coverage in the future. While states must cover nearly all Food and Drug Administration (FDA) approved drugs for medically accepted indications, a long-standing statutory exception allows states to choose whether to cover weight-loss drugs under Medicaid. As a result, Medicaid coverage of GLP-1 drugs for the treatment of obesity remains optional for states, while coverage is required for other indications (diabetes, cardiovascular disease, and sleep apnea). High costs continue to be the key consideration in state Medicaid program obesity drug coverage decisions, and given recent state budget challenges, state interest in expanding Medicaid coverage of obesity drugs is waning, though the landscape continues to evolve. Rising prescription drug costs (and the costs of new specialty drugs in particular) are an ongoing concern for states. Most responding states reported at least one new or expanded initiative to contain prescription drug costs in FY 2025 or FY 2026, with many states reporting initiatives that specifically target high-cost specialty drugs such as cell and gene therapies or other physician-administered drugs.

- Future Outlook. Now that the pandemic-era unwinding process has ended, many states are confronting more difficult fiscal conditions and facing fiscal uncertainty driven, in part, by H.R.1. States reported managing Medicaid cost growth, especially growth driven by higher acuity, increased long-term care demand, and high-cost drugs and treatments, as significant challenges facing the program. Although many Medicaid provisions in the reconciliation law do not take effect until FY 2027 or later, states are assessing budgetary and programmatic impacts and preparing to implement policy changes required by the law. States expressed concern about the scope and complexity of the required changes, the compressed implementation timeframes for certain provisions, and the need for timely federal implementation guidance. States highlighted process and systems challenges that they must address to operationalize the new requirements, including work requirements. In addition to navigating state budget challenges and implementing H.R.1 provisions, states cited a continued focus on other varied Medicaid program priorities including expanding access, implementing initiatives that target specific populations (e.g., pregnant individuals, justice-involved), continuing delivery system efforts, and improving administrative systems and functions.

Acknowledgements

Pulling together this report is a substantial effort, and the final product represents contributions from many people. The combined analytic team from KFF and Health Management Associates (HMA) would like to thank the state Medicaid directors and staff who participated in this effort. In a time of limited resources and challenging workloads, we truly appreciate the time and effort provided by these dedicated public servants to complete the survey and respond to our follow-up questions. Their work made this report possible. We also thank the leadership and staff at the National Association of Medicaid Directors (NAMD) for their collaboration on this survey.

Introduction

Medicaid is the primary program providing comprehensive health and long-term care to one in five people living in the United States and accounts for nearly $1 out of every $5 spent on health care (and over half of all spending on long-term care). In FY 2025, state Medicaid programs returned to more routine operations following the unwinding of the pandemic-related continuous enrollment provision and were focused on an array of priorities, including improving access to care (particularly behavioral health and long-term care) and launching key initiatives related to social determinants of health or reentry services for justice-involved populations. Heading into FY 2026, state Medicaid programs were facing fiscal and policy pressures, stemming from state budget challenges that predate passage of the 2025 federal budget reconciliation law (H.R.1) as well as from the passage of H.R.1.

In response to the COVID-19 pandemic, Congress enacted legislation that required states to keep people continuously enrolled in Medicaid in exchange for enhanced federal funding. As a result, enrollment in Medicaid reached record highs, and Medicaid enrollment growth along with enhanced subsidies in the Affordable Care Act (ACA) Marketplaces contributed to significant declines in the uninsured rate. Following the end of the continuous enrollment provision on March 31, 2023, states began the process of “unwinding” (i.e., resuming historically typical eligibility redeterminations and disenrolling individuals found to be no longer eligible for Medicaid), resulting in millions being disenrolled from Medicaid. The enhanced federal funding also phased down through end of 2023. Total Medicaid and Children’s Health Insurance Program (CHIP) enrollment as of June 2025 was 77.7 million, an 18% decline from total enrollment in March 2023 but still 9% higher than enrollment levels in February 2020, prior to the pandemic.

States are navigating the new “normal” for their programs following the expiration of pandemic-era policies and focusing on an array of other priorities. At the same time, states are facing a more tenuous fiscal climate and starting to prepare for the impact of the recently passed reconciliation law. While state fiscal conditions and the expected impact of federal changes vary across states, these changes may make it more challenging for states to sustain recent efforts to improve enrollee access and reduce health disparities. The Medicaid provisions in H.R.1, which are numerous and complicated, are estimated to reduce federal Medicaid spending by $911 billion (or by 14%) over a decade and increase the number of uninsured people by 7.5 million, though the impacts vary by state with spending cuts ranging from 4% to almost one-fifth of all federal Medicaid spending in some states. While many provisions in the new law, including some of the largest sources of federal Medicaid savings such as work requirements and financing changes, do not take effect until FY 2027 or later, state Medicaid programs are anticipating the new law’s implementation and impact.

This report draws upon findings from the 25th annual budget survey of Medicaid officials in all 50 states and the District of Columbia conducted by KFF and Health Management Associates (HMA), in collaboration with the National Association of Medicaid Directors (NAMD). (Previous reports can be found here.) This year’s KFF/HMA Medicaid budget survey was conducted from June through October 2025 via a survey sent to each state Medicaid director in June 2025 followed by a set of focus groups with Medicaid officials in different roles (state Medicaid directors and chief financial officers) from various states. Overall, 48 states responded by October 2025,3 although response rates for specific questions varied. The District of Columbia is counted as a state for the purposes of this report. Given differences in the financing structure of their programs, the U.S. territories were not included in this analysis. The survey instrument is included as an appendix to this report.

This report examines Medicaid policies in place or implemented in FY 2025, policy changes implemented at the beginning of FY 2026, and policy changes for which a definite decision has been made to implement in FY 2026 (which began for most states on July 1, 20254). Policies adopted for the upcoming year are occasionally delayed or not implemented for reasons related to legal, fiscal, administrative, systems, or political considerations, or due to CMS approval delays. Key findings, along with state-by-state tables, are included in the following sections:

Delivery Systems

Context

Managed Care Models. For more than three decades, states have increased their reliance on managed care delivery systems with the aim of improving access to certain services, enhancing care coordination and management, and making future costs more predictable. Across the states, there is wide variation in the populations required to enroll in managed care, the services covered (or “carved in”), and the quality and performance incentives and penalties employed. Most states contract with risk-based managed care organizations (MCOs) that cover a comprehensive set of benefits (acute care services and sometimes long-term care), but many also contract with limited benefit prepaid health plans that offer a narrow set of services such as dental care, non-emergency medical transportation, or behavioral health services. A minority of states operate primary care case management (PCCM) programs which retain fee-for-service (FFS) reimbursements to providers but link enrollees with a primary care provider who is paid a small monthly fee to provide case management services in addition to primary care. While the shift to MCOs has increased budget predictability for states, the evidence about the impact of managed care on access to care and costs is both limited and mixed.5,6,7 In 2024, the Biden administration finalized major Medicaid managed care regulations designed to advance access and promote quality of care for enrollees. These rules are complex and set to be implemented over several years unless overturned or delayed by Congress or the Trump administration.

Capitation Rates and Risk Mitigation. MCOs are at financial risk for services covered under their contracts, receiving a per member per month “capitation” payment for these services. Capitation rates must be actuarially sound8 and are applied prospectively, typically for a 12-month rating period, regardless of changes in health care costs or utilization.9 States may use a variety of risk mitigation tools to ensure payments are not too high or too low, including risk sharing arrangements, risk and acuity adjustments, medical loss ratios (MLR), or incentive and withhold arrangements. When, however, significant enrollment, utilization, cost, and acuity changes began to emerge early in the COVID-19 public health emergency, CMS allowed states to modify managed care contracts, and many states implemented COVID-19 related “risk corridors” (where states and health plans agree to share profit or losses), allowing for the recoupment of funds. States and plans faced another period of heightened rate setting uncertainty when the continuous enrollment provision expired on March 31, 2023, resulting in acuity and utilization shifts within the remaining population that were difficult to predict.

Looking ahead, the 2024 Medicaid managed care rule requires states to incorporate all state directed payments (SDPs) through capitation rate setting adjustments instead of using “separate payment terms” (which provide payments outside of base capitation rates) beginning in July 2027.10 The 2025 federal budget reconciliation law (H.R.1) will also create rate setting challenges for states as the Medicaid provisions impacting enrollment and spending (e.g., work requirements, more frequent eligibility redeterminations, and provider tax and SDP caps and reductions) roll out over the next several years.

Prior Authorization and Artificial Intelligence (AI). MCOs often require patients to obtain approval of certain health care services or medications before the care is provided, an insurance practice commonly referred to as “prior authorization”. Subjecting a service or drug to prior authorization allows the MCO to evaluate whether the care is covered, medically necessary, and being delivered in the appropriate setting, but can also increase the administrative burden on providers and sometimes delay or limit access to care. To reduce administrative costs and processing times and increase consistency of decisions, health insurers are increasingly turning to AI to automate the processing of prior authorization requests. Using AI for this purpose, however, is drawing scrutiny due to concerns that poorly implemented AI can harm patients. In June 2025, the Department of Health and Human Services (HHS ) announced a voluntary initiative where dozens of health insurers pledged to reduce the burden of prior authorizations across insurance markets, including a commitment to expand “real time” responses to electronic prior authorization requests, which may involve increasing the use of AI. In July 2025, the Trump administration released an AI action plan, emphasizing the removal of regulatory “red tape” and enabling faster adoption of AI tools, and in 2026, the Administration plans to launch a new innovation model to test the use of technologies, including AI and machine learning, in the prior authorization review process for select Medicare services. In September 2025, the launch of the Safe AI in Medicaid Alliance was announced, bringing together 32 states and industry leaders to develop frameworks for AI adoption and use in state Medicaid programs.

This section provides information about:

- Managed care models

- MCO medical loss ratio (MLR) and remittance requirements

- Risk corridors

- MCO capitation rate amendments and rate setting challenges

- State oversight of MCO use of AI in prior authorization processes

Findings

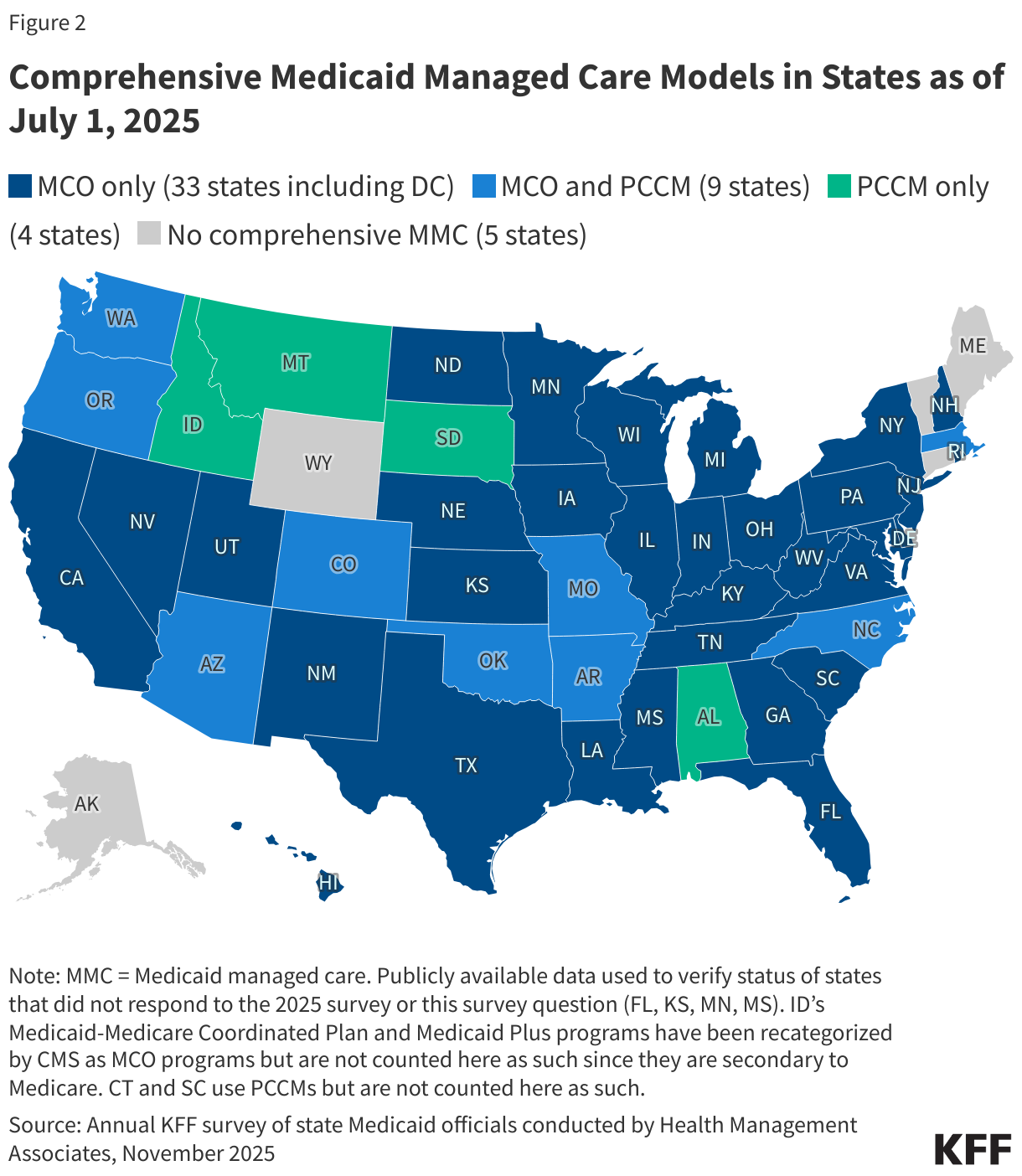

Managed Care Models

Capitated managed care remains the predominant delivery system for Medicaid in most states. As of July 1, 2025, all states except five – Alaska, Connecticut,11 Maine, Vermont,12 and Wyoming – had some form of managed care (MCOs and/or PCCM) in place (Figure 2). As of July 1, 2025, 42 states13 were contracting with MCOs (unchanged from 2024); only two of these states (Colorado and Nevada) did not offer MCOs statewide (although Nevada plans to expand MCOs statewide in 2026). Thirteen states reported operating a PCCM program (with the addition of Missouri).14 Although not counted in this year’s report, following the passage of HB 345, Idaho expects to end its PCCM program by December 2025 and implement comprehensive MCOs by January 2029.

Of the 46 states that operate some form of comprehensive managed care (MCOs and/or PCCM), 33 states operate MCOs only, four states operate PCCM programs only, and nine states operate both MCOs and a PCCM program. In total, 28 states15 were contracting with one or more limited benefit prepaid health plans (PHPs) to provide Medicaid benefits including behavioral health care, dental care, vision care, non-emergency medical transportation (NEMT), or long-term care (LTC).

Capitation Rates and Risk Mitigation

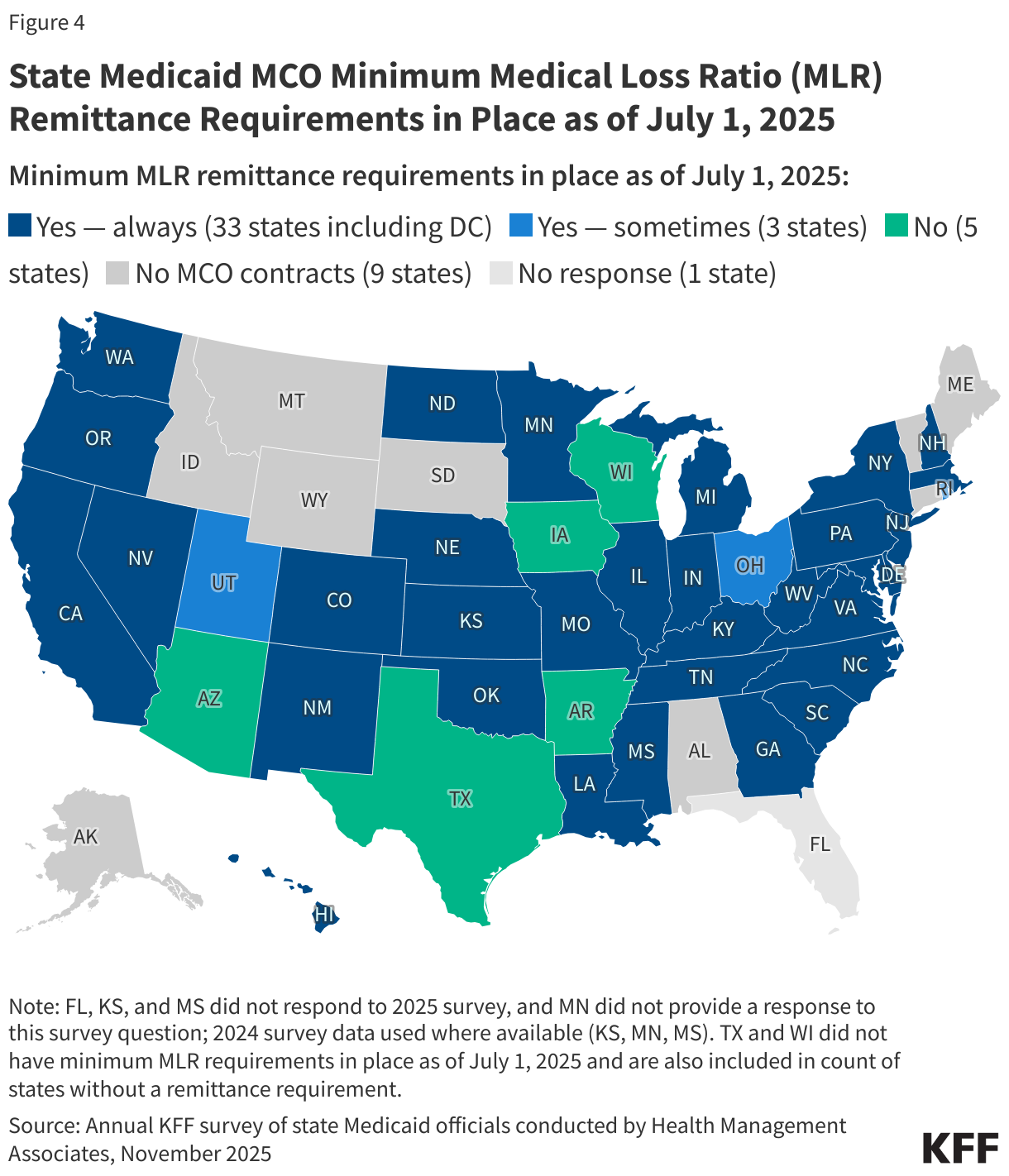

Minimum Medical Loss Ratios (MLRs) and Remittance Requirements

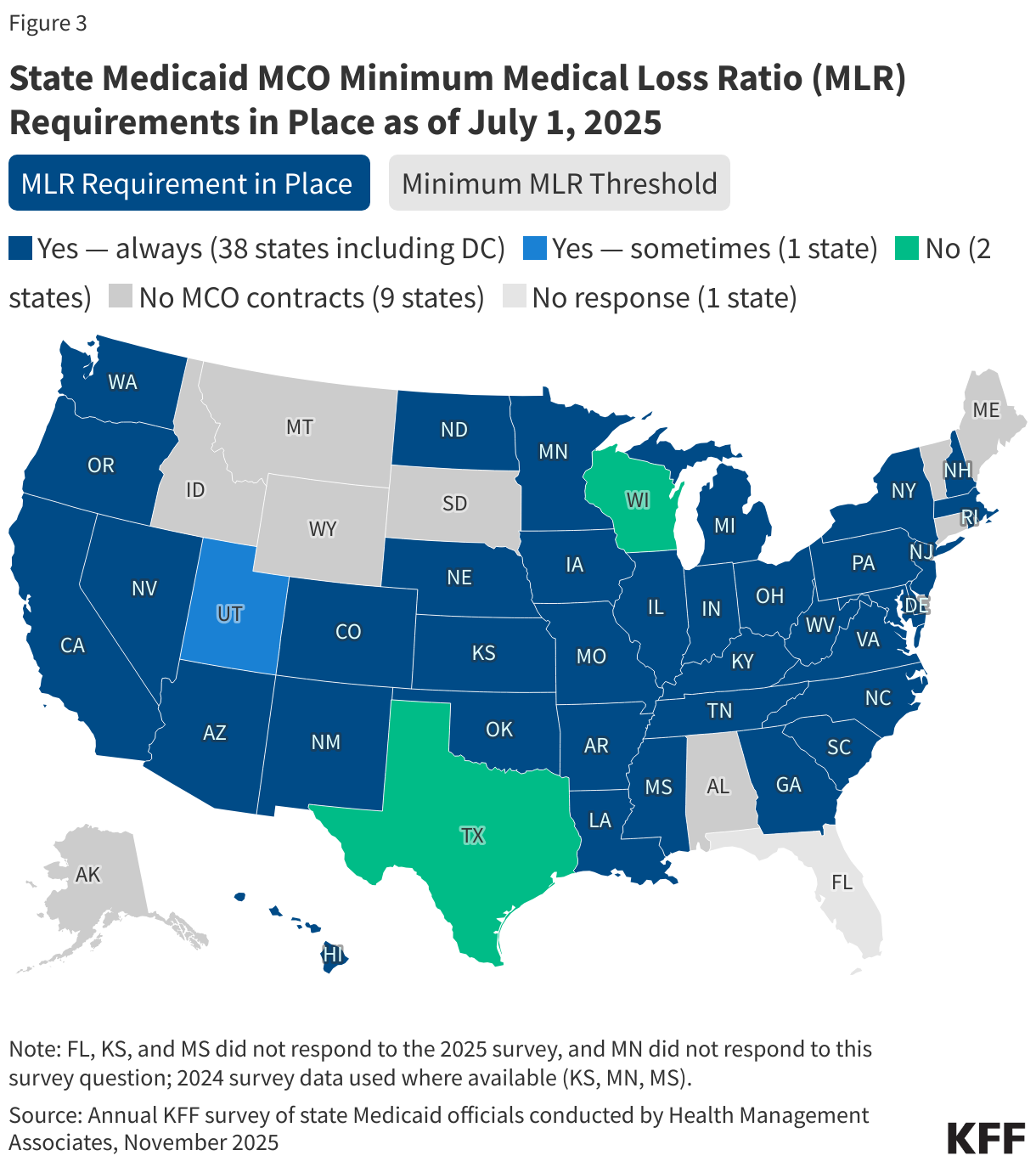

The MLR reflects the proportion of total capitation payments received by an MCO spent on clinical services and quality improvement, where the remainder goes to administrative costs and profits. To limit the amount that plans can spend on administration and keep as profit, CMS published a final rule in 2016 that requires states to develop capitation rates for Medicaid to achieve an MLR of at least 85% in the rate year.16 There is no federal requirement for Medicaid plans to pay remittances to the state if they fail to meet the MLR standard, but states have discretion to require remittances. The 2024 Consolidated Appropriations Act included a financial incentive to encourage certain states to collect remittances from Medicaid MCOs that do not meet minimum MLR requirements. As state Medicaid programs faced heightened uncertainty due to the COVID-19 pandemic (2020) and the unwinding of the pandemic-era continuous enrollment provision (starting in 2023), analysis of Medicaid managed care market data (reported to the National Association of Insurance Commissioners) showed a decrease in the average Medicaid MLR in 2020 – 2022 compared with prior years, followed by an increase in 2023. More recent analysis suggests the average Medicaid MLR continued to increase in 2024. This year’s survey asked states whether they have a state required minimum MLR and whether they require MCOs that do not meet the minimum MLR requirement to pay remittances.

Nearly all MCO responding states (38 of 41) reported a minimum MLR requirement is always in place for MCOs as of July 1, 2025 (Figure 3). Among responding states, responses were unchanged/consistent with last year’s survey. While states must use plan-reported MLR data to set future payment rates so that plans will “reasonably achieve” an MLR of at least 85%, states are not required to set a minimum MLR for their managed care plans. If states set a minimum MLR requirement, it must be at least 85%.17 While most states that described their requirements reported a minimum MLR requirement of 85%, several states reported higher requirements that ranged from 86% to 93%. A few states noted that minimum MLRs may vary by program or population. For example, in Pennsylvania, the minimum MLR requirement is set at 85% for MCOs covering acute care only (hospital and physician services) and at 90% for MCOs that cover acute care and LTC. Similarly, New Jersey reported the minimum MLR requirement is set at 85% for non-LTC populations and 90% for LTC populations covered under MCO contracts. In Indiana, the minimum MLR requirement is set at 85% for MCOs that cover children and pregnant individuals, 87% for MCOs that cover ACA expansion adults, and 90% or higher for MCOs that cover more complex populations such as older adults (that may be receiving LTC) and people with disabilities.

More than three-quarters of responding MCO states (33 of 41) report they always require remittance payments when an MCO does not meet minimum MLR requirements (Figure 4). Thirty-three states reported that they always require MCOs to pay remittances, while three states indicated they sometimes require MCOs to pay remittances (among responding states, responses were generally consistent with last year’s survey18). States reporting that they sometimes require remittances may limit this requirement to certain MCO contracts. For example, Rhode Island reported that the remittance requirement did not apply to all populations.

Additionally, some states (e.g., North Carolina, Oregon, and Tennessee) give MCOs that fail to meet the state required minimum MLR the option to either remit funds to the state and/or use funds towards community reinvestments. California reported CMS requires its plans to pass MLR reporting and remittance requirements down to risk-bearing subcontractors.19 Five states do not require remittances (including two states that do not set a minimum MLR requirement). States that do not have minimum MLR and remittance requirements in place may have other risk mitigation strategies such as profit caps or experience rebates and/or risk corridors.

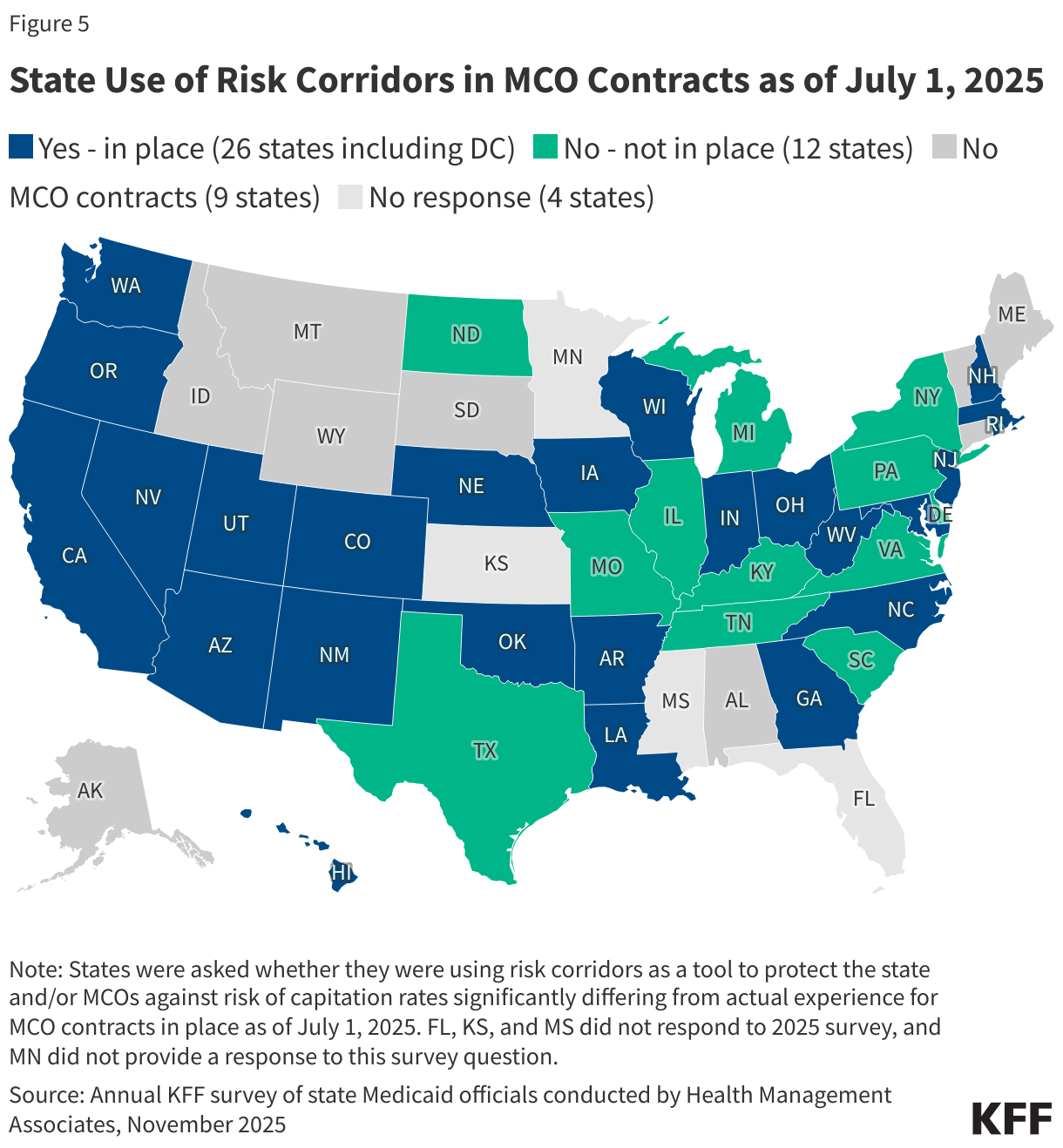

Risk Corridors

Risk corridors allow states and health plans to share profit or losses (at percentages specified in plan contracts) if aggregate spending falls above or below specified thresholds. Under two-sided risk corridors, states and plans may share in plan profits and losses. Although less common, some states may use “one-sided” risk corridors that apply only to profits or losses. Risk corridor thresholds may be tied to a target MLR. Risk corridors may cover all/most medical services (and enrollees) under a contract or may be more narrowly defined, covering a subset of services or enrollees. States may introduce risk corridors on a time-limited basis—for example, following the expansion of coverage to new groups (e.g., ACA Medicaid expansion adults). CMS encouraged states to implement two-sided risk mitigation strategies, including risk corridors, for rating periods impacted by the COVID-19 public health emergency. In 2023, nearly two-thirds of responding MCO states reported implementing a pandemic-related MCO risk corridor (in 2020, 2021, and/or 2022), leading to the recoupment of payments for many states. In this year’s survey, states were asked whether they were using risk corridors as a tool to protect the state and/or MCOs against risk of capitation rates significantly differing from actual experience for MCO contracts in place as of July 1, 2025.

Over two-thirds of responding MCO states (26 of 38) reported using risk corridors for MCO contracts in place as of July 1, 2025 (Figure 5).20 Some of the risk corridors that states described broadly apply to all/most populations and/or costs while other risk corridors apply to specific populations and/or a subset of costs. States frequently reported the use of multiple risk corridors. For example, Arizona reported using a two-sided medical risk corridor (for all programs) which includes benefit costs but excludes administrative costs and a two-sided risk corridor for fixed administrative costs for its largest program with the most population fluctuation (to ensure fixed costs are covered regardless of population fluctuations). California reported several risk corridors including a two-sided risk corridor for its new Enhanced Case Management (ECM) benefit, noting the potential variability (e.g., by plan and region) associated with the implementation and ramp up of ECM supports; a two-sided risk corridor for state directed supplemental payments for family planning services; and a two-sided risk corridor for a new federally qualified health center alternative payment model (APM) program. While the majority of risk corridors described by states are two-sided, at least three states (Nebraska, Washington, and West Virginia) reported using one-sided risk corridors for at least certain populations or MCO programs.

Rate Amendments and Rate Setting Challenges

State Medicaid programs use the most recent and accurate enrollment, cost, and utilization data available to ensure that MCO capitation rates are actuarially sound and that MCOs are not over-paid or under-paid for the services they deliver. Even if risk mitigation strategies are in place (e.g., MLR with remittance and/or risk corridors), states may determine rate amendments are necessary, for example, if their actual experience differs significantly from the assumptions used for the initial certified rates. During a contract rating period, states may increase or decrease rates by 1.5% per rate cell (which apply to population subgroups with one or more common characteristics such as age, gender, eligibility category, and geographic region) without seeking CMS approval for the change (different rules apply for states with approved rate ranges per cell).21 To make a larger change, states must submit a rate amendment for federal approval that addresses and accounts for all differences from the most recently certified rates.

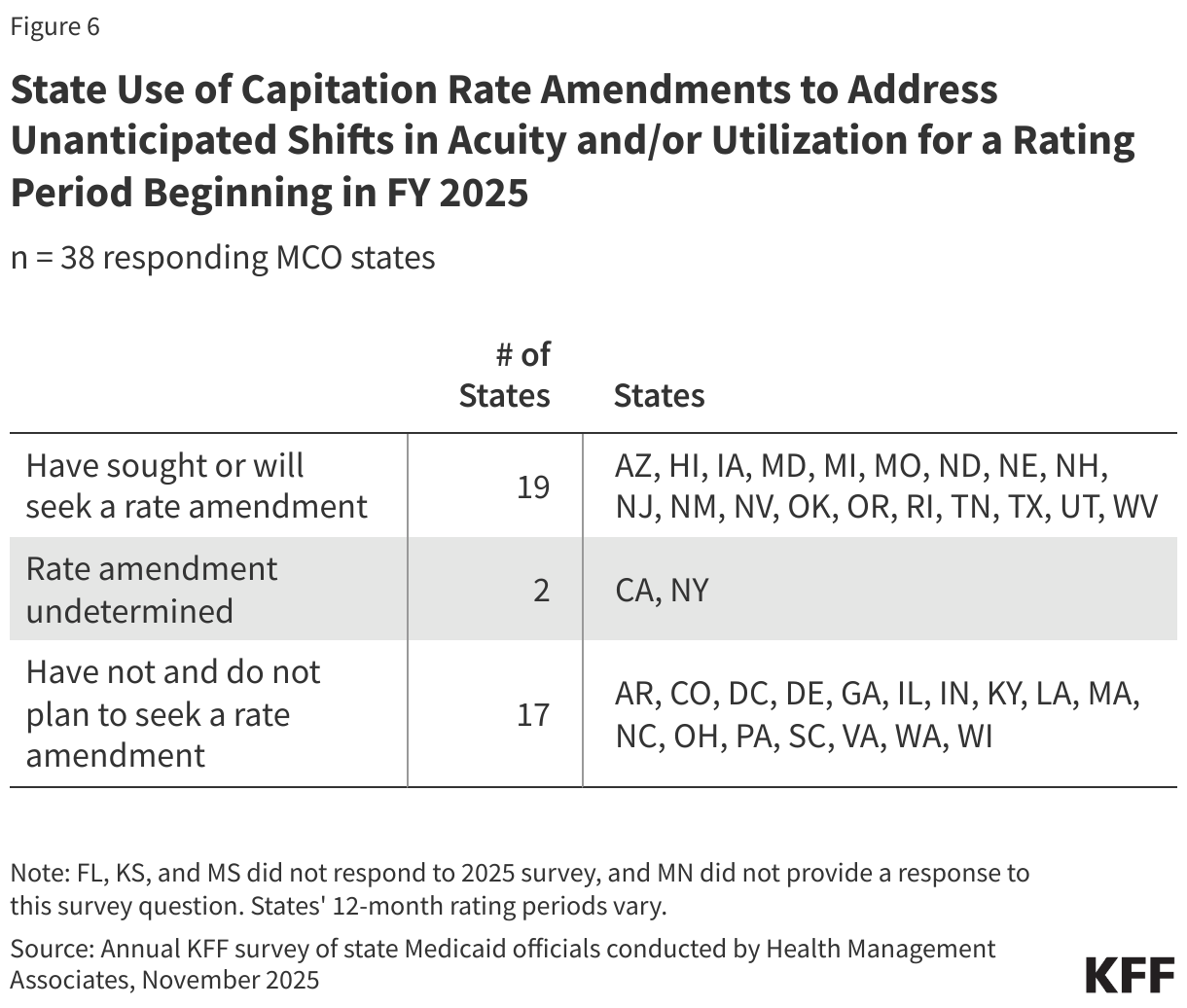

During the unwinding of the pandemic-era Medicaid continuous enrollment provision, millions of people were disenrolled and states and plans faced considerable rate setting uncertainty. Higher member risk and utilization patterns began to emerge by late 2023, and many states sought federal approval to adjust rates to address these shifts in FY 2024. This year’s survey asked states whether they have or will seek CMS approval for a capitation rate amendment to certified rates to address unanticipated shifts in acuity and/or utilization in the rating period that began in FY 2025.

Half of responding MCO states (19 of 38) reported seeking CMS approval for a capitation rate amendment to address unanticipated shifts in acuity and/or utilization for a rating period beginning in FY 2025 (Figure 6). Of the 19 states that reported seeking rate amendments, nearly all reported that the amendment(s) resulted in an increase to capitation rates and about two-thirds reported that the changes applied retrospectively (i.e., adjusted capitation rates for a period that already passed).

During the unwinding period, state actuaries used a variety of approaches to account for changes in cost, utilization, and member acuity.22 This year’s survey included questions to better understand capitation rate setting challenges in the post-unwinding environment. Some states noted making significant changes to the process for developing actuarially sound capitation rates post-unwinding, including the incorporation of acuity adjustments and mid-year reviews of rates to determine if changes are appropriate.

Most responding MCO states reported experiencing or expecting to experience new or notable challenges setting capitation rates for rating period(s) that begin in FY 2026. Many of these states reported challenges due to higher acuity and utilization trends. Some states reported challenges with projecting future pharmacy trends and costs. A few states also mentioned rising medical costs (e.g., inpatient hospital costs) as well as state budgetary pressures and uncertainty. Many states anticipate challenges with projecting potential impacts of federal policy changes effective after FY 2026. This includes work requirements and more frequent eligibility redeterminations for expansion adults under the recently passed reconciliation law, which has implications for member enrollment and acuity (on average). Several states also mentioned challenges with calculating SDPs stemming from regulatory changes (e.g., the 2024 managed care rule’s prohibition on separate terms), and a few states mentioned uncertainty regarding the reconciliation law’s limits on SDPs.

Prior Authorization and Artificial Intelligence (AI)

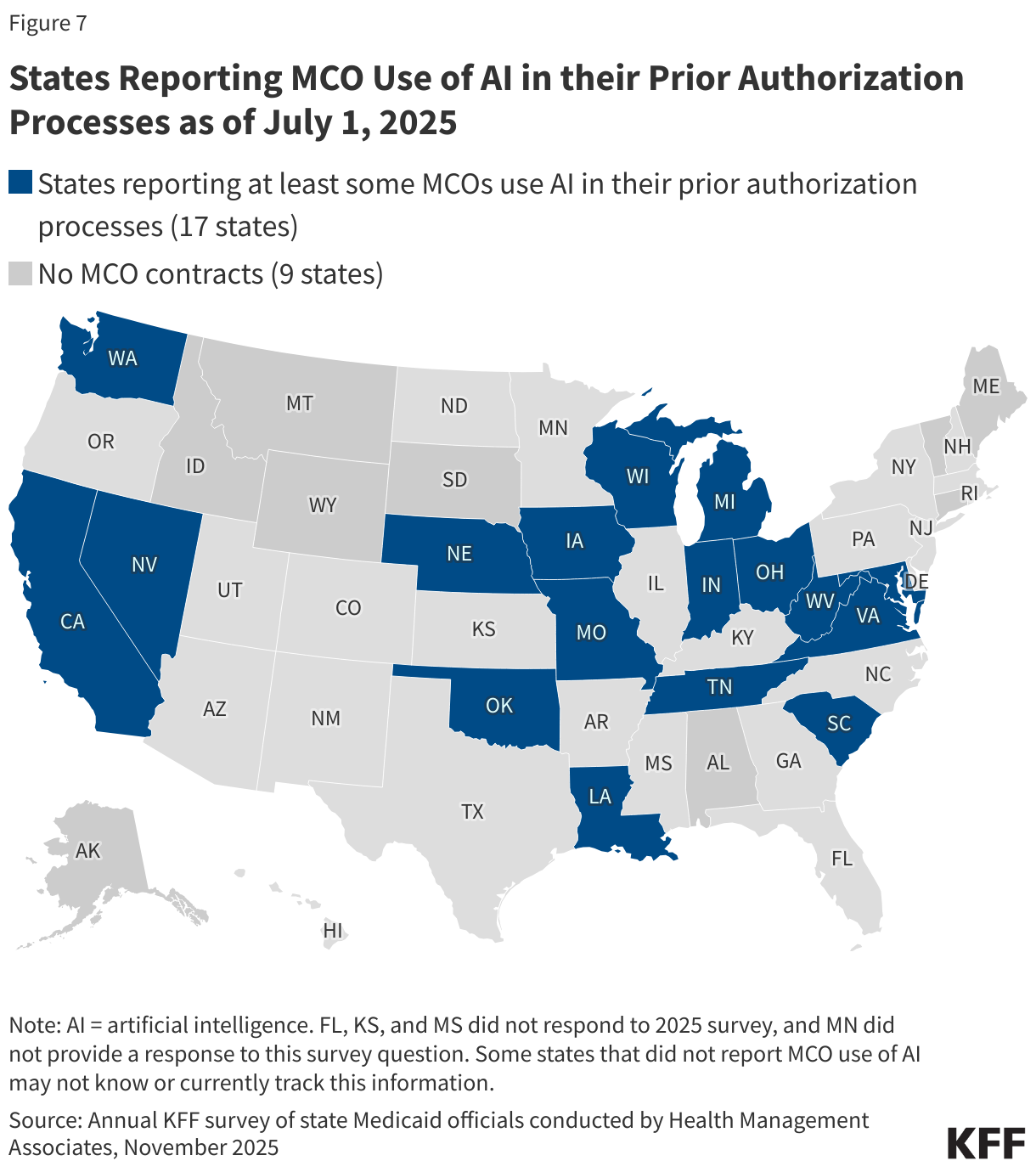

While health insurers are increasingly using AI to automate parts of the prior authorization process, there is limited information available about its use and impact within Medicaid managed care. The Medicaid and CHIP Payment And Access Commission (MACPAC) found that while there are potential benefits of automation in prior authorization such as administrative efficiencies and faster processing times, it may also pose potential risks or challenges depending on how it is administered and monitored. In the absence of comprehensive federal policy governing AI use and oversight in prior authorization, some states have taken steps to regulate or monitor use of AI by health plans. A November 2024 report from the National Association of Insurance Commissioners highlighted that transparency to consumers, providers, and regulators is an important component of AI oversight. This year’s survey asked states whether the MCOs with which they contract use AI in their prior authorization processes as of July 1, 2025.23

Nearly half of responding MCO states (17 of 38) reported knowledge of at least some of the MCOs with which they contract using AI in their prior authorization processes as of July 1, 2025 (Figure 7). At least two states (Oklahoma and South Carolina) reported that AI is used only for prior authorization approvals (vs. use for denials/adverse determinations). Some states that did not report MCO usage of AI may not know or currently track this information.

Less than one-quarter of responding MCO states (7 of 38) reported requiring MCOs to disclose the use of AI in prior authorization processes. States were asked if they require MCOs to disclose the use of AI in prior authorization processes (to the state Medicaid agency, enrollees, and/or providers) as of July 1, 2025. Seven states (California, District of Columbia, Georgia, Indiana, Nebraska, Tennessee, and Virginia) reported requiring disclosure to the state Medicaid agency. Five of those states (District of Columbia, Indiana, Nebraska, Tennessee, and Virginia) indicated MCOs must submit a request to use AI to the state technology officer or Medicaid agency for review before implementation. Three states (California, Georgia, and Indiana) reported requiring disclosure to enrollees and providers.

State examples of AI disclosure requirements include:

- In California, MCOs are required to disclose the use and oversight of AI tools in their written utilization management policies and procedures. These documents must be made available to providers, enrollees, and the public upon request.

- Indiana has adopted an AI policy governing the use of AI technologies across all state agencies. In alignment with this policy, the state Medicaid agency requires plans to submit any AI tools or systems for formal review. Indiana’s State Agency AI Systems Standard requires MCOs to conduct a readiness assessment prior to implementation or use of any AI tool or system as well as annual follow-up or ad hoc assessments when significant changes are made to the AI tool.

- In Tennessee, MCOs are required to contact the state Medicaid agency’s AI Governance Committee when the use of AI is contemplated in any capacity. MCOs must share what vendor is being considered, what purpose the AI is serving, how outputs are being verified, what system risks and vulnerabilities exist, and how data is being safeguarded.

Many states reported concerns and challenges with the use of AI in MCO prior authorization processes. When asked to describe their top concerns or challenges (if any) with the use of AI in MCO prior authorization processes, states frequently cited potential for bias, improper denials, privacy and security risks, and inadequate human/clinician oversight. Some states also reported concerns with ensuring compliance with federal and state requirements, complexities related to oversight, and transparency of AI decision-making processes.

Several states reported implementing new or expanded oversight activities or adopting other safeguards in FY 2025 or 2026 to support appropriate use of AI in MCO prior authorization processes. For example, five states (California, Maryland, Nevada, New Hampshire, and Ohio) reported introducing or plans to introduce language in MCO contracts regarding the use of AI. Texas reported working to develop a standard process to review MCO AI tools prior to implementation.

Provider Rates and Taxes

Context

States have substantial flexibility to establish Medicaid provider reimbursement methodologies and amounts, especially within a fee-for-service (FFS) delivery system where a state Medicaid agency pays providers or groups of providers directly. While states with capitated managed care arrangements are generally not permitted to direct how their contracted managed care organizations (MCOs) pay providers, state determined FFS rates remain important benchmarks for MCO payments in most states.

Fee-for-Service Rates. Federal law and regulations grant states broad latitude to determine FFS provider payments but also requires that payments be sufficient to ensure that Medicaid enrollees have access to care that is equal to the level of access enjoyed by the general population in the same geographic area.24 CMS reviews and approves state changes to FFS payment methodologies through the Medicaid state plan amendment process.25 In addition to FFS provider payments, states are permitted to make multiple types of “supplemental” payments. States make these payments for a variety of purposes including to supplement Medicaid “base” FFS payment rates that often do not fully cover provider costs as well as to help support the costs of care for uninsured patients. States may also develop special payment policies or tailor supplemental payments to specific provider types, including rural hospitals or other rural providers, to ensure access.

Provider Rate Implications of Economic and Fiscal Conditions. Historically, FFS provider rate changes have generally reflected broader economic conditions. During economic or fiscal downturns that weaken state revenue collections, states have typically turned to provider rate restrictions to contain costs. Conversely, states are more likely to increase provider rates during periods of recovery and revenue growth. During the COVID-19 public health emergency, however, states were able to generally avoid rate cuts due to temporary federal support from the pandemic-related enhanced Medicaid matching funds as well as enhanced funding for home and community-based services (HCBS). With pandemic-era relief largely expired and growing fiscal uncertainty driven, in part, by slowing state revenue growth and federal funding cuts, states are again facing budget pressures, leading some to turn to provider rate restrictions to close budget gaps.

Managed Care Provider Rates. States pay Medicaid MCOs a set per member per month (“capitation”) payment for the Medicaid services specified in their contracts. Under federal law, payments to Medicaid MCOs must be actuarially sound. Actuarial soundness means that “the capitation rates are projected to provide for all reasonable, appropriate, and attainable costs that are required under the terms of the contract and for the operation of the managed care plan for the time period and the population covered under the terms of the contract.” Plan rates are usually set for a 12-month rating period and must be reviewed and approved by CMS each year.

State Directed Payments. States are generally prohibited from contractually directing how an MCO pays its providers.26 Subject to CMS approval, however, states may implement certain “state directed payments” (SDPs)27 that require MCOs to adopt minimum or maximum provider payment fee schedules, provide uniform dollar or percentage increases to network providers (above base payment rates), or implement value-based provider payment arrangements. The 2024 Managed Care rule codified an SDP upper limit for hospitals, nursing facilities, and professional services at an academic medical center equal to the “average commercial rate” (ACR), which is generally higher than the Medicare payment ceiling used for other Medicaid fee-for-service supplemental payments. The 2025 federal budget reconciliation law (H.R.1) directs HHS to revise SDP regulations to cap the total payment rate for inpatient hospital and nursing facility services at 100% of the total published Medicare payment rate for states that have adopted the Medicaid expansion and at 110%28 of the total published Medicare payment rate for states that have not adopted the expansion. Previously approved and submitted SDPs are initially grandfathered29 but will be reduced by ten percentage points each year (starting January 1, 2028) until they reach the allowable Medicare-related payment limit. States may continue funding for approved and submitted SDPs at their current expenditure levels until January 1, 2028, at which point they will be reduced. The Congressional Budget Office (CBO) estimated revising the payment limit for state directed payments will result in $149 billion in federal savings over ten years.

Provider Taxes. States have considerable flexibility in determining how to finance the non-federal share of state Medicaid payments, within certain limits. In addition to state general funds appropriated directly to the Medicaid program, most states also rely on funding from health care providers and local governments generated through provider taxes, user fees, intergovernmental transfers (IGTs), and certified public expenditures (CPEs). Over time, states have increased their reliance on provider taxes, with expansions often driven by economic downturns or a desire to fund eligibility expansions or provider reimbursement increases. Federal regulations30 require provider taxes to be broad-based (imposed on all non-governmental entities, items, and services within a class), and uniform (consistent in amount and scope across the entities, items, or services to which it applies), and must not hold taxpayers harmless (i.e., directly or indirectly guarantee that the provider will be repaid for all or a portion of the tax). Also, a provider tax will meet the hold harmless “safe harbor threshold” if it generates revenue that does not exceed 6% of net patient revenue.

H.R.1 imposes significant new restrictions on states’ ability to generate Medicaid provider tax revenue. Effective upon passage, the law prohibits states from establishing any new provider taxes or from increasing the rates of existing taxes. It also revises the conditions under which states may receive a waiver of the requirement that taxes be broad-based and uniform making some taxes currently in place impermissible in future years.31 These provisions overlap with a proposed rule released May 12, 2025. Beginning in federal fiscal year (FFY) 2028, H.R.1 also gradually reduces the safe harbor limit for states that have adopted the ACA expansion by 0.5% annually until the safe harbor limit reaches 3.5% in FFY 2032. The new limit also applies to local government taxes in expansion states. However, this revised threshold does not apply to provider taxes on nursing facilities and intermediate care facilities. CBO estimated these provider tax policy changes will reduce federal Medicaid spending by $191 billion over ten years (or more than $200 billion after also accounting for the uniformity changes).

This section provides information about:

- Hospital reimbursement

- Nursing facility reimbursement

- FFS reimbursement rates for other provider types

- Rural payment adjustments

- Provider taxes

Findings

FFS Reimbursement Rates

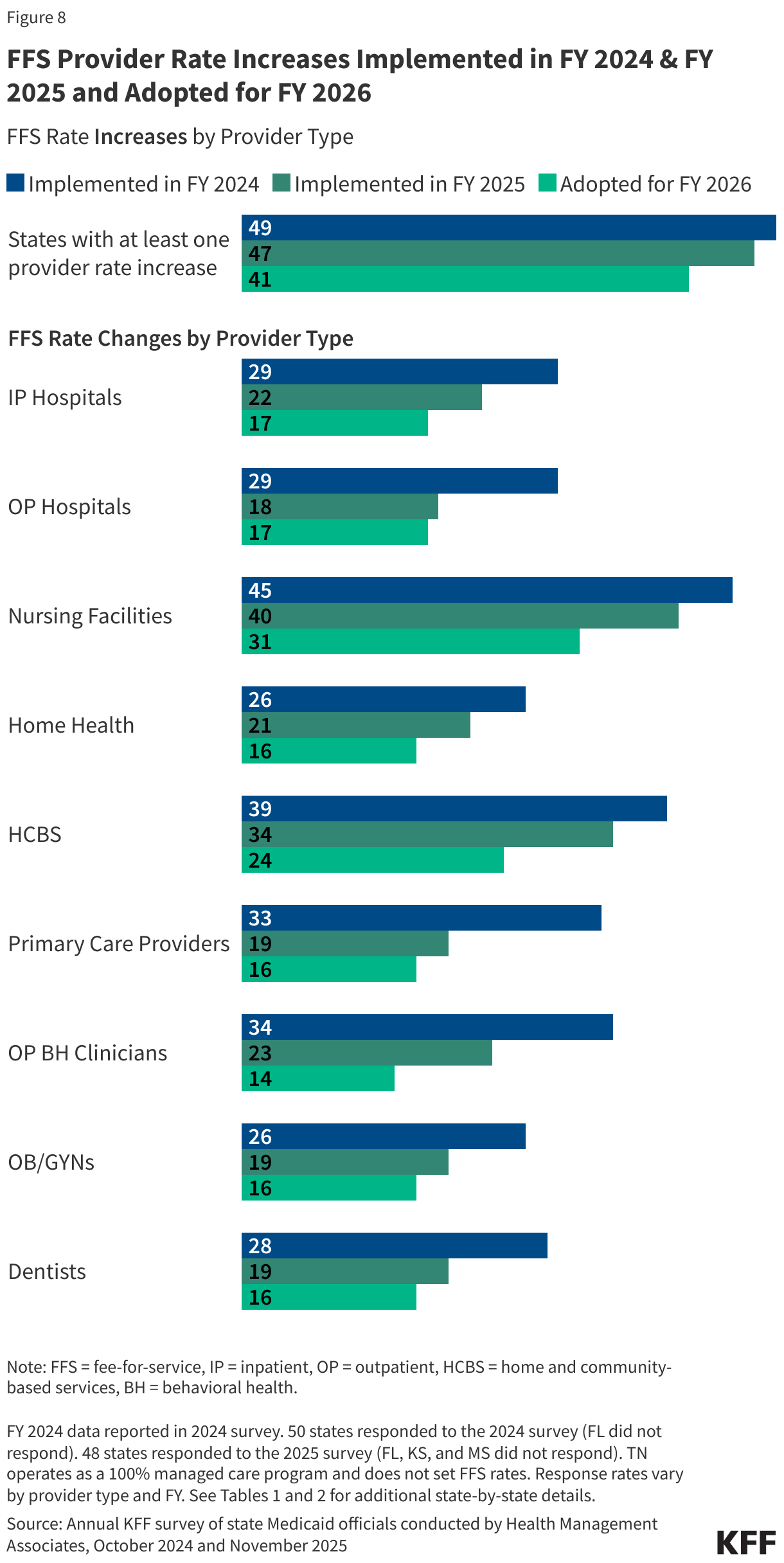

At the time of the survey, responding states had implemented or were planning more FFS rate increases than rate restrictions in both FY 2025 and FY 2026 (Tables 1 and 2). More than three-quarters of responding states in FY 2025 (47 of 48) and three-quarters of responding states in FY 2026 (41 of 48) reported implementing rate increases for at least one category of provider, comparable to prior survey results for 2024 (49 of 50 responding states). However, across many individual provider types, notably fewer states reported rate increases in FY 2025, or planned for FY 2026, compared with FY 2024 (Figure 8) (or the previous four fiscal years FY 2021-FY 2024), likely reflecting the expiration of pandemic-era fiscal relief and growing fiscal uncertainty driven by softening state revenue growth and federal funding reductions.

States continue to report rate increases for nursing facilities and HCBS providers more often than for other provider categories (Figure 8). Many states employ cost-based reimbursement methodologies for nursing facility services that automatically adjust for inflation and other cost factors during the rate setting process. Several states also commented that HCBS increases reflected inflationary adjustments, were implemented following rate or cost studies, or were tied to minimum wage changes. Likely reflecting the ongoing staffing-related challenges impacting nursing facility services, several states reported more significant nursing facility rate increases:

- Maine reported increasing rates in January 2025 as part of broader reform of its nursing facility reimbursement methodology which includes a quality bonus pool that will reward improvements in staff stability and resident and family satisfaction as well as reductions in the inappropriate use of antipsychotic medications. Maine also reported making one-time supplemental payments to nursing facilities in FY 2025 to address continued post-pandemic cost challenges and to assist facilities with the transition to the new reimbursement methodology.

- Oklahoma increased rates by 8.96% in FY 2025, and Pennsylvania increased rates by 7.04% effective January 1, 2025.

- Rhode Island increased rates by 14.5%, effective October 1, 2024, following the completion of a Medicaid rate review, and reported plans to transition from a Resource Utilization Groups (RUGs)-based reimbursement methodology to a Patient-Driven Payment Model (PDPM) methodology on October 1, 2025.

- Washington reported increasing overall rates by 10% in FY 2025 to ensure a stable transition from a RUGs-based reimbursement methodology to a PDPM methodology.

However, only a few states reported notable HCBS increases:

- Michigan increased personal care services rates by 37.4% for agency providers and 16.5% for individual providers 16.5% in FY 2025.

- Washington reported a 7.5% increase for home health and private duty nursing providers in FY 2025.

- Wisconsin does not make adult HCBS FFS payments but did implement a minimum fee schedule for adult home and community-based services as of October 1, 2024, that MCOs must pay certain HCBS providers. The change, funded from the state’s American Rescue Plan Act (ARPA) allocation, was estimated to result in an average 15% rate increase for most supportive home care services.

About half of states (23) implemented FFS rate increases for one or more outpatient behavioral health providers in FY 2025; fewer states (14) are planning to implement behavioral health rate increases in FY 2026 (Figure 8). Several states commented that increases reflected inflationary adjustments or were driven by rate studies. A few states mentioned more notable increases:

- In addition to inflationary adjustments for other behavioral health services, Alaska increased rates for autism services by 12.1% effective July 1, 2024.

- Iowa reported FY 2025 rate increases of approximately 10.6%.

- Michigan reported increasing psychiatric procedure codes by 4% and non-physician behavioral health rates (e.g., for psychologists, professional counselors, family and marriage therapists, and social workers) from 75% of physician rates to 90% for FY 2025.

- Minnesota added an annual inflation adjustment (using the CMS Medicare Economic Index) to certain behavioral health services rates in FY 2025 and is increasing behavioral health rates to 83% of Medicare rates in FY 2026.

Box 1: Rural Payment Adjustments.

Rural hospitals often face financial pressures related to lower occupancy rates, high levels of uncompensated care, and other challenges. Many have recently closed or are at risk of closure as a result of these pressures. States were asked if they have any Medicaid payment adjustments or enhancements in place in FY 2026 designed to promote access to hospitals or other providers in rural areas — about half of states reported at least one policy to support rural providers.

Many states have adopted special payment policies for rural hospitals, including cost-based reimbursement for Critical Access Hospitals (CAHs) and targeted supplemental payments. In addition to these mechanisms, states reported enhanced base rates, add on payments, and wage index adjustments for rural hospitals and other providers. A handful of states reported that they target rural payment adjustments or enhancements to specific services, including maternity, psychiatry, and dental. For example, at least three states (Georgia, Texas, Wyoming) support maternity services in rural areas with add-on payments or other payment policies, Ohio offers an enhanced fee schedule for dental services in rural counties, and Maine makes add-on payments for ambulance providers and pharmacies located in rural areas. Michigan reported an Inpatient and Outpatient Rural Hospital Pool, partially supported by Medicaid funds, to incentivize improvements by rural hospitals in quality and efficiency metrics.

Several states also noted plans to leverage the Rural Health Transformation Program included in H.R.1. This program provides $50 billion in funding for state grants that can be used to support rural areas in a variety of ways including to pay for health care services, expand the rural health workforce, promote care interventions, and provide technical assistance with system transformation.

Six states in FY 2025 and six states in FY 2026 restricted rates for at least one provider type, a notable uptick compared with the number of states reporting provider rate decreases for FY 2024 (1 state) and FY 2023 (2 states).

Most of the reductions reported were limited or targeted:

- Three of the four states reporting primary care and/or OB/GYN rate reductions in FY 2025 (Idaho, Indiana, and Maine) commented that the state’s rates were benchmarked to Medicare rates resulting in a net decrease, overall, as of January 1, 2025.

- California reported that, for FY 2025, Designated Public Hospitals (DPHs)32 saw an average rate decrease of 13.4% while its non-DPH hospitals that follow a DRG methodology saw base rate increases of 4.8%. Maryland and Massachusetts also reported decreases to inpatient and outpatient hospital FFS base rates for FY 2025.

- Nebraska reported reductions to Applied Behavioral Analysis (ABA) rates in FY 2026.

- Wyoming reported decreases to some HCBS rates in FY 2026 due to the expiration of ARPA enhanced HCBS funding.

A few states, however, reported broader reductions in FY 2026 driven by the need to reduce overall Medicaid expenditures:

- Idaho officials announced 4% across the board reductions, starting September 1, 2025, for all provider types and services, citing unsustainable health care cost growth. The state Department of Health and Welfare noted the cuts will save $36.8 million in FY 2026.

- Washington reported FY 2026 rate reductions to selected programs and codes, including certain primary care (excluding E&M) and certain mental health codes, dental rate cuts for both adults and children, and a modest (less than 1%) rate reduction for nursing facilities.

- Also, at the time of this report, the North Carolina legislature was considering legislation to increase FY 2026 Medicaid appropriations for the purpose of reversing 3% across the board rate reductions that went into effect on October 1, 2025, but ended its October 2025 session without taking action on the Medicaid reductions or passing a full state budget.

While not counted as rate reductions, two states reported a pause or reversal of previously planned increases: California reported pausing provider tax-funded FY 2026 rate increases for primary care providers, OB/GYNs, and behavioral health clinicians, due to provisions in H.R.1 affecting those taxes, and in August 2025, Colorado Governor Polis announced the state’s plans to reverse the 1.6% across the board increases in FY 2026 Medicaid provider rates (as of October 1, 2025).

Provider Taxes

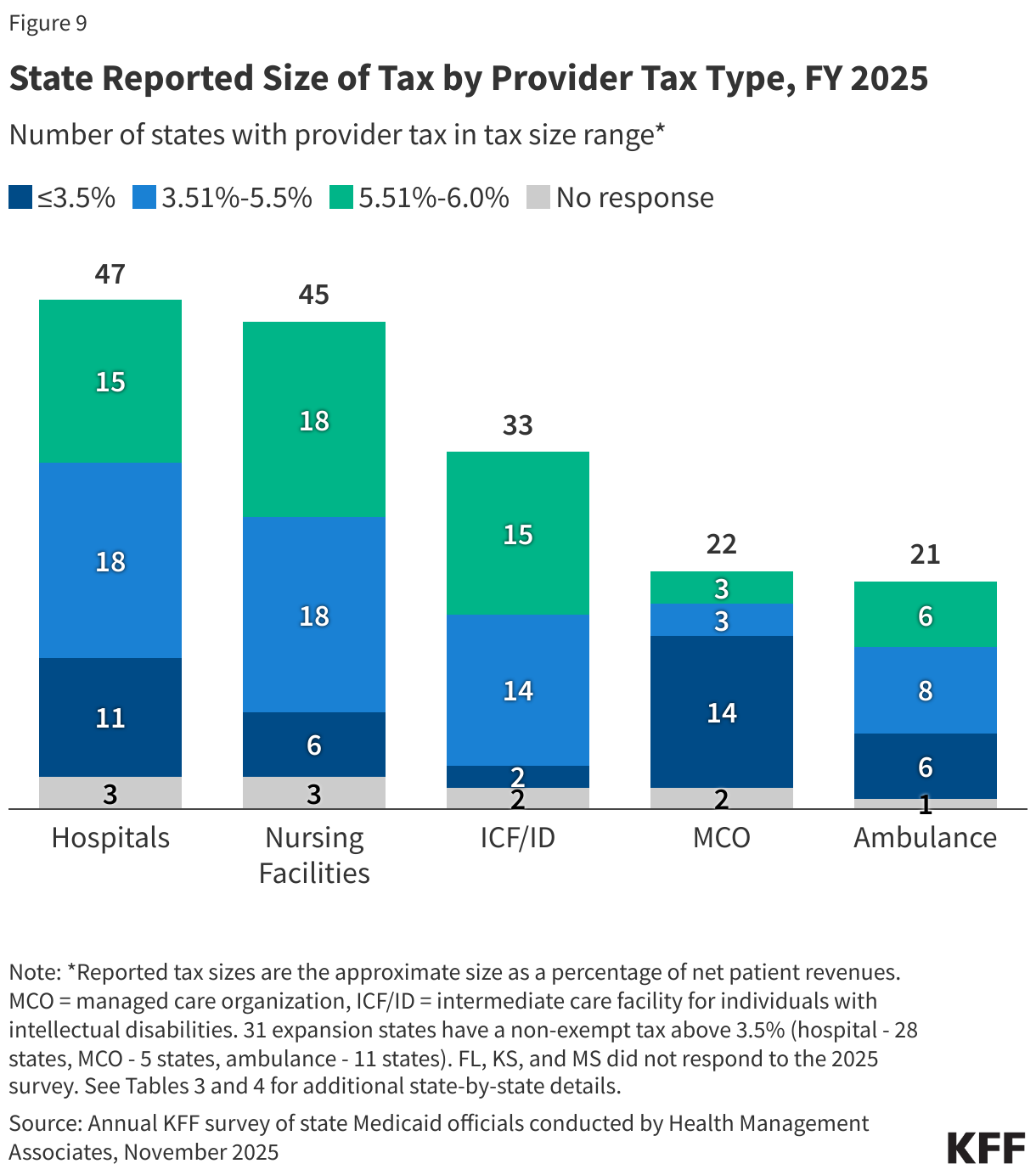

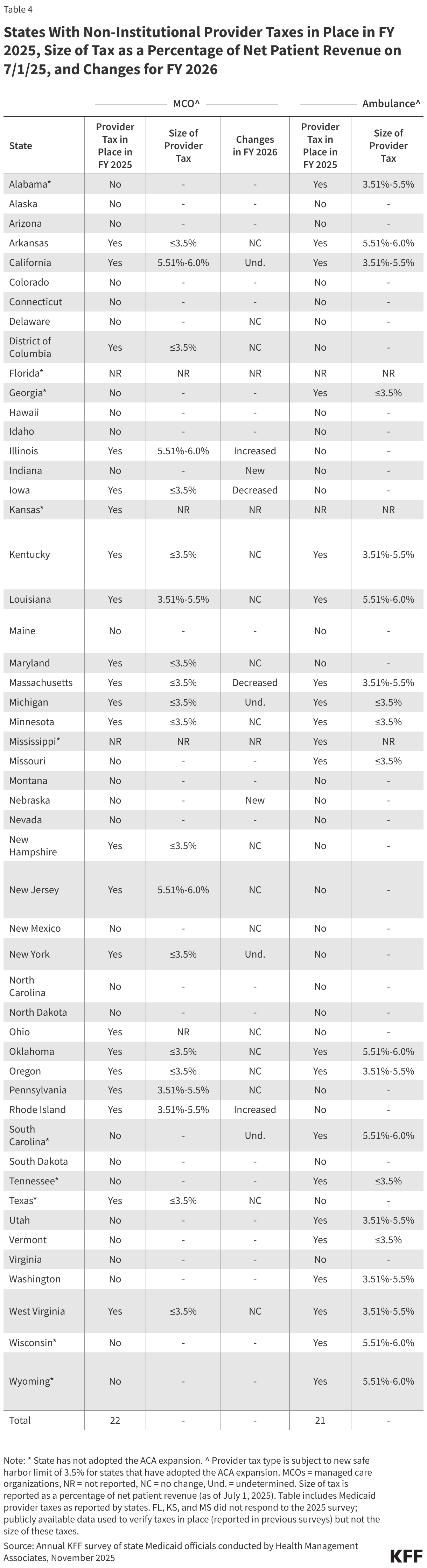

Almost all states rely on provider taxes and fees to fund a portion of the non-federal share of Medicaid costs. Since 2013, all states, except Alaska, have had at least one provider tax or fee in place, and these provider taxes and fees comprised a significant share (a median across states of 18%) of the non-federal share of total Medicaid payments in FY 2026 according to KFF analysis, though there was considerable variation across states. In FY 2025, most states had multiple provider taxes in place (Tables 3 and 4).33 The most common Medicaid provider taxes in place in FY 2025 were taxes on hospitals (47 states) and nursing facilities (45 states), intermediate care facilities for individuals with intellectual disabilities (33 states), MCOs34 (22 states), and ambulance providers (21 states) (Figure 9 and Tables 3 and 4). Provider tax revenues are most likely to be near the 6% safe harbor limit for nursing facilities followed by hospitals and intermediate care facilities for people with intellectual or developmental disabilities (Figure 9 and Table 3).

Most responding states indicated provider tax revenue is used to increase FFS or MCO payment rates or supplemental payments to providers. Some states reported using revenue from provider taxes to finance eligibility expansions, including the ACA Medicaid expansion. In contrast, some states indicated provider tax revenues are used generally to support the Medicaid program/state share while other states indicated provider tax revenues end up in the state general fund and are not earmarked for Medicaid specifically.

Effective upon passage (July 4, 2025) the reconciliation law prohibits states from establishing any new provider taxes or from increasing the rates of existing taxes. H.R.1 also revises the conditions under which states may receive a waiver of the requirement that taxes be broad-based and uniform – i.e., generally redistributive. This provision, which is likely to result in some current taxes becoming impermissible (especially certain MCO taxes), is effective upon passage, but the HHS secretary has discretion to apply a transition period of up to three fiscal years.35

Beginning in FFY 2028, H.R.1 reduces the safe harbor limit for states that have adopted the ACA expansion by 0.5% annually until the safe harbor limit reaches 3.5% in FFY 2032. The new limit applies to taxes on all providers except nursing facilities and intermediate care facilities. As of July 1, 2025, 31 Medicaid expansion states reported having a non-exempt provider tax exceeding 3.5% (Table 4).36

At the time of the survey, four states reported plans to add new taxes in FY 2026 and 18 states37 reported plans to increase one or more taxes in FY 2026, but these plans may be affected by the passage of H.R.1. The four states reporting plans to add new taxes in FY 2026 include Montana and Nevada (adding new ambulance taxes) and Indiana and Nebraska (adding new MCO taxes). Increases reported in FY 2026 were most commonly for taxes on hospitals. No states reported plans to eliminate taxes in FY 2026 but six states reported plans to decrease one or more provider taxes in FY 2026: Arkansas and Washington are planning to decrease their ambulance taxes; Idaho is planning to decrease its tax on intermediate care facilities for individuals with intellectual disabilities; Iowa and Massachusetts are planning to decrease their MCO taxes; and Pennsylvania is planning to decrease its nursing facility tax.

Several states commented on the implications of the 2025 reconciliation law safe harbor changes for their states in the future. Some noted the potential for significant state budget impacts while others noted that provider payment reductions would result. A few states commented that state directed payments funded with provider tax revenues would need to be reduced if states were unable to offset lost provider tax revenues from other state revenue sources.

Benefits

Context

Scope of Medicaid Benefits. State Medicaid programs must cover a comprehensive set of “mandatory” benefits, including items and services typically excluded from traditional insurance such as non-emergency medical transportation and long-term care. States may additionally cover a broad range of optional benefits defined in statute or permissible under other authorities such as Section 1115 waivers. All states cover prescription drugs as an optional benefit, and most states cover other optional services such as physical therapy, eyeglasses, and adult dental care. While most home and community-based services (HCBS) are optional and all states offer some HCBS through Medicaid, changes to HCBS services are tracked in a separate KFF survey.

States may apply reasonable service limits based on medical necessity or to control utilization, but once covered, services must be “sufficient in amount, duration and scope to reasonably achieve their purpose.”38,39 There are additional protections and flexibilities for children and youth up to age 2140 under the Early and Periodic Screening, Diagnostic, and Treatment (EPSDT). This benefit ensures access to any medically necessary service identified in federal Medicaid statute without limitation, including services the state does not otherwise cover. EPSDT is especially important for children with disabilities because it allows children access to a broader set of benefits to address complex health needs.

The ability to cover optional benefits and place limits on items and services results in wide variation across states. State Medicaid benefit design is also impacted by prevailing economic and fiscal conditions: states are more likely to adopt restrictions or limit benefits in response to state budgetary pressures and expand or restore benefits as conditions improve. In the last few years, many states expanded coverage of behavioral health, maternity, and dental services. States also invested in new Medicaid benefits to address social determinants of health (SDOH) and associated health-related social needs (HRSN) (e.g., housing, nutrition). In March 2025, however, the Trump administration rescinded the Biden administration HRSN Section 1115 waiver guidance. CMS has indicated that, while existing HRSN approvals remain in place, going forward CMS will consider SDOH waiver requests on a case-by-case basis.

In FY 2025 and FY 2026, benefit expansions far outweigh benefit restrictions and limitations (consistent with prior years), but as states face a more tenuous fiscal climate and start to prepare for the impact of the 2025 federal budget reconciliation law (H.R.1), state Medicaid agencies are likely to face increasing pressure to cut or limit optional benefits to reduce Medicaid costs. This section provides information about benefit changes made in FY 2025 or planned for FY 2026.

Findings

Benefit Changes

States were asked about benefit changes implemented during FY 2025 or planned for FY 2026, excluding eligibility expansions, telehealth policy changes, HCBS, and changes made to comply with federal requirements.

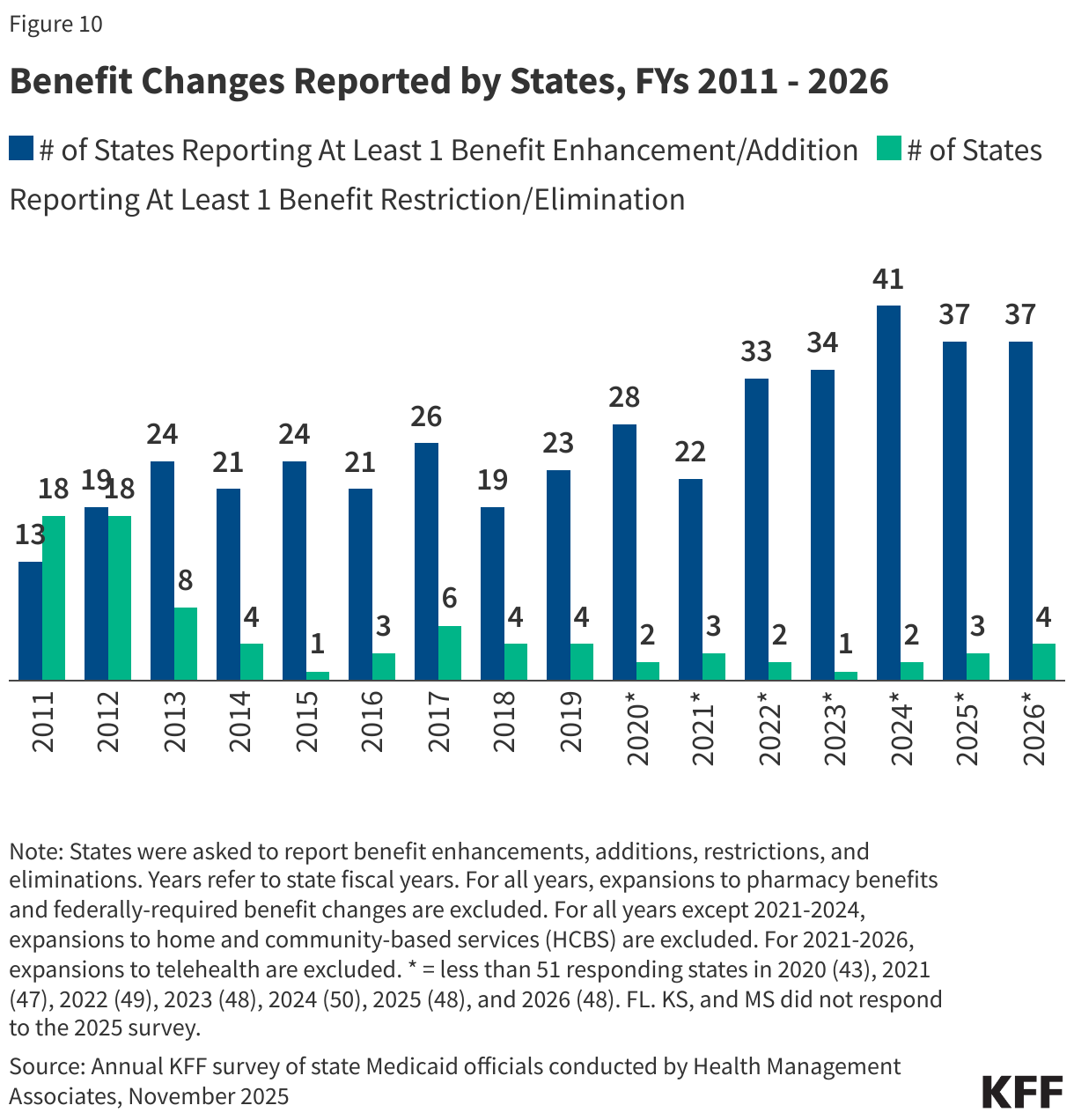

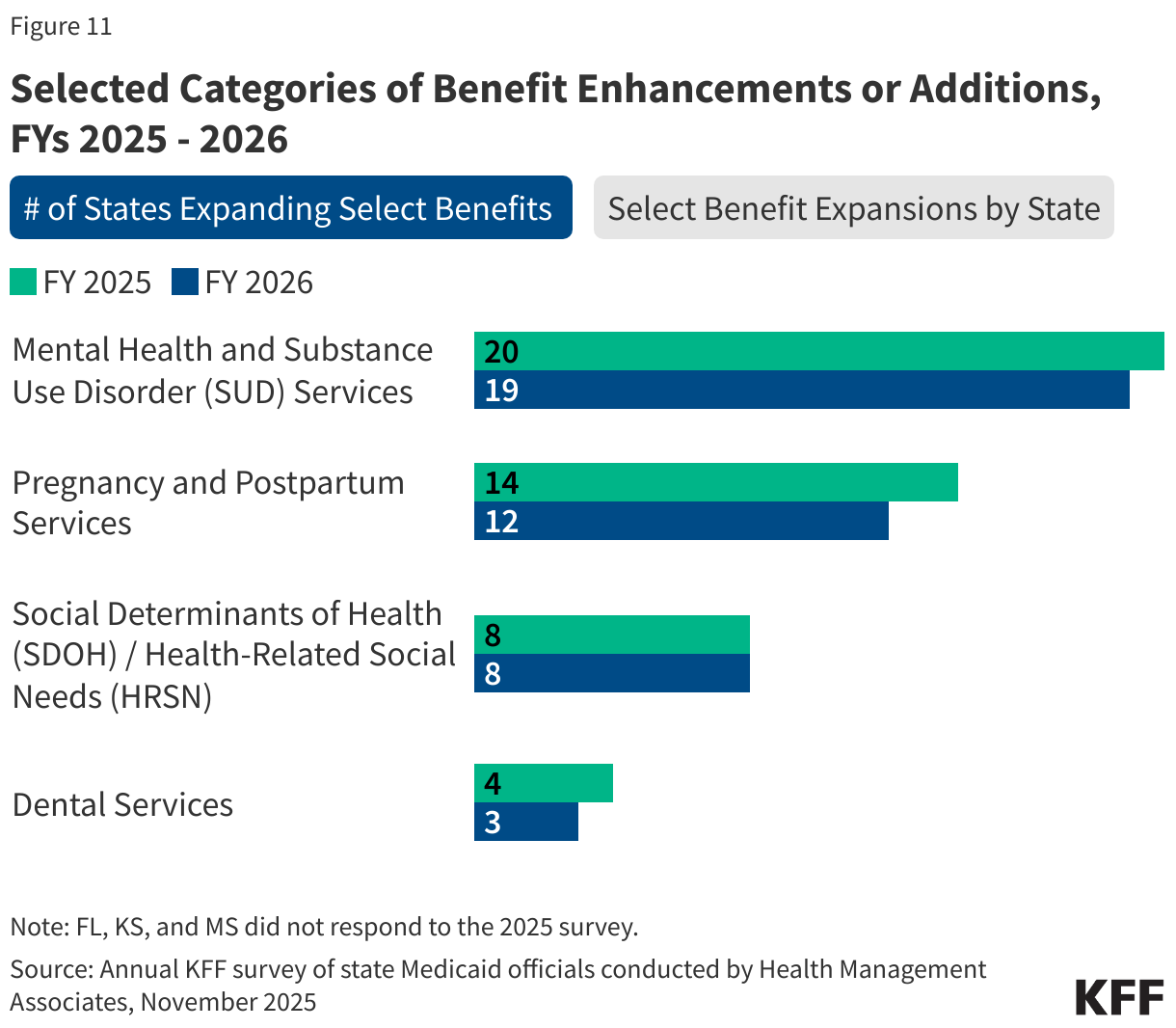

The number of states reporting new benefits and benefit enhancements continues to greatly outpace the number of states reporting benefit cuts and limitations (Figure 10 and Table 5). Thirty-seven states reported new or enhanced benefits in FY 2025, and 36 states reported plans to add or enhance benefits in FY 2026.41 Three states reported benefit cuts or limitations in FY 2025, and four states reported cuts or limitations in FY 2026. There are additional details about benefit enhancements or additions in select benefit categories below (Figure 11).

Behavioral Health Services. Behavioral health services are not a specifically defined category of Medicaid benefits. Some fall under mandatory Medicaid benefit categories (e.g., physician services) while others fall under optional benefit categories (e.g., rehabilitative services). Compared with adults, behavioral health services for children are more comprehensive due to Medicaid’s EPSDT benefit for children. Mental health and substance use disorder (SUD) services continue to be one of the most frequently reported categories of benefit expansions. Consistent with trends in recent years, states reported expanding services across the behavioral health care continuum, particularly community-based behavioral health services. One of the most frequently reported benefit enhancements is the addition or expansion of peer supports. Peer support services are provided by individuals with lived experience and can help enrollees by providing emotional support or navigation of health care or other social services.

- Services for Children and Youth. At least ten states reported expanding behavioral health services for children, youth, and/or families,42 including those involved in the child welfare system. These include therapeutic foster care and parenting support services. For example, Texas implemented certified family partner services for parents, legally authorized representatives, or primary caregivers of Medicaid-eligible children or youth diagnosed with a serious emotional disturbance or MH/SUD condition. Services include introducing the family to the mental health treatment process, modeling advocacy skills, providing information, making referrals, providing skills training, and helping to identify supports for the child and family.

- Crisis Services. At least four states43 reported benefit actions related to the addition or expansion of crisis services, including two states (Maine and Nebraska) enhancing their mobile crisis response.

- Physical and Behavioral Health Integration. Nine states44 reported benefit actions related to promoting more coordinated and integrated physical and behavioral health care, including adding coverage for services provided under the Collaborative Care Model (CoCM) and implementing or expanding Certified Community Behavioral Health Clinics (CCBHCs).45

- Comprehensive Behavioral Health Reforms. A few states reported comprehensive initiatives to expand access to community-based behavioral health services and services to keep individuals living with significant behavioral health needs in the community. For example, California’s BH-CONNECT initiative uses Section 1115 waiver authority to add coverage of evidence-based practices such as assertive community treatment (ACT), coordinated specialty care (CSC) for first episode psychosis, and clubhouse services. BH-Connect will also implement a new incentive program for behavioral health plans and make significant investments in strengthening the behavioral health workforce. Kentucky’s 1915(i) RISE initiative for adults with serious mental illness provides a package of ten wraparound services to promote recovery, including but not limited to assistive technology, case management, housing and tenancy supports, supported education and employment, non-medical transportation, and caregiver respite.

Pregnancy and Postpartum Services. Medicaid covers more than four in ten births nationally and the majority of births in many states. To help reduce maternal morbidity and mortality, as well as address disparities in maternal and infant health outcomes, states continue to expand and enhance covered prenatal, delivery, and postpartum services. Alongside these benefit enhancements, the vast majority of states have implemented a Medicaid 12-month postpartum coverage extension. Fifteen states reported adding or expanding coverage of doula services in FY 2025 or FY 2026.46 Seven states reported new benefits to help parents initiate or maintain breastfeeding, including breast pumps, human donor milk, and lactation consultation.47 Other examples of expanded pregnancy and postpartum services include:

- Illinois added coverage for professional midwife services in FY 2025. In FY 2026, Colorado plans to allow professional midwives as an allowed provider type for home birth services, and Oklahoma plans to add coverage for professional midwives.

- Arkansas and Texas reported adding coverage of community health workers for pregnant individuals.

- In FY 2025, Tennessee began covering 100 diapers per month for children under age two under its TennCare 1115 waiver. In FY 2026, New Mexico and New Jersey will cover home-delivered, medically tailored meals for pregnant and postpartum individuals with diabetes under approved Section 1115 waivers.

- In FY 2025, Illinois and New Jersey reported expansions of home visiting services during and after pregnancy.

- Nebraska reported implementing the Prenatal Plus Program, which provides services for pregnant individuals at risk of having a negative maternal or infant health outcome. Services include nutrition counseling, psychosocial counseling and support, education and health promotion, breastfeeding support, and targeted case management.

- Massachusetts reported coverage of perinatal peer recovery coach and recovery support navigator services for perinatal enrollees navigating substance use disorder in FY 2026.

Services Targeting Social Determinants of Health (SDOH). Outside of Medicaid home and community-based services programs, state Medicaid programs have more limited flexibility to address enrollee social needs (e.g., housing, food, transportation, etc.). Certain options exist under Medicaid state plan authority as well as Section 1115 waiver authority to add non-clinical benefits. The Biden administration expanded flexibility under Section 1115 for states to address enrollee social needs (see Box 2 for more information). In FY 2025 and FY 2026, states reported adding or expanding coverage for services targeting SDOH (Figure 11), including housing services and supports, nutrition services, and medical respite (also known as recuperative care or pre-procedure/post-hospitalization housing), approved under several different authorities.

Box 2: Section 1115 “HRSN” Waivers

In 2022, CMS (under the Biden administration) announced a demonstration waiver opportunity to expand the tools available to states to address enrollee “health-related social needs” (or “HRSN”) including housing instability, homelessness, and nutrition insecurity, building on CMS’s 2021 guidance. In 2023, CMS issued a detailed Medicaid and CHIP HRSN Framework accompanied by an Informational Bulletin, which were updated in 2024.

In March 2025, however, the Trump administration rescinded the Biden administration HRSN guidance. CMS has indicated that, while existing HRSN approvals remain in place, going forward CMS will consider SDOH requests (including renewals) on a case-by-case basis.

Dental Services. While EPSDT requires states to provide comprehensive dental services for children, dental benefits are optional for adults. In recent surveys, several states reported expanding adult dental coverage from limited benefits (e.g., extractions or emergency services) to more comprehensive coverage (e.g., diagnostic, preventive, and restorative services). In this year’s survey, Utah reported adding comprehensive dental benefits for adults, and Georgia reported expanding its adult dental benefit to include diagnostic, preventive, restorative, periodontal, prosthodontic, orthodontic, endodontic, emergency dental services, and oral surgery.48 Other dental benefit expansions include:

- Nebraska and Illinois expanded coverage of dental anesthesia in FY 2026. Colorado reported removing prior authorization requirements for dozens of adult and child dental services and procedures in FY 2025. Texas expanded its children’s dental benefit in FY 2025, adding oral health literacy education.

Other State Benefit Expansions. In this year’s survey, several states reported expanding other optional benefits covered by their Medicaid programs. Two states (Illinois and New Jersey) reported adding palliative care benefits, and one state (Arizona) reported adding traditional healing services.

- School-based services. Schools can be a key setting for providing services to Medicaid-covered children. Eight states (Alaska, Maryland, Nebraska, New Jersey, Ohio, Oklahoma, Utah, and Vermont) report expanding their school-based services programs. Examples include adding services (e.g., screening services, psychological testing and evaluations, and individual and group therapy) and provider types (e.g., school psychologists). As reported in last year’s survey, states are also continuing to extend services to children who do not have an Individualized Education Program (IEP) or Individualized Family Service Plan (IFSP).

- Pre-Release Services. In April 2023, the Biden administration released guidance encouraging states to apply for a new Section 1115 demonstration opportunity to test transition-related strategies to support community reentry for people who are incarcerated. This demonstration allows states a partial waiver of the inmate exclusion policy, which prohibits Medicaid from paying for services provided during incarceration (except for inpatient services). States with governors in both political parties have pursued these waivers. In this year’s survey, several states reported adding pre-release services (e.g., case management and medication assisted treatment (MAT)) under approved 1115 waivers in FY 2025 or FY 2026. Due to state funding uncertainty or capacity challenges (in part from the passage of H.R.1), a few states (Maine, Michigan, and New Mexico) reported that implementation or expansion of pre-release services is on hold or may be delayed, and Oregon has cancelled implementation of its pre-release waiver initiative.

Most benefit restrictions in FY 2025 or FY 2026 reflect the application of new utilization controls. Benefit restrictions include the elimination of a covered benefit, benefit caps, or the application of utilization controls for existing benefits. Five states (California, Colorado, Indiana, Minnesota, and Rhode Island) reported plans to implement utilization controls and/or benefit caps for one or more specific services. For example, Rhode Island implemented service limits for community health worker services without prior authorization, and Indiana plans to implement weekly and lifetime limitations for applied behavioral health analysis (ABA) services (subject to CMS approval).

Three states reported eliminating certain benefits altogether. Notably, North Carolina ceased “Healthy Opportunities Pilots” program services as of July 1, 2025, due to a lack of appropriations. The pilots covered certain non-medical services that target social needs, including housing, nutrition, transportation, and interpersonal relationship supports to specific and limited enrollees. Evaluations of the “Healthy Opportunity Pilots” 1115 waiver (approved by the first Trump administration) showed lower costs over time and largely positive outcomes. California removed COVID-19 vaccine coverage in its family planning program in FY 2025, and Minnesota plans to remove coverage of chiropractic services for adults in FY 2026.

Pharmacy

Context

Drug Expenditures. Management of rising pharmacy costs continues to be a focus area at both the state and federal levels. Between federal fiscal year (FFY) 2017 and FFY 2023, net Medicaid spending on prescription drugs (after rebates) grew by 72% and in FFY 2023, prescription drugs accounted for approximately 6% of total Medicaid spending. In this year’s survey, several states also reported rising pharmacy costs as an upward pressure on total Medicaid expenditures for FY 2025 and FY 2026, and some states noted challenges with projecting future pharmacy trends and costs in setting managed care organization (MCO) capitation rates. Much of the spending growth in recent years has been attributed to high cost specialty drugs, including obesity drugs and emerging cell and gene therapies that treat, and sometimes cure, rare diseases but at a high cost to Medicaid and other payers.

State Level Controls. The federal Medicaid Drug Rebate Program (MDRP) requires states to cover nearly all Food and Drug Administration (FDA) approved drugs from rebating manufacturers, limiting states’ ability to control drug costs through restrictive formularies. Instead, states use an array of payment strategies and utilization controls to manage pharmacy expenditures, including preferred drug lists (PDLs), prior authorization, managed care pharmacy carve-outs, and value-based arrangements (VBAs) negotiated with individual pharmaceutical manufacturers that increase supplemental rebates or refund payments to the state if the drug does not perform as expected.

States and MCOs often contract with external vendors like pharmacy benefit managers (PBMs) to manage or administer the pharmacy benefit. PBMs may perform a variety of administrative and clinical services for Medicaid programs (e.g., developing a provider network, negotiating rebates with drug manufacturers, adjudicating claims, monitoring utilization, overseeing PDLs, etc.) and are used in both fee-for-service (FFS) and managed care settings. PBMs, however, have faced increased scrutiny in recent years as more states adopt reforms to increase transparency and improve oversight.

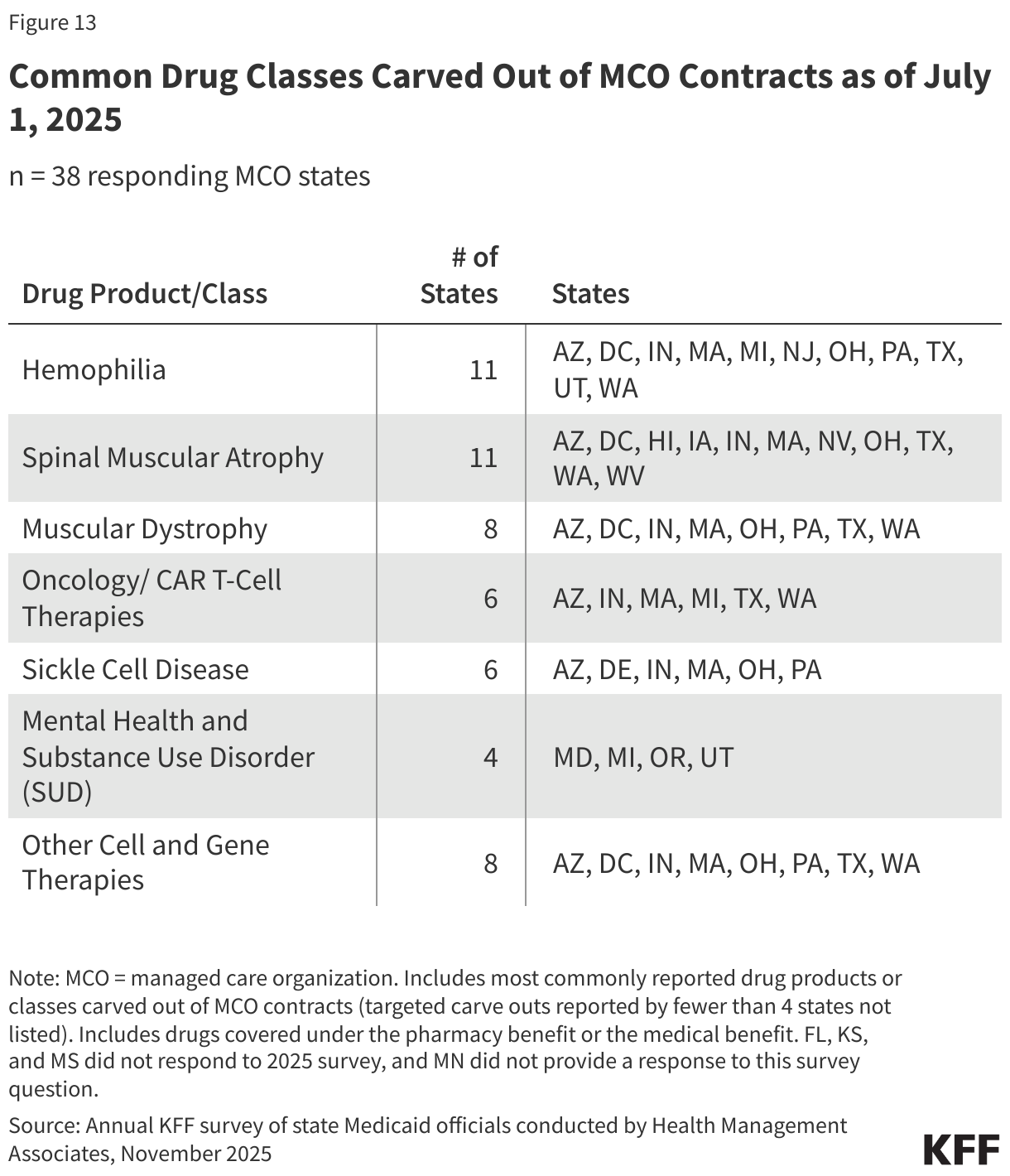

Most Medicaid prescription drugs are covered through the pharmacy benefit. Some, however, are covered through the medical benefit and, depending on how they are dispensed and administered, may be covered under both the pharmacy benefit and medical benefit. Physician-administered drugs are drugs dispensed by a provider in a clinical setting, such as cell and gene therapies, and are typically covered under the medical benefit. Physician-administered drugs can be eligible for rebates under the MDRP if they meet the definition of a “covered outpatient drug,” generally meaning a prescription drug that is FDA approved from a rebating manufacturer and identified separately on a claim for payment (not paid for as a bundled service). State coverage criteria and utilization controls for drugs covered under the medical benefit can be the same or differ from those under the pharmacy benefit, and states have identified a number of challenges managing utilization and spending of drugs under the medical benefit.

Recent Federal Initiatives. In addition to implementing the Cell and Gene Therapy (CGT) Access Model created under the Biden administration (see Box 3), the Trump administration has launched a new initiative to deliver most-favored nation (MFN) prescription drug pricing. The administration recently announced reaching agreements with some manufacturers, including Pfizer and AstraZeneca, to provide MFN pricing in Medicaid and announced a new drug payment model through which MFN prices will be available to participating state Medicaid programs, though it remains unclear how these changes will impact overall Medicaid drug spending or how many manufacturers or states will participate. Enrollees are not likely to be impacted, as they already pay little or no copays for prescription drugs. In addition, provisions to prohibit PBM spread pricing and increase price transparency in Medicaid were included in the House version of the 2025 federal budget reconciliation bill but ultimately were not included in the final law (H.R.1) enacted on July 4, 2025. These provisions, along with other Medicaid prescription drug proposals, could be included in future federal legislation. Lastly, a manufacturer (Bausch Health) recently pulled out of the MDRP, meaning their drugs will likely no longer be covered by state Medicaid programs (as states will no longer receive rebates), which raises concerns for enrollee access to prescription drugs, especially if more manufacturers follow suit.

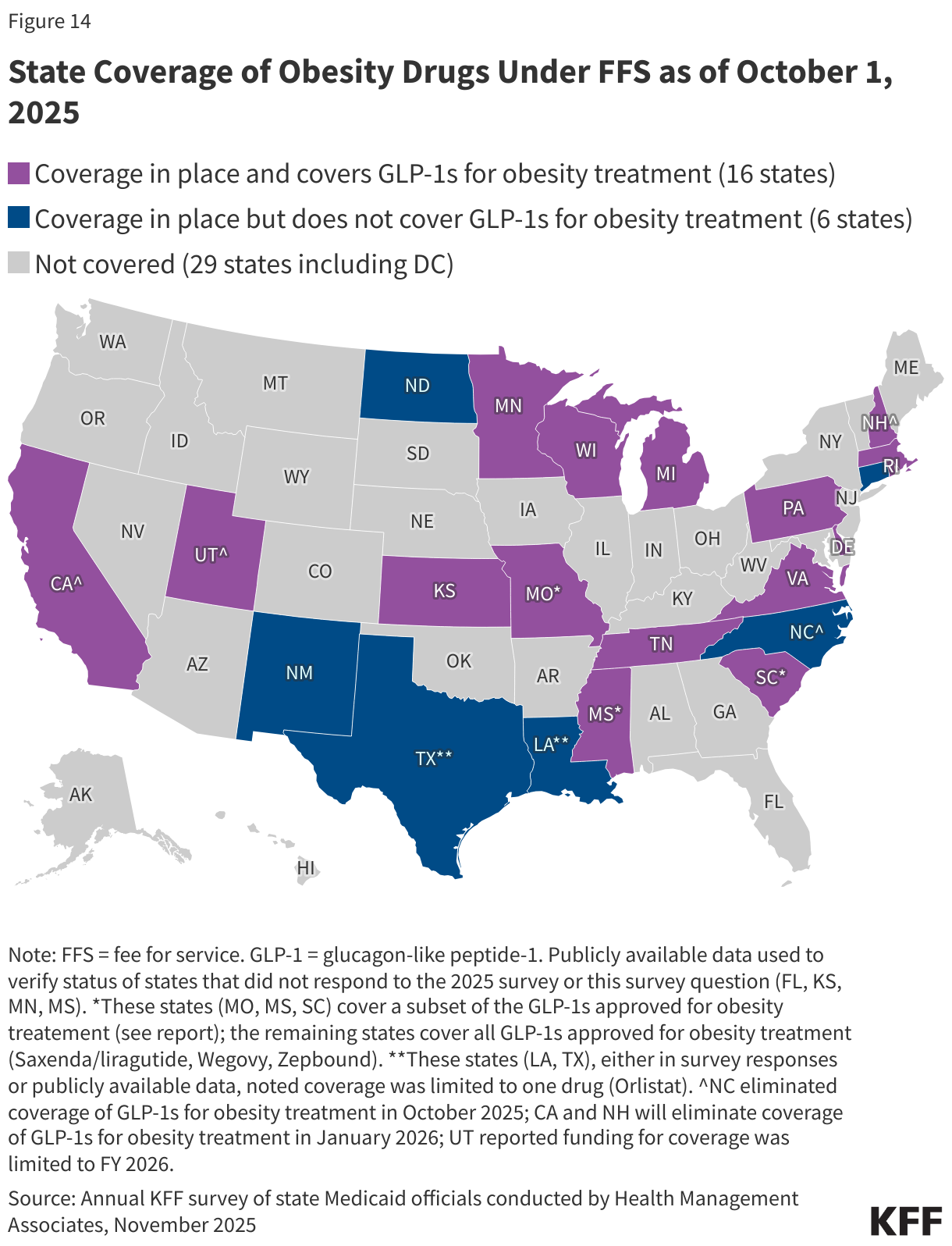

Obesity Drugs. GLP-1 (glucagon-like peptide-1) drugs have been used as a treatment for type 2 diabetes for over a decade, but newer, more expensive forms of these drugs have gained widespread attention for their effectiveness as a treatment for obesity. Due to their cost, however, coverage of GLP-1s for obesity treatment in Medicaid, ACA Marketplace plans, and most large employer firms remains relatively limited, and coverage in Medicare for treatment of obesity is prohibited. While state Medicaid programs must cover nearly all FDA-approved drugs for medically accepted indications, a long-standing statutory exception allows states to choose whether to cover weight-loss drugs under Medicaid for adults. As a result, coverage of GLP-1 drugs for the treatment of obesity remains optional for states, while coverage is required for the treatment of diabetes and, since March 2024 and December 2024, for the treatment of cardiovascular disease (Wegovy) and moderate to severe obstructive sleep apnea in adults with obesity (Zepbound), respectively. Coverage is also required if deemed medically necessary for children under Medicaid’s Early and Periodic Screening, Diagnostic and Treatment (EPSDT) benefit.

Almost four in ten adults and a quarter of children with Medicaid have obesity, and expanding Medicaid coverage of these drugs could address some disparities in access to these medications. However, expanded coverage could also increase Medicaid drug spending and put pressure on overall state budgets. A KFF analysis found that utilization and gross spending on GLP-1s nearly doubled each year from 2019 to 2023. In the longer term, however, reduced obesity rates among Medicaid enrollees could also result in reduced Medicaid spending on chronic diseases associated with obesity, such as heart disease, type 2 diabetes, and types of cancer.

The Trump administration has sent mixed signals about its support of coverage for obesity drugs. The administration did not move forward with a Biden administration proposal to allow Medicare and require Medicaid to cover drugs used to treat obesity by recognizing obesity as a chronic disease. However, the Trump administration recently announced reaching a deal with Eli Lilly and Novo Nordisk to lower the cost of their obesity drugs for Medicare, Medicaid, and those purchasing the drugs directly. While lower costs for state Medicaid programs could result in more states expanding coverage of obesity drugs, the implementation details as well as how the new costs compare to the net prices state Medicaid programs currently pay for obesity drugs remain unclear.

This section provides information about:

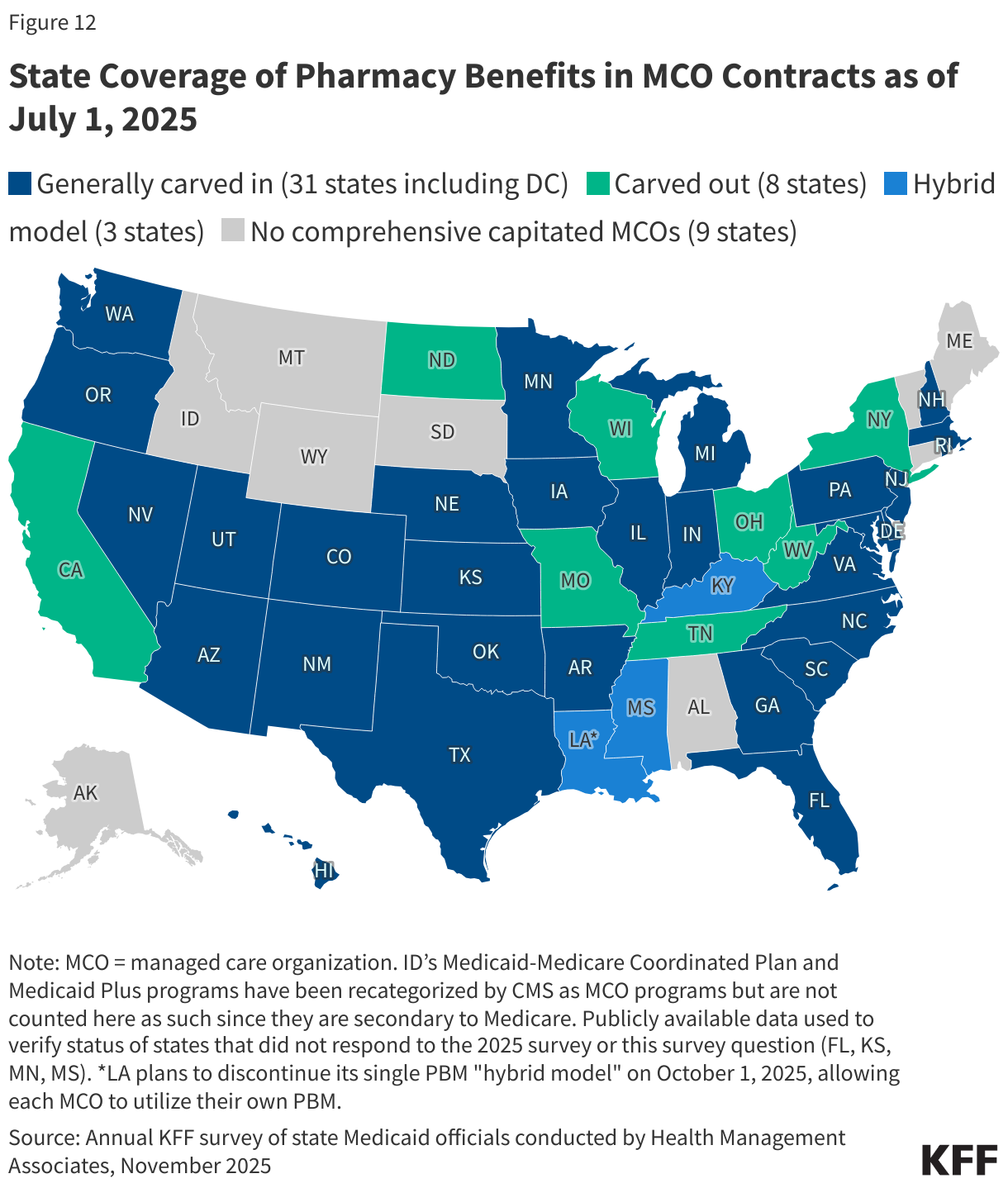

- Managed care’s role in administering pharmacy benefits

- Pharmacy cost containment

- Coverage of obesity drugs